Global Corn Seeds Market Size, Share, Trends and Growth Forecasts Report, Segmented By Type (Baby Corn, Field Corn, Sweet Corn, Pop Corn), End Products (Animal Feed, Corn Flour or meal, Corn Starch, Corn Syrup), And By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Forecast 2026 to 2034

Market Size, 2025

$33.01 BnMarket Estimate, 2026

$35.42 BnMarket Forecast, 2034

$62.24 BnCAGR, 2026–2034

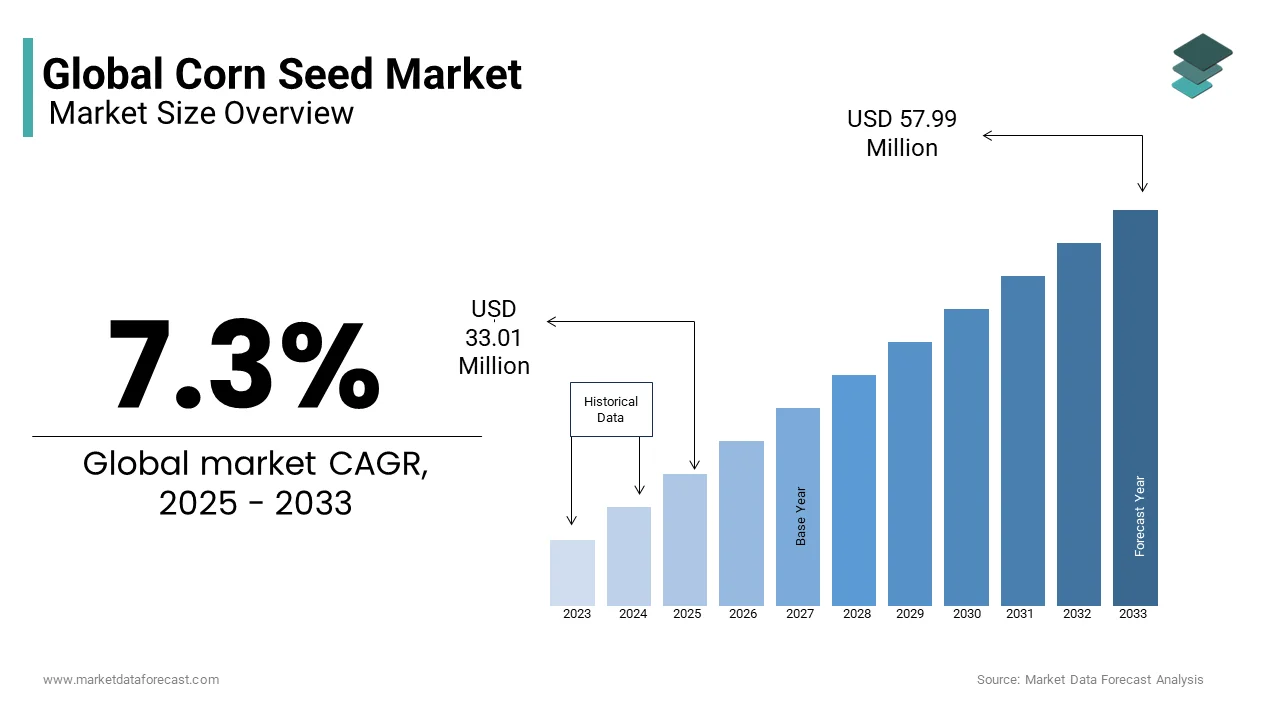

7.3%Global Corn Seeds Market Size

The global corn seeds market was valued at USD 33.01 billion in 2025 and is anticipated to reach USD 35.42 billion in 2026 from USD 62.24 billion by 2034, growing at a CAGR of 7.3% from 2026 to 2034.

