Global Adhesion Barrier Market Size, Share, Trends & Growth Forecast By Product, Product Form, Surgical Application and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Adhesion Barrier Market Report Summary

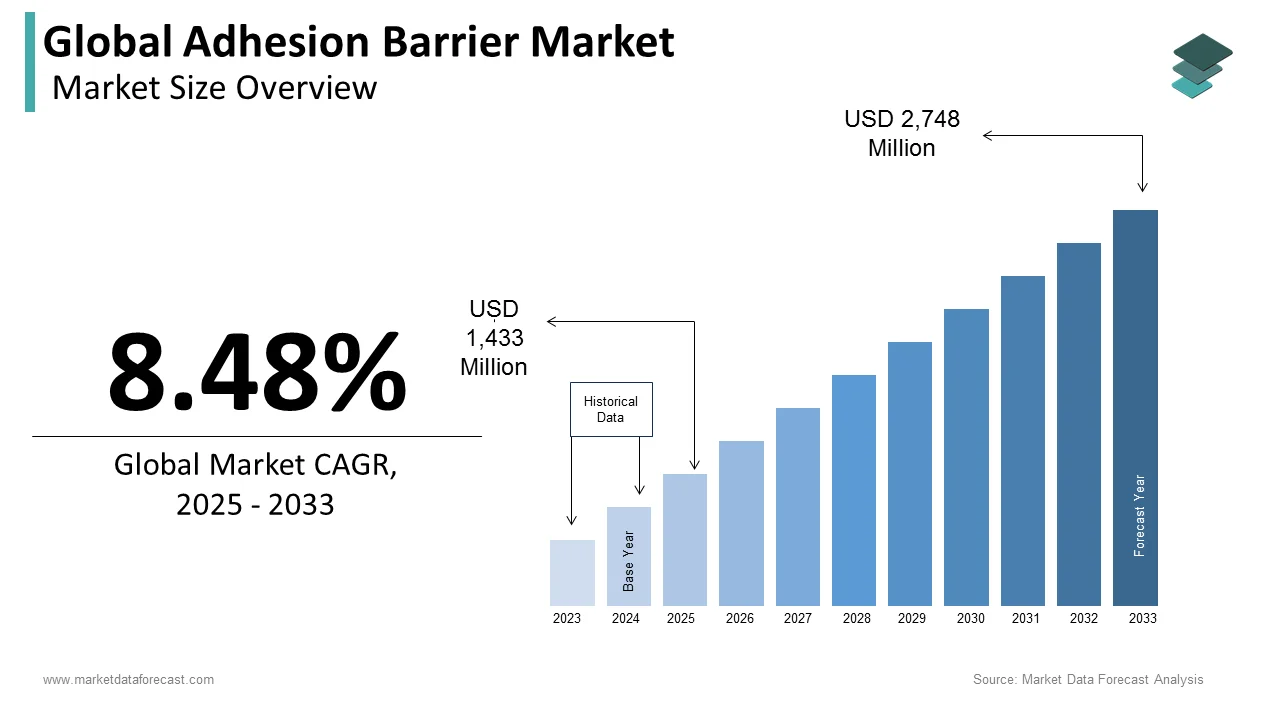

The global adhesion barrier market was valued at USD 1,433 million in 2025 and is projected to grow from USD 1,554.52 million in 2026 to USD 2,981 million by 2034, registering a CAGR of 8.48% from 2026 to 2034. Market growth is driven by the increasing volume of surgical procedures, growing awareness of postoperative complications, and rising adoption of advanced surgical care solutions. Adhesion barriers are widely used to reduce the formation of postoperative adhesions, which can lead to chronic pain, infertility, bowel obstruction, and repeat surgeries. Advancements in biomaterials, increasing preference for minimally invasive procedures, and the growing emphasis on improving surgical outcomes are further supporting market expansion worldwide.

Key Market Trends

- Rising adoption of adhesion prevention products in abdominal and gynecological surgeries.

- Increasing awareness regarding postoperative adhesion-related complications.

- Growing demand for biocompatible and bioresorbable adhesion barrier materials.

- Expansion of minimally invasive and laparoscopic surgical procedures.

- Continuous innovation in synthetic and next-generation adhesion barrier technologies.

Segmental Insights

- Based on product, the synthetic adhesion barriers segment dominated the global adhesion barrier market in 2025 by accounting for 62.1% market share, driven by their consistent manufacturing quality, predictable resorption characteristics, and extensive clinical validation across multiple surgical specialties.

- Based on product form, the film segment led the market by capturing 48.3% share in 2025, supported by ease of application, effective tissue separation, and widespread utilization in various surgical procedures.

- Based on surgical application, the general and abdominal surgeries segment held the largest share of 35.8% in 2025, owing to the high incidence of postoperative adhesion formation in abdominal surgical interventions and the growing adoption of preventive measures.

Regional Insights

The global adhesion barrier market is witnessing significant growth across major regions, supported by increasing surgical volumes, technological advancements, and growing focus on patient safety.

- North America dominated the global market in 2025 with 40.6% share, driven by advanced healthcare infrastructure, high procedural volumes, strong adoption of surgical innovation, and increasing awareness of adhesion prevention strategies.

