Asia-Pacific Fintech Market Size, Share, Trends, & Growth Forecast Report By Service (Payments, Personal Finance, Loans, Insurance, Fund Transfer, Wealth Management and Others), Application (Banking, Insurance, Trading, Taxation, and Others) and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore & Rest of APAC), Industry Analysis From 2025 to 2033

Asia-Pacific Fintech Market Summary

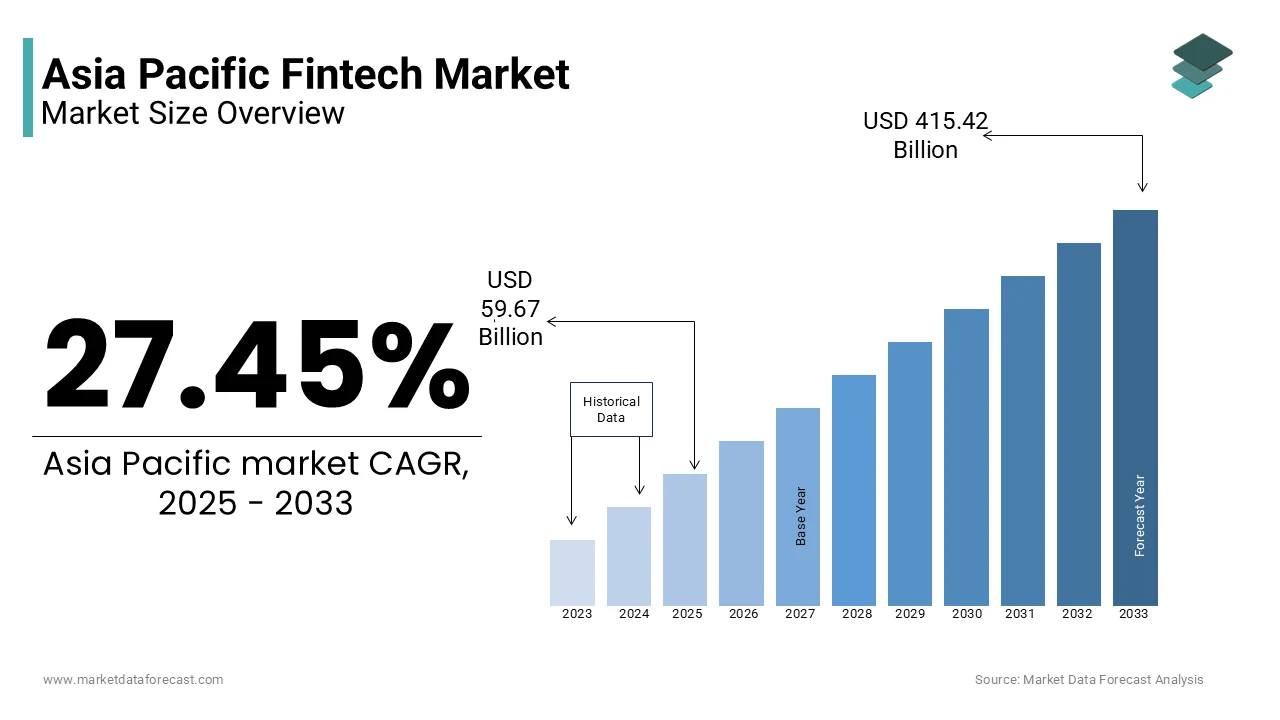

The Asia-Pacific fintech market was valued at USD 46.82 billion in 2024 and is projected to reach USD 59.67 billion in 2025 before surging to USD 415.42 billion by 2033, expanding at a CAGR of 27.45% from 2025 to 2033. The fintech market growth in the Asia-Pacific region is driven by the rapid adoption of digital payments, AI-driven financial solutions, and blockchain applications, alongside government initiatives supporting financial inclusion and digital banking ecosystems. Increasing smartphone penetration, a large unbanked population, and strong investment activity are further fueling fintech expansion across the region.

Key Market Trends

- Rising adoption of AI and blockchain-based platforms to enhance security and efficiency.

