Africa Beer Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Ale, Lager, Stout), Packaging Type, Production Type, And Country (Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest Of Africa), Industry Analysis From 2026 To 2034

Africa Beer Market Size

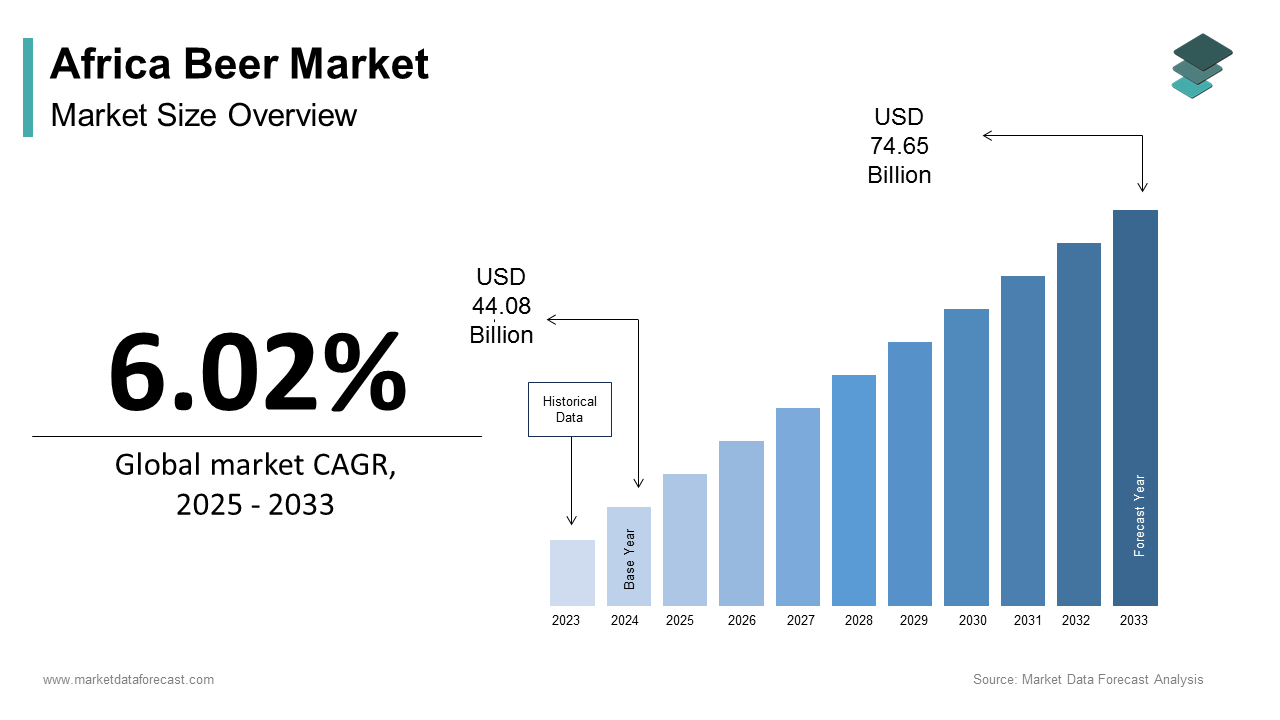

The Africa Beer Market Size was calculated to be USD 46.75 billion in 2025 and is anticipated to be worth USD 79.11 billion by 2034, from USD 49.56 billion in 2026, growing at a CAGR of 6.02% during the forecast period.

Africa beer market growth is driven by cultural preferences, economic conditions, regulatory frameworks, and evolving consumer tastes. As per the Food and Agriculture Organization (FAO), beer remains one of the most consumed alcoholic beverages in sub-Saharan Africa in countries such as South Africa, Nigeria, Ethiopia, and Uganda. Innovation in product composition, packaging designs, and marketing strategies aimed toward African customers has been more prevalent in recent years. According to the International Centre for Trade and Sustainable Development (ICTSD), local breweries have increasingly adopted sustainable sourcing practices, which utilize indigenous ingredients like sorghum and millet to produce cost-effective and culturally relevant brews. Moreover, digital transformation is reshaping distribution networks, especially in East and West Africa, where mobile money platforms and e-commerce are enabling small retailers and informal vendors to access supply chains more efficiently.

