Global Aquafeed Market Size, Share, Trends & Growth Forecasts Report, Segmented By Type (Fish, Crustaceans, Mollusks and Others), Ingredient (Soybean, Corn, Fishmeal, Fish Oil, Additives and Others), Application (Carp, Rainbow Trout, Salmon, Crustaceans, Tilapia, Catfish, Sea Bass, Grouper and Others), Additives (Antibiotics, Vitamins & Minerals, Antioxidants, Amino Acids, Enzymes, Probiotics, Prebiotics and Others), Form (Dry, Wet, Moist), Lifecycle (Starter Feed, Grower Feed, Finisher Feed, Brooder Feed), and Region (Asia Pacific, Europe, North America, Latin America, Middle East & Africa), Industry Analysis (2026 to 2034)

Market Size, 2025

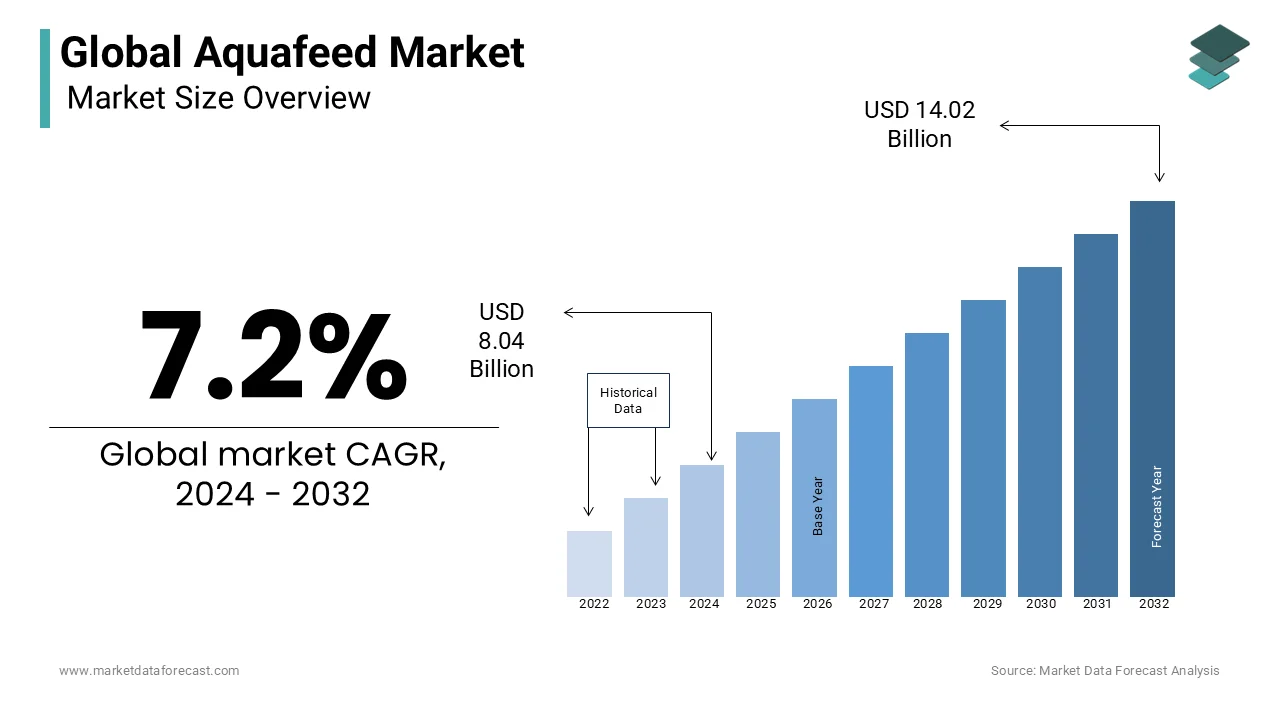

$8.62 BnMarket Estimate, 2026

$7.76 BnMarket Forecast, 2034

$13.96 BnCAGR, 2026–2034

7.2%Global Aquafeed Market Size

The size of the global aquafeed market was valued at USD 8.62 billion in 2025 and is anticipated to reach USD 7.76 billion in 2026 and USD 13.96 billion by 2034, growing at a CAGR of 7.2% from 2026 to 2034.

MARKET OVERVIEW

Aquafeed is engineered to optimize growth rates enhance immune response and improve feed conversion ratios in controlled aquaculture environments. The market serves as the backbone of modern aquaculture which has become essential for meeting the global demand for animal protein as wild capture fisheries plateau. According to the Food and Agriculture Organization of the United Nations aquaculture production reached 122.6 million tons in live weight in 2020 accounting for nearly half of all fish intended for human consumption. This shift from hunting to farming necessitates a robust supply chain of high quality feed to sustain productivity. Furthermore the World Bank states that by 2030 aquaculture will provide two thirds of global fish consumption highlighting the critical role of nutrition in food security. The composition of aquafeed has evolved significantly moving away from heavy reliance on fishmeal and fish oil toward sustainable alternatives such as plant proteins insect meal and single cell proteins. Regulatory frameworks in major producing nations increasingly mandate sustainability standards influencing ingredient sourcing and manufacturing processes. As consumer awareness regarding environmental impact grows the market is pivoting towards eco friendly formulations that minimize nitrogen and phosphorus discharge into water bodies. This transition underscores the strategic importance of innovation in feed technology to support the intensification of aquaculture while preserving ecological balance.

