U.S. Mobile Advertising Market Size, Share, Trends & Growth Forecast Report By Format Type, By Vertical, and By Country (California, New York, Texas, Florida & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

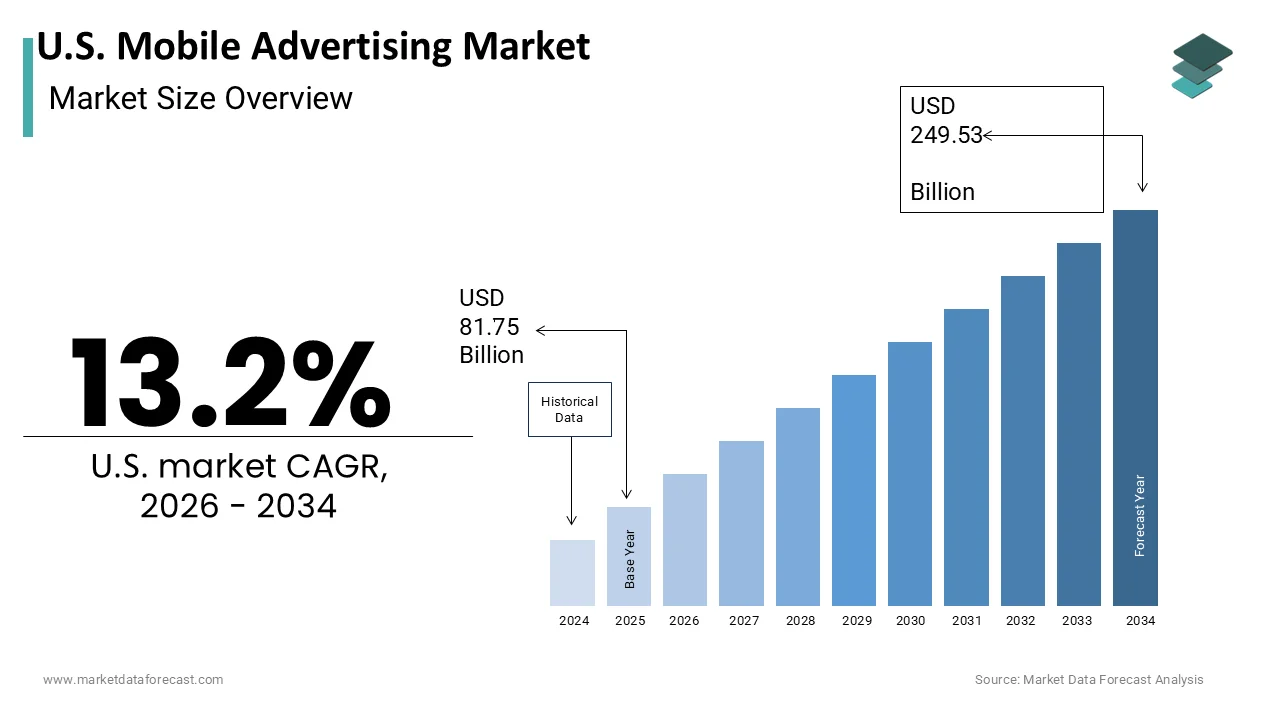

Market Size, 2025

$81.75 BnMarket Estimate, 2026

$92.54 BnMarket Forecast, 2034

$249.53 BnCAGR, 2026–2034

13.2%U.S. Mobile Advertising Market Size

The U.S. Mobile Advertising Market is projected to grow from USD 81.75 billion in 2025 to USD 92.54 billion in 2026 and reach USD 249.53 billion by 2034, registering a CAGR of 13.2% during the forecast period from 2026 to 2034.

Over the next few years, the U.S. is likely to experience substantial growth in its mobile advertising landscape, driven by the expansion of next-generation telecom infrastructure and shifting content consumption habits. The ubiquity of mobile devices has transformed them into the primary interface for consumer engagement with brands. As per the Pew Research Center, approximately 90% of American adults own a smartphone, creating an extensive addressable audience for advertisers. The shift in consumer behavior towards mobile-first content consumption dictates media spending strategies across industries. According to the Bureau of Labor Statistics, Americans spend an average of 3 hours daily on leisure and sports activities, which heavily includes digital media consumption on mobile devices, indicating the substantial attention economy available for monetization. The integration of location-based services allows marketers to deliver contextually relevant ads based on physical proximity to retail outlets. Privacy regulations and operating system updates have fundamentally altered data collection practices, forcing the industry to adopt new measurement standards. The transition away from third-party cookies necessitates innovative solutions for identity resolution and attribution. Mobile advertising serves as the backbone of digital commerce, driving direct response actions such as app installs and e-commerce purchases. The interplay between user experience, ad format innovation, and regulatory compliance defines the current operational landscape. This market is characterized by rapid technological adaptation and intense competition for user attention in an increasingly saturated digital environment.

