Global Aquatic Feed Market Size, Share, Trends & Growth Forecast Report, Segmented By Ingredient (Soybean, Corn, Fish Meal, Fish Oil, Additives And Others), Additive (Antibiotics, Vitamins, Antioxidants, Amino Acids, Feed Enzymes, Feed Acidifiers And Other Additives), End-User (Fish Feed Such As Tilapia, Salmon, Carp And Catfish Feed, Molluscs Such As Oyster Feed And Mussel Feed, Crustaceans Such As Shrimp Feed And Crab Feed And Others), And By Region (North America, Europe, Latin America, Asia-Pacific, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Aquatic Feed Market Size

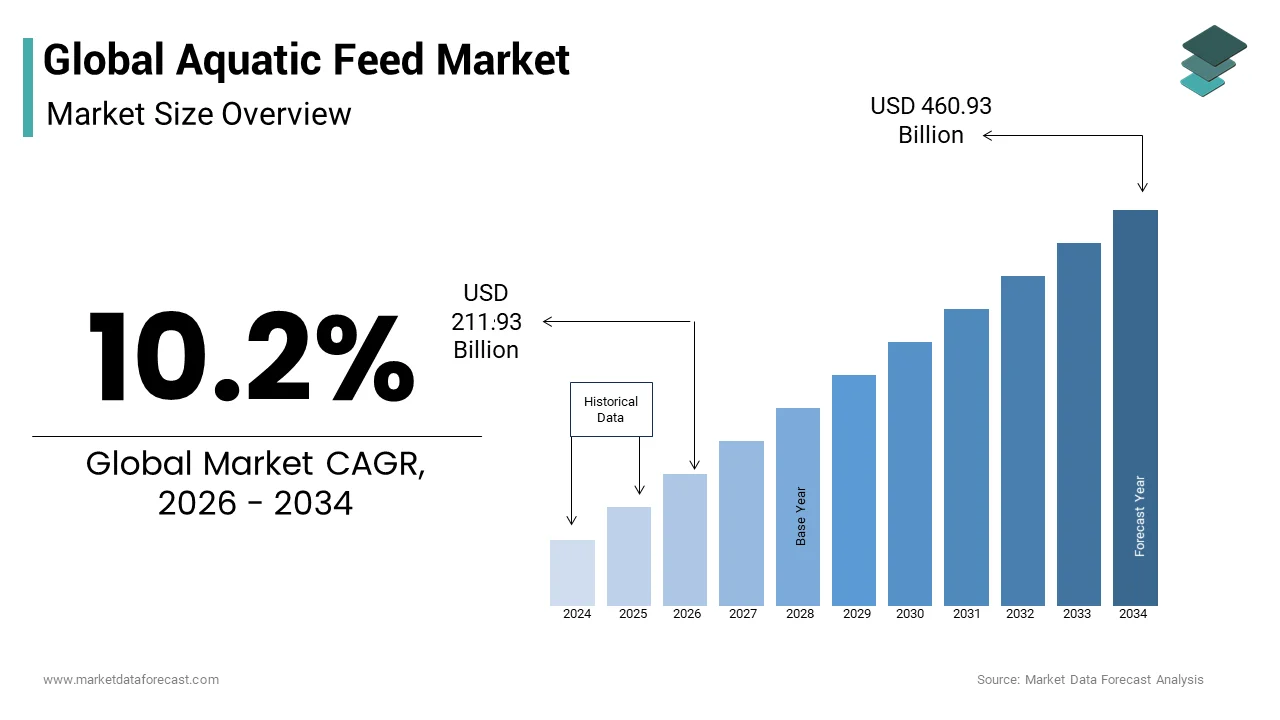

The global aquatic feed market size was valued at USD 192.31 billion in 2025 and is anticipated to reach USD 211.93 billion in 2025 from USD 460.93 billion by 2034, growing at a CAGR of 10.2% from 2026 to 2034.

Aquatic feed is the animal nutrition dedicated exclusively to farmed aquatic species, including finfish, crustaceans, and mollusks, formulated to optimize growth, health, and yield in controlled aquaculture environments. As per the Food and Agriculture Organization of the United Nations, global aquaculture production exceeded 122 million metric tons in live weight in 2020, with feed-dependent species accounting for over 70% of that volume.

