U.S Online Advertising Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Video Advertising, Native Advertising, Display Advertising, Full-Screen Interstitials, Others), Platform, Pricing Model, Industry, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 To 2034

U.S. Online Advertising Market Report Summary

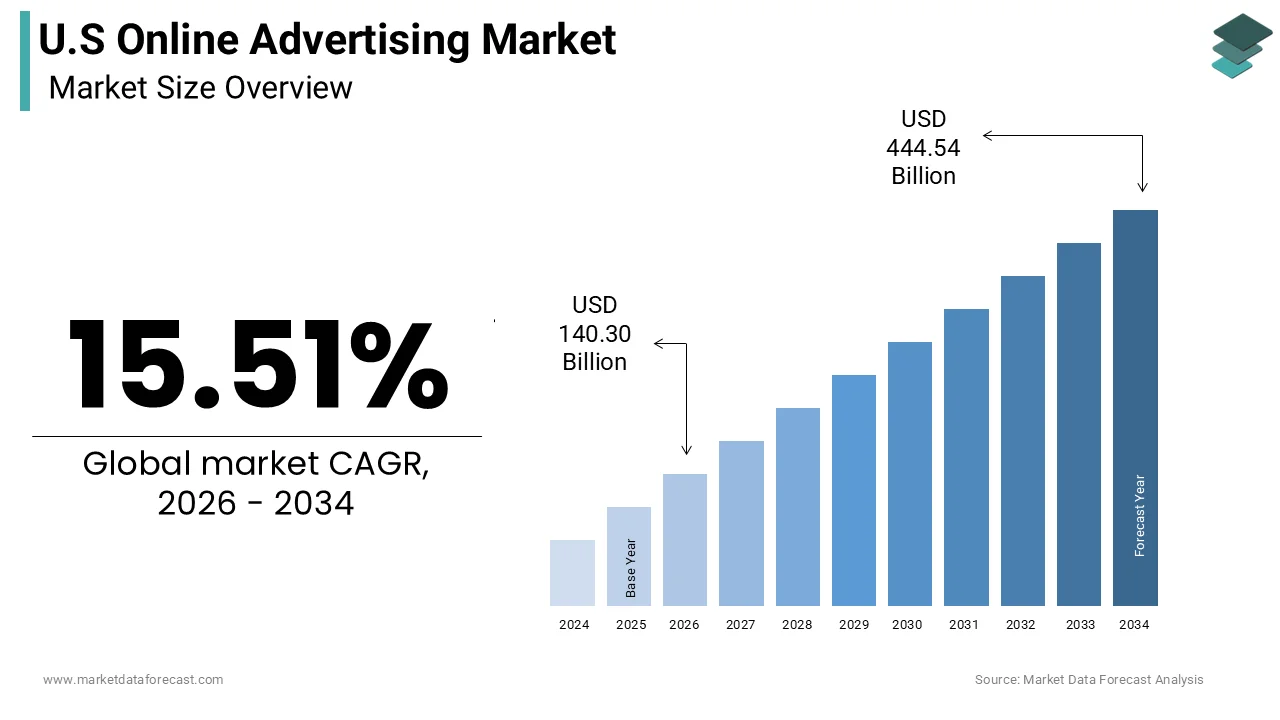

The United States online advertising market was valued at USD 121.46 billion in 2025 and is projected to reach USD 444.54 billion by 2034, growing from USD 140.30 billion in 2026 at a CAGR of 15.51% during the forecast period. Market growth is driven by increasing digital media consumption, rising mobile internet usage, and the growing adoption of data-driven advertising strategies. Advancements in AI, programmatic advertising, and personalized marketing are further accelerating the expansion of the U.S. online advertising market.