Corn seeds refer to the genetically selected or engineered kernels used for cultivating Zea mays, a staple cereal crop critical for food, feed, biofuel, and industrial applications. These seeds range from conventional open-pollinated varieties to advanced hybrids and biotech traits engineered for herbicide tolerance, insect resistance, and climate resilience. The global corn seeds market is fundamentally shaped by agronomic performance, regulatory frameworks governing genetically modified organisms, and regional cropping patterns. According to the Food and Agriculture Organization, corn is cultivated on over 200 million hectares worldwide, making it the most widely grown cereal by area. As per the International Maize and Wheat Improvement Center, maize provides at least 20 percent of the dietary calories for over 900 million people in sub-Saharan Africa and Latin America. The U.S. Department of Agriculture estimates that 92 percent of corn planted in the United States in 2024 was genetically modified, primarily for dual traits combining insect protection and herbicide tolerance. These biological and policy dimensions underscore that corn seeds are not mere agricultural inputs but strategic instruments of food security, energy policy, and rural livelihoods across diverse geographies.

MARKET DRIVERS

Expansion of Biofuel Mandates Driving Feedstock Demand

Government biofuel policies, particularly ethanol blending requirements, are a primary driver of corn seed demand by directly linking agricultural output to energy markets. According to the U.S. Energy Information Administration, the United States consumed 15.6 billion gallons of fuel ethanol in 2024, requiring approximately 5.4 billion bushels of corn—nearly 40 percent of the nation’s total production. Brazil’s RenovaBio program mandates a 27 percent ethanol blend in gasoline by 2025, significantly increasing domestic corn ethanol capacity and driving hybrid seed adoption in the Center West region. Similarly, the European Union’s Renewable Energy Directive II requires 14 percent of transport energy to come from renewable sources by 2030, spurring investment in advanced biofuels, including corn-based ethanol, in Eastern Europe. China’s National Development and Reform Commission has approved 12 new corn ethanol plants since 2022, projected to consume 18 million metric tons of corn annually. This policy anchored demand creates a stablelarge-scalele market for high-yield corn hybrids, insulating seed companies from pure food market volatility and reinforcing corn’s dual role as both food and fuel feedstock.

Adoption of Climate Resilient Hybrid Varieties in Vulnerable Regions

Rising climate volatility is accelerating the adoption of drought-tolerant and heat-resilient corn hybrids, particularly in sub-Saharan Africa and South Asia, where rainfall unpredictability threatens yields. According to the Intergovernmental Panel on Climate Change, maize yields in Africa could decline by up to 40 percent by 2050 under high emission scenarios without adaptive measures. In response, the Water Efficient Maize for Africa partnership has deployed drought-tolerant hybrids across 12 countries, benefiting over 8 million smallholder farmers with yield advantages of 20 to 35 percent under water stress, as documented by the International Institute of Tropical Agriculture. India’s National Agricultural Innovation Project reports that adoption of short-duration, heat-tolerant hybrids increased by 60 percent between 2020 and 2024 in states like Rajasthan and Maharashtra. Similarly, the Philippines’ Department of Agriculture distributed 150,000 bags of flood-tolerant corn seeds in 2023 following typhoon-induced crop losses. These context-specific innovations transform corn seeds from generic inputs into climate adaptation tools, driving demand through resilience rather than just productivity.

MARKET RESTRAINTS

Stringent Biosafety Regulations Limiting Biotech Seed Access

Divergent and often restrictive regulatory frameworks for genetically modified corn seeds impede market access and innovation diffusion, particularly in developing economies. According to the International Service for the Acquisition of Agri-biotech Applications, only 32 countries approved GM corn for cultivation or import in 2024, leaving major potential markets like Kenya and Indonesia in regulatory limbo despite demonstrated agronomic benefits. The European Union’s de facto moratorium on new GM crop approvals—despite scientific endorsement by the European Food Safety Authority—has stifled investment in trait development for European conditions. In Mexico, a 2023 Supreme Court ruling upheld a ban on GM corn for human consumption, affecting over 28 million hectares of potential planting area and forcing seed companies to maintain separate non-GM supply chains. These regulatory barriers increase compliance costs, delay product launches, and fragment global breeding pipelines, ultimately limiting farmer access to advanced traits that could enhance yield stability and reduce pesticide use in vulnerable regions.

