Global Automated Security E-Gate Market Size, Share, Trends & Growth Forecast Report By Component, By Application, By End User, and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Automated Security E-Gate Market Report Summary

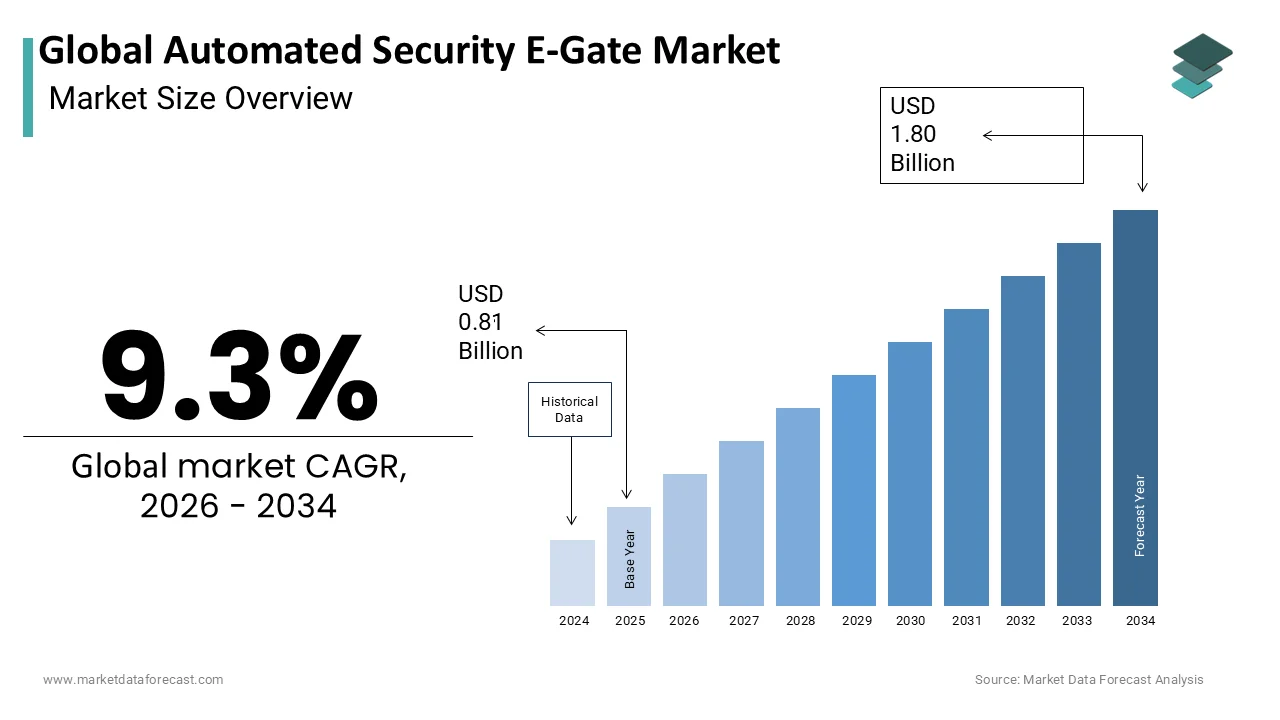

The Global Automated Security E-Gate Market was valued at USD 0.81 billion in 2025 and is projected to reach USD 1.80 billion by 2034, growing from USD 0.88 billion in 2026 at a CAGR of 9.3% during the forecast period. Growth is driven by rising global passenger volumes, stringent biometric security regulations, and expansion into land and sea border crossings. Cybersecurity risks and high implementation costs are shaping market dynamics.

Key Market Trends

- Rising deployment of e-gates beyond airports into land borders and seaports

- Growing integration of mobile digital identity wallets with border control systems

- Increasing adoption of AI-driven liveness detection and fraud prevention

- Growing regulatory pressure from systems like the EU Entry-Exit System

- Rising cybersecurity investment to protect centralized biometric databases

Segmental Insights

- Based on component, hardware dominated the market in 2025, driven by capital-intensive sensor, camera, and secure computing infrastructure requirements.

- Based on application, airports held the largest share in 2025, driven by massive passenger volumes at major international transit hubs.

- Based on end user, transportation dominated the market in 2025, driven by direct financial incentives for airlines and airport operators to reduce processing delays.

