Global Cutting Tools Market Size, Share, Trends & Growth Forecast Report Segmented, By Type of Tools (Indexable Inserts and Solid Round Tools), Material (Exotic Materials, Cubic Boron Nitride, Stainless Steel, Ceramics, High-Speed Steel, Cemented Carbide and Polycrystalline Diamond), Application (Electronics, Automotive, Construction, Aerospace and Defense, Wood, Die & Mold, Oil & Gas and Power Generation), & By Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

Global Cutting Tools Market Size

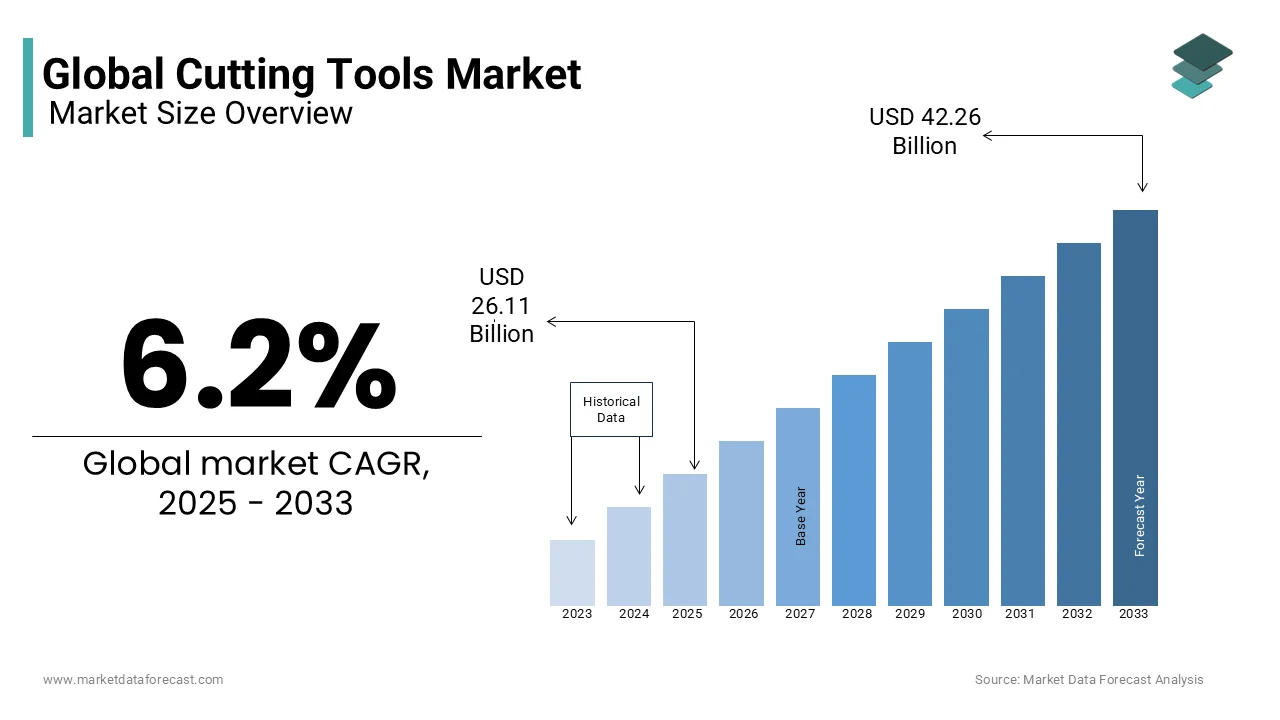

The global cutting tools market was valued at USD 26.11 billion in 2025 and is anticipated to reach USD 27.73 billion in 2026 from USD 44.87 billion by 2034, growing at a CAGR of 6.2% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

The cutting tools market is a diverse array of industrial implements designed to remove material from a workpiece through shear deformation. These essential components include drills, mills, turning tools, and grinding wheels, which are critical for shaping metals, composites, and plastics in manufacturing processes. The efficacy of these tools directly influences production efficiency, surface finish quality, and overall operational costs in sectors such as automotive, aerospace, and general engineering. As industrial automation advances, the demand for high precision and durability in cutting instruments has intensified, driving innovation in materials like carbide, ceramics, and cermets. The European manufacturing landscape, known for its high standards in engineering excellence, relies heavily on advanced cutting solutions to maintain competitive advantage. According to Eurostat, the manufacturing sector in the European Union accounted for approximately 15% of the total value added in the non-financial business economy in recent years, underscoring the foundational role of precise machining capabilities. Furthermore, as per the Federal Ministry for Economic Affairs and Climate Action in Germany, the country alone hosts over 200000 manufacturing enterprises, many of which depend on continuous and efficient metalworking operations. This extensive industrial base creates a sustained requirement for reliable cutting tools that can withstand rigorous production schedules while delivering consistent performance. The integration of digital monitoring systems into tooling solutions further enhances their utility by enabling predictive maintenance and reducing unplanned downtime, thereby solidifying their position as indispensable assets in modern industrial ecosystems.

