Global Automotive Aftermarket Market Size, Share, Trends and Growth Forecast Report, Segmented By Replacement Type (Battery, Tyre, Filters, Brake Parts, Turbochargers, Body Parts, Wheels, and Others); Service Channel (DIFM, DIY, and OE); Distribution Channel (Wholesalers & Distributors and Retailers); Certification (Certified Parts, Genuine Parts, and Uncertified Parts) and Region (North America, Europe, Aisa-Pacific, Latin America, Middle East And Africa), Industry Analysis (2026 to 2034)

Market Size, 2025

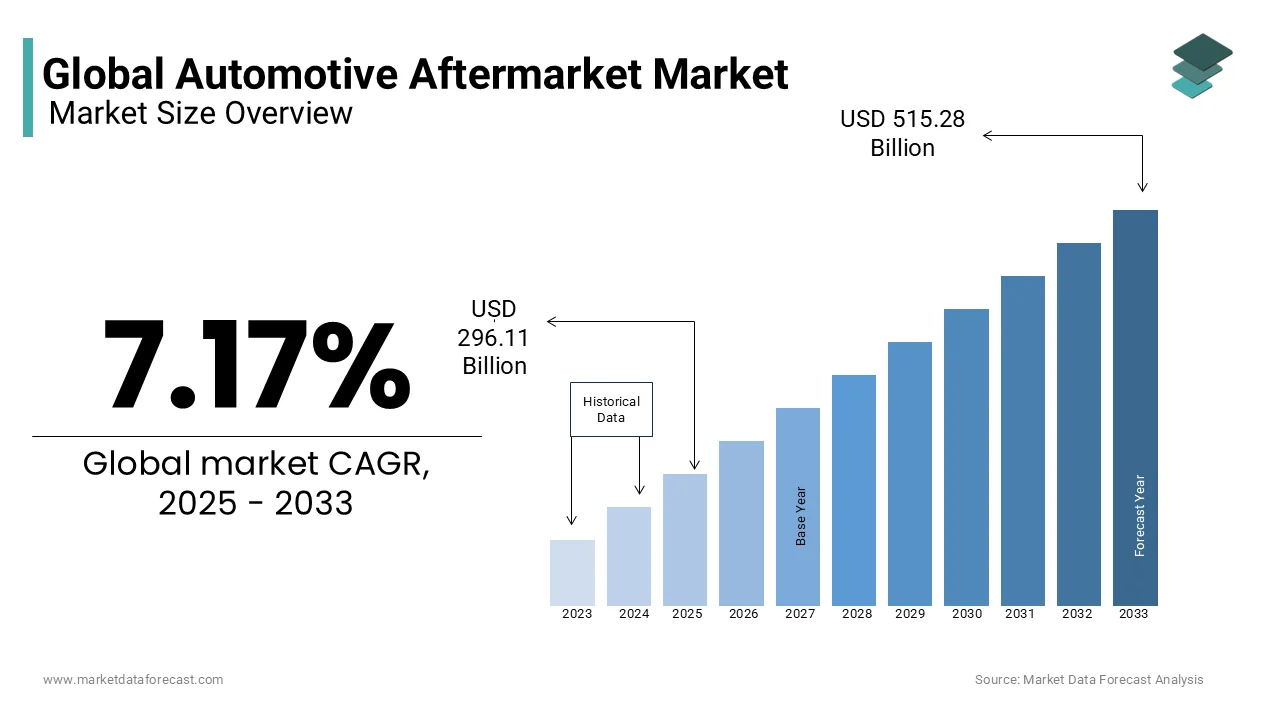

$296.11 BnMarket Estimate, 2026

$317.34 BnMarket Forecast, 2034

$552.22 BnCAGR, 2026–2034

7.17%Global Automotive Aftermarket Market Summary

The global automotive aftermarket market was valued at USD 296.11 billion in 2025, and is projected to reach USD 317.34 billion in 2026, from USD 552.22 billion by 2034, growing at a CAGR of 7.17% from 2026 to 2034. The growth of the global automotive aftermarket market is driven by rising vehicle ownership, increasing average vehicle age, and growing consumer demand for vehicle customization and maintenance services. Technological advancements in distribution channels and the rising availability of uncertified but cost-effective parts are further fueling market expansion.

Key Market Trends

- Growing demand for brake parts due to increased focus on road safety and replacement cycles.

- Rising penetration of online platforms and e-commerce in aftermarket part distribution.