Key Market Trends

- Rapid growth of video and short-form digital advertising

- Increasing adoption of programmatic and AI-driven advertising

- Rising dominance of mobile advertising platforms

- Expansion of social media and influencer marketing campaigns

- Increasing use of personalized and data-driven ad targeting

Segmental Insights

- Based on type, the video advertising segment dominated the U.S. online advertising market in 2025 by accounting for 46.4% of the market share, driven by increasing video streaming and social media engagement

- Based on platform, the mobile devices segment held the dominant share in 2025 due to high smartphone penetration and mobile internet consumption

- Based on pricing model, the cost per mille (CPM) segment led the market in 2025 by capturing 46.3% of the market share, supported by widespread brand awareness campaigns

- Based on industry, the retail and consumer goods segment accounted for a significant share in 2025, driven by the growth of e-commerce and digital shopping behavior

Competitive Landscape

- The U.S. online advertising market is highly competitive, with companies focusing on AI-powered targeting, programmatic advertising, and cross-platform campaigns. Market players are investing in analytics, automation, and immersive advertising formats to improve customer engagement and advertising performance.

- Prominent players in the U.S. online advertising market include Google, Meta Platforms, Amazon Advertising, Microsoft Advertising, Adobe, LinkedIn, X Corp., Dentsu, Publicis Groupe, GroupM, The Interpublic Group of Companies (IPG), Hulu, BuzzFeed, WebFX, Outbrain

U.S Online Advertising Market Size

The U.S. online advertising market size was calculated to be USD 121.46 billion in 2025 and is anticipated to be worth USD 444.54 billion by 2034, from USD 140.30 billion in 2026, growing at a CAGR of 15.51% during the forecast period.

The online advertising is a digital ecosystem, where brands purchase ad space on internet-based platforms to reach consumers through search engines, social media websites, and mobile applications. Furthermore, the Federal Communications Commission reports that broadband adoption remains high, with 93% of adults having access to high-speed internet at home, facilitating seamless delivery of rich media content. According to the United States Census Bureau, e-commerce sales accounted for 15.6% of total retail sales in the fourth quarter of 2023, demonstrating the critical link between online visibility and consumer purchasing behavior. The integration of artificial intelligence and machine learning allows for precise audience segmentation by enhancing the efficiency of ad spend.

MARKET DRIVERS

Pervasive Mobile Device Adoption and Connectivity

The widespread ownership of smartphones by ensuring constant consumer connectivity, is propelling the growth of the United States online advertising market. As per the Research, 85% of American adults own a smartphone, which provides advertisers with continuous access to potential customers throughout the day. This device penetration enables location-based targeting and real-time engagement strategies that are impossible with traditional media. The average user spends over four hours daily on their mobile device, creating ample inventory for display video and social media advertisements. Mobile apps account for a significant portion of this usage, with consumers spending nearly 90% of their mobile time within applications rather than mobile browsers. This behavior drives demand for in-app advertising formats that offer immersive experiences. The rollout of fifth-generation networks further enhances this dynamic by reducing latency and enabling high-quality video ads without buffering issues. As per the study, 5G coverage has expanded rapidly, reaching over 80% of the population in urban areas. This infrastructure improvement supports richer ad formats such as augmented reality and interactive video, which command higher engagement rates. Advertisers leverage these capabilities to create personalized campaigns that resonate with users based on their immediate context and location. The seamless integration of commerce within mobile platforms allows for direct conversion from ad exposure to purchase.

Expansion of E-Commerce and Digital Retail Channels

The rapid growth of e-commerce directly fuels demand for online advertising as retailers compete for visibility in an increasingly crowded digital place, which is also bolstering the growth of the United States online advertising market. As per the United States Census Bureau, e-commerce sales reached 1.1 trillion dollars in 20,23 with a substantial portion of total retail activity. This shift necessitates robust digital marketing strategies to attract traffic and convert visitors into buyers. Online retailers rely heavily on search engine marketing and social media ads to reach consumers at various stages of the purchasing funnel. The ability to track user behavior and attribute sales to specific ad clicks provides a level of accountability that traditional advertising cannot match. The rise of marketplaces such as Amazon and Walmart has further intensified competition, prompting brands to invest in sponsored product listings and display ads within these platforms. This trend extends beyond pure play e-commerce giants as brick-and-mortar stores adopt omnichannel strategies that integrate online ads with offline inventory. The convenience of online shopping combined with targeted promotions drives consumer expectations for personalized offers. Advertisers respond by utilizing customer data to create relevant messages that increase click-through rates and conversions.