- Strong growth of digital wallets and mobile payment ecosystems.

- Expansion of regulatory sandboxes promoting fintech innovation.

- Increasing integration of embedded finance and neobanking services.

- Surge in venture capital and private equity funding in fintech startups.

Segmental Insights

- Based on technology, the AI and blockchain segments together accounted for the largest share of the Asia-Pacific fintech market in 2024, reflecting strong demand for intelligent and secure financial solutions.

- Based on service, the payments segment dominated with a 44.2% share in 2024, supported by booming e-commerce activity and the growing preference for cashless transactions.

Regional Insights

- China led the Asia-Pacific fintech market, commanding 32.7% of the regional share in 2024, driven by large-scale adoption of mobile payments and digital banking platforms.

- India is witnessing rapid growth, fueled by government-backed digital initiatives and a thriving startup ecosystem.

- Japan shows steady adoption, particularly in blockchain-based financial solutions and cashless payment expansion.

- Australia is growing strongly with increased regulatory support for fintech innovation.

Competitive Landscape

Prominent companies operating in the Asia-Pacific fintech market include Oscar, ZhongAn, Qufeng, Lufax, Avant, Atom Bank, Kabbage, Kreditech, JD Finance, Nubank, SoFi, Square, Klarna, and Funding Circle. These firms are focusing on scaling digital payment platforms, AI-driven lending solutions, and cross-border financial technologies to strengthen their market footprint.

Asia-Pacific Fintech Market Size

The Asia-Pacific fintech market was worth USD 46.82 billion in 2024. The Asia Pacific market is expected to grow at a whopping CAGR of 27.45% from 2025 to 2033 and be worth USD 415.42 billion by 2033 from USD 59.67 billion in 2025.

Fintech refers to the technology-driven financial services that are reshaping how individuals and businesses access credit, make payments, invest, and manage risk across the region. Unlike traditional financial infrastructure, fintech in Asia-Pacific leverages mobile connectivity, alternative data analytics, and decentralized platforms to deliver inclusive, real-time, and user-centric financial solutions. What distinguishes this market is its fusion of rapid urbanization, youthful demographics, and regulatory experimentation, creating fertile ground for innovation beyond the reach of conventional banking. The expansion of 4G and 5G networks across rural and semi-urban areas has dismantled geographic barriers to financial access, allowing fintech solutions to penetrate underserved populations. Moreover, the proliferation of digital identity systems, such as India’s Aadhaar and Indonesia’s National Digital Identity initiative, has strengthened the foundation for secure, scalable financial transactions. These structural shifts are not merely technological but socio-economic, as they empower informal workers, micro-entrepreneurs, and women with tools to participate in formal financial systems, fundamentally altering the region’s economic trajectory.

MARKET DRIVERS

Unbanked and Underbanked Population Demand for Financial Inclusion

The vast segment of unbanked and underbanked individuals who are increasingly demanding accessible financial tools is a pivotal force propelling the Asia-Pacific fintech market. This gap is particularly pronounced in rural areas of India, Bangladesh, and the Philippines, where traditional banks have limited physical presence due to high operational costs and low population density. Fintech platforms, however, bypass these constraints by leveraging mobile wallets, agent banking, and AI-driven credit scoring to deliver services directly to smartphones. The demand is further intensified by the growing informal workforce which relies on fintech for payroll, microloans, and insurance. These platforms offer tailored solutions such as split payments, instant credit via transaction history, and peer-to-peer lending, which traditional institutions are ill-equipped to provide. As a result, fintech is not merely supplementing but redefining financial access, transforming inclusion from a policy goal into a market-driven reality.

