Global Blood Pressure Monitoring Devices Market Size, Share, Trends & Growth Forecast Report By Type (Automated B.P. Monitors, Ambulatory B.P. Monitors, Sphygmomanometers, B.P. Transducers and B.P. instruments accessories) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Blood Pressure Monitoring Devices Market Size

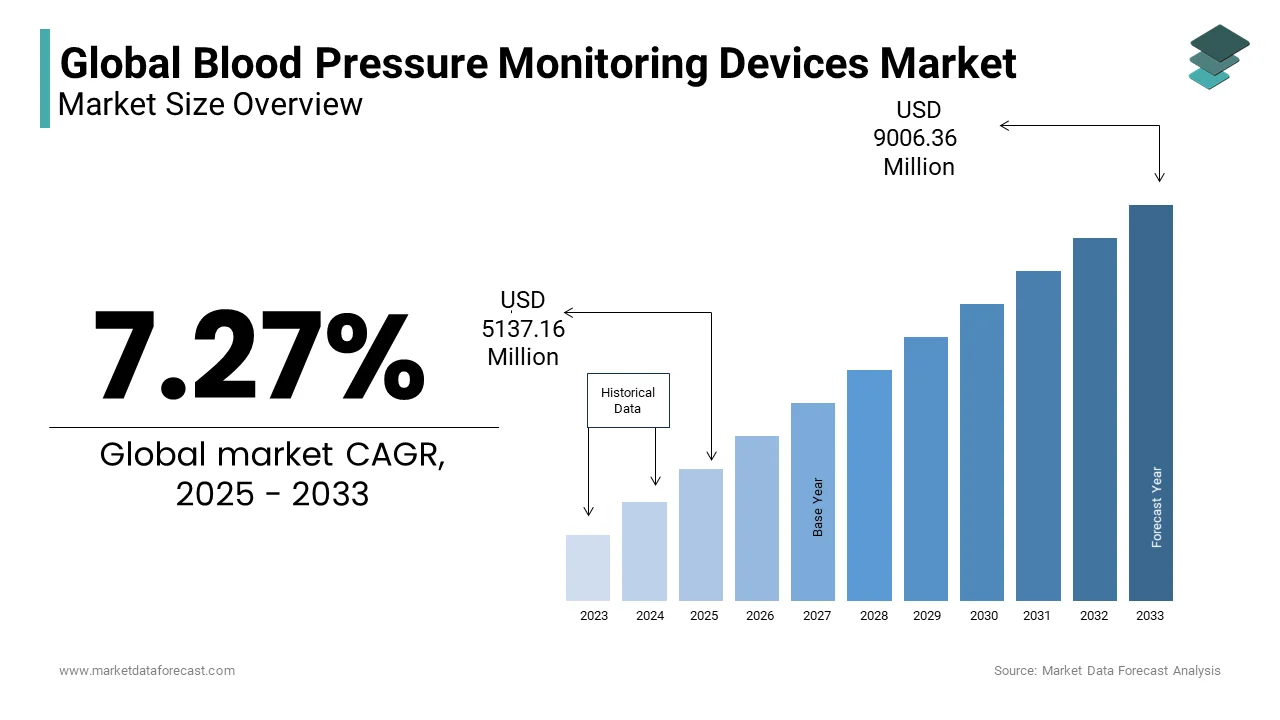

In 2024, the global blood pressure monitoring devices market was valued at USD 4789 million, and it is expected to reach USD 9006.36 million by 2033 from USD 5137.16 million in 2025, growing at a CAGR of 7.27% during the forecast period.

The blood pressure monitoring devices are medical instruments designed to measure systolic and diastolic arterial pressure by serving as tools in the diagnosis, management, and prevention of hypertension and cardiovascular disease. These devices are broadly categorized into upper-arm, wrist, and ambulatory blood pressure monitors, with both manual (aneroid) and digital (oscillometric) variants, the latter increasingly incorporating connectivity features for data tracking and telehealth integration. The clinical significance of consistent blood pressure assessment is underscored by the World Health Organization, which identifies hypertension as the leading risk factor for premature death globally, contributing to nearly 10.8 million fatalities annually.

