U.S. Functional Drinks Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S Functional Drinks Market Size

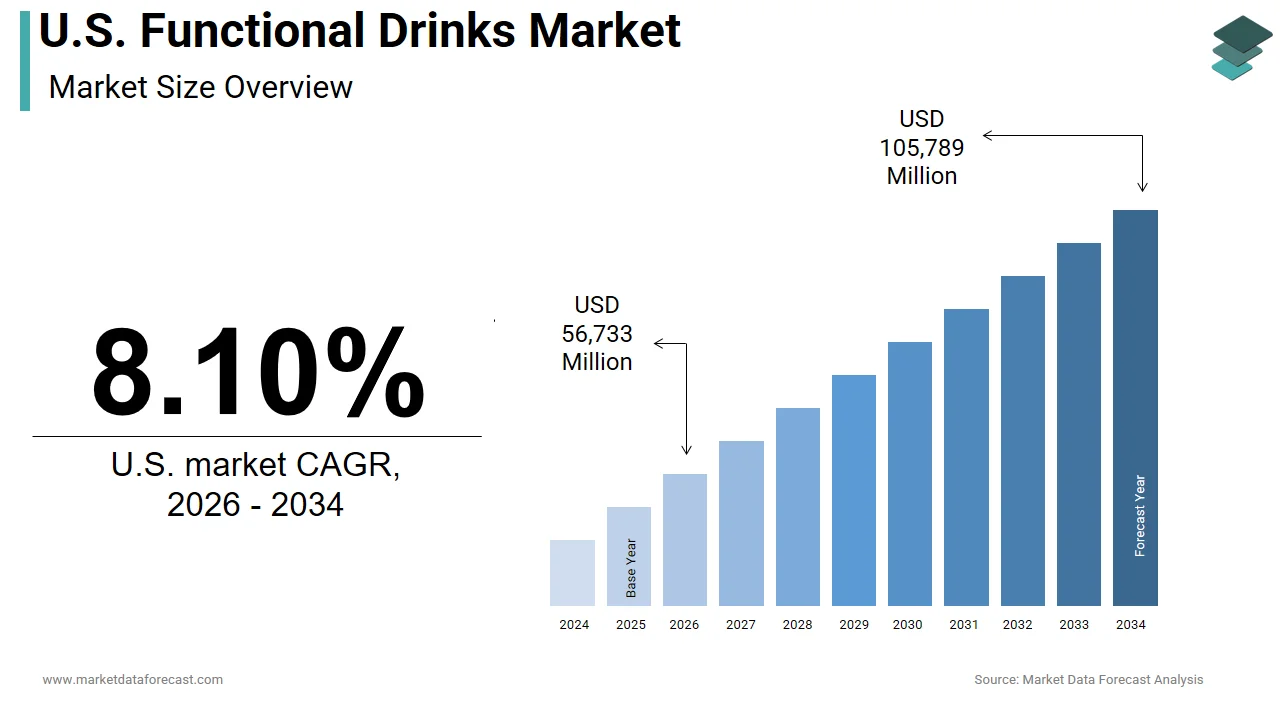

The U.S. functional drinks market was valued at USD 52,482 million in 2025, is estimated to reach USD 56,733 million in 2026, and is projected to reach USD 105,789 million by 2034, growing at a CAGR of 8.10% from 2026 to 2034.

Functional drinks are non-alcoholic beverages enhanced with ingredients like vitamins, minerals, herbs, or amino acids, designed to provide specific health benefits, such as improved energy, focus, or gut health, beyond basic hydration. These products include energy drinks, sports drinks, enhanced waters, and ready-to-drink teas that are fortified with vitamins, minerals, antioxidants, probiotics, or adaptogens. The sector has evolved from niche athletic performance aids to mainstream lifestyle products addressing specific consumer needs such as mental clarity, immune support, and digestive health. According to the International Food Information Council, approximately 60 percent of American consumers actively seek out foods and beverages with specific health benefits, indicating a profound shift in dietary priorities. This demand is driven by a growing awareness of preventive healthcare and the desire for convenient wellness solutions. The Centers for Disease Control and Prevention states that chronic diseases such as heart disease and diabetes affect 6 in 10 adults in the United States, prompting individuals to adopt healthier consumption habits. Functional drinks offer an accessible avenue for integrating beneficial ingredients into daily routines without significant lifestyle changes. The regulatory landscape overseen by the Food and Drug Administration ensures safety and labeling accuracy, which builds consumer trust. As urbanization increases, with over 80 percent of the population residing in urban areas as per the United States Census Bureau, the need for on-the-go health solutions intensifies. This convergence of health consciousness, convenience, and scientific innovation defines the current state of the functional drinks landscape in the United States.