MARKET DRIVERS

Rising Automotive Production Volumes Drive Demand for High Performance Cutting Solutions

The automotive sector stands as a primary consumer of cutting tools due to the extensive machining required for engine components, transmission systems, and chassis parts, which is a key factor propelling the cutting tools market expansion worldwide. As vehicle manufacturers strive for greater fuel efficiency and reduced emissions, the use of lightweight materials such as aluminum alloys and high strength steel has increased significantly. These materials are notoriously difficult to machine and require specialized cutting tools with superior hardness and heat resistance to ensure precision and tool longevity. According to the European Automobile Manufacturers Association, the European Union produced approximately 12.1 million cars in 2023, reflecting a steady recovery and growth in automotive manufacturing activities. This substantial production volume necessitates a robust supply of cutting tools capable of handling high speed machining operations without compromising on accuracy. The shift towards electric vehicles further amplifies this demand, as the production of electric motors and battery housings involves complex milling and drilling processes that require advanced tooling solutions. As per the International Organization of Motor Vehicle Manufacturers, global vehicle production is expected to continue its upward trajectory, driven by emerging markets and technological advancements. Consequently, cutting tool manufacturers are investing heavily in research and development to create products that meet the stringent requirements of modern automotive assembly lines. The need for reduced cycle times and improved surface finishes in mass production environments ensures that the automotive industry remains a pivotal driver for the cutting tools market, compelling suppliers to innovate continuously.

Expansion of Aerospace Manufacturing Initiatives Fuels Requirement for Precision Machining Tools

The aerospace industry demands exceptional precision and reliability in component manufacturing, making it a significant driver for the cutting tools market. Aircraft structures and engines utilize advanced materials such as titanium alloys, nickel based superalloys, and carbon fiber reinforced polymers, which pose unique challenges during machining processes. These materials exhibit low thermal conductivity and high strength at elevated temperatures, leading to rapid tool wear and increased cutting forces. Therefore, aerospace manufacturers rely on high performance cutting tools made from polycrystalline diamond and cubic boron nitride to achieve the necessary tolerances and surface integrity. According to the Aerospace Industries Association, the global aerospace and defense industry generated revenues exceeding 900 billion USD in recent years, indicating strong investment in new aircraft programs and maintenance services. In Europe, as per the European Association of Aerospace Industries, the sector supports millions of jobs and contributes significantly to the regional economy, with major manufacturing hubs in France, Germany, and the United Kingdom. The introduction of next generation aircraft models, which incorporate higher proportions of composite materials, further intensifies the need for specialized cutting solutions that can handle abrasive textures without delamination. Additionally, the growing emphasis on sustainability in aviation drives the adoption of lightweight designs, which require intricate machining operations. This trend ensures a consistent demand for advanced cutting tools that can deliver high precision and efficiency, thereby supporting the continuous growth and innovation within the aerospace manufacturing sector.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Cost Structures and Profit Margins

The production of cutting tools relies heavily on raw materials such as tungsten, cobalt, and high speed steel, whose prices are subject to significant fluctuations due to geopolitical tensions and supply chain disruptions, which is primarily hampering the cutting tools market growth. Tungsten carbide, a predominant material in cutting tool manufacturing, is particularly vulnerable to market instability as its supply is concentrated in a few countries, notably China. According to the US Geological Survey, global tungsten production was estimated at 78000 metric tons in 2023, with China accounting for more than 80% of this output. This concentration creates a precarious supply environment where any regulatory changes or export restrictions can lead to sudden price spikes. As per the World Bank commodity markets outlook, prices for critical minerals have experienced considerable volatility in recent years, affecting the cost structures of manufacturing industries worldwide. For cutting tool producers, these fluctuations complicate pricing strategies and profit margin management, as passing increased costs to customers may reduce competitiveness. Furthermore, the energy intensive nature of producing cemented carbide adds another layer of cost pressure, especially in regions with high energy prices such as Europe. The European Commission noted that industrial energy prices in the region remained elevated compared to historical averages, impacting the operational expenses of manufacturing facilities. Consequently, manufacturers must navigate these economic uncertainties by optimizing supply chains and exploring alternative materials, yet the inherent dependency on scarce resources remains a persistent restraint that challenges the stability and growth potential of the cutting tools market.