MARKET DRIVERS

Rising Global Burden of Hypertension and Cardiovascular Diseases

The escalating prevalence of hypertension is a primary driving factor for the growth of the Blood Pressure Monitoring Devices Market. According to the World Health Organization, the number of people living with hypertension has nearly doubled since 1990, reaching 1.3 billion in 2023, with the majority residing in low- and middle-income countries. Cardiovascular diseases, of which hypertension is a principal risk factor, remain the leading cause of death globally, responsible for 17.9 million deaths annually, as reported by the Global Burden of Disease Study 2023. In India, the National Family Health Survey-5 (2022) revealed that 25.6% of adults suffer from high blood pressure, a 7% increase from 2016, prompting the government to integrate BP screening into its Ayushman Bharat Health and Wellness Centers. Similarly, in China, the China Hypertension Survey found that 27.9% of adults are hypertensive, with only 15% achieving controlled levels, underscoring the need for continuous monitoring. The U.S. Centers for Disease Control and Prevention estimates that 47% of American adults have hypertension, driving widespread adoption of home monitoring devices. This chronic condition requires lifelong management, necessitating regular self-measurements to assess treatment efficacy and prevent complications such as stroke and heart failure.

Integration of Digital Health and Remote Patient Monitoring

The integration of digital health technologies with chronic disease management is accelerating the growth of the Blood Pressure Monitoring Devices Market. According to the World Health Organization, over 80 countries have implemented national digital health strategies, many of which include remote monitoring for non-communicable diseases. These devices sync with smartphone applications and electronic health records, allowing clinicians to track patient data in real time and adjust treatment plans remotely. In the United States, the Centers for Medicare & Medicaid Services now reimburses remote physiologic monitoring (RPM) codes, incentivizing providers to adopt telehealth-integrated devices over 4.2 million RPM claims were submitted in 2023, a 65% increase from the previous year, according to CMS. Companies like Omron and Withings have developed FDA-cleared devices that integrate with Apple Health and Google Fit, enhancing patient engagement. Additionally, corporate wellness programs in Japan and South Korea are distributing smart BP monitors to employees, with Toyota and Samsung providing devices to over 150,000 workers annually, as per their corporate sustainability reports.

MARKET RESTRAINTS

Inaccuracy and Misuse of Consumer-Grade Devices

The prevalence of inaccurate readings due to improper device selection, user error, or substandard product quality is hindering the growth of the Blood Pressure Monitoring Devices Market. According to the British and Irish Hypertension Society, only 30% of consumer-grade BP monitors on the global market have undergone independent clinical validation, raising concerns about reliability. In a 2023 evaluation of 120 popular wrist and upper-arm devices, 41% failed to meet the accuracy standards set by the International Organization for Standardization (ISO 81060-2), as reported by the Stride BP initiative. Wrist monitors, in particular, are prone to positional errors measurements taken with the wrist below heart level can overestimate systolic pressure by up to 20 mmHg, according to research published in the Journal of Human Hypertension.

Limited Access and Affordability in Low-Income Regions

The access remains severely constrained in low-income and rural areas due to cost, infrastructure limitations, and supply chain inefficiencies, which is also hampering the growth of the Blood Pressure Monitoring Devices Market. In Malawi, a 2023 assessment by the Ministry of Health found that only 38% of health centers had a working digital sphygmomanometer, with the remainder relying on obsolete mercury devices or manual auscultation. The average cost of a validated upper-arm monitor ($40–$60) exceeds one month’s income for 45% of households in low-income countries, as per the International Poverty Centre. Even when devices are available, maintenance and battery supply pose challenges Ethiopian clinics reported a 33% failure rate of digital monitors due to power fluctuations and lack of replacements, according to the Ethiopian Public Health Institute. Public procurement is often fragmented, with tenders favoring low-cost, non-validated models. In Bangladesh, government tenders in 2023 awarded contracts to suppliers offering monitors at $12 each, well below the cost of clinically accurate devices, as documented by the Directorate General of Health Services. Additionally, training gaps persist only 22% of community health workers in rural Nepal received formal instruction on BP measurement, according to the Nepal Health Research Council.

