U.S. Outdoor Furniture Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Material, End User, Price Range, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Outdoor Furniture Market Report Summary

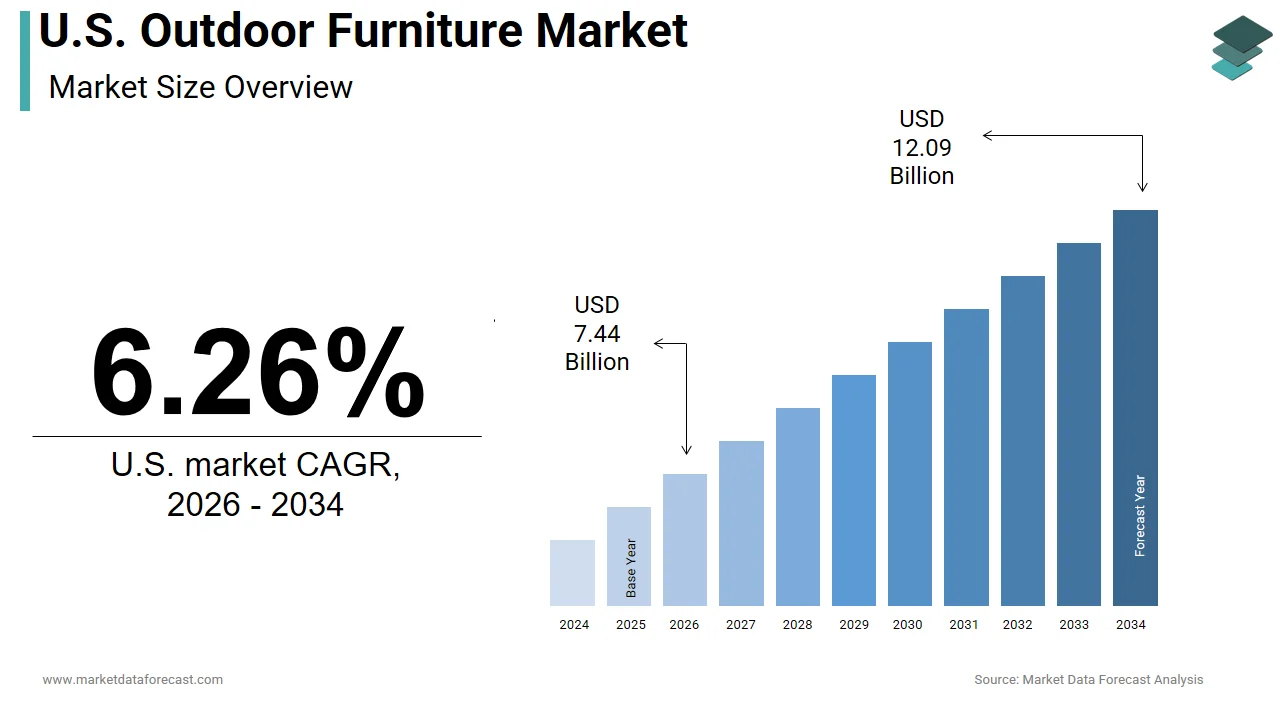

The U.S. outdoor furniture market was valued at USD 7 billion in 2025, is estimated to reach USD 7.44 billion in 2026, and is projected to reach USD 12.09 billion by 2034, growing at a CAGR of 6.26% from 2026 to 2034. Market growth is driven by increasing consumer spending on home improvement, rising demand for outdoor living spaces, and growing popularity of backyard leisure and entertainment activities. Consumers are increasingly investing in aesthetically appealing and durable outdoor furniture to enhance patios, gardens, balconies, and outdoor dining areas. Additionally, rising disposable incomes, growth in premium furniture demand, and expansion of e-commerce retail channels are supporting market growth across the United States.

Key Market Trends

- Rising demand for premium and durable outdoor furniture.

- Increasing consumer focus on home improvement and outdoor living spaces.

- Growth in residential patio and backyard renovation projects.

- Expansion of online furniture retail and direct-to-consumer sales channels.