MARKET DRIVERS

Rising Global Demand for Animal Protein and Declining Wild Catch

The escalating global demand for animal protein coupled with the stagnation of wild capture fisheries is a key factor boosting the expansion of the Aquafeed Market. As the world population grows and incomes rise particularly in developing economies dietary preferences are shifting towards high quality protein sources such as fish and seafood. According to the Food and Agriculture Organization of the United Nations global fish consumption has increased at an average annual rate of 3.1 percent since 1961 outpacing the growth of most other animal proteins. Wild fish stocks are increasingly under pressure, with 37.7% of global marine fish stocks classified as overfished as of 2021, a continuing increase from previous assessments FAO SOFIA 2024. This supply gap necessitates the intensification of aquaculture production which relies entirely on formulated feeds to achieve high stocking densities and rapid growth. The transition from extensive to intensive farming systems requires precise nutritional inputs to maintain health and productivity. Consequently the demand for aquafeed is directly correlated with the expansion of aquaculture operations worldwide. Governments in Asia and Latin America are actively promoting aquaculture as a means to enhance food security and rural livelihoods further driving feed consumption. The inability of wild fisheries to meet growing demand ensures that aquaculture remains the fastest growing food production sector thereby sustaining robust demand for specialized aquatic nutrition solutions.

Technological Advancements in Feed Formulation and Ingredient Innovation

Technological advancements in feed formulation and the development of novel ingredients significantly drive the growth of the Aquafeed Market. This enhances efficiency and sustainability. Modern aquafeed manufacturers are increasingly replacing traditional marine ingredients like fishmeal and fish oil with alternative protein sources such as soybean meal corn gluten meal and insect protein. According to the Global Seafood Alliance the inclusion of plant based proteins has reduced the dependency on wild caught fish for feed production by over 50 percent in the last two decades. Innovations in extrusion technology allow for the creation of floating and sinking pellets with improved water stability reducing nutrient leaching and waste. Additionally the integration of functional additives such as probiotics prebiotics and enzymes enhances gut health and nutrient absorption in aquatic species. These advancements improve the feed conversion ratio which is a critical metric for profitability in aquaculture. Research institutions and private companies are investing heavily in biotechnology to produce single cell proteins and algae based oils that mimic the nutritional profile of marine ingredients. The ability to formulate cost effective and environmentally sustainable feeds encourages farmers to adopt commercial feeds over traditional methods. As precision nutrition becomes more accessible the overall productivity of aquaculture systems increases thereby driving the continuous adoption of advanced aquafeed products across diverse species and geographies.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and frequent supply chain disruptions are restraining the expansion of the Aquafeed Market. This affects profitability and operational stability. Key ingredients such as soybeans corn and fishmeal are subject to global commodity price fluctuations influenced by weather conditions geopolitical tensions and trade policies. According to the World Bank food price indices often experience sharp spikes due to climate related events such as droughts or floods which impact crop yields in major producing regions. For instance El Niño phenomena can drastically reduce anchovy catches in South America leading to shortages and price surges in fishmeal a critical component of high performance aquafeeds. These cost variations make it difficult for feed manufacturers to maintain consistent pricing structures forcing them to either absorb losses or pass costs onto farmers who may already operate on thin margins. Supply chain bottlenecks exacerbated by global logistics challenges further delay the availability of essential ingredients. The reliance on imported raw materials in many aquaculture hubs exposes manufacturers to currency exchange risks and tariff barriers. Such economic uncertainties discourage long term investment in capacity expansion and research. Small and medium sized feed producers are particularly vulnerable as they lack the financial reserves to hedge against price volatility. This instability constrains market growth by limiting the ability of manufacturers to offer competitive and reliable products to the aquaculture sector.

Stringent Environmental Regulations and Sustainability Standards

Stringent environmental regulations and evolving sustainability standards impose considerable constraints on the Aquafeed Market. This increases compliance costs and limits ingredient choices. Governments and international bodies are implementing stricter guidelines to mitigate the environmental impact of aquaculture including nutrient discharge and resource usage. According to the European Union the Water Framework Directive and other environmental laws require aquaculture facilities to minimize nitrogen and phosphorus release into water bodies which necessitates the use of highly digestible and low pollution feeds. Compliance with these standards often requires expensive research and development to formulate feeds that meet specific ecological criteria. Additionally certification schemes such as the Aquaculture Stewardship Council mandate sustainable sourcing of ingredients prohibiting the use of fishmeal from overexploited stocks. These restrictions limit the availability of cost effective marine ingredients and force manufacturers to seek alternative sources that may be more expensive or less nutritionally complete. The complexity of navigating diverse regulatory landscapes across different countries adds administrative burdens and delays product launches. Non compliance can result in severe penalties loss of certification and reputational damage. While these regulations aim to promote sustainability they create barriers to entry for smaller players and increase operational costs for established firms. The pressure to balance economic viability with environmental responsibility remains a persistent challenge restraining the rapid expansion of the market.

MARKET OPPORTUNITIES

Expansion of Insect Protein and Alternative Ingredient Sources

The proliferation of insect protein and other alternative ingredient sources offers a strong opening for the Aquafeed Market. This expansion paves the way to enhance sustainability and reduce costs. Insect meal derived from species such as black soldier fly larvae offers a high quality protein source with a favorable amino acid profile comparable to fishmeal. According to the International Platform of Insects for Food and Feed the production capacity for insect protein is projected to grow exponentially as regulatory approvals expand in key markets including the European Union and North America. Insects require significantly less land and water than traditional livestock and can be reared on organic waste streams making them an environmentally friendly option. The incorporation of insect meal into aquafeed reduces reliance on volatile marine ingredients and lowers the carbon footprint of production. Additionally algae based oils are emerging as a viable substitute for fish oil providing essential omega 3 fatty acids without depleting ocean resources. Companies are investing in scalable production facilities to meet the growing demand for these novel ingredients. The acceptance of insect based feeds by major aquaculture producers is increasing as trials demonstrate comparable growth performance and health benefits. This shift towards circular economy principles aligns with consumer preferences for sustainable seafood. By diversifying ingredient portfolios with insect and algae based products feed manufacturers can unlock new revenue streams and strengthen their position in the eco conscious market.

