U.S Textile Market Size, Share, Growth, Trends & Analysis Research Report, Segmented By Raw Material, Product, Application, And By Country (The U.S, Canada, Mexico and Rest of North America), Industry Analysis From 2026 to 2034

U.S Textile Market Size

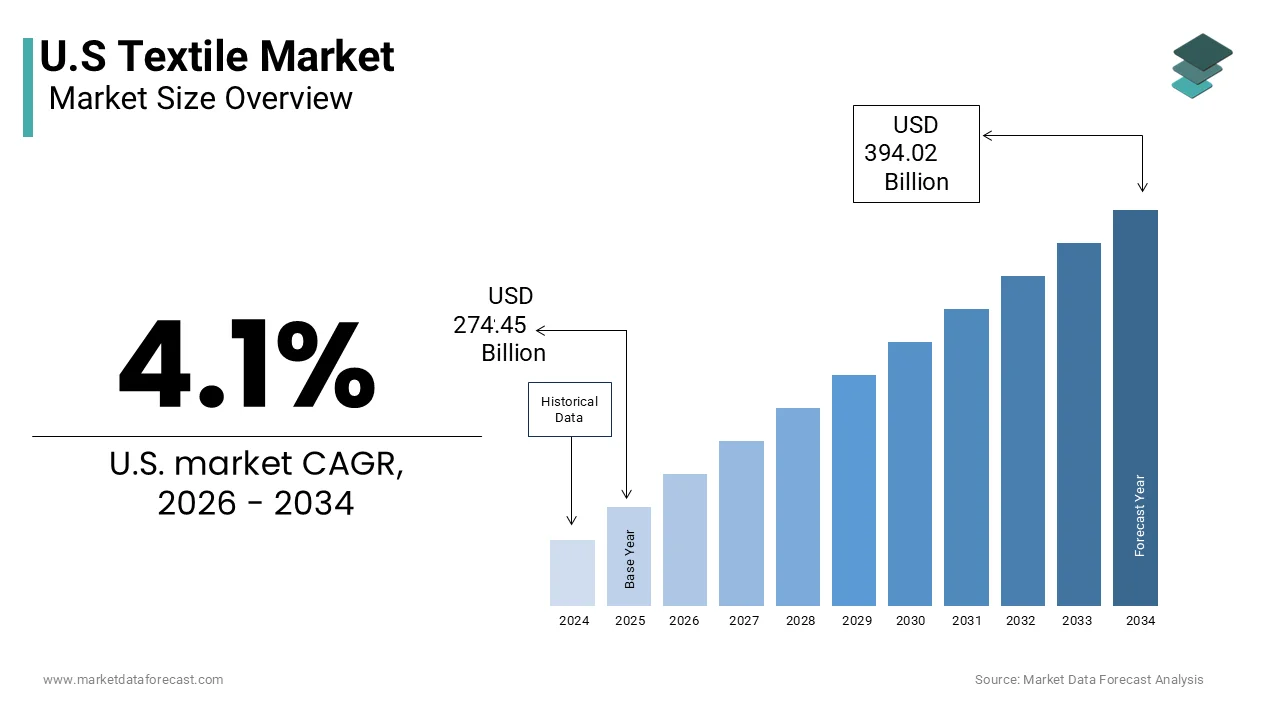

The U.S textile market size was valued at USD 274.45 billion in 2025 and is anticipated to reach USD 285.70 billion in 2026 and USD 394.02 billion by 2034, growing at a CAGR of 4.1% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

A textile is any flexible material made from natural or synthetic fibers, typically by weaving, knitting, or felting. This broad term includes raw fibers and yarns, as well as the resulting fabrics. The textiles manufacturing isa traditional method evolving into a high-value, technology-integrated sector, which includes technical fabrics, defense textiles, medical nonwovens, and advanced composites. Textiles serve a wide range of purposes, from basic uses like clothing, bedding, and home furnishings to highly technical applications. For instance, specialized or "technical textiles" are engineered for specific functions, such as medical dressings, protective gear, and automotive interiors. They are a fundamental part of everyday life and industry. As per the Data from the Bureau of Labor Statistics (BLS) and industry reports, such as a USFIA analysis citing the U.S. Census Bureau, indicate that total employment across the textile and apparel manufacturing sectors is around 270,700. The structural pivot redefines textiles not as a sunset industry but as a significant materials platform embedded in national infrastructure, defense, and health systems.