MARKET DRIVERS

Rising Health Consciousness and Preventive Healthcare Adoption

The escalating focus on preventive healthcare and holistic wellness is a major factor behind the expansion of the United States functional drinks market. Consumers are increasingly proactive about managing their health through diet and lifestyle choices rather than relying solely on medical interventions after illness occurs. According to the Global Wellness Institute, the wellness economy in the United States is valued at over 2.1 trillion dollars, reflecting the substantial financial commitment individuals make toward maintaining their health. This trend is particularly evident among millennials and Generation Z who prioritize transparency in ingredient sourcing and functional benefits. Data from the Hartman Group indicates that 75 percent of consumers believe that food and beverage choices significantly impact their overall well being. Consequently there is a surge in demand for beverages that offer tangible health advantages such as immune boosting properties stress reduction and improved sleep quality. The prevalence of chronic conditions has further amplified this driver with the Centers for Disease Control and Prevention reporting that 40 percent of American adults are obese. This statistic underscores the urgent need for healthier alternatives to sugary sodas and traditional soft drinks. Functional drinks positioned as low sugar or no sugar options with added nutrients align perfectly with these health goals. Additionally the rise of digital health platforms and wearable technology has empowered consumers to track their nutritional intake more accurately fostering a data driven approach to wellness. This informed consumer base seeks products that complement their health metrics driving sustained growth in the functional beverage sector.

Increasing Demand for Convenience and On the Go Wellness Solutions

The fast-paced nature of modern American life has created a robust demand for convenient wellness solutions that can be easily integrated into busy schedules, and thereby accelerates the growth of the United States functional drinks market. Functional drinks offer a portable and immediate way to consume essential nutrients and energy boosts without the time commitment required for meal preparation or supplement regimens. According to the Bureau of Labor Statistics, the average employed American spends approximately 8.2 hours per day working on days worked, which limits the time available for healthy eating practices. This temporal constraint drives consumers toward ready to drink formats that provide instant gratification and functional benefits. The proliferation of single serve packaging and vending machine availability in offices gyms and transit hubs further enhances accessibility. Data from the National Association of Convenience Stores shows that ready to drink beverages account for a significant portion of impulse purchases in convenience channels highlighting the role of accessibility in driving sales. Urbanization plays a critical role as well, with the United States Census Bureau noting that 80 percent of the population lives in urban areas where quick service and portability are highly valued. The integration of functional drinks into daily routines such as morning commutes or workout sessions makes them an indispensable part of the modern lifestyle. Furthermore the development of shelf stable formulations allows for longer storage periods and wider distribution networks ensuring that these products are available whenever and wherever consumers need them. This convenience factor combined with perceived health benefits creates a powerful value proposition that sustains market growth.

MARKET RESTRAINTS

Regulatory Scrutiny and Labeling Compliance Challenges

Stringent regulatory oversight and complex labeling requirements are impeding the growth of the United States functional drinks market. This increases compliance costs and limits marketing claims. The Food and Drug Administration maintains rigorous standards for health and structure function claims requiring substantial scientific evidence to support any assertions made on product packaging. According to the Federal Trade Commission companies must ensure that their advertising is not deceptive or unsubstantiated which necessitates extensive legal and scientific review processes. This regulatory burden can delay product launches and increase operational expenses particularly for smaller brands with limited resources. The distinction between dietary supplements and conventional foods also creates confusion regarding classification and labeling obligations. Data from FDA enforcement audits indicates that mislabeling issues account for a notable percentage of regulatory warning letters and compliance failures issued to supplement manufacturers annually. Additionally the varying state level regulations regarding ingredients such as cannabidiol or specific herbal extracts add another layer of complexity for national distributors. Companies must navigate a fragmented legal landscape which can hinder uniform marketing strategies and distribution efficiency. The risk of litigation related to false advertising or adverse health effects further discourages aggressive promotional tactics. As per the American Beverage Association compliance with evolving FDA guidelines requires continuous monitoring and adaptation of formulation and packaging. These regulatory hurdles can stifle innovation and slow down the introduction of novel functional ingredients thereby restraining market expansion and limiting consumer access to new products.

Consumer Skepticism Regarding Efficacy and Ingredient Safety

Growing consumer skepticism concerning the actual efficacy and safety of functional ingredients further constraints the expansion of the United States functional drinks market. Despite the popularity of these beverages many consumers remain uncertain about whether the claimed health benefits are scientifically proven or merely marketing hype. According to a survey by the International Food Information Council, nearly 47 percent of consumers express doubt about the health claims made by food and beverage manufacturers. This lack of trust is exacerbated by the presence of numerous brands with varying levels of transparency and scientific backing. High profile recalls and negative media coverage regarding unsafe additives or excessive caffeine content have further eroded consumer confidence. Data from Consumer Reports highlights that incidents of adverse reactions to energy drinks and other functional beverages have led to increased scrutiny from health advocates and regulatory bodies. The complexity of ingredient lists and the use of proprietary blends often obscure the exact dosage and source of active compounds making it difficult for consumers to assess value and safety. Additionally the placebo effect associated with some functional claims leads to disappointment when expected results are not achieved. As per the Journal of the Academy of Nutrition and Dietetics inconsistent study results regarding certain adaptogens and nootropics contribute to this uncertainty. This skepticism forces companies to invest heavily in third party certifications and clinical trials to build credibility which increases costs. Until trust is fully established through transparent communication and verified results this skepticism will continue to limit market penetration and customer loyalty.

