U.S. Electric Bus Market Size, Share, Trends & Growth Forecast Report By Fuel Category (BEV, FCEV, HEV), and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$474.80 MnMarket Estimate, 2026

$541.03 MnMarket Forecast, 2034

$1,537.93 MnCAGR, 2026–2034

13.95%U.S. Electric Bus Market Report Summary

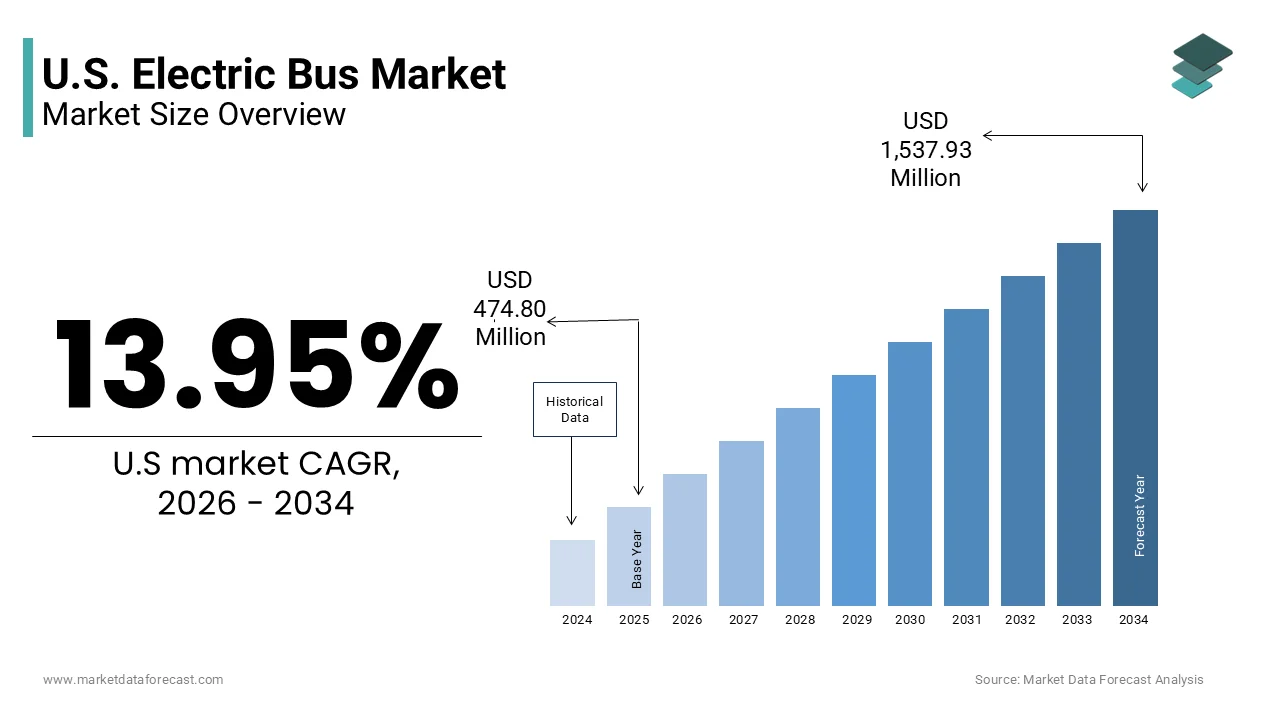

The U.S. electric bus market was valued at USD 474.80 million in 2025, is estimated to reach USD 541.03 million in 2026, and is projected to reach USD 1,537.93 million by 2034, growing at a CAGR of 13.95% during the forecast period. Market growth is driven by increasing investments in clean public transportation infrastructure, rising government initiatives to reduce carbon emissions, and growing adoption of zero emission mobility solutions. Electric buses are gaining traction across transit systems due to lower operating costs, environmental benefits, and advancements in battery technologies. Expanding charging infrastructure development and public transportation electrification programs are further supporting market growth across the United States.

