Global Consumer Healthcare Market Size, Share, Trends & Growth Forecast Report By Product (OTC Pharmaceuticals and Dietary Supplements), Distribution Network (Departmental Stores, Independent Retailers, Pharmacies or Drugstores, Specialist Retailers and Supermarkets or Hypermarkets) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Consumer Healthcare Market Summary

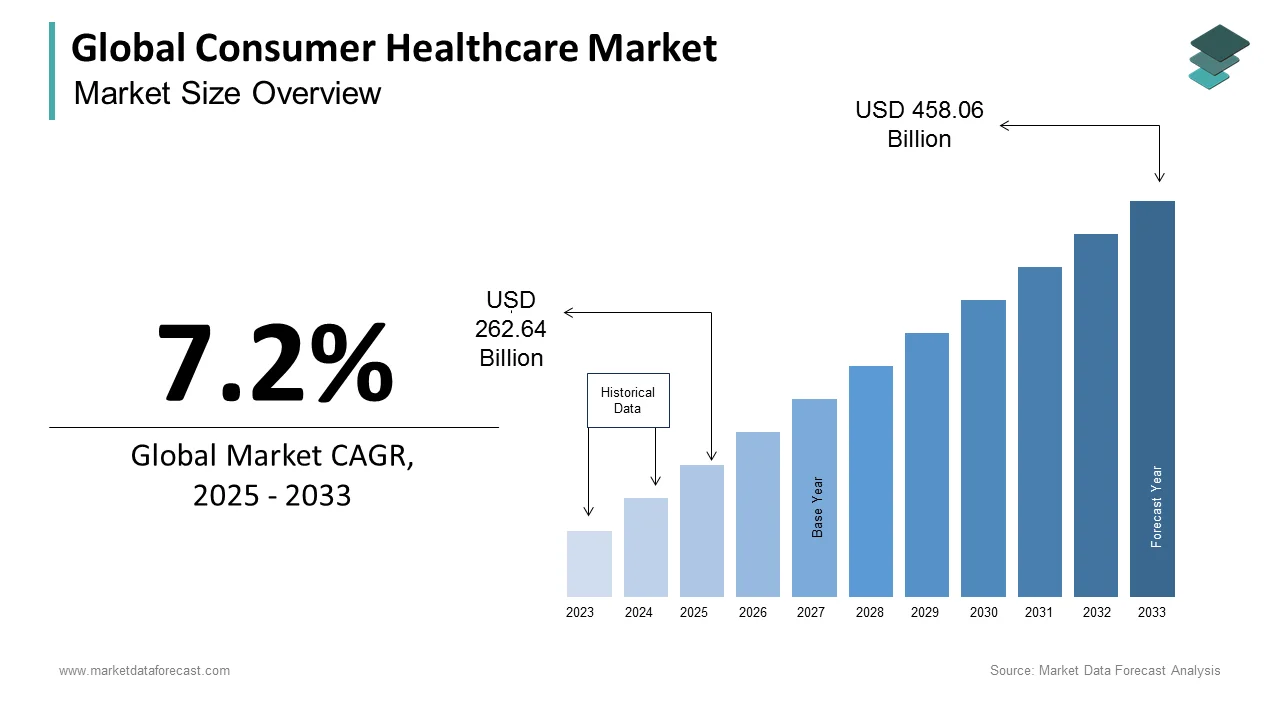

The global consumer healthcare market was valued at USD 262.64 billion in 2025, is projected to reach USD 281.55 billion in 2026, and is expected to expand to USD 491.04 billion by 2034, growing at a CAGR of 7.2% from 2026 to 2034. The growth of the global consumer healthcare market is driven by increasing awareness of self-care, rising demand for over-the-counter (OTC) products, and growing focus on preventive healthcare solutions. Expanding retail and e-commerce channels, coupled with increasing disposable incomes in emerging markets, are also contributing to industry expansion.

Key Market Trends

- Rising adoption of OTC pharmaceuticals for self-medication and preventive care.

- Growth of pharmacies and drugstores as the primary consumer healthcare distribution channel.

- Expanding penetration of e-commerce platforms for health supplements and wellness products.

- Increasing consumer focus on natural and herbal healthcare products.

- Strong demand for dietary supplements, vitamins, and functional foods.

Segmental Insights

- Based on product type, the OTC pharmaceuticals segment was the largest in 2024, supported by strong demand for pain relief, digestive health, and cold & flu treatments.

- Based on distribution channel, the pharmacies or drugstores segment dominated with 48.3% share in 2024, reflecting their accessibility and trusted role in healthcare purchases.

Regional Insights

- North America was the largest contributor to the global consumer healthcare market in 2024, accounting for 34.2% share, driven by high healthcare expenditure, established retail channels, and rising consumer preference for OTC and dietary supplements.

- Europe shows steady growth, supported by regulatory frameworks and rising consumer interest in natural products.

