Africa Construction Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Sector, Construction Type, Construction Method, Investment Source And Country (Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa), Industry Analysis From (2026 to 2034)

Market Size, 2025

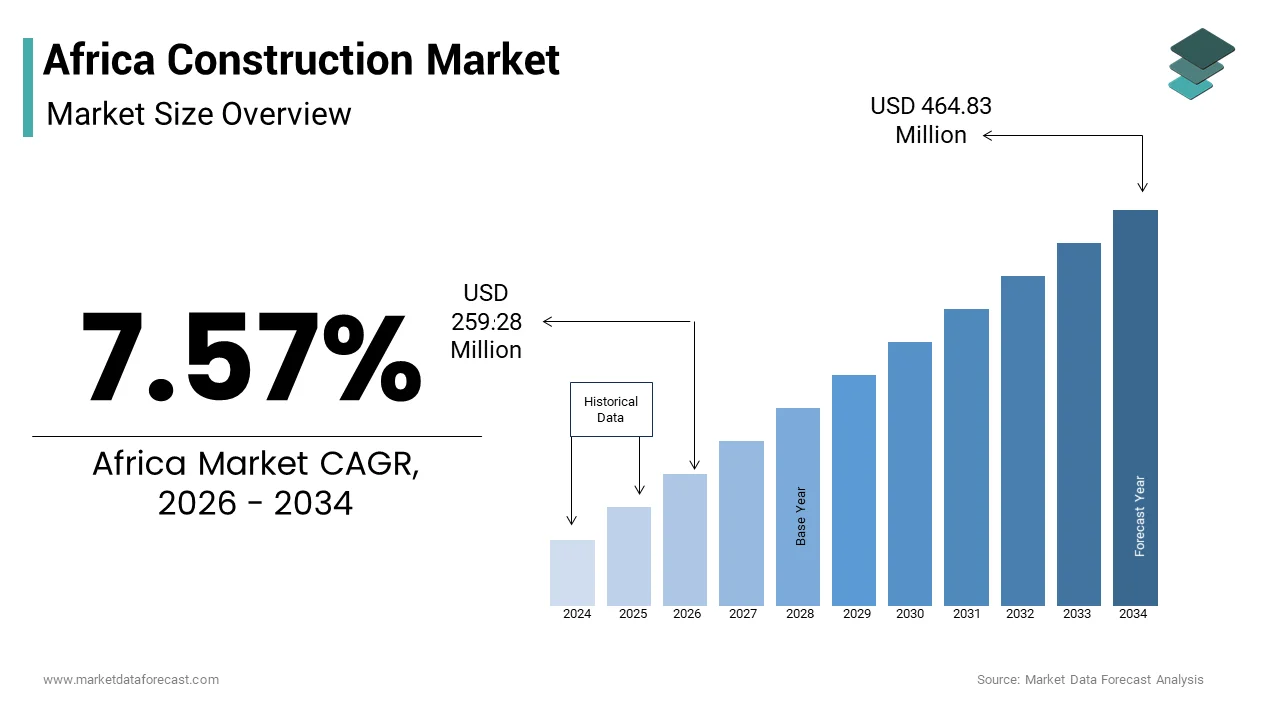

$241.03 MnMarket Estimate, 2026

$259.28 MnMarket Forecast, 2034

$464.83 MnCAGR, 2026–2034

7.57%Africa Construction Market Report Summary

The Africa construction market was valued at USD 241.03 million in 2025, is estimated to reach USD 259.28 million in 2026, and is projected to reach USD 464.83 million by 2034, expanding at a CAGR of 7.57% during the forecast period from 2026 to 2034. The Africa construction market is witnessing strong momentum, driven by rapid urbanization, population growth, and rising investments in residential, commercial, industrial, and public infrastructure projects. Governments across the region are prioritizing large-scale transportation networks, affordable housing developments, energy facilities, and smart city initiatives to address growing infrastructure demands and support long-term economic development. Increasing foreign direct investment, public-private partnerships, and funding from international development institutions are further accelerating construction activity across key African economies. In addition, the expansion of manufacturing hubs, logistics infrastructure, and renewable energy projects is creating substantial opportunities for contractors, engineering firms, and infrastructure developers throughout the continent.

Key Market Trends

- Governments are increasing investments in transportation, energy, water, and urban infrastructure to support long-term economic growth and regional connectivity.