Regional Insights

- North America led the market in 2025 by holding 34.3% of the global market share, supported by extensive Customs and Border Protection modernization programs.

- Europe holds a significant share, driven by the EU Entry-Exit System and European Travel Information and Authorization System mandates.

- Asia-Pacific is expected to witness considerable growth during the forecast period, driven by massive airport construction projects in China and rising air travel demand.

Competitive Landscape

The market is highly competitive, with companies focusing on biometric accuracy, cybersecurity robustness, and seamless integration with legacy border control infrastructure. Companies are investing in AI-driven verification and cloud-based platforms to serve government and airport clients globally.

Prominent players in the market include Thales Group, IDEMIA, NEC Corporation, Vision-Box (Amadeus IT Group), Gunnebo Entrance Control Ltd., Dormakaba Holding AG, SITA, Leidos Holdings Inc., Magnetic Autocontrol GmbH (FAAC Group), Secunet Security Networks AG, Boon Edam International B.V., and Honeywell International Inc.

Global Automated Security E-Gate Market Size

The Global Automated Security E-gate Market is projected to grow from USD 0.81 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.80 billion by 2034, registering a CAGR of 9.3% during the forecast period from 2026 to 2034.

Automated security e-gate is an advanced biometric and document verification system designed to streamline passenger processing at border control points while maintaining rigorous security standards. These self-service kiosks integrate optical character recognition, facial recognition, and fingerprint scanning technologies to authenticate traveler identity against government databases without human intervention. The deployment of such systems addresses the critical need for efficiency in high-traffic international hubs where manual processing creates bottlenecks. According to the International Air Transport Association, the total number of air travelers is expected to reach 8 billion by 2040, necessitating infrastructure capable of handling massive volumes without proportional increases in staffing costs. The European Union Agency for Cybersecurity emphasizes that digital identity solutions must comply with strict data protection regulations such as the General Data Protection Regulation to ensure traveler privacy. As per the International Civil Aviation Organization, over 150 countries have adopted machine-readable travel documents, creating a standardized foundation for automated verification. Airports like Changi in Singapore process over 60 million passengers annually, demonstrating the operational scale where automation becomes essential rather than optional. The technology reduces average processing time per passenger from several minutes to under 30 seconds, significantly enhancing throughput capacity. Government initiatives worldwide focus on smart border management to balance security imperatives with the facilitation of legitimate travel. The integration of these systems into existing airport infrastructure requires careful planning to ensure seamless interoperability with legacy databases and physical security protocols.

MARKET DRIVERS

Rising Global Passenger Volumes Drive Automation Adoption

The exponential growth in international travel is majorly fuelling the adoption of automated security e-gates across major transportation hubs and is a key market driver. Airports face increasing pressure to process larger crowds efficiently while maintaining stringent security checks that prevent unauthorized entry. According to the International Air Transport Association, global passenger numbers reached 4.5 billion in 2023 and continue to climb toward pre-pandemic peaks and beyond. Manual border control processes typically require 2 to 3 minutes per passenger, whereas automated e-gates reduce this duration to approximately 15 to 30 seconds, enabling facilities to handle significantly higher throughput with existing staff levels. Heathrow Airport in London reported processing over 80 million passengers in recent years, illustrating the sheer volume that necessitates technological intervention to prevent excessive queuing times. As per the World Tourism Organization, international tourist arrivals exceeded 1.3 billion globally, placing immense strain on border infrastructure in popular destinations. Airlines and airport authorities recognize that prolonged wait times negatively impact customer satisfaction and operational efficiency, driving investment in self-service solutions. Automated systems allow border agencies to reallocate human resources to complex cases requiring detailed scrutiny rather than routine verification tasks. This shift improves overall security posture by enabling officers to focus on high-risk individuals while low-risk travelers experience expedited clearance. The scalability of e-gate systems allows airports to adjust capacity dynamically based on flight schedules and seasonal demand fluctuations.