Surge in Digital Commerce and Embedded Financial Services

The explosive growth of e-commerce across Asia-Pacific is catalyzing demand for integrated financial technologies that streamline transactions, lending, and customer engagement. This shift has created a fertile environment for embedded finance, where payment gateways, buy-now-pay-later (BNPL) options, and merchant financing are seamlessly integrated into shopping experiences. Small and medium enterprises (SMEs) are increasingly adopting fintech-powered invoicing, inventory-linked credit, and cross-border payment solutions to compete in digital marketplaces. Platforms like Paytm in India and Xendit in Indonesia have evolved from payment processors into full-stack financial service providers, offering working capital loans based on real-time sales data. Moreover, social commerce, where platforms like TikTok Shop and Facebook Marketplace drive sales, relies heavily on instant settlement and fraud detection algorithms developed by fintech firms. This convergence of commerce and finance is not only enhancing user experience but also generating vast datasets that improve credit risk modeling and fraud prevention. As digital consumption becomes the norm, the demand for agile, embedded financial tools continues to accelerate, positioning fintech as the backbone of the region’s digital economy.

MARKET RESTRAINTS

Fragmented Regulatory Landscapes and Compliance Complexity

The fragmented and evolving nature of regulatory frameworks across jurisdictions is one of the most significant impediments to the harmonized growth of the Asia-Pacific fintech market. This lack of standardization forces fintech firms to navigate a labyrinth of compliance obligations, including data localization laws, capital adequacy rules, and anti-money laundering (AML) protocols, which vary drastically even between neighboring countries. Additionally, the absence of mutual recognition agreements between financial regulators slows down innovation cycles and discourages investment inconsistencies not only delay product launches but also fragment the market, preventing the emergence of pan-Asian fintech champions. As a result, many startups opt to focus on single markets, limiting their growth potential and reinforcing regional disparities in financial innovation.

Cybersecurity Vulnerabilities and Erosion of Consumer Trust

The rapid digitization of financial services in Asia-Pacific has exposed critical vulnerabilities in cybersecurity infrastructure, undermining consumer confidence and impeding broader adoption. In India, the Reserve Bank reported a year-on-year increase in digital payment fraud between 2022 and 2023, affecting a large number of users and resulting in losses. The problem is exacerbated by the widespread use of legacy systems in traditional banks that partner with fintechs, creating weak links in the digital chain. Moreover, many emerging fintech apps, particularly in Southeast Asia, lack robust encryption, multi-factor authentication, and real-time fraud monitoring, making them attractive targets for cybercriminals. This erosion of trust is particularly damaging in markets where financial literacy is low and users are already skeptical of digital platforms. Until systemic improvements in cyber resilience are implemented, security concerns will remain a formidable barrier to the sustainable scaling of fintech services.

MARKET OPPORTUNITIES

Expansion of Central Bank Digital Currencies (CBDCs)

The development and pilot deployment of central bank digital currencies (CBDCs) across Asia-Pacific present a transformative opportunity for the fintech market by enabling secure, programmable, and inclusive financial infrastructure. Unlike traditional payment systems, CBDCs operate on sovereign-backed digital ledgers, allowing for instant settlement, reduced transaction costs, and enhanced transparency. This infrastructure opens new avenues for fintech innovation, such as smart contracts for conditional payments, automated tax collection, and targeted social welfare disbursements. For example, in India, the Reserve Bank’s digital rupee (e₹) pilot for retail transactions involves fintechs as distribution partners, enabling them to integrate CBDC wallets into existing apps. This integration allows for programmable money, such as subsidies that expire after a set period or funds restricted to healthcare use, enhancing financial accountability. Moreover, CBDCs can bridge the gap between formal and informal economies by providing a digital trail for cash-like transactions without compromising privacy. As governments prioritize financial sovereignty and monetary efficiency, the collaboration between central banks and fintech firms is expected to deepen, creating a new layer of innovation that transcends traditional banking models.

Rise of Decentralized Finance (DeFi) and Blockchain-Based Financial Infrastructure

The growing maturity of blockchain technology and decentralized finance (DeFi) platforms is unlocking new financial paradigms in the Asia-Pacific region, particularly in markets with limited access to traditional credit and investment vehicles. These platforms enable peer-to-peer lending, decentralized exchanges, and tokenized assets without intermediaries, offering faster, cheaper, and more transparent alternatives to conventional finance. In Japan, the Financial Services Agency has licensed over a dozen cryptocurrency exchanges, allowing regulated access to blockchain-based savings and yield-generating products. The integration of non-fungible tokens (NFTs) and digital asset collateralization is further expanding credit access for freelancers and gig workers who lack traditional credit histories. Additionally, institutional interest is rising. This shift is not merely technological but cultural, as younger demographics increasingly view digital assets as legitimate components of wealth management. As regulatory clarity improves and interoperability standards emerge, DeFi is poised to evolve from a niche alternative into a core component of the region’s financial architecture, empowering fintech firms to pioneer new business models rooted in decentralization and user ownership.

