Global Automotive Bumpers Market Size, Share, Trends & Growth Forecast Report By Material, By Positioning, By End Market, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Automotive Bumpers Market Report Summary

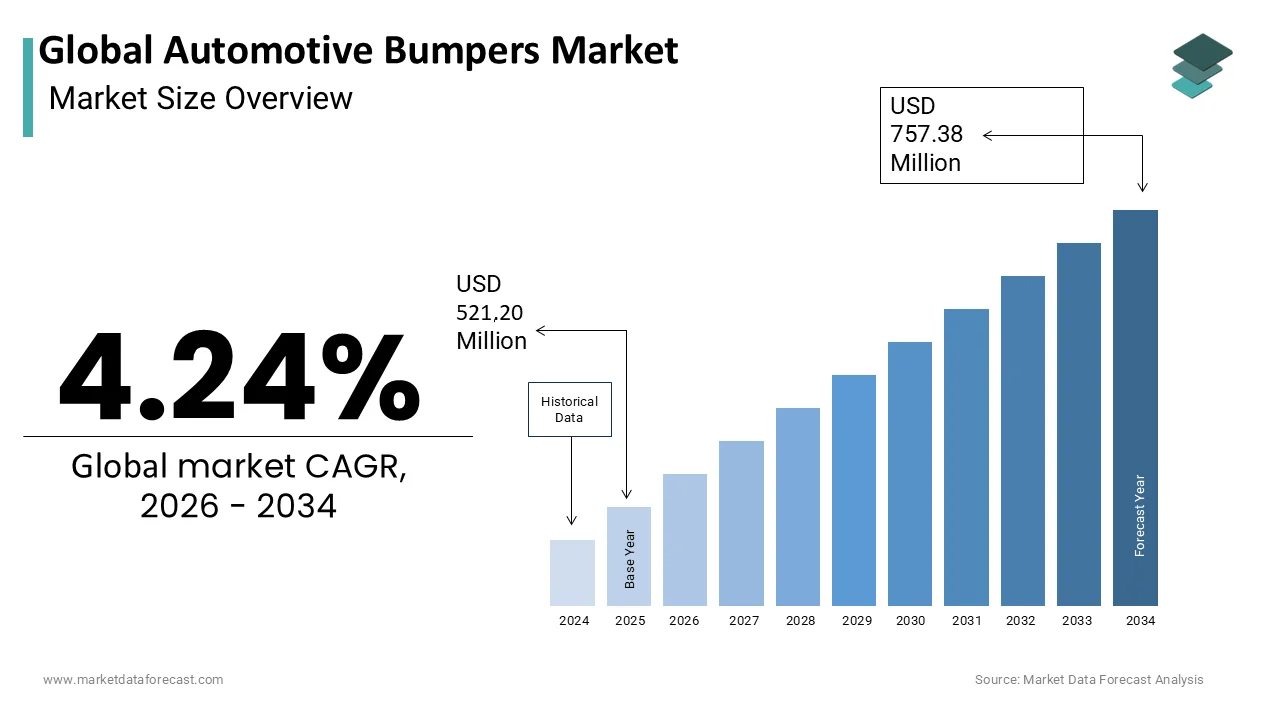

The Global Automotive Bumper Market was valued at USD 521.20 million in 2025 and is projected to reach USD 757.38 million by 2034, growing from USD 543.30 million in 2026 at a CAGR of 4.24% during the forecast period. Growth is driven by stringent pedestrian safety and crashworthiness regulations, accelerated adoption of lightweight materials for fuel efficiency, and expansion of electric vehicle-dedicated platforms. Raw material price volatility and the complexity of ADAS sensor integration are shaping market dynamics.