- Increasing popularity of weather-resistant and sustainable furniture materials.

Segmental Insights

- Based on product type, the chairs and individual seating segment dominated the United States outdoor furniture market in 2025, driven by strong consumer demand for flexible and comfortable seating solutions.

- Based on end user, the residential segment held the leading share with 55.1% in 2025, supported by increasing spending on home décor and outdoor entertainment areas.

- Based on price range, the premium segment is projected to witness the fastest CAGR of 8.5% during the forecast period, driven by rising disposable incomes and growing preference for high-quality long-term furniture investments.

- Based on distribution channel, the retail and business-to-consumer segment led the market by accounting for 43.5% share in 2025, supported by strong retail presence and growing e-commerce penetration.

Country-Level Insights

The United States dominated the North American outdoor furniture market by capturing 85.7% share in 2025, supported by strong consumer spending, large residential housing infrastructure, and increasing demand for outdoor leisure products.

Competitive Landscape

The U.S. outdoor furniture market is highly competitive, with companies focusing on premium product offerings, sustainable materials, and omnichannel retail expansion. Product innovation, customization options, and investments in outdoor lifestyle branding are shaping the competitive landscape.

Prominent companies operating in the U.S. outdoor furniture market include Ashley Furniture Industries Inc., Brown Jordan Inc., Tropitone Furniture Company Inc., The Home Depot, Lowe's Companies Inc., Telescope Casual Furniture, and Williams-Sonoma Inc.

U.S. Outdoor Furniture Market Size

The U.S. outdoor furniture market was valued at USD 7 billion in 2025, is estimated to reach USD 7.44 billion in 2026, and is projected to reach USD 12.09 billion by 2034, growing at a CAGR of 6.26% from 2026 to 2034.

Outdoor furniture, or garden furniture, refers to specialized furnishings designed for exterior environments like patios, gardens, balconies, and decks. This sector includes seating dining sets, loungers, umbrellas, and accessories crafted from weather-resistant materials such as teak, aluminum wicker, and synthetic rattan. The definition of this market has evolved from purely functional items to extensions of indoor living spaces reflecting a desire for seamless indoor-outdoor lifestyles. The National Association of Home Builders (NAHB) reports that roughly 62% of new single-family homes are constructed with patios, demonstrating a steady, structural foundation for long-term outdoor furnishing and exterior design demand. According to the U.S. Census Bureau, there are more than 146 million housing units in the United States, with a significant portion of these properties featuring private outdoor residential spaces. Consumer behavior indicates a strong preference for high-quality, durable pieces that withstand varied climatic conditions. Also, consumer sentiment data from the International Casual Furnishings Association shows that nearly 75% of homeowners prioritize upgrading or maintaining their outdoor living spaces for relaxation and entertainment. The demographic trend towards suburban living has further amplified this demand as families seek to maximize their private outdoor environments. The market is characterized by seasonal fluctuations yet shows resilience due to the increasing perception of backyards as essential wellness and social hubs. Regulatory standards for material safety and durability influence product development, ensuring longevity and consumer protection. As urbanization continues, the integration of compact and modular outdoor solutions gains traction among apartment dwellers. This evolution underscores the market's adaptation to changing living arrangements and lifestyle priorities.

MARKET DRIVERS

Expansion of Home Improvement and Renovation Activities

The robust expansion of home improvement and renovation activities is a key factor propelling the growth of the United States outdoor furniture market. This encourages homeowners to invest in exterior aesthetics and functionality. Following the pandemic-induced surge in home-centric spending, many Americans continue to prioritize upgrades that enhance livability and property value. According to the Joint Center for Housing Studies of Harvard University (JCHS), annual homeowner spending on improvements and repairs was projected to reach an annualized rate of $485 billion by late 2025, with forecasts suggesting continued growth to over $520 billion in early 2026. Outdoor renovations often include the installation of decks, pergolas, and landscaping, which naturally necessitate the purchase of complementary furniture. Homeowners view outdoor areas as additional rooms requiring furnished setups for dining, lounging, and entertaining. The rise of do-it-yourself projects has also contributed to this trend, with individuals seeking stylish yet affordable furniture options to complete their renovations. Retailers report increased sales of outdoor sets during spring and summer renovation seasons. The availability of financing options for home improvements further facilitates larger purchases, including premium outdoor furniture. This driver ensures consistent demand as homeowners seek to create inviting and functional exterior environments that reflect their personal style and comfort preferences.