MARKET DRIVERS

Rising Protein Diversification Fuels Strong Growth in the Aquatic Feed Market

The global dietary pivot toward protein diversification is a key driver for the aquatic feed market. It is particularly in the Asia-Pacific region, where fish protein now constitutes a portion of average animal protein intake per capita, as per the research. This nutritional transition is not merely cultural but structural, with populations in countries like Bangladesh and Indonesia consuming kilograms of fish annually per person; demand for a consistent, farm-raised supply intensifies. Aquaculture, unable to scale without optimized feed, relies on compounded pellets that deliver precise amino acid and lipid profiles.

Intensified Aquaculture in China and Vietnam Accelerates Demand for Precision-Formulated Aquatic Feeds

The intensification of aquaculture systems in China and Vietnam, where high-density cage and pond farming now dominate production, is escalating the growth of the aquatic feed market. China’s freshwater carp production and a share of its marine shrimp output depend entirely on commercial extruded or sinking pellets. The shift from extensive and low-input systems to industrialized models requires scientifically engineered feeds. These feeds prevent nutrient leaching, reduce feed conversion ratios, and mitigate disease outbreaks. Farms adopting precision-formulated feeds achieve FCRs that are low for tilapia, compared to those in traditional systems, which directly amplifies feed demand while compressing biological waste output.

MARKET RESTRAINTS

Limited Fishmeal and Fish Oil Supply Emerges as a Major Constraint for the Aquatic Feed Market

The volatility and scarcity of marine-derived ingredients, particularly fishmeal and fish oil, which remain irreplaceable for larval and marine species nutrition, pose a considerable restraint for the aquatic feed market. As per the International Fishmeal and Fish Oil Organization, global fishmeal production plateaued at approximately 4.8 million metric tons annually over the past decade, while aquaculture’s consumption of these ingredients grew by 6.2% year-on-year. This imbalance forces feed formulators into costly substitutions or dilutions, compromising nutritional efficacy.

Regulatory Fragmentation and GMO Restrictions Hinder Innovation in the Aquatic Feed Market

Regulatory fragmentation across geographies, particularly concerning novel ingredients and genetically modified components, imposes another formidable constraint on the aquatic feed market. As per the study, many distinct regulatory classifications govern aquatic feed additives across EU member states alone, which delays market entry for alternative proteins like insect meal or single-cell oils by several months. In Latin America, inconsistent labeling and compositional standards across Brazil, Ecuador, and Chile increase compliance costs for multinational feed manufacturers. This regulatory asymmetry not only inflates operational overhead but also stifles innovation, as developers hesitate to invest in region-specific formulations without harmonized approval pathways.

MARKET OPPORTUNITIES

Emerging Insect and Microbial Proteins Create Sustainable Growth Opportunities in the Aquatic Feed Market

The commercialization of non-conventional protein sources, particularly microbial and insect-derived meals, which offer sustainable alternatives to finite marine resources, gives new opportunities for the aquatic feed market. According to research, black soldier fly larvae meal achieves protein concentrations exceeding a certain percentage on a dry matter basis, with amino acid profiles closely mirroring fishmeal. Also, replacing a share of fishmeal with Hermetia illucens meal in pangasius diets yielded no statistical difference in weight gain or survival rates. The global insect protein production capacity is projected to reach notable metric tons annually by 2030.

Digital Feed Management and IoT-Enabled Nutrition Drive Innovation in the Aquatic Feed Market

Digital feed management systems that enable real-time nutrient optimization and waste minimization form new prospects for the aquatic feed market. These systems, by leveraging machine learning algorithms calibrated to species-specific metabolic rates and environmental variables, dynamically adjust pellet dispersion and composition. Feed manufacturers are embedding digital compatibility into formulations to transform passive inputs into intelligent, responsive biological facilitators, a shift toward cognitive nutrition as IoT infrastructure proliferates, particularly in aquaculture zones in India and Chile.

MARKET CHALLENGES

Biochemical Limits of Plant-Based Proteins Restrict Growth of the Aquatic Feed Market

The biochemical incompatibility of many plant-based substitutes with carnivorous marine species, particularly during early life stages, limits the expansion of the aquatic feed market. A share of marine finfish larvae exhibit impaired intestinal development when fed soy-based protein beyond inclusion levels, which triggers chronic inflammation and higher mortality in hatchery environments. This physiological constraint forces reliance on expensive marine ingredients despite sustainability burdens. According to a study, attempts to excessively replace fishmeal with canola or pea protein in barramundi diets can result in lysine and taurine deficiencies, which reduce final harvest weights.

