North America diapers Market Size, Share, Trends & Growth Forecast Report By Product Type, Distribution Channel, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Diapers Market Summary

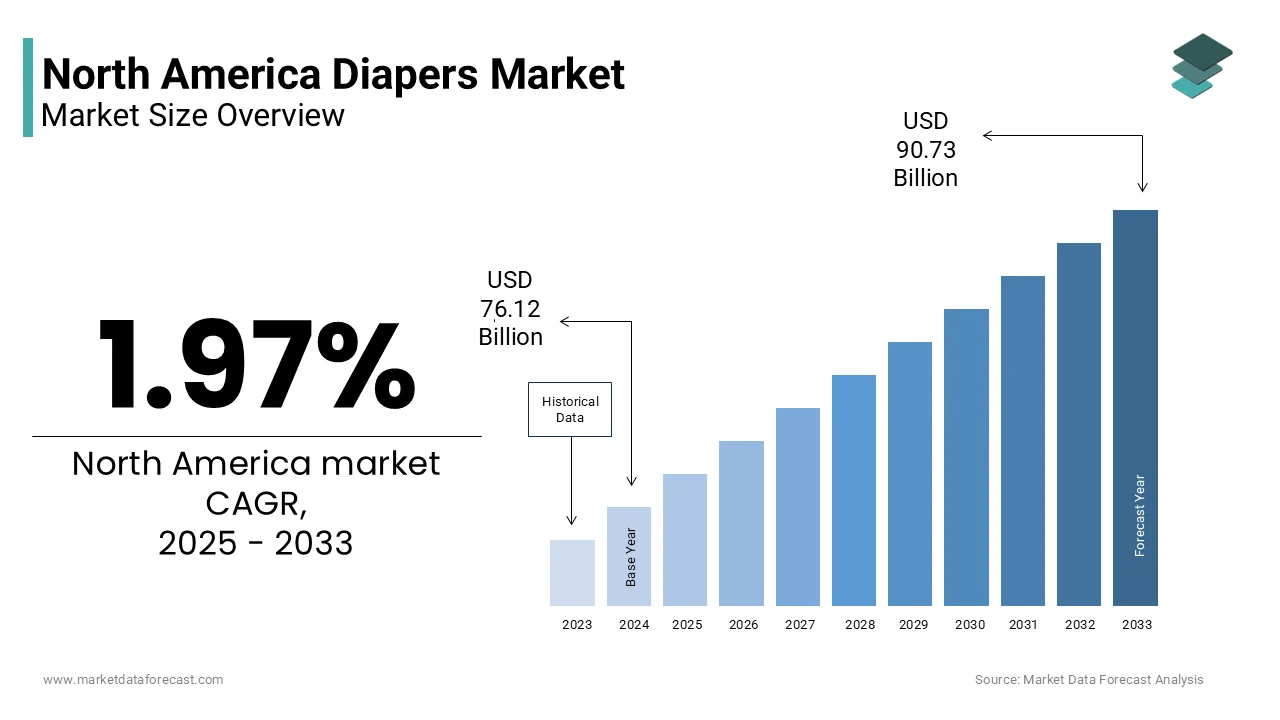

The North America diapers market was valued at USD 76.12 billion in 2024 and is projected to reach USD 90.73 billion by 2033 from USD 77.62 billion in 2025, growing at a CAGR of 1.97% from 2025 to 2033. Convenience, sustainability trends, technological innovations, and e-commerce adoption are driving market growth.

Key Market Trends & Insights

- United States held 88.2% market share in 2024, driven by high infant disposable diaper use, strong adult incontinence demand, and innovation leadership.

- Canada held 12.3% share in 2024, with strict product safety regulations, strong eco-diaper adoption, and rising adult incontinence demand.

- Disposable diapers dominated in 2024 due to unmatched convenience, availability, and improved comfort features.

- Biodegradable diapers are the fastest-growing product segment (CAGR 13.8%), fueled by eco-conscious consumer demand and compostable material adoption.

- Supermarkets & hypermarkets led distribution in 2024, benefiting from bulk pricing, wide availability, and cross-category sales strategies.

