Global Corn Starch Market Size, Share, Trends, & Growth Forecast Report Segmented By Product (Modified Starch, Native Starch And Sweeteners), Application (Animal Feed, Food And Beverages, Paper And Board And Others), And Region (North America, Europe, Asia Pacific, Latin America, And Middle East & Africa) - Industry Analysis (2026 To 2034)

Market Size, 2025

$26.33 BnMarket Estimate, 2026

$28.52 BnMarket Forecast, 2034

$53.97 BnCAGR, 2026–2034

8.3%Global Corn Starch Market Size

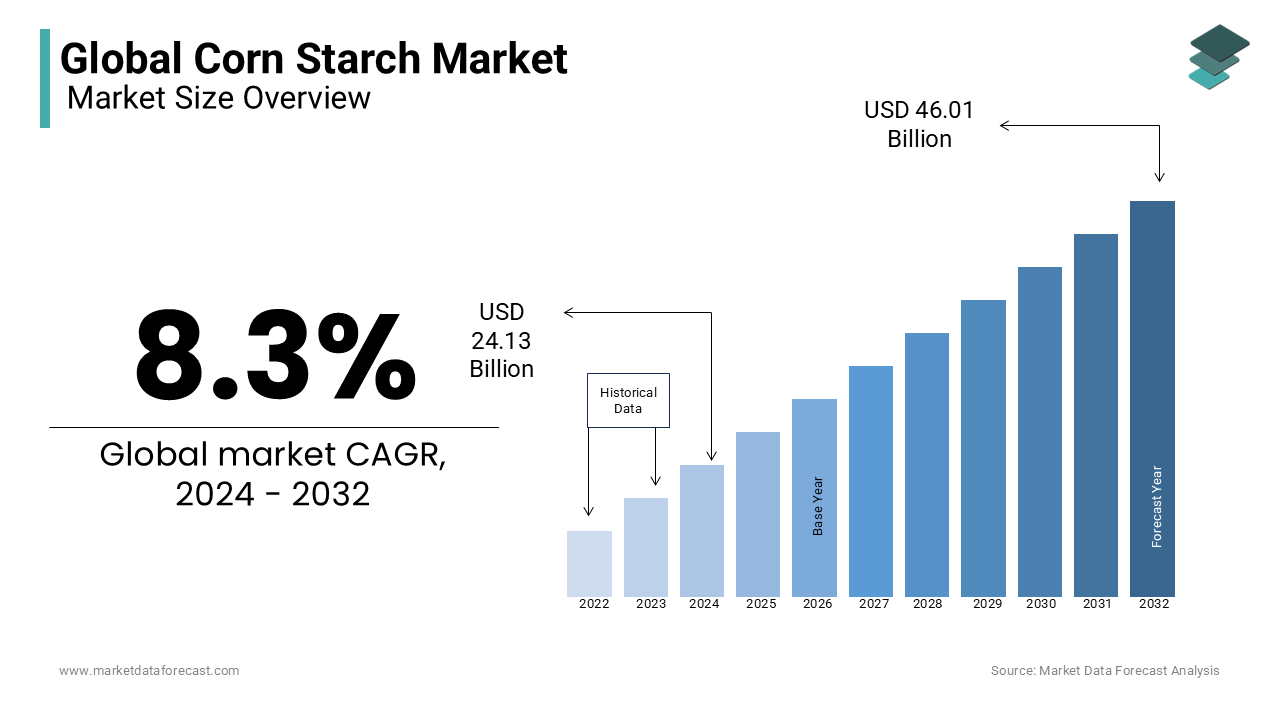

The size of the global corn starch market was worth USD 26.33 billion in 2026. The global market size is expected to grow at a CAGR of 8.3% from 2026 to 2034 and be worth USD 53.97 billion by 2034 from USD 28.52 billion in 2026.

Corn Starch refers to the starch extracted from the endosperm of corn kernels, primarily used across food and beverage, pharmaceutical, textile, and paper industries. As a highly versatile carbohydrate, corn starch functions as a thickening agent, stabilizer, and binder, with growing utility in biodegradable packaging and bio-based polymers. According to the United States Department of Agriculture (USDA), the U.S. alone harvested approximately 14.4 billion bushels of corn in 2023. The expansion of clean-label food formulations and non-food industrial innovations continues to redefine the functional scope of corn starch in global supply chains.