- Europe held the second-largest position with 30.2% share in 2025, supported by favorable healthcare systems, increasing use of minimally invasive surgeries, and growing emphasis on reducing postoperative complications.

- Asia-Pacific is projected to register the fastest growth during the forecast period, driven by rapid healthcare infrastructure development, rising surgical procedure volumes, and increasing awareness regarding surgical safety and patient outcomes.

Competitive Landscape

The global adhesion barrier market is characterized by the presence of established medical device manufacturers and biotechnology companies focusing on innovative adhesion prevention solutions and advanced biomaterials. Market participants are investing in product development, clinical research, and strategic collaborations to enhance product efficacy and expand their market presence. Continuous advancements in synthetic barrier technologies, bioresorbable materials, and surgical applications are shaping competitive dynamics across the market.

Prominent companies operating in the global adhesion barrier market include Baxter International Inc., Medtronic Plc., Johnson & Johnson Services Inc., C. R. Bard, Inc., Johnson & Johnson, Sanofi Group, Atrium Medical Corporation, Integra LifeSciences Corporation, Anika Therapeutics Inc., FzioMed, Inc., and MAST Biosurgery AG.

Global Adhesion Barrier Market Size

The global adhesion barrier market was worth US$ 1,433 million in 2025 and is anticipated to reach a valuation of US$ 2,981 million by 2034 from US$ 1,554.52 million in 2026, and it is predicted to register a CAGR of 8.48% during the forecast period 2026 to 2034.

An adhesion barrier is a temporary physical film, fabric, or gel placed between layers of tissue during surgery. These barriers act as physical or chemical separators during the critical healing phase, reducing the risk of postoperative adhesions, which can lead to chronic pain, bowel obstruction, and infertility. The clinical significance of this technology is underscored by the high prevalence of adhesion-related complications in abdominal and pelvic surgeries. According to the National Institutes of Health (NIH) StatPearls registry, postoperative peritoneal adhesions develop in approximately 90% of patients after open abdominal surgery. Additionally, longitudinal studies published by the National Center for Biotechnology Information (NCBI) indicate that these internal scars lead to at least one hospital readmission for one-third (33%) of those patients within the subsequent 10 years. This widespread occurrence creates a substantial clinical need for effective preventive measures. The aging global population further amplifies demand, as older individuals are more likely to require multiple surgical interventions. As documented by the World Health Organization (WHO) Ageing and Health Fact Sheet, the world's population of people aged 60 years and older is expected to double to 2.1 billion by 2050. This demographic shift is projected to increase the global proportion of older individuals from 1 in 8 people to 1 in 5 people, placing unprecedented demands on health and social care systems globally. Additionally, the rise in minimally invasive procedures such as laparoscopy has heightened awareness of adhesion prevention, as these techniques still carry significant risks despite smaller incisions. Regulatory bodies like the United States Food and Drug Administration continue to refine approval pathways for novel bioresorbable materials, encouraging innovation in polymer-based and hydrogel formulations. The integration of these barriers into standard surgical protocols reflects a growing recognition of their role in improving patient outcomes and reducing long-term healthcare costs associated with adhesion-related morbidity.

MARKET DRIVERS

Increasing Volume of Abdominal and Pelvic Surgeries Drives Demand

The escalating frequency of abdominal and pelvic surgical procedures fuels the growth of the adhesion barrier market. These interventions carry the highest risk of postoperative complication formation. General surgeries, including colorectal resections, hysterectomies, and appendectomies, involve extensive tissue manipulation that triggers the body’s natural healing response, often resulting in unwanted fibrous connections. According to data from the Agency for Healthcare Research and Quality (AHRQ) HCUP Statistical Brief, approximately 14.4 million operating room procedures are performed during inpatient stays annually in the United States. Furthermore, figures from the American College of Surgeons highlight that a substantial portion of these include major abdominal entries, with roughly 4 million laparotomies performed nationwide each year. The rising incidence of conditions such as endometriosis, uterine fibroids, and colorectal cancer further contributes to this surgical volume. As stated by the World Health Organization (WHO), endometriosis is a chronic disease that affects an estimated 10% of reproductive-age women and girls globally. Because the condition commonly leads to severe pelvic pain and infertility, clinical guidelines emphasize that surgical interventions must focus heavily on minimizing postoperative adhesions to safely preserve reproductive health. Similarly, the prevalence of colorectal cancer continues to rise, with the American Cancer Society estimating over 150000 new cases in the United States in 2025, many requiring complex resections. Surgeons are increasingly recognizing that preventing adhesions during the initial operation is more effective and cost-efficient than managing complications later. This shift in clinical mindset drives the routine use of barrier products in operating rooms. Hospitals and surgical centers are incorporating these devices into standard care pathways to improve quality metrics and reduce readmission rates. The direct correlation between surgical volume and adhesion risk ensures sustained demand for reliable and easy-to-apply barrier solutions across diverse medical specialties.

