Africa Mobile Payments Market Size, Share, Trends & Growth Forecast Report By Technology (NFC, Direct Mobile Billing, Mobile App, Others), Payment Type (B2B, B2C, B2G, Others), Location, End-Use, and Country (Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa) – Industry Analysis, 2026 to 2034

Africa Mobile Payments Market Size

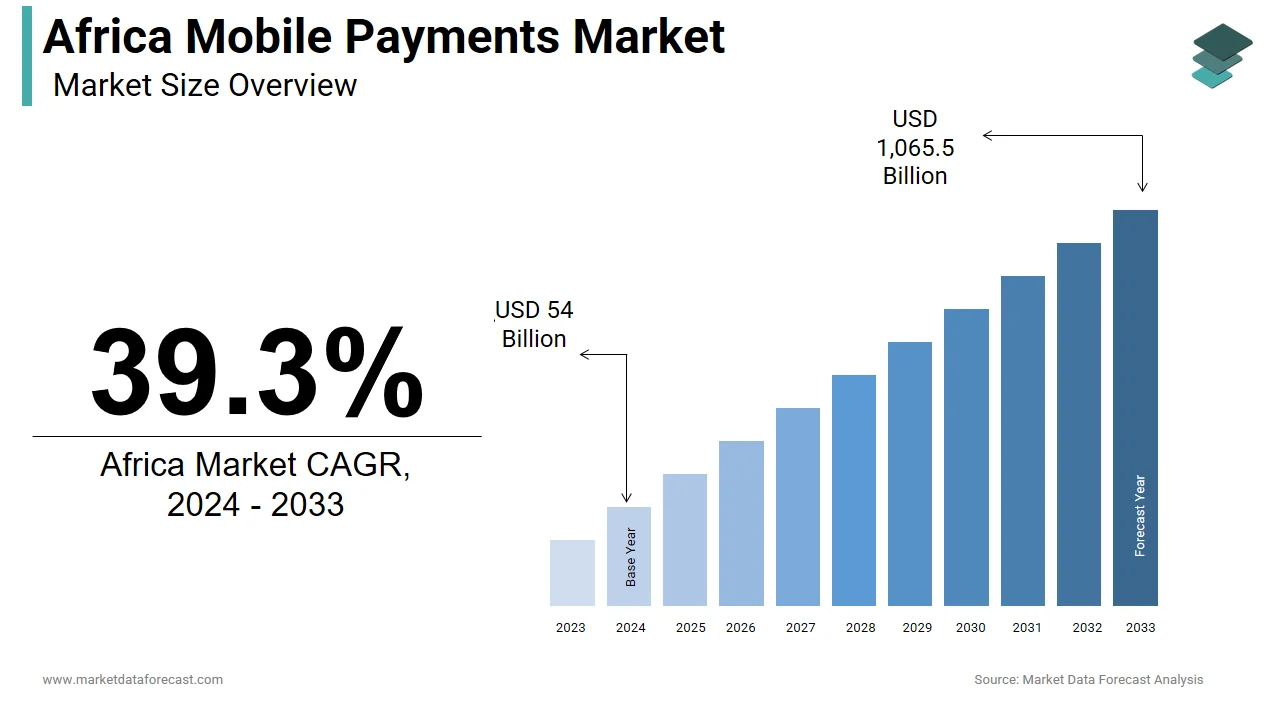

The size of the Africa mobile payments market was valued at USD 75.22 billion in 2025. This market is expected to grow at a CAGR of 39.3% from 2026 to 2034 and be worth USD 1,486 billion by 2034 from USD 105 billion in 2026.

Mobile payments are an ecosystem of digital financial transactions conducted via mobile devices, enabling users to send, receive, and manage money without reliance on traditional banking infrastructure. This sector has evolved as a cornerstone of financial inclusion across the continent, especially in regions where access to formal banking services remains limited. Countries like Kenya, Nigeria, Ghana, and Tanzania have emerged as key markets, driven by rising smartphone penetration, expanding mobile network coverage, and growing trust in mobile-based financial solutions.