Key Market Trends

- Rising integration of ADAS sensors like radar and lidar within bumper assemblies

- Growing adoption of fiber-reinforced composites for ultra-lightweight EV applications

- Increasing demand for aftermarket customization, including sporty and rugged bumper kits

- Expansion of active aerodynamic features like air curtains and grille shutters for EVs

- Rising regulatory pressure for closed-loop recycling under end-of-life vehicle targets

Segmental Insights

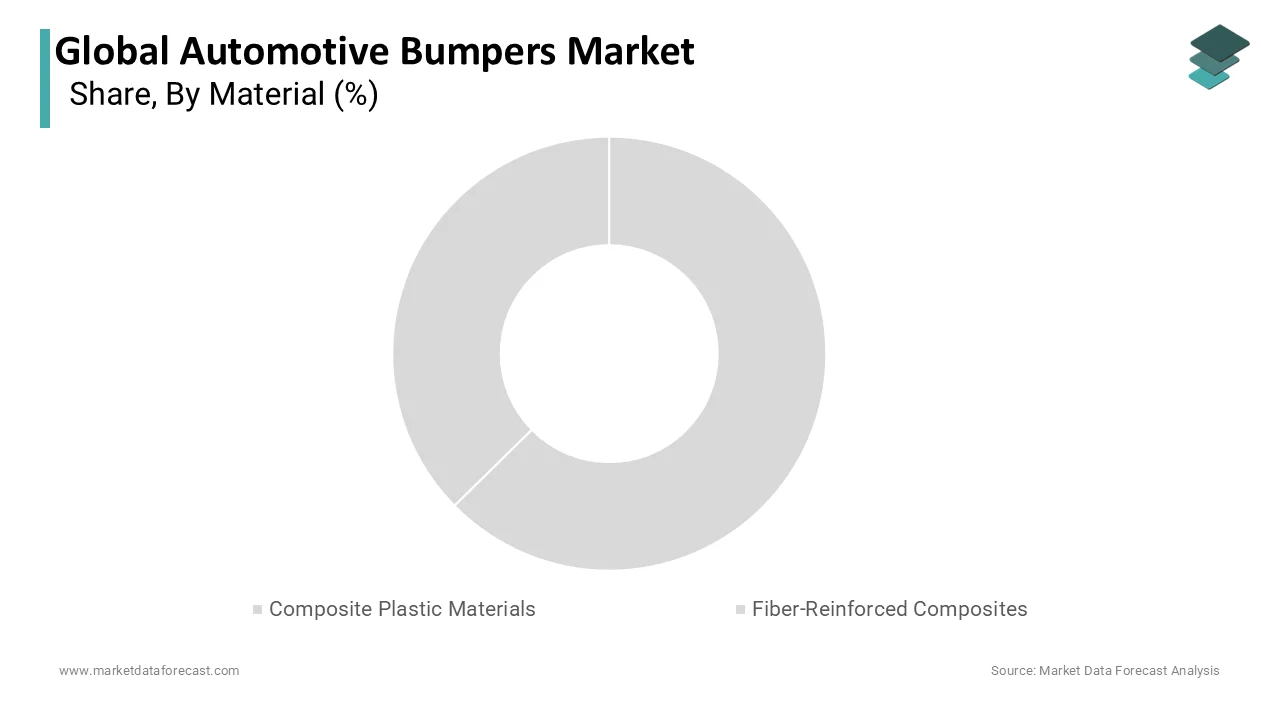

- Based on material, composite plastic materials held 32.1% of the market share in 2025, driven by weight reduction capabilities and cost-effective mass production.

- Based on positioning, front-end bumpers held 36.2% of the market share in 2025, driven by their role in housing ADAS sensors and engine protection.

- Based on the end market, OEM accounted for 34.5% of the market share in 2025, driven by continuous new vehicle production requiring precisely engineered bumpers.

Regional Insights

- North America led the market in 2025 by holding 34.6% of the global market share, supported by high vehicle ownership and a strong customization culture.

- Europe holds a significant share of 24.7%, driven by EU Green Deal lightweighting mandates and a strong emphasis on pedestrian safety.

- Asia Pacific is expected to witness the fastest growth during the forecast period, driven by rapid industrialization and China's EV adoption push.

- Rear-end bumpers are the fastest-growing positioning segment, projected at a CAGR of 12.6%, driven by rising rear-view camera and parking sensor integration.

Competitive Landscape

The market is highly competitive, with multinational corporations and regional suppliers competing on materials science innovation, cost efficiency, and ADAS integration capability. Companies are investing in lightweight composites and sustainability initiatives like recycled material use to meet regulatory and OEM demands.

Prominent players in the market include Plastic Omnium SE, Magna International Inc., Flex-N-Gate Corporation, Toyoda Gosei Co. Ltd., Hyundai Mobis Co. Ltd., Samvardhana Motherson International Limited (SMR), Faurecia SE (FORVIA), Tong Yang Group, Montaplast GmbH, Gestamp Automoción S.A., Valeo SA, and Yanfeng Automotive Interiors Co. Ltd.