MARKET DRIVERS

Rising Demand in Plant-Based Food Formulations

The surge in plant-based food consumption has significantly amplified the demand for corn starch as a functional ingredient. With consumers increasingly adopting vegan and vegetarian diets, food manufacturers are leveraging corn starch for its texturizing and binding properties in meat analogs, dairy alternatives, and ready-to-eat meals. Corn starch is particularly valued in plant-based meat products for its ability to mimic the fibrous texture of animal muscle when processed under high moisture and shear conditions. This shift in dietary patterns, coupled with clean-label trends favoring recognizable ingredients, positions corn starch as a critical enabler of next-generation plant-based innovation.

Expansion in Biodegradable Packaging Applications

Corn starch has emerged as a pivotal component in the development of compostable and biodegradable packaging materials, driven by tightening global regulations on single-use plastics. Its thermoplastic properties allow it to be blended with polylactic acid (PLA) and other biopolymers to produce flexible films, trays, and cushioning materials. According to the United Nations Environment Programme, over 11 million metric tons of plastic enter aquatic ecosystems annually, prompting governments to incentivize bio-based alternatives. In response, the European Union’s Circular Economy Action Plan mandates that all packaging be reusable or recyclable by 2030, accelerating the adoption of starch-based materials. Furthermore, companies like TotalEnergies Corbion and NatureWorks have scaled production of starch-PLA composites, with global bioplastic production capacity expected to reach 2.8 million metric tons by 2026, as per European Bioplastics.

MARKET RESTRAINTS

Volatility in Raw Material Supply Due to Climate Variability

The stability of corn starch production is increasingly threatened by climate-induced disruptions in corn cultivation. Erratic weather patterns, prolonged droughts, and unseasonal flooding have impaired crop yields in key producing regions. These climatic instabilities not only constrain raw material access but also amplify price volatility, undermining long-term planning for starch processors dependent on consistent grain supply.

Intense Competition from Alternative Starch Sources

Corn starch faces mounting competition from non-corn starches such as tapioca, potato, and cassava, particularly in specialty food and industrial applications. These alternatives often offer superior clarity, freeze-thaw stability, or hypoallergenic profiles, appealing to niche markets. According to the International Center for Tropical Agriculture (CIAT), global cassava production exceeded 300 million metric tons in 2023, with Thailand and Nigeria expanding industrial starch extraction capacities. Additionally, tapioca starch imports into the U.S. grew between 2022 and 2023, driven by demand in gluten-free and clean-label products. This diversification of starch sources pressures corn starch producers to innovate or risk market share erosion in high-value segments.

MARKET OPPORTUNITIES

Integration into Controlled-Release Pharmaceutical Systems

Corn starch is gaining prominence in pharmaceutical formulations, particularly in controlled-release drug delivery systems and tablet disintegration technologies. Its biocompatibility, low cost, and natural origin make it ideal for oral solid dosage forms. Furthermore, as per the U.S. Pharmacopeia, corn starch meets stringent purity standards for use in pediatric and geriatric medications, reinforcing its regulatory acceptance. Hence, the role of corn starch as a functional excipient is poised for accelerated integration in cost-effective, scalable drug manufacturing.

Adoption in Textile Sizing and Finishing Processes

The textile industry is increasingly revisiting corn starch as an eco-friendly alternative to synthetic sizing agents in yarn preparation. Conventional polyvinyl alcohol (PVA) binders are non-biodegradable and contribute to water pollution during desizing. In contrast, corn starch offers biodegradability and reduced environmental impact. Also, starch consumption in Chinese textile mills rose in 2023, driven by national green manufacturing mandates. Additionally, enzyme-treated corn starch improves warp yarn strength while reducing waterborne effluent toxicity. This shift aligns with global sustainability benchmarks, offering corn starch producers a high-growth avenue in industrial non-food sectors.

