North America Fintech Market Size, Share, Trends & Growth Forecast Report By Technology, Service, Application, Deployment Mode and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Fintech Market Summary

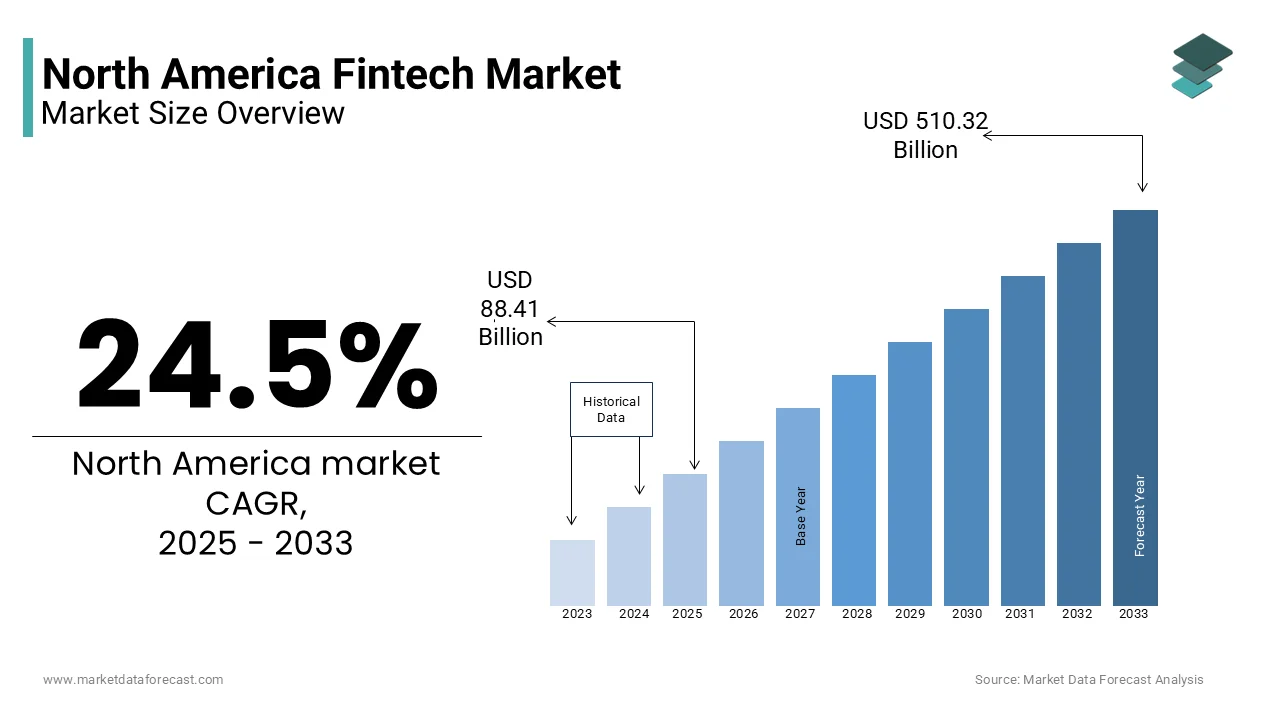

The North American fintech market was valued at USD 71.01 billion in 2024, projected to reach USD 88.41 billion in 2025, and expand significantly to USD 510.32 billion by 2033, growing at a CAGR of 24.5% from 2025 to 2033. The growth of the fintech market in North America is driven by increasing adoption of digital payments, innovations in embedded finance, and supportive regulatory sandboxes. Rapid technological advancements and rising demand for efficient, customer-centric financial services are further fueling market expansion.

Key Market Trends

- Growing adoption of digital and contactless payment solutions

- Increasing innovations in embedded finance and open banking

- Expansion of API-driven financial platforms for seamless service integration

- Supportive regulatory frameworks promoting fintech experimentation and growth

Segmental Insights

- Based on technology, the API technology segment led in 2024 with a 38.2% share, driven by demand for seamless integration of financial services across platforms.

- Based on service, the payment services segment dominated with a 32.2% share in 2024, reflecting the growing popularity of digital payments and mobile wallets.

- Based on application, the banking segment held a prominent share in 2024, supported by fintech innovations in retail banking, lending, and financial management services.