Mobile payments in Africa are not only reshaping consumer behavior but also transforming economies. The market has become an essential tool for small businesses, rural communities, and informal traders, offering secure and convenient alternatives to cash-based transactions. Unlike traditional payment systems, mobile money platforms often operate through USSD codes or SMS, making them accessible even on basic feature phones. This adaptability has made mobile payments a lifeline for millions of Africans, fostering economic resilience and innovation across the continent.

MARKET DRIVERS

Rapid Expansion of Smartphone Penetration and Mobile Internet Adoption

The rapid expansion of smartphone penetration and mobile internet adoption is one of the most significant drivers of the africa mobile payments market. According to the International Telecommunication Union (ITU), mobile cellular subscriptions in Africa grew from approximately 650 million in 2015 to over 1 billion by 2023, representing a compound annual growth rate of nearly 5%. This proliferation of mobile connectivity has laid the foundation for the widespread use of mobile payment platforms, particularly among younger, tech-savvy demographics.

Smartphone adoption in Africa has been particularly transformative. This trend is further supported by decreasing smartphone prices and increasing affordability of mobile data plans, which have enabled broader access to mobile wallets, peer-to-peer transfers, and digital banking applications.

Moreover, mobile network operators have expanded their infrastructure into previously underserved rural areas, improving both coverage and reliability. As a result, mobile payments have become increasingly viable for daily commerce, utility bill payments, and microfinance services. This technological leapfrogging, bypassing traditional banking channels, has positioned mobile payments as a critical enabler of financial inclusion and economic participation across the African continent.

High Levels of Financial Exclusion and Demand for Alternative Banking Solutions

The historically high levels of financial exclusion and the corresponding demand for alternative banking solutions is another major driver of the Africa mobile payments market. According to the World Bank’s Global Findex Database 2021, approximately 57% of adults in Sub-Saharan Africa remained unbanked, compared to a global average of around 30%. This gap has created fertile ground for mobile money services, which offer accessible, low-cost financial tools to individuals who lack access to traditional banking institutions.

In response, mobile network operators and fintech companies have developed innovative platforms that allow users to store value, transfer funds, pay bills, and even access credit all through a mobile phone. For instance, in Tanzania, mobile money accounts outnumbered bank accounts by a ratio of 4:1 as of 2023, as reported by the Bank of Tanzania.

These platforms have proven especially valuable in rural areas, where physical bank branches are scarce and transportation to financial centers is costly or impractical. Mobile payments thus serve as a vital bridge, enabling users to participate in the formal economy, save securely, and access emergency funds quickly.

MARKET RESTRAINTS

Limited Regulatory Harmonization Across African Markets

The lack of regulatory harmonization across national jurisdictions is a major restraint impeding the growth of the africa mobile payments market. While several African countries have established robust legal frameworks for mobile money operations, others lag, creating inconsistencies that hinder cross-border interoperability and large-scale integration.

This fragmented regulatory landscape complicates compliance for mobile money operators aiming to expand beyond domestic markets. For example, in Nigeria, the Central Bank introduced stringent Know Your Customer (KYC) requirements and transaction limits in 2022, while neighboring Benin maintained more lenient policies. Such discrepancies create operational inefficiencies and increase costs for service providers attempting to standardize their offerings across borders.

Apart from these, differences in taxation policies pose another challenge. In Kenya, mobile money transactions are subject to a 1.5% excise duty, whereas in Ghana, mobile money transfers were taxed at 1% before being temporarily suspended in 2023 due to public backlash. These variations not only affect user adoption rates but also discourage foreign investment in regional fintech ecosystems.

Furthermore, inconsistent anti-money laundering (AML) and counter-terrorism financing (CTF) laws make it difficult to establish unified digital payment corridors.