Shortage of Skilled Labor Hinders Optimal Utilization of Advanced Tooling Technologies

The effective deployment of advanced cutting tools requires a workforce proficient in computer numerical control machining, tool selection, and process optimization, which is further hindering the global market growth. However, the manufacturing sector faces a growing shortage of skilled labor, which limits the ability of companies to fully leverage the capabilities of modern cutting technologies. According to the European Centre for the Development of Vocational Training, projections indicate that millions of job vacancies in the European Union will remain unfilled due to skills mismatches and demographic changes. This deficit is particularly acute in specialized machining roles where expertise in handling complex tools and interpreting technical data is essential. As per the National Association of Manufacturers in the United States, the skills gap could result in 2.1 million unfilled jobs by 2030, highlighting a global trend that affects industrial productivity. Without adequately trained personnel, manufacturers may experience increased tool breakage, suboptimal cutting parameters, and reduced overall equipment effectiveness, thereby diminishing the return on investment in high performance cutting solutions. Furthermore, the rapid evolution of digital manufacturing technologies requires continuous upskilling, which many organizations struggle to provide due to resource constraints. This lack of technical proficiency not only hampers operational efficiency but also stifles innovation, as companies hesitate to adopt new tooling systems that require specialized knowledge. Addressing this labor shortage through enhanced training programs and educational initiatives is crucial, yet the current scarcity of skilled workers remains a significant restraint on the widespread adoption and optimal utilization of advanced cutting tools in the industrial landscape.

MARKET OPPORTUNITIES

Integration of the Internet of Things Enables Predictive Maintenance and Enhanced Efficiency

The incorporation of Internet of Things technology into cutting tools is a substantial opportunity for enhancing operational efficiency and reducing downtime in manufacturing environments. Smart tools equipped with sensors can monitor parameters such as vibration, temperature, and cutting forces in real time, providing valuable data for predictive maintenance and process optimization. According to the International Data Corporation, global spending on Internet of Things solutions is projected to reach 1.1 trillion USD by 2025, indicating widespread adoption across various industrial sectors. In the context of cutting tools, this connectivity allows manufacturers to detect tool wear before failure occurs, thereby preventing costly machine damage and production interruptions. As per McKinsey and Company, predictive maintenance applications can reduce machine downtime by up to 50% and extend asset life by 20% to 40%, offering significant economic benefits. The ability to analyze machining data also enables engineers to refine cutting parameters for improved surface finish and tool longevity, leading to higher productivity and lower operational costs. Furthermore, the integration of digital twins facilitates virtual simulations of machining processes, allowing for the testing of different tooling strategies without physical trials. This technological advancement supports the transition towards Industry 4.0, where data driven decision making becomes central to manufacturing excellence. By leveraging these digital capabilities, cutting tool manufacturers can offer value added services that differentiate their products in a competitive market. The growing emphasis on smart factory initiatives across Europe and North America further accelerates the demand for connected tooling solutions, creating a lucrative opportunity for innovation and market expansion in the cutting tools sector.

Adoption of Sustainable Manufacturing Practices Drives Development of Eco Friendly Tools

The growing environmental regulations and corporate sustainability goals are driving the demand for eco-friendly cutting tools and processes that minimize waste and energy consumption. Manufacturers are increasingly focusing on developing tools with longer lifespans and recyclable materials to reduce the environmental footprint of machining operations. According to the European Environment Agency, industrial activities account for a significant portion of resource consumption and waste generation in Europe, prompting stricter regulatory frameworks such as the European Green Deal. This initiative aims to make Europe the first climate neutral continent by 2050, influencing manufacturing practices across various sectors. As per the United Nations Industrial Development Organization, sustainable industrial development requires the adoption of cleaner production techniques, including the use of dry machining and minimum quantity lubrication, which reduce the need for hazardous coolants. Cutting tool manufacturers are responding by designing products that perform efficiently under these conditions, thereby supporting environmentally responsible manufacturing. Additionally, the recycling of tungsten carbide scrap has gained traction, with companies implementing closed loop systems to recover valuable materials. The Global Recycling Standard indicates that the recycling rate for hard metals has improved significantly, contributing to resource conservation. By aligning with sustainability trends, cutting tool providers can access new market segments that prioritize environmental stewardship. This shift not only enhances brand reputation but also meets the growing expectations of customers who seek sustainable supply chain solutions. The convergence of regulatory pressure and consumer preference for green products creates a compelling opportunity for the development and adoption of sustainable cutting tools in the global market.