MARKET OPPORTUNITIES

Expansion of National Hypertension Control Programs

The governments worldwide are launching large-scale hypertension control initiatives is to create new opportunities for the growth of the Blood Pressure Monitoring Devices Market. In India, the National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS) distributed over 120,000 digital BP monitors to rural health centers between 2020 and 2023, as reported by the Ministry of Health and Family Welfare. China’s “Healthy China 2030” plan aims to control hypertension in 70% of diagnosed patients by 2030, requiring widespread deployment of home and clinic-based devices. The Pan American Health Organization supported a regional initiative in 2023 that provided 50,000 monitors to clinics in Honduras, Guatemala, and El Salvador to strengthen chronic disease tracking. These programs often include training for healthcare workers, public awareness campaigns, and linkage to treatment, ensuring sustained device utilization. Additionally, international funding mechanisms such as the Global Fund and World Bank are financing medical equipment procurement in low-resource settings.

Integration with Wearable Technology and Smart Ecosystems

The wearable technology and consumer health platforms is additionally to propel the growth of the Blood Pressure Monitoring Devices Market in the coming years. According to the International Data Corporation, global shipments of smartwatches and fitness trackers reached 208 million in 2023, with health monitoring as the primary driver of consumer adoption. While most wearables currently estimate BP indirectly through pulse wave analysis, emerging technologies are enabling more accurate non-invasive measurement. In 2023, the University of California, San Diego, demonstrated a smartwatch prototype using ultrasound sensors to measure BP continuously, achieving 95% accuracy against clinical standards, as published in Nature Biomedical Engineering. These devices integrate with mobile apps to provide trend analysis, medication reminders, and physician sharing, enhancing patient engagement.

MARKET CHALLENGES

Regulatory Fragmentation and Lack of Harmonized Standards

The inconsistent regulatory requirements and validation standards across countries is to inhibit the growth of the blood pressure monitoring devices market. According to the Global Harmonization Task Force, over 60 different validation protocols are used worldwide to assess device accuracy, creating a fragmented compliance landscape. In the United States, the FDA requires conformance with the AAMI/ESH/ISO 81060-2 standard, while the European Union mandates CE marking under the Medical Device Regulation (MDR), which includes clinical evaluation but allows variations in testing methodologies. In contrast, many low- and middle-income countries lack independent regulatory bodies, enabling the circulation of non-validated devices. Additionally, the rise of AI-driven and wearable devices introduces new regulatory gray areas, with agencies like the FDA still developing frameworks for continuous monitoring algorithms. Manufacturers must navigate overlapping requirements for software, hardware, and data privacy, particularly when devices integrate with telehealth platforms.

Data Privacy and Security Risks in Connected Devices

The increasing connectivity of blood pressure monitoring devices introduces significant data privacy and cybersecurity risks, particularly as sensitive health information is transmitted and stored across digital platforms. According to the U.S. Department of Health and Human Services, healthcare data breaches affected over 133 million individuals in 2023, with medical devices and mobile health apps emerging as vulnerable entry points. Many consumer-grade BP monitors transmit data via unencrypted Bluetooth or store information on third-party cloud servers without robust access controls. A 2023 study by the University of Michigan found that 68% of popular BP apps failed to comply with basic data protection standards by exposing user identities and health records. In the European Union, the General Data Protection Regulation imposes strict requirements on health data processing, with violations carrying fines up to 4% of global revenue, as enforced by national data protection authorities. However, enforcement remains uneven only 12 of 27 EU member states have fully implemented medical device cybersecurity guidelines, according to the European Cybersecurity Agency.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Challenges, Restraints, Opportunities; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Market Players | G.E. Healthcare, Welch Allyn, A&D Medical Inc., SunTech Medical, Rossmax International Ltd, Spacelabs Healthcare Inc., Panasonic Corporation, Philips Healthcare, Contec Medical Systems Co. Ltd, Omron Healthcare, and Microlife AG. |

