Australia Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Ind5stry Analysis From 2024 to 2033

Australia Cards And Payments Market Size

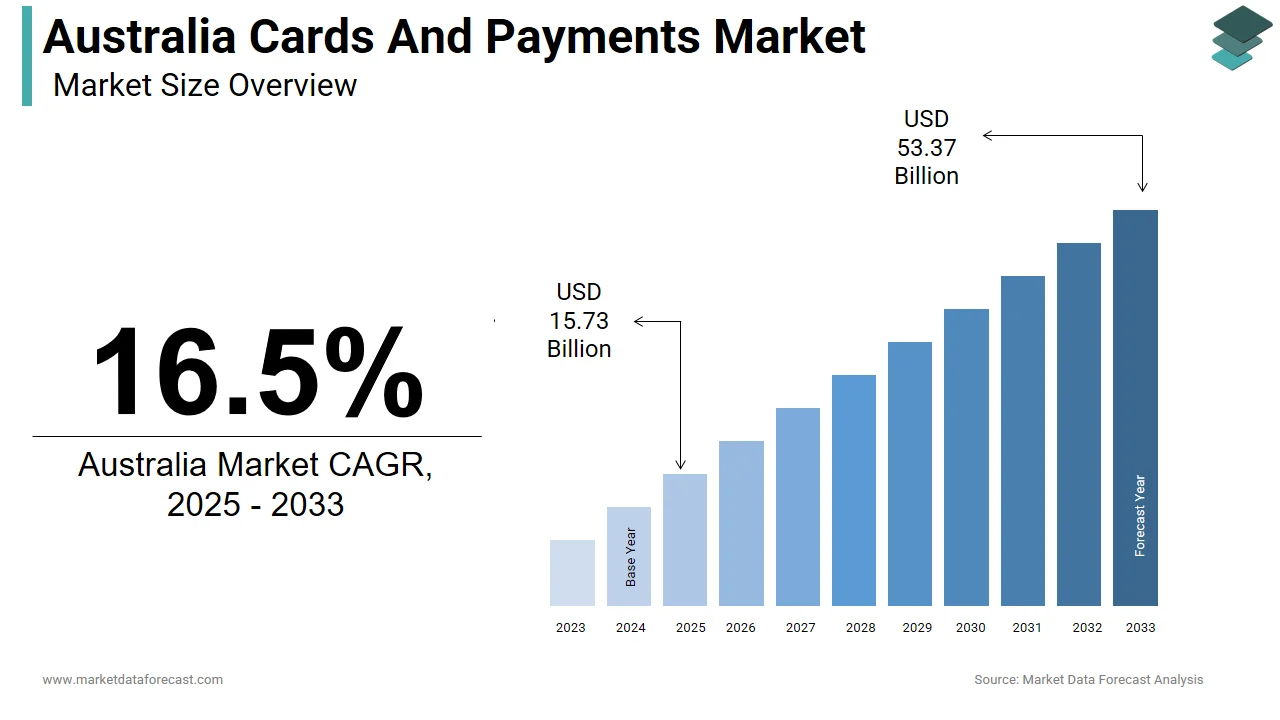

The Australia cards and payments market size was valued at USD 13.5 billion in 2024. This market is expected to grow at a CAGR of 16.5% from 2025 to 2033 and be worth USD 53.37 billion by 2033 from USD 15.73 billion in 2025.

MARKET DRIVERS

High Digital Adoption and Mobile Payment Growth

Australia has seen a significant shift toward digital payments, driven by widespread smartphone usage, strong internet penetration, and growing consumer preference for convenience. According to the Australian Communications and Media Authority (ACMA), 96% of Australians aged 18–64 owned a smartphone, enabling seamless access to mobile payment solutions. The adoption of contactless cards and mobile wallet payments has surged in recent years. The Reserve Bank of Australia (RBA) reported that in 2023, nearly 75% of all card transactions were contactless, with Apple Pay, Google Pay, and Samsung Pay accounting for over 20% of point-of-sale (POS) payments. This growth is supported by banks and fintechs investing heavily in NFC-enabled cards and mobile integration. Consumers are also increasingly using digital wallets for peer-to-peer (P2P) transfers through platforms like Google Pay, PayPal, and Afterpay, which further reinforces the move away from cash.

