- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

U.S. Smart Home Market Report Summary

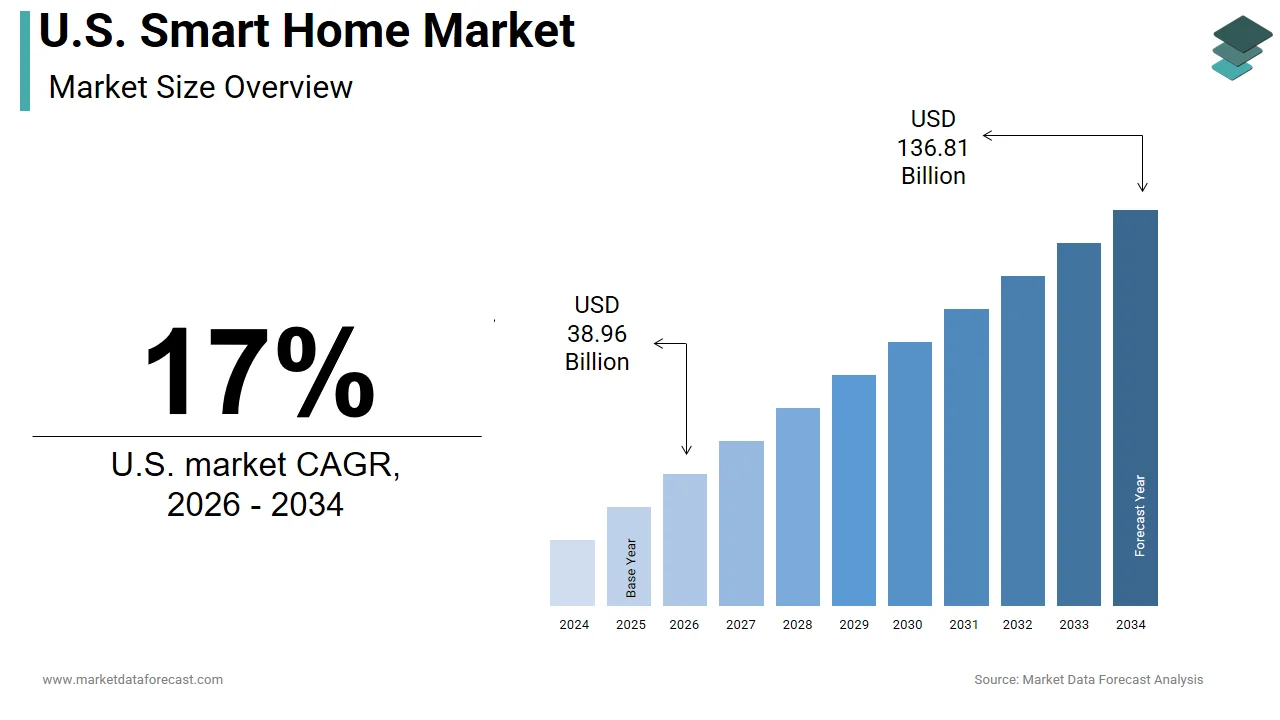

The U.S. smart home market was valued at USD 33.30 billion in 2025, is estimated to reach USD 38.96 billion in 2026, and is projected to reach USD 136.81 billion by 2034, growing at a CAGR of 17% from 2026 to 2034. Market growth is driven by increasing adoption of connected devices, rising consumer demand for home automation, and advancements in IoT, AI, and voice assistant technologies. The growing focus on energy efficiency, security, and convenience is accelerating the integration of smart devices across households. Additionally, strong ecosystem development by major tech companies and the expansion of smart home platforms are further fueling market expansion.

Key Market Trends

- Rising adoption of connected and IoT-enabled home devices.

- Increasing demand for home automation and convenience.

- Growing focus on home security and surveillance systems.

- Expansion of AI-powered voice assistants and ecosystems.

- Rising emphasis on energy efficiency and smart energy management.

Segmental Insights

- Based on device type, the safety and security devices segment dominated the United States smart home market by capturing 30.4% share in 2025, driven by increasing demand for smart surveillance and monitoring solutions.

- Based on housing type, the single-family dwellings segment held the majority share in 2025, supported by higher adoption of smart home technologies in independent housing units.

Country-Level Insights

- The United States led the global smart home market by holding 40.5% share in 2025, driven by high consumer awareness, advanced technological infrastructure, and strong presence of leading technology companies. The country continues to dominate due to rapid innovation and widespread adoption of smart home ecosystems.