- Expansion of the uncertified parts segment offers cost advantages to consumers.

- Increasing adoption of data-driven predictive maintenance solutions.

- Strategic focus on sustainability and eco-friendly aftermarket products.

Segmental Insights

- Based on replacement, the brake parts segment held a prominent share in 2024, supported by consistent replacement needs and safety regulations.

- Based on distribution channel, the wholesalers and distributors segment dominated the market in 2024, reflecting their strong presence in global supply chains.

- Based on service channel, the OE (original equipment) and IAM (independent aftermarket) networks play a significant role, with IAM channels expanding rapidly.

- Based on certification, the uncertified parts segment led the market with 52.3% share in 2024, reflecting consumer price sensitivity and demand for affordable alternatives.

Regional Insights

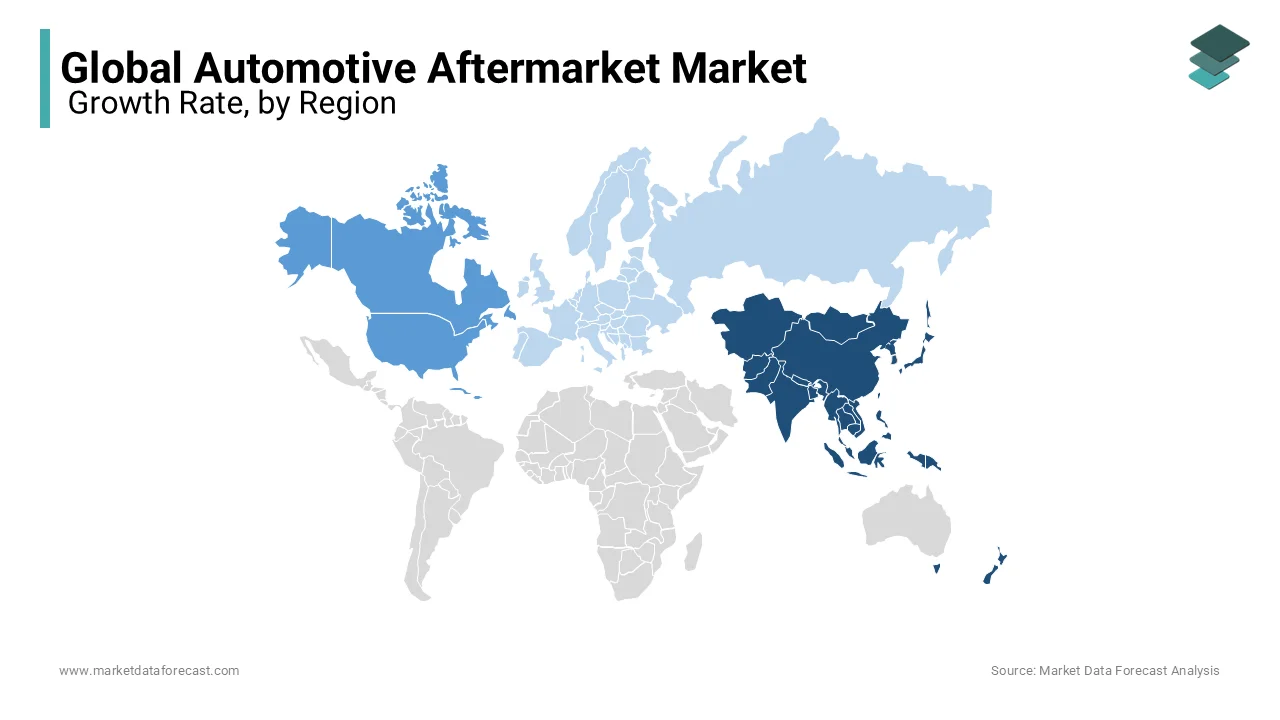

- North America was the largest contributor to the global automotive aftermarket market in 2024, accounting for a 32.3% share, supported by a mature vehicle fleet, high vehicle ownership rates, and robust aftermarket service infrastructure.

- Europe shows steady growth, driven by strong OEM presence and stringent vehicle safety regulations.

- Asia-Pacific is projected to grow at the fastest CAGR, fueled by rapid vehicle sales, expanding middle-class demand, and strong aftermarket networks in China and India.

- Latin America and the Middle East & Africa are emerging markets, supported by growing vehicle parc and rising investments in aftermarket service networks.