Expansion of E-commerce and Online Spending

E-commerce growth has been a powerful driver of the cards and payments market in Australia, fueled by rising online shopping activity and increasing trust in digital transactions. This surge in online retail spending has directly boosted card usage, particularly credit and debit cards, which remain the most preferred payment method for digital purchases. AusPayNet reported that in 2023, card payments accounted for 68% of all online transactions, with Visa and Mastercard leading the market share. Also, the Australian Bureau of Statistics (ABS) found that nearly 80% of adults made at least one online purchase in 2023, reinforcing the need for secure and efficient digital payment options. As cross-border e-commerce grows, particularly with international retailers entering the Australian market, the demand for multi-currency and global card acceptance continues to rise, further strengthening the cards and payments ecosystem.

MARKET RESTRAINTS

Declining Use of Physical Cards Due to Embedded Finance and Super Apps

Despite high digital payment adoption, the traditional card issuance model in Australia is facing a decline due to the rise of embedded finance and super apps that integrate payment functionalities directly into non-financial platforms. Consumers are increasingly opting for seamless in-app payment experiences rather than carrying or using physical cards. According to McKinsey’s 2023 Global Payments Report, Australia experienced a 6.3% drop in new card issuance in 2023 compared to the previous year, primarily attributed to the growing popularity of tokenized and app-based payment methods. A Deloitte 2023 survey revealed that 37% of millennials and Gen Z consumers rarely use their physical debit cards, preferring to transact via mobile wallets or embedded financial tools. Banks are also reporting lower card activation rates. For instance, Commonwealth Bank of Australia (CBA) noted in Q4 2023 that only 72% of newly issued cards were activated within the first month, down from 85% in 2021.

Regulatory Compliance and Data Privacy Challenges

Australia's financial sector operates under a complex regulatory framework that includes stringent data protection laws and financial compliance requirements, posing a restraint on the cards and payments market. The Privacy Act 1988, along with the Notifiable Data Breaches (NDB) Scheme, mandates strict handling of personal and financial data, increasing operational complexity for fintech firms and banks alike. In addition, the implementation of Open Banking regulations under the Consumer Data Right (CDR) has increased liability for fraud and required additional layers of authentication, sometimes slowing transaction speeds and affecting user experience. A 2023 report by the Australian Competition and Consumer Commission (ACCC) found that smaller payment service providers faced an average compliance cost increase of 14% post-CDR, limiting their ability to compete with larger players.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

Australia is a global leader in the Buy Now, Pay Later (BNPL) industry, offering a major opportunity for the cards and payments market. BNPL allows consumers to split purchases into interest-free installments, aligning with the spending habits of millennials and Gen Z, who prefer flexible payment options over traditional credit cards. Leading domestic players like Afterpay (now part of Block Inc.) and Zip Co have expanded their services across major retailer,s including Kmart, David Jones, and Amazon Australia, integrating seamlessly into online checkout systems. According to AusPayNet, more than 30% of online merchants now offer BNPL as a payment option, reflecting growing merchant acceptance. Banks and card issuers can leverage this trend by partnering with BNPL providers to embed installment features into existing card products, thereby enhancing customer engagement and boosting transaction volumes while meeting evolving consumer finance demands.