SEGMENT ANALYSIS

By Type Insights

The automated blood pressure monitors segment held 58.3% of the blood pressure monitoring devices market share in 2024 with its user-centric design, accuracy, and integration into both clinical and home healthcare settings. The primary driver is the escalating global burden of hypertension. The World Health Organization reports that over 1.3 billion people worldwide suffer from hypertension, with nearly half unaware of their condition. This has triggered a surge in self-monitoring, where automated devices offer ease of use without requiring technical expertise. Their adoption is further accelerated by technological advancements such as Bluetooth connectivity, smartphone integration, and data tracking features. A 2022 American Heart Association survey revealed that 72% of hypertensive patients in the U.S. use home-based automated monitors, citing convenience and real-time feedback as key benefits. Additionally, initiatives like the U.S. Centers for Disease Control and Prevention’s Million Hearts 2027 program promote home monitoring to improve control rates, which currently stand at only 25% globally. Reimbursement policies in countries like Germany and Japan covering home monitoring devices have also expanded access.

The ambulatory blood pressure monitoring segment is likely to grow with an expected CAGR of 9.4% from 2025 to 2033. ABPM records blood pressure at regular intervals over 24 hours by capturing nocturnal hypertension, white-coat effects, and masked hypertension with conditions missed in routine checks. Moreover, clinical guidelines in the UK, under the National Institute for Health and Care Excellence (NICE), now mandate ABPM for confirming hypertension diagnoses, which is significantly boosting adoption. In 2023, the UK’s NHS reported a 35% increase in ABPM referrals over two years due to guideline adherence. Technological miniaturization and improved patient comfort have also enhanced compliance.