Key Market Trends

- Increasing investments in sustainable public transportation systems are driving market growth.

- Growing government regulations focused on reducing transportation emissions are boosting market expansion.

- Rising adoption of battery electric buses is supporting industry development.

- Expansion of charging infrastructure networks is enhancing electric bus deployment capabilities.

- Innovation in battery technologies and fleet management systems is influencing market advancement.

Segmental Insights

- Based on fuel category, the battery segment accounted for the dominant share of the U.S. electric bus market in 2025. This dominance is attributed to advancements in battery performance, improving vehicle range, and increasing deployment of battery electric public transit fleets.

Regional Insights

- The United States electric bus market is experiencing strong growth due to increasing public transit modernization initiatives, expanding sustainability targets, and growing investments in clean transportation technologies. Federal and state level programs supporting fleet electrification continue to strengthen market development.

Competitive Landscape

The U.S. electric bus market is highly competitive, with manufacturers focusing on battery innovation, vehicle efficiency improvements, and fleet electrification solutions to strengthen their market position. Companies are investing in advanced propulsion technologies and transit modernization initiatives. Prominent players in the U.S. electric bus market include Proterra Inc., BYD Motors Inc., NFI Group Inc, AB Volvo, Green Power Motor Company Inc., Gillig LLC, Blue Bird Corporation, Isuzu Motors Ltd, Nova Bus Corporation, and MAN Truck & Bus AG.

U.S. Electric Bus Market Size

The U.S. electric bus market size was valued at USD 474.80 million in 2025, is estimated to reach USD 541.03 million in 2026, and is projected to reach USD 1,537.93 million by 2034, growing at a CAGR of 13.95%.

The electric bus is shift in public transportation infrastructure driven by stringent environmental mandates and technological advancements. Electric buses are defined as zero emission vehicles powered entirely by electricity stored in onboard batteries or supplied via overhead lines although battery electric variants dominate current procurement strategies. This transition is not merely a replacement of diesel engines but a comprehensive overhaul of urban mobility systems aimed at reducing carbon footprints and improving air quality in densely populated areas. As per the Environmental Protection Agency, the transportation sector accounted for approximately 29% of total greenhouse gas emissions in the United States in 2021 with heavy duty vehicles contributing significantly to this figure. The federal government has intensified its focus on decarbonization through initiatives such as the Bipartisan Infrastructure Law, which allocates substantial funding for clean school and transit buses. The adoption rate is further influenced by state level policies such as the California Advanced Clean Fleets rule, which mandates that all new bus purchases be zero emission by 2040. These regulatory frameworks combined with declining battery costs and improved charging infrastructure create a robust ecosystem for market expansion. The integration of smart grid technologies also enables more efficient energy management ensuring that the electrical load from bus fleets does not overwhelm local power networks.

MARKET DRIVERS

Stringent Federal and State Regulatory Mandates Drive Adoption

The implementation of rigorous federal and state level environmental regulations is primarily surging the growth of the United States electric bus market. The Inflation Reduction Act and the Bipartisan Infrastructure Law have collectively allocated billions of dollars in grants and rebates specifically targeting the replacement of internal combustion engine buses with zero emission alternatives. State level initiatives further amplify this momentum particularly in regions with aggressive climate action plans. For instance, the California Air Resources Board has enforced the Innovative Clean Transit regulation which requires all public transit agencies in the state to transition to 100% zero emission bus fleets by 2040. This mandate has compelled major metropolitan areas such as Los Angeles and San Francisco to accelerate their procurement timelines significantly. Additionally, the Environmental Protection Agency has tightened emissions standards for heavy duty vehicles effectively increasing the operational costs of maintaining diesel fleets. These regulatory frameworks create a compelling financial and legal imperative for transit authorities to adopt electric solutions. The alignment of federal funding with state mandates ensures a consistent demand pipeline thereby stabilizing market growth and encouraging manufacturers to scale up production capacities to meet the impending surge in orders from public sector entities nationwide.

