Global API Management Market Size, Share, Trends, Growth Forecast Report Segmentation By Deployment Type (Cloud, On-Premises, and Hybrid), Services, Industry, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2025 to 2033

Global API Management Market Summary

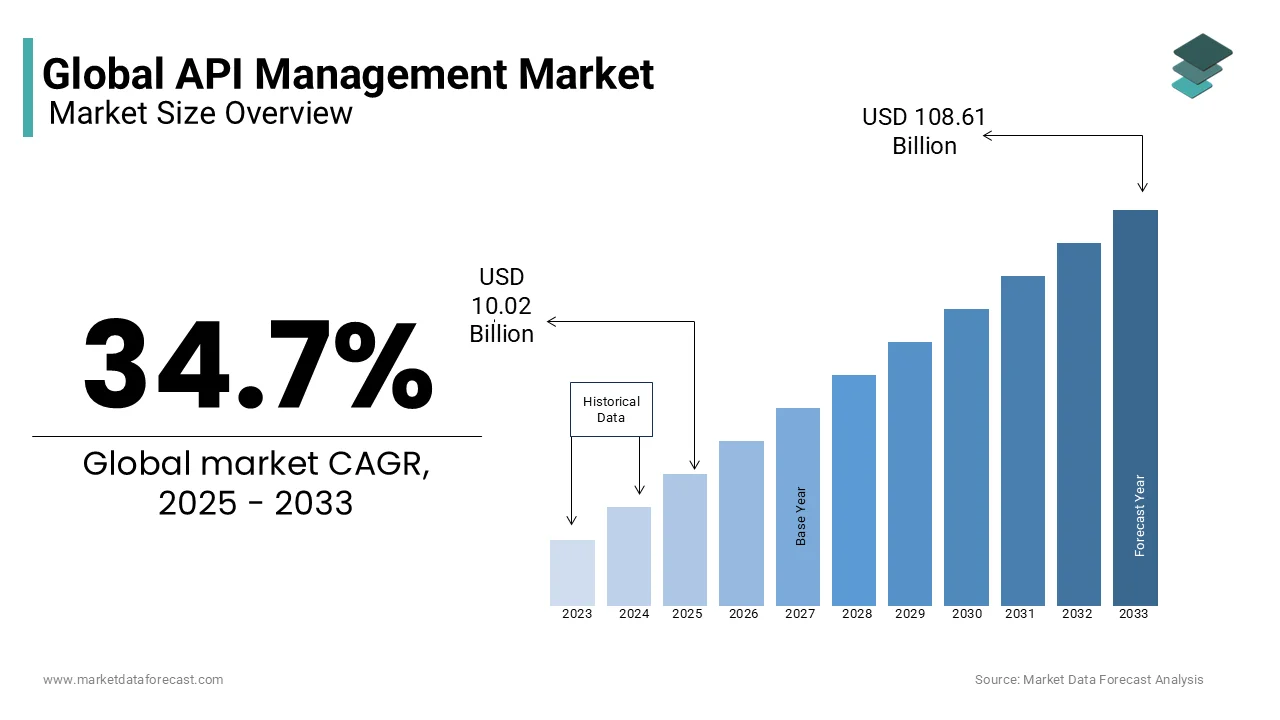

The global API management market was valued at USD 7.44 billion in 2024, is projected to reach USD 10.02 billion in 2025, and is expected to expand to USD 108.61 billion by 2033, growing at a CAGR of 34.7% from 2025 to 2033. The growth of the global API management market is driven by the rising adoption of digital transformation, growing demand for cloud integration, and the increasing need for secure, scalable, and real-time data connectivity. Expanding use of APIs across industries such as banking, healthcare, retail, and IT is fueling market growth, along with advancements in microservices and containerized application architectures.

Key Market Trends

- Strong adoption of cloud-based API management solutions for scalability and flexibility.

- Rising demand for API security solutions to protect sensitive enterprise and customer data.

- Increasing use of APIs in open banking and digital finance ecosystems.

- Expansion of API monetization strategies among enterprises.

- Integration of AI and analytics to enhance API performance and monitoring.

Segmental Insights

- Based on deployment type, the cloud deployment model dominated the global API management market in 2024 with 59.3% share, driven by growing SaaS adoption and lower infrastructure costs.

