Middle East and Africa Fintech Market Size, Share, Trends & Growth Forecast Report By Technology (API, Artificial Intelligence, Blockchain, and Distributed Computing), Service (Payment, Fund Transfer, Personal Finance, Loans, Insurance, and Wealth Management), Application(Banking, Insurance, and Securities), Deployment Mode(Cloud, and On-Premises) and Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, and Rest of MEA) - Industry Analysis From 2024 to 2033

Middle East and Africa Fintech Market Summary

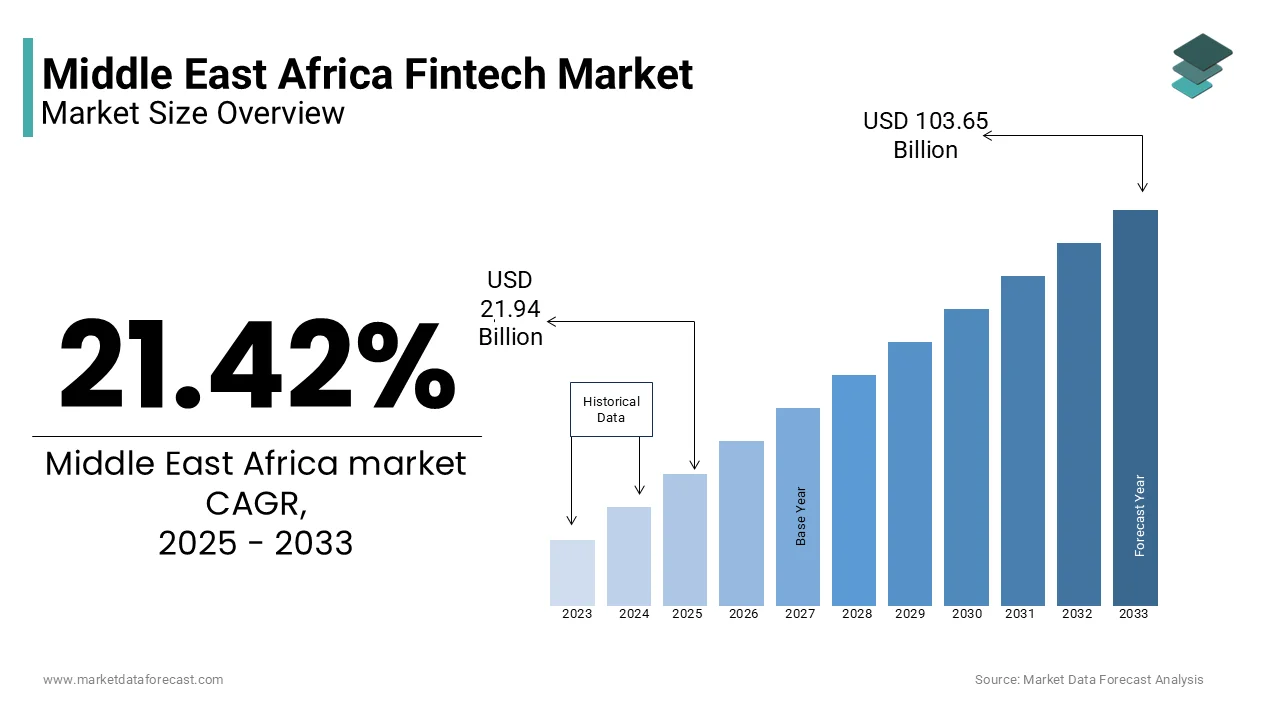

The Middle East and Africa fintech market was valued at USD 18.07 billion in 2024 and is projected to reach USD 103.65 billion by 2033, expanding at a CAGR of 21.42% during the forecast period. The growth of the fintech market in the Middle East and Africa is fueled by rapid digital transformation in financial services, rising adoption of mobile payments, government-led digital economy initiatives, and increasing venture capital investments in fintech startups across the region.

Key Market Trends

- Expansion of digital payment ecosystems and contactless transactions.

- Widespread adoption of API-driven open banking models to boost financial inclusion.

- Bank-fintech partnerships to accelerate digital lending and mobile-first banking solutions.