Competitive Landscape

The U.S. smart home market is highly competitive, with companies focusing on ecosystem integration, product innovation, and AI-driven solutions. Strategic partnerships, acquisitions, and expansion of smart platforms are key strategies shaping the market.

Prominent companies operating in the U.S. smart home market include Amazon Inc., Apple Inc., Alphabet Inc., Honeywell International Inc., LG Electronics Inc., Samsung Group, Koninklijke Philips N.V., Wink Labs Inc., Sony Corporation, and August Inc.

U.S. Smart Home Market Size

The U.S. smart home market was valued at USD 33.30 billion in 2025, is estimated to reach USD 38.96 billion in 2026, and is projected to reach USD 136.81 billion by 2034, growing at a CAGR of 17% from 2026 to 2034.

A smart home is a residence equipped with internet-connected devices that allow for remote monitoring, automation, and control of amenities like lighting, heating, security, and appliances. This market relies on the Internet of Things to enable remote monitoring and management through smartphones, voice assistants, and automated routines. The integration of artificial intelligence allows these systems to learn user preferences and optimize energy consumption proactively. According to the United States Census Bureau, there are approximately 146 million housing units in the country as of July 2024, providing a vast potential base for technology adoption. Furthermore, the Federal Communications Commission reports that legacy broadband access (25/3 Mbps) is available to over 94 percent of American households. However, access to the modern 100/20 Mbps benchmark, which is critical for reliable connectivity and cloud processing, is available to only about 73 percent of households. The demographic shift toward millennial homeownership also influences market dynamics as this group demonstrates a higher affinity for digital solutions and convenience-driven technologies. Regulatory frameworks regarding data privacy and cybersecurity are evolving to address concerns related to personal information collected by these devices. The market is characterized by rapid innovation with manufacturers focusing on interoperability and seamless user experiences. This environment reflects a mature yet expanding sector where consumer expectations for comfort, efficiency, and safety drive continuous technological advancement and product diversification across various residential segments.

MARKET DRIVERS

Increasing Consumer Focus on Energy Efficiency and Sustainability

The growing emphasis on energy efficiency and environmental sustainability is a big boost for the United States smart home market. This motivates homeowners to adopt technologies that reduce utility costs and carbon footprints. Smart thermostats, lighting systems, and energy monitors allow users to track and optimize electricity consumption in real time, leading to significant savings. As per the United States Energy Information Administration, residential energy consumption accounts for a substantial portion of national usage, creating strong incentives for conservation measures. Smart devices can automatically adjust heating and cooling based on occupancy patterns and weather conditions, ensuring that energy is not wasted on empty rooms. Government incentives such as tax credits for energy-efficient upgrades further encourage the installation of smart home systems. Consumers are increasingly aware of the environmental impact of their lifestyles and seek ways to contribute to sustainability goals through technology. The ability to integrate renewable energy sources like solar panels with smart home management systems enhances the appeal of these solutions. Additionally, utility companies offer rebates for installing smart meters and connected devices, promoting wider adoption. Therefore, the combination of economic benefits, regulatory support, and environmental consciousness drives sustained demand for energy-efficient smart home products.

Rising Demand for Enhanced Home Security and Safety

The escalating demand for enhanced home security and safety is also a major factor pushing the growth of the United States smart home market. This addresses consumer concerns about property protection and personal well-being. Smart security systems, including video doorbells, smart locks, and surveillance cameras, provide real-time monitoring and instant alerts to homeowners via mobile applications. The Federal Bureau of Investigation reports that property crime rates declined by 8.1% in 2024, continuing a downward trend. Despite this, homeowner interest in advanced security solutions remains high due to the desire for remote visibility and proactive monitoring. These systems allow users to verify visitors, grant remote access to service providers, and review footage from anywhere in the world. The integration of artificial intelligence enables features such as facial recognition and anomaly detection, reducing false alarms and improving response accuracy. Insurance companies often offer discounts for homes equipped with monitored smart security systems, providing additional financial motivation for adoption. The ease of installation and user-friendly interfaces of modern devices make them accessible to a broad demographic, including renters and elderly individuals. Furthermore, the ability to integrate security features with other smart home functions, such as lighting and sirens, creates a comprehensive safety ecosystem. Hence, the desire for peace of mind and proactive protection fuels robust growth in the smart security segment of the market.