- Affordable housing initiatives are driving significant residential construction activity across rapidly urbanizing African cities.

- Public-private partnerships and international financing are accelerating the execution of large-scale infrastructure and industrial development projects.

- Adoption of digital construction technologies, Building Information Modeling (BIM), and modern project management solutions is improving construction efficiency and project delivery.

- Sustainable building practices, green construction materials, and energy-efficient infrastructure are gaining greater importance across public and private sector developments.

Segmental Insights

Based on sector, the residential construction segment accounted for 43.1% of total African construction activity in 2025. The segment continues to dominate due to rapid population growth, increasing urban migration, rising demand for affordable housing, and government-led residential development programs across major African economies.

Based on construction type, the new construction segment represented 64.1% of the total construction value in 2025. Ongoing investments in new infrastructure, expanding urban development projects, industrial facilities, and large-scale public works continue to strengthen the segment's leadership across the continent.

Regional Insights

Nigeria emerged as the leading construction market in Western Africa by accounting for 31.3% of the region's total construction value in 2025, supported by expanding transportation infrastructure, housing projects, and energy investments. South Africa continues to play a pivotal role in Southern Africa through its well-developed construction ecosystem, diversified economy, and ongoing commercial and infrastructure developments. Kenya remains a major construction hub in Eastern Africa, benefiting from its strategic geographic location, improving investment climate, and growing regional infrastructure projects. Egypt is experiencing exceptional construction activity driven by ambitious government-led megaprojects, including the New Administrative Capital and extensive transportation and urban development initiatives. Ethiopia has also emerged as a significant construction market in the Horn of Africa, supported by expanding infrastructure investments, industrial parks, and long-term national development programs.

Competitive Landscape

The Africa construction market is highly competitive, with international engineering firms, regional contractors, and domestic construction companies competing across infrastructure, residential, commercial, industrial, and energy projects. Leading market participants are expanding their capabilities through strategic partnerships, mergers, acquisitions, and joint ventures while investing in advanced construction technologies, digital project management platforms, and sustainable building practices. Companies are increasingly focusing on infrastructure modernization, renewable energy developments, transportation networks, and smart city projects to strengthen their market presence across high-growth African economies. Investments in local workforce development, supply chain optimization, and environmentally responsible construction methods are further enhancing long-term competitiveness. As governments continue to prioritize infrastructure expansion and economic diversification, technological innovation, execution efficiency, and integrated project delivery will remain critical success factors within the African construction market.

Prominent players in the Africa construction market include China Communications Construction Group Ltd., China Railway Construction Corp. Ltd., Vinci SA, Dangote Group, Bouygues SA, Aveng Ltd., WBHO (Wilson Bayly Holmes-Ovcon), Orascom Construction, Bam International, Shapoorji Pallonji Group, Julius Berger Nigeria PLC, Sonatrach (Infrastructure Arm), Consolidated Contractors Company (CCC), China National Machinery Industry Corp. (Sinomach), Power Construction Corp. of China (PowerChina), Shapoorji Pallonji Africa, Group Five Construction, Arab Contractors, Dumez Nigeria PLC, and General Nile Company for Roads & Bridges.

Africa Construction Market Size

The African construction market size was valued at USD 241.03 million in 2025 and is anticipated to reach USD 259.28 million in 2026 to reach USD 464.83 million by 2034, growing at a CAGR of 7.57% during the forecast period from 2026 to 2034.

Construction is a dynamic and evolving landscape of infrastructure development, residential expansion, and commercial real estate growth across 54 diverse nations. Characterized by significant regional disparities, the sector is shaped by urbanization, public investment, and foreign development financing.

As of 2023, over 40% of Africa’s population resides in urban areas, a figure projected to rise to 50% by 2030 according to the United Nations Department of Economic and Social Affairs. This demographic shift exerts immense pressure on housing and transportation networks. Additionally, the African Development Bank indicates that the continent faces an annual infrastructure financing gap of approximately $68 billion, underscoring the scale of unmet demand. Regulatory frameworks, labor availability, and material sourcing further define the operational contours of construction activities across jurisdictions.