MARKET RESTRAINTS

Privacy Regulations and Data Protection Constraints

The stringent privacy regulations and evolving data protection standards by limiting the availability of user data for targeting are limiting the growth of the United States advertising market. The implementation of state-level laws, such as the California Consumer Privacy Act and the Virginia Consumer Data Protection Act, requires advertisers to obtain explicit consent before collecting personal information. The compliance with these regulations increases operational costs and complexity for digital marketing firms. The deprecation of third-party cookies by major web browsers further restricts the ability to track users across different websites. This change disrupts established retargeting and audience segmentation models, forcing advertisers to seek alternative solutions. The lack of standardized identity frameworks creates fragmentation, making it difficult to measure campaign effectiveness accurately. These methods often provide less granular insights than previous tracking mechanisms, leading to lower precision in ad delivery. This sentiment drives the adoption of ad blockers and privacy-focused browsers, which reduce the reachable audience. Advertisers must balance personalization with privacy compliance, resulting in potentially lower return on investment and increased friction in campaign execution.

Ad Fraud and Invalid Traffic Issues

Ad fraud and invalid traffic that undermines confidence and efficiency are restricting the growth of the United States online advertising market. Fraudulent activities, such as bot traffic click injection and domain spoofing, divert advertising budgets away from genuine human audiences. As per the Association of National Advertisers, ad fraud costs US businesses an estimated 5 billion dollars annually, resulting in wasted spend and distorted performance metrics. The sophistication of fraudulent schemes continues to evolve with bad actors using artificial intelligence to mimic human behavior and bypass detection systems. This environment forces advertisers to invest heavily in verification tools and third-party audits to ensure the integrity of their campaigns. The lack of transparency in the supply chain exacerbates the problem, as advertisers often do not know exactly where their ads are placed. Complex intermediaries between buyers and sellers obscure visibility by making it difficult to identify and block fraudulent sources. Brands may reduce their digital ad budgets or shift spend to walled gardens, where fraud risk is perceived to be lower.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Programmatic Advertising

The integration of artificial intelligence and machine learning into programmatic advertising platforms for enhanced efficiency and personalization is likely to pose new opportunities for the growth of the United States online advertising market. AI algorithms analyze vast amounts of data in real time to optimize bidding strategies and ad placement, ensuring that impressions are served to the most relevant audiences. The generative AI has the potential to add significant value to marketing and sales functions by automating content creation and improving customer insights. Programmatic platforms use predictive analytics to forecast user behavior and adjust campaigns dynamically, maximizing return on investment. This technology enables hyper-personalization where ads are tailored to individual preferences, browsing history, and contextual signals. AI facilitates this level of customization at scale, allowing brands to deliver unique messages to millions of users simultaneously. The automation of routine tasks, such as bid management and creative testing, frees up marketers to focus on strategic initiatives. Advances in natural language processing also enable better analysis of unstructured data such as social media comments and reviews, providing a deeper understanding of consumer sentiment. These insights inform creative strategies and improve engagement rates.

Growth of Connected Television and Streaming Services

The rapid adoption of connected television and streaming services for advertisers to reach cord-cutting audiences with premium video content is also expected to boost the growth of the United States online advertising market. Many US broadband households subscribe to at least one over-the-top video service, indicating a massive shift away from traditional cable. This trend creates new inventory for digital video ads that combine the impact of television with the targeting capabilities of the internet. Streaming platforms offer detailed viewer data, allowing advertisers to target specific demographics, interests, and viewing habits. The ability to measure view through conversions and attribution is superior to traditional TV, giving advertisers clearer insights into campaign performance. The proliferation of free ad-supported streaming television services further expands the addressable market by offering content without subscription fees. These platforms attract price-sensitive consumers who are willing to watch ads in exchange for free access. Advertisers can leverage this inventory to reach diverse audiences with high-quality video creatives.