Competitive Landscape

Major players in the global automotive aftermarket market include Continental AG (Germany), ZF Friedrichshafen AG (Germany), HELLA KGaA Hueck & Co. (Germany), Denso Corp. (Japan), Marelli (Japan), 3M (US), Goodyear (US), DRiV Inc. (US), Federal-Mogul Corp. (US), Cooper Tire (US), Delphi Tech (UK), and Valeo Group (France). These companies are focusing on supply chain digitalization, e-commerce expansion, and product innovation to strengthen their global aftermarket presence.

Global Automotive Aftermarket Market Size

The global automotive aftermarket market was valued at USD 296.11 billion in 2025 and is anticipated to reach a valuation of USD 317.34 billion by 2026 from USD 552.22 billion by 2034, growing at a CAGR of 7.17% during the forecast period from 2026 to 2034.

The Automotive Aftermarket includes replacement parts such as brakes, filters, batteries, lighting, and performance-enhancing accessories, alongside maintenance and repair services to vehicle longevity and performance. As global vehicle parc expands and average vehicle age rises, the aftermarket sector gains momentum, driven by consumer demand for cost-effective maintenance solutions and customization. In 2023, the average age of light vehicles on U.S. roads reached 12.6 years, as reported by S&P Global Mobility, reflecting a growing need for replacement parts and repair services. Furthermore, as per the Motor & Equipment Manufacturers Association (MEMA), over 80% of vehicles on American roads are older than five years, reinforcing reliance on aftermarket components. The complexity of modern vehicles, particularly with advanced driver-assistance systems (ADAS) and electrified powertrains, is reshaping service requirements and creating new demand for specialized diagnostic tools and technician training. Regulatory frameworks, such as right-to-repair legislation gaining traction in the European Union and the United States, are also influencing market dynamics by enhancing consumer and independent service provider access to vehicle data and software.

MARKET DRIVERS

Rising Average Vehicle Age and Extended Ownership Periods

The increasing average age of vehicles on the road is escalating the growth of the Automotive Aftermarket Market. Consumers are retaining their vehicles longer due to economic pressures, improved vehicle durability, and rising new car prices. According to S&P Global Mobility, the average age of light vehicles in operation in the United States climbed to 12.6 years in 2023, up from 9.5 years in 2002, indicating a structural shift toward prolonged vehicle usage. This trend directly amplifies the need for replacement parts and maintenance services, as older vehicles require more frequent repairs and component upgrades. In Europe, the average vehicle age stands at approximately 11.8 years, as noted by the European Automobile Manufacturers’ Association (ACEA), further validating the global nature of this phenomenon.

Expansion of Vehicle Parc and Emerging Market Mobility Growth

The global increase in the number of vehicles in operation is another factor prompting the growth of the Automotive Aftermarket Market. As per the International Organization of Motor Vehicle Manufacturers (OICA), over 1.4 billion motor vehicles were in use worldwide in 2022, with Asia-Pacific accounting for nearly 40% of this total. Countries like India and Indonesia are witnessing rapid growth in personal vehicle ownership due to urbanization, rising disposable incomes, and expanding middle-class populations. India alone added over 3.5 million new passenger vehicles in 2023, as reported by the Society of Indian Automobile Manufacturers (SIAM), significantly contributing to the long-term aftermarket base. Moreover, informal repair networks and localized part manufacturing in countries such as Thailand and Vietnam support accessibility and affordability, reinforcing aftermarket penetration. The proliferation of two-wheelers, with over 240 million registered in India as of 2023, according to the Ministry of Road Transport and Highways, further diversifies the aftermarket landscape, requiring a broad spectrum of service offerings.

MARKET RESTRAINTS

Proliferation of Counterfeit and Substandard Aftermarket Parts

The widespread availability of counterfeit and low-quality automotive parts poses a significant impediment to the integrity and growth of the Automotive Aftermarket Market. These non-OEM, often unregulated components flood the market in developing regions, undercutting legitimate manufacturers and compromising vehicle safety and performance. According to the International Chamber of Commerce (ICC), the global value of counterfeit automotive parts reached an estimated $12.3 billion in 2022, with brake pads, filters, and lighting units among the most commonly faked products. In India, the Automotive Component Manufacturers Association (ACMA) estimates that up to 30% of parts sold in the informal sector are counterfeit, leading to increased warranty claims, reduced brand trust, and potential liability for repair shops. Substandard parts often fail to meet safety or durability standards, resulting in premature failures and, in extreme cases, accidents. The U.S. Department of Transportation has linked faulty aftermarket brake components to over 1,200 vehicle recalls between 2018 and 2022. Furthermore, the lack of traceability and certification in gray-market supply chains complicates regulatory enforcement and consumer protection. While initiatives such as blockchain-based part authentication are emerging, their adoption remains limited.