Persistent Digital Literacy Gaps among Rural and Elderly Populations

The persistent digital literacy gap, particularly among rural and elderly populations is another significant constraint on the Africa mobile payments market. Despite the rapid spread of mobile technology, a substantial portion of the population lacks the skills necessary to navigate digital financial tools effectively. According to UNESCO, in 2023, adult literacy rates in Sub-Saharan Africa averaged just 66%, significantly lower than the global average of 86%. In countries like Niger and South Sudan, literacy rates fell below 30%, limiting the ability of large segments of the population to engage confidently with mobile money platforms.

Digital literacy challenges are compounded by generational divides. As per a study by study ICT Africa in 2022, only 35% of individuals aged 55 and above in Kenya, Ghana, and Senegal used mobile money regularly, compared to over 70% among those aged 18–35. This disparity spotlighted how older populations, despite having mobile phones, often rely on intermediaries to perform digital transactions, undermining the efficiency and security of mobile payments.

Moreover, in rural areas, where mobile money could have the greatest impact, awareness campaigns and training initiatives remain insufficient. Consequently, misconceptions about digital finance persist, discouraging adoption and limiting the scalability of mobile payment solutions across the continent.

MARKET OPPORTUNITIES

Integration of Mobile Money with E-commerce Platforms

The integration of mobile money with e-commerce platforms, opening new avenues for digital commerce and financial engagement is a major opportunity emerging within the Africa mobile payments market. As internet penetration expands and smartphone usage grows, online shopping is gaining traction across the continent. According to the United Nations Conference on Trade and Development (UNCTAD), e-commerce sales in Africa reached approximately $25 billion in 2023, with projections indicating a double-digit growth rate over the next five years.

Mobile money serves as a natural payment gateway for these digital transactions, especially given the limited reach of credit cards and online banking in many African markets. Major marketplaces such as Jumia and Konga have integrated mobile wallet options, allowing consumers to complete purchases seamlessly without requiring a bank account.

Kenya’s M-Pesa has also partnered with various online retailers to facilitate mobile-based checkout processes. This convergence between mobile payments and online retail not only enhances consumer convenience but also expands revenue streams for service providers.

Furthermore, the rise of social commerce, where users transact via social media platform,s is accelerating this trend. With mobile money embedded into WhatsApp, Facebook Shops, and Instagram, users can now shop and pay digitally using familiar communication tools. This evolution gives a transformative opportunity for the mobile payments market to deepen its integration into everyday commerce across Africa.

Expansion of Mobile-Based Microcredit and Lending Services

The expansion of mobile-based microcredit and lending services is an emerging opportunity within the Africa mobile payments market. Traditional banking systems often exclude low-income individuals and small business owners due to a lack of collateral or formal credit history. However, mobile money platforms have begun leveraging transactional data to assess creditworthiness, enabling the delivery of microloans directly through mobile wallets.

In Kenya, M-Shwari which is a savings and loan product offered jointly by Safaricom and Commercial Bank of Africa had disbursed over $1.5 billion in microloans by the end of 2023, with a repayment rate exceeding 90%, as per the Central Bank of Kenya. These services are particularly beneficial for informal sector workers, including artisans, traders, and farmers, who rely on quick access to capital for business expansion.

MARKET CHALLENGES

Cybersecurity Vulnerabilities and Fraud Risks

The growing risk of cybersecurity vulnerabilities and fraud is a pressing challenge facing the Africa mobile payments market. As mobile money adoption accelerates, so too does the interest of cybercriminals seeking to exploit weaknesses in digital transaction systems. According to the African Union’s African Cybersecurity Yearbook 2023, reports of mobile money-related fraud increased significantly between 2021 and 2023, with losses amounting to hundreds of millions of dollars across the continent.

The prevalence of SIM swap fraud, where attackers gain control of a victim's phone number to access their mobile money account is one of the primary concerns. In South Africa, mobile network provider MTN reported a 200% surge in SIM swap attacks in 2023, prompting regulatory scrutiny and calls for stronger identity verification protocols. Likewise, in Nigeria, the Economic and Financial Crimes Commission (EFCC) recorded over 1,500 cases of mobile money fraud during the same period, drawing attention to the urgent need for enhanced security measures.