MARKET RESTRAINTS

Data Privacy and Cybersecurity Concerns

Data privacy and cybersecurity concerns hold back the expansion of the United States smart home market. This creates hesitation among consumers regarding the collection and storage of personal information. Smart home devices continuously gather data on user behaviors, habits, and preferences, raising fears about unauthorized access and misuse by third parties. As per the research, a majority of Americans express concern about the amount of data collected by connected devices and the potential for breaches that could expose sensitive information. High-profile security incidents involving hacked cameras or compromised networks have heightened awareness of vulnerabilities within the Internet of Things ecosystem. Consumers worry that manufacturers may share data with advertisers or insurance companies without explicit consent, leading to a lack of trust in the technology. The complexity of securing multiple devices with varying levels of encryption and update protocols adds to the burden for average users who may lack technical expertise. Regulatory uncertainty regarding data ownership and liability further complicates the landscape, making it difficult for consumers to understand their rights and protections. Thus, these privacy and security anxieties limit the willingness of some households to fully embrace smart home technologies, slowing market penetration among privacy-conscious demographics.

High Initial Costs and Complexity of Installation

High initial costs and the complexity of installation curb the growth of the United States smart home market. This limits accessibility for budget-constrained consumers and those lacking technical skills. While prices for individual devices have decreased, setting up a comprehensive smart home system involving multiple interconnected components can still require a substantial upfront investment. As per data and the Consumer Technology Association (CTA), while device adoption is rising, professional full-system integration remains a premium niche, with costs often exceeding several thousand dollars compared to affordable DIY options. Many consumers find the process of configuring networks, pairing devices, and troubleshooting connectivity issues daunting and time-consuming. The need for compatible hubs, routers, and stable broadband connections adds to the overall cost and technical barrier. Older homes may require electrical upgrades or structural modifications to support certain smart devices, increasing installation expenses. The lack of standardized protocols means that users must carefully research compatibility before purchasing, leading to decision fatigue and potential frustration. Additionally, ongoing subscription fees for cloud storage and premium features contribute to the long-term cost of ownership. So, the financial and technical hurdles associated with smart home adoption deter a significant segment of potential buyers, particularly in lower-income households and rural areas with limited technical support.

MARKET OPPORTUNITIES

Integration with Healthcare and Assisted Living Solutions

The integration of smart home technology with healthcare and assisted living solutions offers strong potential for the growth of the United States smart home market. This addresses the needs of an aging population seeking to age in place. Smart sensors and wearable devices can monitor vital signs, detect falls, and track daily activities, providing valuable data to caregivers and medical professionals. According to the Administration for Community Living's 2020 Profile of Older Americans, the population aged 65 and older is projected to increase from 54.1 million in 2019 to 94.7 million by 2060 (a 75% increase). Studies anticipate that this demographic shift will drive demand for assistive technologies, including remote health monitoring. Smart home systems can alert family members or emergency services in case of anomalies, enabling timely interventions and reducing hospital readmissions. Voice-activated assistants can help elderly individuals manage medications schedule appointments, and communicate with loved hands free, enhancing their independence and quality of life. Insurance providers and healthcare systems are increasingly recognizing the cost-effectiveness of preventive monitoring, leading to potential reimbursement models for smart home health technologies. Partnerships between technology companies and healthcare providers can facilitate the development of specialized devices tailored to medical needs. Therefore, the convergence of smart home and healthcare sectors offers a vast growth avenue driven by demographic trends and the shift toward value-based care.

Expansion of Interoperable Ecosystems and Standards

The proliferation of interoperable ecosystems and the adoption of universal standards open a clear path for the expansion of the United States smart home market. This resolves fragmentation issues and enhances user experience. The introduction of standards such as Matter aims to create a unified language for smart devices, allowing products from different manufacturers to communicate seamlessly. As per the Connectivity Standards Alliance, major technology companies have committed to supporting Matter, which simplifies setup and improves reliability for consumers. This interoperability reduces the risk of vendor lock-in and encourages users to mix and match devices based on preference rather than compatibility constraints. Retailers and installers can offer more flexible and customized solutions, knowing that components will work together effectively. The ease of integration fosters greater consumer confidence and accelerates adoption among mainstream audiences who previously hesitated due to technical complexities. Developers can focus on innovation and feature enhancement rather than proprietary connectivity solutions, driving faster product cycles. Furthermore, interoperable systems enable more sophisticated automation scenarios where devices from various categories work in harmony to create intuitive living environments. Hence, the move toward open standards unlocks new potential for market growth by making smart home technology more accessible, reliable, and appealing to a broader consumer base.