Rise of Real-Time Payments and Instant Transfer Systems

Australia’s real-time payments infrastructure, powered by the New Payments Platform (NPP), offers a transformative opportunity for the cards and payments market. Launched in 2018, the NPP enables instant, 24/7 fund transfers between individuals and businesses using just a payee’s email or phone number. According to Payments Australia, in 2023, the NPP processed over 1.4 billion transactions, with a total value exceeding AUD 220 billion, representing a year-on-year growth of 28%. This system supports faster settlements, improving liquidity management for businesses and encouraging more digital transactions. Banks such as Westpac, ANZ, and Commonwealth Bank have integrated NPP into their mobile banking apps, allowing customers to make immediate transfers without relying on traditional card-based systems. Additionally, the Reserve Bank of Australia (RBA) is exploring the introduction of a wholesale central bank digital currency (CBDC), which could further enhance real-time settlement capabilities. As real-time payments become more prevalent, they provide a complementary alternative to card transactions, especially in peer-to-peer (P2P) and small business payments. This evolution opens up new avenues for financial institutions to innovate and expand their digital offerings beyond traditional card-based models.

MARKET CHALLENGES

Rising Cybersecurity Threats and Payment Fraud Incidents

Australia's advanced digital payments ecosystem makes it an attractive target for cybercriminals, leading to a sharp rise in fraud incidents and cybersecurity threats. According to the Australian Cyber Security Centre (ACSC), in 2023, there were over 94,000 reported cybercrime incidents, with online payment fraud accounting for nearly 34% of these cases. The Australian Payments Network (AusPayNet) reported that CNP fraud losses totaled AUD 268 million in 2023, representing a year-on-year increase of 16%. Phishing scams, malware attacks, and data breaches have contributed to declining consumer confidence in digital payments, especially among older users. Furthermore, Europol’s 2023 Internet Organised Crime Threat Assessment (IOCTA) identified Australia as a key node in transnational cybercrime networks, often exploited due to its high-value financial infrastructure and dense digital economy. To mitigate risks, financial institutions must invest in advanced fraud detection technologies such as AI-driven analytics, biometric verification, and end-to-end encryption, which could increase operational costs and impact transaction speed.

Uneven Digital Payment Adoption across Regional and Demographic Segments

While urban centers like Sydney and Melbourne exhibit high levels of digital payment adoption, disparities persist in regional and rural areas, hindering the uniform growth of the cards and payments market. This digital divide affects both consumers and merchants. Many small businesses in rural Australia still rely on cash due to limited access to POS terminals or unstable internet connections required for card transactions. On the consumer side, ABS data shows that digital payment adoption among residents in regional and remote areas was lower than in metropolitan regions, primarily due to low digital literacy and lack of access to mobile banking services. Addressing this imbalance requires coordinated efforts between the government and the private sector to expand digital infrastructure, provide training, and ensure inclusive access to modern payment solutions across all regions of Australia.

KEY STATISTICS OFFERED

- Existing and future values of debit cards, charge and credit cards, and others in every market of the payment cards industry of Australia.

- Information on the alternative payment options of the country, including the highlights of existing instruments like credit transfers, cheques, direct debit, and cash payments.

- Prospects of the online sales market in the country, along with the focus on different growth drivers and government regulations in the cards and payment industry of the country.

- Various marketing strategies of banking and financial institutions for promoting their payment cards.

MARKET KEY INSIGHTS

The intense competition in the alternative payments market of Australia with options like BPAY, POLi, Paymate and PayPal, and several mobile payment solutions like Google's Android Pay, Samsung's Samsung Pay in partnership with American Express and Citibank, National Australia Bank's (NAB) NAB Pay and ANZ's ANZ Mobile Pay.

The trials for their bank-branded mobile payment apps on Apple smartphones by Commonwealth Bank of Australia (CBA), Westpac, NAB, and Bendigo and Adelaide Bank, and the declined approval from the Australian Competition and Consumer Commission (ACCC).

The growing preference for contactless payments forced many banking and payment providers to launch contactless solutions. Few such initiatives are contactless bands and stickers in the mobile payments of Optus called Cash by Optus, an NFC technology-based Tap & pay service by CBA for Android smartphone users, and the collaboration of Electronic Fund Transfer Point of Sale (EFTPOS) with the contactless payments movement.