MARKET OPPORTUNITIES

Expansion into Personalized Nutrition and Customized Formulations

The emerging trend toward personalized nutrition unlocks significant potential for the United States functional drinks market. This shift allows brands to differentiate products and enhance customer engagement. Advances in biotechnology and data analytics enable companies to create beverages tailored to individual genetic profiles metabolic needs and lifestyle factors. According to the Nutrition Business Journal the personalized nutrition market is projected to grow significantly as consumers seek solutions that address their unique health challenges. Brands can leverage mobile applications and online quizzes to collect user data and recommend specific functional drinks that align with personal health goals such as weight management muscle recovery or stress relief. This customization fosters a deeper connection between the brand and the consumer leading to higher retention rates and premium pricing potential. A study suggests that personalization most often drives a 5 to 15 percent revenue lift compared to standard offerings, with digitally native outperformers capturing even higher returns due to increased customer intimacy. Furthermore, partnerships with healthcare providers and fitness trackers can integrate functional drinks into comprehensive wellness plans. The ability to adjust ingredient dosages based on real time health metrics offers a competitive edge in a crowded market. As per the Academy of Nutrition and Dietetics personalized dietary recommendations are more effective in achieving health outcomes than generic advice. By embracing this trend companies can move beyond one size fits all solutions and position themselves as partners in individual health journeys. This strategic shift not only drives sales but also establishes brand authority in the science backed wellness space.

Innovation in Plant Based and Clean Label Ingredients

The increasing demand for plant based and clean label ingredients is a key area for innovation within the United States functional drinks market. Consumers are increasingly scrutinizing ingredient lists and preferring natural sustainably sourced components over synthetic additives. According to historical data from the Plant Based Foods Association, retail sales of plant-based products spiked by 27 percent during the 2020 market surge, though the sector has since experienced recent market stabilization and slight unit volume contraction. Functional drinks formulated with organic herbs adaptogens and natural sweeteners appeal to health conscious individuals who prioritize purity and environmental sustainability. The use of upcycled ingredients such as fruit peels or spent grain from brewing processes also aligns with circular economy principles and reduces waste. Research shows that products with clean label claims grow faster than those without demonstrating the commercial viability of this approach. Brands can differentiate themselves by highlighting transparent sourcing practices and non GMO certifications which build trust and loyalty. Additionally the incorporation of exotic superfoods such as moringa ashwagandha and turmeric provides unique flavor profiles and functional benefits that attract adventurous consumers. As per consumer market research, a majority of shoppers are willing to pay a premium for products that support ethical farming practices and sustainable agriculture. By focusing on plant based innovation companies can tap into the growing vegan and flexitarian demographics while addressing environmental concerns. This strategy not only expands the customer base but also future proofs brands against shifting regulatory and consumer preferences regarding synthetic ingredients.

MARKET CHALLENGES

Intense Market Saturation and Brand Differentiation Difficulties

Intense saturation with thousands of brands competing for shelf space and consumer attention is greatly challenging the growth of the United States functional drinks market. This overcrowded landscape makes it difficult for new entrants and even established players to distinguish their products and maintain market share. According to the Specialty Food Association, a high volume of new beverage launches has led to cluttered retail environments and diluted brand visibility, challenging traditional marketing structures. Consumers often experience decision fatigue when confronted with excessive choices which can result in loyalty to familiar brands rather than experimentation with new options. A study indicates that private label functional drinks are gaining traction due to lower prices further squeezing margins for branded products. The high cost of marketing and promotion required to stand out in such a competitive environment strains financial resources particularly for small and medium sized enterprises. Additionally the rapid imitation of successful trends by larger corporations reduces the window of opportunity for innovators to capitalize on novel concepts. As per the Harvard Business Review brand differentiation in saturated markets requires significant investment in storytelling and community building which is not always feasible for all players. The constant pressure to innovate while maintaining profitability creates a precarious balance that many companies struggle to manage. This saturation also leads to price wars which can devalue the category and undermine the premium positioning of functional beverages. Navigating this competitive density requires strategic agility and distinct value propositions that resonate deeply with targeted consumer segments.