Inadequate Feed Storage and Distribution Infrastructure Limits Aquatic Feed Market Growth in Emerging Economies

The infrastructural deficit in feed distribution and storage across emerging aquaculture economies in sub-Saharan Africa and parts of South Asia holds back the aquatic feed market growth. According to the study, a share of compounded aquafeed suffers nutrient degradation due to inadequate cold-chain logistics and prolonged exposure to tropical humidity. Furthermore, as per the study, vitamin C and lipid-soluble nutrient concentrations in stored feed decline within tens of days under ambient conditions, which directly impairs fish immune response and growth metrics. Therefore, even the most scientifically advanced formulations lose efficacy before reaching farm sites due to the lack of investment in hermetic storage, moisture-controlled transport, and localized micro-milling facilities, which render innovation futile and perpetuate yield gaps that threaten market confidence and farmer adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.2% |

| Segments Covered | By Ingredient, Additive Type, End User, Molluscs, Crustaceans, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cargill Inc., BioMaGroupup, Waterbase Ltd, BASF SE, Alltech Inc., Coppen International, Evonik Industries, Archer Daniels Midland Company, Ridley Corporation, Nutreco NV, Avanti Feeds Ltd, Ewos |

SEGMENT ANALYSIS

By Ingredient Insights

In 2024, the fishmeal segment was the largest contributor to the aquatic feed market with a 38.8% share. The prominence of the fishmeal segment in the global market is largely driven by its irreplaceable biochemical architecture. Fishmeal delivers a complete amino acid profile, high digestibility, and essential micronutrients like taurine and nucleotides that are vital for larval and carnivorous species development. According to a study, Atlantic salmon juveniles fed diets with a portion inclusion of premium-grade fishmeal exhibit higher survival rates and faster weight gain compared to plant-protein-dominated alternatives during the first 90 days post-hatch. Furthermore, as per the study, marine shrimp fed fishmeal-based starter feeds achieve molting synchronicity faster, which directly correlates with uniform harvest sizes and premium pricing.

The additives segment is experiencing a rapid expansion with a CAGR of 9.8% from 2025 to 2033. The growth of the additives segment is propelled by intensifying regulatory bans on prophylactic antibiotics and rising disease burden in high-density farms. As per the study, a share of EU-licensed aquaculture operations have eliminated antibiotic growth promoters since 2020, triggering a surge in demand for immunostimulant additives like beta-glucans and nucleotides.

By Additive Insights

The vitamins segment led the aquatic feed market by accounting for 34.8% of share in 2024. Non-negotiable physiological roles in metabolic regulation, immune competence, and stress resilience mainly drive the growth of the vitamins segment. These are the functions that cannot be compensated for by macronutrients alone. Commercial formulations now embed stabilized vitamin complexes, such as microencapsulated B-complex and lipid-soluble ADEK blends, to withstand thermal extrusion and tropical storage. As per research, vitamin premix inclusion rates in marine carnivore feeds rose to counterbalance fishmeal dilution, which supports their indispensability even as feed costs climb.

The feed enzymes segment is likely to experience a CAGR of 12.4% during the forecast period due to the urgent need to enhance nutrient bioavailability from plant-based ingredients while minimizing phosphorus and nitrogen discharge. As per the study, inclusion of phytase and protease blends in tilapia diets increases phosphorus digestibility and reduces fecal phosphorus load per metric ton of feed — an important compliance metric. In parallel, according to research, carp fed enzyme-supplemented soybean meal diets achieve feed conversion ratios that match fishmeal-based benchmarks, while lowering production costs per kilogram of biomass.

By End-User Insights

The fish feed held a substantial share of the aquatic feed market in 2024, with the global protein economy. Fish contribute a share of the world’s animal protein intake, with aquaculture supplying a portion of food fish consumption, as per a study. Carp alone, predominantly farmed in China and India, consumes millions of metric tons of compounded feed annually, a volume exceeding global poultry starter feed demand, according to the study. Salmonids, though smaller in biomass, drive premium feed innovation.