Growing Emphasis on Outdoor Living and Entertainment

The growing emphasis on outdoor living and entertainment is also an accelerator of the United States outdoor furniture market. This transforms backyards into central hubs for social interaction and leisure. Consumers increasingly view their outdoor spaces as extensions of their indoor living areas, leading to higher expenditure on comfortable and stylish furnishings. Recent surveys by the American Institute of Architects (AIA) continue to show elevated demand for outdoor living features, sustaining the trend established in 2021 when 70% of architects first reported a massive surge in client requests for exterior functional spaces. This trend is fueled by the desire for al fresco dining, barbecues, and casual gatherings, which require adequate seating and dining solutions. The popularity of outdoor kitchens, fire pits, and heating elements has further extended the usability of these spaces into cooler months, driving year-round furniture sales. Social media platforms showcase curated outdoor setups inspiring consumers to upgrade their own spaces to match aspirational lifestyles. The shift towards health and wellness also encourages outdoor relaxation, prompting purchases of loungers and daybeds. Manufacturers respond by offering weather-resistant fabrics and ergonomic designs that cater to prolonged use. This cultural shift towards embracing outdoor environments ensures sustained growth in the furniture sector as consumers prioritize experiences and comfort in their private sanctuaries.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

Volatility in raw material prices and supply chain disruptions is impeding the growth of the United States outdoor furniture market. This increases production costs and causes inventory inconsistencies. Key materials such as aluminum, steel, teak, and synthetic wicker are subject to global price fluctuations influenced by trade policies and geopolitical tensions. According to the Producer Price Index (PPI), manufacturing input costs faced broad-based inflationary pressures and tariff-driven volatility in 2025, forcing furniture manufacturers to navigate rising material expenses to protect production margins. These cost increases are often passed on to consumers, resulting in higher retail prices that may dampen demand, particularly among budget-conscious buyers. Supply chain bottlenecks exacerbated by port congestion and logistics challenges have led to delayed shipments and stockouts. The reliance on imported components from Asia makes the sector vulnerable to international trade disruptions and tariff impositions. Retailers struggle to maintain consistent pricing strategies amidst fluctuating input costs, leading to margin compression. Small and medium-sized enterprises face greater challenges in absorbing these costs compared to larger corporations. The unpredictability of material availability forces companies to hold higher inventory levels, tying up capital. This restraint limits the ability of manufacturers to innovate and expand product lines due to financial constraints. The ongoing instability in global supply networks requires strategic adaptations to mitigate risks.

Seasonal Demand Fluctuations and Weather Dependence

Seasonal demand fluctuations and weather dependence are also constraints on the United States outdoor furniture market. This creates uneven sales cycles and inventory management challenges. The majority of outdoor furniture sales occur during the spring and summer months, leading to intense competition and promotional pressure during these periods. This concentration of demand forces retailers to manage complex inventory levels to avoid overstocking or stockouts. Unpredictable weather patterns, such as prolonged rains or early winters, can significantly impact consumer purchasing behavior. The National Oceanic and Atmospheric Administration (NOAA) tracked 23 billion-dollar extreme weather events across the U.S. in 2025, highlighting an unpredictable climate landscape that often temporarily disrupts local retail traffic and outdoor consumer activities. Retailers face the risk of unsold inventory at the end of the season, which often requires deep discounting to clear storage space. The off-season period sees minimal sales, leading to cash flow challenges for businesses reliant on seasonal revenue. Manufacturers must balance production schedules to align with short selling windows, which can lead to inefficiencies. The dependence on favorable weather conditions makes revenue forecasting difficult for industry participants. This restraint necessitates diversified product offerings and marketing strategies to extend the selling season and mitigate seasonal risks.