Stringent Security Regulations Mandate Advanced Verification

Governments worldwide are implementing stricter border security mandates that require advanced biometric verification capabilities only achievable through automated e-gate systems, which is further propelling the expansion of the global automated security e-gate market. Regulatory bodies demand higher accuracy in identity authentication to combat fraud, human trafficking, and terrorism threats effectively. The European Union Entry-Exit System regulation requires third-country nationals to undergo biometric registration upon entry and exit, a process that is practically unmanageable manually given the volume of travelers. According to the European Commission, the system is designed to process the entries and exits of non-EU citizens crossing external borders, necessitating robust automated infrastructure to handle data collection and verification efficiently. The United States Department of Homeland Security has expanded its Biometric Exit program, requiring facial comparison technology at all major international airports to verify departures against visa records. As per the International Civil Aviation Organization, new standards for digital travel credentials encourage the adoption of systems capable of reading encrypted data from next-generation passports. These regulatory frameworks compel airports and border agencies to upgrade legacy equipment to meet compliance deadlines or face penalties and operational restrictions. The push for interoperability between national databases also drives the adoption of standardized e-gate technologies that can communicate securely across borders. Security agencies prioritize systems that offer audit trails and real-time alerts for suspicious activities, features inherent in modern automated solutions. Compliance with these evolving legal requirements ensures that automated e-gates remain a mandatory investment rather than an optional enhancement for international transit points.

MARKET RESTRAINTS

High Initial Implementation Costs Restrict Market Penetration

The substantial capital expenditure required for deploying automated security e-gates is primarily hampering the automated security e-gate market growth, particularly for airports in developing regions with limited budgets. A single e-gate unit involves sophisticated hardware, including high-resolution cameras, biometric sensors, and secure computing modules, along with complex software integration costs. According to industry estimates, the installation cost for a fully functional e-gate lane ranges from 50000 to 150000 dollars, depending on customization and integration requirements. Smaller regional airports often lack the financial resources to undertake such investments without external funding or government subsidies. The total cost of ownership includes ongoing maintenance, software updates, and technical support,t which further strains operational budgets. As per the Airports Council International, many airports in Africa and Latin America operate with tight margins, making large upfront technology investments challenging despite long-term efficiency gains. Budget constraints force these facilities to rely on manual processing or semi-automated solutions that do not offer the same level of throughput or security assurance. The complexity of integrating e-gates with existing border control databases and legacy IT infrastructure adds to the implementation burden, requiring specialized expertise that may not be locally available. Financial institutions and leasing options exist but often come with high interest rates or stringent conditions that deter potential buyers. Consequently, market penetration remains skewed toward wealthy nations and major international hubs, leaving a significant portion of global airports without access to advanced automation technologies.

Privacy Concerns and Data Protection Issues Hinder Acceptance

Growing public awareness regarding data privacy and surveillance creates resistance to the widespread adoption of automated security e-gates that rely on biometric data collection, which is further impeding the global market expansion. Travelers express apprehension about how their facial images, fingerprints, and personal information are stored, shared, and protected against cyber threats. According to a survey by the International Air Transport Association, nearly 40% of passengers cite privacy concerns as a barrier to accepting biometric boarding and border control processes. The European General Data Protection Regulation imposes strict limitations on the processing of biometric data, requiring explicit consent and robust security measures that complicate system deployment. Incidents of data breaches in other sectors heighten skepticism about the safety of centralized biometric databases managed by government agencies or private vendors. As per the Electronic Privacy Information Center, the lack of transparency in algorithmic decision-making raises fears of discriminatory profiling and false positives that could deny entry to legitimate travelers. Legal challenges in various jurisdictions have delayed or halted e-gate projects due to insufficient safeguards for individual rights. Public trust is essential for the smooth operation of these systems, and negative publicity surrounding data misuse can lead to boycotts or political pressure to dismantle installed infrastructure. Companies must invest heavily in cybersecurity and transparent communication strategies to mitigate these concerns, adding to the overall cost and complexity of market expansion. Ensuring compliance with diverse international privacy laws requires continuous legal monitoring and system adjustments, creating an ongoing operational burden.