Growing Awareness of Long-Term Complications Influences Clinical Practice

Heightened awareness among healthcare providers and patients regarding the severe long-term consequences of postoperative adhesions is significantly influencing clinical decision-making and driving the growth of the global adhesion barrier market. Adhesions are not merely minor scar tissue but can lead to debilitating conditions such as small bowel obstruction, chronic pelvic pain, and secondary infertility, which profoundly impact quality of life. According to data from the National Institutes of Health, adhesive small bowel obstruction accounts for approximately 60 to 75 percent of all small bowel obstruction cases in developed countries, often requiring emergency reoperation. These secondary surgeries are complex, risky, and expensive, placing a substantial burden on healthcare systems. Patient advocacy groups and medical societies are actively educating stakeholders about these risks, prompting a proactive approach to prevention. Women undergoing gynecological surgeries are particularly concerned about fertility preservation, leading to increased demand for adhesion barriers during procedures like myomectomy and ovarian cystectomy. The economic argument for prevention is also compelling, as studies indicate that the cost of treating adhesion-related complications far exceeds the price of preventive barriers. Insurance providers and hospital administrators are beginning to recognize the value proposition, supporting broader reimbursement policies. This comprehensive understanding of the clinical and economic implications encourages surgeons to adopt adhesion barriers as a standard of care rather than an optional adjunct. The shift from reactive treatment to preventive strategy marks a pivotal change in surgical practice that sustains market expansion.

MARKET RESTRAINTS

High Cost of Advanced Barrier Products Limits Accessibility

The substantial financial burden associated with advanced barrier products limits the penetration of the adhesion barrier market. This restriction is particularly visible in cost-conscious healthcare environments and developing regions. Premium barrier devices such as hyaluronic acid-based gels and oxidized regenerated cellulose sheets often command high prices due to complex manufacturing processes and rigorous regulatory compliance requirements. According to healthcare expenditure studies, the cost of a single application of a high-end adhesion barrier can range from several hundred to over a thousand dollars, adding considerable expense to surgical procedures. In many healthcare systems, especially those with fixed reimbursement rates or limited budgets, these additional costs are difficult to justify without clear, immediate financial returns. While the long-term savings from prevented complications are evident, the upfront expenditure remains a barrier for many hospitals and surgical centers. Public healthcare facilities in lower-income countries often prioritize essential life-saving equipment over preventive adjuncts, limiting market access. Furthermore, inconsistent reimbursement policies across different insurance providers create uncertainty for healthcare providers, discouraging routine use. Some payers still classify adhesion barriers as experimental or investigational, denying coverage and forcing patients to bear out-of-pocket costs. This financial friction slows adoption rates even when clinical evidence supports efficacy. Manufacturers face pressure to demonstrate clear cost-effectiveness through robust health economic studies, but the complexity of tracking long-term outcomes makes this challenging. Cost will remain a critical impediment to widespread utilization. This will hold true until pricing structures become more accessible or reimbursement becomes universal.

Lack of Standardized Guidelines and Surgeon Preference Variability

The absence of universally standardized clinical guidelines for the use of these barriers leads to significant variability in surgeon preference and adoption rates, which hampers the consistent expansion of the adhesion barrier market. Unlike mandatory safety protocols, the application of adhesion barriers is often left to the discretion of the individual surgeon, resulting in inconsistent usage patterns across institutions and specialties. According to national surveys published in peer-reviewed journals such as Digestive Surgery, there is a significant lack of consensus regarding adhesion prevention, with approximately 40% to 60% of surveyed surgeons indicating they rarely or never use barrier products due to doubts concerning their efficacy and difficulties with intraoperative handling. This lack of consensus creates confusion and hinders the establishment of best practices. Training and familiarity play crucial roles, as surgeons are more likely to use products they have been trained on and trust. However, the rapid introduction of new materials and formats requires continuous education, which is not always readily available. Some surgeons express concerns about potential interference with wound healing or increased operative time, despite evidence to the contrary. The variability in surgical technique and patient anatomy further complicates the selection of the most appropriate barrier. Without strong endorsements from major medical associations mandating or strongly recommending their use in specific procedures, adoption remains fragmented. This subjective decision-making process limits the predictability of demand and prevents the market from achieving its full potential, as many eligible patients do not receive preventive care due to provider hesitation or habit.

MARKET OPPORTUNITIES

Development of Bioresorbable and Next-Generation Materials Offers Growth Potential

The continuous innovation in bioresorbable and next-generation adhesion barrier materials offers a significant opportunity for global market expansion. This addresses limitations of existing products. Traditional barriers sometimes pose challenges related to ease of application stability in wet environments or potential inflammatory responses. Newer formulations utilizing advanced polymers, hydrogels, and composite materials offer improved adherence, flexibility, and biocompatibility. According to research published in biomedical engineering journals, next-generation hydrogel barriers can conform better to irregular tissue surfaces and maintain integrity during the critical healing window before safely absorbing into the body. These advancements enhance surgeon confidence and user experience, encouraging broader adoption. The development of sprayable barriers allows for minimally invasive application during laparoscopic and robotic surgeries, which are becoming increasingly prevalent. This compatibility with modern surgical techniques opens new avenues for product integration. Furthermore, the incorporation of therapeutic agents such as anti-inflammatory drugs or antibiotics into barrier matrices offers multifunctional benefits that appeal to clinicians seeking comprehensive solutions. Regulatory agencies are showing willingness to expedite approvals for innovative materials that demonstrate superior safety profiles. Companies investing in research and development can differentiate themselves in a crowded market by offering unique value propositions. The trend toward personalized medicine also supports the creation of tailored barrier solutions for specific patient populations. Manufacturers can capture market share from older technologies by focusing on material science breakthroughs. This allows them to expand into underserved surgical specialties.

