Asia Pacific Wine Market Research Report Segmented By Taste (Dry, Medium, And Sweet Wine), Style (Still Wine, Sparkling Wine, Dessert Wine, And Fortified Wine), Color (Red Wine, White Wine And Rose Wine), & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore & Rest Of APAC) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Asia Pacific Wine Market Size

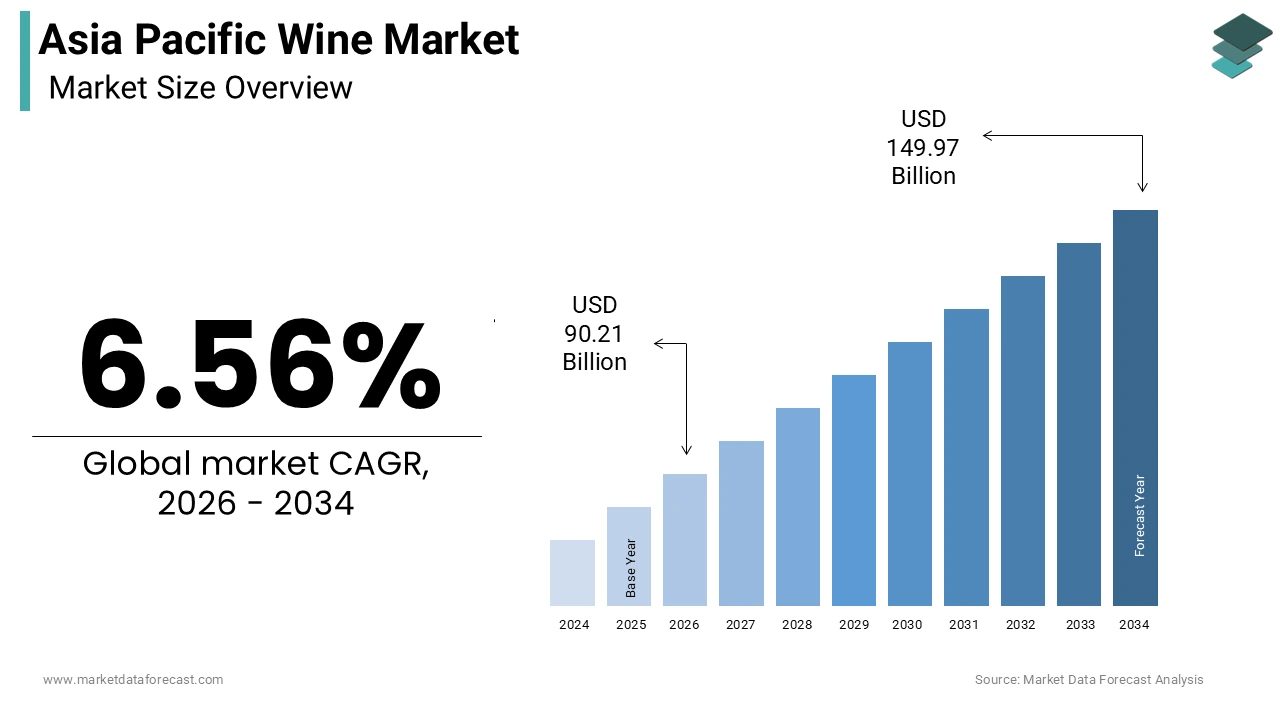

The Asia Pacific Wine Market was calculated to be USD 84.66 billion in 2025 and is anticipated to be worth USD 149.97 billion by 2034, from USD 90.21 billion in 2026, growing at a CAGR of 6.56% during the forecast period.

Wine represents a dynamic and evolving sector characterized by shifting consumer preferences toward premiumization and diverse varietals across emerging economies. This market encompasses the production, importation, and distribution of still, sparkling, and fortified wines throughout the region, including key nations such as China, Australia, New Zealand, India, and Japan. The cultural integration of wine into social and culinary experiences has accelerated, particularly among urban millennials and high-net-worth individuals who view wine as a symbol of sophistication and lifestyle enhancement. As per recent industry analysis, the Asia Pacific wine market size was valued at approximately 61.62 billion USD in 2025 and is estimated to grow from 65.08 billion USD in 2026. Another assessment indicates the market was calculated at 84.66 billion USD in 2025, with expectations to reach 149.97 billion USD by 2034. The region demonstrates a unique dichotomy where mature markets like Australia face saturation while emerging markets like India and China exhibit robust growth potential driven by rising disposable incomes. Per capita consumption remains relatively low compared to European counterparts, yet the trajectory is upward. For instance, Singapore saw its per capita wine consumption rise to 2.6 liters, up from approximately 2 liters in 2020. The market is also influenced by local production capabilities, with countries like China and India expanding their domestic vineyard areas to meet internal demand. This introductory landscape sets the stage for a complex interplay of global trade dynamics, local regulatory frameworks, and evolving consumer behavior that defines the current state of the Asia Pacific Wine Market.