- Asia-Pacific is expected to record the fastest growth, fueled by rising middle-class incomes, growing urbanization, and increased healthcare awareness.

- Latin America and the Middle East & Africa are emerging markets, supported by expanding pharmacy networks and rising adoption of self-care practices.

Competitive Landscape

Key players in the global consumer healthcare market include Johnson & Johnson, Boehringer Ingelheim GmbH, GlaxoSmithKline plc, Amway, Bayer AG, Pfizer Inc., Abbott Laboratories, Sanofi, BASF SE, DSM, American Health, Herbalife, The Himalaya Drug Company, Kellogg, Takeda Pharmaceuticals, and Teva Pharmaceuticals. These companies are focusing on product innovation, natural health products, e-commerce expansion, and strategic partnerships to strengthen their global presence.

Global Consumer Healthcare Market Size

The size of the global consumer healthcare market was worth USD 262.64 billion in 2025. The global market is anticipated to grow at a CAGR of 7.2% from 2026 to 2034, reaching USD 491.04 billion by 2034, up from USD 281.55 billion in 2026.

Consumer healthcare encompasses over-the-counter (OTC) pharmaceuticals, dietary supplements, personal care products, and self-diagnostic tools that empower individuals to manage their health independently, outside formal clinical settings. This domain reflects a paradigm shift from reactive treatment to proactive wellness management, driven by increasing health literacy and the decentralization of medical care. According to the World Health Organization, approximately 4.6 billion people globally lack access to essential health services, compelling populations to rely on self-care solutions for minor ailments and preventive needs. According to the Global Fund, in low- and middle-income countries, community pharmacies and drug sellers serve as the first point of contact for over 60% of patients seeking treatment for common conditions such as headaches, gastrointestinal discomfort, and respiratory symptoms. The rise of digital health platforms has further accelerated self-care adoption, with mobile apps now offering symptom checkers, dosage reminders, and teleconsultations that complement OTC product use. Regulatory frameworks, such as those established by the U.S. Food and Drug Administration and the European Medicines Agency, ensure the safety and efficacy of consumer-available treatments, fostering public trust. Additionally, aging populations in countries like Japan and Germany are driving demand for chronic condition management at home, including products for joint health, digestive support, and immune enhancement. The integration of nutraceuticals and evidence-based formulations into daily routines underscores a growing cultural emphasis on preventive health. With urbanization, rising disposable incomes, and the normalization of self-diagnosis, the consumer healthcare sector is evolving into a critical component of global health infrastructure.

MARKET DRIVERS

Rising Burden of Chronic Diseases and Preventive Health Awareness

The escalating prevalence of non-communicable diseases (NCDs) is a pivotal force driving the expansion of the global consumer healthcare market. According to the World Health Organization, NCDs such as cardiovascular diseases, diabetes, and chronic respiratory conditions account for 74% of all global deaths, with a significant proportion occurring prematurely in individuals under 70. This growing disease burden has intensified public focus on prevention and early intervention, prompting consumers to adopt self-care strategies that mitigate long-term risks. According to the Indian Council of Medical Research, the prevalence of type 2 diabetes in India has surged to 11.4% among urban adults, which is fuelling demand for glucose monitoring kits, dietary supplements, and herbal formulations marketed for metabolic support. According to the Centers for Disease Control and Prevention, over 60% of adults live with at least one chronic condition in the United States, fostering reliance on OTC pain relievers, antacids, and cardiovascular supplements. The integration of wearable devices, such as smart watches that track heart rate and blood oxygen, has further normalized health monitoring outside clinical environments. According to the Korean Society of Hypertension, in South Korea, where hypertension affects nearly 30% of adults, sales of home blood pressure monitors and plant-based circulatory supplements grew by 17% annually between 2020 and 2023. Public health campaigns promoting early detection and lifestyle modification have reinforced consumer confidence in self-management. This shift toward proactive health engagement is transforming the consumer healthcare market from a remedy-focused sector into a preventive, data-informed ecosystem.

Expansion of Digital Health Platforms and Teleconsultation Services

The proliferation of digital health technologies has fundamentally reshaped consumer engagement with self-care products, which is further contributing to the consumer healthcare market expansion. According to the World Bank, global internet penetration reached 67% in 2023, enabling widespread access to online pharmacies, symptom assessment tools, and virtual consultations. According to the Asian Development Bank, telehealth adoption in Southeast Asia surged by 45% between 2021 and 2023, with platforms like Halodoc in Indonesia and Doctor Anywhere in Singapore integrating OTC product recommendations into digital consultations. These services allow users to receive personalized treatment plans and purchase recommended medications without visiting a clinic, streamlining the care pathway. According to the World Health Organization, mobile health apps have become essential for diagnosing and managing common ailments in Nigeria, where physician density is only 0.4 per 1,000 people. Additionally, artificial intelligence-powered chatbots are being deployed to guide consumers in selecting appropriate OTC treatments, reducing misuse and enhancing safety. The U.S. Food and Drug Administration has recognized this trend by approving digital therapeutic platforms that complement OTC drug use for conditions like insomnia and anxiety. In Europe, the European Commission’s Digital Health Infrastructure initiative has facilitated cross-border e-prescriptions and OTC access, improving care continuity. The convergence of e-commerce, AI diagnostics, and secure payment systems has created a seamless self-care ecosystem, particularly appealing to younger, tech-savvy demographics. This digital transformation not only increases accessibility but also fosters data-driven health decisions, positioning digital integration as a cornerstone of modern consumer healthcare.