Global Automotive Bumpers Market Size

The Global Automotive Bumper Market is projected to grow from USD 521.20 million in 2025 to USD 543.30 million in 2026 and reach USD 757.38 million by 2034, registering a CAGR of 4.24% during the forecast period from 2026 to 2034.

The automotive bumpers are the design, manufacture, and distribution of protective structures installed at the front and rear extremities of motor vehicles. These components serve a dual purpose by absorbing impact energy during low-speed collisions to minimize damage to vehicle systems, such as lights, radiators, and exhaust systems, while also contributing significantly to the aesthetic appeal and aerodynamic efficiency of the automobile. Modern bumpers have evolved from simple steel bars into complex assemblies comprising plastic covers, foam absorbers,s and reinforcement beams made from advanced materials like aluminum or composite plastics. According to the International Organization of Motor Vehicle Manufacturers, global motor vehicle production reached approximately 89 million units in 2023, reflecting the sustained demand for new vehicles and consequently their constituent parts. Furthermore, the European Commission states that transport accounts for nearly 25% of total greenhouse gas emissions in the European Union, prompting manufacturers to adopt lighter materials in bumper construction to enhance overall vehicle efficiency. As consumer preferences shift towards sport utility vehicles and electric vehicles, the structural requirements for bumpers change,e necessitating robust yet lightweight solutions.

MARKET DRIVERS

Stringent Safety Regulations and Pedestrian Protection Standards

The global regulatory frameworks mandating enhanced crashworthiness and pedestrian safety for innovation and demand are fuelling the growth of the automotive bumpers market. Governments worldwide are implementing stricter norms that require bumpers to absorb impact energy effectively, while minimizing injury risks to pedestrians in the event of a collision. The National Highway Traffic Safety Administration in the United States enforces Federal Motor Vehicle Safety Standard 215, which specifies exterior protection standards for passenger cars, rs ensuring that bumpers meet specific height and energy absorption criteria. Similarly, the European New Car Assessment Program evaluates pedestrian protection performance, influencing design choices across major automakers. According to the World Health Organization, road traffic injuries result in approximately 1.19 million deaths annually globally, with pedestrians representing a significant proportion of vulnerable road users. Automakers are increasingly integrating flexible fascia designs that deform upon impact to reduce leg and head injuries. Compliance with these rigorous standards necessitates continuous research and development,t leading to the adoption of advanced materials and modular designs. The regulatory pressure not only ensures higher safety benchmarks but also drives the replacement cycle for older designs, ns fostering consistent demand for technologically advanced bumper systems that align with contemporary safety protocols and legal requirements.

Accelerated Adoption of Lightweight Materials for Fuel Efficiency

The imperative to reduce vehicle weight to enhance fuel efficiency and extend electric vehicle range is significantly promoting the growth of the automotive bumpers market. Automakers are aggressively replacing traditional steel components with lightweight alternatives, such as thermoplastics, carbon fiber-reinforced polymers, and aluminum alloys. In the context of electric vehicles, every kilogram saved contributes directly to extended driving range, which is a key selling point for consumers. Major material suppliers are developing high-performance polymers that maintain structural integrity under impact, while minimizing mass. For instance, the use of long glass fiber-reinforced polypropylene allows for thinner wall thicknesses without compromising strength. This shift supports the broader industry goal of sustainability by lowering energy consumption during both vehicle operation and manufacturing processes. As emission norms tighten globally, the demand for lightweight bumper solutions intensifies, prompting suppliers to innovate in material science and processing technologies to deliver cost-effective and efficient components that meet the rigorous performance expectations of modern automotive platforms.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuations in the prices of key raw materials, such as polypropylene, polycarbonate, and aluminum is hindering the growth of the automotive bumpers market. These materials constitute a substantial portion of production costs, and their prices are subject to global commodity dynamics,s geopolitical tensions and energy costs. The global commodity price indices experienced significant volatility in recent years, as energy prices impacted the cost of producing plastics and metals. For example, a surge in crude oil prices directly increases the cost of petrochemical derivatives used in manufacturing plastic bumper fascias. Additionally, supply chain disruptions caused by geopolitical conflicts or natural disasters can lead to shortages of essential resins and alloys, forcing manufacturers to seek alternative sources at premium prices. The Semiconductor Shortage, which affected the broader automotive industry, also had ripple effects on the production of smart bumpers integrated with sensors. These uncertainties complicate financial planning and pricing strategies for bumper manufacturers, who often operate on thin margins. Long-term contracts with suppliers may mitigate some risks but cannot fully shield companies from sudden shocks. Consequently, the unpredictability of input costs restrains investment in new capacities and innovation as firms prioritize cost containment over expansion.