MARKET DRIVERS

Rising Disposable Incomes and Premiumization Trends Drive Demand

The escalation in disposable incomes across emerging Asian economies is primarily fuelling the expansion of the wine market in the Asia-Pacific region, particularly through the lens of premiumization. As middle-class populations expand in countries such as China, India, and Vietnam, consumers are increasingly shifting from traditional spirits and beers to wine, which is perceived as a healthier and more sophisticated alternative. This demographic transition is accompanied by a willingness to spend on higher-quality products, thereby driving value growth even if volume growth remains moderate. In India, the wine market is estimated to reach 400 million USD in 2025, growing at a compound annual growth rate of approximately 8.3% from 2020 to 2025. Another source projects the Indian wine market size valued at 266.33 million USD in 2025 to reach 985.50 million USD by 2034 at a compound annual growth rate of 15.65% during 2026 to 2034. This robust growth is underpinned by urbanization and exposure to global cultures, which foster an appreciation for diverse wine varietals. Consumers are no longer satisfied with entry-level offerings but are exploring premium and super-premium segments, which offer better quality and branding. In Singapore, premium wine now accounts for 23% of the market, defined as bottles priced at 70 SGD or more. This trend is mirrored in China, where, despite overall import volume declines, the average price of imported wine has risen, indicating a shift toward quality over quantity. The average price of wine imports in China rose by 38% to 7.6 USD per liter between January and July 2025. Such data underscores that economic empowerment directly correlates with the adoption of premium wine products, thereby sustaining market momentum.

Expansion of Modern Retail and E-Commerce Channels Facilitates Access

The proliferation of modern retail formats and the rapid adoption of e-commerce platforms are further boosting the expansion of the Asia-Pacific wine market. Traditional trade channels often faced limitations in terms of product variety and consumer education, whereas digital platforms offer extensive catalogs, detailed product information, and competitive pricing. This digital transformation has been particularly crucial in reaching younger consumers who prefer the convenience of online shopping and the ability to compare products seamlessly. In China, e-commerce has become a vital channel for wine sales, with platforms offering a wide range of domestic and imported options. Although specific recent e-commerce volume data for the entire region is varied, the trend is unmistakable, with digital sales contributing substantially to overall market reach. The ease of access provided by online retailers helps overcome geographical barriers, allowing consumers in tier-two and tier-three cities to purchase wines that were previously unavailable in their local markets. Furthermore, digital marketing strategies employed by wine brands on social media platforms have increased brand awareness and consumer engagement. The integration of logistics and cold chain solutions has also improved the quality of wine delivery, ensuring that products reach consumers in optimal condition. This infrastructural development supports the growth of the wine market by reducing friction in the purchase process and enhancing customer satisfaction. As digital penetration deepens across the region, the role of e-commerce will continue to expand, thereby driving further market growth and diversification.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and High Taxation Impede Growth

The Asia Pacific wine market faces significant headwinds due to stringent regulatory frameworks and high taxation policies imposed by various governments across the region. Alcohol is often subject to heavy excise duties and special consumption taxes, which elevate retail prices and dampen consumer demand. In Vietnam, the National Assembly approved a revised Excise Tax Law in June 2025 that raises taxes on alcoholic beverages, with rates for strong liquor set to increase from 65% in 2026 to 90% by 2031. Such aggressive tax hikes are designed to curb alcohol consumption for public health reasons, but they inadvertently stifle market growth by making wine less affordable for the average consumer. Similarly, in other countries, complex licensing requirements and restrictions on advertising limit the ability of wine producers and distributors to promote their products effectively. These regulatory barriers create an uneven playing field where compliance costs are high, and market entry is difficult for new players. The uncertainty surrounding policy changes also discourages long-term investment in the sector. For instance, proposals to increase the special consumption tax on alcoholic beverages to 100% in certain markets pose a significant threat to established players, including Sabeco. These fiscal measures not only impact profitability but also restrict the potential for market expansion by limiting consumer access and affordability. Consequently, the regulatory environment remains a critical restraint that market participants must navigate carefully to sustain their operations and growth trajectories.