MARKET DRIVERS

Pervasive Smartphone Penetration and Increased Screen Time

Pervasive smartphone penetration and increased screen time are fuelling the growth of the U.S. mobile advertising market by ensuring constant connectivity and engagement. The widespread adoption of mobile devices has created an always-on environment where consumers are accessible throughout the day. According to the Pew Research Center, 90% of U.S. adults own a smartphone, which provides advertisers with a direct channel to reach diverse demographics. This high level of device ownership ensures that mobile advertising campaigns can achieve broad reach and frequency. As per eMarketer, the average American adult spends more than 4.5 hours per day on mobile devices, significantly surpassing time spent on desktop computers or traditional television. This substantial allocation of attention creates ample inventory for ad placements across social media, streaming apps, and mobile games. The convenience of mobile access encourages impulse purchases and immediate interactions with branded content. Consumers frequently use their devices for shopping research, price comparisons, and social networking, making these moments valuable for targeted advertising. The habitual nature of mobile usage fosters deeper engagement with interactive ad formats, such as playable ads and augmented reality experiences. Advertisers leverage this sustained attention to build brand awareness and drive conversions. The continuous growth in mobile internet speeds further enhances the quality of ad delivery, enabling rich media experiences. Consequently, the sheer volume of time spent on mobile devices sustains robust demand for advertising inventory.

Advancements in Programmatic Advertising and Artificial Intelligence

Advancements in programmatic advertising and artificial intelligence significantly propel the expansion of the U.S. mobile advertising market. Programmatic platforms automate the buying and selling of ad inventory using algorithms that analyze user data in real time. According to the Interactive Advertising Bureau, more than 90% of digital display ad dollars are transacted through programmatic channels, allowing for precise targeting and optimization. Artificial intelligence enhances this process by predicting user behavior and identifying high-value audiences with greater accuracy. As per Gartner, companies employing AI-facilitated marketing strategies have witnessed campaign performance improve by 30%, which manifests through improved personalization and reduced waste. Machine learning models analyze vast datasets to determine the optimal timing, placement, and creative elements for each impression. This level of sophistication enables advertisers to deliver relevant messages to users at the right moment in their customer journey. Real-time bidding ensures that ad spend is allocated efficiently, maximizing impact within budget constraints. The ability to adjust campaigns dynamically based on performance metrics reduces manual intervention and improves agility. Advanced analytics provide deeper insights into consumer preferences, enabling more compelling creative strategies. The integration of AI also facilitates fraud detection, protecting advertisers from invalid traffic. These technological enhancements make mobile advertising more measurable and accountable. Thus, the evolution of programmatic and AI technologies drives continued investment in mobile channels.

MARKET RESTRAINTS

Stringent Data Privacy Regulations and Consent Requirements

Stringent data privacy regulations and consent requirements hinder the growth of the U.S. mobile advertising market. Laws such as the California Consumer Privacy Act and the Virginia Consumer Data Protection Act impose strict guidelines on how personal information is gathered and used. According to the International Association of Privacy Professionals, compliance with these varying state laws increases operational complexity and legal costs for advertisers. Users are increasingly empowered to opt out of data tracking, which reduces the volume of actionable insights available for targeting. As per Apple, the implementation of App Tracking Transparency requires apps to obtain explicit user permission before tracking activity across other companies' apps and websites. Industry estimates suggest that only 25% of iOS users opt in to tracking, severely limiting the ability to create detailed user profiles. This reduction in data availability hinders the precision of audience segmentation and attribution modeling. Advertisers face challenges in measuring campaign effectiveness and return on ad spend without granular, user-level data. The fragmentation of privacy standards across different jurisdictions creates uncertainty for national campaigns. Companies must invest heavily in legal counsel and compliance infrastructure to avoid penalties. The shift towards privacy-centric models requires fundamental changes in advertising strategies. Consequently, regulatory pressures act as a significant brake on traditional targeting methods.