Growth of Precision Aquaculture and Digital Feed Management

The growth of precision aquaculture and digital feed management technologies opens the door for the Aquafeed Market. This helps to improve efficiency and reduce waste. Advanced sensors and automated feeding systems enable real time monitoring of fish behavior and water quality allowing for precise adjustment of feed rations. According to the Global Aquaculture Alliance the adoption of smart feeding technologies can reduce feed waste by up to 20 percent significantly lowering production costs and environmental impact. Digital platforms integrate data from multiple sources to optimize feeding schedules based on factors such as temperature oxygen levels and fish size. This data driven approach ensures that nutrients are delivered when most needed maximizing growth rates and feed conversion ratios. Feed manufacturers are increasingly partnering with technology providers to offer integrated solutions that combine high quality feed with smart dispensing hardware. The ability to track feed consumption and fish health remotely enhances decision making for farmers. As connectivity improves in rural aquaculture zones the accessibility of these technologies is expanding. The trend towards intensification and industrialization of aquaculture drives the demand for such precision tools. By leveraging digital innovations feed companies can provide value added services that differentiate their offerings and foster long term customer loyalty. This technological integration positions the aquafeed sector at the forefront of modern agricultural efficiency.

MARKET CHALLENGES

Risk of Disease Outbreaks and Biosecurity Concerns

The risk of disease outbreaks and biosecurity concerns is a serious challenge to the aquafeed market. These health issues can devastate aquaculture production and disrupt feed demand. High stocking densities in intensive farming systems create ideal conditions for the spread of pathogens such as viruses bacteria and parasites. According to the World Organisation for Animal Health diseases like Early Mortality Syndrome in shrimp and Infectious Salmon Anemia in fish cause billions of dollars in losses annually. When outbreaks occur farmers often halt feeding or reduce stock leading to immediate declines in feed consumption. The need for medicated feeds introduces regulatory complexities and requires specialized formulation capabilities that not all manufacturers possess. Furthermore the emergence of antibiotic resistant strains necessitates the development of alternative health boosting ingredients such as immunostimulants and probiotics. Ensuring the biosecurity of feed itself is critical as contaminated ingredients can introduce pathogens into farms. Manufacturers must implement rigorous quality control measures to prevent contamination during production and storage. The unpredictability of disease patterns makes it difficult to forecast demand accurately. Investment in research for disease resistant feed formulations is costly and time consuming. The constant threat of epidemics undermines farmer confidence and financial stability thereby affecting the consistency of feed purchases. Addressing these health challenges requires continuous innovation and collaboration between feed producers veterinarians and farmers.

Limited Awareness and Adoption Among Small Scale Farmers

Limited awareness and slow adoption of commercial aquafeed among small scale farmers hold back the market expansion in developing regions within the aquafeed market. A substantial portion of global aquaculture is conducted by smallholder farmers who often rely on traditional feeding practices such as using farm made mixes or natural food sources. According to the Food and Agriculture Organization of the United Nations small scale producers account for a significant share of aquaculture output in Asia and Africa but often lack access to information about the benefits of formulated feeds. The perceived high cost of commercial aquafeed compared to traditional methods discourages adoption despite evidence of superior growth rates and profitability. Lack of technical knowledge regarding proper feeding rates and storage conditions leads to inefficient use of feed and potential spoilage. Distribution networks in remote rural areas are often underdeveloped making it difficult for manufacturers to reach these customers effectively. Cultural preferences and resistance to change further hinder the transition to modern feeding practices. Educating farmers requires significant investment in extension services and demonstration projects which may not yield immediate returns. Without widespread adoption the market potential remains untapped in key producing regions. Bridging the knowledge gap and improving accessibility are essential for unlocking the full growth potential of the aquafeed industry among smallholder communities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.2% |

| Segments Covered | By Type, Ingredient, Application, Additives, Form, Lifecycle, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC. PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cargill, Archer Daniels Midland Company, Altech, Purina Animal Nutrition, Nutreco N.V., and Ridley Corporation Ltd |

SEGMENT ANALYSIS

By Type Insights

The fish segment dominated the Aquafeed Market and accounted for a 63.1% share in 2025. This dominance of the segment in the global market was driven by the overwhelming dominance of finfish species in global aquaculture production. Species such as carp tilapia salmon and catfish constitute the bulk of farmed aquatic animals requiring substantial volumes of formulated feed to sustain growth and health. According to the FAO SOFIA 2024 report, finfish accounted for 58.1% of total global aquatic animal aquaculture production by volume in 2022. The intensification of fish farming particularly in Asia has led to a shift from extensive pond culture to intensive systems that rely heavily on commercial feeds to maximize stocking densities. The high protein requirements of carnivorous and omnivorous fish species necessitate nutrient dense formulations which drive consistent demand for specialized aquafeed. Furthermore the global preference for fish as a primary source of animal protein ensures steady market expansion. The economic viability of fish farming compared to other aquatic species encourages continuous investment in feed technology and infrastructure. As production volumes increase the corresponding demand for feed rises proportionally. The established supply chains and manufacturing capabilities for fish feed further reinforce its market leadership. The ability to formulate cost effective diets using diverse ingredients allows manufacturers to cater to various price segments ensuring widespread adoption across different geographic regions. In addition, the industrialization of fish farming practices and the focus on optimizing feed conversion ratios significantly support the dominance of the fish segment. Modern aquaculture operations prioritize efficiency and profitability which drives the adoption of high quality commercial feeds that offer superior nutritional balance. According to the Global Seafood Alliance improved feed formulations can enhance feed conversion ratios by up to 20 percent reducing waste and lowering production costs. This efficiency is critical for large scale producers who operate on thin margins. The transition towards automated feeding systems and precision nutrition further increases the reliance on standardized pellet feeds designed for specific fish species and life stages. Industrial farms require consistent feed quality to maintain uniform growth rates and minimize disease risks. The availability of specialized feeds for different developmental stages from fry to grow out ensures optimal performance throughout the production cycle. Additionally the integration of functional additives such as probiotics and enzymes in fish feed enhances gut health and immunity reducing mortality rates. These technological advancements make commercial feed an indispensable input for modern fish farming. The scalability of fish production systems allows for rapid expansion which directly translates to increased feed consumption. The strong correlation between industrial farming practices and feed usage cements the fish segment as the primary driver of the aquafeed market.