Complexity of Integrating Advanced Driver Assistance Systems

The increasing integration of Advanced Driver Assistance Systems sensors into bumper assemblies introduces technical complexities and cost pressures that are impeding the growth of the automotive bumpers market. Modern bumpers are no longer passive protective elements but active components housing radar, lidar,r and ultrasonic sensors essential for features like adaptive cruise control,rol automatic emergency braking, and parking assistance. However, embedding these sensitive electronic components within plastic or composite structures requires precise engineering to ensure signal transparency and protection from environmental factors, such as heat, moisture, and physical impact. Any misalignment or material interference can degrade sensor performance, leading to safety risks and costly recalls. The need for specialized testing and validation processes increases development time and expenditure for manufacturers. Furthermore, the repairability of such integrated bumpers is challenging as minor damages may require recalibration or replacement of expensive sensors rather than just the plastic cover. This complexity raises the total cost of ownership for consumers and insurers,s potentially slowing the adoption of highly integrated bumper systems.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Production and Dedicated Platforms

The rapid proliferation of electric vehicles, as manufacturers develop dedicated platforms with unique design requirements,s is likely to pose new opportunities for the growth of the automotive bumpers market. Electric vehicles often feature distinct front ends due to the absence of large internal combustion engines, allowing for innovative bumper designs that enhance aerodynamics and cooling efficiency for battery systems. According to the International Energy Agency, electric car sales exceeded 14 million units globally in 20,23 accounting for 18% of all cars sold, indicating a robust shift in automotive architecture. This transition creates demand for specialized bumper systems that integrate air curtains and active grille shutters to optimize airflow and reduce the drag coefficient. Lower drag directly translates to improved range, which is a critical metric for electric vehicle competitiveness. Bumper manufacturers can capitalize on this trend by offering lightweight aerodynamic solutions tailored specifically for electric platforms. Additionally, the modular nature of many electric vehicle designs facilitates easier customization and faster iteration of bumper styles,s enabling brands to differentiate their models visually. Supplies that collaborate early with electric vehicle developers can secure long-term contracts and establish themselves as preferred partners in this growing segment. The focus on sustainability in electric vehicle production also opens avenues for using recycled and bio-based materials in bumper construction, aligning with the eco-friendly brand image of many electric vehicle manufacturers and appealing to environmentally conscious consumers.

Growth in Aftermarket Customization and Personalization Trends

The rising consumer interest in vehicle customization and personalization is another factor that promotes new opportunities for the growth of the automotive bumpers market. Car enthusiasts and owners increasingly seek to modify their vehicles with sporty, aggressive,e or luxury-styled bumpers to enhance aesthetic appeal and individuality. Social media platforms and automotive culture have amplified the desire for unique vehicle appearances, driving demand for aftermarket bumper kits,s including lip spoilers, rs diffusers, and body colored replacements. This trend is particularly prominent among younger demographics and owners of popular models, such as trucks and sport utility vehicles. Manufacturers and retailers can leverage this demand by offering a wide variety of designs, materials, and finishes, including carbon fiber look-alikes and matte coatings. The availability of online marketplaces and installation services further facilitates access to these products, making customization more accessible to the average consumer. Additionally, the rise ofdo-it-yourselff culture encourages the purchase of bolt-on bumper accessories that require minimal professional intervention.