MARKET OPPORTUNITIES

Expansion into Land and Sea Border Crossings Presents Growth Potential

The application of automated security e-gates is expanding beyond airports to land borders and seaports, which is opening new revenue streams for the automated security e-gate market. Traditional border crossings between neighboring countries often suffer from congestion due to manual vehicle and pedestrian checks, creating demand for efficient automated solutions. According to the European Commission, there are over 1500 land border crossing points within the Schengen Area alone, many of which are undergoing modernization to implement smart border controls. The United States Customs and Border Protection agency has piloted automated pedestrian lanes at several land ports of entry, demonstrating the feasibility of adapting e-gate technology for non-aviation environments. Seaports handling cruise passengers also present opportunities, with major terminals processing millions of tourists annually who require quick and secure embarkation and disembarkation procedures. As per the Cruise Lines International Association, global cruise passenger numbers reached 31.7 million in 2023, generating significant demand for streamlined border processing at port facilities. Railway stations serving international routes, such as those connecting France and the United Kingdom via the Channel Tunnel, are increasingly adopting e-gates to manage high-volume cross-border traffic. These diverse applications require customized hardware designs capable of withstanding different environmental conditions and usage patterns, offering manufacturers chances to develop specialized product lines. Government initiatives to enhance regional connectivity and facilitate trade often include funding for border infrastructure upgrades, providing financial incentives for adoption in these emerging segments.

Integration with Mobile Digital Identity Solutions Offers Innovation

The convergence of automated e-gates with mobile digital identity applications creates innovative opportunities for the automated security e-gate market growth. Governments and technology firms are developing smartphone-based digital wallets that store verified identity credentials, allowing passengers to present their documents electronically at e-gates. According to the International Civil Aviation Organization, the Type 1 Digital Travel Credential standard enables secure transmission of identity data from mobile devices to border control systems, reducing reliance on physical passports. This integration allows for pre-arrival verification, where travelers submit their biometric data and travel documents via apps before reaching the border, enabling faster processing upon arrival. Apple and Google have introduced digital identity features in their operating systems, facilitating widespread adoption among consumers with compatible devices. As per the European Union, the European Digital Identity Wallet initiative aims to provide citizens with secure digital credentials usable across member states, including for border crossing purposes. E-gate manufacturers are updating their hardware to include near-field communication and Bluetooth capabilities to interact with mobile devices, creating a more flexible and user-friendly interface. This trend supports contactless processing, which gained importance during health crises and remains preferred for hygiene reasons. The ability to update credentials remotely and revoke compromised identities instantly enhances security compared to static physical documents. Technology providers that successfully integrate mobile compatibility into their e-gate solutions gain a competitive advantage by offering future-proof systems aligned with global digital transformation trends.

MARKET CHALLENGES

Cybersecurity Threats Pose Significant Operational Risks

Automated security e-gates are increasingly targeted by cybercriminals seeking to exploit vulnerabilities in biometric databases and network connections, which is posing severe operational and reputational challenges to the automated security e-gate market. These systems rely on continuous connectivity to central government databases for real-time verification, making them susceptible to denial-of-service attacks, data interception, and malware infiltration. According to the European Union Agency for Cybersecurity, critical infrastructure sectors, rs including border control,rol experienced a 30% increase in cyber-attacks in recent years, and this indicates the growing threat landscape. A successful breach could compromise sensitive biometric data of millions of travelers, leading to identity theft and fraud on a massive scale. Ransomware attacks targeting airport operations have caused significant disruptions in the past, forcing reversion to manual processes and causing extensive delays. As per the Department of Homeland Security, ensuring the integrity of biometric matching algorithms is crucial to prevent spoofing attempts using deepfake technology or synthetic identities. The complexity of securing interconnected systems involving hardware vendors, software developers, and government agencies creates multiple attack vectors that are difficult to monitor comprehensively. Regular security audits and penetration testing are required but often lag behind the rapid evolution of cyber threats. Insurance coverage for cyber incidents in critical infrastructure is expensive and may not cover all potential liabilities. The need for constant vigilance and investment in advanced cybersecurity measures adds to the total cost of ownership and requires specialized skills that are in short supply. Failure to adequately protect these systems can result in regulatory fines, loss of public trust, and suspension of operations.