Expansion into Emerging Markets With Growing Healthcare Infrastructure

The rapid development of healthcare infrastructure in emerging nations across the Asia Pacific, Latin America, and the Middle East opens the door for the expansion of the adhesion barrier market. Countries such as China, India, Brazil, and Saudi Arabia are investing heavily in modernizing their hospital facilities and increasing access to advanced surgical care. Projections from the World Bank indicate that government health expenditure in lower-middle-income countries is expected to grow by approximately 17% through 2030, driven by rising national incomes and efforts to achieve universal health coverage, though total spending per capita remains a fraction of that in high-income nations. As the number of skilled surgeons and equipped operating rooms increases, so does the volume of complex surgical procedures that benefit from adhesion prevention. Local manufacturing partnerships and strategic alliances with global players can facilitate market entry by reducing costs and navigating regulatory landscapes. The growing middle class in these regions is increasingly aware of quality healthcare options and is willing to pay for premium medical devices that improve outcomes. Government programs aimed at reducing surgical complications and healthcare costs provide a favorable policy environment for adopting preventive technologies. Educational initiatives and training programs for local surgeons can drive awareness and acceptance of adhesion barriers. By tailoring products to meet the specific needs and budget constraints of these markets, companies can unlock significant growth potential. The untapped patient population in these regions represents a vast reservoir of future demand as healthcare standards converge with global best practices.

MARKET CHALLENGES

Regulatory Hurdles and Lengthy Approval Processes Delay Market Entry

Navigating the complex and stringent regulatory landscape for medical devices is a major constraint for companies in the adhesion barrier market. This often delays product launches and increases development costs. Regulatory bodies such as the United States Food and Drug Administration and the European Medicines Agency require extensive clinical data to demonstrate safety and efficacy before granting approval. According to FDA performance reports, the regulatory review phase for a Class III Premarket Approval (PMA) typically averages 12 to 18 months. However, the total time-to-market often spans 3 to 7 years when including the mandatory multi-phase clinical trials required to generate the safety and efficacy data for submission. This prolonged timeline restricts the ability of companies to respond quickly to market needs and technological advancements. The requirement for large-scale randomized controlled trials is particularly burdensome given the difficulty in measuring adhesion formation objectively without second-look surgeries. Changes in regulatory frameworks, such as the transition to the new Medical Device Regulation in Europe, add further complexity and uncertainty for manufacturers. Small and medium-sized enterprises often lack the resources to navigate these hurdles effectively, leading to market consolidation favoring larger corporations. The high cost of compliance diverts funds from research and innovation. Additionally, differing regulatory requirements across jurisdictions necessitate separate applications and strategies for each region, fragmenting efforts. These barriers to entry slow the introduction of innovative products and limit competition, ultimately affecting patient access to the latest technologies.

Limited Reimbursement Coverage Creates Financial Uncertainty

Inconsistent and limited reimbursement coverage for these barrier products creates significant financial uncertainty for healthcare providers and restricts patient access to these preventive treatments, which holds back the expansion of the adhesion barrier market. While some insurance plans cover specific barrier types for certain procedures, many others exclude them or classify them as investigational, leaving hospitals and patients to bear the cost. According to sources, reimbursement policies vary widely across different payers and regions, creating a fragmented landscape that complicates billing and revenue cycle management. Hospitals are often reluctant to stock expensive inventory if they cannot guarantee reimbursement, leading to supply shortages or selective use only in high-risk cases. This financial ambiguity discourages routine adoption even when clinical guidelines support usage. Physicians may hesitate to recommend barriers if they know patients will face high out-of-pocket expenses, prioritizing affordability over optimal care. The lack of standardized coding for newer barrier technologies further exacerbates billing challenges. Advocacy efforts to secure broader coverage are ongoing, but progress is slow due to the need for robust health economic data proving cost savings. Until reimbursement becomes more uniform and comprehensive, the market will struggle to achieve widespread penetration. This financial barrier disproportionately affects patients in private insurance systems or those without adequate coverage, limiting equitable access to preventive care.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Product Form, Surgical Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Baxter International Inc., Medtronic Plc., C. R. Bard, Inc., Johnson & Johnson, Sanofi Group, Atrium Medical Corporation, Integra Lifesciences Corporation, Anika Therapeutics Inc., FzioMed, Inc., and MAST Biosurgery AG, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

In 2025, the synthetic adhesion barriers segment held the majority share of 62.1% of the global market because of its consistent manufacturing quality, predictable resorption rates, and extensive clinical validation across various surgical specialties. Products based on oxidized regenerated cellulose and hyaluronic acid carboxymethylcellulose are widely accepted as the standard of care in abdominal and gynecological surgeries because they offer reliable physical separation of tissues without triggering significant immune responses. Surgeons prefer these materials because they are easy to handle and do not require complex preparation before application. The ability of synthetic barriers to maintain structural integrity in wet surgical environments ensures effective protection during the critical initial healing phase. Major clinical trials have demonstrated that these barriers significantly reduce the incidence and severity of adhesions compared to no treatment, providing robust evidence that supports their widespread adoption. Hospitals and surgical centers favor synthetic options due to their longer shelf life and stability under varying storage conditions. The standardized production processes allow for scalable manufacturing, which helps meet the high global demand. Furthermore, the familiarity of surgical teams with these products reduces the learning curve and minimizes operative time. This combination of reliability, ease of use, and strong clinical backing cements the dominance of synthetic adhesion barriers in the global market.