MARKET CHALLENGES

Balancing Aesthetic Design with Structural Integrity Requirements

Achieving the optimal balance between sleek aesthetic designs and robust structural integrity poses a major challenge for the growth of the automotive bumpers market. Consumers and automakers demand visually appealing bumpers with smooth lines and seamless integration into the vehicle body, yet these components must withstand rigorous crash tests and environmental stresses. According to the Insurance Institute for Highway Safety, low-speed crash tests evaluate bumper performance at speeds of 2.5 miles per hour and 5 miles per hour, requiring them to protect vital components without excessive deformation. Meeting these structural requirements often necessitates thicker reinforcement beams and denser foam absorbers, which can conflict with design goals for slim and aerodynamic profiles. Engineers must employ sophisticated simulation tools and iterative prototyping to resolve these conflicts,s increasing development time and costs. The use of mixed materials, such as combining plastic fascias with metal or composite reinforcements, ts adds complexity to the manufacturing process, ess requiring advanced joining techniques like adhesive bonding or laser welding. Ensuring consistent quality across high-volume production runs, while maintaining tight tolerances for sensor alignment, further complicates operations. Any compromise in structural integrity can lead to safety failures and reputational damage, while overly bulky designs may deter buyers. Thus, manufacturers face the continuous challenge of innovating materials and processes to deliver bumpers that satisfy both the visual expectations of designers and the rigorous safety standards of regulators without escalating production costs excessively.

Managing End-of-Life Recycling and Sustainability Compliance

The automotive industry faces mounting pressure to address the environmental impact of vehicle components, including bumpers, which are predominantly made from mixed plastics and composites. The management of end-of-life recycling and sustainability compliance is also a challenge for the growth of the automotive bumpers market. According to the European Automobile Manufacturers Association, the automotive sector aims to achieve a 95% reuse and recycling rate for end-of-life vehicles by 2025, requiring efficient processing of all parts, including bumpers. Traditional mechanical recycling methods often struggle with multi-material bumper systems, leading to downcycling,g where materials are used for lower-value applications. Regulatory bodies are increasingly mandating the use of recycled content in new vehicles, which forces manufacturers to develop closed-loop recycling systems. However, the presence of additives in paints and coatings in bumper fascias can contaminate recycled streams, reducing quality and usability. Developing chemical recycling technologies or design for disassembly principles requires substantial investment and collaboration across the supply chain. Additionally, the lack of standardized labeling for plastic types complicates sorting processes at recycling facilities. Manufacturers must navigate these regulatory and technical hurdles to ensure compliance with circular economy goals.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Positioning, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Market Leaders Profiled | Plastic Omnium SE, Magna International Inc., Flex-N-Gate Corporation, Toyoda Gosei Co., Ltd., Hyundai Mobis Co., Ltd., Samvardhana Motherson International Limited (SMR), Faurecia SE (FORVIA), Tong Yang Group, Montaplast GmbH, Gestamp Automoción S.A., Valeo SA, Yanfeng Automotive Interiors Co., Ltd. |

SEGMENTAL ANALYSIS

By Materials Insights

The composite plastic materials segment accounted for 32.1% of the automotive bumpers market share in 2025 due to their superior weight reduction capabilities, design flexibility,y and cost effectiveness in mass production. Thermoplastics, such as polypropylene, polycarbonate, and acrylonitrile butadiene styrene,ne are extensively used for bumper fascias because they can be molded into complex aerodynamic shapes, while providing adequate impact resistance. According to the Society of Plastics Engineers, plastic components can reduce vehicle weight by up to 50% compared to traditional steel parts, which directly contributes to improved fuel efficiency and lower emissions. Additionally, composite plastics offer excellent corrosion resistance and durability against minor impacts,cts reducing maintenance costs for consumers. The ability to integrate color and texture during the molding process eliminates the need for painting in some applications, further reducing manufacturing costs and environmental impact. The widespread adoption of injection molding technologies allows for high-volume production with consistent quality, ensuring that composite plastics remain the material of choice for original equipment manufacturers seeking to balance performance, aesthetics, and economic efficiency in modern vehicle designs.

Thefiber-reinforcedd composites segment is projected to expand at a CAGR of 7.2% during the forecast period owing to the increasing demand for ultra-lightweight materials in high-performance vehicles and electric cars, where every kilogram saved extends driving range. The use of carbon fiber in automotive applications has increased significantly due to its exceptional strength-to-weight ratio, which is five times stronger than steel. Electric vehicle manufacturers are particularly inclined towards fiber composites to offset the heavy weight of battery packs, thereby maintaining vehicle efficiency and handling characteristics. Advances in manufacturing processes, such as resin transfer molding, have reduced production times and costs,s making fiber composites more accessible for mainstream vehicles. Furthermore, these materials offer superior energy absorption properties, es enhancing pedestrian safety and crashworthiness. As production scales up and recycling technologies for carbon fiber improve, the economic viability of these materials increases,ses positioning them as a key growth area for suppliers aiming to meet the rigorous demands of next-generation mobility solutions.