The shrimp feed segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 8.9% from 2025 to 2033. The expansion of the shrimp feed segment is fueled by Asia’s export-oriented intensification and Latin America’s biosecure revival. As per the study, in Ecuador, its shrimp production surged to notable metric tons, a year-over-year jump, demanding notable metric tons of specialized pelleted feed with immunostimulant fortification. Disease resilience is another accelerator. Thus, feed manufacturers are reformulating for biosecurity, traceability, and metabolic efficiency, which transforms shrimp feed into the most dynamically evolving niche in aquatic nutrition.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific outperformed other regions in the aquatic feed market by capturing 68.1% of the share in 2024 with the state-backed aquaculture parks, vertically integrated feed-to-farm conglomerates, and species diversity spanning carp, tilapia, shrimp, and eel. China allocates funds in aquaculture infrastructure subsidies by enabling feed mills to operate at a notable capacity utilization. Concurrently, India’s Department of Fisheries reports year-over-year feed demand growth, propelled by new smallholder ponds.

Europe Market Analysis

Europe was the next prominent region in the aquatic feed market by occupying 14.9% of share in 2024. In 2022, nearly 98% of marine ingredients like fishmeal used by companies such as Skretting were certified or from a sustainability program. Spain's total aquaculture feed consumption in 2022 was 114,177 metric tons, and it produces a significant portion of its aquaculture feed and dominates EU output. In addition, technology for automated and sensor-augmented feeding is in use and being developed in Scotland's aquaculture industry to reduce waste and improve efficiency.

North America Market Analysis

North America is another key region in the aquatic feed market, with the United States producing significant metric tons of aquafeed. The growth of North America is driven by technological precision and regulatory stringency. The FDA’s Center for Veterinary Medicine requires commercial aquafeeds to undergo nutritional adequacy trials before market release, a process that takes several months on average. Canada saw a portion of its Atlantic salmon output rely on feeds containing no terrestrial antibiotics, which drives demand for yeast-based immunostimulants and phytogenics. Recirculating aquaculture systems (RAS) are reshaping feed design. Mexico saw strong shrimp production in 2023, particularly in Sinaloa and Sonora.

Latin America Market Analysis

Latin America expanded steadily in the aquatic feed market, with Ecuador emerging as the world’s notable world shrimp feed consumer by utilizing large metric tons. This growth is vertically integrated. Companies operate local premix plants that customize formulations for Pacific white shrimp under varying salinity and temperature regimes. Brazil reports notable metric tons of tilapia feed produced, an increase, driven by tax incentives for feed mills in the Amazon basin. Chile points out that its notable metric tons of salmon output require significant metric tons of high-energy, and astaxanthin-fortified feed, a portion produced domestically.

Middle East and Africa Market Analysis

The Middle East and Africa are likely to grow in the aquatic feed market, with Egypt alone consuming notable metric tons annually, a significant share of regional demand. The growth of the Middle East and Africa is driven by state-led tilapia and mullet farming in the Nile Delta, where feed mills operate under subsidized energy tariffs and wheat bran quotas. In Nigeria, a portion of feed volume growth is driven by new catfish farms, though a share of feed is still imported due to local milling deficiencies. Saudi Arabia produces notable metric tons of shrimp and seabream feed annually under controlled-environment facilities, with the inclusion of heat-stable vitamins to withstand desert storage.

COMPETITIVE LANDSCAPE

The aquatic feed sector is characterized by oligopolistic rivalry among multinational nutrition giants and agile regional formulators. Competition pivots on biochemical precision, regulatory foresight, and logistical resilience — not merely price. Players differentiate via species-specific clinical validation, digital feeding integration, and sustainable ingredient substitution. While global leaders dominate marine carnivore and RAS segments, local mills retain share in carp and tilapia through cost-optimized, government-subsidized blends. Mergers focus on acquiring novel protein IP and regional distribution networks. Regulatory fragmentation, particularly in Africa and Latin America, creates niches for compliance-specialized entrants. Innovation velocity, not scale alone, now dictates competitive advantage.

KEY MARKET PLAYERS

A few of the market players in the global aquatic feed market include

- Cargill Inc.

- BioMar group

- Waterbase Ltd

- BASF SE

- Skretting (Nutreco)

- Alltech Inc.

- Cargill Aqua Nutrition

- Coppen International

- Evonik Industries

- Archer Daniels Midland Company

- Ridley Corporation

- Nutreco NV

- Avanti Feeds Ltd

- Ewos.

Top Players in the Market

- Cargill leverages its global grain and protein supply chains to formulate species-specific aquafeeds across many countries. It also co-developed localized tilapia and carp feeds with Indonesia’s government using fermented cassava, reducing reliance on imported soy. Its R&D collaborations focus on insect-protein scalability, which strengthens its position as an innovation anchor in emerging markets while maintaining compliance with EU and ASEAN sustainability mandates.