Seed Saving Practices Among Smallholder Farmers

Persistent seed saving and informal exchange among smallholder farmers in Africa and Asia constrain commercial seed market penetration despite the availability of higher-yielding hybrids. According to the Alliance for a Green Revolution in Africa, over 80 percent of small-scale maize farmers in sub-Saharan Africa replant grain from previous harvests rather than purchasing certified seed annually. This practice stems from limited cash liquidity, weak extension services, and cultural preference for locally adapted landraces. In India, the National Sample Survey Office estimates that only 35 percent of mathe ize area is planted with certified hybrid seed, with the remainder using farm-saved or uncertified sources. While open-pollinated varieties can be saved, hybrids lose vigor in subsequent generations, leading to a yield drag of 15 to 30 percent, as confirmed by the Indian Council of Agricultural Research. Until formal seed systems address affordability, accessibility, and trust through localized distribution and education, a significant portion of global corn area will remain outside the commercial seed economy, limiting both farmer productivity and industry growth.

MARKET OPPORTUNITIES

Gene Editing Technologies Enabling Non-GMO Trait Development

The emergence of precise gene editing tools like CRISPR Cas9 is unlocking new opportunities to develop high-performance corn seeds without triggering stringent GMO regulations in sensitive markets. According to the U.S. Department of Agriculture, over 20 gene-edited corn lines have been granted non-regulated status since 2020, including varieties with improved nitrogen use efficiency and waxy starch profiles. In Japan, the Ministry of Health, Labour and Welfare approved the first CRISPR-edited corn for food use in 2023, paving the way for commercial cultivation. Companies like Pairwise and Benson Hill are leveraging gene editing to develop non-browning, high fiber, or drought-resilient corn without foreign DNA insertion, enabling faster regulatory approval and consumer acceptance. The European Commission’s 2024 proposal to exempt certain gene-edited crops from GMO rules could open a 20 billion euro market for next-generation seeds. This technological pivot allows seed developers to bypass decades of GMO controversy while delivering agronomic and nutritional benefits, creating a parallel innovation track with lower regulatory friction.

Integration of Digital Agriculture and Precision Planting

The convergence of corn seed technology with digital farming platforms is creating new value propositions through data-driven agronomy and variable rate planting. According to the American Farm Bureau Federation, 68 percent of U.S. corn growers used precision planting equipment in 2024, which requires seed lots with uniform size and germination to optimize singulation. Companies like Corteva and Bayer now offer seed prescriptions that match hybrid genetics to soil type, moisture, and historical yield data via platforms such as Granular and Climate FieldView. In Brazil, John Deere’s ExactEmerge planters paired with proprietary seed enable planting speeds of 10 miles per hour while maintaining spacing accuracy, boosting effective yield by 5 to 8 percent. Additionally, blockchain traceability from seed to harvest is being piloted in the European Union to verify non-GM or organic status for premium markets. This integration transforms corn seeds from static inputs into dynamic components of algorithmic farming systems, enhancing performance while generating recurring data revenue for seed companies.

MARKET CHALLENGES

Intellectual Property Enforcement and Seed Piracy

Weak enforcement of plant variety protection laws in key corn-producing regions enables widespread seed piracy and unauthorized propagation, undermining innovation incentives and revenue integrity. According to the International Seed Federation, counterfeit or illegally multiplied corn seed accounts for an estimated 25 to 30 percent of sales in countries like Pakistan, Vietnam, and parts of Eastern Europe. In Argentina, where hybrid corn seed is not protected under plant breeders’ rights, companies lose an estimated 120 million dollars annually to illegal seed multiplication, as reported by the Argentine Seed Association. Even in regulated markets, bag repackaging and trait mimicry erode brand value; the U.S. Department of Justice prosecuted three firms in 2024 for selling mislabeled corn seed containing unlicensed biotech traits. Without robust legal recourse and supply chain authentication—such as DNA fingerprinting or digital tagging—breeders face diminishing returns on R&D investment, particularly for traits targeting smallholder markets where margins are already thin.