MARKET DRIVERS

Rapid Urbanization and Housing Deficit

Africa’s urban population is expanding at an unprecedented rate. The United Nations estimated that the continent will account for 25% of the world’s urban population growth between 2020 and 2050. This surge has intensified demand for residential infrastructure, particularly in megacities like Lagos, Nairobi, and Kinshasa, where housing deficits exceed 50 million units, as per the Centre for Affordable Housing Finance in Africa. In Nigeria alone, the annual housing shortfall is estimated at 700,000 units, driven by population growth outpacing construction capacity. Governments and private developers are increasingly compelled to invest in affordable housing projects to mitigate social pressures. For instance, Kenya’s “Affordable Housing Programme” under the Big Four Agenda targets 500,000 units by 2027, reflecting policy-level recognition of this demand. The scarcity of formal housing stock continues to fuel informal settlements, reinforcing the urgency for scalable construction solutions.

Continental Infrastructure Development Initiatives

The African Union’s Agenda 2063 envisions a fully integrated and industrialized continent, with infrastructure development as a cornerstone. This has catalyzed large-scale transport and energy projects across regional corridors. The African Development Bank confirms that over $130 billion is allocated to priority infrastructure projects under the Programme for Infrastructure Development in Africa (PIDA), including the Abidjan-Lagos Highway and the East African Railway. These initiatives stimulate demand for construction firms, engineering services, and local material supply chains. Furthermore, multilateral funding from institutions such as the Islamic Development Bank and the European Union continues to support feasibility studies and early-stage development, accelerating project execution.

MARKET RESTRAINTS

Chronic Shortage of Skilled Labour

The construction sector across Africa faces a critical deficit in skilled technical personnel, undermining project efficiency and quality. As per the International Labour Organization, only 18% of the workforce in sub-Saharan Africa has access to formal vocational training, severely limiting the availability of qualified engineers, masons, and electricians. In South Africa, the Construction Industry Development Board points out that over 60% of contractors cite skilled labor shortages as a primary operational constraint. This gap is exacerbated by brain drain. Training institutions struggle to keep pace with technological advancements, particularly in green building techniques and digital project management. Consequently, projects experience delays and cost overruns, deterring investor confidence and reducing competitiveness in public tenders.

Volatility in Building Material Supply Chains

Construction activities across Africa are frequently disrupted by inconsistent supply and escalating costs of essential materials such as cement, steel, and roofing sheets. According to the African Development Bank, import dependency for construction materials exceeds 40% in more than 20 African countries, exposing them to global price fluctuations and shipping delays. Moreover, local production capacity remains underdeveloped; for example, Nigeria produces only 30 million metric tons of cement annually against a demand of 45 million tons, as per the Nigerian Bureau of Statistics.

MARKET OPPORTUNITY

Adoption of Sustainable and Modular Construction Technologies

A growing emphasis on environmental resilience and cost efficiency is driving interest in sustainable building methods across Africa. As per the United Nations Environment Programme, buildings account for nearly 40% of energy-related carbon emissions globally, prompting regulatory shifts toward green construction. Countries like Rwanda and Ghana have introduced energy efficiency codes and incentives for eco-friendly designs. Modular and prefabricated construction is gaining traction, with firms such as 14 Trees in Kenya and Malawi deploying 3D-printed homes to address housing shortages. This technology reduces construction time. The International Finance Corporation estimates that green building investments in Africa could unlock $25 billion in economic value by 2030, signaling strong potential for innovation-led growth.

Expansion of Special Economic Zones and Industrial Parks

Governments across Africa are prioritizing industrialization through the development of special economic zones (SEZs) and industrial parks, creating substantial construction demand. As per the United Nations Economic Commission for Africa, over 560 SEZs are operational or under development across the continent, with Ethiopia hosting 37 and Senegal planning 12 new zones by 2027. These zones require comprehensive infrastructure, including warehouses, utilities, roads, and worker housing. For instance, the Dawa Industrial Park in Ethiopia spans 200 hectares and requires $1.2 billion in construction investment, funded jointly by the Ethiopian government and China’s EXIM Bank. Similarly, the Lekki Free Trade Zone in Nigeria, covering 16,000 hectares, is projected to generate over $60 billion in construction and operational activity over two decades, according to the Nigerian Export Processing Zones Authority. These projects attract foreign direct investment and stimulate local construction ecosystems.