Market Size & Forecast

- 2024 Market Size: USD 76.12 Billion

- 2025 Market Size: USD 77.62 Billion

- 2033 Projected Market Size: USD 90.73 Billion

- CAGR (2025–2033): 1.97%

- United States: Largest market in 2024

- Canada: Strong growth region

North America Diapers Market Size

The diapers market size in North America was valued at USD 76.12 billion in 2024 and is predicted to be worth USD 90.73 billion by 2033 from USD 77.62 billion in 2025 and grow at a CAGR of 1.97% from 2025 to 2033.

MARKET DRIVERS

Rising Birth Rates in Specific Demographic Cohorts

The sustained fertility rates among certain population segments within Hispanic and immigrant communities, which exhibit higher birth rates than the national average is propelling the growth of the North America diapers market. According to the U.S. Centers for Disease Control and Prevention (CDC), the general fertility rate in the United States declined to 56.3 births per 1,000 women aged 15–44 in 2023, yet the Hispanic population maintained a fertility rate of 68.4, nearly 21% above the national figure. Additionally, immigrant families, who constitute 14% of all U.S. households with children under five, as per the Migration Policy Institute, tend to have larger family sizes and higher birth rates, contributing disproportionately to infant product demand. The U.S. Department of Agriculture’s Economic Research Service notes that 89% of Hispanic households with infants purchase premium disposable diapers, citing convenience and skin health as key factors. Retailers like Walmart and Target have responded by tailoring product assortments and bilingual marketing in high-growth neighborhoods.

Increasing Adoption of Premium and Specialty Diapers

The growing consumer preference for premium, hypoallergenic, and eco-conscious diaper variants with the heightened awareness of infant skin health and product safety is driving the growth of the North America diapers market. Parents are increasingly scrutinizing ingredient lists, avoiding fragrances, lotions, and chlorine bleaching, which are linked to dermatological irritation. According to the American Academy of Pediatrics, diaper dermatitis affects up to 35% of infants, prompting a shift toward dermatologist-tested and pediatrician-recommended brands. Brands such as Pampers Pure, Huggies Little Snugglers, and Seventh Generation Free & Clear have gained traction by emphasizing plant-based materials, breathable fabrics, and transparent sourcing. Additionally, the rise of subscription services like Amazon Subscribe & Save and Hello Bello has made premium options more accessible, with 62% of subscribers opting for higher-priced, specialty formulations, according to Brick Meets Click. Furthermore, specialty products such as overnight ultra-absorbent diapers and sensitive-skin lines are seeing accelerated adoption, with sales growing at twice the rate of standard variants.

MARKET RESTRAINTS

Environmental Concerns and Regulatory Pressure on Single-Use Plastics

The escalating environmental scrutiny surrounding single-use plastics and non-biodegradable waste generated by disposable diapers is restricting the growth of the North America diapers market. These products, composed of polyethylene, polypropylene, and superabsorbent polymers, can take up to 500 years to decompose, raising concerns among environmental agencies and consumers alike. The Canadian government has classified single-use plastics under Schedule 1 of the Canadian Environmental Protection Act, paving the way for future restrictions. In the U.S., states like California and New York are exploring extended producer responsibility (EPR) legislation that would require manufacturers to fund waste management and recycling programs. According to a 2023 survey by the Environmental Defense Fund, 67% of parents express concern about the environmental impact of disposable diapers.

Declining Birth Rates Among Non-Hispanic White and Urban Populations

The declining birth rates among non-Hispanic white and urban-dwelling populations is also hindering the growth of the North America diapers market. According to the U.S. National Center for Health Statistics, the total fertility rate in the United States fell to 1.62 children per woman in 2023, well below the replacement level of 2.1. Economic factors such as housing costs, childcare expenses, and workforce participation are key contributors; the Economic Policy Institute notes that the average annual cost of childcare in the U.S. exceeds $10,000 per child, discouraging larger families. This demographic shift directly reduces the pool of primary diaper users and limits organic market growth. While immigrant and minority populations partially offset this trend, their numbers are insufficient to fully compensate for the broader fertility decline.