- Based on services, the security segment accounted for 29.1% share in 2024, reflecting the critical need to protect API endpoints and ensure compliance.

- Based on industry, the banking and finance sector held the largest share at 34.2% in 2024, supported by open banking regulations and demand for digital financial services.

Regional Insights

- North America led the global API management market in 2024 with a 42.3% share, driven by strong adoption of cloud computing, mature IT infrastructure, and high investments in digital innovation.

- Europe is showing steady growth, supported by open banking regulations, GDPR compliance, and rising enterprise digitalization.

- Asia-Pacific is projected to record the fastest growth, fueled by digital banking, fintech expansion, and cloud adoption in emerging economies.

- Latin America and the Middle East & Africa are emerging markets, with rising demand for API-driven solutions to modernize legacy systems and support digital ecosystems.

Competitive Landscape

Key players in the global API management market include IBM (USA), Google (USA), Oracle (USA), Red Hat (US), Software AG (Germany), Axway (US), MuleSoft (US), Microsoft (US), SAP SE (Germany), AWS (US), CA Technologies (US), TIBCO (US), Kony (US), Rogue Wave Software (US), Sensedia (Brazil), Torry Harris Business Solutions (US), Tyk Technologies (England), WSO2 (US), Osaango (Finland), Dell Boomi (US), and Postman (US). These companies are focusing on cloud-first strategies, API monetization, security enhancements, and AI-powered monitoring tools to expand their market presence globally.

Global API Management Market Size

The size of the global application programming interface management (API) market was valued at USD 7.44 billion in 2024. The global market is anticipated to grow from USD 10.02 billion in 2025 to USD 108.61 billion by 2033, recording a CAGR of 34.7% from 2025 to 2033.

API management solutions provide critical functionalities such as access control, rate limiting, analytics, and developer portals by ensuring both operational efficiency and regulatory compliance. The growing interconnectivity between cloud-native applications, third-party services, and legacy systems has elevated API management from a technical enabler to a strategic business imperative. According to Gartner, by 2025, over 90% of new enterprise applications will incorporate APIs as core components of their architecture, underscoring their foundational role in modern software development. Furthermore, as per the World Economic Forum, digital platforms leveraging APIs contributed to over $12 trillion in global economic value in 2023, illustrating their macroeconomic significance. The proliferation of open banking mandates, smart cities, and IoT ecosystems has further intensified the demand for robust API governance frameworks.

MARKET DRIVERS

Accelerated Digital Transformation Across Enterprises

The digital transformation remains a paramount strategic objective for organizations globally, which is directly fueling the growth of the API Management Market. Enterprises are increasingly decommissioning monolithic architectures in favor of modular, cloud-native systems that rely heavily on API-driven integration. According to McKinsey, over 70% of Fortune 500 companies have initiated enterprise-wide digital transformation programs since 2022, with API infrastructure cited as a critical enabler in 85% of these initiatives. The financial services sector exemplifies this trend: in India, the Unified Payments Interface (UPI), powered by open APIs, processed over 11 billion transactions in May 2024 alone, as reported by the National Payments Corporation of India. Similarly, in Australia, the Consumer Data Right (CDR) initiative mandates banks to expose customer data via secure APIs, compelling institutions to adopt sophisticated API management frameworks. The healthcare industry is following suit; the U.S. Centers for Medicare & Medicaid Services enforced interoperability rules in 2024, requiring all healthcare providers to adopt FHIR-based APIs, affecting over 900,000 medical facilities.

Expansion of Cloud-Native and Microservices Architectures

The architectural shift toward cloud-native development and microservices is greatly to propel the growth of the API Management Market. This architectural model demands rigorous API governance to manage service discovery, authentication, monitoring, and versioning across distributed environments. As per the Cloud Native Computing Foundation’s 2023 survey, 96% of responding organizations are either using or evaluating Kubernetes for container orchestration, a core component of cloud-native infrastructure that inherently depends on API-driven automation. Moreover, AWS reported in 2024 that enterprises deploying microservices experience an average of 40% faster time-to-market for new features, reinforcing the model’s appeal. However, this agility introduces complexity: a single application may expose hundreds of internal and external APIs, increasing the risk of security breaches and performance degradation without centralized management. For instance, Netflix manages over 2 trillion API requests daily across its microservices ecosystem, as disclosed in its engineering blog. To handle such scale, enterprises are investing in API gateways, observability tools, and policy enforcement mechanisms. Google Cloud noted in 2023 that organizations using managed API platforms observed a 50% reduction in integration-related downtime.