On the other hand, the crustaceans segment is estimated to register the fastest CAGR of 7.4% over the forecast period. This quick surge of the segment is propelled by the surging global demand for shrimp and other premium seafood products. Shrimp farming has expanded rapidly in countries like India Ecuador Vietnam and China due to high export values and consumer preference. According to the United States Department of Agriculture global shrimp production has increased significantly with exports reaching record highs in recent years. This growth necessitates a corresponding increase in high quality aquafeed to support intensive farming methods. Crustaceans have specific nutritional requirements including higher levels of certain amino acids and lipids which drive the development of specialized feed formulations. The shift from traditional extensive farming to semi intensive and intensive systems has amplified the need for commercial feeds to ensure consistent yields and quality. The profitability of shrimp farming attracts significant investment in infrastructure and technology further boosting feed demand. Additionally the rising middle class in emerging markets is increasing domestic consumption of shrimp creating a dual driver of export and local demand. The ability of crustacean feeds to improve survival rates and growth performance makes them essential for competitive production. As farming techniques advance and production scales up the crustacean feed segment continues to expand at a robust pace. Technological advancements in crustacean nutrition and health management are key factors contributing to the rapid growth of this segment. Research into the specific dietary needs of shrimp and crabs has led to the development of highly specialized feeds that enhance immune response and disease resistance. According to the World Aquaculture Society the incorporation of functional ingredients such as beta glucans and nucleotides in crustacean feed has shown significant improvements in survival rates against common pathogens like White Spot Syndrome Virus. These health boosting formulations are critical for maintaining productivity in high density farming environments where disease outbreaks can be devastating. The development of slow sinking pellets and stable emulsions ensures better water stability and nutrient retention reducing waste and environmental impact. Innovations in ingredient sourcing including the use of marine derived proteins and novel plant based alternatives allow for cost effective and sustainable feed production. The focus on improving molting efficiency and shell quality through mineral supplementation further enhances product value. As farmers adopt these advanced feeding strategies to mitigate risks and optimize returns the demand for specialized crustacean feed grows. The continuous innovation in feed technology addresses the unique biological challenges of crustaceans driving the segment's accelerated expansion in the global aquafeed market.

By Ingredient Insights

In 2025, the soybean segment led the Aquafeed Market and captured a 28.5% share. This leading position of the segment was attributed to its cost effectiveness wide availability and high protein content. As the industry seeks to reduce reliance on expensive marine ingredients soybean meal has become the primary plant based protein source in many formulations. According to the United States Department of Agriculture global soybean production exceeds 350 million metric tons annually ensuring a stable and abundant supply for feed manufacturers. The high protein digestibility and balanced amino acid profile of soybean meal make it a suitable substitute for fishmeal in diets for omnivorous species such as tilapia and carp. The economic advantage of soybean over marine ingredients allows producers to lower feed costs while maintaining acceptable growth performance. Advances in processing technologies have reduced anti nutritional factors in soybean meal enhancing its suitability for aquatic species. The widespread cultivation of soybeans in major agricultural regions facilitates efficient logistics and distribution networks. Furthermore the consistency in quality and composition of soybean meal supports standardized feed production. The ability to blend soybean with other ingredients to create balanced diets reinforces its central role in aquafeed formulation. Sustainability concerns are driving a shift away from finite marine resources. Consequently, soybean remains the cornerstone of plant-based aquafeed ingredients. The integration of soybean into sustainable feed formulations and supportive regulatory frameworks further solidify its market leadership. Governments and industry bodies are promoting the use of plant based ingredients to reduce the environmental footprint of aquaculture. According to the Aquaculture Stewardship Council standards encourage the use of responsibly sourced plant proteins to minimize pressure on wild fish stocks. Soybean meal certified by sustainability initiatives such as the Round Table on Responsible Soy gains preference among eco conscious producers. The reduction of fish in fish out ratios through soybean inclusion aligns with global sustainability goals and consumer expectations. Research indicates that partial replacement of fishmeal with soybean meal does not compromise fish health when properly formulated. The versatility of soybean allows it to be used in feeds for a wide range of species from freshwater fish to marine shrimp. The ongoing improvement in soybean processing techniques enhances nutrient bioavailability making it more competitive with marine ingredients. The strategic alignment of soybean usage with sustainability mandates and economic incentives ensures its continued dominance in the aquafeed ingredient market. The scalability of soybean production supports the long term growth of the aquaculture industry without depleting ocean resources.