MARKET OPPORTUNITIES

Integration of Smart Technology and Sustainable Materials

The integration of smart technology and sustainable materials offers a significant opportunity for the United States outdoor furniture market. This appeals to tech-savvy and environmentally conscious consumers. Innovations such as solar-powered lighting, heated seating, and app-controlled features enhance the functionality and appeal of outdoor furnishings. According to projections from the Consumer Technology Association (CTA) and broader market research, the smart home outdoor device market is sustaining a strong 8% to 11% annual growth rate, driven by steady consumer demand for automated exterior lighting and security systems. Consumers are increasingly interested in furniture that offers convenience and energy efficiency, aligning with broader smart home trends. Sustainability is another key driver, with buyers preferring products made from recycled plastics, reclaimed wood, and eco-friendly fabrics. Manufacturers can capitalize on this opportunity by obtaining certifications such as Forest Stewardship Council approval, which builds trust and credibility. The use of durable, low-maintenance materials reduces long-term replacement costs, attracting value-oriented shoppers. Collaborations with technology firms can accelerate the development of integrated outdoor solutions. Retailers can highlight these features in marketing campaigns to differentiate their offerings. The combination of innovation and sustainability creates a unique value proposition that resonates with modern lifestyles. This opportunity allows companies to command premium prices and build loyal customer bases committed to ethical consumption.

Growth in Multi-Functional and Space-Saving Designs

The growing demand for multi-functional and space-saving outdoor furniture creates a pathway for the expansion of the United States market. This addresses the needs of urban dwellers and those with limited outdoor space. As housing trends shift towards smaller yards and balconies, consumers seek versatile pieces that maximize utility without compromising style. The National Association of Home Builders (NAHB), tracking a historical downward trend in residential lot sizes, emphasizes a shifting market where smaller property footprints are steadily driving consumer demand for space-efficient and multi-functional furniture. Foldable tables, stackable chairs, and modular sectional sets allow users to adapt their spaces for different activities such as dining, lounging, or entertaining. Manufacturers can innovate by designing lightweight, durable pieces that are easy to store and rearrange. The rise of vertical gardening and balcony ecosystems also creates opportunities for integrated furniture planters. Retailers can curate collections specifically for small spaces, appealing to urban demographics. Marketing campaigns emphasizing versatility and space optimization resonate with city residents. The ability to transform limited areas into functional living spaces enhances the appeal of these products. This opportunity supports market expansion in densely populated regions where space is at a premium. Companies can capture a growing segment of urban consumers by focusing on adaptability. These consumers are seeking practical yet stylish outdoor solutions.

MARKET CHALLENGES

Impact of Climate Change and Extreme Weather Conditions

Climate change and extreme weather conditions are negatively impacting the United States outdoor furniture market. This accelerates product degradation and alters consumer usage patterns. Increasing frequency of hurricanes, heatwaves, and heavy rainfall exposes outdoor furnishings to harsher environmental stressors, reducing their lifespan. According to historical data tracked by Climate Central, the number of billion-dollar weather and climate disasters in the U.S. reached 23 separate events in 2025, marking the third-highest annual count on record and highlighting the intense threat to outdoor residential and commercial infrastructure. These conditions require manufacturers to develop more resilient materials and coatings, which increase production costs. Consumers face higher replacement frequencies due to weather-related damage, leading to potential dissatisfaction with product durability. The unpredictability of the weather makes it difficult for consumers to plan outdoor investments confidently. Retailers must educate customers on proper maintenance and storage practices to mitigate damage. The need for weather-resistant covers and storage solutions adds to the overall cost of ownership. Manufacturers face pressure to balance aesthetic appeal with rugged durability. This challenge necessitates continuous research and development in material science. The industry must adapt to changing climate realities to ensure product longevity and customer satisfaction. Failure to address these issues may lead to decreased consumer confidence and market contraction.