- Increasing traction of Buy Now, Pay Later (BNPL) services among millennials and Gen Z.

- Strong government initiatives in the UAE, Saudi Arabia, and South Africa to foster fintech innovation hubs.

Segmental Insights

- Based on technology, the API segment dominated the Middle East and Africa fintech market with a 42.5% share in 2024, supported by open banking adoption and integration-driven services.

- Based on service, the payments segment accounted for a 46.3% share in 2024, reflecting the shift toward digital wallets, cross-border remittances, and contactless transactions.

- Based on application, the banking segment commanded a 65.1% share in 2024, driven by mobile-first banking adoption, digital lending, and neobanking platforms.

Regional Insights

- The United Arab Emirates emerged as the fintech hub of the Middle East and Africa, commanding a 28.5% share in 2024, supported by progressive regulation and a thriving startup ecosystem.

- Saudi Arabia is rapidly advancing with Vision 2030-driven financial inclusion initiatives.

- South Africa leads sub-Saharan Africa with a mature digital payments ecosystem.

- Nigeria and Kenya are rising fintech hotspots, fueled by mobile money adoption and startup innovation.

Competitive Landscape

Leading players in the Middle East and Africa fintech market include Flutterwave, M-Pesa (Safaricom), STC Pay (Saudi Telecom Company), PayPal Holdings, Inc., Ant Group, Afterpay Limited, Google Pay (Alphabet Inc.), Nexi SpA, Klarna Bank AB, Social Finance, Inc., and Avant, LLC. These companies are focusing on scaling digital payments, investing in BNPL solutions, enhancing mobile-first platforms, and expanding regional collaborations to strengthen their market presence

Middle East and Africa Fintech Market Size

The fintech market in the Middle East and Africa is anticipated to reach USD 103.65 billion by 2033 from USD 18.07 billion in 2024, at a CAGR of 21.42%.

Fintech refers to the ecosystem of financial technology innovations transforming traditional financial services across banking, payments, lending, insurance, and wealth management. Characterized by rapid digital adoption and regulatory evolution, the sector is redefining financial inclusion and service delivery in regions historically marked by underbanked populations. Furthermore, the developments are not merely technological upgrades but represent a fundamental reconfiguration of financial infrastructure, where decentralized platforms, blockchain-based remittances, and AI-driven credit scoring are becoming institutionalized. The convergence of regulatory sandboxes, rising smartphone penetration, and youth-driven digital demand is creating a fertile ground for scalable fintech models across diverse economic landscapes.

MARKET DRIVERS

Expanding Mobile Penetration and Digital Identity Infrastructure

The proliferation of mobile connectivity across the Middle East and Africa has become a foundational enabler of fintech adoption, particularly in regions with limited traditional banking infrastructure. This expansion is complemented by national digital identity programs that enhance trust and verification in digital financial transactions. India’s Aadhaar model has inspired similar frameworks, with Nigeria’s National Identity Management Commission issuing millions of National Identification Numbers by 2023, enabling seamless KYC integration for fintech platforms. Moreover, the integration of biometric authentication and SIM-based verification has reduced onboarding friction, allowing neobanks like Nigeria’s Kuda and South Africa’s TymeBank to acquire millions of users within months of launch. This digital infrastructure leapfrogs legacy systems, allowing fintech providers to deploy scalable, low-cost solutions tailored to informal economies and rural populations.

Government-Led Financial Inclusion and Regulatory Innovation

Public sector initiatives across the Middle East and Africa have become pivotal in accelerating fintech adoption through strategic policy frameworks and institutional support. These regulatory advancements reduce entry barriers while ensuring consumer protection. Additionally, the African Union’s Digital Transformation Strategy for Africa 2020–2030 emphasizes cross-border interoperability of digital financial services, fostering regional integration. These top-down interventions create an ecosystem where fintech firms can operate with legal certainty, access public infrastructure, and align with national development goals, thereby amplifying demand for digital financial solutions.