MARKET RESTRAINTS

Regulatory Heterogeneity and Compliance Complexity Across Regions

A significant impediment to the global expansion of the consumer healthcare market is the lack of harmonized regulatory standards governing product safety, labeling, and claims substantiation. According to the World Health Organization, over 150 countries have distinct regulatory frameworks for OTC medicines and supplements, creating substantial barriers for multinational manufacturers. In the European Union, the Traditional Herbal Medicinal Products Directive requires rigorous evidence for herbal claims, whereas in Southeast Asia, regulatory oversight is fragmented, with countries like Thailand and the Philippines maintaining divergent approval timelines and ingredient restrictions. This inconsistency increases time-to-market and compliance costs, particularly for small and medium enterprises lacking dedicated regulatory affairs teams. According to the Central Drugs Standard Control Organization, over 30% of OTC product applications in India were delayed in 2023 due to incomplete documentation or non-alignment with revised labeling guidelines. Furthermore, the absence of universal standards for dietary supplements allows for varying levels of quality control, and according to the U.S. Government Accountability Office, 20% of supplement products tested in 2022 contained undeclared ingredients or inaccurate potency levels. According to the European Consumer Organisation, over 500 complaints were filed in 2023 against brands for unsubstantiated wellness assertions. These regulatory disparities not only hinder market access but also erode consumer trust, particularly in regions where counterfeit or substandard products remain prevalent. Until greater international alignment is achieved, regulatory fragmentation will continue to constrain innovation and equitable access.

Persistent Use of Unproven Remedies and Low Health Literacy in Developing Regions

Despite advancements in consumer healthcare, a substantial portion of the global population continues to rely on traditional or unverified treatments due to limited health literacy and inadequate access to evidence-based information, which is further impeding the consumer healthcare market expansion. According to UNESCO, over 750 million adults worldwide lack basic reading and writing skills, severely limiting their ability to interpret medication labels, dosage instructions, or contraindications. According to the World Health Organization, up to 80% of the population in Sub-Saharan Africa uses traditional medicine as a primary source of care, often delaying or forgoing validated treatments scientifically. According to the Nigerian Institute of Medical Research, a 2023 study found that 65% of respondents in rural Nigeria could not distinguish between prescription and OTC drugs, leading to inappropriate self-medication. According to the International Centre for Diarrhoeal Disease Research, it was reported that only 38% of mothers in Bangladesh correctly administered oral rehydration salts for childhood diarrhea, opting instead for ineffective home remedies. The proliferation of misinformation through social media further exacerbates the issue, and in India, WhatsApp-driven health myths have led to dangerous practices such as using turpentine or neem oil as antiviral treatments. According to the Pan American Health Organization, it is noted that only 45% of hypertensive patients in Latin America consistently use recommended OTC supplements or lifestyle interventions. These behavioral and educational gaps undermine the effectiveness of consumer healthcare products and limit market penetration, particularly in regions where public health infrastructure remains underdeveloped.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Personalized Self-Care Solutions

The application of artificial intelligence (AI) in consumer healthcare is a promising opportunity for the global consumer healthcare market. According to the World Economic Forum, AI-powered health tools are projected to influence over 3 billion consumer health decisions by 2025, enabling real-time symptom analysis, treatment recommendations, and medication tracking. In the United States, AI-driven apps like Ada Health and K Health analyze user-reported symptoms against vast medical databases to suggest appropriate OTC remedies, reducing unnecessary doctor visits. According to the Journal of Medical Internet Research, these platforms have demonstrated clinical accuracy rates exceeding 85% in preliminary validation studies. In China, Alibaba Health’s AI assistant processed over 100 million consumer health inquiries in 2023, providing instant guidance on cold remedies, digestive aids, and vitamin supplements. The integration of AI with wearable devices allows for continuous physiological monitoring, enabling dynamic adjustments to self-care regimens. For instance, smart inhalers with embedded sensors can recommend OTC bronchodilators based on environmental triggers and usage patterns, as noted by the Global Initiative for Asthma. Additionally, AI enhances supply chain efficiency by predicting regional demand surges for seasonal products like antihistamines or immune boosters. With increasing computational power and access to anonymized health data, AI is poised to transform consumer healthcare from a static product market into an adaptive, intelligent ecosystem tailored to individual needs.