Intense Competition and Price Sensitivity

Intense competition and price sensitivity hold back the United States outdoor furniture market. This compresses margins and forces continuous innovation. The market is saturated with numerous players ranging from high-end luxury brands to mass market retailers, creating a highly competitive landscape. This saturation leads to price wars, particularly during peak seasons, as retailers attempt to capture market share. The Bureau of Labor Statistics shows that persistent headline inflation hovered near 3% throughout 2025, compounded by rising import tariffs on goods like household furnishings, which private market research notes has dramatically heightened consumer price sensitivity. Buyers often compare prices across multiple channels, seeking the best deals, which undermines brand loyalty. Private label offerings from large retailers further intensify competition by providing lower-cost alternatives. Manufacturers struggle to differentiate their products in a crowded market, leading to increased marketing expenditures. The pressure to reduce costs may compromise quality, affecting long-term brand reputation. Small businesses face difficulties in competing with the economies of scale enjoyed by larger corporations. This challenge requires strategic positioning and value addition to justify premium pricing. Companies must focus on unique design elements and superior customer service to stand out. The constant need for innovation and cost management strains operational resources. Navigating this competitive environment demands agility and strategic foresight.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material, End User, Price Range, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Ashley Furniture Industries Inc., Brown Jordan Inc., Tropitone Furniture Company Inc, Home Depot Product Authority LLC, Lowe’s Companies Inc., Telescope Casual Furniture, Williams-Sonoma Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The chairs and individual seating segment held the majority share of the United States outdoor furniture market in 2025. This supremacy of the segment was credited to its versatility essential nature and lower entry price point compared to larger sets. Consumers often begin outfitting outdoor spaces with individual chairs before investing in complete dining or lounge sets, making this category the primary entry point for market participation. According to market research supported by the International Casual Furnishings Association, lounge seating and dining chairs represent the largest overall product category in the outdoor sector, reflecting their foundational importance in residential patio designs. The dominance is further supported by the diverse range of styles available, including Adirondack chairs, rocking chairs, and accent seats that cater to varied aesthetic preferences. The ability to mix and match different chair styles allows for personalized decor, which appeals to modern consumers seeking unique looks. Replacement cycles for individual chairs are shorter than for large sets due to frequent use and exposure to elements, driving repeat purchases. Retailers report higher turnover rates for chairs, particularly during peak seasons, as customers replace worn items or add seating for guests. The compact size of chairs also facilitates easier shipping and storage, reducing logistical costs for both manufacturers and consumers. This accessibility and functional necessity secure the leading status of the chair segment. Additionally, the rise of portable and foldable chair designs appeals to urban dwellers with limited space, further boosting sales volume.

But the loungers and daybeds segment is predicted to witness the highest CAGR of 9.2% between 2026 and 2034. This rapid expansion is fueled by the increasing emphasis on wellness, relaxation, and the transformation of backyards into personal retreats. According to research from the Global Wellness Institute, the Wellness Real Estate sector has emerged as one of the fastest-growing segments in the wellness economy, heavily driven by high consumer demand for dedicated home relaxation and residential spa environments. Consumers are investing in high comfort outdoor loungers and daybeds to create sanctuary-like environments for reading, napping, and meditation. The influence of resort-style living has popularized daybeds as statement pieces that combine functionality with luxury aesthetics. Social media trends showcasing serene outdoor setups have amplified the desire for these premium items among Millennials and Gen Z. Manufacturers are introducing weather-resistant cushions and adjustable features to enhance comfort and durability. The integration of loungers with other wellness elements, such as fire pits and water features, creates cohesive outdoor experiences. Retailers highlight these products in lifestyle marketing campaigns, emphasizing mental health benefits. The higher price point of loungers and daybeds contributes significantly to revenue growth despite lower unit volumes compared to chairs. This segment benefits from the ongoing trend of treating outdoor spaces as extensions of indoor living rooms where comfort is paramount.