Supply Chain Volatility and Ingredient Sourcing Instability

Supply chain volatility and the instability of sourcing key functional ingredients negatively impact the United States functional drinks market. Many functional beverages rely on specialized ingredients such as rare botanicals probiotics and specific vitamins that are subject to fluctuating availability and pricing. According to the United States Department of Agriculture weather events geopolitical tensions and logistical disruptions can significantly impact the production and transport of agricultural commodities. For instance droughts in regions producing stevia or turmeric can lead to shortages and price spikes that affect manufacturing costs. Data from the Institute for Supply Management shows that supply chain volatility has prompted organizations to qualify backup suppliers at premiums of 15 percent to 20 percent to protect material pipelines. This unpredictability complicates inventory management and production planning forcing companies to hold higher safety stocks which ties up capital. Additionally the reliance on international suppliers for certain exotic ingredients exposes brands to currency fluctuations and trade policy changes. As per FMI (The Food Industry Association), supply chain resilience has become a top priority, yet achieving it requires substantial investment in diversified sourcing and local partnerships. The complexity of verifying the quality and purity of functional ingredients across multiple suppliers adds another layer of difficulty. Any compromise in ingredient quality can damage brand reputation and lead to regulatory issues. Consequently managing these supply chain risks requires robust contingency planning and strong supplier relationships which are resource intensive to maintain. This ongoing instability threatens profit margins and consistent product availability posing a persistent challenge to market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | The Coca-Cola Company, Monster Beverage Corporation, PepsiCo, Inc., Celsius Holdings Inc., Red Bull GmbH, Otsuka Holdings Co., Ltd., Suntory Group, DANONE SA, Nestlé, The Hut.com Limited (Myprotein), Biotech USA, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The energy drinks and shots segment maintained dominance by accounting for a 54.5% share of the United States functional drinks market in 2025. This segment’s dominance in the regional market is driven by its widespread adoption among diverse consumer demographics and its association with high performance and alertness. Also, this category benefits from strong brand loyalty established by major players who have effectively marketed their products as essential tools for productivity and physical endurance. The versatility of energy drinks allows them to be consumed in various contexts including work study and exercise which broadens their appeal beyond traditional athletic use. According to various sources, energy drinks lead as the largest functional beverage category, accounting for approximately one-third of total functional beverage sales in the United States, reflecting their dominant position in consumer preferences. The availability of diverse formats such as cans bottles and concentrated shots caters to different consumption occasions and portability needs. Major brands like Red Bull and Monster Energy invest heavily in sponsorships of extreme sports and gaming events which reinforces their image as lifestyle enhancers. Data from public health tracking logs indicates that a significant portion of young adults consume energy drinks regularly to supplement or replace caffeine from traditional coffee. The innovation in flavor profiles and the introduction of sugar free variants have further expanded the customer base to include health conscious individuals who seek energy boosts without excessive calorie intake. This segment's ability to adapt to trending consumer interests while maintaining core functional benefits ensures its continued leadership in the market. The dominance of the energy drinks and shots segment is significantly fueled by the high prevalence of fatigue and the increasing demand for cognitive enhancement among the American workforce and student population. Modern lifestyles characterized by long working hours and academic pressures have created a persistent need for substances that can improve focus and sustain energy levels. According to the Centers for Disease Control and Prevention one in three adults does not get enough sleep leading to widespread daytime drowsiness and reduced productivity. This sleep deficit drives consumers to seek quick and effective solutions such as energy drinks that provide immediate stimulation through caffeine and other stimulants. The rise of the gig economy and remote work has also blurred the boundaries between work and rest requiring individuals to manage their energy levels more actively. Data from the American Psychological Association reveals that stress levels have increased significantly with many individuals reporting difficulty in concentrating and maintaining mental clarity. Energy drinks are often perceived as reliable aids for overcoming these challenges offering a convenient way to boost alertness during critical tasks. Furthermore the growing popularity of esports and competitive gaming has created a niche market where players rely on energy shots to maintain reaction times and focus during prolonged sessions. This sustained demand for cognitive and physical enhancement ensures that energy drinks remain the leading type in the functional beverages sector. The leadership of the energy drinks and shots segment is reinforced by aggressive marketing strategies and the cultivation of strong brand loyalty among younger demographics particularly millennials and Generation Z. Companies in this sector utilize high impact advertising campaigns featuring influencers athletes and musicians to create an aspirational image associated with energy and vitality. These marketing efforts often emphasize themes of adventure extreme sports and social connectivity which resonate deeply with youth culture. The integration of brands into popular cultural events such as music festivals and gaming tournaments further solidifies their presence in the lives of target audiences. The use of limited edition flavors and collaborative packaging designs creates a sense of exclusivity and urgency that drives repeat purchases. Additionally social media campaigns encourage user generated content which amplifies brand visibility and fosters community engagement. As per the Journal of Consumer Research brand identity plays a crucial role in purchase decisions for this demographic making loyalty a key driver of market share. The ability of energy drink companies to maintain relevance through dynamic marketing ensures their continued domination in the functional drinks landscape.