The additives segment is anticipated to witness the fastest CAGR of 8.8% between 2026 and 2034. This swift growth of the segment is fuelled by the increasing focus on disease prevention and immune system enhancement in intensive farming systems. As stocking densities rise the risk of disease outbreaks increases necessitating the use of functional additives to maintain animal health. According to the World Organisation for Animal Health the use of immunostimulants probiotics and prebiotics in aquafeed has been shown to significantly reduce mortality rates and improve growth performance. These additives help modulate the gut microbiome enhancing nutrient absorption and protecting against pathogens. The ban on antibiotic growth promoters in many regions has accelerated the adoption of natural alternatives such as organic acids and essential oils. Farmers are increasingly recognizing the value of preventive health measures over therapeutic interventions leading to higher demand for health boosting additives. The ability of additives to improve stress tolerance during handling and transport further enhances their appeal. The development of targeted additive packages for specific species and life stages allows for precise health management. As aquaculture intensifies globally the reliance on these functional ingredients becomes critical for sustaining productivity. The continuous research into new additive combinations and their mechanisms of action drives innovation and market expansion. Regulatory restrictions on the use of antibiotics in aquaculture and the push for natural solutions are key factors contributing to the rapid growth of the additives segment. Many countries have implemented strict regulations prohibiting the use of antibiotics for growth promotion due to concerns about antibiotic resistance. According to the European Medicines Agency the reduction of antibiotic use in food producing animals is a priority leading to increased adoption of alternative health solutions. Probiotics prebiotics and phytogenics offer safe and effective ways to maintain gut health and prevent diseases without the risks associated with antibiotics. Consumers are also demanding seafood produced without chemical residues driving producers to adopt natural feed additives. The market for organic and eco labeled seafood further incentivizes the use of natural additives. Innovations in encapsulation technologies improve the stability and efficacy of these additives in feed pellets. The growing awareness of the benefits of functional ingredients among farmers and integrators accelerates their adoption. The shift towards holistic health management strategies positions additives as essential components of modern aquafeed. The regulatory landscape and consumer preferences create a favorable environment for the sustained growth of the additives segment in the global aquafeed market.

By Application Insights

The carp segment held the majority share of 24.6% of the Aquafeed Market in 2025. This supremacy of the segment was credited to its massive production volumes particularly in the Asia Pacific region. Species such as common carp grass carp and silver carp are staples in Asian diets and are cultivated extensively in ponds and reservoirs. According to the Food and Agriculture Organization of the United Nations carps remain the most produced species group in global freshwater aquaculture, reaching a production volume of 49.4 million tonnes in 2022, which represents over 80% of total inland aquatic animal production. This vast production base creates a substantial demand for affordable and nutritious feed. The intensification of carp farming in countries like China India and Vietnam has shifted practices from reliance on natural food to commercial feed usage. The availability of cost effective feed formulations using plant based ingredients makes carp farming economically viable for small and medium scale farmers. The adaptability of carp to various environmental conditions and feeding regimes supports widespread cultivation. Government initiatives in Asia promoting aquaculture as a source of food security and income further boost carp production. The established supply chains for carp feed ensure easy accessibility for farmers. The sheer scale of carp cultivation compared to other species ensures its dominance in the aquafeed market. The continuous growth in population and protein demand in Asia sustains the high volume of carp production and feed consumption. Besides these, the affordability and accessibility of carp feed for small scale farmers significantly contribute to its market leadership. Carp feed formulations often utilize locally available and inexpensive ingredients such as rice bran wheat bran and oilseed meals making them cost effective for resource constrained farmers. According to the World Bank smallholder farmers constitute a significant portion of aquaculture producers in developing countries and rely on affordable inputs to maintain profitability. The simplicity of carp feeding requirements allows for the production of basic yet effective feeds that do not require complex manufacturing processes. This accessibility ensures that even remote rural farmers can participate in commercial aquaculture. The widespread distribution networks for carp feed in Asia facilitate easy procurement. The economic resilience of carp farming due to low input costs encourages continuous production cycles. The ability to achieve reasonable growth rates with modest feed investments makes carp an attractive option for livelihood improvement. The cultural significance of carp in many Asian countries ensures steady domestic demand. The combination of low production costs and high market acceptance sustains the leading position of carp in the aquafeed application segment. The focus on inclusive growth in aquaculture further supports the dominance of carp farming.

On the other hand, the salmon segment is likely to experience the fastest CAGR of 5.6% from 2026 to 2034 due to its premium market value and the expansion of offshore farming operations. Atlantic salmon is one of the most traded seafood commodities globally with high demand in North America Europe and Asia. According to the Norwegian Seafood Council salmon exports continue to reach record values reflecting strong consumer preference. The high profitability of salmon farming encourages investment in advanced feed technologies to maximize growth and quality. The expansion of offshore and land based recirculating aquaculture systems allows for increased production capacity and geographical diversification. These intensive systems require high performance feeds with precise nutritional profiles to ensure optimal health and flesh quality. The focus on improving feed conversion ratios and reducing environmental impact drives innovation in salmon feed formulations. The use of alternative ingredients such as insect meal and algae oil in salmon feed supports sustainability goals while maintaining product quality. The global expansion of salmon farming into new regions such as Chile Canada and Scotland further boosts feed demand. The premium pricing of salmon allows farmers to invest in high quality feeds that enhance product value. The continuous growth in global consumption of salmon drives the rapid expansion of this segment. Moreover, innovation in sustainable feed ingredients for carnivorous species like salmon is a key factor contributing to the rapid growth of this segment. Salmon require high levels of protein and omega 3 fatty acids traditionally sourced from fishmeal and fish oil. According to the Global Seafood Alliance the industry is actively replacing marine ingredients with sustainable alternatives such as single cell proteins and genetically modified oilseeds to reduce environmental impact. These innovations allow for the production of high performance feeds that meet the nutritional needs of salmon while addressing sustainability concerns. The development of feeds that improve flesh color and texture enhances market appeal and consumer satisfaction. The focus on reducing the fish in fish out ratio through innovative ingredients aligns with corporate sustainability targets and regulatory requirements. The ability to produce salmon with a lower environmental footprint appeals to eco conscious consumers and retailers. The continuous research into novel ingredients and their effects on salmon health and quality drives market differentiation. The adoption of these advanced feeds by major salmon producers accelerates segment growth. The commitment to sustainability and quality ensures that salmon feed remains a dynamic and rapidly evolving area in the aquafeed market.