By End User Insights

The residential end-user segment dominated the United States outdoor furniture market and accounted for a 55.1% share in 2025. This dominance of the segment was driven by the widespread ownership of homes with private outdoor spaces and the personalization of living environments. Homeowners invest heavily in outdoor furnishings to enhance comfort, aesthetics, and property value, driving substantial volume sales. "According to the U.S. Census Bureau, there are more than 146 million housing units across the United States, providing an expansive, structurally established foundation for residential outdoor lifestyle products. The emotional connection to home and the desire for private leisure spaces motivate residents to purchase high-quality, durable furniture. The rise of remote work has further intensified this trend as individuals seek pleasant outdoor environments for breaks and informal meetings. Retailers cater to this segment with diverse styles ranging from traditional to modern, ensuring broad appeal. The replacement cycle for residential furniture is influenced by personal taste changes and wear, leading to consistent demand. DIY home improvement projects often include furniture upgrades, contributing to steady sales. The residential segment benefits from seasonal promotions and financing options that make large purchases more accessible. This dominant position is reinforced by the cultural importance of backyard gatherings and family time in American life.

By Price Range Insights

The premium price range segment is estimated to register the fastest CAGR of 8.5% during the forecast period due to the increasing disposable income among affluent consumers and the tendency to view outdoor furniture as long-term investments rather than disposable items. According to Federal Reserve wealth distribution metrics, the collective net worth of the top 10% of U.S. households sustained a strong upward trajectory throughout 2025, consistently fueling robust capital reserves for discretionary luxury purchases. Consumers in this segment prioritize high-quality materials such as teak, stainless steel, and performance fabrics that offer durability and superior aesthetics. The demand for custom-made and designer pieces has risen as buyers seek unique items that reflect their personal style. Brands focusing on sustainability and ethical sourcing attract conscientious, wealthy shoppers willing to pay a premium. The integration of smart technology and advanced comfort features further justifies higher price points. Retailers report increased sales of high-end collections despite economic uncertainties, indicating resilience in this segment. The perception of outdoor spaces as valuable extensions of the home drives willingness to invest in lasting quality. This trend ensures continued rapid growth for premium offerings.

By Distribution Channel Insights

In 2025, the retail and business-to-consumer channels segment remained in the lead by capturing a 43.5% share of the United States outdoor furniture market. This leading position of the segment was attributed to consumer preference for physical inspection, immediate availability, and wide selection. Brick and mortar stores, including home improvement centers, furniture specialty shops, and department stores, allow shoppers to test comfort and assess quality before purchasing. According to broader consumer tracking data, brick-and-mortar retail remains the dominant channel for outdoor furniture sales, commanding the majority of market share as brick-and-mortar locations continue to anchor high-value seasonal purchases. The dominance is driven by the tactile nature of furniture buying, where consumers value the ability to sit on chairs and examine fabric textures. Major retailers like Home Depot, Lowe’s, and Wayfair offer extensive showrooms and online catalogs that cater to diverse tastes. Promotional events and seasonal discounts in physical stores drive foot traffic and impulse buys. The immediate gratification of taking home products appeals to consumers undertaking urgent renovation projects. Trusted retail brands assure warranty and return policies, which influence buying decisions. The integration of online research with in-store purchases creates a seamless omnichannel experience. This combination of convenience, trust, and sensory evaluation ensures that retail and B2C channels maintain their leading status.

The online sales channel segment is anticipated to witness the fastest CAGR of 11.5% between 2026 and 2034, owing to the increasing comfort of consumers with e-commerce platforms, the convenience of home delivery, and the ability to compare prices and reviews easily. The driving force behind this trend is the improved logistics infrastructure that enables safe and timely delivery of bulky items. Research notes that while competitive pricing and wide digital variety have made online channels critical for product research, the modern furniture shopper heavily favors an omnichannel approach, expecting integrated experiences that bridge digital browsing with physical showroom confirmation. Digital tools such as augmented reality allow users to visualize how furniture will look in their spaces, reducing purchase hesitation. Direct-to-consumer brands leverage social media marketing to reach niche audiences effectively. Subscription services and easy return policies enhance customer confidence in online transactions. The ability to access global brands and unique designs not available locally attracts discerning shoppers. Younger demographics, particularly Millennials and Gen Z, favor digital channels for their seamless integration with mobile devices. This combination of convenience selection and technology ensures that online sales continue to grow at the fastest rate.