MARKET CHALLENGES

Digital Divide and Unequal Access to Technology

A persistent digital divide continues to hinder the equitable expansion of fintech across Asia-Pacific, particularly in rural and remote communities. This gap is compounded by low smartphone ownership, limited digital literacy, and inadequate last-mile connectivity in regions such as Papua New Guinea, Myanmar, and parts of India’s northeastern states. Even where mobile networks exist, poor signal quality and high data costs prevent consistent engagement with fintech platforms. Moreover, linguistic diversity poses a barrier many fintech apps are available only in dominant languages like English, Mandarin, or Bahasa, excluding speakers of regional dialects. Women, in particular, face disproportionate exclusion. Without targeted investments in infrastructure, education, and inclusive design, the fintech revolution risks deepening existing inequalities rather than bridging them.

Talent Shortage in Specialized Fintech Domains

The Asia-Pacific fintech market faces a critical shortage of skilled professionals in areas such as blockchain development, cybersecurity, regulatory technology (RegTech), and artificial intelligence-driven risk modeling. Universities in countries like Indonesia, the Philippines, and Bangladesh offer limited fintech-specific curricula, while industry-academia collaboration is still in its infancy. This skills gap is particularly acute in emerging domains. The talent competition is further intensified by global tech giants and banks offering higher salaries, making it difficult for startups to retain expertise. Additionally, regulatory complexity demands professionals fluent in both technology and compliance an increasingly rare combination. Without coordinated efforts to upskill the workforce through vocational training, certification programs, and public-private partnerships, the talent deficit will constrain innovation, slow down product development, and weaken the region’s long-term competitiveness in the global fintech arena.

MARKET RESTRAINTS

On the other hand, factors such as security concerns, insufficient infrastructure and connectivity, cybersecurity risks and data privacy concerns, slow adoption of fintech solutions in rural areas and competition from traditional financial institutions are hindering the growth of the fintech market in the Asia-Pacific region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology, Service, Application, Deployment Mode, and Country |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Rest of Asia Pacific |

| Market Leaders Profiled | Oscar, ZhongAn, Qufeng, Lufax, Avant, Atom Bank, Kabbage, Kreditech, JD Finance, Nubank, SoFi, Square, Klarna, and Funding Circle. |

SEGMENTAL INSIGHTS

By Technology Insights

The AI and blockchain segments together held the major share of the fintech market in Asia-Pacific in 2024, and the domination of these segments is expected to continue throughout the forecast period. The usage of AI-powered chatbots and virtual assistants by banks to provide enhanced customer support and real-time support has seen a spike in the recent past in the Asia-Pacific. Blockchain technology is being increasingly used in payments, remittances, and trade finance across the Asia-Pacific region, and this technology is gaining tremendous attraction.

By Service Insights

The payments segment dominated the Asia-Pacific fintech market by capturing 44.2% of the total share in 2024. This preeminence is anchored in the region’s rapid shift from cash-based economies to real-time digital transaction systems. A further driver is the explosive adoption of mobile wallets and instant payment infrastructures. China’s Alipay and WeChat Pay collectively serve over 1.2 billion active users, processing trillions of yuan annually. These platforms have become embedded in daily commerce, from street vendors to e-commerce, due to their zero-fee structures and interoperability. An additional critical factor is government-led digitalization initiatives. India’s Digital India campaign and Indonesia’s National Digital Identity (NDI) framework have accelerated financial inclusion by linking biometric IDs to payment systems. Additionally, cross-border remittance demand fuels growth. This efficiency is transforming payments from a transactional function into a foundational layer of the digital economy.