However, the natural adhesion barriers segment is likely to experience the fastest CAGR of 7.8% from 2026 to 2034 due to increasing preference for biocompatible and bioresorbable materials derived from biological sources. Materials such as fibrin, collagen, and chitosan are gaining traction because they mimic the body’s natural extracellular matrix, promoting better integration and healing while minimizing inflammatory reactions. As per research published in the Journal of Biomedical Materials Research, natural barriers exhibit superior hemostatic properties and encourage tissue regeneration, which is particularly beneficial in delicate procedures such as neurosurgery and reconstructive surgery. The rising awareness of potential adverse reactions to synthetic polymers has prompted surgeons to seek safer alternatives that align with the body’s physiological processes. Advances in purification technologies have reduced the risk of disease transmission and immunogenicity associated with earlier natural products, enhancing their safety profile. Regulatory agencies are approving more natural-based devices as clinical data demonstrates their efficacy in reducing adhesion formation. The trend toward personalized medicine and regenerative therapies further supports the adoption of natural barriers that can be combined with growth factors or stem cells. Patients are increasingly requesting biologically derived products perceived as safer and more natural. Manufacturers are investing in sourcing ethical and sustainable raw materials to meet this demand. This shift toward biocompatibility and regenerative potential drives the rapid expansion of the natural adhesion barrier segment.

By Product Form Insights

The film segment led the adhesion barrier market and captured a 48.3% share in 2025. This leading position of the segment was attributed to its user-friendly format that allows for precise placement and immediate coverage of targeted tissue areas. These solid sheets made from materials like oxidized regenerated cellulose are easy for surgeons to manipulate, cut, and position exactly where needed during open and laparoscopic procedures. According to surgical usage surveys conducted by major medical device distributors, film barriers account for over 50 percent of total adhesion barrier sales, reflecting their widespread acceptance among operating room staff. The tactile nature of films provides confidence to surgeons that the barrier remains in place despite fluid movement or organ shifting. Films are particularly effective in covering large flat surfaces such as the abdominal wall or pelvic sidewalls, where adhesions are common. They do not require mixing or waiting time for setting, allowing for efficient workflow in busy operating rooms. The stability of film barriers ensures they remain intact throughout the procedure, providing consistent protection. Hospitals prefer films due to their straightforward storage requirements and long shelf life. Training for new surgical staff is simpler with film formats as the application technique is intuitive and visual. This operational efficiency, combined with reliable performance, sustains the leadership of film adhesion barriers in the global market.

On the other hand, the gel segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 8.5% during the forecast period, owing to its suitability for minimally invasive and laparoscopic surgeries, which are becoming the standard of care. Gels can be delivered through trocars and catheters, allowing them to conform to irregular tissue surfaces and hard-to-reach areas that rigid films cannot access effectively. Gels provide uniform coverage over complex anatomical structures, ensuring comprehensive protection against adhesion formation. Recent innovations in thermosensitive and photocrosslinkable gels allow them to solidify upon contact with body temperature or light, offering enhanced retention and durability. Surgeons appreciate the ability to cover large areas quickly without the need for sutures or staples. The versatility of gel formulations allows for the incorporation of therapeutic agents such as anti-inflammatories, adding functional value. Patient outcomes improve as gels reduce the risk of missed spots in adhesion prevention. Manufacturers are focusing on developing low-viscosity gels that are easy to administer yet stable enough to remain in place. This alignment with modern surgical trends ensures rapid growth for the gel segment.

By Surgical Application Insights

The general and abdominal surgeries segment dominated the adhesion barrier market and accounted for a 35.8% share in 2025. This dominance of the segment was driven by the high frequency of these procedures and the significant risk of adhesion formation associated with them. Procedures such as colorectal resections, appendectomies, and hernia repairs involve extensive manipulation of the peritoneum, which triggers the body’s healing response and leads to fibrous band formation. Also, the Agency for Healthcare Research and Quality (AHRQ) HCUP registry shows that out of the millions of annual inpatient surgeries in the United States, major abdominal entries account for a massive percentage, with specialized audits tracking millions of abdominal cavity interventions per year. The consequences of abdominal adhesions, including bowel obstruction and chronic pain, are severe and costly, driving surgeons to adopt preventive measures routinely. Clinical guidelines increasingly recommend the use of adhesion barriers in high-risk abdominal cases to improve patient outcomes and reduce readmission rates. The economic burden of adhesion-related complications encourages hospitals to invest in preventive technologies that lower long-term healthcare costs. Surgeons are well-trained in the application of barriers in abdominal settings, making adoption seamless. The availability of robust clinical data supporting efficacy in abdominal surgeries reinforces confidence among practitioners. Insurance coverage for these procedures is generally well established, facilitating access for patients. This combination of high-volume clinical necessity and economic incentive sustains the dominance of general abdominal surgeries in the market.