Soil Degradation and Nutrient Depletion: Reducing Yield Response

Widespread soil health deterioration is diminishing the yield response to even the most advanced corn hybrids, creating a ceiling on productivity gains regardless of seed quality. According to the Food and Agriculture Organization, 33 percent of global soils are degraded due to erosion, compaction, and nutrient mining, with maize systems particularly affected due to continuous monoculture. In the U.S. Corn Belt, long-term studies by Iowa State University show that soil organic matter has declined by 50 percent since the 1950s, reducing water holding capacity and nitrogen mineralization. In sub-Saharan Africa, the African Union estimates that nutrient depletion costs the region 4 billion dollars annually in lost maize productivity. While seed companies promote nutrient-efficient hybrids, their efficacy is limited without concurrent soil restoration. This agronomic bottleneck shifts the performance bottleneck from genetics to land management, requiring integrated solutions that seed alone cannot deliver and complicating value communication to farmers expecting guaranteed yield increases.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.3% |

| Segments Covered | By Type, End Product, And Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Monsanto, DuPont Pioneer, Bayer CropScience, and Hefei Fengbao. Some other key players in the market include Pacific Seeds, Syngenta, Nuziweedu Seeds, China National Seeds, and DLF Trifolium. |

SEGMENTAL ANALYSIS

By Type Insights

Market Share Distribution and Dominant Segment

Field Corn dominates the global corn seeds market with a share of 76 percent, as reported by the International Maize and Wheat Improvement Center in 2025. This overwhelming prevalence stems from its dual role as the primary feedstock for animal protein production and industrial biofuel processing. According to the U.S. Department of Agriculture, over 90 percent of the 377 million metric tons of corn produced globally in 2024 was field corn, cultivated specifically for its high starch content and yield potential. In the United States alone, 5.4 billion bushels of field corn were processed into ethanol, fulfilling 40 percent of national gasoline blending mandates under the Renewable Fuel Standard. Similarly, Brazil’s expanding poultry and pork sectors consumed 42 million metric tons of field corn as feed in 2024, as documented by the Brazilian Animal Protein Association. The segment’s scale is further amplified by its compatibility with large-scale mechanized farming and genetically modified trait platforms, which enhance herbicide tolerance and insect resistance across millions of hectares. Unlike specialty corn types, field corn benefits from integrated value chains linking seed, agronomy, logistics, and end-use markets, ensuring consistent demand regardless of consumer food trends.

Fastest Growing Segment: Baby Corn

The Baby Corn segment is projected to grow at a compound annual growth rate of 11.3 percent through 2030, according to the Food and Agriculture Organization. This acceleration is driven by rising global demand for ready-to-eat vegetables, plant-based diets, and export-oriented horticulture in Asia. Unlike other corn types harvested at maturity, baby corn is picked 2 to 3 days after silking, requiring specialized short-duration hybrids and precise agronomic timing. Thailand, the world’s largest exporter, shipped 120,000 metric tons of canned and fresh baby corn in 2024, primarily to the European Union and Japan, as per the Thai Ministry of Commerce. In India, the National Horticulture Board reports a 45 percent increase in baby corn cultivation since 2021, supported by contract farming with food processing companies like ITC and Nestlé. Urban consumers in China and South Korea now favor baby corn in salads and stir fries, with retail sales growing by 18 percent annually, according to NielsenIQ. Additionally, its status as aanon-GMOO, labor-intensive crop makes it ideal for smallholder inclusion in high-value supply chains, transforming it from a niche vegetable into a strategic diversification tool for farmers in densely populated regions.

By End Product Insights

Market Share Distribution and Dominant Segment

Animal Feed accounts for the largest end product segment with 58 percent of global corn utilization, as per data from the International Feed Industry Federation in 2025. This dominance reflects corn’s irreplaceable role as the primary energy source in poultry, swine, and cattle rations due to its high metabolizable energy and digestible starch content. According to the U.S. Grains Council, one metric ton of corn provides the caloric equivalent of 1.4 tons of barley or 1.6 tons of sorghum in feed formulations, making it the most cost-efficient cereal globally. In China, the world’s largest pork producer, 185 million metric tons of corn were used in compound feed in 2024, representing 62 percent of national corn consumption as reported by the Chinese Ministry of Agriculture. Similarly, Brazil’s poultry industry, which exported 4.8 million metric tons of chicken in 2024, relies on locally grown corn for 70 percent of feed energy, per the Brazilian Animal Protein Association. The segment’s scale is further reinforced by vertical integration in meat production, where feed mills, hatcheries, and processing plants operate under unified supply chains, ensuring stable, high-volume corn demand independent of direct human consumption trends.