MARKET DRIVERS

Rising Urbanization and Young Demographics

The rapid urbanization and growing young population are major factors driving the Africa's beer market. According to the United Nations, over 60% of Africans were under the age of 25 in 2023, which makes it the youngest continent globally. This group of people profile plays a crucial role in shaping consumption patterns, particularly for socially consumed beverages like beer. Beer consumption has grown as a result of the growth of social events, pubs, and entertainment hubs in urban areas including Lagos, Nairobi, Kinshasa, and Cape Town. For instance, according to the Kenya Licensing Board, the number of licensed drinking facilities increased by more than 18% in Kenya between 2020 and 2023, which indicates a higher demand for alcohol-based beverages. Additionally, individuals’ disposable incomes and exposure to commercial brands also rise when more individuals relocate to urban areas.

Expansion of Informal Distribution Networks

The wide distribution of informal retail channels, which are essential for delivering beer to people living in rural and semi-urban areas, is another major factor propelling the beer market in Africa. According to the African Economic Research Consortium (AERC), more than 70% of beer sales in Sub-Saharan Africa occur through unregulated or informal outlets, which includes kiosks, roadside vendors, and small taverns. These informal networks allow producers to bypass complex supply chain constraints and reach consumers who may not frequent supermarkets or large retail stores. Breweries have strategically partnered with local distributors and wholesalers to ensure widespread availability of their products even in remote areas. Moreover, companies are utilizing mobile technology and digital payment systems to enhance logistics and inventory tracking within these informal channels. For instance, in Ghana and Tanzania, some breweries introduced mobile-based ordering and delivery systems, which improves efficiency and reducing stockouts.

MARKET RESTRAINTS

Increasing Health Awareness and Government Regulations

Growing awareness around health risks associated with alcohol consumption is one of the main factors restraining the Africa beer market growth. Governments across several African countries have intensified efforts to regulate alcohol use through taxation, advertising restrictions, and public health campaigns. According to the World Health Organization (WHO), alcohol-related mortality rates in Sub-Saharan Africa increased by 12% between 2016 and 2022, which leads to more stringent regulatory measures. For instance, the government of South Africa suggested raising the national alcohol charge in 2023 in an effort to reduce excessive drinking, while the government of Kenya placed new restrictions on late-night sales and advertising near schools. These measures have led to reduced consumption among certain consumer groups, particularly in urban centers. Additionally, there is increasing advocacy from non-governmental organizations and religious bodies against alcohol abuse, which further influencing consumer behaviour. Beer manufacturers are under increasing pressure to diversify into low-alcohol or non-alcoholic alternatives in order to stay competitive in a changing regulatory environment as health-conscious attitudes gain popularity among younger generations.

Economic Volatility and Currency Depreciation

Economic instability poses a significant barrier to the Africa beer market in countries experiencing inflation, currency depreciation, and declining purchasing power. According to the International Monetary Fund (IMF), eight African economies recorded inflation rates above 20% in 2023, which includes Nigeria, Zimbabwe, and Sudan, directly affecting consumer spending on discretionary items like beer. Currency devaluation has also impacted production costs, as many breweries rely on imported raw materials and packaging components. According to the Central Bank of Nigeria, the naira lost more than 40% of its value versus the US dollar in 2023, which increased input costs and compelled businesses to raise prices. International and premium brands' profits are being squeezed by the move toward cheaper or locally brewed alternatives driven out by this economic pressure. Additionally, consumers are opting for cheaper substitutes such as homemade or illicit alcohol, which further fragmenting the market. Beer producers will continue to struggle to maintain affordability and volume expansion across key markets in the absence of macroeconomic stability.

MARKET OPPORTUNITIES

Growth of Craft and Premium Beer Segments

The expansion of craft and premium beer options, which is being fueled by shifting consumer preferences and increasing disposable incomes, represents an opportunity in the African beer market. According to the African Microbrewers Association (AMA), the number of craft breweries across the continent has more than doubled since 2018, with notable growth observed in South Africa, Kenya, and Morocco. Consumers in urban areas are showing a growing interest in unique flavors, locally sourced ingredients, and artisanal brewing techniques. Breweries are responding by introducing innovative products such as fruit-infused lagers, hop-forward IPAs, and heritage-style beers using indigenous grains like sorghum and millet. Moreover, the rise of experiential dining and social drinking culture has created demand for taprooms, microbrew pubs, and branded tasting experiences.