MARKET RESTRAINTS

Fragmented Regulatory Landscapes and Compliance Complexity

The lack of harmonized regulatory frameworks, resulting in operational inefficiencies and increased compliance burdens, is a significant impediment to the scalability of fintech solutions across the Middle East and Africa. Each country maintains distinct licensing requirements, data localization laws, and anti-money laundering (AML) protocols, complicating cross-border expansion. Moreover, only a few African nations have established dedicated fintech regulations, leaving many startups navigating ambiguous legal environments. In West Africa, despite the existence of the Economic Community of West African States (ECOWAS), fintech firms face divergent tax regimes and capital adequacy rules, reducing economies of scale. Regulatory compliance costs consume a notable share of revenue for early-stage fintechs in countries like Tanzania and Angola. Moreover, the absence of unified data protection laws raises concerns about consumer trust and cybersecurity risks. In the Gulf, while the UAE and Bahrain have advanced regulatory sandboxes, neighboring jurisdictions lack equivalent mechanisms, forcing firms to duplicate compliance efforts. This fragmentation discourages investment and slows innovation, as companies must tailor products to each jurisdiction rather than deploying standardized solutions.

Cybersecurity Vulnerabilities and Digital Trust Deficits

The Middle East and Africa face escalating cybersecurity threats that undermine consumer confidence in fintech platforms. The situation is exacerbated by limited cybersecurity infrastructure and a shortage of skilled professionals. Furthermore, the absence of standardized incident reporting mechanisms hampers threat intelligence sharing. Without robust encryption standards, regulatory oversight, and public awareness campaigns, digital trust remains fragile, constraining the long-term growth of the fintech ecosystem.

MARKET OPPORTUNITIES

Expansion of Cross-Border Payment Corridors and Remittance Digitization

The digitization of remittance flows presents a transformative opportunity for fintech players in the Middle East and Africa, given the region’s reliance on international labor transfers. As per the World Bank’s Migration and Development Brief 2023, Sub-Saharan Africa received $54 billion in remittances in 2023, yet the average cost of sending $200 to the region remained at 8.2%, significantly above the global average of 6.3%. Fintech platforms leveraging blockchain and API-driven networks are positioned to reduce these costs and improve speed. The African Continental Free Trade Area (AfCFTA) agreement, which entered the operational phase in 2023, aims to establish a unified payments system across 55 countries, enabling seamless cross-border transactions. Ripple’s partnership with banks in Kenya and Ghana has already reduced settlement times from days to seconds. So, the untapped potential for fintech-driven efficiency gains remains substantial.

Embedded Finance and E-Commerce Ecosystem Integration

The convergence of fintech with e-commerce and gig economy platforms is unlocking new avenues for financial service delivery across the region. The e-commerce sales in the Middle East and North Africa grew, driven by platforms like Jumia, Souq, and Noon. This expansion creates fertile ground for embedded financial products such as buy-now-pay-later (BNPL), micro-insurance, and instant merchant financing. The African Development Bank points out that a smaller share of small merchants on digital marketplaces have access to working capital, indicating a vast underserved segment. Thus, the integration of financial services into non-financial platforms is poised to redefine customer acquisition and retention strategies, enabling hyper-personalized, context-aware financial solutions.

MARKET CHALLENGES

Talent Shortage and Skilled Workforce Gaps in Emerging Technologies

The rapid evolution of fintech in the Middle East and Africa is outpacing the availability of skilled professionals in critical domains such as artificial intelligence, blockchain engineering, and cybersecurity. Moreover, academic curricula in most regional universities lag behind industry demands. This talent deficit impedes product innovation, slows time-to-market, and increases dependency on offshore development teams, undermining the sustainability of homegrown fintech ecosystems.

Infrastructure Limitations in Connectivity and Power Supply

Despite digital ambitions, persistent gaps in physical and digital infrastructure constrain the reach of fintech services, particularly in rural and peri-urban areas. This digital divide limits the effectiveness of mobile-based financial services, which rely on stable connectivity for transaction processing and authentication. Additionally, as per the World Bank’s 2023 Africa Infrastructure Outlook, over 600 million people in Africa lack reliable electricity, with rural electrification rates averaging just 27%. In Nigeria, where fintech adoption is high in urban centers, only 45% of households have access to grid power, forcing reliance on expensive generators that increase operational costs for agents and merchants. These infrastructural deficiencies disrupt service continuity, reduce customer trust, and increase transaction failure rates. Without coordinated investment in fiber networks, renewable energy microgrids, and last-mile connectivity, the scalability of fintech solutions will remain uneven, reinforcing urban-rural disparities in financial access.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 21.42% |

