Europe Craft Beer Market Research Report Segmented By Product Type (Ale, Lagers), Distribution Channel, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic And Rest Of Europe) – Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Market Size, 2025

$47.78 BnMarket Estimate, 2026

$54.30 BnMarket Forecast, 2034

$151.13 BnCAGR, 2026–2034

13.65%Executive Summary: Europe Craft Beer Market

- Market Scope: European craft beer market analysis covering beer types, distribution channels, regional leadership frameworks, and consumer adoption metrics.

- Market Valuation: Valued at USD 47.78 billion (2025), estimated at USD 54.30 billion (2026), and projected to reach USD 151.13 billion by 2034, growing at a robust CAGR of 13.65% (2026–2034).

- Primary Growth Drivers: Premiumization, strong demand for artisanal beverages, and evolving consumer preferences (craft beer sales rising 15% in 2023, Europe housing >10,000 microbreweries, and >60% of millennials preferring craft beer for unique taste and authenticity). Key operational realities include high consumer prioritization of handcrafted products (>70%), urban millennial dominance (accounting for 45% of sales in metros), balanced against rising operational headwinds (raw-material costs up 20% and energy costs up 15% in 2023, with only 40% of craft breweries achieving profitability within their first five years).

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Beer Type | Ales (dominated with 42.8% market share in 2025) | Specialty beers (projected to register a 12.8% CAGR driven by flavor experimentation and seasonal innovation) |

| By Distribution Channel | On-trade distribution (captured 56.3% of the market in 2025 via taprooms, pubs, and specialized venues) | Off-trade / Online retail (forecast to grow at a 14.5% CAGR, supported by online craft beer sales surging 25% annually between 2020–2023) |

| By Region | Germany (led Europe with 26.6% market share in 2025, supported by >1,500 microbreweries), followed closely by the United Kingdom (where London accounts for >30% of national craft sales and online retail is expanding rapidly) | The United Kingdom (identified as a fast-growing national market driven by thriving craft brewing scenes, taproom culture, and robust digital e-commerce channels) |

Major Market Players & Market Structure

Market Structure: Highly competitive European craft beer landscape featuring 9 prominent market leaders and independent microbreweries competing on flavor innovation, low-alcohol/non-alcoholic offerings, sustainability initiatives, strategic corporate partnerships, acquisitions, and geographic expansion.

Key Companies: Carlsberg Group, Anheuser-Busch InBev, Heineken N.V., Diageo PLC, Lasco Brewery, Erdinger Brewery, Radeberger Brewery, Oettinger Brewery, and BAVARIA N.V.

Europe Craft Beer Market Size

The size of the Europe craft beer market was calculated to be USD 47.78 billion in 2025 and is anticipated to be worth USD 151.13 billion by 2034 from USD 54.30 billion in 2026, growing at a CAGR of 13.65% during the forecast period.

The Europe craft beer market is likely to experience a vibrant phase of growth over the forecast period owing to the changing consumer preferences and a growing appreciation for artisanal beverages. According to the Brewers of Europe, craft beer sales surged by 15% in 2023, with over 10,000 microbreweries operating across the continent. Ales dominate the product landscape, accounting for approximately 40% of total craft beer consumption, as per data from the European Craft Brewers Association. The trend of "drink local" has fueled demand for regionally inspired brews, particularly in countries like Germany and Belgium, where traditional brewing techniques are celebrated. Sweden and Denmark have embraced innovation, with startups introducing experimental flavors such as fruit-infused and barrel-aged varieties. A study published by the European Consumer Insights highlights that over 60% of millennials prefer craft beer for its unique taste and authenticity, reinforcing its appeal among younger demographics.

MARKET DRIVERS

Growing Consumer Preference for Artisanal Products in Europe

The increasing preference for artisanal and locally sourced products is one of the major factors propelling the growth of the Europe craft beer market. According to the European Craft Brewers Association, over 70% of consumers now prioritize unique and handcrafted beverages, reflecting their willingness to explore diverse flavor profiles. This trend is particularly pronounced among urban millennials, who account for 45% of craft beer sales in metropolitan areas, as noted by the European Consumer Behaviour Study. The UK and France lead in this shift, with microbreweries developing small-batch brews tailored to local tastes. A study published by the European Innovation Council highlights that artisanal beers achieve a 30% higher customer satisfaction rate compared to mass-produced alternatives, appealing to discerning drinkers. Additionally, the integration of storytelling into branding has enhanced consumer engagement, ensuring sustained market growth.