REGIONAL ANALYSIS

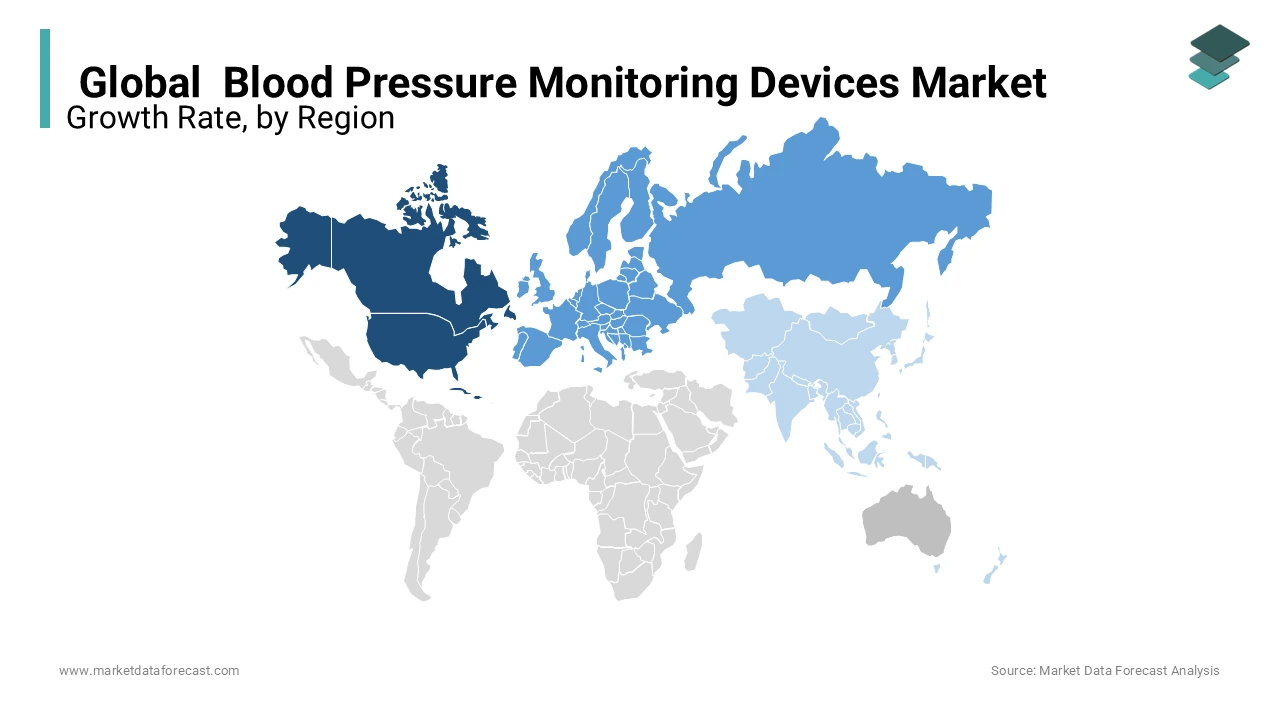

North America Blood Pressure Monitoring Devices Market Insights.

North America was the top performer of the global blood pressure monitoring devices market by holding 38.3% of share in 2024 with the advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and strong regulatory support for preventive care. The United States alone accounts for the bulk of this share, driven by an estimated 116 million adults with hypertension, representing nearly half the adult population, according to the American Heart Association’s 2023 Heart Disease and Stroke Statistics update. The widespread integration of digital health platforms and FDA-cleared smart monitoring devices has accelerated home-based tracking. In 2022, the Centers for Medicare & Medicaid Services expanded reimbursement for remote patient monitoring, covering blood pressure devices, which led to a 40% increase in telehealth-based BP management programs, as reported by the Healthcare Information and Management Systems Society (HIMSS). Furthermore, major players like Omron Healthcare and Welch Allyn are headquartered in the U.S., fostering rapid innovation and commercialization. The presence of large-scale screening initiatives such as the CDC’s State Heart Disease and Stroke Prevention Programs has also enhanced early detection.

Europe Blood Pressure Monitoring Devices Market Insights

Europe blood pressure monitoring devices market was ranked second by holding 29.3% of share in 2024 with the presence of healthcare systems and strong emphasis on evidence-based medicine have positioned it as a hub for clinically integrated blood pressure monitoring. Countries like Germany, the UK, and France lead adoption, supported by national health policies that prioritize cardiovascular risk reduction. The European Society of Cardiology reports that hypertension affects over 150 million adults across Europe, with control rates below 40% in most countries. In Germany, statutory health insurers fully reimburse home blood pressure monitors, resulting in over 60% of hypertensive patients using self-monitoring devices, as noted in a 2022 report by the Robert Koch Institute. Additionally, the EU’s Digital Health Initiative has funded cross-border telemonitoring projects, such as the EU SmartCare program, which demonstrated a 22% improvement in BP control among 10,000 participants across six countries.

Asia-Pacific Blood Pressure Monitoring Devices Market Insights

The Asia Pacific blood pressure monitoring devices market growth is accounted in registering a fastest growth during the forecast period. China and India alone account for over 600 million hypertensive individuals, as reported by The Lancet’s 2021 Global Burden of Disease study, creating massive unmet demand. Urbanization and lifestyle changes have led to a sharp increase in cardiovascular risk factors; in India, hypertension prevalence has nearly doubled in the past two decades, affecting 30% of adults, per the Indian Council of Medical Research. Government initiatives like China’s Healthy China 2030 and India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS) are expanding screening access. In 2023, India distributed over 2 million digital BP monitors through public health centers, as confirmed by the Ministry of Health.