MARKET CHALLENGES

Regulatory Fragmentation and Bureaucratic Delays

The African construction market contends with a complex web of regulatory standards and approval processes that vary significantly between and within countries. According to the World Bank’s “Doing Business” retrospective data, obtaining construction permits in sub-Saharan Africa takes an average of 152 days, nearly double the global average. In countries like the Democratic Republic of the Congo, overlapping jurisdictions between municipal, provincial, and national authorities lead to protracted approval timelines and inconsistent enforcement. Besides, zoning laws and land tenure systems remain ambiguous in many regions, particularly in rapidly urbanizing areas. These inefficiencies increase project risk, deter foreign investors, and inflate development costs, ultimately slowing the pace of infrastructure delivery.

Climate Vulnerability and Environmental Constraints

Construction projects across Africa are increasingly exposed to climate-related disruptions, including flooding, droughts, and extreme temperatures. As per the Intergovernmental Panel on Climate Change, Africa is warming faster than the global average, with significant implications for infrastructure durability. Coastal cities such as Lagos and Dar es Salaam face rising sea levels, with the World Resources Institute projecting that by 2050, over 150 million Africans could be affected by coastal flooding. In 2022, floods in South Africa’s KwaZulu-Natal province destroyed over 4,000 homes and damaged critical road networks, costing an estimated $1.5 billion in reconstruction, as reported by the South African National Disaster Management Centre. Additionally, water scarcity affects concrete curing and dust suppression, particularly in arid regions like the Sahel. These environmental pressures necessitate climate-resilient design standards, which many local firms lack the expertise or capital to implement, posing a systemic challenge to sustainable construction growth.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.57% |

| Segments Covered | By Sector, Construction Type, Construction Method, Investment Source, Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa |

| Market Leaders Profiled | China Communications Construction Group Ltd, China Railway Construction Corp. Ltd, Vinci SA, Dangote Group, Bouygues SA, Aveng Ltd, WBHO (Wilson Bayly Holmes-Ovcon), Orascom Construction, Bam International, Shapoorji Pallonji Group, Julius Berger Nigeria PLC, Sonatrach (Infrastructure arm), Consolidated Contractors Company (CCC), China National Machinery Industry Corp. (Sinomach), Power Construction Corp. of China (PowerChina), Shapoorji Pallonji Africa, Group Five Construction, Arab Contractors, Dumez Nigeria PLC, General Nile Company for Roads & Bridges |

SEGMENTAL ANALYSIS

By Sector Insights

The residential construction sector commanded the African construction market by accounting for 43.1% of total construction activity in 2025. This dominance of the segment is due to an acute housing deficit across urban and peri-urban centers, where population growth consistently outpaces housing delivery. The United Nations estimates that over 60% of Africa’s urban dwellers live in informal settlements, with countries like Nigeria and Kenya facing deficits of 22 million and 2 million units, respectively. This imbalance has triggered large-scale public-private housing initiatives. Moreover, rising youth demographics, where more than 70% of Nigeria’s population is under 30, fuel demand for first-time homeownership, further entrenching residential construction as the backbone of the sector.

The infrastructure (transportation) construction segment is emerging as the fastest-growing segment and is projected to expand at a CAGR of 8.7% between 2025 and 2033. This acceleration is driven by continental integration efforts and the urgent need to modernize outdated transport networks. According to the African Union, reports indicate that only 43% of rural Africans live within 2 kilometers of an all-season road, severely limiting economic access. In response, flagship projects such as the $2.3 billion Nairobi Expressway and the Abidjan-Ouagadougou Highway Corridor are reshaping regional connectivity. Additionally, urban mass transit systems are gaining momentum, with Lagos’ Blue and Red Rail Lines and Addis Ababa’s Light Rail system signaling a shift toward sustainable mobility.

By Construction Insights

The new constructions segment led within the African construction market by construction type and contributed an estimated 64.1% of total construction value in 2024. This dominance is underpinned by the foundational need to expand physical infrastructure across rapidly urbanizing economies. With Africa’s urban population expected to double by 2050, according to the United Nations Department of Economic and Social Affairs, entirely new residential neighborhoods, commercial hubs, and industrial zones are being developed from the ground up. In Rwanda, the Kigali Innovation City project spans 740 hectares and is being built entirely as a greenfield development, reflecting a broader trend across the continent. Similarly, Egypt’s New Administrative Capital, a $58 billion megaproject, is one of the most ambitious new city constructions globally. These large-scale initiatives, often backed by sovereign investment and foreign development finance, underscore the necessity of new builds in addressing structural deficits in housing, transport, and energy.