MARKET OPPORTUNITIES

Expansion of Adult Incontinence Product Lines

The rapid growth of the adult incontinence segment with the aging and increasing social acceptance of incontinence care products is creating new opportunities for the growth of the North America diapers market. The U.S. Census Bureau projects that by 2030, over 21% of the American population will be aged 65 or older, up from 17% in 2023, creating a vast and expanding user base. According to the National Association for Continence, more than 25 million Americans suffer from urinary incontinence, yet only 28% seek treatment or use appropriate products, indicating significant unmet demand. Manufacturers are responding by developing discreet, high-absorbency, and lifestyle-adaptive solutions such as pull-on briefs, protective underwear, and odor-control technologies. The Veterans Health Administration distributes over 120 million incontinence units annually, highlighting institutional demand. In Canada, the situation is equally pressing; the Canadian Institute for Health Information reports that 68% of long-term care residents require daily incontinence management, with provincial health systems increasingly procuring branded products. Retailers like CVS and Walgreens have expanded adult diaper sections, while digital platforms such as Amazon now offer subscription services tailored to seniors.

Innovation in Biodegradable and Compostable Diaper Technologies

The advancement of biodegradable, compostable, and plant-based diaper formulations that address environmental concerns while meeting performance expectations is substantially to fuel the growth of the North America diapers market. Traditional disposable diapers are composed of up to 60% plastic, but new technologies are enabling the use of bamboo, cornstarch, and wood pulp-based absorbent cores that decompose within 50 years under industrial composting conditions, as verified by the Biodegradable Products Institute. Companies like Dyper, Naty, and Jackson Reece have introduced fully compostable diapers certified under ASTM D5338 and OK Compost standards, appealing to eco-conscious parents. According to a 2023 study by the Natural Marketing Institute, 52% of millennial parents are willing to switch brands for a truly sustainable diaper, even at a 30% price premium. San Francisco diverts over 80% of its waste from landfills, accepting compostable diapers in its green bin program, as reported by the city’s Department of the Environment.

MARKET CHALLENGES

Supply Chain Vulnerability in Raw Material Sourcing

The significant operational challenges due to its dependence on a fragile global supply chain for raw materials such as fluff pulp, superabsorbent polymers (SAP), and polypropylene is quiet challenge for the growth of the North America diapers market. Fluff pulp, primarily sourced from softwood forests in Canada and Scandinavia, is subject to climate-related disruptions and logging restrictions. According to Natural Resources Canada, the 2023 wildfire season burned over 18 million hectares of boreal forest by impacting pulpwood availability and delaying shipments to major diaper manufacturers. Superabsorbent polymers, essential for moisture retention, are largely produced in Asia, with 70% of North American supply originating from China and South Korea, as reported by the American Chemistry Council. The U.S. Energy Information Administration notes that ethylene and propylene production declined by 9% in 2021 due to Gulf Coast refinery outages, directly affecting nonwoven fabric output for diaper outer layers. These dependencies create production uncertainties, forcing manufacturers to maintain higher inventory levels and absorb cost shocks. Additionally, sustainability mandates are pressuring companies to shift to recycled or bio-based materials, which currently lack the scalability and consistency of conventional inputs.

Intensifying Competition from Reusable and Hybrid Diaper Systems

The growing competitive pressure from reusable cloth diapers and hybrid systems that combine disposable inserts with washable covers by appealing to environmentally conscious and cost-sensitive consumers is also to hamper the growth of the North America diapers market. According to a 2023 survey by the Sustainable Parenting Coalition, 18% of new parents in urban U.S. and Canadian centers now use cloth diapers full- or part-time, a figure that has doubled since 2018. While still a minority, this segment is concentrated among high-income, educated demographics who influence broader consumer trends. Brands like BumGenius, Thirsties, and Charlie Banana have modernized cloth diapering with snap-fit designs, breathable fabrics, and easy washing protocols, reducing historical barriers related to convenience and hygiene. The Real Diaper Industry Association estimates that a single child using cloth diapers can save up to 1.5 tons of waste from landfills. Hybrid systems like GroVia and Wonderoos offer a middle ground, allowing parents to use compostable inserts with reusable shells, combining sustainability with convenience. Retailers such as Buy Buy Baby and Babylist now feature dedicated eco-diaper sections, and online communities on Reddit and Instagram amplify peer recommendations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 1.97 % |

| Segments Covered | By Product Type, Distribution Channel, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | Procter & Gamble Co., Kimberly-Clark Corporation, Unicharm Corporation, Essity AB, Ontex Group, First Quality Enterprises, Inc., Hengan International Group Company Ltd., Domtar Corporation, Kao Corporation, and Drylock Technologies, and others |