MARKET CHALLENGES

Lack of Standardization and Fragmentation

The lack of standardization and market fragmentation is a primary barrier to the United States smart home market. This creates confusion and compatibility issues for consumers. With numerous manufacturers producing devices using different communication protocols such as Zigbee, Z-Wave, Wi-Fi, and Bluetooth, ensuring seamless interaction between products remains difficult. As per the Consumer Technology Association, the sheer variety of incompatible ecosystems forces users to invest in multiple hubs and bridges, complicating the setup process and increasing costs. This fragmentation leads to a disjointed user experience where individuals must manage several applications to control different aspects of their home. The absence of a single dominant standard slows down mass adoption as consumers fear investing in technology that may become obsolete or unsupported. Manufacturers often prioritize proprietary solutions to retain customer loyalty, hindering the development of a cohesive market. Although initiatives like Matter are emerging, widespread implementation takes time, and legacy devices may not be upgradable. Retailers struggle to educate customers on compatibility, leading to higher return rates and dissatisfaction. Thus, the fragmented landscape impedes the realization of a truly integrated smart home experience, requiring industry-wide collaboration to establish and enforce universal norms.

Reliability and Connectivity Issues

Reliability and connectivity issues are the main hindrances to the United States smart home market. This decreases user trust and satisfaction with connected devices. Smart home systems depend heavily on stable internet connections and robust local networks to function correctly, yet many households experience intermittent bandwidth or signal dead zones. As per the Federal Communications Commission's 2024 Section 706 Report, advanced telecommunications capability is not yet deployed to all Americans in a reasonable and timely fashion. Significant gaps persist, particularly regarding infrastructure in rural areas and affordability in urban centers. Device failures, software glitches, and latency problems can disrupt critical functions such as security monitoring or climate control, leading to frustration and potential safety risks. Users expect instantaneous responses from voice assistants and automated routines, but delays can occur due to server outages or processing bottlenecks. The dependence on cloud computing means that internet disruptions can render devices useless until connectivity is restored. Additionally, the increasing number of connected devices strains home networks, requiring upgrades to routers and mesh systems that add to the overall cost and complexity. Troubleshooting connectivity issues often requires technical knowledge that average consumers may lack, leading to reliance on customer support, which may be inconsistent. So, ensuring consistent and reliable performance remains a critical hurdle that manufacturers and service providers must address to maintain consumer confidence and drive sustained market growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Device Type, Housing Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Amazon Inc., Apple Inc., Alphabet Inc., Honeywell International Inc., LG Electronics Inc., Samsung Group, Koninklijke Philips N.V., Wink Labs Inc., Sony Corporation, August Inc., and Others. |

SEGMENTAL ANALYSIS

By Device Type Insights

The safety and security devices segment maintained dominance by accounting for a 30.4% share of the United States smart home market in 2025. Factors such as the paramount consumer priority of protecting property and ensuring personal safety drive the dominance of this segment. This segment includes smart locks, video doorbells, surveillance cameras, and alarm systems that provide real-time monitoring and remote access control. As per the Federal Bureau of Investigation, property crime remains a significant concern for American households, with hundreds of thousands of burglaries reported annually, which motivates residents to invest in proactive security measures. The biggest reason behind this domination is the ability of these devices to offer peace of mind through instant alerts and visual verification of events. Smart cameras equipped with artificial intelligence can distinguish between humans, animals, and vehicles, reducing false alarms and enhancing reliability. The integration of these devices with mobile applications allows homeowners to monitor their properties from anywhere in the world, providing a sense of control and security. Additionally, insurance companies often provide premium discounts for homes equipped with monitored security systems, creating a financial incentive for adoption. The ease of installation for DIY security kits has also broadened the market appeal, allowing renters and homeowners alike to enhance safety without professional help. Therefore, the critical nature of home protection combined with technological advancements and economic benefits cements safety and security devices as the dominant segment in the smart home landscape.