Technical Limitations in Biometric Accuracy Affect Reliability

Despite advancements in technology, biometric verification systems used in automated e-gates still face challenges related to accuracy and reliability under varying conditions, which is further challenging the expansion of the global automated security e-gate market. Facial recognition algorithms may struggle with changes in lighting, angles, or appearance due to aging, injuries, or accessories such as glasses and masks. According to the National Institute of Standards and Technology, error rates in facial recognition can vary significantly across different demographic groups, raising concerns about fairness and potential discrimination. Fingerprint scanners may fail to read prints accurately if fingers are wet, dirty, or worn, leading to false rejections that frustrate travelers and require manual intervention. As per the International Civil Aviation Organization, achieving high accuracy in high-throughput environments remains technically challenging. Environmental factors such as humidity, temperature, and dust in land border crossings or seaports can degrade sensor performance over time, requiring frequent calibration and maintenance. The diversity of passport designs and quality from different issuing countries also affects optical character recognition accuracy, leading to processing errors. System downtime due to technical glitches can cause significant backlogs, negating the efficiency benefits of automation. Continuous improvement in algorithm training and sensor technology is necessary to address these limitations, but perfect accuracy remains elusive. Operators must maintain sufficient staff to handle exceptions and failures, limiting the extent to which human resources can be reduced. Balancing speed with accuracy remains a critical engineering challenge that impacts user satisfaction and security effectiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Application, End User, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment dominated the market by holding the highest share of the global automated security e-gate market in 2025 due to the physical infrastructure requirements essential for biometric verification and document authentication at border points. The substantial capital investment required for specialized sensors, cameras, and secure enclosures drives revenue concentration in this category. According to the International Civil Aviation Organization, over 150 countries have mandated machine-readable travel documents, necessitating hardware upgrades at thousands of border crossing points globally to read encrypted chips and optical characters accurately. Each e-gate installation requires high-resolution facial recognition cameras, fingerprint scanners, and passport readers that meet stringent international standards for durability and accuracy. As per industry estimates, a single fully equipped e-gate lane costs between 50000 and 150000 dollars, with hardware accounting for approximately 60% of total system value. Government procurement cycles favor long-term hardware investments that provide operational stability for 10 to 15 years before replacement is necessary. The physical nature of these systems creates recurring demand as airports and border agencies expand capacity or replace aging equipment. Manufacturing complexity involving precision optics and secure computing modules limits supplier options, maintaining premium pricing structures. Hardware vendors benefit from proprietary designs that create vendor lock-in effects, ensuring sustained service contracts and component sales throughout the product lifecycle.

However, the software segment is expected to demonstrate the fastest growth and grow at a CAGR of 13.2% during the forecast period in the global market owing to the continuous algorithmic improvements and regulatory compliance updates. Unlike hardware, which has longer replacement cycles, software requires frequent updates to address emerging security threats and integrate new biometric modalities. According to the European Union Agency for Cybersecurity, border control systems must undergo regular security patches and algorithm retraining to counter evolving spoofing techniques and maintain compliance with data protection regulations. The implementation of the European Union Entry-Exit System mandates significant software integration work across member states to connect national databases with centralized EU systems, generating substantial licensing and development revenues. As per the National Institute of Standards and Technology, facial recognition algorithms require ongoing refinement to reduce demographic bias and improve matching accuracy under varying environmental conditions. Cloud-based software architectures enable remote updates and centralized management, creating subscription revenue models that provide predictable income streams for vendors. Artificial intelligence enhancements for liveness detection and behavioral analysis add new functionality without requiring hardware replacements. Software customization for specific national requirements and interoperability standards drives professional services revenue alongside licensing fees. The shift toward digital travel credentials and mobile identity integration further accelerates software development needs as systems must support multiple credential types simultaneously.

By Application Insights

The airports segment held the largest share of the global market in 2025 and will likely maintain its dominant position in the coming years due to massive passenger volumes and the necessity for automated processing at major international transit hubs. The concentration of high-value infrastructure and regulatory pressure makes aviation the primary deployment environment for these systems. According to the International Air Transport Association, global air passenger traffic reached 4.5 billion in 2023, with major hubs processing tens of millions of travelers annually through limited border control resources. Heathrow Airport alone handles over 80 million passengers yearly, requiring extensive e-gate networks to maintain acceptable processing times and security standards. As per the Airports Council International, airport capital expenditure on security technology remains a significant portion of overall security investments. International aviation regulations established by the International Civil Aviation Organization create uniform requirements for passenger verification that drive standardized e-gate deployments across jurisdictions. The economic impact of flight delays caused by border congestion incentivizes airports to invest heavily in automation to improve throughput and passenger satisfaction. Premium airline alliances and government-trusted traveler programs further accelerate adoption by creating dedicated lanes for eligible passengers. Airport modernization projects in emerging markets consistently include e-gate installations as core components of new terminal designs, ensuring sustained demand growth in this application segment.