Regional Insights

- The United States was the top-performing country in 2024, holding a 92.3% share of the North American fintech market, driven by advanced technological infrastructure, high smartphone penetration, and strong venture capital investments.

- Canada is expected to grow steadily with increased adoption of digital banking, payment solutions, and fintech regulations supporting innovation.

- Mexico is emerging as a growth market with rising mobile payment adoption and expanding digital financial services.

Competitive Landscape

Key players in the North America fintech market include Oscar, Square, ZhongAn, Qufeng, Lufax, Avant, Atom Bank, Kabbage, Kreditech, JD Finance, Nubank, SoFi, Klarna, and Funding Circle. These companies focus on technological innovation, strategic partnerships, service diversification, and regulatory compliance to strengthen their market presence and enhance customer experience

North American Fintech Market Size

The fintech market size in North America was valued at USD 71.01 billion in 2024 and is predicted to be worth USD 510.32 billion by 2033, from USD 88.41 billion in 2025 and grow at a CAGR of 24.5% from 2025 to 2033.

The fintech is a transformative force reshaping traditional financial services through innovative technology-driven solutions that enhance accessibility, efficiency, and customer experience. According to the Federal Reserve Bank of San Francisco, mobile payment adoption in the United States reached 87% among smartphone users by 2023, with the widespread consumer acceptance of digital financial transactions. The regulatory environment has evolved to accommodate these innovations, with the Office of the Comptroller of the Currency granting special-purpose national bank charters to fintech companies, legitimizing their role in the financial system. Canada's financial sector has similarly embraced digital transformation, with the Bank of Canada reporting that over 70% of Canadians now use at least one fintech service regularly. The integration of artificial intelligence and machine learning algorithms has enabled sophisticated risk assessment models and personalized financial recommendations that traditional institutions struggle to match.

MARKET DRIVERS

Digital Payment Revolution and Contactless Transaction Adoption

The exponential growth of digital payment solutions is propelling the North America fintech market growth. The COVID-19 pandemic accelerated this transformation, as health concerns drove unprecedented adoption of contactless payment methods and mobile wallet solutions. According to the Nilson Report, contactless payment transaction volume in North America surged by 156% between 2020 and 2023, reaching over 38 billion transactions annually. Apple Pay, Google Pay, and Samsung Pay have become integral components of daily financial interactions, with PYMNTS.com data indicating that 68% of North American smartphone users now possess at least one digital wallet application. Traditional financial institutions have responded by integrating real-time payment capabilities, as the Federal Reserve's FedNow service processed over 1.2 million instant payment transactions within its first six months of operation.

Regulatory Sandboxes and Progressive Financial Legislation

The progressive regulatory frameworks and government-sponsored innovation initiatives by enabling companies to test revolutionary financial products within controlled environments, which is amplifying the growth of the North America fintech market. Regulatory sandboxes established by federal and provincial authorities provide temporary exemptions from certain regulatory requirements, allowing fintech startups to experiment with novel solutions while maintaining consumer protection standards. The Consumer Financial Protection Bureau has granted over 150 regulatory sandbox approvals since 2020, which is facilitating the launch of innovative lending platforms, digital banking services, and cryptocurrency exchanges. The OCC's special purpose national bank charter program has enabled 23 fintech companies to operate under federal banking regulations, providing them with nationwide operational scope and enhanced credibility. State-level initiatives have also contributed significantly, with 38 U.S. states implementing modified regulatory frameworks that accommodate digital banking services and cryptocurrency operations. The Securities and Exchange Commission's guidance on digital asset regulation has provided clarity for blockchain-based financial products, encouraging institutional investment in cryptocurrency infrastructure.

MARKET RESTRAINTS

Cybersecurity Vulnerabilities and Data Breach Concerns

The cybersecurity threats and data protection vulnerabilities is hindering the growth of the North America fintech market. The increasing sophistication of cyberattacks targeting financial technology platforms has heightened regulatory scrutiny and consumer skepticism regarding digital financial services. According to the Identity Theft Resource Center, fintech companies experienced a 78% increase in reported data breaches between 2022 and 2023, with average breach costs exceeding $4.5 million per incident. The complexity of securing distributed financial ecosystems, particularly those involving blockchain technologies and cross-border transactions that creates additional vulnerabilities that malicious actors exploit. Small and medium-sized fintech companies struggle to implement enterprise-grade security measures due to resource constraints, with the Ponemon Institute reporting that 64% of emerging fintech firms lack dedicated cybersecurity personnel.