The energy and water control devices segment is predicted to witness the highest CAGR of 18.6% from 2026 to 2034 due to rising utility costs and increasing environmental consciousness. This segment includes smart plugs, energy monitors, smart irrigation controllers, and leak detectors that help users optimize resource consumption. As per the United States Energy Information Administration, residential electricity prices have seen consistent increases, prompting consumers to seek ways to reduce their monthly bills through efficient management. The primary factor driving this growth is the ability of smart devices to provide detailed insights into usage patterns and automate conservation efforts. Smart irrigation systems adjust watering schedules based on weather forecasts, preventing water waste while maintaining lawn health. Leak detectors alert homeowners to potential plumbing issues before they cause significant damage, saving thousands of dollars in repair costs. Government incentives and rebates for energy-efficient appliances further encourage the adoption of these technologies. The integration of these devices with broader home automation systems allows for comprehensive energy management strategies that align with sustainability goals. Additionally, the rise of net-zero energy homes drives demand for precise monitoring and control tools. Hence, the combination of economic savings, environmental benefits, and regulatory support accelerates the rapid expansion of the energy and water control segment.

By Housing Type Insights

The single-family dwellings segment held the majority share of the United States smart home market in 2025. This supremacy of the segment is credited to the higher ownership rates, greater control over property modifications, and larger living spaces that accommodate multiple devices. Homeowners in single-family houses are more likely to invest in comprehensive smart home systems, including security lighting, climate control, and entertainment, as they have the authority to make permanent installations. As per the United States Census Bureau, single-family homes account for the majority of housing units in the country, providing a vast addressable market for smart technology providers. A key driver for this domination is the desire to increase property value and enhance lifestyle convenience through automation. Owners of single-family homes often have yards, driveways, and multiple entry points that require robust security and monitoring solutions such as outdoor cameras and smart garage door openers. The spatial layout of these homes also benefits from whole-house audio and lighting systems that create cohesive ambient experiences. Furthermore, the demographic profile of single-family homeowners often includes families with children and pets who benefit from safety features and remote monitoring capabilities. The financial stability associated with homeownership allows for higher discretionary spending on technology upgrades. Thus, the structural demographic and economic characteristics of single-family dwellings establish them as the primary adopters of smart home technologies.

The multifamily dwellings segment is estimated to register the fastest CAGR of 20.7% during the forecast period, owing to the increasing adoption of smart apartment technologies by property managers and developers. This segment includes apartment complexes, condominiums, and townhouses where smart devices are installed to enhance tenant experience, improve operational efficiency, and attract high-quality renters. As per the National Multifamily Housing Council's 2024 Renter Preferences Survey, a significant percentage of new multifamily constructions are incorporating smart home features, specifically keyless entry, smart thermostats, and package lockers, as standard amenities to meet evolving resident demands. The main factor accelerating this growth is the competitive rental market, where landlords use technology to differentiate their properties and justify higher rents. Smart access control systems reduce the need for physical key management and improve security for residents. Property managers leverage smart sensors to monitor maintenance issues such as leaks or HVAC failures, proactively reducing repair costs and downtime. The rise of remote work has also increased the demand for high-speed connectivity and smart home environments that support productivity and comfort. Developers recognize that tech-savvy renters, particularly millennials and Gen Z, prioritize connected living spaces. So, the strategic integration of smart technologies in multifamily properties drives rapid market expansion as it becomes a standard expectation rather than a luxury.

COUNTRY LEVEL ANALYSIS

U.S. Smart Home Market Analysis

The United States led the global smart home market and captured a 40.5% share in 2025. This leading position of the US market is attributed to its advanced technological infrastructure, high disposable income, and strong consumer culture centered on convenience and innovation. The country’s market status is characterized by a mature ecosystem where major technology companies compete to offer integrated platforms and devices. While the Consumer Technology Association (CTA) projected overall U.S. tech industry revenue to grow in 2024, smart home device shipments specifically were expected to stall or remain flat (0.6% growth globally) due to market saturation, with growth projected to return in 2025. Additionally, while household penetration is high, adoption varies significantly, with recent surveys showing lower prevalence among lower-income demographic groups. The presence of leading tech giants such as Amazon, Google, and Apple fosters intense competition and rapid innovation in voice assistants and interoperability standards. High broadband penetration and smartphone usage facilitate seamless connectivity and control of smart devices. Regulatory frameworks regarding data privacy and cybersecurity are evolving to protect consumers while encouraging industry growth. The aging population and increasing focus on energy efficiency further drive demand for health monitoring and conservation technologies. The United States serves as a trendsetter for global markets, influencing product development and consumer expectations worldwide. The combination of economic strength, technological leadership, and cultural affinity for automation solidifies the United States' position as the dominant force in the global smart home industry.