Latin America Blood Pressure Monitoring Devices Market Insights

Latin America blood pressure monitoring devices market is esteemed to grow with the fragmented healthcare systems and low hypertension control rates, yet it is witnessing steady market expansion due to increasing public health awareness and private sector involvement. In Brazil, over 25 million people have hypertension, but only 15% have it under control, as reported by the Brazilian Society of Hypertension in 2023. To address this, the Ministry of Health launched the Hiperdia program, which has enrolled over 8 million patients in structured monitoring since 2002. Private health insurers in Mexico are increasingly covering home monitoring devices, contributing to a 12% annual growth in digital BP monitor sales, per a 2023 analysis by BMI Research. Additionally, telehealth adoption surged post-pandemic, with platforms like Chile’s Telesalud integrating BP tracking for remote consultations.

Middle East and Africa Blood Pressure Monitoring Devices Market Insights

The Middle East and Africa blood pressure monitoring devices market growth is emerging as a strategic growth frontier due to escalating cardiovascular disease rates and evolving healthcare infrastructure. Gulf Cooperation Council (GCC) countries lead adoption, with Saudi Arabia and the UAE investing heavily in preventive health under national visions like Saudi Vision 2030. The World Health Organization estimates that cardiovascular diseases cause 45% of non-communicable disease deaths in the Eastern Mediterranean region, with hypertension prevalence exceeding 35% in adults. In South Africa, the burden is equally severe one in three adults has high blood pressure, as per the South African Heart Association in 2023.

KEY MARKET PLAYERS

Companies leading the global blood pressure monitoring devices market profiled in the report are G.E. Healthcare, Welch Allyn, A&D Medical Inc., SunTech Medical, Rossmax International Ltd, Spacelabs Healthcare Inc., Panasonic Corporation, Philips Healthcare, Contec Medical Systems Co., Omron Healthcare, and Microlife AG.

TOP LEADING PLAYERS IN THE MARKET

Omron Healthcare

Omron Healthcare is a global leader in blood pressure monitoring, renowned for its accuracy and innovation in home healthcare devices. In the Asia Pacific region, Omron has established a strong footprint through localized product development and extensive distribution networks in countries like Japan, India, and China. The company collaborates with healthcare providers and governments to promote hypertension awareness and self-monitoring. In 2023, Omron launched its HeartGuide wearable BP monitor in South Korea and Australia, expanding its digital health portfolio. It also partnered with telehealth platforms in India to integrate its devices with remote monitoring apps. Omron continues to invest in AI-driven analytics and cloud-based data management, enhancing user engagement. Its participation in public health campaigns, such as World Hypertension Day initiatives across Southeast Asia, reinforces its commitment to preventive care.

A&D Medical

A&D Medical has become a key player in the Asia Pacific blood pressure monitoring market by delivering clinically accurate, user-friendly devices tailored to diverse populations. The company has deep roots in Japan and has expanded aggressively into emerging markets like Indonesia, Thailand, and Vietnam. A&D emphasizes regulatory compliance and collaborates with local health authorities to ensure device reliability. In 2022, it introduced upper-arm monitors with irregular heartbeat detection in India, addressing rising cardiovascular concerns. The company also launched Bluetooth-enabled devices compatible with regional telemedicine platforms, enhancing remote patient management. A&D actively participates in hypertension screening programs in rural areas, often in partnership with NGOs. Its focus on affordability without compromising clinical standards has strengthened brand trust. In 2023, A&D collaborated with a major Australian digital health provider to integrate its BP data into electronic medical records.