The additions and renovations segment is registering the highest growth rate among construction types, with a projected CAGR of 7.4% from 2025 to 2033. This surge is fueled by increasing asset optimization strategies in both public and private sectors, where expanding existing structures proves more cost-effective and faster than greenfield projects. Educational institutions are also driving demand. Additionally, adaptive reuse of industrial buildings into mixed-use spaces, such as the conversion of old warehouses in Cape Town into residential lofts, is gaining traction, supported by municipal incentives for urban densification and heritage preservation.

COUNTRY-LEVEL ANALYSIS

Nigeria Construction Market Analysis

Nigeria stood as the dominant construction market in Western Africa by capturing an estimated 31.3% of the region’s total construction value in 2024. Despite macroeconomic volatility, Nigeria’s construction sector remains buoyant due to its massive population-driven demand and federal infrastructure commitments. The country faces a housing shortfall of 22 million units, as per the Nigerian Institute of Building, necessitating large-scale residential developments. Projects like Federal Housing Estate in Lekki and private initiatives by developers such as Redbrick Homes are scaling delivery. Simultaneously, transportation infrastructure is being prioritized. Although foreign exchange constraints and material import dependence pose challenges, public-private partnerships and real estate investment trusts are gradually improving capital access.

South Africa Construction Market Analysis

South Africa holds a pivotal position in Southern Africa’s construction landscape. The country’s relatively mature regulatory environment and developed financial systems enable complex project financing, particularly in energy and commercial infrastructure. Eskom’s Just Energy Transition Investment Plan includes the construction of 12.5 GW of renewable energy capacity by 2030, catalyzing utility-scale solar and wind farm developments. Additionally, the Industrial Development Corporation committed a substantial amount to infrastructure projects in Special Economic Zones like Coega and Dube TradePort. However, structural constraints such as load-shedding and municipal insolvency affect project timelines. Despite this, South Africa remains a hub for engineering expertise and construction innovation, with firms like Group Five and Murray & Roberts executing cross-border projects.

Kenya Construction Market Analysis

Kenya is a leading construction market in Eastern Africa. The country’s strategic location and political stability have made it a gateway for regional infrastructure investment. The Standard Gauge Railway (SGR), though partially completed, has already mobilized funds in construction activity, with phase two expected to generate an additional $3.2 billion in contracts. Nairobi’s real estate market is also expanding. The government’s Affordable Housing Programme aims to deliver 500,000 units by 2027, attracting developers like Acorn Holdings and Gertrude’s Children’s Hospital Housing Initiative. Moreover, geothermal energy construction in the Rift Valley, where Kenya generates 38% of its electricity from geothermal sources, as reported by the Kenya Electricity Generating Company, adds a unique dimension to its construction profile.

Egypt Construction Market Analysis

Egypt leads Northern Africa’s construction sector. The country’s state-driven development model has unleashed an unprecedented wave of megaprojects, most notably the New Administrative Capital, which spans 700 square kilometers and is expected to house 6.5 million people. Over 20 ministries have already relocated, and construction of residential towers, diplomatic quarters, and the Iconic Tower, Africa’s tallest building, is progressing rapidly. Additionally, renewable energy construction is accelerating; the Benban Solar Park, one of the world’s largest photovoltaic installations, has a capacity of 1.8 GW and attracted $2 billion in investment, as confirmed by the New and Renewable Energy Authority. These initiatives position Egypt as a continental leader in state-led construction transformation.

Ethiopia Construction Market Analysis

Ethiopia has emerged as a key construction player in the Horn of Africa. Despite recent political instability, the country continues to advance large-scale infrastructure to support its industrialization agenda. The Ethiopian government has invested in industrial parks since 2015, including the Hawassa and Bole Lemi parks, which have attracted foreign manufacturers in textiles and pharmaceuticals. Residential construction is also expanding. The Grand Ethiopian Renaissance Dam represents one of Africa’s most significant energy construction endeavors, with 85% completion reported by the Ministry of Water and Energy in 2023. These projects underscore Ethiopia’s ambition to leverage construction as a catalyst for economic transformation.