| Segments Covered | By Technology, Service, Application, Deployment Mode, and Country |

|

Various Analyses Covered | Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, Rest Of GCC Countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, Rest Of MEA |

|

Market Leaders Profiled | PayPal Holdings, Inc., Ant Group, Afterpay Limited, Google Pay (Alphabet Inc.), Nexi SpA, Klarna Bank AB, Social Finance, Inc. and Avant, LLC |

SEGMENTAL INSIGHTS

By Technology Insights

The API (Application Programming Interface) segment dominated the Middle East and Africa Fintech Market by technology with an estimated 42.5% share in 2024. This lead position is due to the critical role APIs play in enabling interoperability between financial institutions, fintech startups, and third-party service providers. The rise of open banking frameworks across key markets is one primary driver of this dominance. Furthermore, the integrations facilitate real-time payments, fraud detection, and personalized financial products, making APIs the backbone of digital financial ecosystems. As governments and regulators push for financial inclusion through digital rails, the demand for secure, scalable, and compliant API infrastructure continues to surge, reinforcing its market leadership.

The artificial intelligence (AI) segment is expanding at the fastest pace within the technology classification and is registering a CAGR of 34.7% between 2025 and 2033 This acceleration is fueled by the urgent need for intelligent automation in credit scoring and risk management, particularly in markets with large unbanked populations lacking traditional credit histories. In Kenya, fintech lenders such as Tala and Branch utilize AI-powered algorithms to analyze alternative data, such as mobile usage patterns, social media behavior, and utility payments, to assess creditworthiness, achieving a high accuracy rate in predicting loan defaults. A further critical factor is AI’s role in fraud detection. With increasing investments from tech giants like Google and Microsoft in AI labs across Cairo and Nairobi, the region is building indigenous capacity to scale intelligent financial solutions, propelling AI to the forefront of technological adoption.

By Service Insights

The payments segment emerges as the largest service in the Middle East and Africa Fintech Market by accounting for a 46.3% of total revenue in 2024. This dominance is primarily driven by the widespread adoption of mobile money platforms, particularly in Sub-Saharan Africa, where cash remains the dominant transaction medium but digital alternatives are rapidly gaining traction. The platforms are not only replacing cash but also serving as gateways to broader financial services, such as savings and microloans. The integration of QR codes, biometric authentication, and cross-border remittance corridors has further solidified payments as the foundational layer of the fintech ecosystem, making it the most monetizable and scalable service segment across the region.

The loans segment is experiencing the fastest growth among all service categories and is projected to expand at a CAGR of 29.3% during the forecast period. This surge is fueled by the rising demand for digital credit among unbanked and underbanked populations, particularly in urban and peri-urban areas where traditional banks have limited reach. These platforms leverage alternative data analytics and AI to offer instant disbursements, with average loan approval times under five minutes. Another key driver is the integration of lending into e-commerce and gig economy platforms.

By Application Insights

The banking segment stands as the prominent application segment in the Middle East and Africa Fintech Market by commanding an estimated 65.1% of total share in 2024. This preeminence is anchored in the region’s structural shift toward digital banking, driven by both consumer demand and institutional transformation. In South Africa, digital banking transactions accounted for a notable share of all retail banking activities, with major banks investing substantial funds in digital infrastructure upgrades. The rise of neobanks such as TymeBank, which surpassed 8 million customers by 2023, reflects a broader trend of mobile-first banking adoption. In the Gulf, Saudi Arabia’s digital banking penetration reached 58% in 2023, up from 32% in 2020, as per the SAMA, fueled by the Vision 2030 agenda’s emphasis on financial digitization. Furthermore, the Central Bank of the UAE recorded that over 90% of personal banking services are now accessible via mobile apps, with digital onboarding times reduced to under ten minutes. The integration of biometric authentication, AI-driven customer service, and real-time transaction monitoring has redefined user expectations. Additionally, the African Union’s Digital Financial Services Strategy emphasizes digital banking as a key pillar for achieving 80% financial inclusion by 2030. With governments, regulators, and private institutions aligning around digital-first banking models, the segment remains the cornerstone of fintech applications across the region.

