U.S Sunscreen Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Lotions, Creams, Gels, Sprays, Sticks, Others), Broad Spectrum Coverage, Water Resistance, Application Form, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

Market Size, 2025

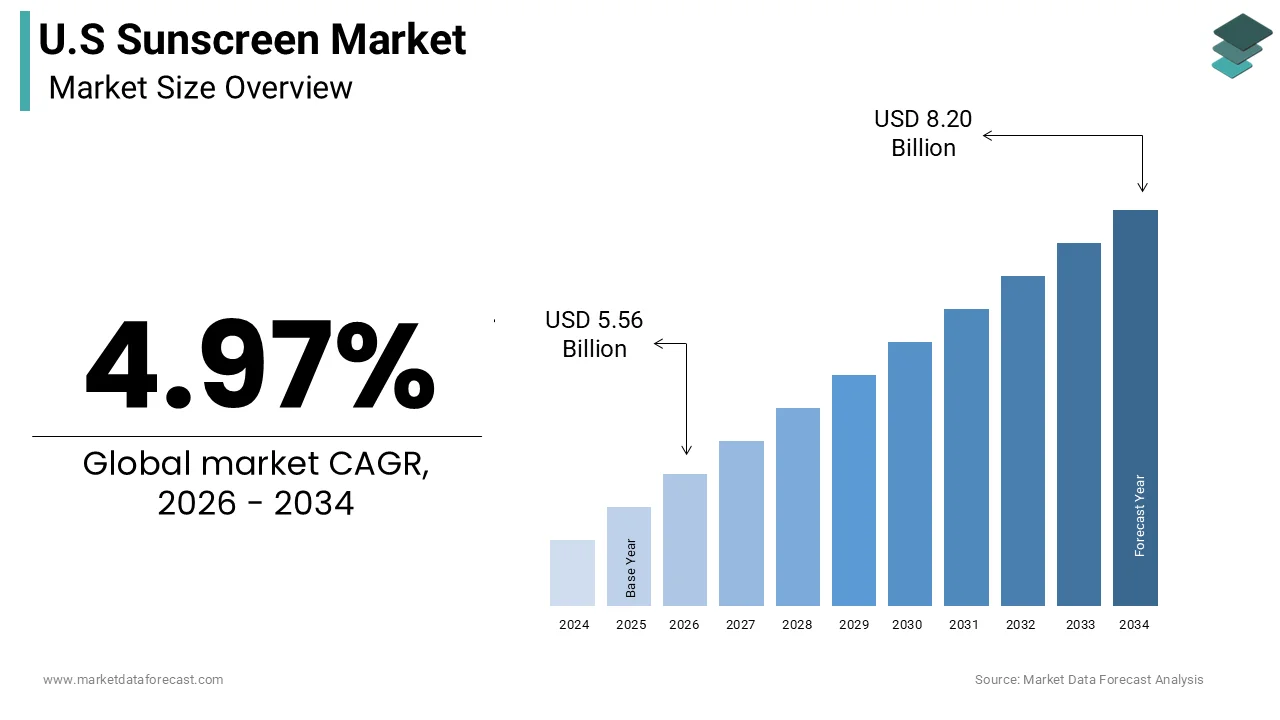

$5.30 BnMarket Estimate, 2026

$5.56 BnMarket Forecast, 2034

$8.20 BnCAGR, 2026–2034

4.97%U.S. Sunscreen Market Report Summary

The United States sunscreen market was valued at USD 5.30 billion in 2025 and is projected to reach USD 8.20 billion by 2034, growing from USD 5.56 billion in 2026 at a CAGR of 4.97% during the forecast period. Market growth is driven by increasing awareness regarding skin protection, rising prevalence of skin-related disorders, and growing consumer preference for personal care and sun protection products. Expanding outdoor recreational activities and innovations in dermatologically tested formulations are further supporting the growth of the U.S. sunscreen market.