Stringent Compliance Requirements and Regulatory Complexity

The intricate web of regulatory compliance requirements across multiple jurisdictions a formidable is also impeding the growth of the North America fintech market. Financial technology companies must navigate varying state-level regulations, federal oversight frameworks, and international compliance standards, which is resulting in complex and often contradictory requirements that increase operational complexity. State-level money transmission licensing requirements vary significantly, with California's Department of Financial Protection and Innovation imposing stricter capital requirements than other jurisdictions, forcing companies to maintain disparate compliance frameworks. The Securities and Exchange Commission's evolving stance on digital asset classification has created regulatory uncertainty, with 45% of cryptocurrency-focused fintech companies reporting delayed product launches due to unclear regulatory guidance according to the Blockchain Association.

MARKET OPPORTUNITIES

Embedded Finance Integration Across Non-Financial Platforms

The emergence of embedded finance, which integrates financial services directly into their customer experiences to enhance value propositions and revenue stream,s shall create new opportunities for the growth of the North America fintech market. This trend enables retailers, e-commerce platforms, and service providers to offer payment processing, lending, insurance, and investment services without requiring customers to leave their primary digital environments. E-commerce giants such as Shopify and Amazon have integrated comprehensive financial services, with Shopify Capital providing over $5.2 billion in merchant financing and Amazon offering co-branded credit cards that process more than 18 million transactions monthly. The automotive sector has embraced embedded finance through digital car purchasing platforms that include financing, insurance, and warranty services within a single interface. Real estate platforms now offer mortgage pre-qualification tools, title insurance, and escrow services, streamlining property transactions that traditionally required multiple service providers. Social media companies have integrated peer-to-peer payment features and cryptocurrency trading capabilities, with Instagram's checkout feature processing over $12 billion in social commerce transactions in 2023. Healthcare platforms are incorporating medical financing options and health savings account management tools, which is creating new revenue opportunities while improving patient access to care.

Cryptocurrency Institutional Adoption and Digital Asset Infrastructure

The growing institutional acceptance of cryptocurrency and digital assets, as traditional financial institutions and corporate entities increasingly recognize the strategic value of blockchain-based financial instruments, will also enhance the growth of the North America fintech market. Major corporations have begun incorporating cryptocurrency into treasury management strategies, with the Wall Street Journal reporting that over 18% of publicly traded companies in North America now hold digital assets on their balance sheets. Financial infrastructure providers have responded by developing comprehensive custody solutions, trading platforms, and settlement services tailored to institutional investors' risk management requirements. According to the Cambridge Centre for Alternative Finance, institutional cryptocurrency trading volume in North America exceeded $1.8 trillion in 2023, representing 67% of global institutional digital asset activity. The Chicago Mercantile Exchange reported that Bitcoin futures trading volume reached 24 million contracts in 2023, indicating sustained institutional interest in regulated cryptocurrency derivatives markets.

MARKET CHALLENGES

Talent Acquisition and Skills Gap in Emerging Technologies

The human capital challenge, as demand for specialized technical expertise in blockchain, artificial intelligence, cybersecurity, and data analytics far exceeds available talent supply, is likely to pose a challenge for the growth of the North America fintech market. This skills shortage creates significant barriers to innovation and market expansion for emerging companies competing against established financial institutions with greater resources for talent acquisition. According to Burning Glass Technologies, job postings for blockchain developers increased by 395% between 2021 and 2023, while the average time to fill fintech positions exceeded 52 days, representing a 31% increase compared to other technology sectors. Salary premiums for specialized fintech roles have escalated dramatically, with senior blockchain engineers commanding compensation packages 65% higher than traditional software development positions, according to Hired.com's 2023 salary report. Educational institutions struggle to keep pace with rapidly evolving technology requirements, with fewer than 25% of North American computer science programs offering dedicated courses in financial technology and blockchain applications.