The securities segment is emerging as the fastest-growing application and is projected to grow at a CAGR of 31.8% from 2025 to 2033. This rapid expansion is driven by the democratization of investment access through digital brokerage platforms, particularly in countries with historically low retail participation in capital markets. A further key factor is the rise of fractional investing, allowing users to purchase partial shares in global equities. With financial literacy campaigns and regulatory easing on foreign exchange for investments, more consumers are engaging with securities, transforming the segment into a high-growth frontier for fintech innovation.

By Deployment Mode Insights

The cloud deployment mode held the biggest share of the Middle East fintech, and lenders are bridging this gap through low-cost distribution models and dynamic risk assessment, enabling financial inclusion while maintaining profitability. This leadership is driven by the need for scalable, cost-efficient, and agile infrastructure, particularly among startups and digital banks that lack legacy systems. With hyperscalers expanding their presence in the region and regulators developing cloud-specific compliance guidelines, the model is becoming the de facto standard for modern fintech operations.

The cloud segment is also the fastest-growing deployment mode and is expanding at a CAGR of 33.2% in the coming years. This growth is propelled by increasing regulatory acceptance and data sovereignty frameworks that enable secure cross-border operations. A different driver is the integration of hybrid cloud models that combine public and private infrastructure for enhanced security and performance. With cloud providers establishing local data centers in Johannesburg, Nairobi, and Riyadh, latency and data residency concerns are being addressed, further fueling growth.

COUNTRY-LEVEL ANALYSIS

United Arab Emirates Fintech Market Insights

United Arab Emirates was positioned as the undisputed fintech hub of the Middle East and commands an estimated 28.5% share of the Middle East and Africa Fintech Market. The country’s leadership is underpinned by a forward-looking regulatory environment and substantial government investment in digital infrastructure. Dubai’s Smart City initiative has integrated fintech into transportation, healthcare, and utilities, creating a seamless digital ecosystem. With the UAE hosting the largest concentration of venture capital funds in the region and hosting major events like STEP Conference, it continues to attract global talent and investment, solidifying its dominance.

Saudi Arabia Fintech Market Insights

Saudi Arabia holds a significant market share, driven by the ambitious financial transformation agenda under Vision 2030. The government’s push for a cashless society is evident in the adoption of the national QR code standard, which now covers a large number of merchants. Riyadh has emerged as a fintech investment hotspot. The establishment of the Fintech Saudi initiative has accelerated collaboration between banks, regulators, and innovators. Moreover, the female fintech participation rate has risen, one of the highest in the region, supported by government-backed entrepreneurship programs. With NEOM and other giga-projects integrating smart financial systems, Saudi Arabia is rapidly transitioning from oil dependency to digital financial leadership.

South Africa Fintech Market Insights

South Africa maintains a notable share of the MEA fintech market, serving as the technological and regulatory anchor for Sub-Saharan Africa. The country hosts the most mature financial ecosystem in Africa, with digital banking penetration increasing. The South African Reserve Bank’s Project Khokha, a blockchain-based interbank settlement pilot, demonstrated the feasibility of distributed ledger technology in real-world banking, influencing regional policy. TymeBank, a fully digital bank, is becoming the fastest-growing bank in the country’s history. The country is also a leader in insurtech, with platforms like OnePlan and Pineapple leveraging AI for on-demand coverage. Despite challenges like load-shedding and inequality, South Africa’s skilled workforce, developed capital markets, and proactive regulatory sandbox continue to attract investment, making it a pivotal player in the continent’s fintech evolution.

Egypt Fintech Market Insights

Egypt also captures a key share of the regional market, emerging as a fintech powerhouse in North Africa due to its large population and state-led digital transformation. The government’s “Digital Egypt” strategy has led to the creation of a substantial number of digital wallets through the national switch, InstaPay. The country’s fintech startups received significant funds in 2023. Cairo has become a talent hub, with fintech academies and incubators producing skilled developers. The integration of fintech into agriculture and microfinance is expanding financial access to rural populations, with millions of farmers now using mobile-based credit and insurance services. With strong government backing and a growing startup ecosystem, Egypt is positioning itself as a gateway for fintech expansion across the Arab world.