Climate Change and Environmental Vulnerabilities Threaten Production

Climate change is further hindering the growth of the Asia-Pacific wine market by affecting grape yields, quality, and the geographical suitability of vineyard regions. Rising temperatures, altered precipitation patterns, and increased frequency of extreme weather events such as droughts and floods disrupt the delicate balance required for viticulture. In Australia, which is a major wine producer and exporter in the region, climate change is already impacting grape phenology and harvest dates, leading to compressed harvesting windows and potential quality inconsistencies. The Australian wine sector acknowledges the ongoing threats that climate change poses to its environment and production capabilities. Similarly, in China, climate change is expected to have a strong impact on the domestic wine industry, affecting both quantity and quality of production. As global temperatures rise, some traditional wine-growing regions may become unsuitable for certain grape varieties, forcing producers to adapt by changing cultivars or relocating vineyards to cooler areas. This adaptation process is costly and time-consuming, requiring significant investment in research and development. Furthermore, water scarcity exacerbated by climate change poses a critical risk to irrigation-dependent vineyards in arid regions. The uncertainty associated with climate impacts makes long-term planning difficult for wine producers and can lead to supply chain disruptions. These environmental challenges not only affect production volumes but also influence the sensory profile of wines, potentially altering consumer preferences and market dynamics. Addressing these vulnerabilities requires sustainable practices and technological innovations, which add to the operational burden of wine producers in the region.

MARKET OPPORTUNITIES

Emergence of Local Wineries and Domestic Production Opportunities

The emergence of local wineries and the expansion of domestic wine production present a significant opportunity for the Asia-Pacific wine market by reducing reliance on imports and catering to local tastes. Countries such as China, India, and Japan are increasingly investing in their domestic wine industries, leveraging favorable climatic conditions in specific regions and government support for agricultural development. In China, the development of wine regions in Ningxia, Shandong, and Xinjiang has gained international recognition, with Chinese wines winning awards in global competitions. This local production not only meets the growing domestic demand but also offers cost advantages by avoiding import duties and logistics costs. In India, the wine industry is witnessing steady growth, with new wineries establishing themselves in regions like Nashik and Karnataka. The total volume of wine production in India stood at about 50 million liters in 2025, with products such as sparkling wines, fortified wines, and dessert wines gaining traction. Local producers are better positioned to understand and respond to local consumer preferences, such as sweeter profiles or pairings with regional cuisines. Furthermore, the promotion of domestic wines aligns with national initiatives to boost agricultural productivity and rural employment. This trend towards localization also appeals to consumers who are increasingly interested in supporting local businesses and exploring indigenous varieties. As domestic quality improves, local wineries are also beginning to explore export opportunities, thereby contributing to the overall growth and diversification of the Asia Pacific Wine Market.

Growing Tourism and Wine Culture Integration Drives Engagement

The integration of wine tourism with cultural experiences offers a compelling opportunity for the Asia-Pacific wine market by enhancing consumer engagement and brand loyalty. Wine tourism allows consumers to visit vineyards, participate in tastings, and learn about the winemaking process, thereby fostering a deeper connection with the product. In regions such as the Hunter Valley in Australia, Marlborough in New Zealand, and the Yarra Valley in Australia, wine tourism has become a significant contributor to the local economy and brand visibility. These destinations attract both domestic and international tourists who seek immersive experiences that combine leisure, education, and gastronomy. The rise of wine festivals and cultural events further promotes wine consumption by creating social occasions centered around wine appreciation. In Japan, wine tourism is gaining popularity, with visitors exploring vineyards in Yamanashi and Hokkaido. This experiential approach helps demystify wine for novice consumers and encourages trial and repeat purchases. Moreover, wine tourism supports the premiumization trend by allowing producers to showcase their high-end offerings directly to engaged consumers. The synergy between tourism and wine culture also facilitates cross-selling of related products, such as local foods and handicrafts, thereby creating a holistic ecosystem. As travel resumes and expands post-pandemic, the potential for wine tourism to drive market growth remains substantial. By leveraging the appeal of travel and cultural exploration, wine producers can build lasting relationships with consumers and differentiate their brands in a competitive market.