Ad Fraud and Invalid Traffic Concerns

Ad fraud and invalid traffic concerns pose a major restraint to the U.S. mobile advertising market by eroding trust and wasting advertising budgets. Fraudulent activities, such as click injection, spoofing, and bot traffic, generate fake impressions and clicks that do not result in genuine user engagement. According to the Association of National Advertisers, ad fraud costs U.S. businesses billions of dollars annually, with mobile channels being particularly vulnerable due to the complexity of the app ecosystem. As per Juniper Research, global losses from digital advertising fraud are projected to escalate dramatically, with mobile channels bearing a disproportionate share as fraudsters employ more sophisticated techniques to mimic human behavior. The prevalence of fraud makes it difficult for advertisers to accurately assess the performance of their campaigns. Brands may hesitate to increase mobile ad spend if they perceive a high risk of financial loss due to invalid traffic. The lack of transparency in the programmatic supply chain exacerbates the problem, as ads may pass through multiple intermediaries before reaching the user. Verification tools and third-party audits add additional costs and complexity to campaign management. Despite advancements in fraud detection technology, the cat-and-mouse game between fraudsters and security firms continues. The reputational damage associated with fraudulent ads can deter premium brands from investing in certain mobile inventory. This persistent threat undermines confidence in mobile advertising metrics. Thus, ad fraud remains a critical challenge that impedes market growth.

MARKET OPPORTUNITIES

Expansion of Retail Media Networks and First-Party Data Utilization

The expansion of retail media networks and first-party data utilization is a promising opportunity for the U.S. mobile advertising market by offering alternative targeting solutions in a post-cookie era. Retailers are leveraging their extensive customer databases to create closed-loop advertising ecosystems where ads are served directly on their mobile apps and websites. According to Insider Intelligence, retail media network ad spending in the U.S. is expected to capture a massive portion of total digital ad budgets as brands seek high-intent audiences. These networks utilize first-party data, such as purchase history and browsing behavior, to deliver highly relevant ads without relying on third-party trackers. As per Amazon Advertising, sponsored product ads on mobile devices drive substantial sales conversion due to their proximity to the point of purchase. The ability to attribute ad exposure directly to sales provides clear return on investment metrics that appeal to marketers. Retail media networks offer a walled-garden environment where data privacy is maintained within the platform, reducing regulatory risks. Brands can target shoppers based on specific product interests and lifecycle stages, enhancing personalization. The integration of offline and online data further enriches audience profiles. This shift towards owned data assets empowers retailers to become major players in the advertising landscape. Advertisers benefit from access to verified consumer insights and high conversion rates. Consequently, the rise of retail media networks creates new revenue streams and strategic partnerships.

Integration of Augmented Reality and Immersive Ad Formats

The integration of augmented reality and immersive ad formats offers a notable avenue for the U.S. mobile advertising market. AR technology allows consumers to visualize products in their real-world environment through their smartphone cameras, creating interactive and memorable experiences. According to Snap Inc., AR lenses and filters generate higher engagement rates and lift in purchase intent compared to traditional static formats. As per Shopify, interaction with 3D and AR products on e-commerce platforms can boost conversion rates by up to 94%, demonstrating the immense commercial value of immersive advertising. Brands in sectors such as beauty, fashion, and home decor utilize AR try-on features to reduce uncertainty and increase confidence in buying decisions. The gamification of ads through AR filters and lenses encourages social sharing, extending organic reach. Mobile devices are uniquely suited for AR experiences due to their built-in cameras and sensors. The advancement of 5G networks supports the seamless delivery of high-quality AR content without latency issues. Advertisers can collect valuable data on user interactions with AR elements to refine future campaigns. The novelty and utility of AR formats differentiate brands in a crowded digital landscape. This technology transforms passive ad viewing into active participation. The growing accessibility of AR development tools lowers barriers for smaller brands. Thus, immersive formats represent a key growth driver for mobile advertising innovation.

MARKET CHALLENGES

Fragmentation of Measurement and Attribution Standards

The fragmentation of measurement and attribution standards is a key challenge to the growth of the U.S. mobile advertising market by complicating the assessment of campaign effectiveness. The deprecation of third-party cookies and identifiers for advertisers has disrupted traditional tracking methods, leading to discrepancies across different platforms. According to the Mobile Marketing Association, the lack of a unified identity solution makes it difficult to track user journeys across multiple devices and apps. As per Google, the transition to privacy sandbox technologies requires advertisers to adopt new attribution models that rely on aggregated data rather than individual user records. This shift reduces the granularity of insights, making it harder to optimize campaigns in real time. Different walled gardens, such as Meta, Amazon, and Google, operate with proprietary measurement systems that do not always align. Advertisers struggle to compare performance metrics across channels, leading to inefficient budget allocation. The complexity of multi-touch attribution in a privacy-constrained environment requires advanced statistical modeling, which may be inaccessible to smaller businesses. Inconsistent reporting standards create confusion and hinder collaboration between agencies and clients. The industry is still experimenting with various solutions, such as clean rooms and contextual targeting, but no single standard has emerged. This uncertainty delays decision-making and increases operational friction. Until a cohesive framework is established, measurement challenges will persist.