COMPETITIVE LANDSCAPE

The competition in the African construction market is highly fragmented, characterized by a mix of multinational firms, regional contractors, and local enterprises vying for dominance across diverse geographies and sectors. While global players like Bouygues and Vinci bring technical expertise and capital, domestic firms such as Dangote and Concor leverage deep market knowledge and political relationships. Competitive advantage is increasingly defined by financial resilience, access to skilled labor, and technological adoption rather than scale alone. Public procurement processes often favor consortium bids, encouraging collaboration over direct rivalry. However, price undercutting and project delays remain common challenges. The rise of Chinese state-backed firms adds another layer of competition, particularly in infrastructure projects funded through bilateral agreements. As demand grows, differentiation through innovation, sustainability, and localized delivery models is becoming critical for long-term market positioning.

KEY MARKET PLAYERS

These are the market players that are dominating the African construction market.

- China Communications Construction Group Ltd

- China Railway Construction Corp. Ltd

- The Bouygues Construction Africa Division (Colas Group & Bouygues TP)

- Vinci SA

- Concor Construction (South Africa)

- Dangote Group

- Bouygues SA

- Aveng Ltd

- WBHO (Wilson Bayly Holmes-Ovcon)

- Orascom Construction

- Bam International

- Shapoorji Pallonji Group

- Julius Berger Nigeria PLC

- Sonatrach (Infrastructure arm)

- Consolidated Contractors Company (CCC),

- China National Machinery Industry Corp. (Sinomach)

- Power Construction Corp. of China (PowerChina)

- Shapoorji Pallonji Africa

- Group Five Construction

- Arab Contractors

- Dumez Nigeria PLC

- General Nile Company for Roads & Bridges

Top Players In The Market

- Dangote Group, headquartered in Nigeria, operates as a vertically integrated industrial conglomerate with a dominant footprint in construction materials and infrastructure development. The company’s construction influence stems from its massive cement production capacity—over 52 million tons annually across six African countries—ensuring supply chain control and project cost efficiency. In recent years, Dangote has expanded beyond materials into large-scale civil works, including the $19 billion Dangote Refinery in Lekki Free Trade Zone, one of the largest construction projects in Africa. The group has also invested in port infrastructure and road networks to support logistics. By leveraging its financial strength and local market knowledge, Dangote continues to secure government partnerships and execute complex projects, reinforcing its role as a key enabler of Nigeria’s infrastructure transformation and setting benchmarks for private-sector-led construction across West Africa.

- Operating across Francophone and Southern Africa, Bouygues Construction and its subsidiary Colas Group have established a robust presence in transportation and energy infrastructure. The firm has executed critical road, rail, and utility projects in countries such as Senegal, Côte d’Ivoire, and South Africa, leveraging French engineering standards and sustainable construction practices. In 2023, the company completed the Dakar-Diamniadio Toll Highway, a 36-kilometer expressway enhancing regional connectivity. Bouygues has also invested in digital construction technologies, including Building Information Modeling (BIM), to improve project delivery accuracy. By forming joint ventures with local firms and adhering to environmental compliance protocols, the group has strengthened its reputation for quality and reliability. Its ongoing participation in PIDA-aligned transport corridors underscores its strategic positioning in Africa’s long-term infrastructure development.

- Concor, a leading South African construction and engineering group, has played a pivotal role in shaping the country’s industrial and energy infrastructure. The company has delivered major projects in mining infrastructure, power plants, and water treatment facilities across Southern and East Africa. Notably, Concor was instrumental in constructing components of Eskom’s Medupi and Kusile coal-fired power stations, two of Africa’s largest energy projects. In 2022, it completed the Cennergi Kabula Energy Storage Facility, showcasing its adaptation to renewable energy trends. The firm has also embraced modular construction techniques to reduce project timelines. Despite financial restructuring in 2023, Concor retained core operational capabilities and secured contracts in Botswana and Namibia, demonstrating resilience. Its technical expertise and project management rigor continue to make it a preferred contractor for complex, high-value developments in the region.

Top Strategies Used by Key Market Participants

Key players in the African construction market employ strategic partnerships, technological integration, vertical integration, local capacity building, and diversification into green infrastructure to strengthen their positions. Firms increasingly form joint ventures with local contractors to navigate regulatory environments and access skilled labor. Investment in digital tools such as BIM, drones, and project management software enhances precision and reduces delays. Vertical integration—exemplified by Dangote’s cement-to-construction model—ensures material availability and cost control. Companies also prioritize workforce development through training academies to address skill shortages. Additionally, expanding into sustainable construction, including solar plants and eco-friendly housing, aligns with global financing trends and climate resilience goals. These strategies collectively enhance competitiveness, operational efficiency, and long-term project sustainability across diverse African markets.