On the other side, the border control segment is poised for rapid growth in the coming years and is predicted to record a CAGR of 12.25 during the forecast period as governments extend automated verification to land crossings and seaports. Traditional manual processing at land borders creates significant bottlenecks for commercial transport and commuter traffic, driving urgent modernization efforts. According to the European Commission, the Schengen Area operates over 1500 land border crossing points, many undergoing smart border upgrades to implement the Entry-Exit System and reduce wait times for legitimate travelers. The United States Customs and Border Protection agency has deployed automated pedestrian lanes at major land ports of entry along the Mexican and Canadian borders, processing millions of crossings annually with enhanced security verification. As per the World Customs Organization, cross-border trade facilitation initiatives prioritize technology adoption to reduce clearance times while maintaining security controls, creating funding opportunities for e-gate deployments. Railway stations serving international routes such as Eurostar terminals are expanding e-gate capacity to handle growing passenger numbers efficiently. Seaport cruise terminals process millions of tourists seasonally, requiring scalable automated solutions to manage peak embarkation and disembarkation periods. Government regional connectivity programs often include border infrastructure funding that specifically targets automation projects. The adaptation of e-gate technology for outdoor environments and vehicle processing creates new product variants and market opportunities distinct from airport installations.

By End User Insights

The transportation end-user segment dominated the market by accounting for the largest share of the automated security e-gate market in 2025 due to the critical need for efficient passenger processing at airports, railways, and maritime facilities. Airlines, airport authorities, and rail operators face direct economic consequences from border delays, making them primary purchasers of automation technology. According to the International Air Transport Association, airlines lose approximately 30 dollars per passenger for every minute of delay caused by ground processing inefficiencies, creating strong financial incentives for automation investment. Major airport operators like Changi Airport Group and Dubai Airports have deployed hundreds of e-gates to handle annual passenger volumes exceeding 60 million and 80 million, respectively. As per the Cruise Lines International Association, global cruise passenger numbers exceeded 30 million in recent years, with port authorities investing in automated border control to streamline embarkation procedures and enhance destination competitiveness. High-speed rail networks connecting international destinations,s such as those between France and the United Kingdom,m require seamless border verification to maintain schedule reliability. Transportation operators benefit from improved passenger satisfaction scores and reduced staffing costs through automation deployment. Public-private partnership models for airport and port operations often include technology upgrade commitments that guarantee e-gate procurement. The competitive nature of international transit hubs drives continuous investment in passenger experience enhancements where automated border control plays a central role in differentiation strategies.

However, the government end-users represent segment is anticipated to register a CAGR of 11.4% during the forecast period as national security agencies expand automated border control beyond traditional transportation venues. Immigration authorities and border protection agencies are deploying e-gates at consulates, visa application centers, and government buildings to enhance security and operational efficiency. According to the United States Department of Homeland Security, federal agencies have allocated billions of dollars for biometric exit and entry modernization programs across multiple fiscal years, driving large-scale government procurement. The European Union’s smart border package mandates member states' implementation of automated systems at all external border points, creating synchronized demand across 27 nations. As per the Australian Department of Home Affairs, the SmartGate system processes over 20 million travelers annually at international airports and is being extended to additional government facilities. National identity programs integrating biometric verification create domestic use cases for e-gate technology at government service centers and electoral offices. Defense departments are adopting similar technologies for base access control and personnel verification, expanding the addressable market beyond civilian border applications. Government digital transformation initiatives of a ten include border security modernization as a priority spending area with dedicated budget allocations. Interagency data sharing requirements drive integration projects that generate additional software and services revenue for vendors serving government clients.