Rising Operational Cost Efficiency and Total Cost of Ownership Benefits

Beyond regulatory compliance, the economic advantage of electric buses in terms of total cost of ownership is additionally propelling the growth of the United States electric bus market. While the initial purchase price of an electric bus remains higher than its diesel counterpart, the long-term operational savings are substantial due to lower fuel and maintenance expenses. According to the National Renewable Energy Laboratory, electric buses can reduce fuel costs by up to 60% compared to conventional diesel buses depending on local electricity rates and diesel prices. Maintenance costs are also significantly lower because electric drivetrains have fewer moving parts eliminating the need for oil changes transmission repairs and exhaust system maintenance. These savings accumulate over the typical 12 year lifespan of a transit vehicle making the total cost of ownership competitive or even superior to traditional options. Furthermore, volatility in global oil markets exposes diesel fleets to unpredictable fuel pricing whereas electricity prices tend to remain more stable allowing for better budget forecasting for municipal operators. The deployment of smart charging systems also enables transit agencies to charge buses during off peak hours when electricity rates are lower further enhancing cost efficiency. As battery technology continues to advance the energy density improves and costs decline the economic case for electrification becomes increasingly irrefutable.

MARKET RESTRAINTS

High Upfront Capital Investment and Funding Accessibility Constraints

Despite the long term economic benefits, the substantial initial capital required to purchase electric buses and install necessary charging infrastructure is limiting the growth of the United States electric bus market. The upfront cost of a standard 40-foot battery electric bus can range from 750000 USD to 1 million USD, which is nearly double the price of a comparable diesel bus. Many smaller transit agencies and rural school districts lack the financial reserves to cover these elevated acquisition costs without external assistance. While federal grants are available the application process is often complex and competitive leaving many applicants unfunded or partially funded. As per the Government Accountability Office, only a fraction of the total demand for zero emission buses is currently met by existing federal funding programs creating a backlog of unfulfilled procurement needs. These infrastructure costs are often borne by the transit agency further straining limited budgets. The uncertainty surrounding the long-term availability of federal subsidies also hesitates decision makers, who fear being left with stranded assets if funding dries up before the total cost of ownership parity is fully realized. Moreover, insurance premiums for electric buses can be higher due to the specialized nature of repairs and the high value of battery packs.

Inadequate Charging Infrastructure and Grid Capacity Limitations

The insufficient development of robust charging infrastructure and concerns regarding electrical grid capacity to the seamless integration of electric buses into existing transit operations is degrading the growth of the United States electric bus market. Most current transit depots were designed for diesel refueling and lack the electrical infrastructure necessary to support simultaneous high-power charging of multiple heavy duty vehicles. The upgrading a single depot to support a fleet of 50 electric buses can require millions of dollars in electrical upgrades, including new substations and transformers. Many local utilities are not equipped to handle the sudden spike in demand caused by simultaneous charging events particularly during peak evening hours when buses return to depots. The timeline for utility upgrades can span several years creating a hurdle that delays fleet electrification plans. Furthermore, the lack of standardized charging connectors and communication protocols between different bus manufacturers and charging equipment providers complicates the deployment process. This fragmentation forces transit agencies to commit to specific vendor ecosystems reducing flexibility and increasing dependency. The scarcity of public fast charging stations along intercity routes also limits the operational range and versatility of electric buses for regional transit services.