Expansion of E-commerce and Digital Retail Channels

The digital transformation is creating new opportunities for beer distribution through mobile-based retail solutions and e-commerce platforms. According to Disrupt Africa, online alcohol sales in selected African markets grew by over 30% in 2023, which indicates a shift in consumer behavior toward convenience-driven purchasing. Distributors and breweries are using delivery apps and mobile money platforms to connect with customers in peri-urban and metropolitan locations. In Ghana and Nigeria, startups like Alcoholtics and DrinkExpress launched mobile-first platforms that enable users to order beer deliveries via WhatsApp or app-based interfaces. Additionally, major brewers are integrating digital tools into their supply chain operations to improve inventory management and reduce logistical inefficiencies.

MARKET CHALLENGES

Regulatory Complexity and Taxation Policies

Inconsistent regulatory frameworks and rising taxation policies across governments provide significant challenges to the beer market in Africa. According to the African Tax Institute, excise duties on beer have increased in over 15 African countries since 2020, and these hikes have frequently not been implemented consistently throughout the various areas. These tax hikes have led to price volatility and reduced affordability, particularly in middle-income and rural markets. In countries like Zambia and Uganda, abrupt changes in duty structures have disrupted supply chains and forced smaller breweries out of business due to compliance burdens. Furthermore, licensing procedures vary widely with some countries imposing stringent requirements on alcohol retailers, which limits market access for both domestic and international brands. In Ethiopia, for instance, bureaucratic hurdles have slowed the expansion of foreign-owned breweries despite growing consumer demand. Navigating these regulatory inconsistencies requires substantial investment in legal and compliance infrastructure, which pose a challenge for both multinational and local beer producers seeking scalable growth in the region.

Competition from Illicit and Homemade Alcohol

Illicit and homemade alcohol remains a persistent challenge in the Africa beer market, which decline formal sales and posing health risks to consumers. According to the World Health Organization (WHO), an estimated 30% of alcohol consumed in parts of East and Southern Africa is produced informally, with little to no quality control. This informal sector thrives due to its affordability and accessibility, especially in rural and low-income communities where official beer prices may be prohibitive. In many places, traditional brews like burukutu in Nigeria and changaa in Kenya still account for the majority of local consumption and are in direct competition with commercially produced beer. Efforts to curb illicit production have been hindered by weak enforcement mechanisms and limited public awareness about the dangers of unregulated alcohol. Meanwhile, legitimate brewers struggle to penetrate these markets without compromising pricing strategies or brand positioning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.02% |

| Segments Covered | By Product Type, Packaging Type, Production Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, and Rest of Africa |

| Market Leaders Profiled | AB InBev, Heineken NV, Diageo Plc, SABMiller Ltd, Castel Group, United National Breweries, Namibia Breweries Ltd, Sierra Leone Brewery Limited, Guinness Nigeria Plc, East African Breweries Limited |