MARKET CHALLENGES

Fragmentation of Media Channels and Audience Attention

The fragmentation of media channels and the dispersion of audience attention for advertisers seeking to achieve consistent reach and frequency which is likely to pose a challenge for the growth of the United States online advertising market. Consumers now distribute their time across numerous platforms, including social media, streaming services, gaming apps, and news websites, making it difficult to capture sustained engagement. The cost of producing diverse creative assets for different platforms increases operational complexity and budget requirements. The attention spans are decreasing with users scrolling quickly through feeds and skipping ads whenever possible. This behavior reduces the effectiveness of standard display and video ads, forcing brands to innovate with shorter, more impactful messages. The lack of unified measurement standards across platforms complicates the assessment of cross-channel performance. Advertisers struggle to attribute sales accurately when users interact with multiple touchpoints before converting. This ambiguity leads to inefficient budget allocation and difficulty in proving return on investment.

Brand Safety and Content Adjacency Risks

The brand safety concerns and the risk of ads appearing alongside inappropriate or harmful content are also contributing to the decline in the growth of the United States online advertising market. Advertisers are increasingly vigilant about protecting their reputation by ensuring their messages do not appear next to hate speech misinformation or violent material. The incidents of ads running alongside controversial content can cause significant reputational damage and consumer backlash. The open nature of programmatic advertising makes it difficult to control every placement, especially when dealing with long tail publishers and user-generated content platforms. These measures can limit reach and increase costs as premium inventory becomes more competitive. Social media platforms face particular scrutiny regarding the moderation of content, with advertisers pausing spending during periods of heightened controversy. Several major brands have temporarily halted advertising on major social networks due to concerns over content moderation practices. The evolving definition of brand safety also includes considerations of environmental, social, and governance issues requiring advertisers to align with broader ethical standards. Automated tools for detecting unsafe content are improving, but are not foolproof, leading to occasional lapses.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.51% |

| Segments Covered | By Type, Platform, Pricing Model, Industry, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Google, Meta Platforms, Amazon Advertising, Microsoft Advertising, Adobe, LinkedIn, X Corp., Dentsu, Publicis Groupe, GroupM, The Interpublic Group of Companies (IPG), Hulu, BuzzFeed, WebFX, Outbrain |

SEGMENTAL ANALYSIS

By Type Insights

The video advertising segment was the largest by holding 46.4% of the United States online advertising market share in 2025 due to its superior ability to capture consumer attention and convey complex messages effectively. Consumers increasingly prefer visual storytelling over static formats, with data from HubSpot indicating that 54% of consumers want to see more video content from brands they support. This preference drives advertisers to allocate larger portions of their budgets to video campaigns across social media streaming platforms and websites. The rise of short-form video has further accelerated this trend, with TikTok and Instagram Reels becoming primary channels for brand discovery. Video formats allow for immersive experiences such as 360-degree views and interactive elements that enhance user participation. This cognitive advantage makes video an indispensable tool for marketers seeking to build strong brand associations. The proliferation of high-speed internet and smartphone cameras has lowered production barriers, enabling even small businesses to create professional-quality video ads.

The native advertising segment is likely to grow at an anticipated to witness a CAGR of 18.5% from 2026 to 2034, with the need to combat ad fatigue and banner blindness among consumers who actively ignore traditional display ads. The seamless integration of native ads into editorial content or social feeds makes them less intrusive and more acceptable to users. Brands are increasingly adopting native formats to build trust and credibility, as these ads often appear alongside reputable journalism or influencer content. The rise of content marketing has further fueled this trend, with companies producing high-quality articles and videos that serve as native advertisements. The strategic shift allows brands to provide value to consumers rather than interrupting their experience. The flexibility of native advertising enables customization for different platforms, from news sites to social networks.