Key Market Trends

- Rising awareness regarding UV radiation and skin cancer prevention

- Increasing demand for broad-spectrum and dermatologist-recommended products

- Growth in mineral and reef-safe sunscreen formulations

- Expansion of premium skincare and cosmetic sunscreen products

- Increasing popularity of lightweight, non-greasy, and tinted sunscreen solutions

Segmental Insights

- Based on product type, the lotions segment dominated the U.S. sunscreen market in 2025 by accounting for 48.1% of the market share, driven by easy application and broad consumer preference

- Based on broad-spectrum coverage, the UVA/UVB broad-spectrum segment held a significant market share in 2025 due to increasing consumer awareness regarding complete sun protection

- Based on water resistance, the not water-resistant segment accounted for 32.1% of the market share in 2025, supported by daily-use skincare applications and indoor lifestyle products

- Based on the application form, the tube segment led the market in 2025 by capturing 44.3% of the market share, driven by portability, convenience, and controlled product dispensing

Competitive Landscape

- The U.S. sunscreen market is highly competitive, with companies focusing on innovative formulations, skin-friendly ingredients, and multifunctional skincare products. Market players are investing in SPF technology, organic ingredients, and eco-friendly packaging to strengthen their market presence.

- Prominent players in the U.S. sunscreen market include Johnson & Johnson, Beiersdorf AG, L'Oréal, Edgewell Personal Care, Sun Bum, Shiseido, The Estée Lauder Companies, Unilever, Coty, and BASF.

U.S Sunscreen Market Size

The U.S. sunscreen market size was calculated to be USD 5.30 billion in 2025 and is anticipated to be worth USD 8.20 billion by 2034, from USD 5.56 billion in 2026, growing at a CAGR of 4.97% during the forecast period.

The sunscreen is a topical formulation designed to protect the skin from harmful ultraviolet radiation, including lotions, sprays, sticks, and powders. The definition extends beyond seasonal beachwear protection to include daily facial moisturizers with SPF integrated into year-round skincare routines. Consumer engagement is driven by medical recommendations and the aesthetic desire for youthful skin free from sun damage. According to the Centers for Disease Control and Prevention, skin cancer is the most common form of cancer in the United States, with more than 5 million cases diagnosed annually, underscoring the urgent need for preventive measures. Furthermore, data from the American Academy of Dermatology indicates that one in five Americans will develop skin cancer by the age of 70, highlighting the pervasive risk across demographics. The shift toward holistic wellness has elevated sunscreen from a niche product to a daily essential for individuals of all ages and skin tones. The UV index levels have remained consistently high in many regions due to atmospheric changes, reinforcing the necessity of daily protection. The integration of broad spectrum coverage and water resistance has become a standard expectation rather than a premium feature.

MARKET DRIVERS

Increasing Prevalence of Skin Cancer and Dermatological Awareness

The rising incidence of skin cancer and heightened public health campaigns are primarily boosting the growth of the United States sunscreen market. Consumers are increasingly educated about the dangers of ultraviolet exposure and the protective benefits of regular sunscreen application. According to the Skin Cancer Foundation, one in five Americans will develop skin cancer in their lifetime, which drives a proactive approach to prevention among health-conscious individuals. Medical professionals consistently recommend daily use of broad-spectrum sunscreen with an SPF of 30 or higher to mitigate risks. The public awareness initiatives have successfully linked sun protection with long-term health outcomes, leading to increased compliance among adults and children. The visibility of skin cancer survivors and advocacy groups on social media platforms further amplifies the message of prevention. Insurance providers and healthcare systems are also promoting preventive care to reduce long-term treatment costs. This medical endorsement creates a sense of urgency and responsibility among consumers. The integration of sunscreen into routine medical checkups and school health programs reinforces habitual use.

Integration of Sun Protection into Daily Skincare Routines

The evolution of sunscreen from a seasonal beach product to a daily skincare staple is additionally fuelling the growth of the United States sunscreen market. Consumers now view sun protection as an essential step in their morning regimen, regardless of weather conditions or indoor activities. According to a survey by the International Spa Association, over 60% of consumers now apply sunscreen daily as part of their skincare routine, reflecting a fundamental shift in behavior. The rise of multitasking products, such as moisturizers, foundations, and primers with built-in SPF, simplifies the application process and encourages consistent use. The demand for cosmetic elegance in sunscreens has surged with users seeking lightweight, non-greasy formulas that do not interfere with makeup application. The influence of beauty influencers and dermatologists on digital platforms promotes the concept of sun safety as a cornerstone of beauty maintenance. Urban pollution and blue light exposure from screens have also expanded the perceived need for protection beyond traditional UV rays. Brands respond by incorporating antioxidants and skincare ingredients like hyaluronic acid and niacinamide into sunscreen formulations. The availability of tinted sunscreens that offer coverage and protection further enhances appeal.