SEGMENTAL ANALYSIS

By Product Type Insights

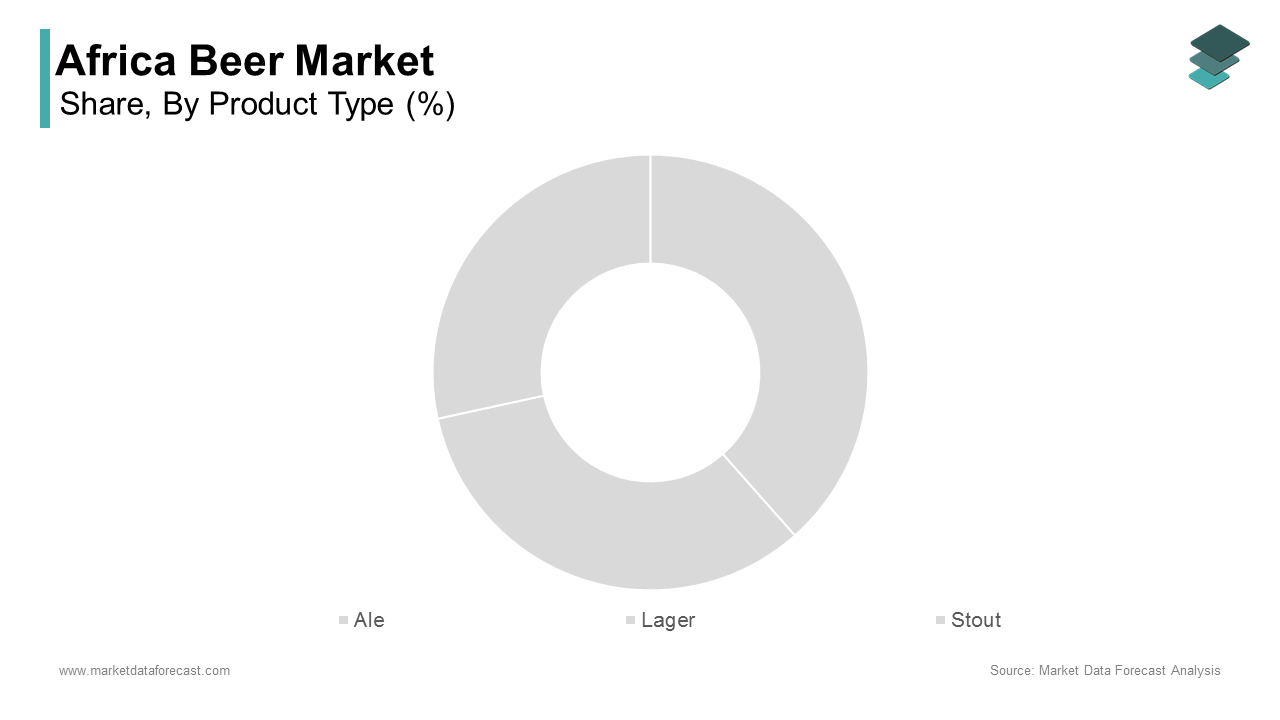

The lager segment dominated the Africa beer market by capturing a major share in 2025. Lager-style beers, which are characterized by their light, crisp, and refreshing flavor, are more frequently drank at social gatherings, athletic events, and casual drinking areas. Additionally, strong marketing and distribution networks of multinational brewers such as Heineken, AB InBev, and SABMiller have reinforced lager’s position in the market. Star Lager, Tusker, and Castle Lite are examples of brands that these companies have localized to suit regional tastes while maintaining their mass-market appeal. Moreover, lager remains the most accessible option in informal retail channels, which account for a significant portion of beer consumption in Sub-Saharan Africa. Lager is anticipated to keep its dominant position in the beer market across the continent with sustained investments in supply chain effectiveness and brand recognition.

The craft beer segment is predicted to witness a CAGR of 9.4% during the forecast period as consumer demands for premiumization, authenticity, and unique flavor profiles continue to rise.A primary growth driver is the rising influence of urban millennials and Gen Z consumers, who are increasingly seeking differentiated and experiential beverage options. Craft breweries have become more popular in places like Cape Town, Nairobi, and Marrakech due to social media-driven branding, beer festivals, and taprooms. Furthermore, local entrepreneurship and government support for small-scale brewing initiatives have enabled microbreweries to enter the market with innovative products. Craft beer is becoming more widely available outside of niche markets due to collaborations with bars, restaurants, and e-commerce platforms.

By Packaging Type Insights

The bottled beer segment was accounted led the Africa beer market by capturing 59.4% of the share in 2025 with the deep-rooted consumer habit of purchasing bottled beer, especially in informal markets such as roadside kiosks and local taverns. According to the African Economic Research Consortium (AERC), more than 70% of beer sold in East and West Africa is distributed via non-refrigerated outlets, where glass bottles remain the preferred choice due to durability and ease of storage. Additionally, bottling infrastructure is well-established in major brewing hubs, which allows large-scale production and distribution without requiring significant capital investment. Breweries such as SABMiller and Heineken continue to leverage existing bottling lines to meet high-volume demand in countries like Nigeria, Ghana, and Kenya. Moreover, glass bottle reuse systems are common in many African markets, which reduces costs for both producers and consumers. Reusable bottles make up a significant amount of beer sales in Ethiopia and Tanzania, which helps to improve their sustainability both economically and environmentally in low-income environments.