MARKET OPPORTUNITIES

Advancements in Battery Technology and Energy Density Improvements

The continuous innovations in battery chemistry and energy density by addressing range anxiety and operational limitations is setting up the growth of the United States electric bus market. Recent developments in lithium iron phosphate and solid state battery technologies are enabling buses to travel longer distances on a single charge while reducing weight and improving safety. According to the Department of Energy, recent breakthroughs in battery manufacturing have led to a 20% increase in energy density over the past five years allowing newer electric bus models to achieve ranges exceeding 250 miles on a single charge. This extended range makes electric buses viable for a broader array of routes including those with demanding topography or extended service hours that previously required diesel alternatives. The emergence of second life applications for used bus batteries also creates additional revenue streams and sustainability benefits. These retired batteries can be repurposed for stationary energy storage systems helping to stabilize the grid and offset some of the initial investment costs. Manufacturers are also integrating modular battery designs that allow for easier upgrades and replacements extending the usable life of the vehicle chassis. These technological advancements not only enhance the performance and reliability of electric buses but also improve their resale value and total lifecycle economics.

Expansion of Smart Grid Integration and Vehicle to Grid Capabilities

The integration of electric buses with smart grid technologies and the development of vehicle to grid capabilities for both transit agencies and utility providers is another factor to elevate the growth of the United States electric bus market. Vehicle to grid technology allows electric buses to discharge stored energy back into the grid during periods of high demand thereby acting as mobile energy storage units. As per a study, such grid services can generate significant additional income for fleet operators offsetting operational costs and improving the financial viability of electric bus deployments. Smart charging systems also optimize energy usage by adjusting charging rates based on real time electricity prices and grid conditions ensuring that buses are charged when renewable energy sources such as solar and wind are most abundant. This synergy between transportation and energy sectors enhances the overall efficiency of the electrical grid and supports the integration of intermittent renewable energy sources. The deployment of bidirectional chargers is becoming increasingly common in new transit depots facilitating this two way flow of energy. This dual utility model not only strengthens the business case for electrification but also contributes to greater grid resilience and sustainability positioning the United States at the forefront of integrated smart mobility and energy infrastructure development.

MARKET CHALLENGES

Workforce Shortage and Technical Skill Gaps in Maintenance

The acute shortage of skilled technicians trained to maintain and repair high voltage electric vehicle systems is to pose a major challenge for the growth of the United States electric bus market. Traditional diesel mechanics possess expertise in internal combustion engines but lack the specialized knowledge required for handling high voltage batteries electric motors and complex software systems. According to the American Public Transportation Association, nearly 60% of transit agencies reported difficulties in hiring qualified staff to manage their growing electric fleets in 2023. This skills gap necessitates extensive retraining programs and partnerships with technical colleges which require time and financial investment. The complexity of electric bus systems also means that minor issues can lead to prolonged downtime if not diagnosed correctly by certified personnel. Furthermore, safety protocols for working with high voltage systems are stringent requiring specialized certification and equipment to prevent accidents. The lack of standardized training curricula across different manufacturers further complicates the recruitment and training process forcing agencies to rely on proprietary training programs from specific vendors. This dependency limits labor mobility and increases operational risks.

Supply Chain Vulnerabilities for Critical Raw Materials

The reliance on a concentrated and often geopolitically sensitive supply chain for raw materials, such as lithium, cobalt, and nickel, is a major challenge for the growth of the United States electric bus market. The majority of these essential battery components are sourced from a limited number of countries creating vulnerabilities to trade disruptions and price volatility. According to the United States Geological Survey, China processes approximately 60% of the world's lithium and 80% of its cobalt giving it substantial influence over global battery supply chains. Any disruption in these supply lines due to geopolitical tensions or export restrictions can lead to significant delays in bus production and increased costs for manufacturers. The mining and processing of these materials also raise environmental and ethical concerns which can impact consumer perception and regulatory compliance. Efforts to domesticize the supply chain through initiatives like the Inflation Reduction Act are underway but building new mining and processing facilities in the United States takes years to reach full operational capacity. In the interim transit, agencies and manufacturers remain exposed to global market fluctuations and supply bottlenecks. This uncertainty complicates long term planning and procurement strategies making it difficult to guarantee consistent delivery schedules and pricing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.95% |

| Segments Covered | By Fuel Category, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Proterra Inc., BYD Motors Inc., NFI Group Inc., AB Volvo, Green Power Motor Company Inc., Gillig LLC, Blue Bird Corporation, Isuzu Motors Ltd, Nova Bus Corporation, and MAN Truck & Bus AG |