Fastest Growing Segment: Corn Starch

The Corn Starch end product segment is expanding at a CAGR of 9.7 percent, according to the International Starch Institute. This growth is fueled by its expanding use in biodegradable packaging, pharmaceutical excipients, and clean-label food formulations. Unlike synthetic polymers, corn starch is renewable, compostable, and non-toxic, aligning with global plastic reduction mandates. The European Union’s Single Use Plastics Directive has spurred investment in starch-based bioplastics, with production capacity in Germany and the Netherlands growing by 25 percent in 2024 alone. In the food industry, corn starch is replacing modified additives in response to consumer demand for simple ingredients; a 2024 survey found that 63 percent of new product launches in sauces and soups highlighted “corn starch” as a clean-label thickener. Additionally, the pharmaceutical sector uses over 200,000 metric tons annually as a binder and disintegrant in tablets, with demand rising due to generic drug manufacturing in India and China. As circular economy principles gain regulatory traction, corn starch is transitioning from a commodity ingredient to a strategic biomaterial.

REGIONAL ANALYSIS

North America Market Analysis

North America holds the leading position in the global corn seeds market, driven by advanced biotechnology adoption, integrated agribusiness, and policy-driven ethanol demand. The United States alone accounts for over 35 percent of global corn production, with 92 percent of planted area using genetically modified hybrids, as per the U.S. Department of Agriculture. Iowa and Illinois, the top-producing states, average yields exceeding 200 bushels per acre through precision agriculture and trait-stacked seeds. Canada complements this with specialty corn production in Ontario for food and feed. The Renewable Fuel Standard mandates 15 billion gallons of corn ethanol annually, creating a stable outlet for field corn. Additionally, companies like Corteva and Bayer operate major seed research centers in the Corn Belt, continuously releasing hybrids with enhanced nitrogen use efficiency and drought tolerance. This synergy of policy, technology, and infrastructure ensures North America’s continued dominance in both volume and innovation.

Latin America Market Analysis

Latin America is a high-growth region anchored by Brazil’s emergence as the world’s second-largest corn producer and exporter. Brazil harvested 135 million metric tons in 2024, with the Center West region—particularly Mato Grosso—accounting for 60 percent of output, according to CONAB, the national supply agency. The country’s safrinha (second crop) system, planted after soybeans, has doubled corn area since 2015, enabled by short-duration, disease-resistant hybrids. Argentina contributes 55 million metric tons annually, primarily for domestic feed and export to neighboring countries. Both nations have embraced biotech seeds; Brazil approved 12 new GM corn events in 2024 alone. Government support through credit programs like Brazil’s ABC+ Plan further accelerates the adoption of high-yielding seeds. As infrastructure improves and double-cropping expands, Latin America is poised to challenge U.S. export dominance, making it the most dynamic corn seed market globally.

Asia Pacific Market Analysis

Asia Pacific is characterized by diverse production systems ranging from smallholder farming to industrial agribusiness. China leads regional demand, consuming 280 million metric tons of corn in 2024, primarily for feed in its massive pork industry, as per the National Bureau of Statistics. However, domestic production meets only 85 percent of needs, driving seed innovation to boost yields. India focuses on hybrid adoption in states like Karnataka and Maharashtra, where yields have risen to 3.2 tons per hectare from 2.1 in 2015, according to the Indian Council of Agricultural Research. Southeast Asia is expanding specialty corn; Thailand and Vietnam are top baby corn exporters, while the Philippines promotes white corn for human consumption. Government initiatives like China’s Seed Industry Revitalization Plan and India’s National Food Security Mission provide subsidies for quality seeds. The region’s blend of food security pressure and export opportunity sustains robust seed market growth.

Europe Market Analysis

Europe maintains a stable but constrained corn seed market due to strict regulations on genetically modified crops and emphasis on sustainability. The European Union produced 58 million metric tons of corn in 2024, primarily in France, Romania, and Hungary, as per Eurostat. While GM corn is banned in most member states, conventional hybrids with drought tolerance and early maturity are in high demand due to climate volatility. France leads in seed innovation, with companies like Limagrain developing non-GM hybrids for organic and integrated farming. The Common Agricultural Policy incentivizes crop diversification, indirectly supporting corn in rotation systems. Additionally, the EU imports over 15 million metric tons of feed corn annually, mostly from Ukraine and Brazil, reducing pressure for domestic yield expansion. Nevertheless, rising interest in bioplastics and bioethanol is creating niche demand for high starch varieties, ensuring the continued relevance of corn seeds in the European bioeconomy.