The canned beer segment is likely to experience a CAGR of 8.2% from 2026 to 2034. Improved cold-chain logistics in African countries, increased portability, and shifting customer lifestyles are all contributing factors to this expansion. Canned beer is easier to transport, store, and consume in open-air environments, which makes it ideal for picnics, concerts, and beach outings. Another contributing factor is the expansion of modern retail and supermarket chains, which favor cans for their stackability, longer shelf life, and lower breakage risk. Retailers in Nigeria and Kenya are increasingly stocking canned varieties of popular brands like Gulder and Tusker, which enhances visibility and accessibility. Additionally, environmental considerations are influencing packaging choices with aluminum cans being more recyclable than glass. Breweries are responding by investing in canning lines and promoting eco-friendly branding strategies to attract sustainability-conscious consumers.

By Production Type Insights

The macro breweries segment held a prominent share of the Africa Beer market in 2025. Multinational corporations like AB InBev, Heineken, and SABMiller dominate this market sector and run substantial operations in key areas around Africa. According to the African Beverage Industry Report, macro breweries control over 75% of the licensed retail and wholesale market, which ensures consistent availability of their products even in remote areas. Additionally, brand recognition and aggressive marketing campaigns reinforce their market dominance. Companies like South African Breweries (SAB) and Nigerian Breweries make significant investments in internet, radio, and television advertising to appeal to young consumers and sports fans. Moreover, government partnerships and regulatory compliance advantages allow macro breweries to navigate complex tax regimes and licensing requirements more efficiently than smaller players.

The craft breweries segment is expected to witness a CAGR of 11.6% from 2026 to 2034. A key growth factor is the increasing disposable income and lifestyle changes among urban professionals, particularly in cities like Cape Town, Nairobi, and Casablanca. Additionally, entrepreneurship and innovation in brewing techniques are attracting investment into the sector. Startups and independent brewers are experimenting with flavors using indigenous ingredients such as millet, sorghum, and tropical fruits, which differentiate themselves from mainstream offerings. Moreover, the rise of microbrew pubs, beer festivals, and online retail platforms has expanded access to craft beer beyond niche circles.

REGIONAL ANALYSIS

South Africa Beer Market Insights

South Africa was the top performer in the global market in 2025 and accounted for 24.7% of Africa beer market share in 2025. South Africa market was one of the most developed beer markets in the region, characterized by a mature brewing industry, strong brand presence, and diverse consumer preferences. South African Breweries (SAB), a branch of AB InBev, and other important businesses support the nation's well-established brewing infrastructure, which is one of the main drivers. Additionally, urbanization and nightlife culture play a significant role in sustaining demand. Cities like Johannesburg, Durban, and Cape Town host numerous bars, shebeens, and entertainment venues that contribute to high beer consumption levels. Moreover, regulatory reforms and excise duty adjustments have influenced pricing and taxation policies, which affects both formal and informal market segments.

Nigeria Beer Market Insights

Nigeria beer market held 19.8% of share in 2025 due to the high demand for affordable and locally brewed beers in informal retail channels. According to the National Bureau of Statistics (NBS), beer consumption in Nigeria increased by 7% in 2022, which driven by strong cultural ties to social drinking and festive occasions. Additionally, investment in modern brewing facilities and brand localization has strengthened market presence. Nigerian Breweries, a subsidiary of Heineken, and Guinness Nigeria have launched region-specific products such as Hero Lager and Intafact, which aligns with local tastes and affordability. Urbanization and rising disposable incomes are further fueling demand for premium variants among young professionals and expatriates.

Kenya Beer Market Insights

Kenya beer market growth is driven with a strong tradition of beer consumption a growing middle class, and increasing investments in both formal and informal brewing sectors. Consumers are showing a growing preference for locally made, high-quality brews that reflect regional identity and craftsmanship. Additionally, digital transformation in beer retail is reshaping how consumers access products. Startups like DrinkExpress and mobile-based ordering platforms have introduced convenience-focused delivery models, which enhances accessibility and customer engagement. Government policies supporting small businesses and tax incentives for local brewers have also contributed to market dynamism.