MARKET RESTRAINTS

Escalating Cybersecurity Threats Targeting API Endpoints

The exponential growth in API usage has made them prime targets for cyberattacks is posing a significant restraint on the broader adoption and trust in API management ecosystems. As APIs become the primary interface for data exchange between services, their exposure to the internet increases the attack surface for malicious actors. According to the 2024 State of the API Security Report by Noname Security, 94% of organizations experienced at least one API security incident in the past year, with authentication bypass and data exposure being the most prevalent vulnerabilities. A particularly alarming trend is the rise in credential stuffing and broken object-level authorization (BOLA) attacks, which accounted for over 60% of API breaches in 2023, as per the Open Web Application Security Project (OWASP).

Lack of Skilled Workforce and Standardization in API Development Practices

The persistent shortage of professionals with specialized expertise in API design, governance, and security is restricting the growth of the API Management Market. This skills gap is particularly acute in mid-sized enterprises and emerging markets, where investment in training and certification lags behind technological adoption. Additionally, the lack of standardized practices across industries leads to inconsistent API design, documentation, and lifecycle management. The Linux Foundation’s 2023 report on open APIs emphasized that fewer than 30% of enterprise APIs comply with OpenAPI Specification (OAS) standards, resulting in integration inefficiencies and increased maintenance costs. In regulated sectors such as healthcare and finance, non-standardized APIs complicate compliance with data protection mandates like GDPR and HIPAA. For example, a 2023 audit by the UK’s Information Commissioner’s Office found that 45% of NHS trusts using third-party health apps had APIs with inadequate audit logging and access controls due to poor development practices.

MARKET OPPORTUNITIES

Proliferation of Open Banking and Financial Data Sharing Mandates

Regulatory-driven open banking initiatives present a transformative opportunity for the API Management Market in regions enforcing data portability and third-party access to financial services. Governments and central banks worldwide are mandating financial institutions to expose customer data via secure, standardized APIs, catalyzing the need for robust API management platforms. The European Union’s Revised Directive on Payment Services (PSD2), implemented in 2018, laid the foundation for this shift, which requires banks to provide third-party providers access to account information and payment initiation services.

Integration of APIs in Smart City and IoT Infrastructure Development

The global push toward smart city development and the expansion of Internet of Things (IoT) networks are creating substantial opportunities for API management solutions to serve as the connective tissue between heterogeneous urban systems. Municipalities are deploying interconnected networks of sensors, traffic management systems, energy grids, and public services, all of which require seamless data exchange through standardized APIs. According to the International Telecommunication Union, over 1,000 cities worldwide had active smart city initiatives as of 2024, with combined investments exceeding $2.8 trillion since 2020. In Seoul, South Korea, the Smart City Platform integrates over 1.2 million IoT devices through a centralized API gateway, enabling real-time monitoring of air quality, traffic flow, and emergency response systems. Similarly, in Dubai, the Smart Dubai initiative mandates that all government services be accessible via APIs, resulting in the publication of over 2,500 public APIs by 2024, as reported by the Dubai Digital Authority. The scalability of IoT ecosystems further amplifies demand: Cisco estimates that global IoT connections will reach 29 billion by 2025, with each device generating multiple API calls per minute for data synchronization and control.

MARKET CHALLENGES

Managing API Sprawl and Lifecycle Complexity in Large Enterprises

Enterprises often develop APIs in silos, with different teams using disparate tools, protocols, and naming conventions, resulting in a fragmented landscape that is difficult to monitor and secure. According to a 2024 study by Forrester Research, large enterprises manage an average of 1,800 APIs, but only 58% are formally documented or cataloged, which leaves a significant portion invisible to central IT and security teams. In a 2023 incident investigated by the U.S. Department of Homeland Security, a dormant API in a federal agency’s system was exploited to exfiltrate sensitive data, with the dangers of unmanaged endpoints. Furthermore, lifecycle management remains a critical pain point: APIs require continuous updates, deprecation, and versioning, yet only 32% of organizations have automated processes for API retirement, as per the 2024 State of API Lifecycle Management report by Postman. The complexity intensifies in hybrid environments where legacy systems coexist with cloud-native applications, requiring intricate mapping and transformation logic. Without a centralized API governance framework, enterprises struggle with performance degradation, increased latency, and higher maintenance costs. The absence of standardized discovery mechanisms also hampers developer productivity, as teams spend up to 30% of their time searching for or recreating existing APIs, according to a Harvard Business Review analysis in 2023.