Expansion of Preventive Care Models in Aging Populations

The global demographic shift toward older populations is creating a robust opportunity for the consumer healthcare market to expand into preventive and age-related wellness solutions. According to the United Nations Department of Economic and Social Affairs, the number of people aged 65 and over is expected to double by 2050, reaching 1.5 billion, with Japan, Italy, and Germany already classified as super-aged societies. According to the Ministry of Internal Affairs and Communications, demand for OTC joint health supplements, cognitive support formulations, and home diagnostic kits has surged in Japan, where 29% of the population is over 65. The Japanese government’s "Healthy Japan 21" initiative actively promotes self-care among seniors, encouraging the use of blood pressure monitors, glucose testers, and calcium-vitamin D combinations to delay institutionalization. According to the Korean Health Industry Development Institute, sales of probiotics and bone health supplements among adults over 50 in South Korea grew by 22% annually between 2020 and 2023. Preventive strategies are also gaining traction in emerging markets, and in Brazil, the Ministry of Health launched a national self-care program targeting hypertension and diabetes in the elderly, distributing educational materials and subsidizing home testing kits. These initiatives reduce strain on public health systems while fostering long-term consumer loyalty to trusted brands. As aging populations prioritize independence and quality of life, the market for science-backed, easy-to-use preventive products is set to become a dominant growth vector.

MARKET CHALLENGES

Misuse and Overreliance on Over-the-Counter Medications

A growing concern within the consumer healthcare market is the inappropriate use of OTC medications, including dosage errors, drug interactions, and prolonged self-treatment without professional consultation. According to the U.S. Food and Drug Administration, nearly 25% of American adults admit to exceeding recommended doses of pain relievers like acetaminophen, increasing the risk of liver damage. According to the National Agency for the Safety of Medicines and Health Products, a 2023 study in France found that 40% of consumers combined multiple OTC drugs without awareness of potential interactions, particularly between NSAIDs and anticoagulants. The problem is exacerbated by limited labeling comprehension, especially among elderly users and non-native speakers. According to the Public Health Agency of Canada, 18% of emergency room visits for adverse drug events involved OTC products, many of which were preventable. The normalization of self-diagnosis through online sources further compounds the issue, with individuals often misinterpreting symptoms and delaying necessary medical intervention. In India, the overuse of antibiotic-containing topical creams sold as general antiseptics has contributed to rising antimicrobial resistance, as noted by the Indian Council of Medical Research. While consumer autonomy is a cornerstone of self-care, the absence of real-time professional oversight increases the risk of harm. Manufacturers and regulators face the challenge of balancing accessibility with safety, requiring innovative solutions such as QR-coded digital leaflets, AI-driven usage alerts, and pharmacist-led digital triage.

Counterfeit and Substandard Products Undermining Consumer Trust

The proliferation of counterfeit and substandard consumer healthcare products poses a severe threat to public health and market integrity, particularly in regions with weak regulatory enforcement, which is one of the major challenges to the consumer healthcare market growth. According to the World Health Organization, 1 in 10 medical products in low- and middle-income countries is either falsified or substandard, with OTC medicines and dietary supplements among the most commonly affected categories. In Nigeria, the National Agency for Food and Drug Administration and Control seized over 12,000 counterfeit product units in 2023, including fake painkillers, vitamins, and antihistamines, many of which contained harmful fillers or incorrect dosages. Similarly, in Southeast Asia, illicit online marketplaces have been found selling adulterated weight-loss supplements laced with banned stimulants, as reported by the ASEAN Pharmaceutical Regulatory Network. The rise of cross-border e-commerce has made enforcement more difficult, with counterfeit goods often shipped from unregulated jurisdictions. According to Europol, customs officials in the European Union intercepted over 3 million fake health products in 2022, which represents a 30% increase from the previous year. These incidents erode consumer confidence and deter legitimate brands from entering high-risk markets. The economic incentive for counterfeiters remains high, as production costs are minimal compared to retail value. Addressing this challenge requires coordinated international surveillance, blockchain-based authentication, and public awareness campaigns to help consumers identify genuine products, all of which demand significant investment and collaboration across stakeholders.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Distribution Network & Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Johnson & Johnson, Boehringer Ingelheim GmbH, GlaxoSmithKline plc, Amway, Bayer AG, Pfizer Inc., Abbott Laboratories, Sanofi, BASF SE, DSM, American Health, Herbalife, The Himalaya Drug Company, Kellogg, Takeda Pharmaceuticals and Teva Pharmaceuticals. |