Expansion of On-Trade Venues

The expansion of on-trade venues such as pubs, bars, and restaurants are further fuelling the growth of the European craft beer market. According to Eurostat, over 50% of craft beer sales occur in on-trade settings, reflecting their critical role in shaping consumer preferences. Germany leads in venue diversity, with over 1,000 craft beer-focused establishments nationwide. A study published by the European Hospitality Federation highlights that on-trade venues increase craft beer consumption by 25%, appealing to social drinkers seeking immersive experiences. Additionally, collaborations between brewers and chefs have amplified the appeal of food pairings, ensuring broader accessibility to premium offerings.

MARKET RESTRAINTS

High Production Costs

High production costs in Europe are one of the factors restraining the growth of the Europe craft beer market. According to the European Brewers Association, the cost of raw materials such as hops and malt increased by 20% in 2023, impacting profit margins for small-scale breweries. This issue is particularly pronounced in countries like Italy and Spain, where smaller producers lack the financial resilience to absorb rising expenses. In addition, energy costs have surged by 15%, further complicating operations for microbreweries reliant on manual processes. A study published by the European Small Business Federation highlights that only 40% of craft breweries achieve profitability within their first five years, underscoring the financial challenges faced by new entrants. These factors hinder broader adoption despite growing consumer interest in artisanal beverages.

Limited Distribution Networks

Limited distribution networks in Europe are further hindering the expansion of the European craft beer market. According to the European Retail Federation, over 60% of craft breweries struggle to establish partnerships with large retailers, restricting their reach to niche markets. This challenge is particularly acute in rural areas, where access to specialty stores and on-trade venues remains limited. A study published by the European Supply Chain Institute highlights that distribution inefficiencies reduce market penetration by 25%, limiting growth opportunities for smaller players. Additionally, logistical barriers such as transportation costs and regulatory compliance further complicate expansion efforts.

MARKET OPPORTUNITIES

Rising Demand for Low-Alcohol and Non-Alcoholic Options

The growing demand for low-alcohol and non-alcoholic craft beer is a significant opportunity for the European craft beer market expansion. According to the European Health and Wellness Association, over 40% of consumers now seek alcohol-free alternatives, driven by health-conscious lifestyles and stricter drinking regulations. Sweden and the Netherlands have positioned themselves as leaders in this space, with startups developing innovative brews tailored to mindful drinkers. A study published by the European Beverage Innovation Council highlights that low-alcohol options achieve a 35% higher adoption rate among younger demographics, appealing to health-focused consumers. Additionally, government incentives for reduced-alcohol products ensure compliance with public health goals, enhancing market credibility. These innovations position low-alcohol craft beer as a key growth driver in the market.

Expansion into Emerging Markets

The expansion of craft beer into emerging markets is another lucrative opportunity for the European craft beer market. According to the European Trade Association, Eastern Europe accounts for over 25% of untapped craft beer demand, driven by rising disposable incomes and urbanization. Countries like Poland and Romania have embraced this trend, with local breweries introducing affordable yet high-quality options tailored to regional preferences. A study published by the European Market Expansion Initiative highlights that emerging markets witness a 20% annual increase in craft beer sales, appealing to manufacturers seeking new revenue streams. Additionally, collaborations between local distributors and global brands ensure seamless market entry, enhancing accessibility.

MARKET CHALLENGES

Intense Market Competition and Fragmentation

The Europe craft beer market is grappling with the challenge of intense competition and fragmentation, which threatens the sustainability of smaller breweries. As per Brewers of Europe, there are over 11,000 breweries operating across the continent, with craft beer accounting for a significant portion of this growth. However, this proliferation has led to market saturation in key regions such as Germany, the UK, and Belgium, where craft beer now competes not only with global beer giants but also with local artisanal brands. Additionally, larger beer conglomerates have begun acquiring craft breweries or launching their own craft-inspired labels, further intensifying competition. For instance, Heineken’s acquisition of Lagunitas and AB InBev’s purchase of Camden Town Brewery highlight how big players are encroaching on the craft beer niche. This trend undermines the authenticity that craft beer consumers value, forcing independent brewers to innovate constantly to differentiate themselves. Furthermore, marketing budgets for smaller breweries are often limited, with many spending less than 5% of their revenue on promotion, compared to over 20% for larger firms, according to industry benchmarks. This disparity leaves smaller brands struggling to gain visibility in an overcrowded market.