- Skretting drives premiumization in marine carnivore nutrition, particularly for salmon, seabass, and shrimp. Partnering with the University, it pioneered algae-based DHA systems, now replacing fish oil. The company also expanded its sensor-integrated feeding advisory services by linking feed performance to real-time biomass analytics, which transforms feed from input to an intelligent biological interface.

- BioMar specializes in high-performance feeds for recirculating and marine systems, with a strong foothold in Europe and North America. BioMar also leads in ESG-aligned sourcing by securing ASC-certified insect protein from Protix for inclusion in seabream diets, which sets benchmarks for circular aquaculture nutrition.

Top Strategies Used by Key Market Participants

Leading players deploy vertically integrated ingredient sourcing to buffer against commodity volatility, particularly securing long-term contracts for algae, insect meal, and single-cell proteins. They invest heavily in digital feed optimization platforms that link pellet dispersion to real-time fish behavior and water quality sensors. Strategic government partnerships enable localized feed formulation using underutilized regional crops, reducing import dependency. Companies also prioritize clinical validation of functional additives through university alliances, ensuring regulatory pre-approval in stringent markets. Lastly, they expand production footprints near high-growth aquaculture zones, particularly in Latin America and Southeast Asia, to minimize logistics costs and maximize freshness retention.

MARKET SEGMENTATION

This research report on the global aquatic feed market is segmented and sub-segmented into the following categories.

By Ingredient

- Soybean

- Corn, Fish Meal

- Fish Oil

- Additives

- Others

By Additive Type

- Antibiotics

- Vitamins

- Antioxidants

- Amino Acids

- Feed Enzymes

- Feed Acidifiers

- Other Additives

By End User

- Fish Feed

- Tilapia

- Salmon

- Carp

- Catfish Feed

By Molluscs

- Oyster Feed

- Mussel Feed

By Crustaceans

- Shrimp Feed

- Crab Feed

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

The current market size of the global aquatic feed market?

The current market size of the global aquatic feed market is valued at USD 192.31 billion in 2025

Who are the market drivers that are driving the global aquatic feed market?

The major factors affecting the aquatic feed market include the rising populations and the rise in income leading to increased demand for seafood.

Who are the market players that are dominating the global aquatic feed market?

The Cargill Inc., BioMar group, Waterbase Ltd, BASF SE, Alltech Inc., Coppen International, Evonik Industries, Archer Daniels Midland Company, Ridley Corporation, Nutreco NV, Avanti Feeds Ltd, Ewos. These are the market players that are dominating the global aquatic feed market.

What’s driving growth in the automotive airbags and seat belts market?

Stricter global vehicle safety regulations (like UN R16, FMVSS, and Bharat NCAP) and rising consumer demand for advanced occupant protection in both passenger and commercial vehicles are key growth catalysts.

Which regions lead in airbag and seat belt adoption?

North America, Europe, and Japan have near-universal adoption due to mature safety standards, while India, Southeast Asia, and Latin America are fast-growing markets as local regulations mandate more airbags and pretensioner-equipped seat belts.

How is vehicle electrification impacting this market?

Electric vehicles (EVs) often feature enhanced safety architectures—including additional side and curtain airbags and smarter seat belt systems with load limiters—to address battery fire risks and higher vehicle weights, boosting component complexity and value.

What innovations are shaping next-gen restraint systems?

Smart seat belts with sensors for occupant detection, inflatable seat belts, and AI-integrated airbag deployment systems that adjust based on crash severity, seating position, and passenger size are gaining traction in premium and EV segments.

Who are the dominant players in this industry?

Global leaders include ZF Friedrichshafen (via TRW), Autoliv, Joyson Safety Systems, Toyoda Gosei, and Continental—companies with decades of crash-safety expertise, Tier-1 OEM partnerships, and robust R&D in active and passive safety integration.

Are seat belts becoming obsolete with advanced airbags?

No—seat belts remain the primary restraint system; airbags are supplemental. Modern systems work synergistically, with pretensioners and load limiters in seat belts reducing injury risk before airbags even deploy.

How do cost pressures affect emerging markets?

While low-cost vehicles in regions like Africa or parts of Asia may still offer minimal airbag coverage, regulatory mandates (e.g., India’s 6-airbag rule by 2024) are rapidly closing the safety gap, driving volume growth for suppliers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com