By Platform Insights

The mobile devices segment was the largest by holding a dominant share of the United States online advertising market in 2025 due to the ubiquitous presence of smartphones and the constant connectivity they provide. The widespread adoption ensures that advertisers can reach consumers anytime and anywhere by maximizing exposure opportunities. Mobile users spend an average of four hours per day on their devices, creating substantial inventory for mobile ads. The convenience of mobile access drives high engagement rates, particularly for social media and messaging apps where users frequently interact with content. Location-based services enable hyper-local targeting, allowing advertisers to deliver relevant offers based on a user's physical proximity to a store or event. The integration of mobile wallets and one-click payment options facilitates immediate conversions, shortening the purchase journey. This seamless experience encourages impulse buys and increases the effectiveness of mobile campaigns. The rise of fifth-generation networks further enhances mobile advertising by supporting rich media formats such as augmented reality and high-definition video. These immersive experiences capture attention and drive deeper engagement.

The connected TV and smart devices segment is projected to witness the fastest CAGR of 15.2% from 2026 to 2034, with the mass migration of viewers from traditional cable television to streaming services accessed via smart TVs and connected devices. Smart TVs are now present in over 80% of US households, providing a big screen experience that combines the impact of television with the precision of digital advertising. This shift creates new opportunities for advertisers to reach cord-cutters, who are no longer accessible through traditional linear TV. Connected TV ads offer the benefit of large screen visibility while allowing for targeted delivery and measurable outcomes. As per eMarketer, connected TV ad spending is rising rapidly as brands recognize the value of this hybrid medium. The ability to target specific demographics and interests on streaming platforms enhances ad relevance and effectiveness. Unlike traditional TV, connected TV allows for frequency capping and sequential messaging, improving the user experience and reducing ad fatigue.

By Pricing Model Insights

The cost per Mille pricing model segment accounted in holding 46.3% of the United States online advertising market share in 2025 due to its widespread adoption for brand awareness campaigns and display advertising. Cost Per Mille charges advertisers for every thousand impressions delivered, providing a predictable cost structure for reaching large audiences. As per the Interactive Advertising Bureau, display advertising, which primarily uses Cost Per Mille pricing, accounts for a significant portion of digital ad spend. This model is preferred by brands seeking to maximize visibility and recall rather than immediate clicks or conversions. The simplicity of Cost Per Mille makes it easy for advertisers to budget and forecast campaign costs. Programmatic platforms heavily utilize Cost Per Mille bidding, allowing for automated and efficient purchasing of ad space. As per OpenX, the majority of programmatic display transactions are executed on a Cost Per Mille basis. This standardization ensures liquidity in the ad exchange market, enabling seamless trading between buyers and sellers. The model is particularly effective for video and rich media ads where engagement is measured by views rather than clicks.

The Cost Per Click pricing model segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2034, with the increasing demand for performance-based marketing, where advertisers pay only for actual user engagement. The Cost Per Click models offer higher accountability and return on investment compared to impression-based models by appealing to budget-conscious marketers. Search engine advertising predominantly uses Cost Per Click, and the continued growth of search ad spend fuels this segment. According to Google, search ads drive significant traffic and conversions for businesses by making Cost Per Click the preferred model for direct response campaigns. The ability to track clicks and attribute them to specific keywords allows for precise optimization and budget allocation. Data-driven decision-making is becoming central to digital marketing strategies, and Cost Per Click provides the necessary granular data. Small and medium-sized enterprises favor Cost Per Click because it lowers the barrier to entry by minimizing risk. Advertisers can start with small budgets and scale up based on performance. The rise of social media advertising platforms that offer Cost Per Click options also contributes to growth.

By Industry Insights

The Retail and Consumer Goods industry segment held a significant share of the United States online advertising market in 2025 due to the high volume of e-commerce transactions and widespread digital adoption. As per the United States Census Bureau, e-commerce sales reached 1.1 trillion dollars in 2023, driving substantial demand for online advertising to attract customers. Retailers rely heavily on digital channels to showcase products, offer promotions, and drive sales. The competitive nature of the retail sector necessitates continuous advertising to maintain market share and brand visibility. The ability to target specific consumer segments based on browsing history and purchase behavior enhances the effectiveness of retail ads. As per Amazon Ads, sponsored product listings are a key driver of sales for third-party sellers, contributing to the industry's ad spend. Social commerce trends further boost advertising demand, with platforms like Instagram and Pinterest enabling direct purchases from ads. The social commerce sales are growing rapidly by encouraging retailers to invest in social media advertising. The seasonal nature of retail, with peaks during holidays and sales events, creates spikes in ad spending.