The nutraceutical drinks segment is predicted to witness the highest CAGR of 8.5% during the forecast period. This rapid expansion of the segment is driven by the increasing consumer focus on preventive health and the desire for beverages that offer specific wellness benefits beyond hydration. Nutraceutical drinks include products fortified with vitamins minerals probiotics antioxidants and herbal extracts that support immune function digestive health and overall well being. According to the Nutrition Business Journal the demand for functional foods and beverages with health claims has surged as consumers become more educated about the link between diet and disease prevention. The aging population in the United States is also contributing to this growth as older adults seek products that support joint health cognitive function and cardiovascular wellness. The innovation in formulation technologies has allowed manufacturers to create tasty and stable beverages that deliver effective doses of bioactive compounds. Furthermore the rise of personalized nutrition has led to the development of targeted nutraceutical drinks that address individual health needs such as stress relief or sleep improvement. This segment's ability to align with holistic health trends and scientific advancements positions it as the primary engine of future growth in the US functional drinks market. The swift growth of the nutraceutical drinks segment is primarily driven by the rising interest in preventive healthcare and the specific demand for immune support solutions among American consumers. The global health crisis has heightened awareness of the importance of a robust immune system leading many individuals to seek dietary interventions that bolster their natural defenses. Nutraceutical drinks enriched with vitamin C vitamin D zinc and elderberry are particularly popular as they offer a convenient and enjoyable way to consume these essential nutrients. The convenience of ready to drink formats appeals to busy consumers who may not have time to prepare homemade remedies or take multiple pills. Additionally the trend toward holistic wellness has expanded the scope of nutraceutical drinks to include ingredients that support gut health such as probiotics and prebiotics. As per the American Gastroenterological Association there is growing evidence linking gut health to immune function which has further validated the demand for these products. The scientific backing for these ingredients provides consumers with confidence in their efficacy driving sustained adoption. This focus on prevention and immunity ensures that nutraceutical drinks continue to grow at an accelerated pace. The accelerated growth of the nutraceutical drinks segment is further supported by continuous innovation in bioactive ingredients and the increasing scientific validation of their health benefits. Manufacturers are investing in research and development to discover new functional compounds and improve the bioavailability of existing ones ensuring that consumers receive maximum benefit from each serving. According to the Journal of Functional Foods advances in encapsulation technology have enabled the stable incorporation of sensitive ingredients such as curcumin and omega 3 fatty acids into beverages without compromising taste or shelf life. This technological progress has expanded the range of health claims that can be made for nutraceutical drinks attracting a broader audience. The collaboration between beverage companies and nutritional scientists has led to the creation of specialized drinks targeting specific conditions such as inflammation anxiety and metabolic health. As per the National Institutes of Health ongoing studies continue to uncover the potential of adaptogens and nootropics in enhancing mental and physical performance. This scientific rigor builds trust and credibility which are essential for long term market growth. Furthermore the transparency in labeling and sourcing allows consumers to make informed choices reinforcing their commitment to these products. The combination of innovation and validation ensures that nutraceutical drinks remain at the forefront of the functional beverage industry.

By Distribution Channel Insights

In 2025, the convenience stores segment remained the largest by occupying a 38.6% share of the United States functional drinks market. This prominence of the segment was supported by the strategic location of these outlets in high traffic areas and their alignment with the impulse buying behavior of consumers. Functional drinks especially energy drinks and shots are often purchased on the go to address immediate needs for energy or hydration. According to a study, convenience channels account for 43 percent of total beverage alcohol dollar sales and hold a commanding share of immediate-consumption packaged beverage volume in the United States, highlighting their critical role in the distribution network. The extensive network of convenience stores across the country ensures that functional drinks are readily accessible to consumers at any time of day or night. The compact size of these stores allows for efficient placement of high margin items such as functional beverages near checkout counters which increases visibility and purchase likelihood. The speed of transaction and ease of access make convenience stores the preferred choice for busy professionals students and commuters. Additionally the ability of convenience stores to quickly introduce new products and limited time offers allows them to capitalize on emerging trends rapidly. This agility combined with widespread presence ensures that convenience stores remain the primary channel for functional drink consumption. The spearheading of this segment is driven by the strategic location of these outlets and their ability to capitalize on impulse purchase behavior among consumers. Convenience stores are typically situated near workplaces schools gas stations and transit hubs where foot traffic is high and consumers are often in a hurry. According to the U.S. Census Bureau, the average American one-way commute time is approximately 27.6 minutes, during which many individuals stop at convenience stores for refreshments. This proximity to daily routes makes it easy for consumers to grab a functional drink without deviating from their schedule. The layout of convenience stores is designed to facilitate quick transactions with high demand items like energy drinks placed prominently at eye level or near the register. Data from the Point of Purchase Advertising International Institute indicates that impulse buys account for up to 70 percent of convenience store sales demonstrating the effectiveness of this retail environment. The immediate gratification provided by purchasing a cold functional drink satisfies the instant needs of consumers experiencing fatigue or thirst. Furthermore the extended operating hours of convenience stores ensure availability during early mornings and late nights when other retail options are closed. As per the National Association of Convenience Stores the majority of functional drink purchases occur during peak commuting hours reinforcing the link between location and sales. This combination of accessibility and psychological triggers ensures that convenience stores maintain their dominant position in the distribution landscape. The top spot of the convenience store channel is further reinforced by its extensive network and the high product turnover rates characteristic of this retail format. The United States is home to over 150000 convenience stores creating a dense distribution grid that reaches urban suburban and rural communities. According to the National Association of Convenience Stores this vast footprint ensures that functional drinks are available to a wide demographic across diverse geographic regions. The high frequency of restocking in convenience stores allows for fresh inventory and the rapid introduction of new products which keeps the assortment relevant and appealing. This rapid movement of goods reduces the risk of spoilage and ensures that consumers always have access to popular brands. The ability of convenience store operators to negotiate favorable terms with suppliers due to their collective purchasing power also contributes to competitive pricing. As per the Convenience Store News the efficiency of supply chain logistics for single serve beverages has improved significantly enabling faster delivery and reduced stockouts. The high visibility of functional drinks in these high traffic environments drives continuous sales volume. This operational efficiency and widespread availability make convenience stores an indispensable channel for functional drink manufacturers seeking to maximize market penetration.