COUNTRY LEVEL ANALYSIS

North America Automated Security E Gate Market Analysis

North America accounted for 34.35 of the global market share in 2025 and is likely to maintain its leadership position in the coming years due to ongoing government investments and the deployment of advanced biometric programs across its borders. The United States dominates regional demand through extensive Customs and Border Protection modernization programs and major airport infrastructure upgrades. According to the Department of Homeland Security, the Biometric Exit program has been implemented at all major international airports, covering a vast majority of departing air passengers with facial comparison technology. Canada Border Services Agency has deployed Primary Inspection Kiosks at major airports processing over 50 million travelers annually with automated document verification and biometric confirmation. As per the Federal Aviation Administration, US airports handled hundreds of millions of passengers in recent years, creating massive operational pressure that drives continuous e-gate expansion and technology refresh cycles. Regional leadership in biometric algorithm development and cybersecurity standards influences global product specifications and interoperability requirements. Strong privacy regulations and civil liberties oversight shape system design parameters differently than in other regions, requiring vendors to develop compliant solutions. Cross-border cooperation between US and Canadian authorities facilitates harmonized technology standards and joint procurement initiatives. The presence of major technology companies and defense contractors supports domestic innovation and export capabilities. Government funding mechanisms, including homeland security grants,s provide financial support for smaller airports and land border crossings to adopt automation technologies.

Europe Automated Security E-Gate Market Analysis

Europe is expected to continue its synchronized market expansion in the coming years, driven by regional mandates and the full implementation of new border security frameworks. The European Union Entry-Exit System and European Travel Information and Authorization System create synchronized demand across 27 nations, requiring simultaneous infrastructure upgrades. According to the European Commission, the Entry-Exit System will register biometric data for hundreds of millions of third-country nationals annually upon full implementation, representing the largest coordinated border technology deployment globally. The United Kingdom operates one of the world’s most extensive e-gate networks with over 300 units at airports and rail terminals, processing tens of millions of passengers despite post-Brexit regulatory divergence. As per Frontex, the European Border and Coast Guard Agency coordinates technical standards and best practices across member states to ensure interoperability and security consistency. Strict General Data Protection Regulation compliance requirements influence system architecture and data handling procedures differently than in other regions. The Schengen Area’s open internal borders create unique external border security pressures that justify substantial automation investments. Regional manufacturers like Thales and Idemia benefit from home market advantages and a deep understanding of local regulatory requirements. European Investment Bank funding supports infrastructure modernization projects in newer member states with less developed border technology. Ongoing migration management challenges maintain political support for border security technology spending across the region.

Asia-Pacific Automated Security E-Gate Market Analysis

Asia-Pacific is poised to maintain its status as the fastest-growing regional market in the coming years due to massive airport construction projects and increasing demand for seamless travel. China leads regional expansion with plans to construct over 200 new airports by 2035, according to the Civil Aviation Administration of China, each requiring comprehensive automated border control systems. Japan has deployed advanced e-gate networks at Narita, Haneda, and Kansai airports,s processing over 30 million international passengers annually with cutting-edge facial recognition technology. As per the International Air Transport Association, Asia-Pacific remains a high-growth region for global air travel, necessitating significant investment in automated border technologies to maintain efficient operations at transit hubs.

COMPETITIVE LANDSCAPE

The automated security e-gate market features intense competition among established technology giants and specialized security firms vying for government contracts and airport modernization projects. Market participants differentiate themselves through superior biometric accuracy, robust cybersecurity features, a nd seamless integration capabilities with existing border control infrastructure. High barriers to entry due to stringent regulatory requirements and complex procurement processes limit new competitors but encourage continuous innovation among existing players. Companies compete based on technical performance, reliability, and ability to meet strict data protection standards mandated by governments worldwide. Pricing pressure exists but is mitigated by the critical nature of security infrastructure, where quality and compliance often outweigh cost considerations. Technological adoption varies across competitors, rs with leaders investing heavily in artificial intelligence and machine learning to improve verification speeds and reduce error rates. Service quality,ity including installation, support, maintenance, and software updates, serves as a key differentiator in securing long-termcontracts with public sector entities. Geographic reach determines the ability to serve multinational clients requiring consistent technology standards across different jurisdictions. Regulatory compliance long-termers also distinguish competitors as adherence to evolving international standards becomes increasingly complex. The concentration of market power among a few major players creates an oligopolistic structure where collaboration on industry standards coexists with fierce competition for individual high-value projects.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Automated Security E-Gate Market include

- Thales Group

- IDEMIA

- NEC Corporation

- Vision-Box (Amadeus IT Group)

- Gunnebo Entrance Control Ltd.