The healthcare industry segment is expected to grow at an anticipated CAGR of 14.5% from 2026 to 2034, with the rapid adoption of digital health services and the expansion of telemedicine. The telehealth visits have increased significantly, creating a need for online advertising to promote these services. Healthcare providers and pharmaceutical companies are investing in digital channels to reach patients and healthcare professionals. The aging population and increasing prevalence of chronic diseases drive demand for healthcare information and services. As per the Centers for Disease Control and Prevention, six in ten adults in the United States have a chronic disease, creating a large target audience for health-related ads. Online advertising allows healthcare brands to educate consumers and promote preventive care measures. The shift toward patient-centric care encourages providers to use digital marketing to engage with patients and build trust. The personalized health messaging improves patient outcomes and satisfaction. The regulatory environment is also evolving to allow more flexible advertising practices for healthcare products.

COMPETITIVE OVERVIEW

The competition in the United States online advertising market is intense and characterized by the dominance of a few large technology platforms alongside a diverse array of specialized providers. Major players such as Alphabet, Meta, and Amazon leverage their vast user bases and proprietary data to offer unparalleled targeting capabilities. These walled gardens attract significant advertiser spending due to their ability to deliver measurable results and high engagement. However, the rise of retail media networks and connected television platforms is fragmenting the landscape and creating new competitive dynamics. Smaller tech firms and independent publishers are forming alliances to offer alternative inventory sources that emphasize transparency and brand safety. The shift towards privacy-centric advertising has intensified the race for first-party data and advanced identity solutions. Companies are differentiating themselves through innovative ad formats such as augmented reality and shoppable video that enhance user experience. Artificial intelligence plays a critical role in optimizing campaigns and reducing manual effort, giving technologically advanced firms a distinct edge.

KEY MARKET PLAYERS

A few major players of the U.S online advertising market include

- Meta Platforms

- Amazon Advertising

- Microsoft Advertising

- Adobe

- X Corp.

- Dentsu

- Publicis Groupe

- GroupM

- The Interpublic Group of Companies (IPG)

- Hulu

- BuzzFeed

- WebFX

- Outbrain

Leading Players in the US Online Advertising Market

- Alphabet Inc dominates the United States online advertising market through its extensive ecosystem comprising Google Search, YouTube, and the Google Display Network. The company leverages advanced artificial intelligence to deliver highly relevant ads across multiple platforms, ensuring maximum engagement for advertisers. Recent actions include the integration of generative AI tools into its advertising suite, which allows brands to create dynamic creatives and optimize campaigns automatically. Alphabet continues to enhance its privacy sandbox initiatives to address data protection concerns while maintaining effective targeting capabilities. The expansion of connected television advertising on YouTube further strengthens its position by capturing shifting viewer habits. These technological advancements enable Alphabet to maintain its leadership role by offering superior return on investment and scalable solutions for businesses of all sizes seeking to reach diverse audiences effectively.

- Meta Platforms Inc remains a pivotal force in the United States online advertising landscape by connecting billions of users through Facebook, Instagram, and WhatsApp. The company focuses on delivering personalized ad experiences driven by sophisticated social graph data and user behavior insights. Recent strategies involve the development of Advantage Plus shopping campaigns, which utilize automation to improve performance for e-commerce clients. Meta has also invested significantly in artificial intelligence to enhance ad relevance and detection of policy violations. The introduction of new formats, such as reel ads, caters to the growing preference for short-form video content. These innovations help advertisers achieve better conversion rates while navigating evolving privacy regulations. The continuous refinement of its algorithmic targeting ensures that Meta remains a preferred platform for brands seeking high engagement and precise audience reach in a competitive digital environment.