MARKET CHALLENGES

Regulatory Hurdles in Genetically Modified (GM) Corn Utilization

The use of genetically modified corn in starch production faces stringent regulatory scrutiny in several major markets, particularly in the European Union and parts of Africa and Asia. As per the European Food Safety Authority, all starch derived from GM corn must undergo rigorous traceability and labeling procedures, increasing compliance costs for exporters. This regulatory fragmentation forces manufacturers to maintain segregated supply chains for GM and non-GM starch, raising operational complexity. As consumer skepticism persists in key regions, companies face growing pressure to source non-GM corn, constraining scalability and cost-efficiency.

Technological Limitations in Functional Modification

Despite advancements, the modification of corn starch to meet specialized industrial demands remains constrained by technological and biochemical limitations. Native corn starch exhibits poor performance under extreme pH, high shear, or freezing conditions, necessitating chemical or enzymatic modification. Furthermore, research from the Journal of Cereal Science indicates that cross-linking and esterification processes, while enhancing functionality, can generate residual byproducts that trigger regulatory concerns in food-grade applications. These technical barriers hinder the development of high-performance starches for advanced applications in 3D food printing, biodegradable electronics, or injectable pharmaceuticals, limiting the innovation velocity within the sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.3% |

| Segments Covered | By Product, Application, And Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Archer Daniels Midland Company, Associated British Foods plc, Beteiligungs AG, Cargill, Inc., Ingredion Incorporated, Tate & Lyle PLC, Roquette Frères S.A., Hodgson Mill, ACH Food Companies and Global Bio-Chem Technology Group Company Limited. |