The wealth management segment is the fastest-growing service category in the Asia-Pacific fintech market and is projected to expand at a CAGR of 19.4% from 2025 to 2033. This surge is driven by the rising affluence of the middle class and the democratization of investment tools through digital platforms. An additional major factor is the expansion of retail investor participation, particularly among millennials and Gen Z. Platforms like StashAway, Endowus, and Australia’s Six Park offer low-cost, algorithm-driven portfolio management, making wealth accumulation accessible to non-high-net-worth individuals. A further driver is the integration of micro-investing and gamified finance apps. Similarly, in India, Groww and Zerodha have onboarded millions of users collectively, with a notable share of below the age of 35. Furthermore, regulatory support for digital asset diversification is accelerating growth. The rise of ESG-focused robo-advisors and pension-linked investment apps in South Korea underscores a structural shift toward proactive financial wellness.

By Application Insights

The banking application segment held the largest share of the Asia-Pacific fintech market with 52.6% of total revenue in 2024. This dominance is due to the deep integration of fintech into core banking functions such as account management, lending, and customer onboarding. A further driver is the widespread adoption of neobanks and digital-only banking platforms. An additional major factor is the partnership between traditional banks and fintech firms to modernize legacy systems. Additionally, open banking frameworks are accelerating innovation. This infrastructure enables personalized credit scoring, instant loan approvals, and holistic financial planning, transforming banking from a transactional service into an intelligent, data-driven experience.

The insurance application segment is the fastest-growing in the Asia-Pacific fintech market and is projected to grow at a CAGR of 18.9% from 2025 to 2033. This rapid expansion is fueled by rising awareness of risk protection and the digitization of underwriting, claims, and distribution. A further driver is the low insurance penetration in emerging markets, creating a vast untapped opportunity. Fintech platforms like Indonesia’s PasarPolis and India’s Policybazaar are addressing this gap by offering micro-insurance products via mobile apps, often bundled with e-commerce or ride-hailing services. An additional factor is the use of AI and telematics for dynamic pricing and fraud detection. In Australia, insurers like Allianz and IAG have integrated AI models that analyze driving behavior via smartphone sensors, reducing premiums for safe drivers. Similarly, in China, Ping A uses facial recognition and voice analytics to process claims in under five minutes, improving customer satisfaction and reducing fraud. Furthermore, embedded insurance is gaining traction. This seamless integration is transforming insurance from a reactive product into a proactive, contextual service, driving adoption across demographics.

COUNTRY-LEVEL ANALYSIS

China Fintech Market Insights

China commanded the largest share of the Asia-Pacific fintech market at 32.7% in 2024. As the region’s most advanced digital economy, China has set the global benchmark for fintech integration through state-backed innovation and private-sector dynamism. The country’s dominance is rooted in its ubiquitous mobile payment ecosystem, led by Alipay and WeChat Pay. These platforms are not limited to payments but encompass wealth management, insurance, credit scoring, and even government services, creating a closed-loop digital economy. Another critical driver is the supportive yet controlled regulatory environment. While the 2020–2022 regulatory tightening on Ant Group and other fintechs introduced stricter capital and data rules, it also paved the way for a more sustainable, bank-integrated model. Additionally, high smartphone penetration and 5G infrastructure enable seamless service delivery.

India Fintech Market Insights

India is positioned as a high-growth innovation hub. India’s fintech landscape is defined by government-led digital infrastructure and a booming startup ecosystem. The UPI payment system, launched in 2016, has revolutionized digital transactions, processing billions of transactions in 2024, an increase from the previous year. This open, interoperable network has enabled startups like PhonePe, Paytm, and Google Pay to scale rapidly. Another key factor is the India Stack ecosystem, which includes Aadhaar (biometric ID), e-KYC, and the Account Aggregator framework. Furthermore, strong venture capital inflow supports innovation.