Despite efforts by regulators and mobile money providers to implement two-factor authentication and biometric verification, many users remain vulnerable due to weak password habits and limited awareness of phishing scams. Besides, the lack of standardized cybersecurity policies across African markets exacerbates the problem, leaving smaller operators particularly exposed.

Infrastructure Limitations in Rural and Underserved Areas

Infrastructure limitations in rural and underserved areas present a formidable challenge to the sustained growth of the Africa mobile payments market. Although mobile network coverage has expanded significantly, gaps persist, particularly in remote regions where electricity supply is unreliable and internet connectivity is intermittent. According to the World Bank’s 2023 Africa’s Pulse report, only 43% of the rural population in Sub-Saharan Africa had access to stable electricity, severely constraining the usability of mobile devices for financial transactions.

Internet penetration follows a similar pattern. As per the indications from the data of the International Telecommunication Union (ITU), while urban areas in countries like Kenya and Ghana enjoy over 70% internet penetration, rural zones often fall below 20%, limiting the ability of residents to engage in mobile-based financial activities. Even when mobile networks are available, poor signal strength and outdated technologies such as 2G networks hinder real-time transaction processing, leading to failed payments and user frustration.

Apart from these, the lack of agent networks in remote locations poses a barrier to cash-in and cash-out operations, which are essential for mobile money usability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Payment Type, Location, End-Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa |

| Market Leaders Profiled | Google (Alphabet Inc), Alipay, Amazon.com, Inc. (Amazon Payments), Apple, Inc. (Apple Pay), C-SAM, Inc. (MasterCard Incorporated), Tencent Holdings Ltd. (WeChat), MoneyGram International Inc., PayPal Holdings, Inc., Samsung Group (Samsung Pay), and Visa, Inc. |

SEGMENTAL ANALYSIS

By Payment Type Insights

The Business-to-Consumer (B2C) segment dominated the Africa mobile payments market by accounting for 45.5% of total transaction value in 2024. The increasing use of mobile payments for everyday consumer services such as utility bill payments, airtime top-ups, school fees, and retail purchases is one of the key drivers of the dominance of the Business-to-Consumer (B2C) segment. In Kenya, for instance, over 70% of M-Pesa transactions in 2023 were categorized under B2C, with utility providers like Kenya Power and Safaricom integrating mobile payment gateways directly into their billing systems, as per Safaricom’s annual financial report. According to a report by McKinsey & Company, B2C transactions contributed more than $180 billion to the continent’s mobile money ecosystem, underpinned by widespread consumer adoption across both urban and rural economies.

Apart from these, the rise of digital wallets and mobile banking apps has further streamlined B2C interactions. Nigerian fintech firm Flutterwave reported that over 60% of its mobile transaction volume in 2023 came from B2C payments, particularly in e-commerce and subscription-based services.

The Business-to-Business (B2B) segment is emerging as the fastest-growing within the Africa mobile payments market, projected to expand at a CAGR of 22% between 2025 and 2033. The increasing digitization of supply chain and procurement processes is a primary driver behind the growth of the Business-to-Business (B2B) segment. Also, this rapid acceleration reflects a structural shift in how small and medium enterprises (SMEs), as well as large corporations, manage financial operations across the continent.

Companies like Sendy and Jumo have integrated mobile money platforms to facilitate real-time business disbursements, enhancing operational efficiency.

Moreover, regulatory support for digital financial infrastructure has accelerated B2B adoption. In Nigeria, the Central Bank’s Instant Payment (NIP) system linked to mobile money platforms enabled businesses to transact instantly across banks and mobile networks, leading to a 30% increase in B2B mobile transfers in 2023 compared to the previous year, as per the Nigerian Inter-Bank Settlement System (NIBSS).