On the contrary, the gynecological surgeries segment is expected to exhibit a noteworthy CAGR of 9.2% between 2026 and 2034. This swift growth is propelled by the critical importance of preserving fertility and preventing chronic pelvic pain in women. Procedures such as myomectomy ovarian cystectomy and endometriosis excision carry a high risk of adhesion formation which can lead to tubal blockage and infertility. As per the World Health Organization, endometriosis affects approximately 10 percent of women of reproductive age globally, many of whom require surgical intervention. The desire to maintain reproductive potential drives both patients and surgeons to prioritize adhesion prevention aggressively. Advances in minimally invasive gynecological surgery have increased the precision of barrier application, improving outcomes. Awareness campaigns by patient advocacy groups have heightened demand for fertility-sparing techniques, including the use of adhesion barriers. Reimbursement policies for gynecological procedures are evolving to support preventive care. The emotional and psychological impact of infertility adds urgency to the adoption of effective prevention methods. Surgeons are increasingly incorporating barriers into standard protocols for benign gynecological surgeries. This focus on quality of life and reproductive health fuels rapid growth in this segment.

REGIONAL ANALYSIS

North America Adhesion Barrier Market Analysis

North America was the largest region in the global adhesion barrier market and occupied a 40.6% share in 2025 because of its advanced healthcare infrastructure, high surgical volumes, and favorable reimbursement policies. The United States is the largest contributor, driven by a high prevalence of chronic diseases requiring surgical intervention and a strong emphasis on patient safety and quality outcomes. According to the Agency for Healthcare Research and Quality (AHRQ) HCUP Statistical Brief, approximately 14.4 million inpatient operating room procedures are performed annually in the United States. This volume represents a massive addressable clinical market for advanced medical devices and postoperative adhesion prevention solutions. The presence of leading medical device manufacturers and research institutions fosters innovation and rapid adoption of new technologies. Strict regulatory standards ensure high product quality while robust clinical evidence supports widespread use. Insurance coverage for adhesion barriers is relatively comprehensive, reducing financial barriers for patients and providers. The aging population increases the demand for multiple surgical procedures, further boosting market growth. High awareness among surgeons and patients regarding adhesion-related complications drives proactive prevention strategies. Academic medical centers serve as hubs for training and best practice dissemination. This combination of technological leadership, economic strength, and clinical expertise sustains North America’s market leadership.

Europe Adhesion Barrier Market Analysis

Europe was the next prominent region in the global adhesion barrier market and held a 30.2% share in 2025. This position of the European market was fuelled by stringent regulatory frameworks and a rapidly aging population that requires frequent surgical care. Countries like Germany, France, and the United Kingdom have well-established healthcare systems that prioritize patient safety and cost-effectiveness. Eurostat shows that the share of the European Union population aged 65 and older is expected to steadily increase from 22% to roughly 32.5% by 2100. This structural shift will severely expand the demand for specialized age-related surgical interventions for oncological and degenerative conditions. The implementation of the Medical Device Regulation has raised quality standards, encouraging the use of proven and safe adhesion barriers. Public healthcare systems are increasingly recognizing the long-term cost savings of preventing adhesion-related complications, leading to broader adoption. Strong clinical research networks contribute to the generation of real-world evidence supporting barrier efficacy. Cultural emphasis on high-quality care and patient rights influences treatment decisions. Government initiatives to reduce hospital readmissions support the integration of preventive devices. The presence of key market players and distributors ensures wide availability. This focus on regulatory compliance and demographic needs maintains Europe’s strong market position.

Asia Pacific Adhesion Barrier Market Analysis

The Asia Pacific is the fastest-growing region in the adhesion barrier market due to rapid healthcare infrastructure development and increasing awareness of surgical safety. Countries such as China, Japan, and India are investing heavily in modernizing hospitals and expanding access to advanced surgical care. Also, the World Bank tracks significant ongoing healthcare transformations across East Asia and the Pacific, where rising regional incomes and targeted government public health initiatives are shifting fiscal priorities toward managing age-related and chronic diseases. The large population base and increasing prevalence of lifestyle diseases lead to a surge in surgical procedures. Growing medical tourism in countries like Thailand and Singapore drives demand for high-quality care, including adhesion prevention. Local manufacturers are improving product quality and competing with international brands. Rising awareness among surgeons about the benefits of adhesion barriers is changing clinical practices. Government programs aimed at improving surgical outcomes support market growth. The expanding middle class is willing to pay for premium healthcare services. Educational initiatives and training programs are bridging the knowledge gap. This combination of economic growth, infrastructure development, and increasing awareness positions the Asia Pacific for substantial future expansion.