But the online distribution segment is anticipated to witness the fastest CAGR of 11.2% from 2026 to 2034 due to the increasing adoption of e commerce platforms and the changing shopping habits of consumers who prefer the convenience of home delivery. The availability of a wide variety of functional drinks online allows consumers to explore niche brands and specialized products that may not be available in local stores. The subscription models offered by many online retailers provide a convenient way for consumers to ensure a steady supply of their favorite functional drinks without the need for repeated purchases. The ability to read detailed product descriptions and customer reviews online also helps consumers make informed decisions about complex functional ingredients. Furthermore the integration of social media marketing with e commerce platforms has streamlined the path from discovery to purchase. As per the Digital Commerce 360 report the seamless user experience and personalized recommendations offered by online retailers drive higher conversion rates. This digital transformation of beverage retailing positions online distribution as the primary growth engine for the functional drinks sector. The quick surge of this segment is significantly supported by the expansion of e commerce infrastructure and the improvement of last mile delivery services. Major retailers and specialized beverage platforms have invested heavily in warehousing and logistics networks to ensure fast and reliable delivery of functional drinks. According to the United States Postal Service, the volume of package deliveries has increased by approximately 3 percent, reflecting the growing capacity of the delivery ecosystem. The development of advanced tracking systems and real time updates enhances the customer experience by providing transparency and reducing uncertainty about delivery times. The ability to deliver heavy cases of beverages directly to consumers doorsteps eliminates the physical burden of transporting these items from physical stores. Furthermore the integration of automated sorting and routing technologies has reduced delivery costs and improved efficiency. As per the Supply Chain Dive report innovations in delivery drones and autonomous vehicles are being tested to further enhance speed and reliability. The widespread availability of same day and next day delivery options has made online purchasing increasingly competitive with brick and mortar stores. This robust logistical framework enables online retailers to serve a broader customer base and handle higher order volumes. The continuous improvement in delivery infrastructure ensures that online distribution remains a viable and attractive option for functional drink consumers. The rapid expansion of the online distribution segment is further driven by the extensive availability of niche products and the popularity of subscription models. Online platforms offer a virtually unlimited shelf space allowing consumers to access a wide range of functional drinks including those with specialized ingredients or targeted health benefits. This diversity appeals to consumers with specific dietary needs or preferences such as vegan keto or organic options that may not be stocked in local convenience stores. The subscription model has gained traction as it offers convenience and cost savings through recurring deliveries of favorite products. These models often include personalized recommendations and exclusive discounts which enhance customer loyalty and retention. Furthermore online platforms facilitate direct engagement between brands and consumers allowing for feedback and community building. As per the Harvard Business Review subscription models provide predictable revenue streams for companies and ensure consistent product availability for users. The combination of variety and convenience makes online distribution an increasingly preferred channel for functional drink enthusiasts. This trend ensures that online sales continue to outpace other distribution channels in terms of growth rate.