MARKET DRIVERS

Reshoring of Critical Supply Chains for National Security and Resilience

The rising production of mission-critical materials, which is being enhanced by the federal mandatory policies, is significantly escalating the growth of the US Textile Market. According to the Department of Defense’s Industrial Base Analysis, most of the uniforms, body armor, and tentage for U.S. armed forces must now be sourced from domestic mills under modernized Berry Amendment protocols. As per the Federal Emergency Management Agency’s 2023 Strategic National Stockpile replenishment program, which allocated millions for domestically produced medical gowns and N95-grade filtration textiles, which is an increase from pre-pandemic levels. Simultaneously, various sources designated flame-resistant workwear and chemical protective suits as “critical infrastructure items,” requiring 75% U.S. content by 2029. This policy-driven demand creates a volume floor insulated from global price competition and fast fashion cycles.

Consumer and Corporate Shift Toward Traceable, Sustainable Fiber Systems

The verifiable environmental and ethical provenance, which is anchored in regulatory frameworks and brand ESG commitments, is enhancing the demand for the US Textile Market growth 2023 Global Lifestyle Monitor survey reported that globally, sustainability has a strong or moderate influence on clothing purchases for consumers in various countries. For instance, 74% of Chinese consumers were influenced by sustainability, and 73% of Italian consumers were as well. As per the U.S. Federal Trade Commission’s Green Guides, enforcement actions increased in 2023, by penalizing unsubstantiated “eco-friendly” claims and pushing brands toward third-party verified supply chains like U.S. Cotton Trust Protocol. For Instance, the Securities and Exchange Commission’s proposed climate disclosure rules compel public apparel firms to map Scope 3 emissions, 68% of which originate in upstream textile manufacturing. This regulatory and reputational pressure funnels procurement toward transparent, domestically anchored fiber systems.

MARKET RESTRAINTS

Chronic Shortage of Skilled Technical Labor in Advanced Textile Manufacturing

The U.S. textile industry faces a structural workforce deficit that constrains capacity expansion and technology adoption, which is significantly restraining the expansion of the U.S. textile Market. According to the National Council for Advanced Manufacturing, nearly half of the U.S. textile technicians are over age 55, with only 12% of new hires possessing certifications in digital knitting, nonwoven lamination, or composite weaving, which is hindering the market growth. As per the Bureau of Labor Statistics reports, vacancy rates for textile machine operators exceed 18,% the highest among all manufacturing subsectors. For Instance, the Manufacturing Institute’s 2023 Skills Gap Analysis reveals that more than half of the U.S. technical textile firms delay equipment upgrades due to a lack of trained personnel to operate automated looms and plasma coating systems. This human capital deficit throttles innovation velocity and forces reliance on legacy processes, which is undermining competitiveness in high-margin technical segments.

Regulatory Fragmentation and Compliance Cost Inflation

The textile manufacturers navigate an increasingly complex web of overlapping federal, state, and international compliance mandates that inflate operational costs and delay market entry, leading to limited growth of the US Textile Market. According to the Environmental Protection Agency’s 2023 Sector Compliance Report, U.S. textile mills must adhere to distinct regulatory frameworks from PFAS restrictions under TSCA to California’s Proposition 65 labeling for dye metabolites. According to the American Apparel & Footwear Association, estimates compliance adds per linear yard for performance fabrics, which is eroding margins in price-sensitive segments. Simultaneously, the U.S. Customs and Border Protection’s enforcement of the Uyghur Forced Labor Prevention Act increased detention rates for imported textile inputs in 2023, by forcing domestic mills to audit entire upstream chains. This regulatory friction disincentivizes material innovation and penalizes small and mid-sized producers lacking legal infrastructure.