By Location Insights

The remote payments segment held the biggest share of the Africa mobile payments market by contributing 65.5% of all mobile transactions in 2024. The widespread use of mobile money for remittances and peer-to-peer (P2P) transfers, especially among populations lacking access to traditional banking is largely driving the dominance of the remote payments segment. These are non-face-to-face transactions conducted via USSD codes, mobile apps, or web portals, typically used for sending money to family members, paying bills, or purchasing goods online.

In countries like Uganda and Tanzania, remote payments form the backbone of daily financial activity.

Furthermore, the integration of mobile wallets with e-commerce and utility services has reinforced the importance of remote payments. So, this continued expansion ensures that remote payments remain the most widely utilized mode of mobile financial interaction across Africa.

The proximity payments segment is currently the fastest-growing within the Africa mobile payments market, expanding at a CAGR of 28% in the future. The increasing acceptance of mobile-based POS systems among merchants, particularly in urban centers, is one of the main catalysts for the rapid growth of the proximity payments segment. In South Africa, for instance, over 30,000 new mobile POS terminals were deployed in 2023 alone, many of which supported proximity payments via mobile wallets, as reported by Nedbank. Similarly, in Nigeria, Quick Response (QR) code-based payments gained traction, with major retailers like Shoprite and Spar adopting mobile scanning solutions to facilitate seamless checkout experiences. Further, the growing preference for cashless transactions in response to hygiene concerns post-pandemic is another significant factor. A survey by FSD Africa in 2023 found that over 50% of urban consumers in Kenya and Ethiopia preferred using contactless mobile payments at physical stores due to perceived safety benefits.

COUNTRY-LEVEL ANALYSIS

Nigeria Mobile Payments Market Insights

Nigeria stood as the largest market in Africa for mobile payments by holding 25.4% of the regional transaction value in 2024. The country’s mobile payments landscape is driven by a combination of high financial exclusion and strong mobile network infrastructure. Operators such as MTN, Airtel, and indigenous fintech firms like Opay and Palmpay have played a pivotal role in scaling mobile payment services.

Moreover, regulatory developments such as the introduction of Super-Agent licenses in 2021 allowed non-bank entities to offer full financial services, accelerating last-mile delivery of mobile money in rural areas. Besides, the CBN’s push for instant payment systems (NIP) and interoperability between mobile money and bank accounts has enhanced transaction fluidity, reinforcing Nigeria’s leadership position in the African mobile payments space.

South Africa Mobile Payments Market Insights

South Africa’s mobile payments sector caters to both banked and unbanked populations, leveraging a sophisticated digital infrastructure. A key driver is the country’s high smartphone and internet penetration rates. According to Statistics South Africa, over 90% of households had access to a mobile phone in 2023, while over 70% of the population was actively using the internet. This digital readiness has enabled the rapid adoption of mobile wallets, contactless payments, and fintech applications.

Major players such as Vodacom (through VodaPay), Standard Bank, and Discovery Bank have integrated mobile payments into broader digital banking ecosystems. Moreover, the proliferation of QR code-based proximity payments, especially in urban retail and transport sectors, has boosted transaction frequency. The Reserve Bank’s supportive stance on digital finance, including ongoing efforts to establish a national payments system, positions South Africa as a model for advanced mobile payment adoption in the region.

Kenya Mobile Payments Market Insights

Kenya continues to be a trailblazer in the mobile payments market. The success of mobile payments in Kenya stems from early government support, robust agent networks, and deep integration of mobile money into daily economic activities. Beyond person-to-person transfers, mobile money is now embedded in utility payments, microcredit, insurance, and savings products. The Kenyan fintech ecosystem has also expanded significantly, with startups like Lipa Later and Cellulant facilitating digital commerce and cross-border payments via mobile platforms. With continuous innovation and policy backing, Kenya remains a dominant force in shaping Africa’s mobile payments future.