COMPETITIVE LANDSCAPE

The competitive landscape of the Middle East and Africa Fintech Market is marked by a dynamic interplay between homegrown innovators, telecom giants, traditional financial institutions, and global technology players. Unlike mature markets where competition centers on incremental improvements, the region’s fintech rivalry is defined by foundational innovation—building financial rails where none existed. Incumbent banks are under pressure to modernize, often responding through digital subsidiaries or partnerships with agile startups. Meanwhile, telecom operators leverage their vast subscriber bases to launch mobile money and digital banking services, creating a hybrid model of connectivity and finance. Independent fintechs distinguish themselves through niche specialization, such as micro-lending, remittances, or embedded finance, often tailoring solutions to local economic realities. Regulatory divergence across countries fosters both fragmentation and opportunity, allowing first-movers to establish dominance in specific jurisdictions. The race is not merely about market share but about shaping consumer behavior, setting technical standards, and influencing policy frameworks. As venture capital flows into the sector, consolidation is emerging, with larger players acquiring startups to expand capabilities. Ultimately, competition is accelerating financial inclusion, driving down costs, and redefining what it means to be financially empowered in emerging economies.

KEY MARKET PLAYERS

Companies playing a major role in the Middle East and Africa fintech market include

- Flutterwave

- M-Pesa (Safaricom)

- STC Pay (Saudi Telecom Company)

- PayPal Holdings, Inc.

- Ant Group

- Afterpay Limited

- Google Pay (Alphabet Inc.)

- Nexi SpA

- Klarna Bank AB

- Social Finance, Inc.

- Avant, LLC.

TOP LEADING PLAYERS IN THE MARKET

Flutterwave

Flutterwave has emerged as a transformative force in the African fintech landscape by building a robust payment infrastructure that enables seamless cross-border transactions for businesses and financial institutions. The company has played a pivotal role in unifying fragmented payment systems across multiple African countries, offering developers and enterprises a single integration point for local and global payment methods. Its technology stack supports card payments, mobile money, bank transfers, and digital wallets, making it a critical enabler of e-commerce and digital financial services. By focusing on reliability, scalability, and compliance, Flutterwave has become a preferred partner for multinational corporations, fintech startups, and governments seeking to digitize financial ecosystems. Its influence extends beyond Africa, as it facilitates international merchants’ access to African markets and empowers African businesses to transact globally. Through strategic partnerships and a developer-first approach, Flutterwave continues to shape the future of digital payments across emerging economies.

M-Pesa (Safaricom)

M-Pesa, pioneered by Safaricom in Kenya, revolutionized financial inclusion by introducing mobile money to populations with limited access to traditional banking. Its agent-based network and SMS-driven platform enabled millions of unbanked individuals to send, receive, and store money using basic mobile phones. Over time, M-Pesa evolved into a comprehensive financial ecosystem, offering savings, credit, insurance, and merchant payment solutions. Its success inspired similar models across Africa, Asia, and Latin America, establishing a global benchmark for mobile-led financial innovation. The platform’s interoperability with banks and other fintechs has strengthened its integration into national economies. M-Pesa’s resilience lies in its deep community penetration, trusted brand, and continuous product evolution. By demonstrating how technology can leapfrog traditional infrastructure, M-Pesa has become a symbol of inclusive finance and a blueprint for scalable fintech solutions in developing markets.