MARKET OPPORTUNITIES

Integration of Smart and Functional Textiles into Industrial and Medical Applications

The convergence of material science and embedded electronics is unlocking premium markets for textiles that sense, respond, and communicate, creating growth opportunities for the US Textile Market. According to the Advanced Textiles Association, U.S. production of smart textiles for healthcare and defense grew in 2023, including ECG-monitoring garments and temperature-regulating combat uniforms. As per the National Institutes of Health, it funded millions in 2023 for research into antimicrobial wound dressings and biosignal-integrated bandages, with 14 clinical trials now validating textile-based diagnostics. Simultaneously, the Department of Energy is investing millions in U.S. firms developing phase-change material linings for building insulation textiles, which are projected to reduce HVAC loads. This technological pivot transforms textiles from passive materials to active systems, commanding 3–5x value premiums and long-term government and institutional contracts.

Circular Economy Infrastructure and Recycled Fiber Innovation

The Federal and corporate investment in textile-to-textile recycling is creating a parallel domestic supply chain for post-consumer fiber recovery, which is leading to the prominent growth of the US Textile Market. According to the U.S. Environmental Protection Agency’s 2023 Materials Recovery Report, million tons of post-consumer textiles were collected for recycling, which is an increase from 2021, with tons reprocessed into new yarns and nonwovens. As per the Department of Energy’s REMADE Institute, which allocated $42 million in 2023 to scale enzymatic depolymerization of polyester-cotton blends, by achieving 92% fiber purity in pilot runs. For Instance, the Federal Trade Commission’s updated Textile Recycling Claims Guidelines now enable brands to label garments as “Made with X% Recycled U.S. Textiles,” creating consumer-facing value. This closed-loop infrastructure reduces import dependency, satisfies ESG mandates, and unlocks federal grant funding by positioning U.S. mills as circularity enablers rather than linear producers.

MARKET CHALLENGES

Energy Intensity and Decarbonization Pressure in Wet Processing

Textile finishing, which includes dyeing, scouring, and coating, remains one of U.S. manufacturing’s most energy and water-intensive processes, triggering regulatory and cost headwinds that pose prominent challenges in the growth of the US Textile Market. As per the Environmental Protection Agency, its 2023 Clean Water Act enforcement actions targeted 27 U.S. finishing mills for exceeding effluent limits on chromium and formaldehyde, which is resulting in millions in penalties. For Instance, the Department of Energy’s Industrial Assessment Centers report that most of the U.S. dyehouses operate equipment over 20 years old, which lacks heat recovery or water recirculation. Without capital investment in closed-loop systems, mills face escalating compliance costs, carbon fees, and exclusion from corporate supply chains mandating science-based emissions targets.

Global Logistics Disadvantage for Time-Sensitive Fashion Segments

The U.S. textile producers face structural disadvantages in speed-to-market for trend-driven apparel, where Asian supply chains dominate is creating significant challenges in the US Textile Market. According to a survey, U.S. mills average 8.7 weeks for fabric-to-cut delivery, 3.2 times longer than Vietnam or Bangladesh. According to the National Retail Federation, more than half of fast fashion brands bypass U.S. suppliers for seasonal collections due to inflexible minimum order quantities and a lack of digital print-on-demand infrastructure. As per the Surface Transportation Board reports, inland freight delays for textile shipments increased by around half due to rail congestion and chassis shortages at Gulf ports. This logistical friction relegates U.S. producers to basics, uniforms, and technical niches, which excludes them from high-volume, margin-rich fashion cycles despite superior sustainability credentials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Raw Material, Product, Application, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Hengli Petrochemical Co., Ltd., Shenzhou International Group Holdings Ltd, Toray Industries, Inc., Inditex, Chargeurs SA, Far Eastern New Century Corporation, Sasa Polyester Sanayi A.Ş., Eclat Textile Co., Ltd, TJX Companies, Vardhman Textiles |

SEGMENTAL ANALYSIS

By Raw Material Insights

The chemical fibers segment, such as polyester, nylon, and acrylic, dominated the US Textile Market with the most prominent share across the region. This dominance stems from versatility, cost stability, and performance engineering unmatched by natural counterparts. As per the U.S. Department of Defense’s Logistics Agency, most military uniforms and tactical gear utilize high-tenacity polyester blends for moisture-wicking, abrasion resistance, and color fastness under extreme conditions. According to the National Institute for Occupational Safety and Health (NIOSH), part of the Centers for Disease Control and Prevention (CDC), sets the performance standards and certifies N95 respirators. The FDA also regulates N95s for medical use, consuming thousands of tons annually. This institutional reliance, coupled with automotive and geotextile sectors demanding UV-stable synthetics, entrenches chemical fibers as non-substitutable industrial inputs.