Latin America Adhesion Barrier Market Analysis

Latin America is another key player in the global adhesion barrier market. It shows significant potential for growth as healthcare access improves and urbanization increases. Brazil and Mexico are the primary markets benefiting from investments in public and private healthcare facilities. The Pan American Health Organization (PAHO) outlines a unified regional strategy to build robust national surgical, obstetric, and anesthesia systems. These regional frameworks aim to clear long-standing surgical backlogs, expand procedure access for hundreds of millions of underserved people, and enforce higher standards of perioperative care. The growing middle class is demanding higher-quality medical services, including preventive measures like adhesion barriers. Local distribution networks are expanding, improving product availability. Economic stabilization in some countries encourages foreign investment in the medical device sector. Awareness campaigns by professional societies are educating surgeons about adhesion prevention. Challenges related to reimbursement and cost remain, but are gradually being addressed through policy reforms. The rise of medical tourism in certain areas drives demand for internationally recognized standards of care. Partnerships between global manufacturers and local distributors facilitate market entry. While penetration is lower than in developed regions, the trajectory is positive. Continued investment in healthcare infrastructure and education will unlock further growth potential in this region.

Middle East and Africa Adhesion Barrier Market Analysis

The Middle East and Africa region is predicted to expand notably in the global adhesion barrier market during the forecast period due to medical tourism in Gulf states and infrastructure development in Africa. Countries like the United Arab Emirates and Saudi Arabia are investing in world-class healthcare facilities to attract international patients, driving demand for advanced surgical products. As per the World Health Organization, initiatives to improve surgical capacity in Africa are slowly increasing access to safe surgeries. The prevalence of conditions requiring surgical intervention is rising due to demographic changes and lifestyle shifts. Import dependence remains high, but local assembly and distribution are growing. Regulatory frameworks are being strengthened to ensure product safety. Awareness among healthcare professionals is increasing through international collaborations and training. Economic diversification efforts in the Middle East include healthcare as a key sector supporting market growth. In Africa, challenges related to funding and infrastructure persist, but donor-funded programs and public-private partnerships are making progress. The market is small but offers opportunities for specialized players who can navigate local complexities. Continued investment in healthcare systems will drive gradual expansion in this region.

COMPETITIVE LANDSCAPE

The competitive landscape of the adhesion barrier market features intense rivalry among established multinational corporations and specialized biomedical firms vying for dominance through technological innovation and clinical validation. Major players differentiate themselves by offering unique material properties such as enhanced adherence, faster resorption, or ease of application in minimally invasive procedures. Regulatory compliance serves as a significant barrier to entry, favoring companies with robust quality systems and extensive clinical data portfolios. Price competition exists but is secondary to demonstrated clinical efficacy and safety profiles, which drive surgeon preference and hospital procurement decisions. Consolidation trends persist as larger entities acquire niche innovators to secure proprietary technologies and expand therapeutic indications. Collaboration with key opinion leaders and professional societies helps shape clinical guidelines and promote standardization of care. Intellectual property protection around novel polymer formulations and delivery mechanisms creates defensive moats for leading firms. The market remains dynamic with continuous advancements in biomaterial science driving the need for ever more sophisticated and effective adhesion prevention solutions that improve patient outcomes and reduce healthcare burdens globally.

KEY MARKET PARTICIPANTS

Some of the key players dominating the global adhesion barrier market profiled in this report are

- Baxter International Inc.

- Medtronic Plc.

- Johnson & Johnson Services Inc

- C. R. Bard, Inc.

- Johnson & Johnson

- Sanofi Group

- Atrium Medical Corporation

- Integra Lifesciences Corporation

- Anika Therapeutics Inc.

- FzioMed, Inc.

- MAST Biosurgery AG

TOP PLAYERS IN THE MARKET

- Baxter International Inc is a global leader in medical products and therapies with a strong portfolio of adhesion barrier solutions, including Seprafilm. The company focuses on providing innovative surgical care products that improve patient outcomes and reduce postoperative complications. Recent initiatives include expanding manufacturing capabilities to ensure a consistent supply and investing in clinical education programs to promote best practices among surgeons. Baxter actively collaborates with healthcare providers to gather real-world evidence supporting the efficacy of its barriers. Their commitment to quality and safety drives continuous improvement in product design and packaging. By leveraging its extensive global distribution network, Baxter ensures widespread availability of its adhesion prevention technologies. This strategic focus on clinical value and operational excellence strengthens its position as a trusted partner in surgical care worldwide.

- Johnson & Johnson Services Inc contributes significantly to the adhesion barrier market through its Ethicon subsidiary, which offers advanced surgical solutions, including Interceed. The company emphasizes innovation in biomaterials and minimally invasive surgical techniques to enhance recovery and reduce adhesion formation. Recent actions include launching new product variants designed for specific surgical applications, such as gynecological and abdominal procedures. Johnson & Johnson invests heavily in research and development to create next-generation barriers with improved handling and resorption profiles. Strategic partnerships with academic institutions facilitate clinical trials and validation studies. The organization prioritizes surgeon training and support to ensure optimal product usage. By integrating digital tools for surgical planning and education, Johnson & Johnson enhances the user experience. This comprehensive approach to innovation and customer engagement reinforces its leadership in the global surgical adhesions prevention landscape.