Ad Blocking Technology and Banner Blindness

Ad blocking technology and banner blindness pose significant challenges to the U.S. mobile advertising market by reducing viewability and engagement rates. A substantial portion of mobile users employ ad blockers to eliminate intrusive advertisements, improving their browsing experience. According to Blockthrough, mobile ad blocking has reached hundreds of millions of devices globally, with U.S. user adoption rising steadily on compatible browsers. As per HubSpot, banner blindness refers to the phenomenon where users consciously or subconsciously ignore banner-like information regardless of its relevance. This behavior decreases click-through rates and diminishes the effectiveness of traditional display ads. The prevalence of small screen sizes on mobile devices exacerbates the issue, as ads can easily obstruct content, leading to user frustration. Aggressive ad formats, such as pop-ups and auto-play videos, often trigger negative reactions and prompt users to install blocking tools. Advertisers must constantly innovate to create non-intrusive yet engaging formats that respect user experience. Native advertising and sponsored content offer alternatives but require higher production costs and creative effort. The arms race between ad tech providers and blocking software developers continues to evolve. Publishers face revenue losses as blocked ads fail to generate impressions. This dynamic forces the industry to rethink ad delivery mechanisms. Balancing monetization with user satisfaction remains a delicate and ongoing challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Format Type, Vertical, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, and the rest of the United States |

| Market Leaders Profiled | Google LLC, Meta Platforms, Inc., Amazon.com, Inc., Apple Inc., Microsoft Corporation, X Corp. (Twitter), Snap Inc., Pinterest, Inc., The Trade Desk, Inc., InMobi Pte. Ltd., Verizon Communications Inc., AppLovin Corporation |

SEGMENTAL ANALYSIS

By Format Type Insights

The search advertising segment held the dominant position in the U.S. mobile advertising market by capturing 44.7% of the U.S. market share in 2025. The growth of the search advertising segment in the U.S. market can be credited to high user intent and the immediate relevance of ads to consumer queries. High intent and immediate conversion potential drive the domination of search advertising in the U.S. mobile advertising market. Users actively searching for products or services on mobile devices demonstrate a clear purchase intent, making them highly valuable to advertisers. According to Google, mobile searches for local businesses result in a store visit or purchase within a short timeframe in a significant majority of instances. This proximity between query and action results in higher click-through rates and conversion rates compared to passive display formats. As per WordStream, the average click-through rate for search ads on mobile devices is historically strong, tracking significantly higher than the industry average for display ads. Advertisers benefit from paying only when users engage with their ads, ensuring efficient budget utilization. The ability to target specific keywords allows brands to reach consumers at critical decision-making moments. Mobile search often leads to direct actions, such as phone calls, direction requests, or app downloads. The immediacy of mobile devices facilitates instant gratification, aligning with consumer expectations for speed. This direct correlation between ad exposure and transaction sustains the leading position of search advertising. The measurable return on investment encourages continued investment in search campaigns. Consequently, search remains the cornerstone of mobile advertising strategies.

On the other side, the digital video advertising segment is expected to exhibit a promising CAGR of 16.4% during the forecast period in the U.S. market. Surge in short-form video consumption drives the rapid growth of digital video advertising in the U.S. mobile advertising market. Platforms like TikTok, Instagram Reels, and YouTube Shorts have revolutionized how users consume content on mobile devices. According to Nielsen, streaming via mobile and television screens has fundamentally changed daily media tracking, with adults dedicating hours to streaming video content daily. This high engagement provides ample opportunity for advertisers to insert native and non-intrusive ads. As per Insider Intelligence, short-form video ad spending is on pace for rapid multi-billion dollar expansions over the next three years, as brands recognize its effectiveness in reaching younger demographics. The algorithmic nature of these platforms ensures that ads are shown to users with relevant interests, increasing engagement rates. Vertical video formats are optimized for mobile screens, creating an immersive viewing experience. Interactive features, such as shoppable links and swipe-up actions, facilitate direct conversions. The viral potential of short-form content amplifies brand reach organically. Advertisers are shifting budgets from traditional television to mobile video to capture this attention. The creativity and authenticity of user-generated content inspire branded campaigns that resonate with audiences. This trend ensures sustained growth for digital video advertising.