Beurer GmbH

Beurer is a German-based health technology company, has made significant inroads in the Asia Pacific market by offering premium home healthcare devices with advanced features. Known for its high-quality sphygmomanometers and smart health monitors, Beurer has gained popularity in countries like China, South Korea, and Singapore through e-commerce platforms and retail partnerships. The company emphasizes design, ease of use, and integration with mobile health apps, appealing to tech-savvy consumers. In 2023, Beurer launched its AI-powered blood pressure monitor with arrhythmia detection in Taiwan and Malaysia, enhancing early risk identification. It also strengthened its presence via collaborations with regional distributors and participation in health expos across Southeast Asia. Beurer’s devices are increasingly used in wellness centers and corporate health programs, reflecting its expansion beyond individual consumers.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the blood pressure monitoring devices market are deploying multiple strategies to strengthen their competitive edge. Product innovation remains central, with companies integrating Bluetooth, smartphone apps, and AI-driven analytics to enhance user experience and clinical utility. Firms like Omron and A&D Medical are launching devices with irregular pulse detection and cloud-based data storage to support remote monitoring. Strategic partnerships with telehealth platforms and electronic health record providers enable seamless data integration, improving patient management. Market expansion into emerging economies, particularly in Asia Pacific and Latin America is another approach by localized distribution and affordable product variants. Companies are also engaging in public health initiatives and awareness campaigns to build brand trust and drive adoption. Regulatory approvals and compliance with international standards such as ISO and CE marking are prioritized to ensure global market access.

RECENT MARKET DEVELOPMENTS

- In January 2022, Omron Healthcare launched its wearable blood pressure monitor, HeartGuide, in Japan and Australia, which is combining wristwatch design with medical-grade accuracy to promote continuous monitoring and enhance user engagement in the Asia Pacific region.

- In March 2023, A&D Medical partnered with India’s Apollo Telehealth to integrate its Bluetooth-enabled blood pressure monitors with a national teleconsultation platform by enabling real-time data sharing between patients and physicians across urban and rural areas.

- In September 2023, Beurer GmbH introduced its AI-powered BP monitor with arrhythmia detection in Malaysia and Taiwan, which is strengthening its presence in the premium home healthcare segment and aligning with digital health trends in Southeast Asia.

- In June 2022, GE Healthcare collaborated with the Thai Ministry of Public Health to supply automated blood pressure monitors for nationwide hypertension screening programs by enhancing accessibility and reinforcing its role in public health infrastructure.

- In April 2024, Microlife Corporation expanded its manufacturing facility in Vietnam to increase production capacity for low-cost digital BP monitors, which is aiming to meet rising demand in Southeast Asia and support regional distribution networks.

MARKET SEGMENTATION

This research report on the global blood pressure monitoring devices market has been segmented and sub-segmented based on type and region.

By Type

- Automated B.P. Monitors

- Ambulatory B.P. Monitors

- Sphygmomanometers

- Mercury

- Aneroid

- Digital

- B.P. Transducers

- B.P. instruments accessories

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.Which segment by type dominated the blood pressure monitoring devices market in 2025?

Based on type, the sphygmomanometer segment led the market in 2025.

2.What was the size of the global blood pressure monitoring devices market in 2025?

The global blood pressure monitoring devices market size was worth USD 5137.16 million in 2025

3.Which region led the blood pressure monitoring devices market in 2025?

Geographically, the North American region dominated the market in 2024.

4.What are the key challenges faced by the Blood Pressure Monitoring Devices Market?

Challenges include lack of awareness in developing regions, regulatory hurdles, and competition among market players

5.What end users are targeted in the Blood Pressure Monitoring Devices Market?

Primary end users include hospitals, clinics, home care settings, fitness centers, and research institutions.

6.How do home healthcare solutions influence the Blood Pressure Monitoring Devices Market?

The surge in home care and self-monitoring adoption is boosting market growth, as consumers prefer managing BP at home

7.Why is the Blood Pressure Monitoring Devices Market important in chronic disease management?

BP monitoring devices are essential for managing hypertension and reducing risks of cardiovascular diseases and strokes.

8.What trends are shaping the future of the Blood Pressure Monitoring Devices Market?

Major trends include telehealth integration, wearable BP monitors, increased healthcare spending, and proactive health management

9.Who are the leading companies in the Blood Pressure Monitoring Devices Market?

Omron Healthcare, Philips Healthcare, A&D Medical, Withings, GE Healthcare, and Welch Allyn

10.How is the Blood Pressure Monitoring Devices Market segmented by product type?

Segmentation includes upper arm monitors, wrist monitors, ambulatory BP monitors, digital monitors, and accessories.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com