SEGMENTAL ANALYSIS

By Fuel Category Insights

The battery segment was accounted in holding a dominant share of the United States electric bus market in 2025 with the maturity of lithium ion battery technology and the extensive support from federal infrastructure legislation. The substantial reduction in battery costs, which has made battery electric buses economically viable for large scale procurement. According to BloombergNEF, the average price of lithium ion battery packs fell to 139 USD per kilowatt hour in 2023 representing a significant decline from previous years and making the total cost of ownership competitive with diesel alternatives. This cost reduction enables transit agencies to allocate budgets more efficiently while meeting environmental mandates. The second factor is the robust charging infrastructure development supported by the Bipartisan Infrastructure Law which allocated 5 billion USD specifically for electric vehicle charging networks. The availability of diverse bus models from manufacturers, such as New Flyer and Proterra further supports adoption by offering customizable solutions for various route lengths. Additionally, the simplicity of battery electric drivetrains compared to fuel cell or hybrid systems reduces maintenance complexity and training requirements for technical staff.

The fuel cell segment is expected to grow at an anticipated CAGR of 28.3% from 2026 to 2034 with the specific operational advantages that address the limitations of battery electric vehicles in demanding transit environments. According to the National Renewable Energy Laboratory, fuel cell buses can be refueled in under 15 minutes and achieve ranges exceeding 350 miles, which closely mirrors the operational flexibility of conventional diesel buses. The increasing investment in hydrogen production and distribution infrastructure, particularly in states with aggressive clean energy mandates is also propelling the growth of the segment. These incentives combined with the ability to operate in extreme weather conditions without significant range degradation make fuel cell electric buses an attractive option for regions seeking diverse zero emission solutions.

COMPETITIVE LANDSCAPE

The competition in the United States electric bus market is characterized by intense rivalry among established manufacturers and emerging technology providers striving to capture market share. Established players leverage their extensive distribution networks and proven track records to secure large-scale contracts from public transit agencies. Meanwhile, new entrants focus on innovative technologies such as advanced battery chemistries and autonomous driving features to differentiate their offerings. Price competition remains significant as federal subsidies help lower the upfront costs for buyers enabling more manufacturers to compete effectively. Regulatory compliance plays a crucial role in shaping competitive dynamics with companies adapting their products to meet stringent emissions standards. Intellectual property disputes over battery technologies and charging protocols also influence the competitive landscape. Customer service and after sales support have become key differentiators as transit agencies prioritize reliability and minimal downtime.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. electric bus market are

- Proterra Inc.

- BYD Motors Inc.

- NFI Group Inc

- AB Volvo

- Green Power Motor Company Inc.

- Gillig LLC

- Blue Bird Corporation

- Isuzu Motors Ltd

- Nova Bus Corporation

- MAN Truck & Bus AG

Top Players in the Market

- New Flyer Industries maintains a prominent position in the United States electric bus sector through its extensive manufacturing capabilities and diverse product portfolio. The company offers a wide range of battery electric and fuel cell electric buses that cater to various transit needs across North America. Recent actions include the expansion of its production facilities in Alabama and Minnesota to increase output capacity for zero emission vehicles. New Flyer has also invested heavily in research and development to enhance battery efficiency and vehicle durability. Their strategic partnerships with charging infrastructure providers ensure seamless integration of their buses into existing transit systems. The company continues to secure significant contracts from major metropolitan transit authorities demonstrating its ability to meet large scale procurement demands effectively.