Middle East and Africa Market Analysis

The Middle East and Africa region is an emerging market shaped by food security imperatives and climate adaptation needs. South Africa is the largest producer, harvesting 15 million metric tons in 2024 despite drought, using drought-tolerant hybrids from Pannar and Corteva. Nigeria and Ethiopia are expanding their area through government seed subsidy programs; Nigeria’s National Agricultural Seeds Council distributed 80,000 metric tons of certified maize seed in 2024. Egypt imports over 9 million metric tons annually for feed, driving interest in local production. According to the African Union, maize provides 30 percent of dietary calories in sub-Saharan Africa, yet average yields remain below 2 tons per hectare due to limited access to improved seeds. Initiatives like the Water Efficient Maize for Africa partnership have reached 8 million farmers with stress-tolerant varieties. As urbanization increases demand for poultry and processed foods, the region’s corn seed market is set for disproportionate growth driven by both subsistence and commercial farming.

COMPETITIVE LANDSCAPE

The corn seeds market is highly concentrated among a few multinational agribusinesses that compete on genetic performance, trait technology, and digital integration. Corteva, Bayer, and Syngenta dominate through extensive R&D networks, global breeding pipelines, and proprietary trait platforms protected by robust intellectual property. Competition is intense in major producing regions like the U.S. Corn Belt, Brazil’s Cerrado, and China’s Northeast Plain, where yield differentials of even 3 to 5 percent can determine market leadership. While entry barriers are high due to regulatory costs and breeding infrastructure, regional players like KWS Saat and Pannar Seed maintain strongholds in Europe and Africa through localized adaptation. The rise of gene editing and non-GM trait development is creating new competitive dimensions beyond traditional transgenic approaches. Additionally, competition increasingly extends beyond the field to downstream value chains, including ethanol, feed, and food processing, where seed quality directly impacts industrial efficiency. As climate volatility intensifies, the ability to deliver consistent yield stability under stress is becoming the ultimate differentiator.

KEY MARKET PLAYERS

A few of the market players in the global corn seed market include

- Monsanto

- DuPont Pioneer

- Corteva Agriscience

- Bayer CropScience

- Hefei Fengbao

- Syngenta

- Nuziweedu Seeds

- China National Seeds

- DLF Trifolium

Top Players In The Market

- Corteva Agriscience is a global leader in corn seed innovation, offering a broad portfolio of hybrid and trait-enhanced seeds under brands such as Pioneer and Brevant. The company invests heavily in genomic selection and digital agronomy to develop high-yielding, stress-resilient corn varieties tailored to diverse agroclimatic zones. In 2024, Corteva launched its AcreMax Xtreme insect protection platform in North and South America, combining multiple modes of action against corn rootworm and ear borers. It also expanded its Climate FieldView integration to provide seed-specific planting prescriptions. These initiatives reinforce Corteva’s focus on science-driven solutions that enhance productivity while supporting sustainable intensification across global farming systems.

- Bayer CropScience is a major force in the corn seeds market through its Dekalb and Seminis brands, delivering genetically advanced hybrids with integrated pest and herbicide tolerance traits. The company leverages its digital farming platform, Climate FieldView, to link seed performance data with real-time field analytics. In early 2025, Bayer introduced a new line of short-season corn hybrids for Eastern Europe and Canada, engineered for early maturity and cold tolerance. It also partnered with grain elevators in the U.S. Midwest to create identity-preserved channels for non-GMO and specialty corn. These actions strengthen Bayer’s position as a provider of end-to-end corn solutions that bridge genetics, data, and market access.

- Syngenta Group is a key global player offering corn seeds under the NK and Golden Harvest brands, with a strong presence in North America, Latin America, and Asia. The company emphasizes breeding for climate resilience and resource use efficiency, particularly in water and nitrogen-limited environments. In 2024, Syngenta rolled out its Enogen corn platform in Brazil, featuring alpha amylase trait technology that enhances ethanol yield for biofuel processors. It also launched a digital seed matching tool in India that recommends hybrids based on soil type and monsoon forecasts. These strategies highlight Syngenta’s commitment to aligning seed innovation with both farmer profitability and downstream industrial value chains.