MARKET CHALLENGES

Counterfeit Products and Quality Concerns Undermine Trust

The prevalence of counterfeit products and concerns over quality consistency represent a major challenge for the Asia-Pacific wine market by undermining consumer trust and brand integrity. Counterfeiting is particularly problematic in high-value markets where premium wines are targeted for imitation due to their high resale value. In China, despite improvements in regulatory enforcement, counterfeit wine remains a significant issue affecting both domestic and imported brands. The presence of fake products not only results in financial losses for legitimate producers but also poses health risks to consumers who may ingest unsafe substances. This erodes consumer confidence and makes buyers hesitant to purchase high-end wines, especially through unofficial channels. Additionally, quality inconsistency among local producers can hinder the reputation of emerging wine regions. If consumers perceive local wines as inferior or unreliable, they may revert to established international brands, thereby limiting the growth potential of domestic industries. Ensuring quality control and traceability is therefore critical for maintaining market credibility. Technologies such as blockchain and smart labels are being explored to combat counterfeiting, but their widespread adoption is still in progress. The lack of standardized quality certifications across the region further complicates the issue, making it difficult for consumers to verify authenticity. Addressing these challenges requires collaborative efforts between governments, industry bodies, and producers to strengthen regulatory frameworks and enhance consumer education. Until trust is fully restored, the threat of counterfeits and quality issues will continue to impede market development.

Complex Supply Chain and Logistics Constraints Increase Costs

Complex supply chain and logistics constraints pose a significant challenge to the Asia-Pacific wine market by increasing operational costs and affecting product availability. The region's vast geographical diversity and varying infrastructure levels create difficulties in transporting wine efficiently from production sites to consumer markets. Cold chain logistics are essential for maintaining wine quality, particularly in tropical climates where temperature fluctuations can spoil products. However, the lack of adequate cold chain infrastructure in many parts of the Asia Pacific leads to higher spoilage rates and increased costs for producers and distributors. Import dependencies in many countries also expose the market to global supply chain disruptions, such as shipping delays and port congestion. These disruptions can lead to stockouts and price volatility, which negatively impact consumer satisfaction and retailer relationships. Furthermore, complex customs procedures and documentation requirements in different countries add to the administrative burden and delay clearance times. For small and medium-sized wineries, these logistical challenges can be prohibitive, limiting their ability to expand into new markets. The high cost of logistics also reduces profit margins, making it difficult for producers to compete on price. Improving supply chain efficiency requires significant investment in infrastructure and technology, which may not be feasible for all market participants. Until these logistical barriers are addressed, the Asia Pacific Wine Market will continue to face inefficiencies that hinder its full potential for growth and accessibility.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.56% |

| Segments Covered | By Taste, Wine Style, Color & Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the rest of APAC |

| Market Leaders Profiled | Caviro, Concha y Toro, Constellation Brands, Diageo, E & J Gallo, Grupo Penaflor, and Johnnie Walker. |

SEGMENTAL ANALYSIS

By Taste Insights

The dry wine segment dominated the market by capturing the highest share of the Asia-Pacific wine market in 2025. The dominance of the dry wine segment in the Asia-Pacific market is primarily due to the growing health consciousness among consumers who perceive dry wines as a healthier alternative to sweeter alcoholic beverages. The lower sugar content in dry wines aligns with the increasing demand for low-calorie and low-carbohydrate options, particularly among urban professionals and fitness enthusiasts. In China, the preference for dry red wine has been entrenched for decades, driven by the belief in its cardiovascular benefits and association with business banquets. As per industry observations, dry red wine accounts for over 80% of the total wine consumption in China, reflecting a deep-seated cultural preference for this taste profile. This dominance is further reinforced by the influence of Western dining habits, where dry wines are traditionally paired with meals. In Australia, which is a mature market, dry wines constitute the vast majority of domestic production and consumption, with Shiraz and Cabernet Sauvignon being the most popular varieties. The Australian Wine Statistics report indicates that dry table wines make up more than 90% of the total wine sales volume in the country. Similarly, in India, the emerging wine culture is heavily skewed toward dry wines, as new consumers often start with lighter dry whites or rosés before moving to heavier reds. The perception of dry wine as a sophisticated and modern choice drives its adoption among the younger demographic. This health-driven trend is expected to sustain the leadership of the dry wine segment as consumers continue to prioritize wellness in their lifestyle choices.