SEGMENTAL ANALYSIS

By Product Insights

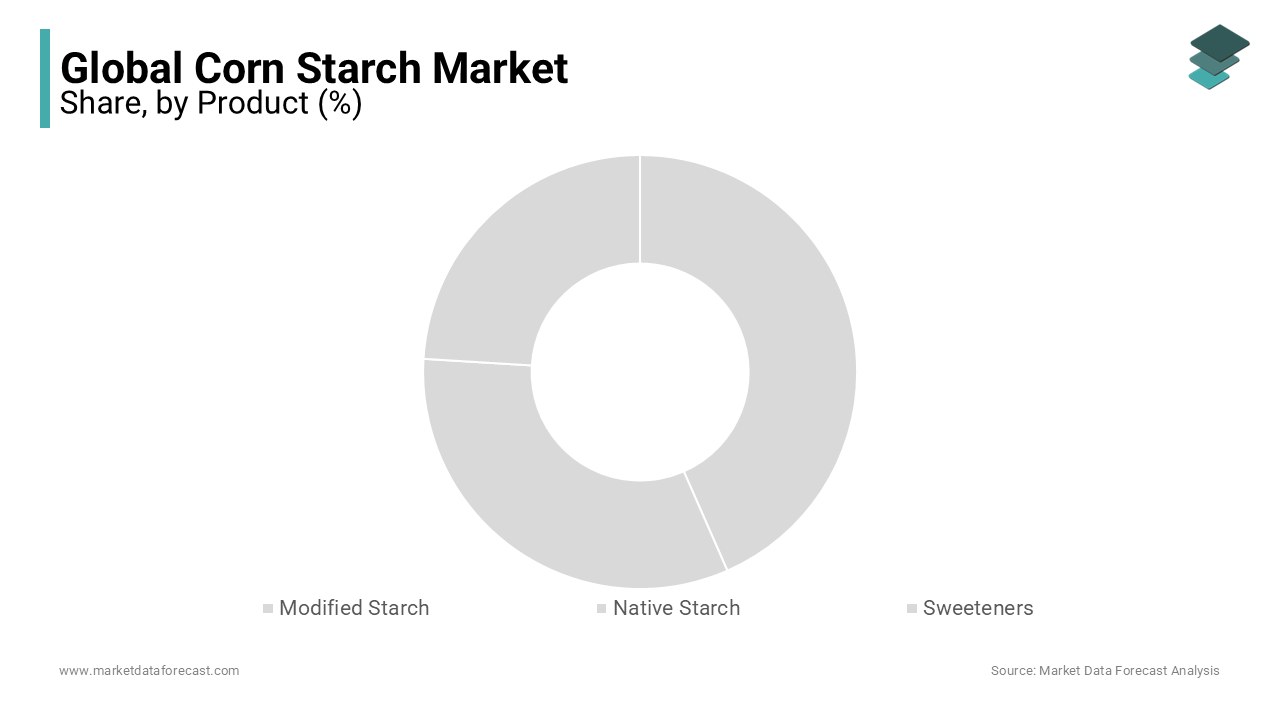

The modified starch segment dominated the global corn starch product by commanding an estimated 55.2% of the market in 2025. Its supremacy is supported by enhanced functional properties such as improved thermal stability, shear resistance, and freeze-thaw resilience, which are indispensable in processed food systems. The food processing industry, particularly in ready-to-eat and convenience foods, relies heavily on modified starch for texture stabilization and shelf-life extension. Additionally, the growing demand for frozen meals has amplified reliance on modified starch due to its ability to prevent syneresis during repeated freezing cycles. This functional superiority, coupled with scalability in production, solidifies its leadership across food, pharmaceutical, and paper sectors.

The corn-based sweeteners segment are expanding at a CAGR 6.8% from 2026 to 2034 and is making this the fastest-growing product segment within the corn starch market. The primary catalyst is the cost-efficiency and fermentability of corn sweeteners in beverage manufacturing, particularly in emerging economies where sugar substitution is economically driven. In India, soft drink producers have shifted to glucose-fructose blends, reducing sweetener costs. Additionally, the versatility of corn sweeteners in bakery and dairy applications, where they enhance browning, moisture retention, and flavour, is accelerating adoption. Hence, the segment’s trajectory is reinforced by both industrial utility and feedstock availability.

By Application Insights

The food and beverages segment accounted for 63.6% of global corn starch consumption in 2025. This dominance is anchored in the ingredient’s multifunctionality—serving as a thickener, stabilizer, and gelling agent across dairy, bakery, confectionery, and savory products. The rise of ultra-processed foods has intensified starch demand, according to the Pan American Health Organization. Additionally, clean-label trends are favoring corn starch over synthetic additives. The sector’s scale is further amplified by its integration into plant-based meat and dairy analogs, where starch provides structural integrity, reinforcing its centrality in modern food systems.

The paper and board application segment is projected to grow at a CAGR of 5.4% through 2030, outpacing other end-use sectors, as forecasted by the World Resources Institute. This acceleration is driven by the resurgence of paper-based packaging as a sustainable alternative to plastic, particularly in e-commerce and food service. Corn starch enhances paper strength, printability, and water resistance, reducing the need for synthetic resins. Moreover, enzyme-modified corn starch has improved adhesion efficiency, cutting application waste. These functional and environmental advantages are propelling starch into a pivotal role in the circular packaging economy.

REGIONAL ANALYSIS

Asia Pacific Corn Starch Market Insights

Asia Pacific stood as the preeminent regional hub in the global corn starch market by capturing 42.7% of total share in 2025. The region’s position is underpinned by robust industrialization, expanding food processing infrastructure, and rising domestic consumption. The proliferation of instant foods, monosodium glutamate (MSG) manufacturing, and pharmaceutical excipient demand has intensified starch utilization. Additionally, India’s ethanol blending program, which mandates 20% ethanol in gasoline by 2026, has redirected corn toward sweetener and fermentation industries, as stated by the Ministry of Petroleum and Natural Gas. With Southeast Asian nations like Thailand and Vietnam expanding starch export capacities, the region’s dominance is further entrenched by integrated agro-industrial ecosystems and government-backed biorefinery initiatives.

North America Corn Starch Market Insights

North America maintains a commanding presence in the corn starch landscape. The region’s strength is rooted in its highly advanced bioprocessing infrastructure and dominance in genetically optimized corn cultivation. The United States produces over 90 million metric tons of corn annually. Major players like ADM, Cargill, and Ingredion operate large-scale biorefineries in the Midwest, achieving economies of scale that drive global export competitiveness. Moreover, the FDA’s recognition of high-purity corn starch as GRAS (Generally Recognized as Safe) has facilitated its integration into pharmaceutical and infant nutrition products.