Top Strategies Used By The Key Market Participants

Key players in the corn seeds market prioritize trait stacking to combine insect resistance, herbicide tolerance, and stress resilience in single hybrids. They invest heavily in genomic and gene editing technologies to accelerate breeding cycles and develop non-GMO solutions for regulated markets. Strategic integration with digital agriculture platforms enables data-driven seed recommendations and performance tracking. Companies expand geographically by tailoring hybrids to local growing conditions and regulatory environments. Partnerships with ethanol producers, feed mills, and food processors create premium channels for specialty corn. Emphasis on sustainability includes developing nitrogen-efficient and drought-tolerant varieties. Intellectual property protection through plant variety rights and biotech patents safeguards innovation. These strategies collectively drive differentiation, farmer loyalty, and value chain integration.

RECENT MARKET NEWS

- In February 2024, Corteva Agriscience launched its AcreMax Xtreme insect protection platform for corn in the United States and Brazil, offering enhanced control of corn rootworm and lepidopteran pests through multi-mode of action traits.

- In October 2024, Bayer CropScience introduced a new portfolio of short-season corn hybrids for Eastern Europe and Western Canada, engineered for early maturity and cold soil emergence under its Dekalb brand.

- In March 202,5, Syngenta Group expanded its Enogen amylase trait corn to commercial ethanol producers in Brazil, enabling higher fermentation efficiency and lower processing costs in biofuel facilities.

- On July 2,024, Corteva partnered with major grain cooperatives in Iowa and Illinois to establish identity-preserved supply chains for non-GMO and waxy corn varieties targeting food and industrial markets.

- In January 2025, Bayer integrated its corn hybrid performance database with Climate FieldView to deliver real-time seed selection recommendations based on historical yield maps and soil moisture forecasts.

MARKET SEGMENTATION

This research report on the global corn seed market is segmented and sub-segmented into the following categories.

By Type

- Baby Corn

- Field Corn

- Sweet Corn

- Pop Corn

By End Products

- Animal Feed

- Corn Flour or meal

- Corn Starch

- Corn Syrup

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

what is the current market size of the global corn seeds market?

The global corn seed market was valued at USD 33.01 billion in 2025 at a CAGR of 7.30%

What’s driving growth in the global corn seed market?

Rising global food demand, advancements in biotechnology (like drought-tolerant and pest-resistant traits), and government support for high-yield agriculture are key growth catalysts. Corn’s role in biofuels and animal feed further amplifies market demand.

Which regions lead in corn seed consumption and production?

North America—particularly the U.S.—dominates due to advanced agri-tech and large-scale farming, while Asia-Pacific (led by China and India) shows rapid growth driven by population pressure and modernization of farming practices.

How is GMO technology influencing the corn seed market?

Genetically modified seeds now account for a significant share, offering higher yields, reduced pesticide use, and climate resilience—though regulatory hurdles and consumer skepticism in regions like Europe limit adoption there.

What are the major challenges facing corn seed producers?

Stringent biosafety regulations, intellectual property disputes, climate volatility, and the high R&D costs of developing new hybrids or traits pose significant operational and financial challenges.

Who are the top players in the global corn seed industry?

Industry leaders include Corteva Agriscience, Bayer (via its acquisition of Monsanto), Syngenta (part of ChemChina), and BASF—companies with deep agronomic expertise, global distribution, and robust innovation pipelines in seed genetics.

How is climate change affecting corn seed demand and development?

Unpredictable weather patterns and increasing droughts are accelerating demand for climate-resilient seed varieties, pushing companies to prioritize R&D in heat-tolerant, water-efficient, and early-maturing corn hybrids.

What role does seed treatment play in the corn seed market?

Seed treatments—such as fungicides, insecticides, and biological coatings—are increasingly integrated to protect young plants, boost germination rates, and reduce field-level chemical use, adding value and performance to premium seed products.

Are organic and non-GMO corn seeds gaining market share?

Yes, especially in North America and Europe, where consumer preference for non-GMO and organic food is driving niche but steady growth—though they remain a small fraction compared to conventional and GM segments due to lower yields and higher costs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com