Ghana Mobile Payments Market Insights

Ghana has established itself as a key player in Africa’s mobile payments market. The country has witnessed a rapid expansion of digital financial services, driven by proactive regulatory reforms and growing collaboration between telecom operators and financial institutions. Ghana’s mobile money interoperability framework, launched in 2022, allows seamless fund transfers between different service providers, enhancing user convenience and driving adoption. Apart from these, the government’s implementation of the Ghana Interbank Payment and Settlement Systems (GhIPSS) Instant Pay platform has facilitated faster and cheaper transactions across mobile and banking channels. Initiatives like the National Identification System (GhanaCard) have also improved Know Your Customer (KYC) compliance, enabling broader participation in digital finance.

Rest of Africa Insights

The Rest of Africa collectively represents a substantial portion of the mobile payments market. This category includes dynamic and fast-evolving markets such as Tanzania, Uganda, Rwanda, Ethiopia, and Côte d'Ivoire, each contributing uniquely to the continent’s mobile payment ecosystem.

Tanzania, for example, saw mobile money transactions exceed $30 billion in 2023, with over 40 million registered users, according to the Bank of Tanzania. In Uganda, mobile money penetration reached over 70% of the adult population, driven by widespread use in rural remittances and microtransactions. Ethiopia, previously lagging due to restrictive regulations, began liberalizing its telecom sector in 2023, opening avenues for mobile money expansion. Rural connectivity initiatives and agent-driven financial inclusion strategies have fueled growth in these markets. Operators such as MTN, Orange, and local fintech startups are investing heavily in expanding agent networks and digital literacy programs.

COMPETITIVE LANDSCAPE

The competition in the Africa mobile payments market is highly dynamic, characterized by a mix of telecom operators, fintech startups, and traditional financial institutions vying for dominance. With mobile money serving as a gateway to financial inclusion, companies are continuously innovating to capture diverse customer segments across both urban and rural markets. Established telecom giants like Safaricom, MTN, and Orange leverage their extensive networks and brand recognition to maintain leadership positions. At the same time, agile fintech firms are entering the space with tailored digital solutions that challenge conventional models. Regulatory landscapes vary across countries, influencing how quickly and effectively players can scale their operations. Interoperability between platforms is becoming a key battleground, as companies seek to enable seamless cross-network transactions. Besides, partnerships with global payment processors and investment from international venture capital firms are intensifying competition. As mobile payments become increasingly embedded in daily life, from retail and utilities to education and healthcare, the race to offer the most integrated, secure, and accessible services continues to accelerate.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Africa mobile payments market profiled in this report are

- Google (Alphabet Inc)

- Alipay

- Amazon.com, Inc. (Amazon Payments)

- Apple, Inc. (Apple Pay)

- C-SAM, Inc. (MasterCard Incorporated)

- Tencent Holdings Ltd. (WeChat)

- MoneyGram International Inc.

- PayPal Holdings, Inc.

- Samsung Group (Samsung Pay)

- Visa, Inc.

TOP LEADING PLAYERS IN THE MARKET

One of the leading players in the Africa mobile payments market is Safaricom (M-Pesa). As the pioneer of mobile money in Kenya, Safaricom revolutionized financial inclusion by introducing M-Pesa, which has since expanded across multiple African markets. Its platform enables millions to conduct secure transactions, access credit, and manage savings through their mobile devices. The company continues to drive innovation by integrating digital services with mobile payments.

Another major player is MTN Group, a pan-African telecommunications giant. MTN has played a crucial role in scaling mobile money across its footprint in over 20 countries. Through strategic partnerships and digital innovations, MTN has enhanced cross-border payments, merchant solutions, and agent banking, contributing significantly to the growth of mobile financial services across the continent.

A third key player is Orange Money, the fintech arm of Orange S.A., operating across several Francophone African countries. Orange Money has been instrumental in expanding mobile payments through user-friendly platforms that support remittances, bill payments, and microloans. Its commitment to financial inclusion and digital transformation continues to strengthen its presence in the African mobile payments ecosystem.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Africa mobile payments market are leveraging strategic partnerships to enhance service offerings and expand market reach. By collaborating with banks, fintech firms, and international payment networks, companies can integrate new functionalities such as cross-border remittances, merchant payments, and microcredit services into their platforms.