Ensuring Regulatory Compliance Across Jurisdictionally Diverse Markets

Operating API-driven services across international borders introduces complex regulatory challenges, as organizations must navigate a fragmented landscape of data protection, privacy, and cybersecurity laws that often conflict in their requirements. The absence of global harmonization in digital regulations forces enterprises to implement region-specific API policies, increasing compliance overhead and technical complexity. The European Union’s General Data Protection Regulation (GDPR) mandates strict controls on data access, consent, and cross-border transfers, requiring APIs to enforce granular access permissions and audit trails. According to the International Association of Privacy Professionals, 78% of multinational corporations faced compliance conflicts when deploying APIs across EU, U.S., and Asian markets in 2023. The California Consumer Privacy Act (CCPA) and Canada’s Digital Charter Implementation Act add further layers of obligation, particularly regarding data subject rights such as erasure and portability, which must be programmatically supported via APIs.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 34.7% |

| Segments Covered | By Deployment Type, Services, Industry and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | IBM (USA), Google (USA), Oracle (USA), Red Hat (United States), Software AG (Germany), Axway (United States), MuleSoft (United States), Microsoft (United States), SAP SE (Germany), AWS (United States), CA Technologies (United States), TIBCO (United States), Kony (United States), Rogue Wave Software (United States), Sensedia (Brazil), Torry Harris Business Solutions (United States), Tyk Technologies (England), WSO2 (United States), Osaango (Finland), Dell Boomi (United States), Postman (United States), and others. |

SEGMENTAL ANALYSIS

By Deployment Type Insights

The cloud deployment model was the largest by capturing 59.3% of the global API Management Market share in 2024, as enterprises increasingly favor scalable, cost-efficient, and rapidly deployable solutions that align with modern software development practices. Cloud-based API management platforms eliminate the need for capital-intensive infrastructure investments, offering pay-as-you-go models that appeal to organizations of all sizes. According to the Cloud Native Computing Foundation, over 90% of enterprises now run containerized workloads in production, with Kubernetes clusters relying heavily on cloud-hosted API gateways for service mesh integration and ingress control. This architectural shift necessitates API management systems that are inherently elastic and interoperable with public cloud ecosystems such as AWS, Microsoft Azure, and Google Cloud.

By Services Insights

The security segment held 29.1% of the API Management Market share in 2024, with increasing frequency and sophistication of API-specific breaches. According to the 2024 API Security Benchmark Report by Salt Security, organizations experienced an average of 850 API attacks per week in 2023, a 333% increase from the previous year, with financial and healthcare sectors bearing the brunt. Enterprises are now investing heavily in API security posture management (ASPM) tools and automated penetration testing services. IBM’s 2023 Cost of a Data Breach report found that organizations with dedicated API security protocols reduced breach response time by 42 days on average, translating to savings of $1.5 million per incident. These tangible risk mitigation benefits are cementing security as the most critical and monetized service segment in API management.

The Analytics service segment is swiftly emerging with a CAGR of 25.1% from 2025 to 2033, owing to the growing need for real-time visibility into API performance, usage patterns, and business impact across distributed digital ecosystems. Enterprises are no longer treating APIs as mere technical conduits but as strategic assets that generate actionable insights into customer behavior, system health, and operational efficiency. Google Cloud reported in 2024 that its Apigee analytics engine processes over 2 trillion API events monthly, enabling predictive monitoring and anomaly detection that reduces downtime by up to 60%. These capabilities allow organizations to optimize API throttling, identify underperforming endpoints, and forecast capacity needs. Another compelling factor is the monetization of APIs, particularly in telecom and fintech. Vodafone disclosed in 2023 that it uses API analytics to track third-party usage of its network services, generating over €120 million in annual revenue from programmable connectivity APIs.