MARKET RESTRAINTS

Concerns Regarding Chemical Ingredients and Environmental Impact

Consumer awareness regarding the safety of chemical filters and their environmental impact is restricting the growth of the United States sunscreen market. Ingredients, such as oxybenzone and octinoxate, have faced scrutiny for potential hormonal disruption and toxicity to marine ecosystems. Many popular sunscreen brands receive low safety ratings due to the presence of these controversial chemicals, leading to hesitation among health-conscious buyers. The state of Hawaii and other coastal regions have enacted bans on certain chemical filters to protect coral reefs, which influences national purchasing trends. As per data from the National Oceanic and Atmospheric Administration, studies linking sunscreen ingredients to coral bleaching have raised awareness among eco-conscious consumers. Some consumers report skin irritation or allergic reactions to chemical filters, further driving demand for alternative options. The lack of clear federal guidelines on ingredient safety creates confusion and mistrust among shoppers. Greenwashing claims by brands exacerbate skepticism as consumers struggle to verify environmental assertions.

Sensory Issues and User Experience Limitations

The unpleasant sensory experience associated with traditional sunscreen formulations, including greasiness,s stickiness, and white residue, is also slowing the growth of the United States sunscreen market. Many consumers find conventional sunscreens uncomfortable to wear under clothing or makeup, leading to irregular application. According to a study published in the Journal of the American Academy of Dermatology, nearly 40% of users cite cosmetic unacceptability as the primary reason for non-compliance with sun protection recommendations. The thick consistency and strong odor of some products further deter daily use, particularly among individuals with sensitive skin or olfactory sensitivities. The sales of traditional heavy lotions have stagnated while lighter formats, such as mists and gels, gain traction, indicating a preference for improved user experience. The difficulty in achieving high SPF values without compromising texture remains a technical challenge for formulators. Mineral sunscreens often leave a noticeable white cast, which is particularly problematic for individuals with darker skin tones, leading to exclusion and dissatisfaction. The time required for proper absorption and the need for frequent reapplication add to the inconvenience. Consumers often skip applications when rushing or engaging in spontaneous outdoor activities due to these friction points. Brands struggle to balance efficacy with aesthetic appeal, resulting in products that either perform well but feel poor or feel good but offer inadequate protection.

MARKET OPPORTUNITIES

Expansion of Mineral and Clean Label Formulations

The growing demand for natural and safe ingredients for manufacturers to innovate with mineral-based and clean-label sunscreens is ascribed to creating new opportunities for the growth of the United States sunscreen market. Consumers are increasingly seeking products free from synthetic chemicals, parabens, and fragrances, preferring zinc oxide and titanium dioxide as active ingredients. These formulations are generally recognized as safe and effective by the Food and Drug Administration, offering a reliable alternative for sensitive skin. As per data from Mintel, launches of mineral sunscreen products have increased significantly as brands respond to consumer demand for transparency and simplicity. Innovations in micronized particles have improved the texture and reduced the white cast of mineral sunscreens, making them more cosmetically elegant. Certifications such as Reef Safe and Non-GMO Project Verified enhance credibility and appeal to eco-conscious shoppers. Marketing campaigns that highlight the purity and gentleness of mineral ingredients resonate strongly with parents and health-aware individuals. The development of hybrid formulas that combine mineral protection with skincare benefits offers additional value. This strategic pivot toward natural solutions addresses both health and environmental concerns, transforming regulatory pressures into competitive advantages.