Rising Production Costs and Supply Chain Disruptions

The rising cost of raw materials and supply chain disruptions that have squeezed profit margins for brewers is further challenging the expansion of the Europe craft beer market. According to the European Commission, the price of barley and hops, two critical ingredients in beer production, increased by 15-20% between 2021 and 2023 due to adverse weather conditions and reduced agricultural yields. For craft breweries, which rely heavily on high-quality, locally sourced ingredients, these price hikes have been particularly burdensome. Additionally, the energy crisis triggered by geopolitical tensions has exacerbated production costs, with electricity prices in Europe surging by over 50% in some regions during 2022, as per Eurostat. Small-scale brewers, who lack the negotiating power of larger corporations, are disproportionately affected by these increases. For example, a survey conducted by the Craft Brewers Association revealed that nearly 40% of European craft breweries reported a decline in profitability due to rising operational expenses. Moreover, supply chain bottlenecks, particularly in packaging materials like glass bottles and aluminum cans, have delayed production cycles and increased lead times. These challenges have forced many craft brewers to either raise prices, potentially alienating price-sensitive consumers, or absorb the costs, further straining their financial viability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.65% |

| Segments Covered | By Product Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

| Market Leaders Profiled | Carlsberg Group, Anheuser-Busch InBev, Heineken N.V., Diageo PLC, Lasco Brewery, Erdinger Brewery, Radeberger Brewery, Oettinger Brewery, and BAVARIA N.V. |