KEY MARKET PLAYERS

The major players in the Australia cards and payments market include

- Commonwealth Bank

- Westpac

- ANZ

- National Australia Bank

- Bendigo and Adelaide Bank

- Citibank

- Coles

- Woolworths

- Jetstar

- Qantas

- EFTPOS

AUSTRALIA CARDS AND PAYMENTS MARKET NEWS

- In February 2018, the Reserve Bank of Australia (RBA) and its Payments System Board introduced the New Payments Platform (NPP), facilitating customers with multiple bank accounts to transfer funds and make payments in real-time, promoting digital payments for transactions of even less value. This platform offers services around the clock for all days of the year. Backed by SWIFT, this platform combines 13 members of Australia’s financial services industry and offers PayID, a service that enables customers to transfer funds by simply providing the mobile number or email of the recipient.

- The banking industry of Australia is expected to witness tremendous growth in the future with the advent of digital-only banks. For example, in May 2018, the Australian Prudential Regulation Authority (APRA) granted a Restricted ADI (RADI) license to Volt Bank, allowing it to provide constrained products and services to customers before receiving a full banking license. Xinja, a Fintech startup in Australia, is also planning for a full banking license to extend its wings into complete banking. '86 400', 'Up', and other challenger banks are also going to initiate their services soon.

- However, the introduction of various regulatory policies is expected to limit the growth of the credit card market in Australia in the coming years. A new bill aimed at barring the unethical practices of the credit card provides was passed by the Australian parliament in February 2018. According to this new bill, financial service providers should assess the ability of the customer to repay credit card loans on time, starting from June 2018. In addition, starting from January 2019, there will be a prohibition on the banks' invitations to increase the limit of the credit cards and any reduced calculation of interest. The banks must provide an online option to cancel the cards or reduce the credit limit. The Australian Competition and Consumer Commission (ACCC) has already prohibited the unfair collection of surcharges on the card payments from all businesses that including small and large merchants. This new bill must be followed by all businesses based in Australia or using an Australian bank.

MARKET SEGMENTATION

This research report on the Australia cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What defines the Australia cards and payments market?

The Australia cards and payments market covers debit, credit, prepaid, and digital methods supporting everyday and online transactions across the country.

2. How is the Australia cards and payments market evolving?

The Australia cards and payments market is evolving through wider contactless, mobile, and online adoption, reshaping how consumers and merchants transact.

3. What drives growth in the Australia cards and payments market?

Innovation, online commerce, and user demand for speed and convenience drive the Australia cards and payments market toward more digital first experiences.

4. Who are the key players in the Australia cards and payments market?

Banks, card schemes, fintechs, and payment processors all contribute to products, rails, and services in the Australia cards and payments market.

5. What role do debit cards play in the Australia cards and payments market?

Debit products in the Australia cards and payments market support everyday spending, bill payments, and online purchases linked directly to bank accounts.

6. How important are credit cards in the Australia cards and payments market?

Credit cards in the Australia cards and payments market enable flexible spending, rewards, and travel benefits while competing with newer digital options.

7. How prominent are contactless payments in the Australia cards and payments market?

Tap and pay has become a core behaviour in the Australia cards and payments market, with contactless widely accepted across retail and services.

8. What impact do mobile wallets have on the Australia cards and payments market?

Mobile wallets integrate phones and wearables into the Australia cards and payments market, enabling secure in store and in app payments.

9. How does e commerce affect the Australia cards and payments market?

Online shopping has increased card and digital wallet usage in the Australia cards and payments market, driving demand for secure remote payments.

10. What is BNPL’s role in the Australia cards and payments market?

Buy now pay later services add instalment based flexibility to the Australia cards and payments market, influencing how consumers finance purchases.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com