COMPETITIVE LANDSCAPE

The competition in the United States smart home market is intense and characterized by the presence of technology giants, specialized device manufacturers, and telecommunications providers vying for ecosystem dominance. Major players compete based on platform interoperability voice assistant capabilities, and device variety to attract and retain users. Differentiation is achieved through superior user experience, robust security features, and seamless integration with existing consumer electronics. Price competition is significant in entry-level devices, while premium segments focus on quality and advanced functionalities. The adoption of open standards like Matter reduces vendor lock-in, forcing companies to innovate beyond proprietary ecosystems. Strategic alliances with real estate developers and property managers help embed smart technologies in new constructions. Customer loyalty is driven by the stickiness of digital assistants and the convenience of unified control apps. Regulatory scrutiny regarding data privacy influences competitive dynamics as firms strive to build trust. The market sees continuous product launches featuring enhanced AI and connectivity options. Success depends on balancing innovation with reliability and addressing consumer concerns about security and complexity.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. smart home market include

- Amazon Inc.

- Apple Inc.

- Alphabet Inc.

- Honeywell International Inc.

- LG Electronics Inc.

- Samsung Group

- Koninklijke Philips N.V.

- Wink Labs Inc.

- Sony Corporation

- August Inc.

TOP PLAYERS IN THE MARKET

- Amazon.com Inc is a dominant force in the United States smart home market, primarily through its Echo device lineup and the Alexa voice assistant platform. The company has created a vast ecosystem of connected devices that allow users to control lighting, security, and entertainment systems using voice commands. Recent actions include the expansion of its Sidewalk network, which extends connectivity for smart devices beyond the home Wi Fi range. Amazon has also integrated Matter support into its devices to ensure interoperability with products from other manufacturers. The company focuses on enhancing privacy features and local processing capabilities to address consumer concerns. By leveraging its extensive retail platform, Amazon promotes third-party smart home products effectively. These initiatives strengthen its market position by creating a sticky ecosystem that encourages user retention and continuous engagement with smart home technologies.

- Alphabet Inc contributes significantly to the United States smart home market through its Google Nest brand and the Google Assistant platform. The company offers a wide range of smart speakers, displays, thermostats, and security cameras that integrate seamlessly with Android devices and Google services. Recent actions involve the discontinuation of the Works with Nest program in favor of the universal Matter standard to improve compatibility across brands. Alphabet has invested heavily in artificial intelligence to enhance the predictive capabilities of its home automation routines. The integration of Google Home with energy management tools helps users optimize electricity usage and reduce costs. By focusing on intuitive user interfaces and robust cloud infrastructure, Alphabet ensures a smooth and reliable experience. These efforts reinforce its reputation as a leader in intelligent home solutions that prioritize convenience and efficiency for consumers.

- Apple Inc plays a pivotal role in the United States smart home market with its HomeKit platform and HomePod smart speakers. The company emphasizes privacy and security by processing data locally on devices whenever possible, appealing to privacy-conscious consumers. Recent actions include the full implementation of Matter support across its product line, enabling seamless interaction with non-Apple smart home devices. Apple has introduced new features in its Home app, such as adaptive lighting and enhanced automation capabilities. The integration of Siri with home controls allows for hands-free management of various connected appliances. By leveraging its strong brand loyalty and ecosystem lock-in, Apple attracts users who already own iPhones and iPads. These strategies strengthen its market presence by offering a secure and cohesive smart home experience that aligns with its premium brand identity.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States smart home market primarily focus on adopting universal standards like Matter to ensure interoperability and simplify user experience across diverse devices. Companies are increasingly integrating artificial intelligence to enable predictive automation and personalized home environments. Strategic partnerships with utility providers and insurance companies create new revenue streams through energy management and security monitoring services. Emphasis on data privacy and local processing builds consumer trust and differentiates premium offerings. Expansion of product portfolios to include health and wellness sensors addresses the needs of aging populations. Investment in cloud infrastructure ensures reliable connectivity and remote access capabilities. Marketing efforts highlight ease of installation and DIY friendly features to broaden appeal. These strategies collectively drive adoption by enhancing convenience, security, and value proposition for homeowners.

MARKET SEGMENTATION

This research report on the U.S. smart home market has been segmented and sub-segmented into the following categories.

By Device Type

- Safety and Security Devices

- Energy and Water Control

- Climate Control

- Lighting Control

- Consumer Electronics

By Housing Type

- Multifamily Dwelling

- Single Family Dwelling

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.