SEGMENTAL ANALYSIS

By Product Type Insights

The disposable diapers segment held a dominant share of the North America diapers market in 2024 due to their unparalleled convenience, widespread availability, and integration into daily childcare routines across urban and suburban households. A 2023 study by the Pew Research Center found that 89% of dual-income families rely exclusively on disposable diapers due to limited time for laundering and hygiene management. Additionally, technological advancements such as wetness indicators, breathable outer layers, and leak-proof leg cuffs have significantly enhanced comfort and skin protection, reducing incidents of diaper rash. The National Institute of Child Health and Human Development confirms that premium disposable brands have reduced dermatitis occurrence by up to 32% compared to basic models.

The biodegradable diapers segment is likely to grow with a CAGR of 13.8% from 2025 to 2033 owing to the rising environmental awareness and shifting consumer values toward sustainable personal care products. Biodegradable diapers, made from bamboo, cornstarch, and chlorine-free pulp, decompose within 50 years under industrial composting conditions significantly faster than conventional disposables, which persist for centuries, as verified by ASTM D5338 testing standards. Companies like Dyper and Naty have capitalized on this trend, offering subscription-based compostable diaper services in 15 U.S. states and three Canadian provinces. Retailers such as Whole Foods Market and Thrive Market have seen a 37% year-over-year increase in biodegradable diaper sales, according to SPINS. Furthermore, partnerships with waste management firms enable closed-loop systems—Dyper’s “Diaper Take-Back” program has diverted over 22 million diapers from landfills since 2020.

By Distribution Channel Insights

The supermarkets and hypermarkets segment held a prominent share of the North America diapers market in 2024 owing to the channel’s ability to offer bulk purchasing, competitive pricing, and one-stop shopping convenience, which aligns with the high-frequency, high-volume nature of diaper consumption. Major chains like Walmart, Kroger, and Costco leverage their scale to offer private-label alternatives at 20–30% lower prices than national brands, attracting cost-conscious families. In Canada, Loblaw Companies and Sobeys control 74% of grocery sales, ensuring widespread product availability. The physical placement of diapers in high-traffic zones near baby formula and wipes also encourages cross-category spending. Furthermore, hypermarkets with pharmacy sections, such as SuperTarget and Walmart Supercenter, combine convenience with trusted retail environments, reinforcing consumer confidence.

The online stores segment is emerging with a CAGR of 14.2% from 2025 to 2033 with the increasing adoption of e-commerce for essential household goods among time-constrained parents and urban dwellers. According to the U.S. Census Bureau, online grocery and baby product sales reached $152 billion in 2023, with diapers ranking among the top five most frequently ordered non-perishable items. Additionally, online reviews and influencer recommendations play a role in decision-making Amazon’s baby category averages over 12,000 verified purchase reviews per top-selling diaper SKU, providing social proof that influences new buyers.

REGIONAL ANALYSIS

United States

The United States was the top performer in the North America diapers market with 88.2% of the share in 2024. According to the Centers for Disease Control and Prevention, 92% of infants are primarily diapered using disposable products. The U.S. also leads in adult incontinence demand, with over 25 million individuals affected, as per the National Association for Continence, driving expansion beyond infant care. Major manufacturers, including Procter & Gamble (Pampers) and Kimberly-Clark (Huggies), are headquartered in the U.S., enabling rapid R&D cycles and market responsiveness. Retail infrastructure is highly developed, with Walmart alone selling over 1.2 billion diaper units annually, according to internal corporate disclosures. The rise of e-commerce, sustainability initiatives, and premium product lines further solidifies the U.S. as the epicenter of diaper innovation and consumption in North America.