Europe Corn Starch Market Insights

Europe commands a significant share of the global corn starch market and is positioning it as a mature yet innovation-driven region. While native corn cultivation is limited, countries like France, Hungary, and Romania sustain a robust starch processing industry through efficient import and refining mechanisms. The EU’s stringent sustainability mandates, particularly under the Green Deal, have spurred investment in enzyme-modified starches for biodegradable packaging and textile applications. With Germany and the Netherlands serving as key distribution and R&D centers, Europe’s market status reflects a balance between regulatory rigor and functional innovation.

Latin America Corn Starch Market Insights

Latin America holds a notable share of the global corn starch market, with Brazil emerging as the regional epicenter. The country’s dual advantage of abundant arable land and advanced agro-industrial capacity enables cost-effective starch production. The expansion of the poultry and swine sectors, where corn starch is used in feed pellet binding, has further stimulated demand. With Argentina and Colombia developing localized wet-milling facilities, the region is gradually reducing import dependency, signaling a shift toward self-sufficiency in starch-based value chains.

Africa Corn Starch Market Insights

Africa accounts for small share of the global corn starch market, but exhibits nascent yet transformative potential. South Africa leads the continent in starch processing. The primary driver is urbanization and the rise of packaged food consumption, particularly in Nigeria and Kenya. Additionally, initiatives like Nigeria’s Presidential Fertilizer Initiative have boosted corn yields, improving feedstock availability for industrial use. However, infrastructure gaps in milling and cold chain logistics remain constraints. With the African Continental Free Trade Area (AfCFTA) promoting regional agro-industrial integration, the stage is set for scaled starch production, particularly in non-food applications like pharmaceuticals and adhesives.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a significant role in the global corn starch market include Archer Daniels Midland Company, Associated British Foods plc, Beteiligungs AG, Cargill, Inc., Ingredion Incorporated, Tate & Lyle PLC, Roquette Frères S.A., Hodgson Mill, ACH Food Companies and Global Bio-Chem Technology Group Company Limited.

The competition in the corn starch market is intensifying as global players strive to differentiate through technological innovation and sustainable operations. While a few multinational corporations dominate production and R&D, regional manufacturers are gaining ground by offering cost-effective, locally adapted solutions. The market is characterized by continuous product refinement, with companies focusing on clean-label compliance, functional performance, and environmental impact. Mergers, joint ventures, and capacity expansions are common as firms seek to strengthen supply chain resilience. Regulatory divergence across regions, particularly regarding genetically modified corn and biodegradable materials, adds complexity to global competition. Additionally, the rise of alternative starch sources like cassava and potato is pressuring corn starch producers to enhance efficiency and versatility. Ultimately, competitive advantage is shifting toward those who integrate sustainability, digital traceability, and application-specific customization into their core offerings.

TOP PLAYERS IN THE MARKET

Ingredion Incorporated

Ingredion has established a formidable presence in the Asia Pacific corn starch market through its localized innovation centers and strategic partnerships with regional food manufacturers. The company operates advanced processing facilities in Indonesia, India, and South Korea, enabling rapid customization of native and modified starches for traditional and modern food applications. The company also expanded its enzyme-modified starch portfolio in China to meet the needs of low-sugar dairy products. Ingredion’s collaboration with Indian startups in the alternative protein space has strengthened its foothold in emerging sectors. Its investment in sustainable sourcing programs across the region further aligns with Asia Pacific’s evolving regulatory and consumer expectations, reinforcing its technological leadership.

Cargill

Cargill plays a pivotal role in the Asia Pacific corn starch landscape by integrating vertically across the value chain, from grain procurement to high-performance ingredient solutions. The company operates one of the largest wet-milling facilities in Malaysia, supplying starch to food, paper, and pharmaceutical industries across ASEAN nations. It also partnered with Japanese beverage producers to optimize corn-based sweeteners for reduced-calorie drinks. Cargill’s digital grain sourcing platform in India has enhanced supply chain transparency and reduced procurement lead times. Furthermore, its collaboration with Chinese packaging firms to develop starch-based biodegradable films underscores its commitment to sustainability. These initiatives reflect Cargill’s deep market integration and adaptive R&D focus in the region.