By Positioning Insights

The front-end bumper segment was the largest, holding 36.2% of the automotive bumper market share in 2025 due to its role in housing advanced driver assistance system sensors and protecting vital engine components. The front bumper assembly integrates radar, lidar cameras, and ultrasonic sensors essential for features like adaptive cruise control, automatic emergency braking, and lane-keeping assist. Additionally, the front end bears the brunt of most low-speed collisions and pedestrian impacts, necessitating robust engineering and frequent design updates to meet stringent safety regulations, such as those mandated by the European New Car Assessment Program. The aesthetic importance of the front fascia in defining brand identity also drives innovation and replacement cycles. The complexity of integrating cooling systems for engines or batteries within the front bumper structure further adds to its significance.

The rear-end bumpers segment is likely to witness the fastest CAGR of 12.6% from 2026 to 2034, with the increasing prevalence of rear-view cameras, parking sensors, and the rising incidence of rear-end collisions. As vehicles become equipped with more sophisticated parking assistance systems, the rear bumper has evolved from a simple protective bar to a complex module housing multiple sensors and cameras. This regulatory push has standardized the inclusion of sensor-ready rear bumpers across various vehicle segments. Furthermore, the rise of ride-sharing services and delivery vehicles has increased urban driving scenarios where rear-end bumps are common, leading to higher demand for durable and easily replaceable rear bumper units. The trend towards sleeker vehicle designs with integrated exhaust tips and diffusers also requires precise engineering of rear-end assemblies. Electric vehicles often feature unique rear-end designs to accommodate different aerodynamic profiles and charging port locations.

By End Market Insights

The Original Equipment Manufacturer segment accounted for 34.5% of the automotive bumpers market share in 2025 due to the continuous production of new vehicles globally and the strict requirement for integrated safety and aesthetic standards. Every new vehicle produced requires a complete set of bumpers that are precisely engineered to match the specific model’s design language and safety protocols. According to the International Organization of Motor Vehicle Manufacturers, approximately 89 million motor vehicles were produced worldwide in 2023, creating a massive inherent demand for OEM bumper systems. OEMs prioritize quality consistency and supply chain reliability, which favors established bumper manufacturers with strong technical capabilities and long-term contracts. The integration of advanced materials and sensors during the initial assembly process is more efficient and cost-effective than retrofitting them later. Additionally, warranty considerations and brand reputation compel automakers to use high-quality OEM parts that undergo rigorous testing and validation. The shift towards modular assembly lines allows for just-in-time delivery of bumper systems, reducing inventory costs for manufacturers.

The aftermarket segment is deemed to grow at the fastest CAGR of 10.2% during the forecast period, with the aging vehicle population increasing accident rates and the rising trend of vehicle customization. As vehicles remain on the road for longer periods, the likelihood of bumper damage from minor collisions,s wear and tear, ar or aesthetic upgrades increases significantly. The availability of affordable and diverse bumper options, including painted, unpainted,nted and textured finishes, allows car owners to choose replacements that suit their budget and style preferences. Insurance claims for minor damages often lead to aftermarket part replacements due to lower costs compared to OEM equivalents. Furthermore, the rise of online retail platforms has made it easier for consumers and independent repair shops to buy high-quality aftermarket bumpers quickly. The growing interest in off-roading and personalization also drives demand for specialized rugged or sporty bumper designs.