Japan Fintech Market Insights

Japan holds a significant share of the Asia-Pacific fintech market. As a mature, high-income economy, Japan’s fintech growth is characterized by gradual digital transformation of a traditionally conservative financial sector. The country’s progress is driven by regulatory modernization and aging demographics. The Financial Services Agency has launched sandbox programs and licensed over 20 crypto exchanges, encouraging innovation in digital assets and robo-advisory services. SBI Holdings and Monex Group have capitalized on this, with millions of retail investors using their platforms for stock and crypto trading, as reported by the Tokyo Stock Exchange. Another factor is the shift from cash to digital payments. However, the government’s “Digital Japan” initiative and pandemic-induced behavioral change have accelerated adoption. Additionally, neobanks like Sony Bank and Z.com Bank are gaining traction, offering AI-driven financial planning and low-cost international transfers. While growth is slower than in emerging markets, Japan’s high disposable income and technological readiness position it as a key market for premium fintech services.

Australia Fintech Market Insights

Australia accounts for a notable share of the regional market, valued at $38 billion in 2024, as per the Australian Securities and Investments Commission (ASIC). As a regulatory leader, Australia has fostered a balanced fintech environment that prioritizes consumer protection and innovation. The Comprehensive Credit Reporting (CCR) system, introduced in 2018, has enhanced credit assessment accuracy, enabling fintech lenders to offer better rates. Another driver is the Consumer Data Right (CDR) framework, which mandates banks to share customer data securely with authorized third parties. Moreover, strong institutional collaboration supports growth. The fintech hub Stone & Chalk, backed by major banks and regulators, hosts several startups focused on regtech, wealthtech, and blockchain. So, Australia serves as a model for regulated, sustainable digital finance adoption.

Singapore Fintech Market Insights

Singapore is also a key player in the market. As a regional innovation hub, Singapore combines strategic geography, regulatory foresight, and strong government backing to attract global fintech players. MAS has been a pioneer in regulatory sandboxes, digital banking licenses, and green finance initiatives. Another key factor is the ASEAN Financial Innovation Network (AFIN), which promotes cross-border fintech collaboration through the API Exchange (APIX). Additionally, strong venture capital and talent inflow bolster growth.

COMPETITIVE LANDSCAPE

The competitive landscape of the Asia-Pacific fintech market is defined by a dynamic interplay between homegrown innovators, global tech giants, traditional financial institutions, and agile startups, all vying for dominance in a region marked by extreme diversity in economic development, regulatory maturity, and consumer behavior. Incumbent banks are under pressure to modernize legacy systems, often partnering with or acquiring fintechs to remain relevant, while neobanks and digital wallets leverage mobile-first design to capture younger, tech-savvy demographics. Super apps like Grab, Gojek, and WeChat have gained an edge by bundling financial services within broader lifestyle ecosystems, creating sticky user engagement. At the same time, regulatory divergence across countries fragments the market, forcing players to adopt localized strategies rather than one-size-fits-all models. Innovation is no longer limited to payment efficiency but extends to AI-driven credit underwriting, decentralized finance, and embedded insurance, raising the bar for technical and operational excellence. The rise of open banking and digital identity frameworks is enabling new entrants to challenge established players, fostering a climate of continuous disruption. Ultimately, competition is not just about technology or scale, but about understanding local financial behaviors, building trust in digital systems, and delivering inclusive, resilient solutions in a region where financial inclusion remains an unfinished agenda.

KEY PLAYERS IN THE MARKET

The most promising companies in the Asia-Pacific fintech market include

- Oscar

- ZhongAn

- Qufeng

- Lufax

- Avant

- Atom Bank

- Kabbage

- Kreditech

- JD Finance

- Nubank

- SoFi

- Square

- Klarna

- Funding Circle

TOP LEADING PLAYERS IN THE MARKET

Ant Group

Ant Group has redefined the digital finance landscape by seamlessly integrating payments, wealth management, credit scoring, and insurance into a single consumer ecosystem. Through Alipay, it pioneered mobile-first financial inclusion, enabling millions of underserved individuals and small businesses to access services beyond traditional banking reach. Its technological innovations in risk analytics and blockchain-based solutions have set global benchmarks, influencing fintech design in emerging markets. By fostering open platforms and cross-border partnerships, Ant Group has extended its impact beyond China, shaping payment interoperability and digital identity frameworks across Southeast Asia and beyond.