SEGMENTAL ANALYSIS

By Product Insights

The OTC pharmaceuticals segment led the market by holding 60.6% of the global market share in 2025. The dominance of the OTC pharmaceuticals segment in the global market can be attributed to the widespread reliance on self-treatment for common, non-life-threatening conditions such as pain, allergies, gastrointestinal disturbances, and respiratory ailments. A key driver of its leadership is the high frequency of usage and immediate symptom relief offered by these products, making them indispensable in household medicine cabinets. According to the U.S. Centers for Disease Control and Prevention, over 80% of Americans use at least one OTC medication annually, with pain relievers like ibuprofen and acetaminophen being the most frequently consumed. According to the German Federal Institute for Drugs and Medical Devices, more than 70% of minor health issues in Germany are managed without physician consultation, where self-medication is deeply embedded in the healthcare culture. The accessibility of OTC drugs, which are available without a prescription in most countries, further amplifies their adoption. According to the Japanese Ministry of Health, Labour and Welfare, over 55% of adults purchase OTC products for cold and flu symptoms each year in Japan, where the government actively promotes self-care to reduce strain on the public health system. Additionally, rigorous regulatory oversight by agencies such as the European Medicines Agency and Health Canada ensures product safety and efficacy, reinforcing consumer confidence. The integration of digital symptom checkers in pharmacies and online platforms has also streamlined product selection, reducing decision fatigue. These factors collectively sustain OTC pharmaceuticals as the cornerstone of consumer healthcare, offering a reliable, cost-effective alternative to clinical visits.

On the other side, the dietary supplements segment is the fastest-growing category within the consumer healthcare market and is expected to record a CAGR of 10.2% during the forecast period owing to a global shift toward preventive health, the increasing perception of supplements as essential tools for long-term wellness, and the rising prevalence of micronutrient deficiencies and lifestyle-related health risks, prompting consumers to proactively address nutritional gaps. According to the World Health Organization, over 2 billion people worldwide suffer from vitamin and mineral deficiencies, including iron, vitamin D, and B12, particularly among urban populations with processed-food-heavy diets. According to the National Family Health Survey-5, 57% of women and 25% of men are anemic in India, driving demand for iron and folic acid supplements. According to the National Health and Nutrition Examination Survey, it was found that over 40% of adults take vitamin D supplements in the United States, citing immune support and bone health benefits. The aging population further amplifies demand, with adults over 50 increasingly using calcium, omega-3, and probiotic supplements to maintain mobility and digestive function. According to the Korean Society of Nutrition, sales of collagen and antioxidant supplements in South Korea grew by 23% annually between 2020 and 2023. Moreover, scientific validation of certain ingredients, such as curcumin for inflammation and magnesium for sleep, has elevated consumer trust. With manufacturers leveraging clinical research, transparent labeling, and e-commerce platforms to reach health-conscious audiences, dietary supplements are evolving from niche products into mainstream wellness essentials.

By Distribution Network Insights

The pharmacies or drugstores segment held 41.5% of the global market share in 2025. The leading position of pharmacies or drug stores segment in the global market is driven by their unique position as trusted, regulated, and professionally staffed access points for self-care products. A critical factor reinforcing their dominance is the presence of licensed pharmacists who provide real-time health advice and product recommendations, enhancing consumer confidence in self-selection. According to the International Pharmaceutical Federation, over 90% of Europeans consult a pharmacist before purchasing OTC medications, particularly for complex conditions like allergies or gastrointestinal issues. According to the Canadian Pharmacists Association, community pharmacies in Canada serve as primary care extensors, with 65% of patients receiving counseling on dosage, interactions, and contraindications. Additionally, pharmacies offer a curated product range that balances brand reliability and regulatory compliance, distinguishing them from general retail outlets. According to the Japan Pharmaceutical Association, drugstores account for 72% of OTC sales in Japan, where self-medication is encouraged by national health policy, with chains like Sugi Pharmacy and Matsumotokiyoshi operating over 10,000 stores nationwide. The integration of private-label brands, which offer cost-effective alternatives without compromising quality, has further strengthened their competitive edge. In emerging markets like Brazil and South Africa, pharmacy chains are expanding into underserved urban and peri-urban areas, supported by government-backed health initiatives. Their role as frontline health advisors, combined with strategic locations and professional credibility, ensures that pharmacies remain the most influential and trusted channel in the consumer healthcare ecosystem.

However, the online retail segment is the fastest-growing distribution network in the consumer healthcare market and is anticipated to witness a CAGR of 16.1% during the forecast period owing to the increasing demand for discreet, convenient, and personalized access to self-care products, particularly among younger and digitally native consumers. A major growth catalyst is the integration of telehealth services with e-pharmacy platforms, enabling users to receive virtual consultations and purchase recommended OTC products in a single digital journey. According to the Indian Brand Equity Foundation, PharmEasy and 1mg reported a 40% increase in consumer healthcare sales in 2023, with over 60% of transactions involving supplements, sexual wellness products, and mental health aids. According to the Office for National Statistics, Boots.com surpassed in-store OTC sales for the first time in 2022 in the United Kingdom, driven by discreet packaging and same-day delivery options. Social commerce is also playing a transformative role, and according to the China E-Commerce Research Center, live-streamed health product launches on platforms like JD Health have generated over $1.8 billion in annual sales. The ability to access niche, premium, and international brands, such as probiotics, adaptogens, and specialty vitamins, further enhances online appeal. According to the United Nations Conference on Trade and Development, e-commerce now accounts for 20% of total retail sales in developed economies, with healthcare products among the fastest-adopted categories. With AI-driven recommendations, subscription models, and digital health records integration, online retail is redefining consumer expectations, positioning it as the most dynamic and scalable distribution force.