COUNTRY LEVEL ANALYSIS

North America Bumpers Market Analysis

North America was the top performer in the global automotive bumpers market by holding 34.6% of the share in 2025, with high vehicle ownership rates and a strong culture of vehicle customization. The region benefits from a well-established automotive manufacturing base in the United States, Canada, and Mexico, which supports robust demand for both OEM and aftermarket bumper solutions. The United States auto industry supports millions of jobs and contributes significantly to the national economy, driving continuous investment in vehicle production and component sourcing. The prevalence of light trucks and sport utility vehicles, which require larger and more durable bumpers, further boosts the market’s growth. Strict safety regulations enforced by the National Highway Traffic Safety Administration mandate high-performance standards for bumper systems, encouraging innovation in materials and design. Additionally, the extensive network of independent repair shops and insurance providers facilitates a vibrant aftermarket sector, where consumers frequently replace damaged bumpers. The trend towards electric vehicles led by major domestic manufacturers is also influencing bumper design requirements,s focusing on lightweighting and aerodynamics.

Europe Bumpers Market Analysis

Europe automotive bumpers market was ranked second, holding 24.7% of the share in 2025, with stringent environmental regulations and a strong emphasis on pedestrian safety. The European Union’s Green Deal and emission reduction targets compel automakers to adopt lightweight materials such as composite plastics and fiber-reinforced composites in bumper construction to improve vehicle efficiency. The presence of major luxury and premium car manufacturers in countries like Germany, Italy, and France drives demand for high-quality, aesthetically pleasing bumper systems. Additionally, the well-developed recycling infrastructure in Europe supports the use of recycled materials in bumper production, aligning with circular economy goals.

Asia Pacific Bumpers Market Analysis

The Asia Pacific automotive bumpers market is significantly growing at the fastest CAGR in the coming years, with the rapid industrialization increasing vehicle production and rising disposable incomes in countries like China, India, and Japan. The expanding middle class in emerging economies is driving demand for passenger cars and sport utility vehicles, which require robust and stylish bumper systems. Government initiatives to improve road infrastructure and safety standards are also influencing bumper design and quality requirements. China, as the world’s largest automobile market,t plays a pivotal role in setting trends for lightweight and smart bumper solutions integrated with advanced driver assistance systems. The presence of major global and local automotive manufacturers ensures a steady demand for OEM bumpers, while the growing vehicle parc supports a burgeoning aftermarket sector. Additionally, the region’s focus on electric vehicle adoption is accelerating the need for specialized bumper designs that enhance aerodynamics and protect battery systems.

Latin America Bumpers Market Analysis

America's automotive bumpers market growth is driven by the automotive industry and increasing vehicle penetration in countries such as Brazil, Mexico, and Argentina. The region benefits from trade agreements and foreign investments that have established it as a manufacturing hub for several global automakers. The demand for durable and cost-effectivebumper systems is high due to varying road conditions and the popularity of utility vehicles and pickup trucks. Local manufacturers are increasingly adopting international safety and quality standards to compete in both domestic and export markets. The aftermarket sector is also expanding as vehicle ownership rises and consumers seek affordable repair solutions. Government efforts to improve road safety and reduce traffic fatalities are prompting stricter regulations on vehicle components, including bumpers.

The Middle East and Africa

The Middle East and Africa automotive bumpers market growth is driven by infrastructure development and a preference for robust vehicles capable of handling harsh terrain. Countries in the Gulf Cooperation Council, such as Saudi Arabia and the United Arab Emirates,s have high per capita income levels and a strong demand for luxury and sport utility vehicles, which require premium bumper systems. The infrastructure investments in Africa are improving connectivity and stimulating economic activity, which indirectly supports the automotive sector. The extreme climate conditions in the Middle East necessitate bumpers made from materials that resist heat degradation and radiation,nn driving demand for high-quality composites. Local assembly plants in countries like South Africa and Egypt are contributing to the OEM segment by producing vehicles tailored to regional needs.

COMPETITIVE LANDSCAPE

The competition in the automotive bumpers market is intense and characterized by the presence of large multinational corporations and specialized regional suppliers, who compete on technology quality and cost efficiency. Major players leverage their extensive research and development capabilities to innovate in materials science, creating lighter and stronger bumper systems that meet rigorous safety standards. Price competition remains significant, particularly in the aftermarket segment, where consumers seek affordable replacement options. However, differentiation through superior design aesthetics and technological integration helps premium suppliers maintain higher margins. The shift towards electric vehicles has intensified competition as manufacturers race to develop specialized bumper solutions that optimize airflow and protect battery systems. Regulatory compliance across different regions adds complexity,y requiring companies to maintain flexible production lines and diverse product portfolios.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Automotive Bumpers Market include

- Plastic Omnium SE

- Magna International Inc.