The

The

Recycled Chemical Fibers segment, primarily rPET and chemically depolymerized nylon, is expected to expand at a 18.7% CAGR between 2025 and 2033 in the U.S. Textile Market. The segment growth is propelled by federal circular economy mandates and corporate ESG procurement: for instance, the Department of Energy’s REMADE Institute announced $19.6 million in new technology research, selecting 14 new research, development, and demonstration projects in 2023. According to the U.S. Customs and Border Protection, the enforcement of UFLPA incentivizes domestic recycling to avoid supply chain detention, transforming waste streams into strategic, tariff-immune feedstock.

By Product Insights

The Polyester segment led the US Textile Market by capturing a 57.7% share in 2024 across the region. The growth is driven by its dominance in non-apparel and performance-driven applications. As per the Advanced Textiles Association document, most of the U.S.-made airbags, seatbelts, and tire cords utilize high-tenacity polyester due to its tensile strength and fatigue resistance. According to the Department of Energy’s Building Technologies Office, polyester-based radiant barrier textiles were installed in millions of U.S. homes in 2023, which reduced cooling loads on average. For Instance, the Federal Aviation Administration utilizes flame-retardant polyester composites in 100% of commercial aircraft interiors, which consumes thousands of tons annually. This technical indispensability, insulated from fashion cycles, anchors polyester as the material substrate of mobility, safety, and energy efficiency.

Bio-based and Regenerative natural fibers segment, including organic cotton, hemp, and Tencel Lyocel, is growing at 2a 2.3% CAGR from 2025 to 2033 in the US Textile Market. This surge is fueled by federal grants and corporate traceability mandates: for instance, the U.S. Department of Agriculture awarded $2.8 billion in 70 selected projects under the first funding pool for Partnerships for Climate-Smart Commodities. This included a $90 million grant for the U.S. Climate Smart Cotton Program. According to the Federal Trade Commission’s “Green Guides,” enforcement prioritizes third-party certifications like U.S. Regenerative Organic Certified, which is creating premium market access and insulating producers from synthetic price volatility.

By Application Insights

The Technical textiles segment dominated the US Textile Market with a significant share by serving medical, automotive, defense, and construction sectors, which is surpassing household applications due to policy-backed and non-discretionary demand. As per the Centers for Disease Control and Prevention, U.S. hospitals consumed billions of procedure gowns and around a billion surgical drapes in 2023, with 92% made from domestically produced SMS nonwovens. As per the Department of Transportation’s Federal Highway Administration, which mandates geotextiles in 100% of federally funded roadbed stabilization projects is consuming tons annually. As per NASA’s Artemis program, 14 metric tons of radiation-shielding and micrometeoroid-resistant woven composites were sourced from U.S. mills for lunar habitat modules. This application segment thrives not on consumer trends but on statutory procurement, engineering specifications, and national mission imperatives.

The Household textiles segment is estimated to grow at a 9.4% CAGR between 2025 and 2033 in the US Textile Market, which includes bedding, towels, and upholstery. The segment growth is driven by consumer preference for “Made in USA” provenance and supply chain transparency. As per the Cotton Board’s 2023 Home Textile Tracker report, more than half of U.S. consumers now prioritize domestically made bedding for perceived quality and ethical labor practices, up from 2020. According to the U.S. International Trade Commission, it documented an increase in anti-dumping petitions on imported towels and sheets since 2021, which is triggering tariffs that are reshoring production. Companies like Standard Textile and Springs Creative Products expanded U.S. manufacturing capacity by 34% in 2023 to meet demand from boutique hotels and e-commerce brands marketing traceable, small-batch home goods by transforming household textiles into a high-margin, brand-driven segment.