By Additives Insights

The vitamins and minerals segment was the largest in the Aquafeed Market and occupied a 24.9% share in 2025. This prominence of the segment was supported by its essential role in metabolic functions growth performance and overall health of aquatic species. These micronutrients are critical for enzyme activity bone development and immune function. According to the National Research Council adequate levels of vitamins and minerals are necessary to prevent deficiency diseases and ensure optimal growth rates in farmed fish and shrimp. The intensification of aquaculture increases the dependency on complete feeds that provide all necessary nutrients including micronutrients. The precise formulation of vitamin and mineral premixes ensures consistent nutritional quality across batches. The widespread use of plant based ingredients which may lack certain micronutrients necessitates supplementation to maintain dietary balance. The stability of vitamins during processing and storage is a key focus area with coated and protected forms gaining popularity. The universal requirement for vitamins and minerals across all aquaculture species ensures broad market applicability. The regulatory standards for feed quality mandate minimum levels of essential micronutrients reinforcing their mandatory inclusion. The cost effectiveness of vitamin and mineral supplements relative to their impact on productivity makes them indispensable. The continuous optimization of premix formulations to enhance bioavailability drives sustained demand. Furthermore, the standardization of feed quality and regulatory compliance significantly support the dominance of vitamins and minerals in the additives market. Regulatory bodies worldwide establish guidelines for minimum nutrient levels in animal feeds to ensure animal health and food safety. Commercial feed production in Europe must comply with EU Regulation (EC) No 183/2005 and related additive regulations; the European Federation of Feed Manufacturers (FEFAC) provides the code of practice to ensure industry-wide compliance with these mandatory safety and nutritional standards. The inclusion of standardized vitamin and mineral premixes simplifies compliance for feed manufacturers. The consistency in micronutrient content ensures predictable performance and reduces the risk of nutritional disorders. The globalization of aquaculture supply chains requires adherence to international quality standards which emphasize comprehensive nutritional profiles. The availability of high quality premixes from specialized suppliers facilitates efficient feed production. The focus on traceability and quality control in the feed industry reinforces the importance of standardized additives. The inability to substitute these essential nutrients with other ingredients ensures their permanent place in feed formulations. The ongoing updates to nutritional recommendations based on scientific research drive the refinement of vitamin and mineral packages. The foundational role of these additives in meeting regulatory and quality benchmarks cements their leading position in the market.

However, the probiotics segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 8.5% during the forecast period owing to the global shift towards antibiotic free production and the emphasis on gut health management. The restriction on antibiotic use in aquaculture has created a vacuum for effective alternatives to control pathogens and enhance immunity. According to the Food and Agriculture Organization of the United Nations probiotics are recognized as safe and effective tools for improving water quality and animal health in aquaculture systems. These beneficial microorganisms colonize the gut inhibiting the growth of harmful bacteria and enhancing nutrient absorption. The increasing prevalence of diseases in intensive farming systems makes probiotics a critical component of health management strategies. The ability of probiotics to reduce stress and improve survival rates appeals to farmers seeking to minimize losses. The growing consumer preference for naturally produced seafood drives the adoption of probiotic supplemented feeds. The expansion of organic aquaculture further boosts demand for natural additives. The versatility of probiotics in being applicable to various species and farming systems supports widespread adoption. The continuous research into new strains and their specific benefits drives innovation and market expansion. The alignment of probiotics with sustainability and health goals positions them as a key growth area in the aquafeed additives market. Advancements in microbial technology and strain specificity are key factors contributing to the rapid growth of the probiotics segment. Recent developments in biotechnology have enabled the identification and isolation of specific bacterial strains with targeted health benefits for aquatic species. According to the Journal of Applied Microbiology tailored probiotic formulations can address specific challenges such as vibriosis in shrimp or enteritis in fish. The improvement in stabilization technologies ensures the viability of probiotic strains during feed processing and storage. The ability to deliver live cultures effectively to the gut enhances their efficacy. The customization of probiotic blends for different species and life stages allows for precise health interventions. The integration of probiotics with prebiotics synbiotics further enhances their performance. The growing body of scientific evidence supporting the benefits of specific strains builds confidence among farmers and integrators. The expansion of production capacities for high quality probiotic ingredients reduces costs and improves accessibility. The focus on mechanism of action and dose response relationships drives the development of more effective products. The technological sophistication of modern probiotics distinguishes them from traditional additives driving their rapid adoption and market growth.

REGION LEVEL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific was the top performer in the global Aquafeed Market and accounted for a 60.5% share in 2025. The region’s top position was supported by its status as the world’s largest producer of farmed fish and shrimp. According to the Food and Agriculture Organization of the United Nations Asia Pacific contributes over 80 percent of global aquaculture production with China India Vietnam and Indonesia being key contributors. The intense cultivation of carp tilapia and shrimp in these countries creates massive demand for commercial feeds. The transition from traditional farming methods to intensive systems in the region accelerates feed adoption. Government support for aquaculture development and food security initiatives further stimulates market growth. The presence of major feed manufacturers and raw material suppliers in the region ensures robust supply chains. The rising middle class and increasing protein consumption in Asian countries drive domestic demand for seafood. The expansion of shrimp farming for export markets particularly in India and Vietnam boosts demand for high quality specialized feeds. The availability of labor and favorable climatic conditions support year round production. The region’s focus on improving feed efficiency and sustainability through technology adoption further enhances market dynamics. The sheer scale of production and consumption in Asia Pacific cements its position as the central hub of the global aquafeed industry.