COUNTRY ANALYSIS

U.S. Outdoor Furniture Market Analysis

The United States was the top performer in the North American outdoor furniture market and secured a 85.7% share in 2025. This dominant position was supported by the country’s vast housing stock, high disposable income, and strong cultural emphasis on outdoor living and entertainment. The market status in the United States is characterized by a mature yet innovative landscape where premium and technologically advanced products are gaining traction. With the U.S. Census Bureau estimating the total housing inventory at over 146 million units, market research indicates that the number of homes featuring private outdoor spaces comfortably exceeds 100 million, establishing a massive consumer base for exterior furnishings. The driving factors behind this leadership include the favorable climate in many regions, such as California, Florida, and Texas, which allows for year-round outdoor activity. Historical climate data from the National Oceanic and Atmospheric Administration (NOAA) confirms extended periods of moderate seasonal temperatures across key regions, fundamentally supporting longer, year-round usage of outdoor residential spaces and furniture. The presence of major global furniture manufacturers and retailers headquartered in the US fosters continuous product innovation and marketing excellence. Consumer education campaigns by industry associations promote the benefits of outdoor living, driving consistent demand. The aging population retains active lifestyles requiring comfortable and durable outdoor solutions. Additionally, the influence of social media and home improvement television shows emphasizes the value of well-furnished patios, boosting sales. The robust retail infrastructure, including widespread home improvement stores, ensures easy product accessibility. These factors collectively ensure that the United States remains the central pillar of the outdoor furniture market in the region.

COMPETITIVE LANDSCAPE

The competition in the United States outdoor furniture market is intense and characterized by the presence of established manufacturers, specialized boutique brands, and large retail chains. Major players like Brown Jordan, Tropitone, and Telescope Casual dominate the premium and mid-range segments through strong brand recognition and quality assurance. These companies leverage their design expertise and manufacturing capabilities to offer differentiated products that appeal to discerning consumers. Private labels from big box retailers pose a significant threat by providing lower-cost alternatives that attract budget-conscious shoppers. The rise of direct-to-consumer brands has increased pressure on traditional manufacturers to innovate and improve customer experience. Competition is also driven by the need for sustainability, with companies vying to demonstrate environmental responsibility through certifications and transparent sourcing. Marketing expenditures remain high as brands compete for visibility in both physical and digital spaces. The market sees frequent product launches and seasonal promotions, which impact profit margins but drive volume. Small and niche players compete by offering unique designs and personalized services that appeal to specific segments. This dynamic environment requires continuous innovation and strategic agility to maintain market relevance and profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. outdoor furniture market include

- Ashley Furniture Industries Inc.

- Brown Jordan Inc.

- Tropitone Furniture Company Inc

- Home Depot Product Authority LLC

- Lowe’s Companies Inc.

- Telescope Casual Furniture

- Williams-Sonoma Inc.

TOP PLAYERS IN THE MARKET

- Brown Jordan International Inc maintains a prestigious position in the United States outdoor furniture market by offering high-end luxury collections that define modern exterior living. The company is renowned for its innovative designs and superior craftsmanship using materials such as aluminum, teak, and all-weather wicker. Recently, Brown Jordan has strengthened its market position by expanding its digital presence and enhancing direct-to-consumer sales channels. The brand actively collaborates with leading architects and designers to create bespoke solutions for upscale residential and commercial projects. Its commitment to sustainability is evident in the use of eco-friendly materials and responsible manufacturing practices. By focusing on exclusivity and quality, Brown Jordan appeals to affluent consumers seeking durable and stylish outdoor furnishings. The company continues to invest in product development, ensuring its collections remain at the forefront of design trends. These strategic initiatives reinforce its reputation as a leader in the luxury segment.

- Tropitone Furniture Company Inc contributes significantly to the United States outdoor furniture market through its extensive portfolio of durable and versatile seating and dining solutions. The company serves both residential and commercial sectors, including hospitality and multifamily housing projects. Recent actions include the introduction of new fabric technologies that offer enhanced stain resistance and UV protection. Tropitone has also expanded its distribution network by partnering with independent dealers across the country to increase market reach. The brand emphasizes customization, allowing clients to select from a wide range of frames, finishes, and cushions. This flexibility appeals to diverse consumer preferences and project requirements. Tropitone actively participates in industry trade shows to showcase innovations and build relationships with specifiers. Its focus on quality and customer service ensures long-term loyalty among contractors and homeowners. These efforts solidify its standing as a trusted provider of reliable outdoor furniture.