On the other hand, the sweet wine segment is emerging as the fastest-growing segment in the Asia Pacific wine market and is expected to exhibit a promising CAGR in the regional market during the forecast period, owing to its appeal to entry-level consumers and those with a preference for sweeter taste profiles. The lower tannin levels and fruity flavors of sweet wines make them more approachable for novice drinkers who may find dry wines too bitter or astringent. In countries like India and Vietnam, where wine consumption is still in its early stages, sweet wines serve as a gateway product, introducing consumers to the world of wine. The Indiana wine market has seen a significant uptake in semi-sweet and sweet varieties, particularly among female consumers and younger demographics. Industry data suggests that sweet wines account for a growing share of new trials in these markets, as brands introduce flavored and fruit-infused options to attract first-time buyers. In China, despite the dominance of dry reds, there is a niche but rapidly expanding market for sweet wines, such as Moscato and Ice Wine, particularly among younger urbanites. The ease of consumption and versatility of sweet wines in cocktails and desserts also contribute to their rising popularity. Social media influencers and digital marketing campaigns often highlight the aesthetic and taste appeal of sweet wines, further driving demand. As wine culture penetrates deeper into tier-two and tier-three cities, the accessibility and palatability of sweet wines ensure their rapid growth trajectory. This segment is expected to register a higher compound annual growth rate compared to dry wines, as it captures the expanding base of new wine drinkers.

By Style Insights

The still wine segment accounted for the highest share of the Asia-Pacific market in 2025. The growth of the still wine segment in the regional market can be credited to its deep integration into social and culinary traditions across the region. The versatility of still wines in pairing with diverse Asian cuisines and their established presence in formal and informal gatherings sustain their dominant market share. In China, red wine remains the cornerstone of the wine industry, driven by its symbolic value in business and family celebrations. The cultural association of red wine with good fortune and health has cemented its position as the preferred choice for gifting and hospitality. As per market data, still wines account for over 85% of the total wine volume consumed in China, reflecting their entrenched status. In Australia, still wines dominate both production and consumption, with Shiraz and Chardonnay being the most widely consumed varieties. The Australian domestic market relies heavily on still wines for everyday consumption as well as premium occasions. In India, the still wine segment is growing steadily as consumers transition from spirits to wine, with dry still reds and whites leading the adoption curve. The availability of affordable local still wines from regions like Nashik has made them accessible to a broader audience. Furthermore, the expansion of retail chains and online platforms has improved the distribution of still wines, ensuring widespread availability. The consistent demand for still wines across various price points, from entry-level to ultra-premium, ensures their continued leadership in the market. This segment benefits from established supply chains and consumer familiarity, which new styles struggle to match.

However, the sparkling wine segment is estimated to showcase the fastest CAGR in the regional market during the forecast period, owing to its strong association with celebrations and luxury lifestyles. The rising frequency of social events, weddings, and corporate gatherings in emerging economies has increased the demand for sparkling wines as a symbol of festivity and prestige. In China, the consumption of sparkling wine has surged among younger consumers who view it as a trendy and sophisticated choice for parties and holidays. The introduction of affordable domestic sparkling wines has also made them more accessible to the mass market. In India, the sparkling wine segment is experiencing robust growth, particularly in urban centers where western-influenced celebrations are becoming common. Brands are launching localized sparkling variants with lower alcohol content and fruity flavors to appeal to new drinkers. In Japan, sparkling sake and wine blends are gaining popularity as unique alternatives to traditional champagne. The flexibility of sparkling wine in mixology and cocktails also contributes to its rising appeal among bartenders and consumers. Social media trends highlighting glamorous events and toast moments further amplify the desire for sparkling wines. As disposable incomes rise and the culture of celebration expands, the sparkling wine segment is poised for accelerated growth. Its ability to cater to both premium and mass-market segments ensures a broad consumer base. The novelty and aspirational value of sparkling wine drive its rapid adoption across the region.

By Color Insights

The red wine segment held the major share of the regional market in 2025. The dominance of the red wine segment in the regional market is attributed to the widespread perceptions of its health benefits and its deep cultural significance in key markets. The presence of antioxidants such as resveratrol in red wine has been widely publicized, leading consumers to view it as a heart-healthy beverage. In China, red wine is deeply embedded in business and social customs, where it is often served at banquets and given as gifts to signify respect and prosperity. This cultural ingrainedness ensures a consistent and high volume of demand. As per industry reports, red wine accounts for approximately 70% to 80% of the total wine consumption in China, making it the undisputed leader in the color segment. In India, red wine is also the preferred choice for new wine drinkers who are introduced to the category through bold and fruity varieties. The availability of affordable local red wines has further accelerated their adoption among the middle class. In Australia, red wine dominates domestic consumption with Shiraz being the most popular variety among consumers. The strong preference for full-bodied reds in these markets sustains the leadership of the red wine segment. Additionally, the pairing of red wine with rich and spicy Asian cuisines enhances its appeal. The enduring popularity of red wine is supported by extensive marketing campaigns that highlight its health attributes and lifestyle benefits. This combination of cultural relevance and health consciousness ensures that red wine remains the dominant color segment in the Asia Pacific region.