Europe Market Analysis

Europe was the second largest market for aquafeed by securing a 20.1% share in 2025 because of high value species production such as salmon sea bass and sea bream. According to the European Market Observatory for Fisheries and Aquaculture Products Norway and the Mediterranean countries are leading producers driving demand for premium feeds. The region is a pioneer in sustainable aquaculture practices with strict regulations on environmental impact and ingredient sourcing. The focus on reducing fish in fish out ratios drives innovation in alternative ingredients such as insect meal and single cell proteins. The high purchasing power of European consumers supports the demand for high quality and eco labeled seafood. The presence of leading feed technology companies and research institutions fosters innovation in feed formulation. The expansion of land based recirculating aquaculture systems in countries like Denmark and the Netherlands creates new opportunities for specialized feeds. The regulatory framework promotes the use of additives that enhance animal welfare and product quality. The emphasis on transparency and traceability in the supply chain influences feed manufacturing practices. The mature market structure and focus on sustainability position Europe as a leader in high value aquafeed solutions.

North America Market Analysis

North America maintains a significant share of the Aquafeed Market due to the production of salmon in Canada and catfish and trout in the United States. According to the National Oceanic and Atmospheric Administration aquaculture production in the US is focused on high value species with increasing interest in offshore marine farming. The demand for sustainable and antibiotic free feeds is high due to stringent regulatory standards and consumer preferences. The development of alternative protein sources such as insect meal and algae is prominent in the region supported by strong research capabilities. The expansion of recirculating aquaculture systems for inland fish production drives demand for specialized feeds. The presence of major multinational feed companies facilitates the adoption of advanced feed technologies. The focus on environmental stewardship and resource efficiency influences feed formulation strategies. The growth of the organic seafood market supports the use of natural additives and certified ingredients. The integration of digital technologies in feed management enhances operational efficiency. The regulatory environment promotes innovation in sustainable aquaculture practices. The combination of technological advancement and regulatory compliance drives the North American aquafeed market.

Latin America Market Analysis

Latin America expanded steadily in the aquafeed market owing to dominance by shrimp farming in Ecuador, Brazil, and Mexico, and salmon production in Chile. According to the Inter American Institute for Cooperation on Agriculture the region is a major exporter of shrimp and salmon driving demand for high performance feeds. The expansion of aquaculture infrastructure and adoption of intensive farming techniques boost feed consumption. The focus on disease management and biosecurity drives the use of functional additives and health boosting ingredients. The availability of raw materials such as soybean and corn supports local feed production. The regulatory frameworks in key producing countries are evolving to support sustainable aquaculture practices. The export orientation of the industry ensures adherence to international quality standards. The growth of domestic consumption of seafood in urban areas creates additional demand. The investment in research and development for tropical species enhances feed efficiency. The region’s potential for expansion in aquaculture production supports long term market growth. The combination of export strength and domestic growth drives the Latin American aquafeed market.

Middle East and Africa Market Analysis

The Middle East and Africa region is an emerging player in the Aquafeed Market due to growing aquaculture activities in countries like Egypt Nigeria and Saudi Arabia. According to the Food and Agriculture Organization of the United Nations Egypt is a leading producer of tilapia in Africa driving demand for affordable feeds. The region faces challenges related to infrastructure and access to quality inputs but shows significant potential for growth. Government initiatives to enhance food security and reduce reliance on imports support aquaculture development. The adoption of commercial feeds is increasing as farmers shift from extensive to semi intensive systems. The availability of local raw materials such as agricultural byproducts supports feed production. The focus on improving feed efficiency and reducing costs is paramount for small scale farmers. The expansion of shrimp farming in coastal areas of the Middle East creates demand for specialized feeds. International partnerships and investments in aquaculture projects facilitate technology transfer and market development. The region’s young population and growing demand for protein offer long term opportunities. The gradual modernization of aquaculture practices drives the emerging aquafeed market in the Middle East and Africa.

COMPETITIVE LANDSCAPE

The competition in the Aquafeed Market is intense and characterized by the presence of large multinational corporations and specialized regional players who vie for dominance through innovation and sustainability. Major companies compete by developing advanced feed formulations that incorporate alternative proteins and functional additives to enhance animal health and reduce environmental impact. The market sees significant rivalry in the adoption of digital technologies such as precision feeding systems that optimize resource use and improve profitability for farmers. Regulatory compliance and certification standards play a crucial role in differentiating products as consumers increasingly demand sustainably sourced seafood. Strategic collaborations with research institutions and technology providers drive continuous improvement in feed efficiency and nutrient utilization. Price competitiveness remains a key factor particularly in high volume segments like carp and tilapia farming. Companies also focus on expanding their geographic footprint through acquisitions and joint ventures to access new markets. This dynamic landscape encourages ongoing investment in research and development to address challenges such as disease management and resource scarcity. The emphasis on sustainability and technological advancement shapes the competitive strategies of key players in the global aquafeed sector.

KEY MARKET PLAYERS

Some of the market players dominate the global aquafeed market.

- Cargill

- Archer Daniels Midland Company

- Altech

- Nutreco N.V.

- Purina Animal Nutrition

- Nutreco N.V.