Development of Advanced Delivery Systems and Textures

The innovation in delivery systems and product textures offers immense potential for enhancing user experience and driving adoption among reluctant users, which is crucial to leverage the growth of the United States sunscreen market. Formats such as powder sunscreens, setting sprays, and stick applicators provide convenient and mess-free options for reapplication and targeted protection. According to Statista, the sales of sunscreen sticks and powders have grown rapidly as consumers seek portable and easy-to-use solutions for on-the-go protection. These formats are particularly appealing for application over makeup and for hard-to-reach areas such as the scalp and ears. As per data from the NPD Group, novelty formats attract younger demographics who prioritize convenience and multifunctionality in their beauty routines. The development of invisible finish technologies and fast-absorbing serums addresses previous complaints about greasiness and residue. Brands are investing in research to create water-resistant formulas that do not sting eyes or clog pores, enhancing comfort during physical activities. The integration of app-connected devices that monitor UV exposure and remind users to reapply adds a technological layer to protection. Subscription models for these innovative formats ensure consistent supply and customer retention.

MARKET CHALLENGES

Regulatory Uncertainty and Approval Delays

The complex and slow regulatory framework for approving new sunscreen active ingredients is acting as a major barrier to the growth of the United States sunscreen market. The proposed Sunscreen Innovation Act aims to streamline the process, but progress remains sluggish, causing frustration among manufacturers. This regulatory lag prevents American brands from accessing advanced filters that offer better protection and cosmetic elegance compared to older ingredients. The lack of modern filters forces companies to rely on outdated formulations that may be less effective or pleasant to use. The uncertainty surrounding the finalization of safety standards creates hesitation in investment and product development. Manufacturers must navigate a patchwork of state-level regulations regarding ingredient bans, adding complexity to compliance. The disparity between US and international standards hinders the global competitiveness of American sunscreen brands. Consumers are increasingly aware of superior foreign formulations, leading to cross-border purchases or reliance on gray market imports.

Counterfeiting and Product Integrity Issues

The prevalence of counterfeit sunscreen products and issues with product integrity pose a severe threat to consumer safety and brand reputation, which also inhibits the growth of the United States sunscreen market. Fake sunscreens often lack active ingredients or contain harmful substances and do not protect against UV radiation. The counterfeit health and beauty products, including sunscreen, are a growing concern, particularly online. Consumers who purchase these fake items are at increased risk of sunburn and long-term skin damage, leading to loss of trust in the category. The fraudulent skincare products have risen as e-commerce channels expand without adequate verification mechanisms. The difficulty in distinguishing between authentic and counterfeit packaging exacerbates the problem, especially for popular premium brands. Temperature fluctuations during shipping and storage can also degrade the efficacy of legitimate sunscreen products, leading to inconsistent performance. Retailers and manufacturers struggle to control the supply chain and ensure product stability from factory to consumer. Legal enforcement against counterfeiters is challenging due to the anonymous nature of online sellers. Brands must invest heavily in authentication technologies and consumer education to combat this issue. However, these measures add to operational costs and complexity. Maintaining product integrity and consumer trust in a digital age remains a persistent challenge for industry leaders striving to ensure safety and efficacy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.97% |

| Segments Covered | By Product Type, Broad Spectrum Coverage, Water Resistance, Application Form, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Johnson & Johnson, Beiersdorf AG, L'Oréal S.A., Edgewell Personal Care, Sun Bum LLC, Shiseido Company Limited, The Estée Lauder Companies Inc., Unilever PLC, Coty Inc., BASF SE |

SEGMENTAL ANALYSIS

By Product Type Insights

The lotions segment was the dominant by capturing 48.1% of the United States sunscreen market share in 2025, with their widespread availability, ease of application, and ability to provide uniform coverage over large body areas. Lotions are the traditional and most recognized form of sun protection, making them the default choice for families and individuals seeking reliable defense against ultraviolet radiation. The lotions are recommended for full-body application due to their ability to spread evenly and ensure adequate dosage per square inch of skin. The consumer familiarity and trust associated with this format, which has been marketed extensively for decades. The lotion-based sunscreens account for the majority of unit sales in mass retail channels due to their competitive pricing and variety of SPF options. The versatility of lotions allows for formulation with additional skincare benefits, such as moisturizers and antioxidants, enhancing their appeal for daily use. Manufacturers can easily adjust the viscosity and texture of lotions to cater to different skin types, including dry, oily, and sensitive skin. The packaging of lotions in bottles or tubes ensures controlled dispensing and minimizes waste. Furthermore, the ability to incorporate high concentrations of active ingredients without compromising stability makes lotions a preferred vehicle for high SPF products.