REGIONAL ANALYSIS

North America Consumer Healthcare Market Analysis

The North American region held the highest share of 35.3% of the global market in 2025 and is expected to experience steady growth and maintain a dominant position over the next few years. The region’s market maturity is defined by high health literacy, strong regulatory frameworks, and a deeply ingrained culture of self-reliance in health management. According to the National Center for Health Statistics, over 80% of consumers in the United States, where healthcare costs are among the highest globally, prefer using OTC medications to avoid doctor visits for minor ailments. The country is a pioneer in evidence-based supplements, with the U.S. Food and Drug Administration enforcing strict labeling and safety standards that enhance consumer trust. According to the Canadian Institute for Health Information, provincial health systems in Canada mirror this trend, actively promoting pharmacist-led self-care to reduce the primary care burden. The presence of major players ensures continuous innovation in pain relief, digestive health, and immune support products. Additionally, digital health adoption is accelerating, with telepharmacy services and AI-powered symptom checkers becoming integral to OTC decision-making. According to the U.S. Census Bureau, the aging population is projected to reach 22% of the U.S. populace by 2050, driving demand for chronic condition management at home. North America’s blend of consumer empowerment, technological integration, and regulatory rigor establishes it as the most advanced and influential market in the global consumer healthcare landscape.

Europe Consumer Healthcare Market Analysis

Europe is projected to show sustained advancement and steady expansion over the next few years. The region’s market is characterized by a strong tradition of self-medication, supported by well-established pharmacy networks and proactive public health policies. According to the German Association of Pharmacists, over 60% of all minor health conditions in Germany, one of the most mature markets, are treated with OTC products. The country’s “Apotheken” (pharmacies) operate under strict regulatory oversight, ensuring product quality and professional guidance, which fosters high consumer confidence. France and the UK exhibit similar patterns, with pharmacists playing a central role in recommending treatments for allergies, colds, and digestive issues. The European Medicines Agency’s harmonized OTC approval process has streamlined cross-border availability, while national initiatives like the UK’s “Pharmacy First” program aim to reduce GP workload by expanding pharmacist prescribing authority. According to the Nordic Council of Ministers, demand for vitamin D, omega-3, and probiotic supplements exceeds 70% among adults in Scandinavia, where preventive health is prioritized. Regulatory emphasis on transparency, such as mandatory front-of-pack nutrition and ingredient labeling, has also shaped consumer behavior. With rising healthcare costs and aging populations, European governments are increasingly viewing consumer healthcare as a cost-effective alternative to clinical care, reinforcing the sector’s strategic importance.

Asia-Pacific Consumer Healthcare Market Analysis

The Asia-Pacific region is anticipated to exhibit rapid market acceleration and significant value creation over the next few years. This region is one of the most rapidly evolving markets due to demographic momentum and rising health consciousness. In China, the world’s second-largest consumer healthcare market, urbanization and increasing disposable incomes have fueled demand for premium vitamins, herbal remedies, and functional foods. According to the China Nutrition Society, over 50% of urban residents now take dietary supplements regularly, with collagen and traditional Chinese medicine-based products gaining popularity. Japan, with its super-aged society, leads in OTC innovation, with the Ministry of Health approving over 1,200 self-care products for conditions ranging from joint pain to cognitive decline. According to the National Family Health Survey-5, rising awareness of diabetes and anemia in India has driven sales of iron, vitamin B12, and glucose regulators, indicating that 42% of households now stock OTC supplements. The expansion of organized retail and e-pharmacies has improved access in both urban and rural areas. Additionally, cultural acceptance of traditional remedies like Ayurveda and Kampo integrates seamlessly with modern self-care practices. With government initiatives promoting preventive health and digital health adoption accelerating, Asia-Pacific is poised for sustained growth, driven by both volume expansion and premiumization.

Latin America Consumer Healthcare Market Analysis

The consumer healthcare market in Latin America is likely to expand progressively and capture higher consumer engagement over the next few years. Brazil and Mexico serve as the primary commercial hubs for this market, which is shaped by a mix of traditional medicine use and growing demand for modern self-care solutions. According to the Brazilian Institute of Geography and Statistics, over 65% of adults in Brazil use OTC medications for pain, colds, and gastrointestinal issues, with major pharmacies dominating distribution. According to the National Institute of Public Health of Mexico, the high prevalence of diabetes and obesity, where 75% of adults are overweight, has increased reliance on glucose monitors, weight management supplements, and digestive aids. However, regulatory fragmentation across countries creates challenges, and according to the Inter-American Conference on Health, countries like Argentina and Colombia maintain distinct approval timelines and labeling requirements. E-commerce is emerging as a key growth channel, and Mercado Libre recorded a 30% increase in OTC sales in 2023, driven by younger consumers seeking discreet access to sexual wellness and mental health products. Public health campaigns in Chile and Peru are promoting pharmacist-led self-care to reduce hospital overcrowding. Despite economic volatility, the region’s young population, urbanization, and rising health awareness offer significant long-term potential for market expansion.