- Amazon.com Inc has emerged as a major player in the United States online advertising market by leveraging its vast e-commerce platform and rich consumer purchase data. The company offers sponsored product display and video ads that appear directly within its shopping ecosystem, where purchase intent is highest. Recent actions include the expansion of Amazon Ads into streaming television through Prime Video and Freevee, providing new opportunities for brand storytelling. Amazon continues to enhance its demand-side platform, allowing advertisers to buy inventory across the open web using its proprietary data. The integration of artificial intelligence helps optimize bidding strategies and creative personalization for better performance. This closed-loop system attracts brands seeking measurable results and efficient spend allocation. The growth of its advertising business demonstrates Amazon's ability to monetize its extensive user base and logistics network effectively while offering unique value propositions to marketers.

Top Strategies Used by Key Market Participants

- Key players in the United States online advertising market primarily focus on integrating artificial intelligence to enhance targeting precision and campaign automation. Companies invest heavily in machine learning algorithms that optimize bidding strategies and creative generation in real time. The adoption of first-party data strategies is crucial as third-party cookies become obsolete due to privacy regulations. Brands are building direct relationships with consumers to gather valuable insights for personalized advertising. Expansion into connected television and retail media networks allows providers to capture attention in high-engagement environments. Strategic partnerships with publishers and technology vendors help create walled gardens that offer secure and measurable ad inventory. Emphasis on transparency and brand safety tools builds trust with advertisers concerned about ad fraud. Diversification of ad formats, including short-form video and interactive experiences, drives higher engagement rates. Continuous innovation in measurement and attribution models ensures accurate performance tracking across fragmented channels. These strategies enable market leaders to maintain competitiveness and deliver superior value to clients.

MARKET SEGMENTATION

This research report on the US online advertising market has been segmented and sub-segmented based on type, platform, pricing model, industry & region.

By Type

- Video Advertising

- Native Advertising

- Display Advertising

- Full-Screen Interstitials

- Others

By Platform

- Mobiles

- Laptop

- Desktops & Tablets

- Others

By Pricing Model

- Flat Rate Pricing Model

- Cost Per Mille Pricing Model

- Cost Per Click Pricing Model

By Industry

- Media & Entertainment

- BFSI

- Education

- Retail & Consumer Goods

- IT & Telecom

- Healthcare

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What are the major drivers of the U.S. online advertising market?

Growing smartphone adoption, rising social media usage, increasing e-commerce activities, and advancements in digital marketing technologies are major growth drivers.

2. Which segment dominates the U.S. online advertising market?

Search advertising holds a significant share of the market due to the high popularity of search engines and targeted advertising capabilities.

3. What is the expected CAGR of the U.S. online advertising market?

The market is projected to witness strong CAGR growth during the forecast period driven by digital transformation and data-driven marketing strategies.

4. How is social media influencing the online advertising market in the U.S.?

Social media platforms enable businesses to reach targeted audiences, improve customer engagement, and enhance brand visibility through personalized advertisements.

5. What role does artificial intelligence play in online advertising?

Artificial intelligence helps optimize ad targeting, automate bidding strategies, analyze consumer behavior, and improve campaign performance.

6. How is mobile advertising impacting the U.S. online advertising market?

Mobile advertising is expanding rapidly due to increasing smartphone penetration and growing consumer preference for mobile applications and mobile browsing.

7. What are the major challenges faced by the U.S. online advertising market?

Ad fraud, data privacy concerns, increasing use of ad blockers, and stringent regulations are major challenges for market growth.

8. What are the emerging trends in the U.S. online advertising market?

Video advertising, influencer marketing, AI-driven advertising, connected TV advertising, and voice search advertising are major emerging trends.

9. Who are the key players in the U.S. online advertising market?

Major market players include Google, Meta Platforms, Amazon Advertising, Microsoft Advertising, and Adobe.

10. What future opportunities exist in the U.S. online advertising market?

Growth opportunities are expected from AI-based personalization, immersive advertising technologies, expansion of digital video platforms, and increasing internet penetration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com