COUNTRY ANALYSIS

U.S. Functional Drinks Market Analysis

The United States led the North American functional drinks market and captured a 85.8% share in 2025. This dominant position is driven by a highly developed consumer culture that prioritizes health wellness and convenience. The country boasts a robust infrastructure for beverage production and distribution enabling efficient market penetration and product availability. According to the United States Department of Agriculture the agricultural sector provides a steady supply of raw materials such as fruits herbs and dairy which are essential for functional drink formulation. The high disposable income of American consumers allows for frequent purchase of premium functional beverages which often command higher prices than standard soft drinks. Data from the Bureau of Economic Analysis indicates that personal consumption expenditures on health related products remain strong reflecting the willingness of individuals to invest in their well being. The presence of major global beverage corporations headquartered in the United States fosters continuous innovation and marketing excellence. These companies leverage advanced research facilities to develop new formulations and validate health claims. Furthermore the diverse demographic landscape of the United States creates varied demand for different types of functional drinks ranging from energy boosters for young professionals to immune supports for older adults. As per the Census Bureau the aging population is expanding the market for health focused beverages. The regulatory framework provided by the Food and Drug Administration ensures product safety and labeling accuracy which builds consumer trust. This combination of economic strength cultural trends and industrial capability ensures that the United States remains the central hub for the functional drinks industry. The leading position of the United States in the functional drinks market is significantly influenced by high consumer awareness and the deep integration of these products into daily lifestyles. Americans are increasingly educated about the benefits of functional ingredients and actively seek beverages that support their health goals. According to a survey by the International Food Information Council, approximately 50 percent of consumers read labels to understand the functional benefits of their food and beverage choices. This informed decision making drives demand for transparent and scientifically backed products. The busy lifestyle of the average American characterized by long work hours and active social schedules creates a need for convenient health solutions. Data from the Bureau of Labor Statistics shows that leisure and personal care time is limited prompting individuals to choose products that offer multiple benefits in a single serving. Functional drinks fit seamlessly into this routine providing hydration energy and nutrition without additional effort. The influence of social media and health influencers further amplifies awareness and encourages experimentation with new products. As per research, a significant portion of adults use social media to discover health and wellness trends. This digital exposure accelerates the adoption of new functional beverages. The cultural acceptance of using supplements and fortified foods as part of a healthy lifestyle reinforces the market position. This synergy between awareness and lifestyle ensures sustained growth and leadership in the global functional drinks sector. The dominance of the United States in the functional drinks market is underpinned by a robust innovation ecosystem and a clear regulatory framework that supports product development. The country is home to leading research institutions and private laboratories that drive advancements in food science and nutrition. According to the National Science Foundation investment in food technology research has increased significantly fostering the discovery of new functional ingredients and delivery systems. This scientific foundation allows companies to create innovative products with proven efficacy. The Food and Drug Administration provides guidelines for labeling and health claims which although stringent offer a pathway for credible marketing. The presence of venture capital firms specializing in food tech further supports startups and emerging brands in bringing novel concepts to market. As per the Crunchbase database funding for food and beverage startups in the United States remains among the highest globally. This financial support enables rapid scaling and commercialization of innovative ideas. The collaborative environment between academia industry and regulators ensures that the market remains dynamic and responsive to consumer needs. This supportive ecosystem encourages continuous improvement and differentiation. The ability to innovate within a structured regulatory environment ensures that the United States maintains its competitive edge and leadership in the functional drinks industry.

COMPETITIVE LANDSCAPE

The competition in the United States functional drinks market is intense and characterized by a mix of established giants and agile newcomers vying for consumer attention. Major corporations leverage their extensive distribution networks and marketing budgets to maintain dominance while niche brands differentiate through specialized formulations and targeted messaging. The market sees frequent product launches as companies strive to meet the evolving demands for health focused and natural ingredients. Price competition is moderate with many brands opting for premium positioning based on perceived health benefits and quality. Innovation in packaging and delivery formats serves as a key differentiator in this crowded landscape. Consumer loyalty is increasingly driven by brand values such as sustainability and transparency rather than just taste. Retailers play a crucial role by deciding shelf space allocation which influences visibility and sales. The rise of private label options adds pressure on branded players to justify higher prices with superior quality or unique benefits. Digital engagement and community building have become essential tools for fostering brand advocacy. Companies must continuously adapt to regulatory changes and consumer trends to remain relevant. This dynamic environment requires constant innovation and strategic agility to sustain growth and profitability in the face of rigorous competition.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. functional drinks market include

- The Coca-Cola Company

- Monster Beverage Corporation

- PepsiCo, Inc.

- Celsius Holdings Inc

- Red Bull GmbH

- Otsuka Holdings Co., Ltd.

- Suntory Group

- DANONE SA

- Nestlé

- The Hut.com Limited (Myprotein)

- Biotech USA

TOP PLAYERS IN THE MARKET

- Monster Beverage Corporation stands as a pivotal entity in the United States functional drinks landscape primarily known for its extensive portfolio of energy beverages. The company leverages a robust distribution network through strategic partnerships with major bottlers to ensure widespread product availability across diverse retail channels. Recent initiatives focus on expanding its product line to include healthier options such as zero sugar variants and natural ingredient formulations to align with evolving consumer preferences. Monster actively invests in marketing campaigns targeting younger demographics through sponsorships of extreme sports and music events. The company also emphasizes innovation in packaging sizes and flavors to capture impulse purchases. By maintaining a strong brand identity and continuously introducing novel products Monster reinforces its competitive stance. Its ability to adapt quickly to market trends and consumer feedback ensures sustained relevance. The corporation prioritizes operational efficiency and supply chain optimization to support growth. These efforts collectively strengthen its position as a leading innovator and distributor in the dynamic functional beverage sector without relying solely on legacy products.