Economic Volatility and Interest Rate Environment Impact

The prevailing economic uncertainty and fluctuating interest rate environment for those operating in lending, investment, and payment facilitation sectors that are highly sensitive to macroeconomic conditions, is inhibiting the growth of the North America fintech market. Rising interest rates have compressed profit margins for lending platforms that rely on interest rate spreads, while simultaneously reducing consumer demand for credit products due to increased borrowing costs. Venture capital funding for fintech companies has also contracted significantly, with PitchBook data indicating that North American fintech investment decreased by 52% between 2022 and 2023, reaching the lowest levels since 2018. Payment processing companies face margin compression as merchants negotiate lower interchange fees during economic uncertainty, while cross-border payment facilitators experience reduced transaction volumes as international trade slows. The banking sector's response to interest rate increases has also affected fintech partnerships, with traditional banks reducing reliance on third-party financial technology providers to maintain control over customer relationships during volatile periods.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.39% |

| Segments Covered | By Technology, Service, Application, deployment mode, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and the Rest of North America |

|

Market Leaders Profiled | Oscar, Square, ZhongAn, Qufeng, Lufax, Avant, Atom Bank, Kabbage, Kreditech, JD Finance, Nubank, SoFi, Klarna, and Funding Circle. |

SEGMENTAL INSIGHTS

By Technology Insights

The API technology segment accounted in holding 38.2% of the North America fintech market share in 2024. Open banking regulations have fundamentally transformed the North American financial landscape by mandating traditional banks to provide third-party access to customer financial data through standardized APIs by creating unprecedented opportunities for fintech innovation. Canada's revised API standards mandate that federally regulated banks offer real-time payment initiation and account information services through open APIs, with the Office of the Superintendent of Financial Institutions reporting that 94% of major Canadian banks now comply with these requirements.

The artificial intelligence segment is anticipated to grow at a CAGR of 24.7% during the forecast period. The escalating sophistication of financial fraud and cyber threats has propelled artificial intelligence adoption as financial institutions seek more effective methods for real-time threat detection and risk mitigation. AI-powered fraud detection systems can analyze millions of transactions per second, identifying anomalous patterns that traditional rule-based systems would miss, thereby significantly reducing financial losses and enhancing customer protection. Mastercard's AI-powered fraud detection platform processes over 135 billion transactions annually, preventing an estimated $28 billion in fraudulent activity through machine learning algorithms that continuously adapt to emerging threat patterns. Financial institutions have reported average fraud loss reductions of 45% following AI implementation, with American Express noting that its AI systems prevent 25% more fraudulent transactions than previous detection methods.

By Service Insights

The payment services segment was the largest and held 32.2% of the North America fintech market share in 2024. The explosive growth of e-commerce and digital commerce platforms has created unprecedented demand for sophisticated payment processing solutions that can handle diverse transaction types, currencies, and security requirements across global marketplaces. The rapid expansion of online shopping, accelerated by changing consumer behaviors and technological adoption, has necessitated a robust payment infrastructure capable of supporting high-volume, low-latency transaction processing. Shopify's payment processing platform handled over $230 billion in gross merchandise volume in 2023, demonstrating the scale at which modern e-commerce payment systems must operate to support growing merchant networks. Cross-border e-commerce has particularly benefited from specialized payment solutions, with PayPal facilitating $189 billion in international transactions during 2023 while reducing currency conversion costs by an average of 35% compared to traditional banking methods.

The wealth management services segment is likely to grow with an anticipated CAGR of 18.9% during the forecast period. The emergence of robo-advisory platforms has fundamentally transformed wealth management accessibility by providing sophisticated investment management services at previously unattainable price points for mass affluent consumers who traditionally lacked access to professional financial advisory services. These automated platforms leverage algorithmic portfolio construction, rebalancing, and tax optimization strategies to deliver institutional-quality investment management without requiring substantial minimum account balances or high advisory fees. Vanguard Digital Advisor has successfully attracted younger investors to automated wealth management services, with 67% of new clients under age 40 and average account sizes 45% smaller than traditional advisory relationships. The integration of environmental, social, and governance investing options within robo-advisory platforms has resonated with millennial and Gen Z investors, with Schwab Intelligent Portfolios reporting that 58% of new client assets are allocated to ESG-focused investment strategies.

By Application Insights

The banking applications segment held a prominent share of the North America fintech market in 2024. The fundamental transformation of traditional banking models toward digital-first service delivery has created massive demand for fintech solutions that enable seamless online and mobile banking experiences while reducing operational costs associated with physical branch networks. Consumers increasingly prefer digital channels for routine banking activities, driving financial institutions to invest heavily in user-friendly mobile applications, online account management platforms, and self-service capabilities that replicate and enhance traditional branch services. According to the Federal Reserve's 2023 Survey of Consumer Payment Choice, 87% of North American consumers now conduct the majority of their banking activities through digital channels, with mobile app usage increasing by 65% since 2020. Digital account opening processes have streamlined customer acquisition, with Ally Bank achieving 98% digital account origination rates and reducing new customer onboarding times from weeks to minutes. Mobile check deposit capabilities have become standard features, with Bank of America's mobile deposit service processing over 25 million checks monthly, representing 78% of total check deposits across participating customers.