By Industry Insights

The Banking & Finance sector segment held 34.2% of the API Management Market share in 2024. Open banking regulations, such as the EU’s PSD2 and the UK’s Open Banking Initiative, require financial institutions to expose customer account data and payment functionalities via standardized APIs, compelling widespread investment in API management infrastructure. As per the European Banking Authority, over 7,500 third-party providers were actively using bank APIs across Europe by mid-2024, facilitating more than 1.3 billion monthly transactions. The Clearing House in the U.S. noted that RTP (Real-Time Payments) network transactions, which rely entirely on secure APIs, grew by 72% year-over-year in 2023, reaching 1.8 billion transactions. Financial institutions are also leveraging APIs to enhance fraud detection; JPMorgan Chase disclosed that its AI-driven fraud prevention system analyzes over 500 million API calls daily to identify suspicious patterns. The sector’s high transaction volumes, stringent compliance requirements, and competitive pressure to innovate have made API management a core operational necessity with its position as the largest industry segment.

The Healthcare & Life Sciences sector is anticipated to grow with a CAGR of 26.8% from 2025 to 2033, with the global push for healthcare interoperability and the digitization of patient records. The U.S. Centers for Medicare & Medicaid Services (CMS) implemented the Interoperability and Patient Access Rule in 2024, mandating all healthcare payers and providers to expose patient data via FHIR (Fast Healthcare Interoperability Resources)-based APIs, affecting over 900,000 medical facilities nationwide. Epic Systems is are leading EHR provider, reported in 2024 that its API network supports over 1.2 million daily requests from third-party health apps, including Apple Health and Google Fit. Another driving force is the integration of AI and genomics into clinical workflows. The Broad Institute disclosed that its genomic data APIs are accessed over 500,000 times per month by researchers globally, enabling collaborative drug discovery and personalized medicine. Additionally, the World Health Organization emphasized in 2024 that API-driven health information systems were instrumental in coordinating pandemic responses across 120 countries. With patient data privacy under strict regulation via HIPAA and GDPR, healthcare organizations are investing in API security and audit logging services at an unprecedented scale.

REGIONAL ANALYSIS

North America API Management Market Insights

North America was the largest contributor to the global API Management Market by holding 42.3% of the share in 2024. The United States serves as a hub for cloud computing and fintech, with Silicon Valley and New York emerging as epicenters of API ecosystem development. According to the U.S. Bureau of Economic Analysis, the digital services sector, heavily reliant on APIs, contributed $1.8 trillion to the national GDP in 2023, reflecting deep integration across industries. The federal government’s adoption of API-first policies through the U.S. Web Design System and the Trusted Internet Connections (TIC) 3.0 initiative has further institutionalized API usage across 106 federal agencies.

Europe API Management Market Insights

Europe was positioned second by capturing 28.3% of the global API Management Market in 2024, owing to the stringent regulatory frameworks that mandate data interoperability and digital service standardization across member states. The European Commission’s Digital Single Market strategy has been instrumental in promoting cross-border API adoption, particularly in finance, healthcare, and public services. The implementation of PSD2 has transformed the banking sector, with over 8,000 third-party providers now accessing bank APIs across the EU, as reported by the European Payments Council. Additionally, Germany’s Gaia-X initiative aims to create a federated data infrastructure based on secure, sovereign APIs, involving over 250 organizations from 18 countries. The UK’s National Health Service has integrated FHIR-based APIs into its digital health platform by enabling 98% of general practices to share patient records electronically, as confirmed by NHS Digital in 2024.

Asia-Pacific API Management Market Insights

Asia-Pacific API management market growth is likely to grow with rapid digitalization, government-led smart initiatives, and a burgeoning fintech ecosystem, particularly in economies such as India, Singapore, and Australia. The National Payments Corporation of India reported that UPI processed 11.7 billion transactions in May 2024 alone, a 58% year-on-year increase, necessitating advanced API management for scalability and uptime. Australia’s Consumer Data Right (CDR) framework, extended to energy and telecommunications in 2024, has compelled over 200 organizations to implement secure API gateways for data sharing. The region also hosts a growing number of API-native startups, with funding in Southeast Asian tech firms reaching $18 billion in 2023, according to DealStreetAsia. However, challenges such as fragmented regulatory environments and uneven digital readiness across countries temper the pace of adoption.