- Telescope Casual Furniture plays a vital role in the United States outdoor furniture market by specializing in high-quality sling and cushioned seating made in America. The company is known for its durable aluminum frames and vibrant fabric options that withstand harsh weather conditions. Recently, Telescope Casual has invested in modernizing its manufacturing facilities to improve efficiency and reduce environmental impact. The brand has launched new collections featuring contemporary designs that appeal to younger demographics while maintaining its classic appeal. Telescope Casual strengthens its market position by offering robust warranty programs that assure customers of product longevity. The company actively engages with retail partners to provide training and marketing support, ensuring consistent brand representation. Its commitment to domestic production resonates with consumers who prioritize American-made goods. These strategies enhance brand credibility and drive sustained growth in a competitive landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States outdoor furniture market employ diverse strategies to maintain competitiveness and drive growth in an evolving landscape. Product innovation is a primary focus, with companies introducing weather-resistant materials and ergonomic designs to enhance durability and comfort. Sustainability initiatives are increasingly important as firms adopt recycled materials and eco-friendly manufacturing processes to appeal to conscious consumers. Digital transformation plays a critical role for brands, enhancing e-commerce platforms and using augmented reality for virtual placement. Strategic partnerships with interior designers and architects help secure high-value commercial contracts. Expansion into direct-to-consumer channels allows manufacturers to capture higher margins and build direct customer relationships. Marketing campaigns often emphasize lifestyle benefits, connecting outdoor furniture with wellness and social interaction. These approaches collectively enable market participants to adapt to changing consumer preferences and maintain strong market positions.

MARKET SEGMENTATION

This research report on the U.S. outdoor furniture market has been segmented and sub-segmented into the following categories.

By Product Type

- Chairs

- Tables

- Seating Sets

- Loungers and Daybeds

By Material

- Wood

- Metal

By End User

- Residential

- Commercial

By Price Range

- Economy

- Mid-Range

- Premium

By Distribution Channel

- Retail / B2C Channels

- B2B Channel / Contractors

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. outdoor furniture market?

The U.S. outdoor furniture market includes patio sets, chairs, tables, loungers, and accessories designed for outdoor living spaces and leisure use.

How does the U.S. outdoor furniture market function?

The U.S. outdoor furniture market operates through manufacturers, retailers, and online stores selling durable products for patios, decks, and gardens.

What drives growth in the U.S. outdoor furniture market?

The U.S. outdoor furniture market grows from home renovation, outdoor entertaining, and rising demand for comfortable backyard spaces.

Which products lead the U.S. outdoor furniture market?

Patio chairs, dining sets, seating sets, loungers, and daybeds lead the U.S. outdoor furniture market because they fit most outdoor spaces.

What materials are popular in the U.S. outdoor furniture market?

Teak, aluminum, wicker, and weather-resistant resin are popular in the U.S. outdoor furniture market for durability and style.

How important are patio sets in the U.S. outdoor furniture market?

Patio sets are central to the U.S. outdoor furniture market because they create coordinated outdoor dining and relaxation areas.

How does e-commerce affect the U.S. outdoor furniture market?

E-commerce expands the U.S. outdoor furniture market by offering wider selection, price comparison, and home delivery convenience.

What trends shape the U.S. outdoor furniture market?

Modular designs, multifunctional pieces, and weatherproof materials define current trends in the U.S. outdoor furniture market.

What role does residential demand play in the U.S. outdoor furniture market?

Residential demand drives the U.S. outdoor furniture market as homeowners upgrade patios, balconies, and backyards for comfort and style.

How does hospitality influence the U.S. outdoor furniture market?

Hotels, resorts, and restaurants support the U.S. outdoor furniture market by investing in outdoor dining and lounge setups.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com