- Flex-N-Gate Corporation

- Toyoda Gosei Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Samvardhana Motherson International Limited (SMR)

- Faurecia SE (FORVIA)

- Tong Yang Group

- Montaplast GmbH

- Gestamp Automoción S.A.

- Valeo SA

- Yanfeng Automotive Interiors Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Magna International Inc stands as a global leader in automotive technology with a strong presence in the bumper systems sector through its exterior systems division. The company designs and manufactures innovative front and rear bumper assemblies that integrate advanced materials and sensor technologies for modern vehicles. Magna strengthens its market position by investing heavily in research and development to create lightweight composite solutions that enhance fuel efficiency and safety. Recent actions include expanding its production capabilities in key regions such as North America and Europe to support major automakers. The company also focuses on sustainability by incorporating recycled materials into its bumper products. Magna’s collaborative approach with original equipment manufacturers ensures that its designs meet stringent regulatory standards while offering aesthetic appeal.

- Flex Ltd is a prominent player in the automotive bumpers market known for its manufacturing excellence and supply chain integration capabilities. The company provides comprehensive bumper solutions ranging from design engineering to large-scale production using advanced thermoplastic and composite materials. Flex strengthens its position by adopting digital manufacturing technologies that improve precision and reduce waste in bumper production. Recent initiatives include partnering with automotive OEMs to develop smart bumper systems equipped with integrated sensors for advanced driver assistance features. The company has also expanded its facilities in Asia and Europe to cater to growing regional demand and ensure timely delivery. Flex emphasizes sustainability by implementing circular economy practices in its manufacturing processes, including the use of bio-based plastics. Its ability to offer end-to-end services from concept to completion allows Flex to maintain strong relationships with global automakers.

- Faurecia SE is a key contributor to the automotive bumpers market, specializing in exterior styling and structural components that enhance vehicle safety and aerodynamics. The company offers a wide range of bumper systems made from lightweight materials, such as polypropylene and carbon fiber composites. Faurecia strengthens its position through strategic acquisitions and partnerships that expand its technological capabilities and geographic reach. The company also focuses on integrating active aerodynamic features into bumper assemblies to reduce drag and improve energy efficiency. Faurecia collaborates closely with automakers to co-develop innovative solutions that meet strict pedestrian safety regulations.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the automotive bumpers market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation is a primary strategy where companies invest in developing lightweight materials such as carbonfiber-reinforcedd polymers and advanced thermoplastics to meet fuel efficiency standards. Strategic partnerships with original equipment manufacturers allow firms to co-develop customized bumper solutions that integrate advanced driver assistance system sensors seamlessly. Geographic expansion is another critical approach enabling companies to establish production facilities in emerging markets like Asia Pacific to reduce logistics costs and serve local demand efficiently. Sustainability initiatives are increasingly important as manufacturers adopt recycled materials and eco-friendly production processes to comply with environmental regulations. Digital transformation through the use of artificial intelligence and automation in manufacturing enhances precision and reduces waste. Additionally, companies focus on strengthening their aftermarket presence by offering durable and customizable bumper options to cater to the growing segment of vehicle owners seeking repairs and upgrades.

MARKET SEGMENTATION

This research report on the global automotive bumpers market is segmented and sub-segmented into the following categories.

By Material

- Composite Plastic Materials

- Fiber-Reinforced Composites

By Positioning

- Front End Bumpers

- Rear End Bumpers

By End Market

- Original Equipment Manufacturer (OEM)

- Aftermarket

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is driving growth in this market?

Growth is driven by higher vehicle output, tougher safety and pedestrian-protection rules, demand for lightweighting to improve fuel efficiency and EV range, and continued material innovation

2. Which material type leads the market?

Fiber and composite-based bumpers (plastics, composites, and fiber-reinforced systems) hold a large share due to their light weight, design flexibility, and cost-effectiveness.

3. Which vehicle segment is most important?

Passenger cars are a major segment, while commercial vehicles also contribute significantly, especially in regions with strong truck and bus production.

4. Which position segment leads?

Front-end bumpers are typically the larger segment, given higher design, safety, and cooling-system integration requirements.

5. Which region leads the market?

Asia Pacific is the largest regional market, supported by high vehicle production in China, India, Japan, and South Korea

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com