The sticks segment is projected to register the fastest CAGR of 8.5% during the forecast period, with the demand for convenient, portable, and mess-free application methods, particularly for targeted areas such as the face, ears, and scalp. The increasing popularity of active lifestyles and outdoor sports, where users require quick reapplication without using their hands. According to the Skin Cancer Foundation, stick sunscreens are ideal for precise application around the eyes and on sensitive areas where lotions may cause irritation or run into the eyes. The rise of stick formats aligns with the trend toward on-the-go beauty and personal care products that fit easily into pockets or bags. The solid formulation of sticks prevents spills and leaks, making them travel-friendly and compliant with airline regulations. Innovations in clear and non-greasy stick formulas have addressed previous concerns about residue and white casts, appealing to a broader demographic, including men and children. The ease of use encourages consistent reapplication, which is critical for effective protection. Brands are launching multifunctional sticks that combine sun protection with tint or hydration, further driving adoption.

By Broad Spectrum Coverage Insights

The UVA/UVB broad spectrum segment was the largest by holding a significant share of the United States sunscreen market in 2025, with the medical recommendations and regulatory standards that emphasize comprehensive protection against both aging and burning rays. Consumers are increasingly educated about the distinct dangers of UVA rays, which penetrate deep into the skin, causing premature aging and DNA damage, and UVB rays, which cause surface burns. According to the Food and Drug Administration, only sunscreens that pass specific testing criteria can be labeled as broad spectrum, ensuring they protect against both types of radiation. As per data from the American Academy of Dermatology, dermatologists strongly advise the use of broad-spectrum sunscreens to prevent skin cancer and photoaging effectively. The integration of broad-spectrum claims into marketing campaigns has become standard practice, reinforcing consumer expectations for dual protection. Retailers and healthcare providers prioritize stocking broad-spectrum products, reducing the visibility of single-spectrum options. The prevalence of skin cancer cases linked to cumulative UVA exposure further motivates consumers to seek comprehensive coverage. Manufacturers invest in advanced filter combinations to achieve high broad-spectrum ratings, enhancing product credibility.

The UVA-only segment is likely to register the fastest CAGR of 4.2% during the forecast period, with the specific consumer needs for anti-aging protection and indoor usage. While not a standalone replacement for broad-spectrum sunscreens, UVA-focused products are gaining traction among individuals concerned primarily with photoaging and hyperpigmentation. The recognition that UVA rays penetrate glass and are present consistently throughout the year, even on cloudy days or indoors. UVA radiation contributes significantly to collagen breakdown and wrinkle formation, prompting skincare enthusiasts to prioritize UVA protection in their daily routines. The rise of indoor sunscreens and makeup products with high UVA protection factors reflects this trend. Consumers working in office environments or spending significant time near windows seek products that shield against incidental exposure. The development of specialized filters that target long-wave UVA rays enhances the efficacy of these products.

By Water Resistance Insights

The not water-resistant segment accounted in holding 32.1% of the United States sunscreen market share in 2025, with its suitability for daily urban use and indoor activities where exposure to water or excessive sweat is minimal. Most consumers apply sunscreen as part of their morning skincare routine before commuting or working in climate-controlled environments, making water resistance unnecessary. Many daily wear sunscreens and facial moisturizers with SPF do not claim water resistance to avoid heavier formulations and potential pore clogging. The preference for lightweight and cosmetically elegant textures that absorb quickly and serve as a base for makeup. These products are often formulated with skincare ingredients that may be compromised by water-resistant polymers. Consumers appreciate the ease of removal at the end of the day without requiring harsh cleansers. The cost-effectiveness of non-water-resistant formulas also appeals to budget-conscious shoppers who use sunscreen daily. The distinction between beachwear and daily wear has led to a bifurcation in the market, with the latter dominating in volume.