ADM (Archer Daniels Midland Company)

ADM has significantly expanded its influence in the Asia Pacific corn starch market by leveraging its global biorefining expertise and forging alliances with regional food technologists. The company operates a state-of-the-art innovation hub in Singapore, dedicated to developing starch solutions for Asian palates and processing conditions. It also introduced a gluten-free baking aid in India using modified corn starch, targeting the growing health-conscious consumer base. ADM strengthened its supply reliability by securing long-term corn supply agreements with Australian and Thai agribusinesses. Additionally, its investment in fermentation-derived functional starches for probiotic beverages highlights its forward-looking approach. These actions demonstrate ADM’s strategic focus on technical differentiation and sustainability in one of the world’s most dynamic starch markets.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the corn starch market are deploying a combination of vertical integration, product innovation, and sustainability-driven initiatives to consolidate their positions. Companies are investing heavily in biorefinery expansions to enhance co-product utilization and reduce waste. Strategic collaborations with food tech startups are enabling rapid development of clean-label and plant-based formulations. Geographic diversification, particularly into high-growth Asian and Latin American markets, is a common tactic to mitigate regional volatility. Firms are also adopting digital supply chain platforms to improve traceability and responsiveness. Moreover, research into enzyme-modified and thermally stable starch variants is accelerating to meet evolving industrial demands. Sustainability certifications and carbon-neutral processing claims are increasingly used as competitive differentiators. These multifaceted strategies reflect a shift from commodity-based competition to value-added, technology-led market positioning.

RECENT HAPPENINGS IN THE MARKET

- In April 2025, Ingredion opened a new application development center in Jakarta, Indonesia, focused on creating native and modified starch solutions for Southeast Asian food manufacturers, enhancing its regional innovation capabilities and accelerating customer-specific product development in the Corn Starch Market.

- In January 2023, Cargill launched a bio-based, fully compostable packaging film in Vietnam, formulated with high-purity corn starch and polylactic acid, targeting the food service industry and reinforcing its leadership in sustainable material solutions in the Corn Starch Market.

- In September 2023, ADM partnered with a Singapore-based alternative protein startup to co-develop a texturized plant-based seafood product using enzyme-modified corn starch, expanding its footprint in the rapidly growing Asian plant-based food sector in the Corn Starch Market.

- In June 2022, Tate & Lyle expanded its modified starch production capacity at its facility in South Korea to meet rising demand from instant noodle and dairy producers, strengthening its supply reliability and technical service support in Northeast Asia in the Corn Starch Market.

- In March 2025, Roquette inaugurated a new enzyme optimization unit in Thailand to enhance the functional properties of native corn starch for use in clean-label bakery and dairy applications, improving product performance and supporting regional customers in the Corn Starch Market.

MARKET SEGMENTATION

This research report on the global corn starch market has been segmented and sub-segmented based on product, application, & region.

By Product

- Modified Starch

- Native Starch

- Sweeteners

By Application

- Animal Feed

- Food and Beverages

- Paper and Board

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors are driving the growth of the Corn Starch Market?

Increasing demand for convenience foods, bakery products, and bio-based industrial applications is driving the Corn Starch Market growth.

2. Which region dominates the global Corn Starch Market?

North America leads the Corn Starch Market, while Asia Pacific is experiencing the fastest growth due to rising food and beverage consumption.

3. What are the key applications of the Corn Starch Market?

The Corn Starch Market is widely used in food processing, sweeteners, paper manufacturing, textiles, pharmaceuticals, and adhesives.

4. What role does modified starch play in the Corn Starch Market?

Modified starch enhances texture, stability, and shelf life, making it a crucial segment in the Corn Starch Market.

5. Which end-user industries contribute most to the Corn Starch Market?

The food and beverage, textile, pharmaceutical, and paper industries are the major consumers of the Corn Starch Market.

6. What are the key challenges in the Corn Starch Market?

Price volatility of raw materials and competition from alternative starch sources are key challenges in the Corn Starch Market.

7. Who are the leading players in the Corn Starch Market?

Key players in the Corn Starch Market include Cargill, Archer Daniels Midland (ADM), Ingredion Incorporated, and Tate & Lyle.

8. What trends are shaping the future of the Corn Starch Market?

Trends in the Corn Starch Market include growing demand for clean-label, non-GMO, and bio-based starch products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com