Another critical strategy is technology innovation and digital infrastructure development. Companies are investing in advanced mobile wallets, USSD-based solutions, and contactless payment systems to improve accessibility and user experience. These upgrades ensure seamless transactions even in low-connectivity environments, making mobile money more reliable for a broader population.

Lastly, agent network expansion and financial literacy initiatives are being prioritized to deepen market penetration. Operators are increasing the number of local agents to facilitate cash-in and cash-out operations, particularly in rural areas. Alongside this, they are launching awareness campaigns to educate users on safe and effective use of mobile payment services, thereby building trust and adoption.

RECENT MARKET DEVELOPMENTS

- In January 2024, Safaricom launched an upgraded version of M-Pesa featuring enhanced security protocols and deeper integration with third-party financial services, aiming to improve user experience and broaden transaction capabilities beyond peer-to-peer transfers.

- In March 2024, MTN announced a strategic partnership with a leading European payments provider to enable instant cross-border remittances, strengthening its position in international mobile money transfers and facilitating easier inflows from diaspora communities.

- In May 2024, Orange Money introduced a suite of digital lending products powered by AI-driven credit scoring, allowing unbanked users in Francophone Africa to access micro-loans directly through their mobile money accounts without collateral requirements.

- In July 2024, a Nigerian fintech firm backed by Visa expanded its QR code-based proximity payment solution to over 10,000 merchants, reinforcing efforts to digitize retail transactions and reduce reliance on cash in small business ecosystems.

- In September 2024, a pan-African mobile money operator rolled out a nationwide agent training program aimed at improving service quality, dispute resolution, and financial literacy among field agents, ensuring smoother last-mile delivery of mobile payment services.

MARKET SEGMENTATION

This Africa mobile payments market research report is segmented and sub-segmented into the following categories.

By Technology

- Near Field Communication

- Direct Mobile Billing

- Mobile Web Payment

- SMS

- Interactive Voice Response System

- Mobile App

- Others

By Payment Type

- B2B

- B2C

- B2G

- Others

By Location

- Remote Payment

- Proximity Payment

By End-Use

- BFSI

- Healthcare

- IT & Telecom

- Media & Entertainment

- Retail & E-commerce

- Transportation

- Others

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- Ghana

- South Africa

- Rest of Africa

Frequently Asked Questions

What drives growth in the Africa Mobile Payments Market?

Growth is fueled by smartphone adoption, fintech innovation, financial inclusion, and demand for fast, secure, and convenient payments

What are the main types of mobile payments in Africa?

Key types include mobile wallets, NFC payments, QR code transactions, SMS billing, and in-app payments for goods and services

Who are the leading players in the Africa Mobile Payments Market?

Major players include MTN, M-Pesa (Vodacom), Airtel, Orange, Visa, MasterCard, PayPal, Google, Apple, and local fintechs

How does mobile money differ from mobile payments in Africa?

Mobile money is a subset focused on P2P transfers and bill payments, while mobile payments also include retail, ticketing, and digital services

Which countries lead the Africa Mobile Payments Market?

Kenya, Nigeria, South Africa, Egypt, Ghana, and Morocco are the top markets for mobile payments adoption and transaction volume

What technologies power the Africa Mobile Payments Market?

Technologies include NFC, QR codes, SMS/USSD, mobile apps, encryption, and biometric authentication for secure transactions

How is financial inclusion impacted by the Africa Mobile Payments Market?

Mobile payments drive financial inclusion by providing banking access to unbanked populations, especially in rural and remote areas

What are the main use cases for mobile payments in Africa?

Popular use cases are P2P transfers, bill payments, merchant purchases, airtime top-ups, government services, and remittances

How are fintechs changing the Africa Mobile Payments Market?

Fintechs are introducing innovative solutions, expanding access, and integrating payments with savings, loans, and insurance products

What security measures are used in the Africa Mobile Payments Market?

Security includes encryption, biometric authentication, and regulatory compliance to protect personal and financial data

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com