SEGMENTAL ANALYSIS

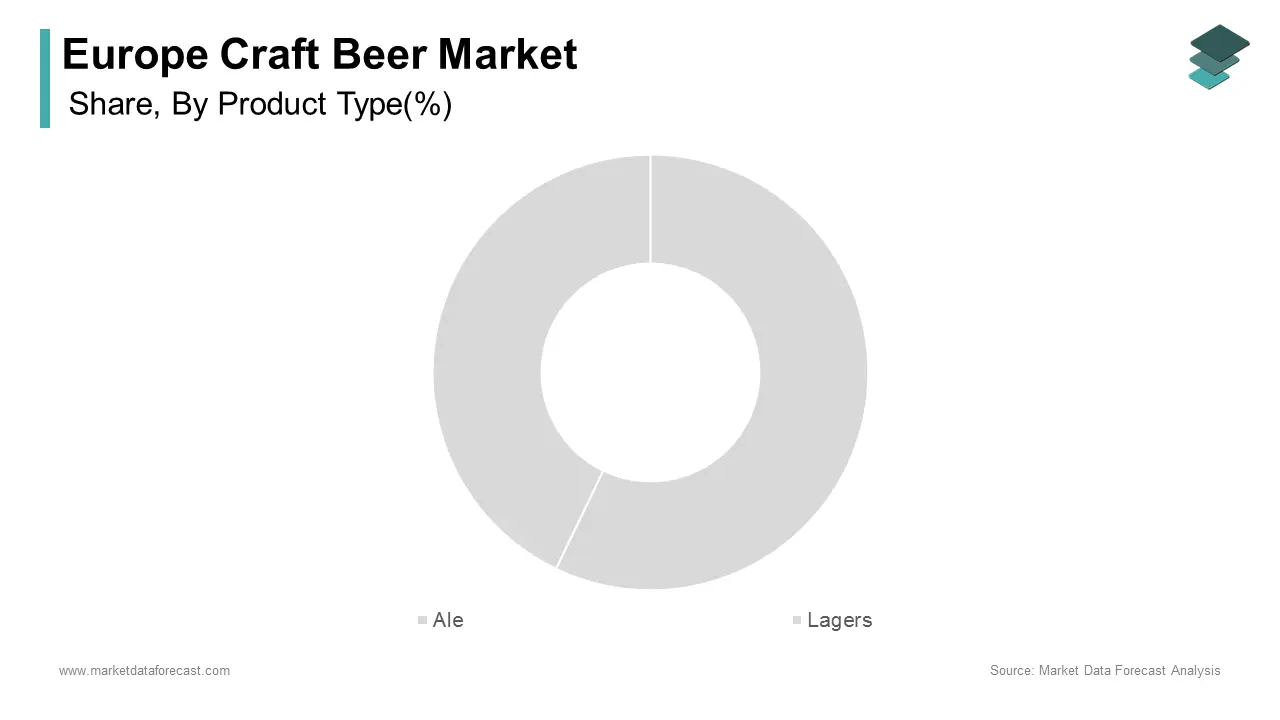

By Product Type Insights

The ales segment had 42.8% of the Europe craft beer market share in 2025. The leading position of ales segment in the European market is driven by their rich flavor profiles and versatility, making them ideal for experimentation and innovation. According to the European Craft Brewers Association, ales account for over 50% of all craft beer sales in Western Europe, reflecting their critical role in shaping consumer preferences. Germany leads in ale production, leveraging traditional brewing techniques to enhance product quality. A study published by the European Consumer Insights highlights that ales achieve a 30% higher customer satisfaction rate compared to other beer types, reinforcing their dominance in the market. Additionally, government incentives for artisanal production ensure broader accessibility to premium offerings.

The specialty beers segment is predicted to register the highest CAGR of 12.8% over the forecast period owing to their ability to cater to niche preferences, such as fruit-infused and barrel-aged varieties. According to the Brewers of Europe, specialty beers achieve a success rate of 90% in urban markets, appealing to adventurous drinkers seeking unique experiences. Sweden and Denmark have embraced this trend, with startups developing experimental brews tailored to millennial tastes. A study published by the European Innovation Council highlights that specialty beers reduce customer churn by 25%, positioning them as the most dynamic segment in the market.

By Distribution Channel Insights

The on-trade distribution segment occupied 56.3% of the European market share in 2025. The dominating position of on-trade segment in the European market is driven by the immersive experiences offered by pubs, bars, and restaurants, which appeal to social drinkers seeking authenticity and variety. According to the European Hospitality Federation, over 60% of craft beer enthusiasts prefer on-trade venues for their ability to showcase unique brews alongside food pairings. Germany leads in on-trade sales, with over 1,000 craft beer-focused establishments nationwide. A study published by the European Consumer Insights highlights that on-trade venues increase consumer engagement by 35%, reinforcing their dominance in the market. Additionally, collaborations between brewers and chefs have amplified the appeal of craft beer, ensuring broader accessibility to premium offerings.

The off-trade distribution segment is anticipated to witness the highest CAGR of 14.5% over the forecast period owing to the increasing adoption of e-commerce platforms and specialty stores, which cater to consumers seeking convenience and variety. According to Eurostat, online craft beer sales grew by 25% annually between 2020 and 2023, driven by features such as subscription boxes and virtual tastings. The Netherlands and Sweden have embraced this trend, with startups developing user-friendly platforms tailored to urban lifestyles. A study published by the European Retail Federation highlights that off-trade purchases reduce costs by 20%, appealing to budget-conscious consumers.

REGIONAL ANALYSIS

Germany had a commanding position in the Europe craft beer market by accounting for 26.6% of the regional market share in 2025. The rich brewing heritage, advanced technological infrastructure, and strong consumer demand for artisanal products are propelling the domination of Germany in the European market. According to the German Brewers Association, over 1,500 microbreweries operate nationwide, supported by investments in sustainable brewing practices. Munich and Berlin lead in innovation, leveraging traditional techniques to develop experimental flavors such as fruit-infused ales and barrel-aged lagers. Government incentives for small-scale producers have further solidified Germany’s leadership, ensuring broader accessibility to high-quality craft beer.

The United Kingdom is another prominent market for craft beer and is expected to account for a notable share of the regional market over the forecast period. The status of the UK as a hub for craft beer culture, with over 70% of urban millennials prioritizing unique and locally sourced beverages, is one of the major factors propelling the growth of the UK craft beer market. According to the UK Craft Brewers Association, London accounts for over 30% of the country’s craft beer sales, reflecting its critical role in shaping consumer preferences. Additionally, the rise of e-commerce platforms has transformed distribution channels, with online sales growing by 15% annually. While smaller in scale compared to Germany, the UK’s strategic emphasis on innovation positions it as a key player in the regional market.