Increasing Complexity of Vehicle Electronics and Software Dependencies

Modern vehicles are increasingly reliant on integrated electronic systems, and proprietary software is creating barriers for independent repair shops and aftermarket suppliers, which is hampering the growth of the Automotive Aftermarket Market. As per the European Association of Automotive Suppliers (CLEPA), over 40% of a vehicle’s value now lies in its electronic and software components, including engine control units, ADAS, and telematics systems. This technological shift limits the ability of third-party service providers to diagnose and repair vehicles without access to manufacturer-specific diagnostic tools, calibration software, and firmware updates. According to the Auto Care Association in the US, 70% of independent repair facilities report difficulties in accessing necessary repair information, directly affecting service turnaround and customer retention. This trend undermines the traditional aftermarket model, where third-party parts and services competed on price and availability.

MARKET OPPORTUNITIES

Integration of Digital Platforms and E-Commerce Expansion

The digitization of the automotive aftermarket is anticipated to have a significant growth opportunity for the Automotive Aftermarket Market. Consumers and repair shops are increasingly adopting online channels for part procurement, driven by convenience, price transparency, and expanded product availability. As per Statista, global online sales of automotive parts reached $185 billion in 2023, with an annual growth rate exceeding 12%, significantly outpacing traditional retail channels. In China, platforms like Alibaba’s Tmall Auto and JD.com have captured over 35% of the replacement parts market, leveraging big data to predict demand and optimize logistics. Similarly, in India, companies such as Bosch’s eAxle and Pitstop have reported a 60% year-on-year increase in online orders, as noted by the Confederation of Indian Industry (CII). Digital integration also enables advanced services such as virtual vehicle health assessments, where AI analyzes telematics data to recommend specific part replacements before failure occurs. Moreover, blockchain technology is being piloted to authenticate parts and ensure supply chain transparency, addressing long-standing concerns about counterfeit goods.

Growth of Electric Vehicle (EV) Aftermarket Services

While EVs have fewer moving parts than internal combustion engine (ICE) vehicles, they introduce new maintenance demands related to battery systems, power electronics, and thermal management. Battery degradation, a key concern, necessitates testing, reconditioning, and eventual replacement, with the average lithium-ion battery requiring service after 8 to 10 years, as noted by the U.S. Department of Energy. The global market for EV battery repurposing and recycling is expected to exceed $12 billion annually by 2030, according to the International Energy Agency (IEA). Additionally, components such as onboard chargers, DC-DC converters, and regenerative braking systems are becoming focal points for aftermarket innovation.

MARKET CHALLENGES

Regulatory Fragmentation and Compliance Pressures

The automotive aftermarket operates within a complex and fragmented regulatory environment that varies significantly across regions, creating operational hurdles for manufacturers and distributors. Emission standards, safety certifications, and part homologation requirements differ between jurisdictions, necessitating customized product designs and extensive testing. In the European Union, Regulation (EU) 2017/1151 mandates that replacement parts for safety systems must undergo rigorous conformity assessments, increasing time-to-market and development costs. Additionally, environmental regulations such as the EU’s End-of-Life Vehicles Directive impose recycling obligations on producers, affecting packaging, material selection, and reverse logistics. The absence of global harmonization forces companies to maintain multiple product variants, inflating operational complexity. In emerging markets, inconsistent enforcement and a lack of standardized testing facilities further distort competition, enabling substandard products to proliferate. As governments intensify scrutiny on vehicle safety and sustainability, the regulatory burden is expected to grow, particularly with the integration of software-defined vehicles and cybersecurity mandates.