On the other hand, the white wine segment is anticipated to showcase a promising CAGR in the regional market during the forecast period, owing to changing climate conditions and evolving taste preferences toward lighter and refreshing beverages. As temperatures rise in many parts of the region, consumers are increasingly opting for white wines, which are perceived as more suitable for warm weather. In Japan, white wine consumption has grown steadily due to its compatibility with light Japanese cuisine such as sushi and sashimi. The delicate flavors of white wines like Riesling and Sauvignon Blanc complement these dishes without overpowering them. In India, the hot climate favors the consumption of chilled white wines, particularly during the summer months. Local producers are responding to this demand by expanding their white wine portfolios with varieties like Chenin Blanc and Viognier. In Southeast Asian countries like Thailand and Vietnam, the rise of international tourism has introduced locals to white wine pairings with seafood and tropical fruits. This exposure has sparked interest in white varieties among younger consumers. The perception of white wine as a lighter and less intimidating option also attracts female drinkers and novice consumers. Social media trends showcasing refreshing white wine cocktails and summer gatherings further boost its appeal. As consumers seek diversity in their wine choices, white wine offers a versatile alternative to the dominant reds. This shift in preference is expected to drive the rapid growth of the white wine segment in the coming years.

REGIONAL ANALYSIS

China Wine Market Analysis

China had the highest share of the Asia-Pacific market in 2025 and is anticipated to experience a strategic shift toward high-value premium formats and a maturation of consumer palettes over the next few years, holding the position of the largest wine market in the Asia-Pacific region, driven by its massive population and growing middle class. The market status in China is characterized by a shift from volume-driven growth to value-driven premiumization as consumers become more discerning. The primary driving factor is the cultural integration of wine into business and social interactions, where it serves as a symbol of status and sophistication. As per recent data, China imported approximately 322 million liters of wine in 2024, reflecting a recovery in demand after previous declines. The average price of imports has risen, indicating a preference for higher-quality products. Domestic production is also expanding, with regions like Ningxia gaining international acclaim. The government support for local agriculture has boosted the competitiveness of Chinese wines. However, the market faces challenges from high taxes and regulatory restrictions on advertising. Despite these hurdles, the long-term potential remains strong due to urbanization and rising disposable incomes. The youth demographic is increasingly open to experimenting with different wine types, including sparkling and white wines. E-commerce platforms play a crucial role in reaching consumers in lower-tier cities. The combination of local production growth and premium import demand defines the current market dynamics. China's influence on the global wine trade continues to be significant as it shapes trends in packaging and branding. The market is expected to stabilize and grow steadily as consumer education improves.

Australia Wine Market Analysis

Australia is projected to maintain a highly stable domestic consumption base while aggressively pivoting toward alternative international trade avenues over the next few years, standing as a mature and highly developed wine market in the Asia Pacific region known for its high-quality production and strong export orientation. The market status is stable with consistent domestic consumption and a robust international presence. The primary driving factor is the reputation of Australian wines, particularly Shiraz and Cabernet Sauvignon, which are favored globally for their bold flavors and consistency. As per industry statistics, Australia produced approximately 1.2 billion liters of wine in the 2025 vintage, maintaining its position as a key global supplier. The domestic market is characterized by a high per capita consumption rate, with consumers preferring premium and super-premium segments. The industry is heavily focused on sustainability and innovation to address climate change impacts. Water management and carbon-neutral initiatives are central to operational strategies. The export market is diversified with key destinations including China, the United States, and the United Kingdom. Recent trade agreements have facilitated easier access to Asian markets. The local retail sector is competitive, with major supermarket chains dominating sales. Wine tourism also contributes significantly to the economy, attracting visitors to renowned regions like the Barossa and Hunter Valley. The maturity of the market means growth is driven by value addition rather than volume expansion. Australian producers continue to invest in branding and quality to maintain their competitive edge. The resilience of the industry ensures its continued leadership in the regional landscape.