COUNTRY ANALYSIS

United States Market Analysis

The United States functions not as a volume leader but as a value and standards setter in global textile markets, which is leveraging policy, innovation, and sovereignty imperatives to carve defensible niches. According to the World Trade Organization, the U.S. ranked significantly in global textile exports in 2023, behind China, India, Germany, and Bangladesh, yet it commands the highest average export value per kilogram due to its technical and specialty product mix. As per the U.S. International Trade Commission, most exported U.S. textiles serve defense, aerospace, or medical sectors, markets where compliance, certification, and IP protection outweigh cost. The majority of U.S. textile and apparel exports go to nearby markets, specifically Mexico and Canada, leveraging free trade agreements like USMCA. In 2023, Mexico and Canada accounted for the two largest export destinations for U.S. textiles. According to the Department of Commerce’s Bureau of Industry and Security restricts the export of 17 advanced textile technologies under EAR controls, which is reinforcing strategic advantage. Unlike mass-market exporters, the U.S. competes on embedded innovation, regulatory alignment, and mission-critical reliability, which is exporting not fabric, but engineered solutions with sovereign assurance.

COMPETITIVE LANDSCAPE

Competition in the U.S. Textile Market is defined by technical sovereignty, regulatory alignment, and embedded sustainability rather than cost or volume. Players compete to position their materials as certified, compliant, and mission-critical within Asia Pacific’s industrial, healthcare, and construction ecosystems. Differentiation stems from chain-of-custody transparency, co-engineered performance attributes, and adherence to overlapping U.S. and Asian environmental standards. With regional governments mandating green building codes and circular procurement, U.S. firms compete as enablers of compliance by exporting not just fabric but auditable systems. The battlefield has shifted from low speed to lifecycle credentials, making competition a contest of certification, co-innovation, and policy fluency, not commodity pricing.

KEY MARKET PLAYERS

A few of the market players in the U.S textiles market include

- Hengli Petrochemical Co., Ltd.

- Shenzhou International Group Holdings Ltd

- Toray Industries, Inc.

- Inditex

- Chargeurs SA

- Far Eastern New Century Corporation

- Sasa Polyester Sanayi A.S.

- Eclat Textile Co. Ltd

- TJX Companies

- Vardhman Textiles

Top Players in the Market

Milliken & Company leverages its advanced material science to supply performance fabrics and nonwovens across the regional automotive, healthcare, and architecture sectors. In 2023, Unifi was involved in other textile innovations and sustainability initiatives. A key announcement in late 2023 was the expansion of their REPREVE product offerings to include biodegradable additives. It also established a technical center in Seoul to support Korean EV manufacturers with battery insulation textiles. These moves embed Milliken as a solutions innovator, aligning its sustainability and safety credentials with Asia’s green infrastructure and electrification mandates.

Unifi Manufacturing, Inc. exports U.S.-made recycled and specialty yarns to the United States through strategic licensing and regional blending hubs. Unifi's subsidiary in China, Unifi Textiles (Suzhou) Co., Ltd., was designated to manage the sales and distribution of REPREVE exported from Vietnam. This structure shows that Unifi works with licensed partners and intermediaries in the region. In Q1 2024, Unifi focused on its own sustainability reports and initiatives, such as expanding its portfolio of circular polyester products and launching new offerings like biodegradable yarn technology. Simultaneously, it opened a color-matching lab in Dhaka to accelerate sampling for Bangladeshi knitwear exporters. These initiatives position Unifi not as a bulk supplier but as a compliance enabler, which is helping Asian manufacturers satisfy Western ESG audits while reducing lead times and enhancing premium fiber differentiation in global supply chains.