Morocco Beer Market Insights

Morocco is gaining huge traction over the highest CAGR during the forecast period. Morocco, a strategically located entry point between Europe and Africa, boasts a comparatively steady beer market supported by tourism, moderate alcohol laws, and a burgeoning hotel industry. One of the main growth drivers is the expansion of international brewing brands and premium beer imports, particularly in tourist-heavy regions such as Marrakech and Casablanca. According to the Moroccan Ministry of Tourism, international visitor numbers surged by 24% in 2023 , which increase demand for imported and craft beers in hotels and upscale restaurants. Additionally, local breweries are adapting to changing consumer preferences by introducing lighter lagers and non-alcoholic variants to cater to a broader audience. In order to lessen dependence on imported raw materials, the state-sponsored Office des Études et de la Recherche Agricoles (OCP) has also encouraged the growing of barley for brewing.

Egypt Beer Market Insights

Egypt beer market is likely to have significant growth opportunities in coming years. Egypt's general alcohol usage remains conservative, although beer access has been gradually liberalized, especially in metropolitan areas and tourist destinations. One of the primary growth factors is the revival of local brewing traditions, with companies like SA Brewing reviving historic Egyptian beer recipes using indigenous ingredients such as dates and barley. According to the Egyptian Chamber of Food Industries, domestic beer production increased by 6% in 2022, which supported by renewed interest in premium and export-oriented offerings. Additionally, tourism recovery post-pandemic has boosted demand in luxury hotels and restaurants, where imported and craft beers are gaining traction.

LEADING PLAYERS IN THE AFRICA BEER MARKET

Heineken N.V. (Netherlands)

Heineken is a dominant force in the Africa beer market with a strong presence across Sub-Saharan and North Africa. It provides a wide range of domestic and foreign brands that are suited to local preferences through subsidiaries like Nigerian Breweries and Brasseries du Maroc. The company plays a significant role in promoting sustainable brewing practices and responsible consumption initiatives globally. Its deep integration into African markets allows it to influence distribution networks, brand development, and industry standards beyond the continent.

Anheuser-Busch InBev (AB InBev) (Belgium)

AB InBev maintains a substantial presence in Africa through its operations under South African Breweries (SAB) and other regional ventures. It maintains efficiency by using economies of scale and advanced logistics to control a significant share of the mainstream and premium beer markets. Globally, AB InBev drives innovation in beverage formulation, packaging sustainability, and digital marketing strategies that often-set trends for emerging markets. Its strategic investments in African breweries reflect its long-term commitment to the region's growth potential.

Carlsberg Group (Denmark)

Carlsberg has been expanding its presence in Africa through partnerships and localized production, particularly in East and Southern Africa. Carlsberg, which is well-known for its quality and brand history, offers the African market its global experience in supply chain optimization and product innovation. Its focus on responsible alcohol consumption and environmental sustainability aligns with evolving consumer expectations worldwide. Carlsberg improves its position in a dynamic and competitive beer market by catering to local tastes while maintaining global standards.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the most impactful strategies employed by major players in the Africa beer market is localization of products and branding, where multinational brewers adapt their offerings to suit regional taste preferences and cultural nuances. This includes developing affordable variants, using locally sourced ingredients, and incorporating traditional brewing elements to resonate with consumers.

Another key approach is expanding informal distribution networks, which are crucial in reaching rural and semi-urban populations. Companies invest in strengthening relationships with independent retailers, micro-distributors, and informal vendors to ensure widespread availability and accessibility of their products beyond modern trade channels.

Leading players are increasingly adopting digital transformation and data-driven marketing to engage younger, tech-savvy consumers. From mobile-based ordering systems to targeted social media campaigns, these strategies enhance customer engagement, improve supply chain visibility, and strengthen brand loyalty across diverse African markets.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the Africa Beer Market include AB InBev, Heineken NV, Diageo Plc, SABMiller Ltd, Castel Group, United National Breweries, Namibia Breweries Ltd, Sierra Leone Brewery Limited, Guinness Nigeria Plc, East African Breweries Limited

The competition in the Africa beer market is marked by a dynamic interplay between global brewing giants, regional producers, and a growing number of independent craft breweries. Multinational companies such as Heineken, AB InBev, and SABMiller continue to dominate due to their vast resources, established distribution networks, and strong brand recognition. These firms leverage economies of scale to maintain pricing power and ensure consistent product availability even in remote areas.