Paytm (One97 Communications)

Paytm has emerged as a transformative force in India’s financial digitization, catalyzing the shift from cash to digital transactions through an accessible, vernacular-enabled platform. It has democratized financial access by offering micro-investments, digital credit, and merchant services to millions of first-time internet users. Beyond payments, Paytm’s ecosystem includes insurance, wealth products, and point-of-sale solutions for small enterprises, embedding itself into the daily economic fabric of the country. Its model of leveraging mobile ubiquity to deliver inclusive financial tools has inspired similar initiatives across developing economies, positioning it as a blueprint for homegrown fintech innovation in large, diverse markets.

Grab Financial Group

As the financial arm of Southeast Asia’s leading super app, Grab Financial Group has integrated financial services into everyday mobility and delivery experiences, creating a contextual banking model. It provides digital wallets, lending, insurance, and payments across multiple countries, adapting to local regulatory and cultural nuances. By leveraging vast transaction data from non-financial services, it delivers hyper-localized credit and risk solutions, particularly for gig workers and micro-merchants. Its cross-border infrastructure and regulatory collaborations have made it a key player in advancing regional financial integration, demonstrating how super apps can serve as de facto financial networks in fragmented markets.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One pivotal strategy is ecosystem integration, where fintech leaders embed financial services into non-financial platforms such as ride-hailing, e-commerce, and social media, creating seamless, high-frequency user engagement. This approach transforms financial products from standalone offerings into contextual experiences. Another key tactic is regulatory collaboration, with major players actively engaging with central banks and financial authorities to shape sandbox policies, digital licensing frameworks, and data-sharing standards, ensuring compliance while driving innovation. Additionally, cross-border expansion through localized partnerships is widely employed, allowing global and regional players to navigate complex regulatory environments by aligning with domestic banks, telcos, and payment networks, thereby accelerating market entry and trust-building in new territories.

Asia-Pacific Fintech Market News

- In March 2023, Ant Group partnered with a leading Southeast Asian bank to launch a cross-border remittance service using blockchain technology, enabling faster and lower-cost transfers between China and Indonesia.

- In July 2023, Paytm collaborated with India’s postal department to expand its digital banking services to rural areas, leveraging post offices as access points for financial inclusion in remote communities.

- In November 2023, Grab Financial Group obtained a digital full bank license in Singapore, allowing it to offer a comprehensive suite of deposit and lending products under its own banking entity.

- In January 2024, Tencent expanded WeChat Pay’s integration with public transportation systems in Japan, enabling Chinese tourists and residents to use mobile payments on trains and buses across major cities.

- In June 2024, Australian neobank Xinja formed a strategic alliance with a cybersecurity firm to enhance its fraud detection capabilities using AI-driven behavioral analytics, strengthening consumer trust in its digital banking platform.

MARKET SEGMENTATION

This research report on the Asia-Pacific fintech market has been segmented and sub-segmented into the following categories.

By Technology

- API

- Artificial Intelligence

- Blockchain

- Distributed Computing

By Service

- Payment

- Fund Transfer

- Personal Finance

- Loans

- Insurance

- Wealth Management

By Application

- Banking

- Insurance

- Securities

By Deployment Mode

- Cloud

- On-premises

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

Which countries in the Asia-Pacific region contribute the most to the fintech market share?

China, India, and Singapore are among the leading contributors to the fintech market share in the Asia-Pacific region, with each country having a dynamic and evolving fintech ecosystem.

What is the CAGR of the fintech market in the Asia-Pacific teio

The Asia-Pacific regional market is expected to grow at a CAGR of 27.45% from 2025 to 2033.

What are the challenges faced by fintech startups in Asia?

Fintech startups in Asia may encounter challenges related to regulatory compliance, cybersecurity, and the need for robust infrastructure. Overcoming these challenges is crucial for sustained growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com