Skilled Labor Shortage in Automotive Repair and Diagnostics

The growing deficit of qualified technicians capable of servicing modern vehicles for those with advanced electronics and hybrid systems is also impeding the growth of the Automotive Aftermarket Market. As vehicle technology evolves, the knowledge required for effective diagnosis and repair has shifted from mechanical expertise to digital proficiency, creating a skills gap that undermines service capacity. According to the U.S. Bureau of Labor Statistics, the automotive repair and maintenance sector faces a shortage of over 80,000 technicians nationwide, with projections indicating a 5% annual shortfall in new entrants relative to retirements. In the United Kingdom, the Institute of the Motor Industry (IMI) reports that 47% of garages struggle to hire technicians trained in hybrid and electric vehicle systems, despite increasing demand. The situation is exacerbated by declining vocational enrollment; Germany’s Federal Institute for Vocational Education and Training notes a 15% drop in automotive apprenticeship registrations between 2018 and 2023. Training programs often lag behind technological advancements, leaving technicians unprepared for tasks such as ADAS calibration, high-voltage system handling, and software updates. Independent repair shops, which constitute over 70% of service outlets in countries like Australia and Canada, are disproportionately affected due to limited resources for continuous training. While OEMs and industry consortia are launching certification initiatives, scalability remains a challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.17% |

| Segments Covered | By Replacement, Service, Distribution, Certification, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Continental AG (Germany), ZF Friedrichshafen AG (Germany), HELLA KGaA Hueck & Co. (Germany), Denso Corp (Japan), Marelli (Japan), 3M (US), Goodyear (US), DRiV Inc (US), Federal-Mogul Corp (US), Cooper Tire (US), Delphi Tech (UK), Valeo Group (France), and Others. |

SEGMENTAL ANALYSIS

By Replacement Insights

The brake parts segment accounted for a prominent share of the automotive aftermarket market in 2024, owing to the safety function of braking systems and their inherent wear characteristics, necessitating regular replacement regardless of vehicle age or drivetrain. The primary driver of this segment’s leadership is the mechanical wear associated with friction-based components such as brake pads, rotors, and calipers, which degrade predictably over time. According to SAE International, the average passenger vehicle requires brake pad replacement every 30,000 to 70,000 miles, with urban driving conditions accelerating wear due to frequent stops. In high-density cities like Mumbai and Jakarta, where stop-and-go traffic is prevalent, brake replacement cycles shorten to as little as 25,000 miles, as observed in field studies conducted by Bosch Automotive Service Solutions. Additionally, regulatory mandates in regions such as the European Union require periodic vehicle inspections (e.g., the MOT test in the UK), which include brake performance checks, directly triggering replacement demand.

The turbocharger segment is anticipated to grow with a CAGR of 7.8% from 2025 to 2033 due to the widespread adoption of downsized, turbocharged engines in both internal combustion and hybrid vehicles, aimed at improving fuel efficiency and reducing emissions. As per the International Council on Clean Transportation (ICCT), over 70% of new gasoline-powered vehicles sold in Europe and North America in 2023 were equipped with turbocharged engines, up from 35% in 2015, significantly increasing the installed base of turbo systems requiring future servicing. Turbochargers operate under extreme thermal and mechanical stress, with failure rates rising after 100,000 to 150,000 miles, as documented by Cummins Turbo Technologies in durability assessments.

By Service Channel Insights

The brake parts segment accounted for the largest share and held a dominant share of the global automotive aftermarket market in 2024, with the growing technical complexity of modern vehicles necessitating specialized tools, software, and trained personnel for accurate diagnostics and repairs. As noted by the U.S. Bureau of Labor Statistics, over 45% of vehicle repairs in 2023 required access to proprietary diagnostic systems, rendering DIY approaches impractical for most owners. Independent repair shops, franchise chains, and dealership service centers collectively form the backbone of the DIFM ecosystem, with over 275,000 such facilities operating in the United States alone, according to the National Institute for Automotive Service Excellence (ASE). Another pivotal factor is time scarcity among urban consumers; a McKinsey & Company survey found that 62% of car owners in major metropolitan areas prefer professional servicing due to a lack of time and garage space. Additionally, warranty considerations play a role—many manufacturers recommend or require professional maintenance to uphold warranty validity, particularly for advanced systems like ADAS and hybrid powertrains.

The Do-It-Yourself (DIY) service channel segment is expected to witness a CAGR of 6.3% during the forecast period, owing to the proliferation of digital resources that empower non-professionals to perform vehicle maintenance with confidence. Platforms such as YouTube, Haynes Manuals Online, and manufacturer-hosted service portals now provide step-by-step video tutorials, torque specifications, and fault code interpretations, significantly lowering the technical barrier to entry. According to Google Trends data analyzed by the Auto Care Association, search volume for “how to change a car battery” and “OBD2 scanner usage” increased by 140% between 2019 and 2023, indicating rising consumer interest in self-repair. Another key driver is the availability of affordable, intelligent diagnostic tools; the global OBD2 scanner market exceeded $1.2 billion in 2023, with entry-level devices priced under $30 enabling users to read and clear error codes, as noted by the Consumer Technology Association. Economic motivations also play a crucial role—AAA estimates that DIY oil changes and battery replacements can save consumers up to 50% compared to professional services. In rural and semi-urban areas of countries like Australia and Canada, where service center density is low, DIY practices remain a necessity.