The very water-resistant segment is potentially growing at the fastest CAGR of 7.8% from 2026 to 2034, with the increasing participation in water sports and outdoor recreational activities. Consumers engaging in swimming, surfing, and intense physical exercise require durable protection that withstands prolonged exposure to water and sweat. The drowning and water-related injuries are significant public health concerns, leading to increased time spent in aquatic environments, where sun protection is important. The regulatory standardization of water resistance claims allows consumers to trust the 80-minute label for extended activities. The participation in water-based outdoor activities has surged post-pandemic, boosting demand for robust sunscreens. Athletes and fitness enthusiasts prefer very water-resistant formulas to ensure continuous protection without frequent reapplication during events. Innovations in film-forming technologies have improved the comfort and durability of these products, reducing the sticky feel associated with older formulations. The rise of family vacations to beach destinations further drives seasonal spikes in sales. Brands are marketing these products as essential gear for an active lifestyle,s enhancing their appeal.

By Application Form Insights

The tube segment was the largest by holding 44.3% of the United States sunscreen market share in 2025, with its practicality, hygiene, and ability to preserve product integrity. Tubes allow for controlled dispensing, minimizing waste and preventing contamination of the remaining product. The tubes are the preferred packaging format for lotions and creams due to their cost-effectiveness and ease of manufacturing. The consumer preference for portable and leak-proof packaging that fits easily into bags and pockets. The tube packaged sunscreens dominate shelf space in retail stores due to their versatility across different product viscosities. The ability to squeeze out the exact amount needed reduces product waste and ensures consistent application. Tubes also provide ample surface area for branding and instructional labels, enhancing consumer communication. The recyclability of certain tube materials aligns with growing environmental consciousness among shoppers. Manufacturers can use multi-layer tubes to protect light-sensitive ingredients, extending shelf life. The familiarity and convenience of tubes make them the default choice for both adults and children.

The aerosol segment is projected to witness the fastest CAGR of 6.5% during the forecast period, with the demand for quick and easy application, especially for hard-to-reach areas. Spray sunscreens offer a convenient solution for parents applying protection to children and for individuals seeking rapid coverage before outdoor activities. The time-saving benefit of aerosols, which allow for uniform coverage without the need for rubbing. The spray sunscreens are popular among families for their ease of use, although proper application techniques are emphasized to ensure efficacy. The convenience factor appeals to active consumers, who value efficiency in their grooming routines. Innovations in nozzle technology have reduced overspray and improved the fineness of the mist, enhancing user experience. The cooling sensation of aerosol sprays is also perceived as refreshing in hot weather. The portability and speed of application make aerosols a preferred choice for sports and travel.

COMPETITION OVERVIEW

The competitive landscape of the United States sunscreen market is characterized by intense rivalry among established pharmaceutical giants and specialized skincare brands. Large players leverage strong brand equity and extensive distribution networks to maintain dominance while competing on innovation and price. Price competition is moderate in the premium segment, whereas mass market brands compete aggressively on value and accessibility. The rise of clean beauty trends has introduced new competitors focusing on natural and mineral formulations. Innovation focuses on texture improvement and multifunctional benefits to differentiate offerings. Supply chain efficiency is critical for maintaining profitability amidst fluctuating raw material costs. Regulatory pressures regarding environmental impact drive investments in sustainable practices. Consumer loyalty is influenced by dermatologist recommendations and personal experience with product texture. Companies must balance scientific credibility with cosmetic elegance to sustain market position. This dynamic environment requires continuous adaptation to changing consumer preferences and scientific advancements.

KEY MARKET PLAYERS

A few major players of the U.S sunscreen market include

- Johnson & Johnson

- Beiersdorf AG

- L'Oréal S.A

- Edgewell Personal Care

- Sun Bum LLC

- Shiseido Company Limited

- The Estée Lauder Companies Inc

- Unilever PLC

- Coty Inc

- BASF SE

Top Strategies Used by Key Market Participants

Key players in the United States sunscreen market employ diverse strategies to maintain a competitive advantage and drive growth. Product innovation remains central with companies developing lightweight, non-greasy, and mineral-based formulations. Brands focus on integrating skincare benefits such as hydration and anti-aging properties into sunscreens. Strategic marketing campaigns emphasize dermatological endorsement and daily protection habits to build trust. Sustainability initiatives are increasingly important as consumers demand reef-safe and eco-friendly packaging. Companies leverage digital platforms to educate consumers about sun safety and proper usage. Omnichannel distribution ensures widespread availability in pharmacies, retail stores, and online channels. Collaborations with influencers and healthcare professionals enhance brand credibility and reach.