India Wine Market Analysis

India is poised to witness exponential growth in urban wine adoption and domestic viticulture tourism over the next few years, representing an emerging wine market in the Asia Pacific region with high growth potential driven by urbanization and changing lifestyle preferences. The market status is nascent but expanding rapidly as wine becomes more accepted among the middle and upper classes. The primary driving factor is the increasing disposable income and exposure to global cultures, which encourage trial and adoption of wine. As per market estimates, the Indian wine market is projected to grow at a compound annual growth rate of over 8% in the coming years. Domestic production is concentrated in states like Maharashtra and Karnataka, with leading players like Sula Vineyards driving awareness. The availability of affordable local wines has made wine accessible to a broader audience. Import duties remain high, which limits the penetration of foreign brands but protects local producers. The young demographic is the key consumer base, with a preference for sweeter and lighter wines. Wine tourism is gaining traction, with vineyards offering experiences that educate consumers. Regulatory challenges, such as varying state laws on alcohol sales, create fragmentation. However, the overall trend is positive with increasing participation in social drinking. E-commerce is emerging as a vital channel for distribution. The market is expected to witness significant expansion as infrastructure improves and consumer knowledge deepens. India's potential to become a major consumer market makes it a focal point for global wine brands.

Japan Wine Market Analysis

Japan is set to reinforce its sophisticated and highly integrated food-pairing wine culture with a particular focus on low-alcohol organic varieties over the next few years, holding a sophisticated position in the Asia Pacific wine market characterized by diverse consumer preferences and a high appreciation for quality. The market status is mature with steady consumption levels and a strong culture of food pairing. The primary driving factor is the integration of wine into dining experiences, particularly with Japanese cuisine, which values harmony and balance. As per industry data, Japan imports a significant volume of wine annually, with France, Italy, and Chile being key suppliers. The domestic production of wine is also growing, with regions like Yamanashi and Hokkaido producing high-quality varieties. Consumers in Japan are well educated about wine and willing to pay premiums for authentic and artisanal products. The popularity of sparkling wine and white wine is notable due to their compatibility.y

COMPETITION OVERVIEW

The competitive landscape of the Asia Pacific wine market is characterized by a mix of established global giants and emerging local producers vying for consumer attention in a rapidly evolving environment. Intense rivalry exists among key players who continuously innovate in product offerings, branding, and distribution channels to differentiate themselves. The market sees significant competition between imported premium wines from Europe and the Americas versus domestically produced varieties that offer cost advantages and local relevance. Companies strive to build strong brand loyalty through targeted marketing campaigns and experiential engagements such as wine tours and tastings. Price competition is prevalent in the mass market segment, while premium segments compete on quality, heritage, and sustainability credentials. The rise of e-commerce has lowered entry barriers, allowing niche brands to reach wider audiences, thereby intensifying competition. Regulatory differences across countries add complexity, requiring players to adapt strategies locally. Consolidation activities, including mergers and acquisitions, are common as firms seek to expand portfolios and achieve economies of scale. This dynamic environment demands agility and strategic foresight from participants to sustain growth and maintain market relevance amidst changing consumer trends and economic conditions.

KEY MARKET PLAYERS

Some of the major companies dominating the market include

- Caviro

- Concha y Toro

- Constellation Brands

- Diageo

- E & J Gallo

- Grupo Penaflor

- Johnnie Walker.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific wine market employ several strategic initiatives to maintain competitiveness and drive growth. Premiumization remains a central strategy where companies focus on launching high-end labels to capture value from affluent consumers seeking quality and exclusivity. Digital transformation is another critical approach with brands leveraging e-commerce platforms and social media to enhance direct-to-consumer sales and engage younger audiences. Sustainability initiatives are increasingly prominent as producers adopt eco-friendly practices in viticulture and packaging to appeal to environmentally conscious buyers. Strategic partnerships and collaborations with local distributors and hospitality sectors help expand market reach and strengthen brand presence in emerging economies. Additionally, companies invest in consumer education through tasting events and wine tourism to build loyalty and deepen appreciation for their products. These multifaceted strategies enable market participants to navigate regulatory challenges and shifting consumer preferences effectively while securing long-term profitability and brand equity in the dynamic Asia Pacific region.