By Distribution Channel Insights

The wholesalers and distributors segment held a prominent share of the automotive aftermarket market in 2024 due to their function as intermediaries between manufacturers and repair facilities, ensuring efficient inventory flow and regional coverage. These entities maintain vast logistics networks capable of delivering parts within 24 to 48 hours across major markets, a capability essential for minimizing vehicle downtime. In emerging economies such as Nigeria and the Philippines, where formal retail infrastructure is limited, wholesalers serve as the primary conduit for parts distribution, often operating mobile delivery units to reach remote workshops. Additionally, digital integration has enhanced their relevance; platforms like Carquest and Euro Car Parts offer online ordering with real-time inventory visibility, blending traditional logistics with modern e-commerce.

The retailers segment is likely to grow with a CAGR of 7.1% from 2025 to 2033, with the integration of e-commerce, urbanization, and changing consumer behavior. This growth is particularly pronounced in online retail, where platforms such as Amazon Automotive, AutoZone.com, and CarParts.com have transformed part procurement into a seamless, home-based experience. According to U.S. Census Bureau data, online sales of automotive parts reached $42.3 billion in 2023, representing 28% of total retail automotive aftermarket sales, up from 15% in 2019. Physical retail is also evolving, with big-box stores like O’Reilly Auto Parts and Advance Auto Parts integrating in-store kiosks that connect to national inventory pools, enabling access to over 1 million SKUs despite limited shelf space. Urban consumers, particularly in megacities like Tokyo and São Paulo, increasingly favor retail due to time constraints and a lack of storage for bulk purchases. Moreover, retailer-led loyalty programs and instant installation services are enhancing customer retention.

By Certification Insights

The uncertified parts segment was the largest by capturing 52.3% of the global automotive aftermarket market share in 2024, owing to the affordability, as uncertified components are typically priced 30% to 50% lower than certified or genuine alternatives by making them accessible to cost-conscious consumers and informal repair networks. In countries like Pakistan and Egypt, where average monthly incomes remain below $500, as reported by the World Bank, the economic imperative to choose lower-cost parts is overwhelming. The U.S. Government Accountability Office (GAO) found in 2022 that 40% of collision repair shops in border states used uncertified body parts due to insurance cost pressures. Additionally, supply chain opacity enables gray-market distribution, where parts bypass formal certification but are functionally adequate for short-term use.

The certified segment is likely to witness an expected CAGR of 8.2% from 2025 to 2033, owing to the rising consumer awareness of part quality and the expansion of formal certification programs such as CAPA (Certified Automotive Parts Association) in North America and K-Mark in South Korea. According to CAPA, the number of certified parts in its database exceeded 120,000 in 2023, with an annual growth of 12%, reflecting increased manufacturer participation. A key driver is insurance industry endorsement, major providers like Allstate and State Farm in the U.S. now prefer certified parts for repairs, citing performance parity with OEM components and lower claim costs, as noted by the Insurance Institute for Highway Safety (IIHS). The IIHS also confirmed through crash testing that CAPA-certified bumpers perform within 5% of OEM equivalents in impact absorption. Regulatory developments are further boosting demand; the EU’s 2023 revision of the End-of-Life Vehicles Directive mandates that replacement parts meet specific environmental and safety benchmarks, effectively incentivizing certification.

REGIONAL ANALYSIS

North America Market Analysis

North America was the largest contributor global automotive aftermarket market with 32.3% of the share in 2024. The U.S. alone operates over 280 million vehicles, the highest in the world, as noted by the Federal Highway Administration, ensuring a vast base for aftermarket activity. The presence of major retailers like AutoZone and O’Reilly, combined with a dense network of independent repair shops, supports robust service delivery. Additionally, federal and state-level right-to-repair laws enhance consumer access to diagnostic data, fostering competition.