By Vertical Insights

The retail and e-commerce vertical segment occupied 29.2% of the U.S. market share in 2025. The dominance of the retail and e-commerce segment in the U.S. market is driven by the seamless integration of shopping and advertising. Direct response and shoppable ad formats drive the domination of the Retail and E-Commerce vertical in the U.S. mobile advertising market. Mobile devices enable instant purchasing, allowing users to buy products directly from ads without navigating to a separate website. According to Shopify, mobile commerce dominates the structural layout of domestic online sales, accounting for the vast majority of all e-commerce transactions in the U.S. Shoppable posts on social media platforms, like Instagram and Pinterest, reduce friction in the customer journey. As per Meta Ads Manager, shoppable ads generate higher conversion rates compared to traditional link-based ads due to their convenience. Retailers leverage dynamic product ads to retarget users who have viewed items but not purchased. The ability to personalize offers based on browsing history increases relevance and sales probability. One-click checkout options further streamline the purchasing process on mobile devices. The immediacy of mobile shopping appeals to impulse buyers and deal seekers. Retailers invest heavily in mobile-optimized landing pages to ensure smooth transactions. The integration of augmented reality try-on features enhances confidence in online purchases. This seamless shopping experience sustains the leading position of the retail vertical. The direct link between ad exposure and revenue drives consistent investment.

On the other side, the healthcare segment is anticipated to register a CAGR of 17.5% during the forecast period in the U.S. market, owing to the rapid growth of the Healthcare vertical in the U.S. mobile advertising market. Consumers increasingly use mobile devices to access medical consultations, manage prescriptions, and track fitness goals. According to the American Telemedicine Association, digital health interactions and remote medical tracking have sustained permanent, elevated integration within the patient journey, creating a large user base for health-related apps. As per App Annie, health and fitness apps regularly log tens of millions of downloads across iOS and Android platforms. Pharmaceutical companies and healthcare providers advertise directly to consumers through these apps to promote services and medications. Mobile ads facilitate easy appointment scheduling and prescription refills, enhancing patient convenience. The personalization of health content based on user data improves engagement and adherence. Wearable device integration allows for real-time health monitoring and targeted interventions. Advertisers leverage this data to deliver relevant health tips and product recommendations. The stigma around certain health issues is reduced by the privacy of mobile interactions. The convenience of accessing care from home drives the adoption of digital health solutions. This trend ensures sustained growth for healthcare mobile advertising. The shift towards preventive care further expands market opportunities.

COUNTRY LEVEL ANALYSIS

U.S. Mobile Advertising Market Analysis

Over the next few years, the U.S. is likely to preserve its standing as the world's most sophisticated and heavily funded incubator for mobile advertising technology. The presence of major tech giants drives technological advancement and ad format innovation. The widespread availability of high-speed 5G networks enables rich media ad delivery and seamless user experiences. According to the Federal Communications Commission, 5G coverage has expanded to over 95% of the U.S. population, facilitating high-quality video and interactive ads. As per the Pew Research Center, the high level of digital literacy among Americans ensures effective engagement with complex ad formats. Consumers are accustomed to using mobile devices for all aspects of life, from banking to shopping, creating diverse advertising opportunities. The robust legal framework for digital commerce supports secure transactions and data handling. The presence of Silicon Valley fosters continuous innovation in ad tech and analytics. Major platforms, like Google and Meta, originate in the U.S., setting global standards for mobile advertising. The competitive landscape drives efficiency and creativity in campaign execution. High disposable income allows consumers to respond to premium product advertisements. The cultural acceptance of digital advertising reduces resistance to branded content. This combination of technological and behavioral factors ensures U.S. leadership. The continuous evolution of mobile capabilities sustains market dynamism. The U.S. serves as a testing ground for new advertising technologies before global rollout.