- Ridley Corporation Ltd

Top Players In The Market

- Cargill Incorporated is a global leader in the aquafeed industry providing comprehensive nutrition solutions for diverse aquatic species including shrimp salmon and tilapia. The company leverages its extensive supply chain and research capabilities to develop sustainable feed formulations that optimize growth and health. Recent strategic initiatives include significant investments in alternative protein sources such as insect meal and single cell proteins to reduce reliance on marine ingredients. Cargill actively collaborates with farmers to implement precision feeding technologies that enhance efficiency and minimize environmental impact. The company also focuses on expanding its production facilities in key markets like Asia and Latin America to meet rising demand. By prioritizing sustainability and innovation Cargill strengthens its position as a trusted partner in the global aquaculture sector. These efforts ensure the delivery of high quality feeds that support the long term viability of aquaculture operations worldwide.

- Nutreco N.V. is a prominent player in the global aquafeed market known for its specialized brands such as Skretting and Trouw Nutrition. The company focuses on delivering advanced nutritional solutions that improve animal performance and welfare across various aquatic species. Recent actions include the expansion of its research and development centers to innovate in functional feed additives and sustainable ingredient sourcing. Nutreco has strengthened its market position by acquiring regional feed manufacturers to enhance local presence and distribution networks. The company emphasizes digital transformation by integrating data analytics into feed management systems to provide customized solutions for farmers. By committing to circular economy principles Nutreco reduces waste and promotes resource efficiency in its operations. These strategic moves enable the company to address complex challenges in aquaculture while maintaining high standards of quality and sustainability. Nutreco continues to drive growth through technological advancement and customer centric service offerings in the global market.

- Alltech Inc. is a key contributor to the global aquafeed market specializing in natural feed additives and nutritional solutions that enhance animal health and productivity. The company is renowned for its expertise in probiotics prebiotics and organic trace minerals which support gut health and immune function in aquatic species. Recent strategic moves include partnerships with biotechnology firms to develop novel ingredients such as algae based oils and yeast derived proteins. Alltech has expanded its manufacturing footprint in emerging markets to ensure consistent supply and accessibility for farmers. The company prioritizes sustainability by promoting regenerative agriculture practices and reducing the environmental footprint of aquaculture. By focusing on natural solutions Alltech addresses the growing demand for antibiotic free production in the industry. These efforts reinforce its reputation as an innovator in animal nutrition and sustainability. Alltech continues to strengthen its global presence through continuous research and collaboration with industry stakeholders to advance aquaculture practices.

Top Strategies Used By The Key Market Participants

Key players in the Aquafeed Market primarily employ strategies such as sustainable ingredient sourcing and product innovation to strengthen their market position. Companies invest heavily in research and development to create alternative protein sources like insect meal and algae to reduce dependency on finite marine resources. Strategic acquisitions and partnerships with local manufacturers facilitate geographic expansion and enhance distribution networks in emerging markets. Additionally firms focus on digital integration by offering precision feeding solutions and data analytics to improve farm efficiency. Sustainability initiatives including carbon footprint reduction and circular economy practices are central to corporate strategies. These approaches enable participants to meet regulatory requirements and consumer demands for eco friendly products while maintaining competitive advantage in the global aquafeed industry.

MARKET SEGMENTATION

This research report on the global aquafeed market has been segmented and sub-segmented based on type, ingredient, application, additive, form, lifecycle, and region.

By Type

- Fish

- Crustaceans

- Mollusks

- Others

By Ingredients

- Soybean

- Corn

- Fishmeal

- Fish Oil

- Additives

By Application

- Carp

- Rainbow Trout

- Salmon

- Crustaceans

- Tilapia

- Catfish

- Sea Bass

- Grouper

- Others

By Additives

- Antibiotics

- Vitamins & Minerals

- Antioxidants

- Amino Acids

- Enzymes

- Probiotics & Prebiotics

- Others

By Form

- Dry

- Wet

- Moist

By Lifecycle

- Starter Feed

- Grower Feed

- Finisher Feed

- Brooder Feed

By Region

- Asia Pacific

- Europe

- North America

- Latin America

- MEA

Frequently Asked Questions

What is the aquafeed market?

The aquafeed market includes nutritionally balanced feed products formulated specifically for farmed aquatic species such as fish, shrimp, and other seafood.

Why is aquafeed important in aquaculture production?

Aquafeed ensures optimal growth, health, and survival rates of aquatic animals while improving overall farming efficiency.

What ingredients are commonly used in aquafeed?

Fishmeal, soybean meal, grains, oils, vitamins, minerals, and functional additives are widely used to create balanced feed formulations.

Which species drive demand in the aquafeed market?

Salmon, tilapia, carp, shrimp, and catfish account for the majority of aquafeed consumption worldwide.

How does aquaculture expansion influence aquafeed demand?

As fish farming increases to meet global seafood demand, the need for specialized and high-performance feed grows accordingly.

Are sustainable feed ingredients becoming more popular?

Yes, producers are adopting plant proteins, algae-based ingredients, and alternative proteins to reduce reliance on marine resources.

How do feed additives improve aquafeed performance?

Additives enhance digestion, boost immunity, improve feed conversion ratios, and support disease resistance in aquatic species.

What role does nutrition play in fish farming profitability?

Proper nutrition reduces feed waste, accelerates growth cycles, and improves harvest quality, directly impacting farm returns.

How does water quality affect aquafeed formulation?

Feed is designed to minimize nutrient loss and maintain water stability to prevent pollution and maintain healthy farming conditions.

Are functional aquafeeds gaining demand?

Yes, feeds designed for specific life stages, stress resistance, and disease prevention are increasingly used in modern aquaculture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com