Europe Market Analysis

Europe held 28.3% of the share in 2024. The EU’s periodic roadworthiness tests (e.g., Germany’s TÜV and France’s Contrôle Technique) mandate part replacements, directly stimulating aftermarket sales. According to the European Commission, over 60% of vehicle repairs are initiated during inspection cycles. The region’s emphasis on sustainability, as seen in the End-of-Life Vehicles Directive,t further influences part recycling and remanufacturing trends.

Asia-Pacific Market Analysis

Asia-Pacific is likely to grow with the rising vehicle ownership and urbanization. China and India together added over 30 million new vehicles in 2023, as reported by the Society of Indian Automobile Manufacturers (SIAM) and China Association of Automobile Manufacturers (CAAM), rapidly expanding the future maintenance base. In India, two-wheelers account for over 80% of vehicle registrations, creating unique demand for small-engine parts, as noted by the Ministry of Road Transport and Highways. Informal repair networks dominate in countries like Indonesia and Vietnam, but e-commerce platforms are formalizing distribution.

Latin America Market Analysis

Latin America's aftermarket market growth is likely to grow with the economic volatility and a strong preference for cost-effective solutions. According to Brazil’s National Association of Vehicle Manufacturers (ANFAVEA), over 70% of parts sold are uncertified due to affordability constraints. However, the rising vehicle parc exceeding 80 million units in 2023, as reported by OICA, signals long-term potential. Urbanization in cities like Bogotá and Lima is increasing demand for tires and filters due to poor road conditions and air quality. The gradual formalization of repair networks and expansion of retail chains are slowly improving the market structure.

COMPETITIVE LANDSCAPE

The competition in the automotive aftermarket is marked by a dynamic interplay between global OEM-affiliated suppliers, independent manufacturers, and emerging digital disruptors. Established players leverage their engineering heritage, brand trust, and extensive distribution networks to maintain dominance in safety and high-technology components. However, the rise of e-commerce platforms and regional private-label brands intensifies price and service-based competition, especially in cost-sensitive markets. Differentiation increasingly hinges on technical support, training, and digital integration rather than just product availability. The growing complexity of modern vehicles, including electric and connected systems, has elevated the importance of software access, calibration capabilities, and certified service networks by creating new battlegrounds for market influence. Independent service providers and third-party part makers face pressure to match OEM-level quality while navigating intellectual property and data access restrictions.

Key Market Participants

Companies that are playing a promising role in the global automotive aftermarket market include

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- HELLA KGaA Hueck & Co. (Germany)

- Denso Corp (Japan)

- Marelli (Japan)

- 3M (US)

- Goodyear (US)

- DRiV Inc (US)

- Federal-Mogul Corp (US)

- Cooper Tire (US)

- Delphi Tech (UK)

- Valeo Group (France)

Top Players in the Market

- Bosch is a global leader in the automotive aftermarket that is renowned for its innovation in powertrain systems, diagnostics, and service solutions. The company provides a comprehensive portfolio of replacement parts, including starters, alternators, fuel injection components, and braking systems, trusted for their reliability and engineering precision. Bosch supports repair workshops worldwide with advanced diagnostic equipment and technical training through its Bosch Car Service network. Its commitment to quality, combined with a strong distribution footprint and digital service platforms, enables seamless integration into diverse repair ecosystems.

- Denso plays a pivotal role in shaping the modern automotive aftermarket with its expertise in thermal systems, electronics, and engine management components. The company supplies a wide array of high-performance parts, from ignition systems and sensors to radiators and compressors, known for their durability and compatibility across vehicle platforms. Denso’s global service network ensures consistent availability and technical support, making it a preferred choice among professional repairers. The company emphasizes innovation through R&D in electrified components and ADAS-related parts, positioning itself at the forefront of technological transition. Its focus on sustainability and system integration allows it to deliver solutions that meet evolving vehicle complexities, which is reinforcing its influence in both conventional and next-generation vehicle servicing.

- ZF Aftermarket is a dominant force in chassis, transmission, and driveline components, offering trusted solutions under its Sachs, LEMFÖRDER, and TRW brands. The company specializes in suspension systems, clutches, and steering parts, known for their precision engineering and safety performance. ZF supports repair shops with extensive technical documentation, training programs, and diagnostic tools, ensuring proper installation and service longevity. Its integration of original equipment expertise into the aftermarket enables high-quality replacements that meet OEM standards. By expanding its portfolio to include remanufactured transmissions and electric vehicle-compatible components, ZF demonstrates strategic foresight. Its global service infrastructure and emphasis on technician enablement strengthen its position as a key enabler of professional vehicle maintenance across diverse markets.