Shaw Industries, a leader in performance flooring and contract textiles, is extending U.S. design and sustainability standards into regional commercial real estate and hospitality sectors. In early 2024, Shaw launched “Cradle to Cradle Platinum” certified hospitality collections tailored for Japanese ryokan renovations and Korean wellness resorts. It also partnered with India’s Godrej Interio to adapt U.S. acoustic textile panels for high-density urban workspaces. These actions embed Shaw’s lifecycle design philosophy into the regional built environment, transforming its brand into a licensable standard for sustainable commercial interiors across the region’s booming urban corridors.

Top Strategies Used By the Key Market Participants

Key players deploy circular material certification, regional technical co-development, digital traceability integration, policy-aligned product adaptation, and trans-Pacific IP licensing to fortify market positioning. They embed third-party verified recycled content claims to satisfy Asia’s tightening green public procurement rules. Strategic joint development with local manufacturers ensures compliance with regional fire and chemical safety codes. Blockchain-enabled traceability reduces audit friction for export-oriented factories. Product lines are reformulated to meet Asia-specific humidity, UV, and acoustic performance standards. Licensing of U.S. textile patents and manufacturing processes enables local production without diluting quality, which is transforming American innovation into embedded regional infrastructure.

RECENT MARKET NEWS

- In January 2024, Shaw Contract announced the "Teamwork" collection, a low-carbon carpet tile for the Asia-Pacific (APAC) market, which aligns with modern workspace design. In May 2024, the company also organized a "Global Day for People + Planet" in multiple Indian cities.

- In April 2024, Unifi Manufacturing announced the launch of REPREVE yarn enhanced with CiCLO technology, a biodegradable additive designed to reduce microplastic pollution.

- In late 2024, FENC was recognized as an industry leader in sustainability, with an emphasis on its own net-zero goals and financial instruments.

MARKET SEGMENTATION

This research report on the U.S textiles market is segmented and sub-segmented into the following categories.

By Raw Material Type

- Cotton

- Chemical

- Wool

- Silk

- Others

By Product Type

- Natural Fibers

- Polyesters

- Nylon

- Others

By Application Type

- Household

- Bedding

- Kitchen

- Upholstery

- Towel

- Others

- Technical

- Construction

- Transport

- Medical

- Protective

- Fashion & Clothing

- Apparel

- Ties & Clothing

- Handbags

- Others

- Others

By Country

- USA

- Canada

- Mexico

Frequently Asked Questions

What are the key drivers of the U.S. textiles market today?

Reshoring of manufacturing, demand for performance and technical textiles (e.g., medical, automotive, protective gear), and rising consumer preference for sustainable and traceable fabrics are reshaping the industry beyond traditional apparel.

How is sustainability influencing textile production in the U.S.?

Brands and mills are increasingly adopting recycled fibers (like rPET), waterless dyeing technologies, and circular design principles—driven by ESG commitments, federal incentives, and state laws like California’s Textile Waste Prevention Act.

Which textile segments are growing the fastest?

Technical and industrial textiles—used in filtration, geotextiles, healthcare, and defense—are outpacing apparel due to high-value applications and government investment in domestic supply chain resilience.

What role does nearshoring play in the current market?

Geopolitical risks and pandemic-era disruptions have accelerated nearshoring from Asia to the U.S. and Mexico, especially for defense, medical, and critical infrastructure textiles under initiatives like the Berry Amendment and CHIPS Act spillovers.

Who are the major players in the U.S. textiles sector?

Leading companies include Milliken & Company, Glen Raven, Inc., W.L. Gore & Associates, and Unifi—firms known for innovation in smart fabrics, sustainability, and vertically integrated manufacturing with strong R&D capabilities.

How is digitalization transforming textile manufacturing?

Automation, AI-driven design, and digital printing are reducing waste, speeding time-to-market, and enabling mass customization—helping U.S. producers compete on agility and quality rather than just cost.

Are natural fibers making a comeback?

Yes—organic cotton, hemp, and Tencel™ are gaining share due to biodegradability and lower environmental impact, though synthetics still dominate performance applications where durability and moisture management are critical.

What are the biggest challenges facing U.S. textile manufacturers?

High energy and labor costs, global competition, inconsistent recycling infrastructure, and complex compliance with evolving chemical and labeling regulations (e.g., PFAS bans) continue to pressure margins and scalability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com