Leading Players in the United States Sunscreen Market

- Johnson and Johnson maintains a significant presence in the United States sunscreen market through its Neutrogena and Aveeno brands. The company contributes by offering dermatologist-recommended products that cater to sensitive skin and specific dermatological needs. Recent actions include launching lightweight facial sunscreens with hyaluronic acid to appeal to skincare-focused consumers. Johnson and Johnson has invested in digital marketing campaigns that emphasize clinical efficacy and daily protection benefits. The firm leverages its extensive retail distribution network to ensure widespread availability in pharmacies and mass market stores. These efforts reinforce its reputation for trust and medical credibility while expanding its reach among younger demographics seeking preventive skincare solutions.

- Beiersdorf AG holds a strong position in the US sunscreen sector through its Eucerin and Coppertone brands. The company drives growth by focusing on specialized sun protection solutions for various skin types and activities. Recent strategies involve introducing mineral-based sunscreens that are reef safe and free from oxybenzone to meet environmental concerns. Beiersdorf has enhanced its product lines with antioxidants and anti-aging ingredients to combine protection with skincare benefits. The firm actively engages consumers through educational initiatives about sun safety and proper application techniques. Investments in sustainable packaging align with growing eco-conscious preferences among shoppers.

- Edgewell Personal Care Company is a key player in the US sunscreen market known for its Hawaiian Tropic and Banana Boat brands. The company focuses on providing affordable and effective sun care products for active lifestyles and family use. Recent actions include revitalizing brand imagery to appeal to younger consumers through vibrant marketing and social media engagement. Edgewell has expanded its portfolio with spray and stick formats that offer convenient application for sports and outdoor activities. The firm emphasizes water resistance and durability in its formulations to meet the needs of swimmers and athletes. Strategic partnerships with retailers ensure prominent shelf placement and promotional visibility.

MARKET SEGMENTATION

This research report on the US sunscreen market has been segmented and sub-segmented based on product type, broad spectrum coverage, water resistance, application form & region.

By Product Type

- Lotions

- Creams

- Gels

- Sprays

- Sticks

- Others

By Broad Spectrum Coverage

- UVA Only

- UVB Only

- UVA/UVB

By Water Resistance

- Not Water Resistant

- Water Resistant (40-80 minutes)

- Very Water Resistant (80+ minutes)

By Application Form

- Roll-On

- Pump

- Tube

- Aerosol

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. sunscreen market?

Increasing awareness about skin cancer, rising skincare consciousness, and growing outdoor recreational activities are major growth drivers.

2. What are the main types of sunscreen products?

The market includes mineral sunscreens, chemical sunscreens, tinted sunscreens, water-resistant products, and SPF moisturizers.

3. Why is SPF important in sunscreen products?

SPF indicates the level of protection a sunscreen provides against UVB rays that can cause sunburn and skin damage.

4. Which ingredients are commonly used in sunscreens?

Common ingredients include zinc oxide, titanium dioxide, avobenzone, octocrylene, and oxybenzone.

5. What is the difference between mineral and chemical sunscreen?

Mineral sunscreens physically block UV rays using natural minerals, while chemical sunscreens absorb UV radiation and convert it into heat.

6. Which distribution channels are important in the market?

Pharmacies, supermarkets, beauty stores, online platforms, and dermatology clinics are major distribution channels.

7. What challenges does the sunscreen market face?

Regulatory restrictions on ingredients, product recalls, and concerns over chemical safety are key challenges.

8. What trends are shaping the U.S. sunscreen market?

Multifunctional skincare products, clean-label formulations, spray sunscreens, and high-SPF products are major trends.

9. How is the beauty industry supporting market growth?

The growing skincare and cosmetics industry is increasing demand for sunscreens integrated with moisturizers and makeup products.

10. What is the future outlook for the U.S. sunscreen market?

The market is expected to witness strong growth due to rising skin health awareness, product innovation, and demand for premium sun care products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com