RECENT MARKET NEWS

- In March 2023, Dangote Group inaugurated its integrated cement and logistics hub in Port Harcourt, Nigeria, enhancing supply chain efficiency and supporting large-scale infrastructure projects across the Niger Delta region.

- In July 2023, Bouygues Construction secured the contract to expand the Abidjan Metro Rail system in Côte d’Ivoire, marking its deepening commitment to urban mobility solutions in West Africa.

- In January 2024, Concor Construction announced a strategic partnership with Namibia’s Neopost Group to deliver industrial infrastructure projects in the Walvis Bay corridor, expanding its footprint in Southern Africa.

- In September 2023, Vinci Construction Grands Projets completed the Kigali Convention Centre in Rwanda, reinforcing its presence in high-profile public infrastructure across East Africa.

- In May 2024, Larsen & Toubro commenced construction of the Tema-Mpakadan Railway Line in Ghana, a $2 standard-gauge project aimed at transforming regional freight and passenger connectivity.

MARKET SEGMENTATION

This research report on the African construction market is segmented and sub-segmented into the following categories.

By Sector

- Residential

- Apartments/Condominiums

- Villas/Landed Houses

- Commercial

- Office

- Retail

- Industrial and Logistics

- Others

- Infrastructure

- Transportation Infrastructure (Roadways, Railways, Airways, others)

- Energy & Utilities

- Others

By Construction Type

- New Construction

- Renovation

By Construction Method

- Conventional On-Site

- Modern Methods of Construction (Prefabricated, Modular, etc.c)

By Investment Source

- Public

- Private

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

Frequently Asked Questions

What is the current market size of the construction industry in Africa?

As of 2024, the African construction market is estimated at USD 224.07 million. This includes residential, commercial, industrial, and infrastructure projects across 54 countries, with significant contributions from North and Sub-Saharan Africa.

What is the projected growth rate from 2025 to 2033?

The market is expected to grow at a CAGR of 7.57% from 2025 to 2033, reaching approximately USD 432.12 billion by 2033. This growth is driven by urbanization, government infrastructure programs, and foreign direct investment (FDI).

Which African countries are leading the construction boom?

Nigeria, Egypt, Kenya, South Africa, Ethiopia, and Morocco are the top contributors. Egypt leads in large-scale urban development (e.g., New Administrative Capital), while Kenya and Ethiopia are expanding transport and energy infrastructure.

How is urbanization shaping construction demand?

Africa is urbanizing faster than any other continent. By 2030, over 500 million people are expected to live in African cities. This is fueling demand for affordable housing, commercial buildings, water systems, and mass transit — especially in Lagos, Nairobi, Addis Ababa, and Kinshasa.

What role do international investors and development banks play?

Multilateral institutions like the African Development Bank (AfDB), World Bank, and China’s Exim Bank fund over 40% of large infrastructure projects. Private equity and Gulf-based investors are also increasing stakes in real estate and industrial construction.

Are local construction firms able to compete with international contractors?

While international firms dominate large, complex projects (especially in oil & gas and mega-infrastructure), local companies are gaining ground in mid-sized residential and municipal projects. Partnerships between local and foreign firms are becoming common to navigate regulatory and logistical challenges.

How is technology adoption impacting construction in Africa?

Technology use is growing slowly but steadily. Some firms are adopting Building Information Modeling (BIM) for complex projects, while mobile-based project management tools are improving site coordination. Drones are being used for surveying in remote areas, and 3D printing is being piloted for low-cost housing in Rwanda and Kenya.

Is sustainable construction gaining traction?

Yes. Green building practices are emerging in South Africa, Morocco, and Ghana, where developers are using solar-integrated designs, rainwater harvesting, and locally sourced materials. However, widespread adoption is limited by higher upfront costs and lack of certification frameworks.

How does political stability affect construction activity?

Political instability in regions like the Sahel, Sudan, and parts of Central Africa deters investment and delays projects. In contrast, stable countries like Rwanda, Botswana, and Senegal are attracting more construction FDI due to predictable governance and policy continuity.

What is the average project timeline for major construction developments?

Large infrastructure projects typically take 3 to 7 years from planning to completion, with frequent delays due to funding gaps or regulatory issues. Residential projects in private developments can be completed in 12–24 months, depending on scale.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com