- Red Bull GmbH maintains a formidable presence in the United States functional drinks market through its iconic branding and unique marketing strategies. The company is renowned for creating high impact events and content that associate its brand with extreme performance and adventure. This approach fosters deep emotional connections with consumers particularly among athletes and young adults. Red Bull focuses on premium positioning and consistent quality to justify its price point in a competitive environment. Recent actions include expanding its distribution into convenience stores and gas stations to enhance accessibility for on the go consumers. The company also invests heavily in digital platforms to engage directly with its audience through social media and interactive experiences. Red Bull continues to innovate with limited edition flavors and specialized product lines tailored to specific lifestyle segments. Its commitment to sustaining high visibility through global sports sponsorships reinforces brand loyalty. By prioritizing brand equity over aggressive pricing Red Bull sustains its leadership. The company’s strategic focus on experiential marketing differentiates it from competitors and drives consistent demand.

- Celsius Holdings Inc has emerged as a significant competitor in the United States functional drinks market by positioning its products as healthy energy alternatives. The company focuses on fitness oriented consumers offering beverages that claim to boost metabolism and provide sustained energy without crashes. Celsius leverages scientific backing and clinical studies to validate its health claims which appeals to health conscious individuals. Recent strategies involve expanding retail presence in major grocery chains and fitness centers to target active lifestyles. The company actively engages with influencers and fitness communities to build credibility and trust. Celsius also emphasizes clean label ingredients avoiding artificial preservatives and high fructose corn syrup. This transparency resonates with modern consumers seeking wholesome options. The brand has invested in digital marketing campaigns highlighting real user testimonials and transformation stories. By aligning with wellness trends and promoting a healthy lifestyle Celsius captures a growing niche market. Its agile approach to product development and targeted marketing enables rapid growth. The company continues to innovate with new flavors and formats to maintain momentum and expand its customer base effectively.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States functional drinks market employ diverse strategies to maintain competitiveness and drive growth. Product innovation remains central with companies frequently launching new flavors and formulations to meet changing consumer preferences. Brands focus on clean label ingredients and natural sweeteners to appeal to health conscious buyers. Strategic partnerships with distributors and retailers ensure widespread availability and visibility in high traffic locations. Digital marketing and social media engagement are utilized to build brand loyalty and connect with younger demographics. Sponsorships of sports events and fitness activities enhance brand association with active lifestyles. Companies also invest in sustainability initiatives such as eco-friendly packaging to address environmental concerns. Subscription models and direct to consumer sales channels are expanded to improve customer retention. Pricing strategies often include premium positioning for specialized products while offering value packs for regular consumers. Continuous research and development support the creation of scientifically backed health claims. These combined approaches enable companies to differentiate their offerings and capture market share in a saturated industry.

MARKET SEGMENTATION

This research report on the U.S. functional drinks market has been segmented and sub-segmented into the following categories.

By Type

- Energy Drinks & Shots

- Sports Drinks

- Isotonic

- Hypotonic

- Hypertonic

- Nutraceutical Drinks

- Probiotic Drinks

- Dairy-based Probiotic Drinks

- Plant-based Probiotic Drinks

- Kombuchas

- Probiotic Juices

- Kefir

- Others

- Functional Water

- Vitamin Water

- Protein Water

- Electrolyte Water

- CBD Infused Water

- Others

- Others

- Probiotic Drinks

By Distribution Channel

- Hypermarkets / Supermarkets

- Convenience Stores

- Specialty Stores

- Online

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. functional drinks market?

The U.S. functional drinks market supplies beverages with added benefits like energy, hydration, or gut health sold through retail and direct channels for wellness seekers.

How does the U.S. functional drinks market work?

The U.S. functional drinks market combines ingredient innovation, branding, and distribution across stores and online to deliver targeted health benefits to consumers.

What drives growth in the U.S. functional drinks market?

Consumer wellness focus, sober-curious trends, and demand for on-the-go nutrition fuel expansion of the U.S. functional drinks market.

Which categories lead the U.S. functional drinks market?

Energy, sports recovery, enhanced waters, and probiotic beverages are top performers shaping product development in the U.S. functional drinks market.

How important is clean labeling in the U.S. functional drinks market?

Clean labels and natural ingredients are critical in the U.S. functional drinks market to build trust and appeal to health-conscious buyers.

What role do retailers play in the U.S. functional drinks market?

Retailers shape availability and visibility in the U.S. functional drinks market through shelf placement, cold display, and promotional support.

How does direct-to-consumer affect the U.S. functional drinks market?

DTC channels let brands in the U.S. functional drinks market educate buyers, test innovations, and build subscription revenue streams.

What trends shape the U.S. functional drinks market?

Adaptogens, low sugar formulations, cognitive claims, and alcohol alternatives are evolving preferences in the U.S. functional drinks market.

How do regulations affect the U.S. functional drinks market?

Labeling and health claim rules shape product messaging and compliance across the U.S. functional drinks market.

What role do natural ingredients play in the U.S. functional drinks market?

Natural botanicals, electrolytes, and probiotics drive product trust and differentiation within the U.S. functional drinks market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com