At the same time, regional and domestic players are gaining traction by offering cost-effective alternatives and catering to local tastes. Craft beer companies and microbreweries are also becoming niche competitors, taking advantage of consumers' growing desire for high-end, artisanal, and regionally produced beverages. This segment benefits from rising disposable incomes and urbanization, especially among younger people seeking differentiated drinking experiences.

Regulatory changes, taxation policies, and health awareness campaigns further shape the competitive landscape, which prompts companies to innovate in product formulation, packaging, and marketing. Agility, localization, and brand distinctiveness are crucial success elements in this rapidly changing business as the competition for market share heats up due to shifting consumers behavior and the growth of digital commerce.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, Heineken launched a new line of affordable lager beers under the "Star Lite" brand in Ghana, which targets price-sensitive consumers while reinforcing its presence in West Africa’s competitive beer market.

- In August 2023, AB InBev partnered with a Kenyan fintech firm to introduce a mobile-based ordering system for small tavern owners, which improves access to branded beer and enhancing supply chain efficiency in informal retail sectors.

- In November 2023, South African Breweries (SAB) expanded its canning facility in Durban in order to promote sustainable manufacturing goals and satisfy the growing demand for portable and environmentally friendly packaging forms.

- In May 2025, Nigerian Breweries introduced a limited-edition sorghum-based beer, which focus on indigenous sourcing and appealing to health-conscious and culturally aligned consumers in Nigeria’s evolving beer landscape.

- In October 2025, Carlsberg announced a joint venture with a local Egyptian brewery to produce and distribute its flagship brand in Cairo and Alexandria, which marks a strategic move into North Africa’s emerging premium beer segment.

MARKET SEGMENTATION

This research report on the African Beer Market has been segmented and sub-segmented based on product type, packaging type, production type and region.

By Product Type

- Ale

- Lager

- Stout

By Packaging Type

- Bottles

- Cans

- Others

By Production Type

- Macro Brewery

- Micro Brewery

- Craft Brewery

By Region

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest Of Africa

Frequently Asked Questions

1. What are the major factors driving the growth of the Africa beer market?

Key drivers include urbanization, rising disposable incomes, expanding young population, cultural shifts towards social drinking, and increasing availability of diverse beer products.

2. Which countries in Africa have the highest beer consumption?

South Africa, Nigeria, Kenya, and Egypt are among the leading countries in terms of beer consumption in Africa.

3. What are the major segments of the Africa beer market?

The market is segmented by product type (Lager, Ale, Stout & Porter, Malt), by distribution channel (On-trade, Off-trade), and by region.

4. Who are the key players in the Africa beer market?

AB InBev, Heineken NV, Diageo Plc, SABMiller Ltd, Castel Group, United National Breweries, Namibia Breweries Ltd, Sierra Leone Brewery Limited, Guinness Nigeria Plc, and East African Breweries Limited.

5. What are the current trends in the Africa beer market?

Trends include increasing demand for craft beer, flavored beers, premiumization, eco-friendly packaging, and a shift toward low-alcohol and non-alcoholic beer variants.

6. What challenges are impacting the Africa beer market?

Challenges include high taxation on alcoholic beverages, regulatory restrictions, illicit alcohol consumption, and supply chain disruptions.

7. What is the market outlook for craft beer in Africa?

Craft beer is witnessing growing popularity, especially among urban consumers looking for unique flavors and premium experiences, though it remains a niche segment.

8. How is the distribution landscape evolving in the Africa beer market?

The off-trade channel, including supermarkets and retail stores, is growing rapidly, while the on-trade (bars, restaurants) segment is recovering post-pandemic.

9. What opportunities exist for new entrants in the Africa beer market?

Opportunities include tapping into underpenetrated markets, developing region-specific flavors, investing in local production facilities, and targeting health-conscious consumers with low-alcohol and non-alcoholic beer options.

10. How is the rise of e-commerce impacting beer sales in Africa?

Online alcohol delivery platforms and e-commerce channels are gaining traction, especially in urban areas, making it easier for consumers to purchase beer conveniently from home.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com