COMPETITIVE LANDSCAPE

The competition in the U.S. mobile advertising market is characterized by intense rivalry among technology giants and emerging retail media networks striving for advertiser budgets. Major players compete based on data granularity, audience reach,h and measurement capabilities. The market features a shift from open web programmatic buying towards walled gardens where companies control both inventory and user data. Google and Meta remain dominant but face increasing pressure from Amazon and TikTok, ok which offer unique engagement opportunities. Companies differentiate themselves through proprietary artificial intelligence tools that enhance targeting precision and creative optimization. The deprecation of third-party cookies has intensified the race for first-party data assets. Retailers are becoming significant competitors by leveraging transaction data for high-intent advertising. Price competitiveness remains important, but value-driven metrics such as return on ad spend are prioritized. Innovation in ad formats like shoppable video and augmented reality drives differentiation. Regulatory compliance and privacy protection are critical factors influencing advertiser trust. This dynamic environment fosters continuous technological advancement and strategic consolidation. The ability to provide transparent and effective solutions determines long-term success in this sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Mobile Advertising Market include

- Google LLC

- Meta Platforms, Inc.

- Amazon.com, Inc.

- Apple Inc.

- Microsoft Corporation

- X Corp. (Twitter)

- Snap Inc.

- Pinterest, Inc.

- The Trade Desk, Inc.

- InMobi Pte. Ltd.

- Verizon Communications Inc.

- AppLovin Corporation

TOP LEADING PLAYERS IN THE MARKET

- Alphabet Inc dominates the U.S. mobile advertising market through its Google search engine and YouTube video platform. The company leverages vast amounts of user data to deliver highly targeted ads across Android devices and mobile web browsers. Recent actions include the development of Privacy Sandbox technologies to replace third-party cookies while maintaining ad relevance. Alphabet has integrated artificial intelligence into its ad bidding systems to optimize campaign performance for advertisers. The firm continues to expand shoppable video features on YouTube, allowing users to purchase products directly from mobile ads. By focusing on privacy-compliant solutions and enhanced measurement tools, Alphabet strengthens its position as a primary destination for mobile ad spend. These innovations ensure sustained advertiser confidence and user engagement in an evolving regulatory landscape.

- Meta Platforms Inc contributes significantly to the market through its Facebook and Instagram applications, ns which are heavily accessed via mobile devices. The company utilizes advanced machine learning algorithms to personalize ad experiences based on user interactions and interests. Recent developments involve the expansion of Reels advertising formats to compete with short-form video competitors. Meta has introduced Advantage Plus shopping campaigns that automate targeting and creative optimization for e-commerce clients. The firm is also investing in augmented reality ad units that allow users to virtually try on products. By enhancing its business messaging tools, Meta facilitates direct communication between brands and consumers. These strategic initiatives improve conversion rates and drive higher return on investment for advertisers using its mobile platforms.

- Amazon.com Inc plays a crucial role in the U.S. mobile advertising market through its retail media network. The company leverages its extensive first-party shopper data to serve highly relevant sponsored product ads within its mobile app. Recent actions include the expansion of streaming television ads accessible via mobile devices and the integration of generative AI for ad creative generation. Amazon has enhanced its demand-side platform to allow advertisers to reach audiences beyond its own ecosystem. The firm focuses on closed-loop attribution, proving the direct impact of ads on sales. By offering unique access to purchase intent data, Amazon attracts brands seeking measurable results. These efforts solidify its status as a powerful alternative to traditional social and search advertising channels.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. mobile advertising market primarily employ strategies focused on artificial intelligence integration and privacy-centric data solutions to maintain a competitive advantage. Companies invest heavily in machine learning algorithms to automate ad buying and optimize creative performance in real time. Strategic partnerships with retail media networks enable access to valuable first-party shopper data for improved targeting. Firms prioritize the development of contextual advertising technologies to reduce reliance on third-party cookies. Expansion into short-form video and connected television formats captures growing user attention on mobile devices. Providers also focus on enhancing measurement tools to demonstrate clear return on investment for advertisers. Investment in augmented reality and interactive ad formats increases user engagement and brand recall. These strategic initiatives enable firms to navigate regulatory changes and deliver superior campaign outcomes.

MARKET SEGMENTATION

This research report on the U.S. mobile advertising market is segmented and sub-segmented into the following categories.

By Format Type

- Search Advertising

- Display Advertising

- Digital Video Advertising

- In-App Advertising

- Native Advertising

- Rich Media Advertising

By Vertical

- Retail & E-Commerce

- Healthcare

- BFSI

- Media & Entertainment

- IT & Telecommunications

- Automotive

- Travel & Hospitality

- Education

- Others

By Country

- California

- New York

- Texas

- Florida

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com