- Proterra Inc is a key innovator in the electric bus market known for its advanced battery technology and lightweight vehicle designs. The company specializes in high energy density battery systems that provide extended range and faster charging times for transit operators. Proterra has recently focused on expanding its charging infrastructure solutions including depot chargers and overhead pantograph systems to support fleet operations. Their commitment to sustainability is evident in their efforts to recycle battery materials and reduce the environmental impact of production processes. Proterra collaborates with utility companies to optimize grid integration and manage energy consumption efficiently. These initiatives help transit agencies lower operational costs while achieving their zero emission goals. The company continues to innovate in software solutions for fleet management enhancing the overall user experience for operators and passengers alike.

- BYD Auto has established a strong presence in the United States electric bus market by leveraging its global expertise in battery electric vehicle manufacturing. The company operates a dedicated bus manufacturing facility in Lancaster California which serves as a hub for producing customized electric buses for North American clients. BYD focuses on delivering robust and reliable vehicles with proven performance in diverse weather conditions. Recent actions include securing multiple contracts with school districts and municipal transit agencies for the deployment of zero emission fleets. The company emphasizes vertical integration by producing its own batteries and electronic components ensuring quality control and supply chain stability. BYD also invests in local workforce development and community engagement to build strong relationships with stakeholders. Their strategic approach combines competitive pricing with high quality standards making them a preferred choice for many public sector buyers.

Top Strategies Used by Key Market Participants

Key players in the United States electric bus market primarily employ strategies focused on vertical integration and strategic partnerships to strengthen their competitive positions. Manufacturers are increasingly investing in domestic production facilities to comply with Buy America provisions and reduce supply chain vulnerabilities. This localization effort ensures faster delivery times and enhances eligibility for federal funding opportunities. Companies are also forming alliances with charging infrastructure providers and utility companies to create comprehensive ecosystem solutions for transit agencies. These collaborations facilitate seamless integration of electric buses into existing operations by addressing grid capacity and charging logistics. Another major strategy involves heavy investment in research and development to improve battery energy density and reduce charging times. Innovations in solid state batteries and fuel cell technologies are prioritized to extend vehicle range and durability. Additionally, firms are expanding their service networks and offering extensive training programs to address the skilled labor shortage.

MARKET SEGMENTATION

This research report on the U.S. electric bus market is segmented and sub-segmented into the following categories.

By Fuel Category

- BEV

- FCEV

- HEV

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is the U.S. Electric Bus Market?

The U.S. Electric Bus Market refers to the industry focused on the production, deployment, and adoption of electric powered buses used for public transportation, school transportation, and commercial transit services.

2.What factors are driving the growth of the U.S. Electric Bus Market?

Market growth is driven by government incentives, emission reduction goals, increasing fuel costs, and rising investments in sustainable transportation infrastructure.

3.Why are electric buses becoming popular in the United States?

Electric buses are gaining popularity because they reduce carbon emissions, lower operating costs, and support clean energy transportation initiatives.

4.What types of electric buses are commonly available in the market?

Battery electric buses, hybrid electric buses, and fuel cell electric buses are among the commonly available electric bus categories.

5.How do electric buses benefit public transportation systems?

Electric buses help improve air quality, reduce noise pollution, and lower long term maintenance and fuel expenses.

6.What role do government policies play in the U.S. Electric Bus Market?

Government funding programs, environmental regulations, and clean transportation policies significantly support market expansion.

7.What battery technologies are used in electric buses?

Lithium ion batteries are the most widely used technology due to their high energy density, long lifespan, and charging efficiency.

8.What challenges affect the U.S. Electric Bus Market?

High upfront vehicle costs, charging infrastructure requirements, battery replacement expenses, and grid capacity concerns remain major challenges.

9.How does charging infrastructure impact electric bus adoption?

Reliable charging infrastructure supports efficient fleet operations and encourages transit agencies to expand electric bus deployment.

10.What is the future outlook for the U.S. Electric Bus Market?

The market is expected to grow steadily due to technological advancements, expanding charging infrastructure, and stronger government support for zero emission transportation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com