Latin America API Management Market Insights

Latin America API Management Market is likely to grow with huge growth opportunities in the coming years. The region’s market status is defined by increasing digital transformation in financial services and government modernization in Brazil, Mexico, and Colombia. Brazil’s Open Banking initiative, launched by the Central Bank in 2021, has become a cornerstone of its digital economy, with over 140 million daily API calls processed by mid-2024, serving 100 million users across 80 financial institutions, as reported by Banco Central do Brasil. However, infrastructure limitations, cybersecurity concerns, and a shortage of skilled developers constrain broader deployment.

Middle East and Africa API Management Market Insights

Middle East and Africa API Management Market is gearing up with new opportunities in the coming years. The UAE leads the region with its Smart Dubai and Dubai Paperless Strategy, which mandates that all government transactions be conducted via APIs, resulting in the deployment of over 2,500 public APIs by 2024, as confirmed by the Dubai Digital Authority. Saudi Arabia’s Vision 2030 includes a national digital infrastructure plan that prioritizes API-based integration across healthcare, transportation, and energy sectors. In South Africa, the adoption of open banking principles is gaining momentum, with the National Payment System reviewing API standards for interoperability. A key driver is the rapid growth of mobile money: according to the GSMA, mobile money accounts in sub-Saharan Africa reached 700 million in 2024, with platforms like M-Pesa relying on APIs to connect banks, merchants, and telecom providers. However, challenges such as inconsistent internet connectivity, regulatory fragmentation, and limited cloud infrastructure hinder scalability.

KEY MARKET PLAYERS

Companies playing a dominating role in the global API management market include IBM (USA), Google (USA), Oracle (USA), Red Hat (United States), Software AG (Germany), Axway (United States), MuleSoft (United States), Microsoft (United States), SAP SE (Germany), AWS (United States), CA Technologies (United States), TIBCO (United States), Kony (United States), Rogue Wave Software (United States), Sensedia (Brazil), Torry Harris Business Solutions (United States), Tyk Technologies (England), WSO2 (United States), Osaango (Finland), Dell Boomi (United States) and Postman (United States).

TOP LEADING PLAYERS IN THE MARKET

Google (Apigee)

Google is the leading player in the API Management Market by delivering a comprehensive suite of tools that enable enterprises to design, secure, and scale APIs efficiently. The company leverages its deep expertise in cloud infrastructure and data analytics to provide intelligent API management solutions that integrate seamlessly with hybrid and multi-cloud environments. Apigee is widely recognized for its robust security protocols, real-time monitoring, and developer-friendly portals, empowering organizations to foster innovation through ecosystem collaboration. Google’s strategic emphasis on AI-driven insights and automation enhances operational visibility and accelerates digital transformation across industries. Its global footprint and integration with Google Cloud ensure high availability and performance by making it a preferred choice for large-scale enterprises seeking scalable and future-ready API governance frameworks.

Microsoft (Azure API Management)

Microsoft plays a dominant role in the API Management Market through its Azure API Management service, which is tightly integrated into the broader Azure cloud ecosystem. The platform enables organizations to publish APIs to internal, partner, and external developers with ease, ensuring consistency, security, and compliance across distributed applications. Microsoft’s approach emphasizes seamless interoperability with existing enterprise systems, particularly those leveraging .NET and Windows environments, while also supporting open standards for broader accessibility. The company’s strong focus on hybrid cloud capabilities allows businesses to extend on-premises workloads to the cloud without disruption. With built-in DevOps support, advanced analytics, and identity management via Azure Active Directory, Microsoft empowers enterprises to manage complex API landscapes efficiently.

IBM (API Connect)

IBM has established a distinguished presence in the API Management Market through its API Connect platform, which offers a unified solution for creating, managing, and securing APIs across hybrid and multi-cloud environments. The platform is designed to support mission-critical operations in highly regulated industries, emphasizing governance, compliance, and lifecycle management. IBM integrates API Connect with its broader portfolio of AI, automation, and integration tools, enabling enterprises to build cohesive digital ecosystems. The company’s long-standing expertise in enterprise IT infrastructure allows it to deliver robust, scalable solutions tailored to complex organizational needs. API Connect supports industry standards such as OAuth, OpenAPI, and REST, ensuring interoperability and ease of adoption. IBM’s consultative approach, combined with its global services network, enables clients to align API strategies with overarching digital transformation goals. Its focus on security, scalability, and enterprise integration continues to make IBM a strategic partner for large organizations navigating digital evolution.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading players in the API Management Market is deep integration with cloud and enterprise ecosystems. Companies are aligning their API platforms with broader cloud infrastructures, identity management systems, and development toolchains to offer seamless, end-to-end solutions. This integration enhances user experience, reduces deployment complexity, and strengthens vendor lock-in by embedding API management into core IT workflows.