The securities segment is expected to register a CAGR of 21.3% from 2025 to 2033. The elimination of trading commissions and the proliferation of accessible investment platforms have fundamentally transformed securities market participation by enabling retail investors to engage in sophisticated trading strategies previously limited to institutional investors and high-net-worth individuals. Commission-free trading models have removed traditional barriers to market entry, allowing investors to build diversified portfolios without incurring transaction cost penalties that historically discouraged frequent trading and portfolio rebalancing activities. The integration of fractional share purchasing has expanded investment accessibility, enabling investors with limited capital to participate in premium securities such as Berkshire Hathaway and Amazon that previously required substantial minimum investments. Interactive Brokers has capitalized on this trend by offering commission-free ETF trading and fractional share capabilities, which process over 1.2 million daily trades while maintaining sub-penny pricing structures that attract price-sensitive investors.

COUNTRY-LEVEL ANALYSIS

United States Fintech Market Insights

The United States was the top performer in the North America fintech market by holding 92.3% of the share in 2024. The integration of Silicon Valley innovation, Wall Street financial expertise, and regulatory support has positioned the United States as the global epicenter of fintech development and deployment. Major metropolitan areas such as San Francisco, New York, and Boston have emerged as fintech hubs, attracting substantial investment and talent while fostering collaborative ecosystems between startups, established financial institutions, and technology companies. The regulatory environment has evolved to accommodate fintech innovation through initiatives such as regulatory sandboxes, special purpose charters, and streamlined compliance frameworks that enable rapid market entry while maintaining consumer protection standards.

Canada Fintech Market Insights

Canada was positioned second by holding 8.2% of the North America fintech market share in 2024. Canadian provinces have demonstrated remarkable commitment to fintech development through comprehensive regulatory frameworks that balance innovation support with consumer protection requirements. Ontario's financial services sector has embraced digital transformation initiatives, with major banks investing over $3.2 billion in fintech partnerships and internal innovation projects during 2023. The federal government's support for open banking initiatives and digital currency research has created favorable conditions for fintech expansion, while provincial regulators have established streamlined licensing processes that reduce time-to-market for emerging companies. Toronto and Vancouver have emerged as key fintech centers, attracting international investment and talent while fostering collaborative ecosystems between financial institutions, technology companies, and academic institutions. The Canadian government's Digital Charter and financial sector modernization programs have allocated substantial funding toward fintech infrastructure development and regulatory harmonization initiatives. Cross-border collaboration with U.S. fintech companies has facilitated technology transfer and market expansion opportunities, while the country's stable regulatory environment has attracted international fintech firms seeking North American market entry.

Mexico Fintech Market Insights

Mexico represents a growing participant in the North America fintech market. The country's strategic positioning as a manufacturing and trade hub has driven significant fintech adoption for cross-border payment processing and supply chain financing applications.

The Mexican government's regulatory support for fintech innovation through the Fintech Law and comprehensive licensing frameworks has created favorable conditions for market expansion. Financial institutions have increasingly integrated fintech solutions to enhance service delivery and expand financial inclusion. The remittance market has particularly benefited from fintech payment solutions, with cross-border money transfer services reducing costs compared to traditional banking channels. Digital banking adoption has accelerated among unbanked and underbanked populations, with fintech companies serving millions of previously unbanked customers through mobile-first banking platforms. E-commerce growth has created demand for payment gateway solutions and merchant acquiring services. The government's financial inclusion initiatives have supported fintech expansion through regulatory sandboxes and innovation grants that encourage the development of solutions targeting underserved market segments.

Rest of North America Fintech Market Insights

The remaining North American countries, including Central American nations and Caribbean territories, collectively represent a modest but growing segment of the regional fintech market. This emerging market segment is primarily driven by financial inclusion initiatives and cross-border payment optimization requirements.