STC Pay (Saudi Telecom Company)

STC Pay has redefined digital finance in the Gulf by leveraging Saudi Arabia’s high mobile penetration and government-backed digital transformation agenda. As a licensed digital bank, it offers a full suite of financial services, including instant payments, peer-to-peer transfers, bill payments, and microloans, all accessible through a mobile app. The platform’s integration with national payment systems and public services has accelerated cashless adoption across the kingdom. STC Pay’s strength lies in its synergy with telecom infrastructure, enabling secure authentication and broad reach even in remote areas. It has also expanded into digital investments and merchant financing, positioning itself as a holistic financial platform. By combining telecom scale with financial innovation, STC Pay has become a key driver of financial inclusion in Saudi Arabia and a model for telco-led fintech expansion in regulated markets. Its success underscores the potential of converged digital ecosystems in advancing national economic visions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- One major strategy employed by leading fintech players in the Middle East and Africa is strategic partnerships with telecommunications providers, banks, and government entities. By aligning with established institutions, fintechs gain access to vast customer bases, regulatory legitimacy, and critical infrastructure, enabling faster deployment and trust-building in fragmented markets. These collaborations allow for seamless integration of financial services into existing digital and physical networks, enhancing reach and usability.

- Another key approach is product localization and contextual innovation. Top players design solutions that reflect regional consumer behaviors, economic conditions, and technological constraints. This includes supporting low-bandwidth interfaces, offline functionality, and multi-language support, ensuring accessibility across diverse user segments. By prioritizing user-centric design and cultural relevance, companies foster deeper engagement and long-term adoption.

- A third critical strategy is investment in agent and merchant network expansion. Fintech firms are building extensive on-the-ground ecosystems of agents and point-of-sale merchants to bridge the digital divide, especially in rural and underserved areas. These networks serve as physical touchpoints for cash-in and cash-out services, enhancing trust and usability for populations unfamiliar with digital-only platforms, thereby driving financial inclusion at scale.

Middle East and Africa Fintech Market News

- In March 2023, Flutterwave partnered with Mastercard to launch a pan-African business payment solution, enabling African enterprises to issue virtual cards and manage expenses globally. This collaboration is expected to enhance cross-border trade capabilities and solidify Flutterwave’s role as a bridge between African businesses and international markets.

- In June 2023, M-Pesa expanded its financial ecosystem by integrating with Kenya’s National Hospital Insurance Fund, allowing users to pay for healthcare services directly from their mobile wallets. This move is anticipated to deepen financial inclusion and strengthen M-Pesa’s position as a critical infrastructure for social and economic transactions.

- In January 2024, STC Pay launched a digital banking platform in Saudi Arabia, offering full banking services under a license from the Saudi Central Bank. This initiative is expected to accelerate the kingdom’s transition to a cashless economy and reinforce STC Pay’s leadership in the Gulf’s digital finance space.

- In September 2023, Paystack, a Nigerian fintech firm, introduced a new merchant lending program in partnership with local banks, enabling small businesses to access working capital based on transaction history. This expansion is anticipated to strengthen Paystack’s ecosystem and deepen its integration into Africa’s digital economy.

- In February 2024, TymeBank of South Africa announced a strategic alliance with a major retail chain to embed banking services into customer loyalty programs. This integration is expected to enhance user acquisition and promote everyday banking adoption among unbanked and underbanked populations.

MARKET SEGMENTATION

This research report on the Middle East and Africa fintech market is segmented and sub-segmented into the following categories.

By Technology

- API

- Artificial Intelligence

- Blockchain

- Distributed Computing

By Service

- Payment

- Fund Transfer

- Personal Finance

- Loans

- Insurance

- Wealth Management

By Application

- Banking

- Insurance

- Securities

By Deployment

- Cloud

- On-Premises

By Country

- Saudi Arabia

- Egypt

- UAE

- Tunisia

- Qatar

- Rest of Middle East and Africa

Frequently Asked Questions

What are the key drivers of fintech growth in the MEA region?

Key drivers include increasing smartphone penetration, a large unbanked population, supportive government policies, and rising demand for digital payment solutions.

What are the main challenges faced by fintech companies in the MEA region?

Major challenges include regulatory hurdles, cybersecurity threats, limited access to funding, and the need for greater financial literacy among consumers.

What role do fintech accelerators and incubators play in the MEA region?

Fintech accelerators and incubators play a crucial role in nurturing startups by providing mentorship, access to funding, and networking opportunities to help them scale and succeed.

What future trends are expected in the MEA fintech market?

Future trends include increased collaboration between traditional financial institutions and fintech startups, the rise of AI and machine learning in financial services, and the growth of digital identity solutions to enhance security and user experience.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com