- Integra LifeSciences Holdings Corporation is a prominent player in the regenerative medicine and surgical care sectors, offering specialized adhesion barrier products like DuraGen. The company focuses on developing biologically active materials that promote healing while preventing unwanted tissue connections. Recent strategies include acquiring complementary technologies to expand its product portfolio and entering new geographic markets to broaden its reach. Integra invests in clinical research to demonstrate the long-term benefits of its barriers in complex surgical cases. The organization emphasizes sustainability and ethical sourcing in its manufacturing processes. Collaborations with key opinion leaders help drive adoption and establish clinical guidelines. By focusing on niche specialties such as neurosurgery and orthopedics, Integra differentiates itself from broader competitors. This targeted approach, combined with robust scientific evidence, strengthens its reputation and market presence in the specialized adhesion barrier segment.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the adhesion barrier market primarily focus on product innovation to develop bioresorbable and biocompatible materials that offer superior safety and efficacy. Companies invest heavily in clinical research and real-world evidence generation to validate product performance and support regulatory approvals. Strategic partnerships with hospitals and surgical centers facilitate training programs and promote best practices for barrier application. Expanding into emerging markets through local manufacturing and distribution agreements helps capture growing demand in developing regions. Mergers and acquisitions allow firms to diversify their portfolios and access new technologies quickly. Emphasis on cost-effectiveness and health economic data appeals to payers and hospital administrators seeking to reduce long-term complication costs. Digital marketing and educational platforms enhance surgeon engagement and brand loyalty while ensuring proper product utilization in diverse surgical settings.

GLOBAL ADHESION BARRIER MARKET NEWS

- In March 2024, Baxter International Inc expanded its manufacturing facility for Seprafilm to increase global supply capacity. This expansion is anticipated to meet rising demand and strengthen the Adhesion Barrier Market's presence

- In June 2024, Johnson & Johnson Services Inc launched a new variant of Interceed designed for laparoscopic gynecological surgeries. This launch is anticipated to enhance surgical precision and strengthen the Adhesion Barrier Market presence

- In September 2024, Integra LifeSciences Holdings Corporation acquired a biotech startup specializing in novel hydrogel barrier technologies. This acquisition is anticipated to diversify product offerings and strengthen the Adhesion Barrier Market presence

- In January 2025, Baxter International Inc partnered with a leading surgical society to develop updated clinical guidelines for adhesion prevention. This partnership is anticipated to promote best practices and strengthen the Adhesion Barrier Market presence

- In May 2025, Johnson & Johnson Services Inc initiated a large scale real world evidence study to validate long term efficacy of its barriers. This initiative is anticipated to provide robust data and strengthen the Adhesion Barrier Market presence.

MARKET SEGMENTATION

This research report on the global adhesion barrier market has been segmented and sub-segmented based on the product, product form, surgical applications, and region.

By Product

- Synthetic Adhesion Barriers

- Regenerated Cellulose

- Hyaluronic Acid

- Polythene Glycol

- Natural Adhesion Barriers

- Fibrin

- Collagen & Protein

By Product Form

- Film Adhesion Barriers

- Gel Adhesion Barriers

- Liquid Adhesion Barriers

By Product Form

- Film Adhesion Barriers

- Gel Adhesion Barriers

- Liquid Adhesion Barriers

By Surgical Application

- Gynecological Surgeries

- Cardiovascular Surgeries

- Neurological Surgeries

- Orthopedic Surgeries

- General/Abdominal Surgeries

- Urological Surgeries

- Reconstructive Surgeries

- Other Surgeries

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the global adhesion barrier market?

The global adhesion barrier market includes products designed to prevent tissue adhesions post-surgery, improving recovery and reducing complications worldwide

2. What drives growth in the global adhesion barrier market?

Rising surgical procedures, minimally invasive techniques, aging population, and awareness of postoperative adhesion risks fuel the global adhesion barrier market growth

3. Which regions lead the global adhesion barrier market?

North America leads followed by Europe, with Asia-Pacific as the fastest-growing region due to healthcare modernization and increasing surgical volumes

4. Which product segments dominate the global adhesion barrier market?

Synthetic barriers dominate due to predictable degradation and biocompatibility, leading revenue share in the global adhesion barrier market

5. What are common formulation types in the global adhesion barrier market?

Film/mesh, liquid, and gel/spray formulations are key types used in the global adhesion barrier market based on surgical application needs

6. How do adhesion barriers improve surgical outcomes?

They reduce internal tissue adhesions, lower complication rates, and speed up recovery, driving demand in the global adhesion barrier market

7. Who are primary end-users in the global adhesion barrier market?

Hospitals and ambulatory surgical centers mainly use adhesion barriers across abdominal, gynecological, orthopedic, and cardiovascular surgeries

8. How do advanced products influence the global adhesion barrier market?

Multifunctional products offering sealing, hemostasis, and anti-adhesion properties provide competitive advantage in the global adhesion barrier market

9. What challenges impact the global adhesion barrier market?

Challenges include product commoditization, high costs, regulatory hurdles, and market penetration barriers in emerging economies

10. How does reimbursement affect the global adhesion barrier market?

Supportive reimbursement policies especially in developed countries boost adoption in the global adhesion barrier market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com