Leading Players in the Asia Pacific Wine Market

- Treasury Wine Estates stands as a pivotal entity within the Asia Pacific wine landscape, leveraging its robust portfolio of premium brands to captivate discerning consumers. The company has strategically focused on enhancing its direct-to-consumer channels and strengthening relationships with key retail partners across Australia, New Zealand, and China. Recent initiatives include the expansion of its luxury brand presence through targeted marketing campaigns that emphasize heritage and quality. By investing in sustainable viticulture practices and innovative packaging solutions, the company aims to align with evolving consumer preferences for environmentally responsible products. Their commitment to digital transformation has also improved customer engagement and data-driven insights, allowing for more personalized marketing efforts. This holistic approach ensures that Treasury Wine Estates maintains its competitive edge by delivering exceptional value and experiences to wine enthusiasts throughout the region while adapting to dynamic market conditions.

- Changyu Pioneer Wine Company dominates the domestic Chinese market by leveraging its extensive distribution network and deep understanding of local consumer preferences. As one of the oldest and largest wine producers in China, the company has consistently invested in modernizing its production facilities and expanding its vineyard holdings in prestigious regions like Ningxia. Recent actions include launching premium product lines that cater to the growing demand for high-quality domestic wines among affluent urban consumers. Changyu has also embraced digital marketing strategies to enhance brand visibility and engage with younger demographics through social media platforms. By collaborating with international winemaking experts, the company continues to improve the quality and complexity of its offerings. These efforts reinforce its position as a leader in the Chinese wine industry while contributing significantly to the overall growth and sophistication of the Asia Pacific wine market.

- Accolade Wines plays a significant role in the Asia Pacific wine market by offering a diverse range of brands that appeal to various consumer segments across Australia and beyond. The company has focused on optimizing its supply chain and enhancing operational efficiency to ensure consistent product quality and availability. Recent strategic moves include the divestment of non-core assets to concentrate on its premium and mainstream brands that drive higher margins. Accolade has also invested in sustainability initiatives such as water conservation and carbon reduction programs to meet the expectations of environmentally conscious consumers. By strengthening its partnerships with key retailers and hospitality providers, the company ensures broad market access and brand visibility. These actions demonstrate AccoladeWines's commitment to long-term growth and resilience in a competitive market environment while maintaining its reputation for delivering accessible and enjoyable wine experiences to customers throughout the region.

SEGMENTAL ANALYSIS

This research report on the Asia Pacific wine market is segmented and sub-segmented based on taste, wine style, color, and region.

By Taste

- Dry

- Medium

- Sweet wine

By Wine Style

- Still wine

- Sparkling wine

- Dessert wine

- Fortified wine

By Color

- Red wine

- White wine

- Rose wine

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the growth of the APAC wine market?

The growth of the APAC wine market is driven by rising disposable incomes, urbanization, changing lifestyles, and increasing adoption of Western drinking habits. The expanding middle-class population across countries such as China and India has also contributed significantly to increased wine consumption.

2. What are the major types of wine available in the APAC market?

The APAC wine market includes red wine, white wine, sparkling wine, and rosé wine. Red wine holds a dominant share due to its perceived health benefits and compatibility with regional cuisines.

4. What role does e-commerce play in the APAC wine market?

E-commerce platforms have expanded the reach of wine products by enabling consumers to explore a wide range of domestic and imported wines conveniently. Online retail has become a key distribution channel in major cities.

5. What are the key challenges facing the APAC wine market?

The market faces challenges such as high import tariffs, complex regulatory frameworks, counterfeit products, and competition from alternative alcoholic beverages such as beer and ready-to-drink cocktails.

6. Which distribution channels dominate the APAC wine market?

Supermarkets and hypermarkets dominate wine distribution due to accessibility and product variety. Restaurants, bars, specialty stores, and online retail channels also contribute significantly to market sales.

7. How is consumer preference evolving in the APAC wine market?

Consumers in the region are increasingly shifting toward premium, organic, and sustainably produced wines. There is also a growing interest in sparkling wines for celebrations and social gatherings

8. What role does wine tourism play in market growth?

Wine tourism has gained popularity in countries such as Australia and China, attracting domestic and international visitors and promoting local wine consumption.

9. Who are the major players in the APAC wine market?

Key companies operating in the region include Treasury Wine Estates, Sula Vineyards, Pernod Ricard, Constellation Brands, and Yantai Changyu Pioneer Wine Co. Ltd.

10. What is the future outlook of the APAC wine market?

The APAC wine market is expected to witness significant growth driven by rising disposable incomes, premiumization trends, expanding retail networks, and increasing consumer awareness about wine culture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com