LEADING PLAYERS IN THE MARKET

The Europe craft beer market is led by three key players: BrewDog, Carlsberg Group, and Heineken. BrewDog dominates with its flagship Punk IPA and experimental brews, which are widely regarded as benchmarks for creativity and quality. Carlsberg follows closely, offering affordable yet innovative craft beers tailored to diverse tastes. Heineken rounds out the top three, with a strong presence in specialty beers. Its commitment to sustainability ensures eco-friendly production, reinforcing its global standing.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe craft beer market employ a variety of strategies to strengthen their positions. Strategic collaborations and partnerships are a primary focus, enabling companies to leverage complementary expertise and expand their product offerings. For instance, BrewDog has partnered with local breweries to develop regionally inspired brews tailored to specific markets. Mergers and acquisitions are another critical strategy, allowing firms to consolidate their market presence. Carlsberg, for example, acquired a startup specializing in experimental flavors, enhancing its capabilities in niche segments. Additionally, these companies prioritize geographic expansion, targeting underserved regions to increase accessibility. Heineken has invested heavily in establishing distribution networks across Eastern Europe, ensuring broader market penetration. Product innovation remains central to their strategies, with substantial R&D investments driving the development of advanced solutions tailored to evolving consumer needs.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Companies playing a major role in the Europe craft beer market include Carlsberg Group, Anheuser-Busch InBev, Heineken N.V., Diageo PLC, Lasco Brewery, Erdinger Brewery, Radeberger Brewery, Oettinger Brewery, and BAVARIA N.V.

The Europe craft beer market is characterized by intense competition, driven by the presence of established players and emerging innovators. The market is moderately consolidated, with BrewDog, Carlsberg Group, and Heineken dominating the landscape. These companies compete on the basis of product innovation, flavor diversity, and strategic collaborations. Smaller firms, however, are gaining ground by focusing on niche segments, such as low-alcohol and experimental brews. The competitive dynamics are further shaped by regulatory requirements, which mandate rigorous testing and compliance, creating barriers to entry for new entrants. Pricing pressures also influence competition, as companies strive to offer cost-effective solutions without compromising quality. Despite these challenges, the market’s growth potential remains robust, fueled by increasing demand for artisanal beverages and advancements in brewing technologies.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, BrewDog launched a new line of low-alcohol craft beers designed for health-conscious consumers. This initiative aimed to address unmet market needs and expand its product portfolio.

- In March 2025, Carlsberg acquired a startup specializing in experimental hop varieties. This acquisition was anticipated to enhance its capabilities in flavor innovation.

- In May 2025, Heineken partnered with a Dutch renewable energy provider to integrate solar panels into its brewing facilities. This collaboration sought to promote sustainable energy solutions.

- In July 2025, AB InBev introduced a subscription-based online platform for delivering craft beer directly to consumers. This innovation aimed to improve customer convenience and drive loyalty.

- In September 2025, Pilsner Urquell expanded its production facilities in the Czech Republic to meet the growing demand for traditional lagers. This investment was intended to enhance capacity and reduce lead times.

DETAILED SEGMENTATION OF EUROPE CRAFT BEER MARKET INCLUDED IN THIS REPORT

This research report on the europe craft beer market has been segmented and sub-segmented based on product type, distribution channel & region.

By Product Type

- Ale

- Lagers

By Distribution Channel

- On-Trade

- Off-Trade

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving growth in the craft beer market?

Key drivers include a rising number of microbreweries, increasing consumer interest in premium and artisanal beers, innovative flavor profiles, and health-conscious options such as low-alcohol and non-alcoholic beers

2. Who are the primary consumers of craft beer?

The primary consumers are typically younger demographics, particularly millennials, who seek unique and high-quality beer experiences. Surveys indicate a strong preference for specialty beers among urban populations

3. How important are online sales for craft beer?

Online sales have become increasingly important as consumers opt for convenience and variety. Many breweries are now utilizing direct-to-consumer models to enhance their reach

4. Which countries are leading in the growth of the craft beer market in Europe?

The countries leading in the growth of the craft beer market in Europe are United Kingdom, France, Germany, Estonia, and Switzerland.

5. Which distribution channels are most important in this market?

On-trade channels such as pubs, bars, and restaurants dominate, followed by off-trade channels including supermarkets, specialty stores, and online retail.

6. How is consumer preference shifting in the Europe craft beer market?

Consumers are shifting toward premium, low-alcohol, alcohol-free, organic, and sustainably produced craft beers.

7. What role does innovation play in the craft beer market?

Innovation in flavors, seasonal offerings, limited editions, and experimental brewing techniques plays a crucial role in attracting and retaining consumers.

8. What challenges does the Europe craft beer market face?

High competition, rising raw material costs, regulatory restrictions on alcohol, and limited shelf space are major challenges.

9. What opportunities exist in the Europe craft beer market?

Opportunities include expansion into non-alcoholic craft beer, exports, craft beer tourism, and collaborations with restaurants and events

10. What is the future outlook for the Europe craft beer market?

The market is expected to grow steadily, supported by premiumization, innovation, and rising demand for unique and authentic beer experiences.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com