- Dormakaba Holding AG

- SITA

- Leidos Holdings, Inc.

- Magnetic Autocontrol GmbH (FAAC Group)

- Secunet Security Networks AG

- Boon Edam International B.V.

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Thales Group stands as a global leader in secure identity solutions with extensive expertise in biometric verification and border control systems. The company provides comprehensive gate hardware and software platforms that integrate facial recognition and document authentication technologies for major international airports. Thales recently enhanced its Smart Border solution suite by incorporating advanced artificial intelligence algorithms to improve processing speed and accuracy under varying lighting conditions. This technological upgrade allows authorities to handle higher passenger volumes while maintaining strict security standards. The firm actively collaborates with government agencies to ensure compliance with evolving international regulations such as the European Union Entry Exit System. Thales maintains a strong presence in Europe and Asia Pacific through strategic partnerships with local integrators. Their continuous investment in research and development ensures their systems remain at the forefront of cybersecurity and biometric innovation.

- IDEMIA is an e-gateinent player in the automated security e-gate market, offering end-to-end solutions for border management and traveler facilitation. The company combines hardware manufacturing with sophisticated software analytics to deliver seamless passenger experiences at airports and land-based end-to-end. IA recently launched its Augmented Identity platform,m which leverages machine learning to enhance fraud detection capabilities and reduce false rejection rates. This innovation strengthens their value proposition by addressing key operational challenges faced by border authorities. The firm's next-generation e-gates contract is for deploying next-generation e-gates in Middle Eastern and Asian hubs.itsIA focuses on interoperability, ensuring its systems work seamlessly with various national databases and legacy infrastructure. Their commitment to privacy by design helps clients navigate complex data protection regulations while delivering efficient border processing services globally.

- SITA specializes in information technology and communication solutions for the air transport industry,y including advanced automated border control systems. The company offers the Smart Pate-gateetric journey solution, which integrates e-gate functionality with airport operational systems for a seamless traveler experience. SITA recently expanded its biometric platform to support mobile digital credentials, allowing passengers to use their smartphones for identity verification at gates. This development aligns with International Civil Aviation Organization standards for digital travel credentials and enhances user convenience. The firm partners with major airports worldwide to implement cloud-based biometric matching services that improve scalability and reduce infrastructure costs. SITA’s focus on open-source enables easy integration with third-party security systems and airline departure control platforms. Their global service network ensures reliable maintenance and support for critical border control infrastructure at high-traffic aviation hubs.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the automated security e-gate market employ several strategic approaches to maintain competitive advantages and drive growth. Product innovation remains a primary strategy as companies use multimodal advanced biometric algorithms and multimodal verification systems to enhance accuracy and speed. Strategic partnerships with government and large-scale airport authorities facilitate large-scale deployments and ensure compliance with regional regulatory requirements. Geographic expansion into emerging markets allows participants to capture growth opportunities in regions with expanding aviation infrastructure and rising passenger volumes. Mergers and acquisitions enable firms to consolidate technical expertise and broaden their product portfolios to offer comprehensive border management solutions. Investment in cybersecurity measures protects sensitive biometric data and builds trust among public sector clients concerned about cloud-based data breaches. Development of cloud-based platforms offers scalable and cost-effective solutions for smaller airports and border crossings with limited IT resources. Focusing on interoperability ensures systems can integrate with diverse national databases and legacy infrastructure, reducing complexity for clients.

MARKET SEGMENTATION

This research report on the global automated security e-gate market is segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

- Services

By Application

- high-value

- ports

- Border Control

- Railway Stations

- Seaports

By End User

- Transportation

- Government

- Commercial Buildings

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is driving growth in this market?

Growth is driven by higher security and border‑control needs, expansion of airports and transport hubs, smart‑city projects, and demand for faster, contactless access.

2. Where are e‑gates used most?

They are used in airports, border control points, corporate offices, stadiums, metro stations, and critical infrastructure sites.

3. Which segment leads the market?

Hardware and e‑gate terminals form the core of the market, supported by sensors, software, and integration services.

4. Which application is most important?

Border control and airport security are leading applications, with strong growth in corporate and venue security as well.

5. Which region leads the market?

North America and Europe are major markets, with strong adoption in the U.S., Germany, and other developed economies.prnewswire+1

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com