Tourism-dependent economies such as Costa Rica and Jamaica have begun implementing fintech solutions for payment processing and currency exchange services to enhance visitor experiences while reducing transaction costs. Agricultural sectors across Central America are adopting fintech lending platforms and mobile payment solutions to improve access to financial services for rural communities and small-scale producers. International development funding and multilateral bank support have facilitated fintech infrastructure development through grants and low-interest financing programs that enable technology adoption. Limited traditional banking infrastructure in these countries has accelerated fintech adoption rates. Remittance optimization has become a primary use case. Regional cooperation through organizations such as the Central American Bank for Economic Integration has facilitated regulatory harmonization and cross-border fintech service provision.

KEY MARKET PLAYERS

Companies playing a leading role in the North American fintech market include Oscar, Square, ZhongAn, Qufeng, Lufax, Avant, Atom Bank, Kabbage, Kreditech, JD Finance, Nubank, SoFi, Klarna, and Funding Circle.

TOP LEADING PLAYERS IN THE MARKET

JPMorgan Chase & Co.

JPMorgan Chase stands as a financial services giant that has successfully transformed itself into a leading fintech innovator while maintaining its traditional banking operations. The company's extensive investment in technology infrastructure and digital capabilities has enabled it to compete effectively with pure-play fintech companies while leveraging its massive customer base and regulatory expertise. Their mobile banking platform has become one of the most downloaded financial applications, offering comprehensive services including contactless payments, investment management, and business banking solutions. The company's blockchain initiatives and cryptocurrency research have positioned it at the forefront of digital asset innovation within traditional banking. Their acquisition strategy has focused on integrating specialized fintech capabilities into their existing service offerings by creating a hybrid model that combines institutional strength with technological agility. JPMorgan's commitment to open banking standards and API development has facilitated partnerships with third-party developers and fintech startups.

Visa Inc.

Visa represents a global payments technology leader that has successfully adapted its business model to embrace fintech innovation while maintaining its core payment processing infrastructure. The company's strategic evolution from a traditional card network to a comprehensive digital payments platform has enabled it to capture significant market share in emerging payment technologies. Their investment in blockchain technology, cryptocurrency integration, and real-time payment solutions has positioned Visa as a bridge between traditional financial systems and digital innovation. The company's extensive merchant network and issuer relationships provide unparalleled scale and reach that fintech startups struggle to match. Visa's acquisition of specialized fintech companies has enhanced their capabilities in areas such as cybersecurity, fraud prevention, and cross-border payment optimization. Their developer platform and API ecosystem have enabled third-party integration while maintaining security and compliance standards across the global payments network.

Square Inc. (Block Inc.)

Square has established itself as a disruptive force in the North America fintech market through its innovative approach to payment processing and financial services for small businesses and individuals. The company's ecosystem approach integrates hardware payment solutions, software platforms, and financial services into comprehensive business management tools that have revolutionized how small merchants operate. Their Cash App has become a cultural phenomenon, transforming peer-to-peer payments into a comprehensive financial platform that includes investment services and cryptocurrency trading. Square's focus on democratizing financial services has enabled underserved market segments to access payment processing, lending, and investment capabilities previously unavailable to them. The company's blockchain and cryptocurrency initiatives, including Bitcoin acquisition and Lightning Network development, have positioned it as a leader in digital asset integration within mainstream financial services. Their hardware-software integration strategy has created seamless user experiences that combine physical payment terminals with sophisticated digital management platforms.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Strategic Acquisitions and Ecosystem Integration Leading players in the North America fintech market actively pursue acquisition strategies to expand their technological capabilities and service offerings while eliminating potential competitive threats. These companies target specialized fintech startups, payment processors, and technology providers to create comprehensive financial service ecosystems that can address diverse customer needs through integrated platforms. Strategic acquisitions enable established players to rapidly acquire innovative technologies and talented teams without the time and resource investment required for internal development. Ecosystem integration strategies focus on creating seamless user experiences across multiple financial services while leveraging existing customer relationships and distribution channels. Companies also pursue vertical integration opportunities to control more aspects of the financial service delivery chain, reducing dependency on third-party providers and improving profit margins.