Top Strategies Used By Key Market Participants

- One major strategy employed by leading players is the expansion of digital service ecosystems, integrating cloud-based diagnostics, e-commerce platforms, and mobile applications to enhance customer engagement and streamline part selection and repair processes. This digital transformation improves accessibility and strengthens brand loyalty among both repairers and end users.

- Another key approach is strategic investment in technician training and certification programs, ensuring that service providers are equipped to handle advanced vehicle technologies, thereby reinforcing brand credibility and service quality.

- Additionally, companies are increasingly adopting vertical integration by combining parts manufacturing with service networks and distribution, which is allowing greater control over product quality, supply chain efficiency, and customer experience, ultimately differentiating their offerings in a competitive landscape.

RECENT MARKET NEWS

- In March 2024, Bosch launched a new digital service portal integrating real-time part availability, vehicle-specific repair guides, and remote diagnostic support for technicians across Europe by enhancing workflow efficiency and reinforcing its support ecosystem.

- In January 2024, Denso expanded its remanufacturing facility in Thailand to include electric vehicle power control units, aiming to strengthen its service capabilities in the Asia-Pacific region and support the growing demand for sustainable repair solutions.

- In February 2024, ZF Aftermarket introduced a unified training platform across its TRW and Sachs brands, offering certified courses on ADAS calibration and electric driveline maintenance to independent workshops in North and South America.

- In May 2024, Advance Auto Parts partnered with a leading AI-driven diagnostic startup to integrate predictive maintenance tools into its retail and commercial sales channels, which is improving customer service accuracy and part recommendation precision.

MARKET SEGMENTATION

This market research report on the global automotive aftermarket market has been segmented and sub-segmented based on replacement, service, distribution channel, certification, and region.

By Replacement Part

- Battery

- Tyre

- Filters

- Brake Parts

- Turbochargers

- Body Parts

- Wheels

By Service Channel

- DIFM

- DIY

- OE

By Distribution Channel

- Wholesalers & Distributors

- Retailers

By Certification

- Certified Parts

- Genuine Parts

- Uncertified Parts

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the automotive aftermarket?

The automotive aftermarket refers to the industry that supplies parts, accessories, and services for vehicles after they leave the factory. It includes everything from replacement components to performance upgrades and maintenance services.

Why is the aftermarket important for vehicle owners?

It offers cost-effective alternatives to dealer-priced parts and enables longer vehicle lifespans through repairs and upgrades. It also supports customization, better performance, and access to service outside manufacturer networks.

What drives demand in the global aftermarket?

Rising vehicle ownership, increasing average vehicle age, and the need for affordable repairs are key drivers. Consumers are also more aware of their right to choose independent service providers and non-OEM parts.

How does the aftermarket differ from the OEM market?

OEM parts are made by the original vehicle manufacturer and often sold through dealerships, while aftermarket parts are made by third-party companies and usually cost less. Aftermarket suppliers offer wider variety and faster availability in many regions.

Are aftermarket parts reliable compared to OEM?

Many aftermarket parts meet or exceed OEM quality, especially from established brands that invest in testing and certifications. However, quality varies, so reputation, compliance standards, and warranties matter when choosing products.

What role do independent repair shops play?

They form the backbone of the aftermarket, offering competitive pricing, faster turnaround, and growing technical expertise. These shops rely on aftermarket parts to keep servicing affordable for everyday drivers.

How is e-commerce changing the aftermarket?

Online platforms now allow consumers to compare prices, read reviews, and have parts delivered quickly, reducing reliance on physical stores. Mobile apps and digital catalogs are also helping mechanics source components more efficiently.

Are electric vehicles affecting the aftermarket?

Yes, EVs have fewer moving parts, which reduces demand for traditional components like exhausts and clutches. However, new opportunities are emerging in battery servicing, charging accessories, and software-related upgrades.

What challenges does the aftermarket face globally?

Counterfeit parts, lack of standardization in some regions, and limited technical data access from automakers remain major hurdles. Independent repairers also face growing complexity due to advanced electronics and software locks.

What’s the future of the global aftermarket?

It will grow through innovation, digital integration, and rising demand in emerging markets. Expect more smart parts, subscription-based diagnostics, and stronger focus on sustainability and remanufactured components.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com