Canada

Canada diapers market held 12.3% of the share in 2024. Canadian parents use an average of 2,600 disposable diapers per child in the first two years, slightly above the U.S. average, according to Health Canada’s 2023 Child Product Usage Survey. The market is characterized by strong regulatory oversight; Health Canada enforces strict safety standards under the Canada Consumer Product Safety Act, requiring third-party testing for chemical content and absorbency. This regulatory rigor has fostered consumer trust in branded products and limited the proliferation of unverified imports. The adult incontinence segment is expanding rapidly due to demographic aging; the Canadian Institute for Health Information reports that 68% of long-term care residents require daily incontinence management, creating institutional demand. Environmentally, Canada is at the forefront of sustainable diaper adoption; municipalities like Toronto and Vancouver accept certified compostable diapers in organic waste programs, encouraging eco-friendly choices. Retail consolidation through Loblaw, Sobeys, and Shoppers Drug Mart ensures efficient distribution, while rising immigration supports stable birth rates among key demographic groups.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the North America diapers market are Procter & Gamble Co., Kimberly-Clark Corporation, Unicharm Corporation, Essity AB, Ontex Group, First Quality Enterprises, Inc., Hengan International Group Company Ltd., Domtar Corporation, Kao Corporation, and Drylock Technologies.

The competitive landscape of the North America diapers market is marked by a dynamic interplay between global giants, regional specialists, and agile niche entrants, each vying for relevance in a category that balances necessity, emotion, and innovation. Established multinational corporations dominate through brand recognition, extensive distribution, and decades of consumer trust, embedding their products into the fabric of daily childcare. However, their supremacy is increasingly challenged by mission-driven startups that prioritize sustainability, transparency, and ethical production, resonating with environmentally conscious and digitally native parents. These challengers often operate in the premium and eco-diaper segments, leveraging social media, influencer partnerships, and subscription models to bypass traditional retail gatekeepers. Private-label expansion by major retailers further intensifies competition, offering cost-effective alternatives that erode brand loyalty. Differentiation now extends beyond absorbency and fit to encompass environmental footprint, ingredient sourcing, and corporate responsibility.

TOP PLAYERS IN THE MARKET

Procter & Gamble (Pampers)

Procter & Gamble, through its Pampers brand, stands as a defining leader in the North America diapers market, renowned for its relentless focus on innovation, pediatric collaboration, and global quality standards. Pampers has redefined infant care by integrating medical research into product design, developing breathable materials, wetness indicators, and skin-health technologies that address real-time parental concerns. The brand’s deep engagement with healthcare professionals and parenting communities has solidified its reputation for safety and reliability. Beyond North America, Pampers influences global diaper standards, pioneering initiatives such as the "1 Pack = 1 Vaccine" program, which has provided millions of immunizations worldwide. Its R&D investments continue to shape industry benchmarks in absorbency, fit, and sustainability, with North American consumer insights often driving worldwide product iterations.

Kimberly-Clark (Huggies)

Kimberly-Clark, operator of the Huggies brand, plays a pivotal role in shaping the North American diaper landscape through its emphasis on comfort, inclusivity, and responsive innovation. Huggies has consistently tailored its product lines to meet diverse consumer needs, from premature infant sizes to adaptive designs for larger toddlers, reinforcing its image as a brand that grows with the child. The company’s commitment to skin health is evident in its dermatologist-tested formulations and partnerships with pediatric organizations to reduce diaper rash incidents. In the global arena, Huggies leverages North American market feedback to refine international offerings, particularly in premium and eco-conscious segments. Through purpose-driven marketing and community engagement, such as supporting neonatal intensive care units with free diaper donations, Huggies builds deep emotional resonance with caregivers. Its integration of empathy, performance, and social responsibility ensures enduring relevance in both regional and global markets.