Middle East and Africa Consumer Healthcare Market Analysis

The Middle East and Africa region is expected to undergo dynamic developments and varying regional growth trajectories over the next few years. There are stark contrasts between affluent Gulf states and developing African nations. According to the Gulf Cooperation Council Standardization Organization, high disposable incomes and expatriate populations in the UAE and Saudi Arabia drive demand for premium vitamins, immune boosters, and weight management supplements, with per capita OTC spending among the highest in the region. In contrast, Sub-Saharan Africa faces significant access barriers, and according to UNICEF, only 30% of the population lives within one hour of a health facility. However, innovative models are bridging gaps, and community health kiosks in Kenya and Nigeria serve over 8 million people monthly, offering fortified supplements and nutritional guidance. According to the South African Pharmacy Council, South Africa leads in modern retail penetration, with pharmacies like Clicks and Dis-Chem accounting for 55% of OTC sales. According to the Ministry of Industry and Trade, government-backed initiatives in Egypt to promote local supplement production have reduced import dependency, with domestic vitamin output rising by 16% in 2023. Mobile health platforms in Ghana are digitizing supply chains, improving availability.

COMPETITIVE LANDSCAPE

The competition in the consumer healthcare market is characterized by a dynamic interplay between legacy strength and disruptive innovation. Established multinational corporations leverage their scientific credibility, extensive distribution networks, and iconic brand portfolios to maintain dominance in core categories such as pain relief, digestive health, and vitamins. However, they face intensifying pressure from agile startups and digital-native brands that specialize in niche wellness segments—ranging from adaptogenic supplements to gut microbiome support. These challengers often differentiate through clean labels, transparent sourcing, and direct-to-consumer models that foster deeper emotional connections with health-conscious consumers. E-commerce and social media have leveled the playing field, enabling smaller players to gain visibility without relying on traditional retail gatekeepers. Sustainability has emerged as a critical battleground, with consumers scrutinizing environmental impact, ethical sourcing, and corporate responsibility. Brand authenticity and scientific substantiation are now as important as efficacy and convenience. Companies are also competing on technological integration, incorporating AI-driven personalization, blockchain traceability, and smart dispensing systems. Strategic partnerships with pharmacies, telehealth providers, and fitness platforms are redefining how self-care is delivered and perceived. As the boundary between medical treatment and daily wellness continues to blur, competition is no longer just about market share and it is about shaping the future of proactive, personalized, and empowered health management.

KEY MARKET PLAYERS

A few of the promising companies operating in the global consumer healthcare market include

- Johnson & Johnson

- Boehringer Ingelheim GmbH

- GlaxoSmithKline plc

- Amway

- Bayer AG

- Pfizer Inc.

- Abbott Laboratories

- Sanofi

- BASF SE

- DSM

- American Health

- Herbalife

- The Himalaya Drug Company

- Kellogg

- Takeda Pharmaceuticals

- Teva Pharmaceuticals

TOP PLAYERS IN THE MARKET

- Johnson & Johnson Consumer Health has long been a defining force in the global self-care sector, offering a portfolio that spans pain relief, gastrointestinal health, dermatology, and wellness. The company’s strength lies in its deep scientific expertise, rigorous safety standards, and trusted brand equity built over decades. Through household names like Listerine, Tylenol, and Neutrogena, J&J has embedded itself in daily health routines across cultures and income levels. Its focus on innovation integrates clinical research with consumer insights, enabling the development of targeted, science-backed solutions. Following its spin-off as Kenvue in 2023, the company has sharpened its strategic focus on consumer-centricity, agility, and digital engagement. By investing in personalized health platforms and sustainable packaging, it aligns with evolving consumer expectations. J&J Consumer Health continues to shape global standards for product efficacy and safety, maintaining a leadership position through a blend of heritage, trust, and forward-looking transformation.

- GSK Consumer Healthcare, now operating as Haleon following its demerger, stands as a dedicated leader in self-care, with a portfolio anchored in oral health, pain management, respiratory care, and vitamins. The company’s global influence stems from iconic brands such as Sensodyne, Panadol, Advil, and Centrum, which are synonymous with reliability and everyday wellness. Haleon’s strategy emphasizes consumer intimacy, leveraging data and digital tools to anticipate health needs and deliver tailored solutions. The company has prioritized scientific rigor, ensuring that product claims are substantiated through clinical research, thereby reinforcing trust in over-the-counter therapeutics. Its commitment to accessibility extends to emerging markets, where it adapts formulations and packaging to local needs. By integrating sustainability into product design and supply chain operations, Haleon strengthens its social license to operate. The separation from GSK’s pharmaceutical arm has enabled greater agility, allowing the company to respond swiftly to shifting consumer behaviors and health trends, positioning it as a pure-play innovator in the evolving self-care ecosystem.