Another key strategy is the incorporation of artificial intelligence and machine learning into API management functionalities. Vendors are leveraging AI to enable predictive analytics, automated threat detection, intelligent traffic routing, and self-healing APIs. These capabilities allow organizations to proactively identify performance bottlenecks, detect anomalies, and optimize API usage without manual intervention. AI-driven insights also enhance developer productivity by recommending best practices and automating routine governance tasks, thereby improving operational efficiency and system reliability.

The expansion of developer-centric tools and ecosystem enablement. Leading providers are investing in intuitive developer portals, interactive documentation, sandbox environments, and community engagement platforms to lower the barrier to API adoption. This strategy not only enhances platform stickiness but also positions API management as a catalyst for business model innovation through open platforms and partner collaborations.

COMPETITIVE LANDSCAPE

The competitive landscape of the API Management Market is characterized by a blend of technological innovation, strategic positioning, and ecosystem dominance. Major players leverage their strengths in cloud infrastructure, enterprise integration, and security to differentiate their offerings in a rapidly evolving digital environment. The market is marked by intense rivalry among established tech giants and specialized vendors, each striving to capture mindshare through advanced features, seamless interoperability, and industry-specific solutions. Differentiation is increasingly achieved not just through core API functionalities, but through added intelligence, automation, and developer experience. Companies are focused on creating sticky ecosystems where API management becomes an integral component of broader digital transformation platforms. The convergence of API governance with security, observability, and microservices architecture has elevated the stakes, pushing vendors to offer holistic, unified solutions rather than standalone tools. Competitive advantage is also shaped by the ability to support hybrid and multi-cloud deployments, cater to regulatory demands, and enable rapid innovation.

RECENT MARKET DEVELOPMENTS

- In March 2024, Google enhanced its Apigee platform with AI-powered anomaly detection and automated policy enforcement, enabling enterprises to identify security threats and performance issues in real time, thereby strengthening its position in intelligent API management.

- In June 2024, Microsoft launched a new hybrid gateway capability within Azure API Management, allowing seamless synchronization between on-premises and cloud environments, reinforcing its position in hybrid cloud integration for enterprise clients.

- In February 2024, IBM introduced advanced governance workflows in API Connect, integrating with its Cloud Pak for Integration suite to offer unified control over API lifecycles, enhancing its appeal to regulated industries.

- In May 2024, Amazon Web Services expanded AWS API Gateway with support for WebSocket APIs and improved developer portal customization, enabling real-time communication and better third-party engagement across its ecosystem.

- In January 2024, MuleSoft, a Salesforce company, unveiled a new API design center with collaborative development features, empowering distributed teams to co-create and standardize APIs, thereby improving governance and accelerating delivery.

MARKET SEGMENTATION

This research report on the global API management market has been segmented and sub-segmented based on deployment type, services, industry, and region.

By Deployment Type

- Cloud

- On-Premises

- Hybrid

By Services

- Analytics

- Portal

- Gateway

- Governance

- Security

- Others

By Industry

- Aerospace & Defense

- Banking & Finance

- Automotive & Transportation

- Public Sector & Government

- Retail & Consumer

- Healthcare & Life Sciences

- Technology & Media

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the current size of the global API management market?

The global API management market size was worth USD 10.02 billion in 2025.

Which industries contribute the most to the global API management market share?

Industries such as IT and telecommunications, BFSI (Banking, Financial Services, and Insurance), healthcare, and retail are among the major contributors to the global API management market share.

Which regions contribute the most to the global API management market share?

Major contributors to the global API management market share include North America, Europe, Asia-Pacific, and regions experiencing rapid digital transformation and increased adoption of cloud technologies.

What are the key factors driving the growth of the global API management market?

Growth in the global API management market is driven by factors such as the proliferation of mobile devices, the rise of cloud computing, increased demand for API-led connectivity, and the expanding ecosystem of digital applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com