Unicharm (Dr. Brown’s, MamyPoko)

Unicharm is a Japanese multinational with growing influence in North America through brands like Dr. Brown’s and MamyPoko, brings a distinct philosophy of precision engineering and minimalist design to the diaper market. While its North American presence is smaller than that of P&G or Kimberly-Clark, the company is gaining traction among discerning parents seeking high-performance alternatives to mainstream options. Unicharm’s success in Asia and Europe has informed its strategic entry into North America, where it emphasizes product differentiation through material science and ergonomic fit. The company invests heavily in R&D to optimize core absorbency systems and reduce environmental impact, setting benchmarks for next-generation diaper functionality.

TOP STRATEGIES USED BY KEY PLAYERS

A primary strategy employed by leading diaper manufacturers is product innovation centered on skin health and comfort. Companies are investing in advanced materials such as breathable nonwovens, hypoallergenic liners, and pH-balanced wetness barriers to minimize irritation and enhance wearability for sensitive infant skin. These improvements are often developed in collaboration with pediatric dermatologists and validated through clinical testing, which is reinforcing brand credibility.

Another key approach is sustainability-driven reengineering of product lifecycles. Major players are reformulating diapers with plant-based polymers, reducing plastic content, and designing for compostability or recyclability. They are also exploring closed-loop systems, such as take-back programs and partnerships with waste management firms to address environmental concerns and align with evolving regulatory expectations.

Also, a strategy is digital engagement and direct-to-consumer (DTC) expansion. Brands are leveraging e-commerce platforms, subscription models, and data-driven marketing to build personalized relationships with parents. Through mobile apps, parenting content, and AI-powered replenishment tools, companies enhance customer retention and gather real-time insights to inform product development and messaging.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Procter & Gamble launched a new line of Pampers Pure Protection diapers made with plant-based outer covers and chlorine-free pulp, which is targeting eco-conscious parents and expanding its sustainable product portfolio in the U.S. and Canada.

- In April 2023, Kimberly-Clark introduced Huggies Little Snugglers with BreatheFree Liners, a new moisture-wicking technology designed to reduce skin irritation, and rolled out a nationwide awareness campaign in partnership with pediatric dermatologists.

- In September 2023, Unicharm expanded its Dr. Brown’s diaper distribution to 10,000 additional retail outlets across the United States through a strategic partnership with a major grocery wholesaler, enhancing its market visibility.

- In February 2024, Pampers launched a digital parenting hub offering personalized diapering advice, growth tracking, and auto-replenishment features, which is strengthening its direct-to-consumer engagement model.

- In June 2024, Huggies initiated a pilot diaper recycling program in collaboration with a Canadian waste technology firm by aiming to convert used diapers into industrial-grade plastic materials and advance circular economy goals.

MARKET SEGMENTATION

This research report on the North America diapers market has been segmented and sub-segmented based on the following categories.

By Product Type

- Baby Diaper

- Disposable Diapers

- Training Diapers

- Cloth Diapers

- Swim Diapers

- Biodegradable Diapers

- Adult Diaper

- Pad Type

- Flat Type

- Pant Type

By Distribution Channel

- Supermarkets and Hypermarkets

- Pharmacies

- Convenience Stores

- Online Stores

- Others

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What types of diapers are popular in North America?

Disposable diapers, cloth diapers, training pants, and swim diapers are widely used.

2. What factors are driving the North America diapers market?

Rising birth rates, aging population, and demand for convenient hygiene solutions.

3. Which countries dominate the North America diapers market?

The United States leads, followed by Canada and Mexico.

4. Who are the key players in the North America diapers market?

Procter & Gamble Co., Kimberly-Clark Corporation, Unicharm Corporation, and Essity AB are major players.

5. What trends are shaping the diapers market in North America?

Eco-friendly diapers, biodegradable materials, and premium comfort features.

6. What are the main distribution channels for diapers in North America?

Supermarkets, pharmacies, online platforms, and wholesale stores.

7. How is e-commerce impacting diaper sales in North America?

Online sales are growing due to subscription models and doorstep delivery.

8. Are biodegradable diapers gaining popularity in North America?

Yes, as sustainability concerns influence purchasing decisions.

9. What challenges does the North America diapers market face?

Price competition, raw material costs, and environmental concerns.

10. How is technology influencing diaper manufacturing?

Advanced absorbent materials, leak-proof designs, and skin-friendly fabrics are being developed.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com