- Bayer Consumer Health is a global pioneer in self-medication, renowned for its science-driven approach and long-standing commitment to preventive care. With flagship brands like Aspirin, Aleve, Bepanthen, and One A Day, the company has established a presence in pain relief, digestive health, allergy management, and nutritional supplementation. Its influence extends beyond product development to public health education, where it collaborates with healthcare providers and governments to promote responsible self-care. Bayer emphasizes innovation through clinical validation, ensuring that its offerings meet stringent safety and efficacy benchmarks. The company has embraced digital health integration, partnering with telehealth platforms to enhance consumer access and guidance. By focusing on lifecycle nutrition and age-specific wellness, Bayer addresses the needs of diverse demographics, from infants to the elderly. Its global footprint, supported by localized strategies and sustainable practices, enables it to maintain relevance across markets. Bayer’s fusion of scientific legacy and consumer-centric evolution solidifies its role as a cornerstone of the modern consumer healthcare landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players is the strategic demerger and creation of dedicated consumer health entities, allowing for greater focus, operational agility, and investor appeal. By separating consumer healthcare from pharmaceutical or biotech divisions, companies like GSK and Johnson & Johnson have established independent entities that can prioritize consumer needs, accelerate innovation, and respond dynamically to market trends without competing for internal resources. This structural shift enables deeper investment in branding, digital engagement, and personalized health solutions.

Another pivotal approach is the integration of digital health ecosystems with self-care products, where companies link OTC medications and supplements with mobile apps, wearables, and AI-driven platforms. This allows for real-time symptom tracking, dosage reminders, and personalized recommendations, transforming passive product use into an interactive health management experience. Brands are increasingly embedding QR codes, smart packaging, and teleconsultation access to enhance user engagement and adherence.

A third key strategy is geographic and demographic customization of product portfolios, where companies tailor formulations, packaging, and messaging to align with regional health challenges, cultural preferences, and lifestyle behaviors. Whether adapting vitamin blends for nutrient-deficient populations or launching discreet packaging for sensitive health categories, this hyper-localized approach strengthens relevance and trust in diverse markets.

MARKET SEGMENTATION

This research report on the global consumer healthcare market has been segmented and sub-segmented based on product, distribution network, and region.

By Product

- OTC Pharmaceuticals

- Dietary Supplements

By Distribution Network

- Departmental Stores

- Independent Retailers

- Pharmacies or Drugstores

- Specialist Retailers

- Supermarkets or Hypermarkets

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the Consumer Healthcare Market?

The Consumer Healthcare Market includes over-the-counter (OTC) medications, dietary supplements, wellness products, personal care items, and digital health solutions directly purchased by consumers for health maintenance, disease prevention, and wellness management

2. What are the main product categories within the Consumer Healthcare Market?

Key categories include OTC drugs, dietary supplements, herbal and natural products, personal care, wellness devices, and digital health platforms

3. Which regions dominate the Consumer Healthcare Market?

North America leads the market due to high health awareness, technological adoption, and e-commerce penetration, followed by Europe and Asia-Pacific which is experiencing rapid growth

4. What are the key factors driving growth in the Consumer Healthcare Market?

Growth factors include increasing health consciousness, aging populations, rising prevalence of lifestyle diseases, expansion of online pharmacies, and advancements in digital health technologies

5. How does e-commerce influence the Consumer Healthcare Market?

The rise of online pharmacies and direct-to-consumer platforms makes health products more accessible, convenient, and affordable, significantly transforming the retail landscape

6. Who are the major players in the Consumer Healthcare Market?

Major companies include Johnson & Johnson, Pfizer, Bayer AG, GlaxoSmithKline, Herbalife, Amway, Nestlé, and numerous regional and emerging brands

7. What role do digital health and telemedicine play in the Consumer Healthcare Market?

Digital health apps, telemedicine consultations, wearables, and AI-driven health management systems enhance consumer engagement, personalized care, and remote diagnostics

8. What are the trends in herbal and natural health products?

Growing consumer preference for organic, herbal, and botanical remedies supports this segment, driven by wellness trends and regulatory approvals

9. How is the aging population impacting the Consumer Healthcare Market?

Older adults seek prevention, chronic disease management, and home care solutions, increasing demand for supplements, OTC medications, and digital health devices tailored for seniors

10. What challenges does the Consumer Healthcare Market face?

Challenges include regulatory complexity, ensuring product quality, counterfeit risks, consumer safety concerns, and supply chain disruptions

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com