Partnership and Collaboration Models Key market participants increasingly adopt collaborative approaches through strategic partnerships with technology companies, financial institutions, and regulatory bodies to accelerate innovation and market expansion. These partnerships enable companies to leverage complementary strengths while sharing development costs and regulatory compliance burdens. Collaboration with traditional banks allows fintech companies to access established customer bases and regulatory expertise while providing banks with innovative technology solutions and customer experience enhancements. Technology partnerships with cloud providers, cybersecurity firms, and artificial intelligence companies enable fintech companies to incorporate cutting-edge capabilities without extensive internal development investments. Regulatory collaboration through participation in regulatory sandboxes and industry working groups helps companies navigate complex compliance requirements while influencing policy development that affects market dynamics.

Platform-Based Business Model Development Market participants are increasingly focusing on platform-based business models that create network effects and ecosystem lock-in to achieve sustainable competitive advantages. These platforms enable third-party developers to create applications and services that enhance the core offering while expanding functionality without direct investment from the platform owner. Platform strategies focus on creating standardized APIs and development tools that facilitate rapid innovation while maintaining security and compliance standards. Companies develop marketplace capabilities that connect service providers with consumers, generating revenue through transaction fees and subscription models while expanding service offerings. Multi-sided platform approaches enable companies to serve multiple customer segments simultaneously while creating synergies between different user groups and service providers.

COMPETITIVE LANDSCAPE

The North America fintech market exhibits intense competitive dynamics characterized by the coexistence of traditional financial institutions, pure-play fintech companies, and technology giants vying for market dominance through innovation and customer-centric service delivery. Established banks have responded to fintech disruption by launching their own digital platforms, investing in fintech startups, and forming strategic partnerships to maintain competitive relevance while leveraging their regulatory expertise and customer trust. Technology companies such as Apple, Google, and Amazon have entered the financial services space through payment solutions, lending platforms, and investment services, leveraging their massive user bases and technological capabilities to challenge traditional providers. Pure-play fintech companies compete primarily on user experience, pricing, and innovative service offerings that address specific customer pain points while maintaining agility and speed to market. The competitive landscape is further complicated by regulatory considerations, as companies must navigate varying state and federal requirements while maintaining compliance across multiple jurisdictions. Intellectual property protection and patent portfolios have become increasingly important competitive differentiators as companies seek to protect their technological innovations and prevent competitor replication. Customer acquisition and retention have emerged as competitive factors, with companies investing heavily in user experience design, customer service capabilities, and loyalty programs to maintain market share. The emergence of platform-based business models has created new competitive dynamics where companies compete to attract third-party developers and service providers to their ecosystems.

RECENT MARKET DEVELOPMENTS

- In March 2024, JPMorgan Chase launched their new blockchain-based payment settlement platform specifically designed for institutional clients, which is featuring real-time cross-border transaction capabilities and enhanced security protocols.

- In June 2024, Visa acquired Plaid Technologies for $12.8 billion, significantly expanding their data analytics capabilities and developer platform offerings to enhance payment processing and financial service integration.

- In September 2024, Square Inc. rebranded as Block Inc. and announced the launch of their decentralized finance protocol that enables peer-to-peer cryptocurrency transactions without traditional banking intermediaries.

- In January 2024, Mastercard partnered with Microsoft to develop an AI-powered fraud detection system that integrates with existing payment processing infrastructure to enhance transaction security and reduce false positives.

- In August 2024, PayPal completed the spin-off of its cryptocurrency and blockchain division into a separate publicly traded company called Pyfinity by allowing focused development of digital asset services and regulatory compliance frameworks.

MARKET SEGMENTATION

This research report on the North American fintech market has been segmented and sub-segmented based on the following categories.

By Technology

- API

- Artificial Intelligence

- Blockchain

- Distributed Computing

By Service

- Payment

- Fund Transfer

- Personal Finance

- Loans

- Insurance

- Wealth Management

By Application

- Banking

- Insurance

- Securities

By Deployment Mode

- Cloud

- On-premises

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

Which countries in North America contribute significantly to the fintech market share?

The United States and Canada are the primary contributors to the fintech market in North America, with a substantial share of fintech activities concentrated in major financial hubs.

How does the regulatory environment in the United States impact the growth of the fintech sector?

The regulatory environment in the United States plays a crucial role in shaping the fintech sector. Regulatory frameworks, such as those governing digital payments and online lending, influence market dynamics and innovation.

What are the key trends driving fintech growth in Canada?

In Canada, key trends driving fintech growth include the adoption of digital wallets, blockchain technology applications, and the integration of artificial intelligence in financial services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com