MARKET CHALLENGES

Supply Chain Disruptions Pose Risks to Material Availability and Delivery Timelines

Global supply chain disruptions continue to pose significant challenges to the cutting tools market, affecting the availability of raw materials and the timely delivery of finished products. The aftermath of the pandemic, coupled with geopolitical conflicts and trade restrictions, has exposed vulnerabilities in international logistics networks. According to the United Nations Conference on Trade and Development, global merchandise trade volume growth slowed considerably in recent years due to port congestions and shipping delays. These disruptions impact the sourcing of critical materials such as tungsten and cobalt, which are essential for producing high performance cutting tools. As per the Institute for Supply Management, manufacturing supply chain pressures remained elevated, with lead times for industrial supplies extending beyond normal levels. For cutting tool manufacturers, these delays can result in production bottlenecks and inability to meet customer demand, leading to lost sales and damaged relationships. Furthermore, the reliance on single source suppliers for certain components exacerbates the risk, as any interruption in their operations can have cascading effects throughout the supply chain. The complexity of global trade regulations also adds to the challenge, requiring manufacturers to navigate varying compliance requirements across different regions. To mitigate these risks, companies are exploring nearshoring strategies and diversifying their supplier bases, yet these adjustments require time and investment. The persistent uncertainty in global logistics networks remains a formidable challenge that necessitates robust risk management strategies to ensure continuity and reliability in the cutting tools market.

Intense Competition from Low Cost Manufacturers Erodes Market Share in Standard Segments

The intense competition from low cost manufacturers, particularly in Asia that offer standard tools at significantly lower prices are further challenging the growth of the global cutting tools market. This price pressure erodes the market share of established players in the standard tool segment, forcing them to compete on factors other than cost. According to the World Trade Organization, exports of machinery and mechanical appliances from Asian countries have grown substantially, increasing their presence in global markets. As per the Chinese Machine Tool Builders Association, China produces a vast quantity of cutting tools annually, catering to both domestic and international demand with competitive pricing strategies. This influx of affordable alternatives challenges premium brands to justify their higher prices through superior performance and service offerings. While high end applications still require advanced tools, many small and medium sized enterprises opt for cost effective solutions for routine machining tasks. The disparity in production costs, driven by lower labor and operational expenses in emerging economies, makes it difficult for Western manufacturers to match these prices without compromising quality or profitability. Consequently, leading companies must focus on innovation and customization to differentiate their products and retain customer loyalty. However, the pervasive availability of low cost options continues to exert downward pressure on prices and margins in the standard tool segment. This competitive dynamic requires strategic positioning and continuous value creation to sustain growth and maintain market leadership in an increasingly crowded and price sensitive landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.2% |

| Segments Covered | By Type, Material, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BIG KAISER Precision Tooling Inc., Kennametal, Nachi-Fujikoshi Corp., OSG USA, INC., Sandvik AB, Ceratizit S.A., Dewalt, Fraisa SA, Guhring, Inc., Kilowood Cutting Tools, Xiamen Golden Egret Special Alloy Co. Ltd., Zhuzhou Cemented Carbide Cutting Tool Co. Ltd., Tiangong International Co., LIMITED, Ingersoll Cutting Tool Company, Sumitomo Electric Hartmetall GmbH, Kyocera Unimerco, and ISCAR LTD and Others. |

SEGMENTAL ANALYSIS

By Type of Tools Insights

The indexable inserts segment dominated the global cutting tools market with the highest share of the global market in 2025 due to their cost effectiveness and versatility in high volume manufacturing environments. These tools allow for quick replacement of worn cutting edges without replacing the entire tool holder, significantly reducing downtime and operational costs. The primary driver for this dominance is the widespread adoption of automated machining centers in the automotive and aerospace sectors, where precision and speed are paramount. According to the Society of Manufacturing Engineers, indexable inserts account for approximately 60% of the total cutting tool consumption in industrial applications, highlighting their critical role in modern production lines. The ability to utilize multiple cutting edges on a single insert further enhances their economic appeal, as manufacturers can rotate the insert to use fresh edges before disposal. As per the American Machinist, the average tool change time for indexable inserts is less than two minutes, compared to significantly longer times for solid tools, which directly contributes to higher machine utilization rates. Furthermore, advancements in coating technologies have extended the life of these inserts, allowing them to withstand higher cutting speeds and temperatures. The European Federation of National Associations Representing Producers of Machine Tools notes that the demand for indexable inserts has grown by 5% annually in Europe, driven by the need for efficient mass production capabilities. This segment's leadership is sustained by continuous innovation in geometry and material composition, ensuring that manufacturers can achieve superior surface finishes and tighter tolerances while maintaining competitive production costs.

However, the solid round tools segment is estimated to grow at a CAGR of 5.1% during the forecast period in the global market owing to the increasing complexity of machined components in the medical and electronics industries, which require high precision and intricate geometries that solid tools can deliver more effectively than indexable options. The miniaturization of electronic devices and the need for micro machining operations have surged the demand for solid carbide end mills and drills. According to the Medical Device Manufacturers Association, the global medical device market is expected to reach 612 billion USD by 2025, necessitating advanced machining solutions for small and complex parts. Solid round tools offer superior rigidity and accuracy, which are essential for producing these delicate components without deflection or vibration. As per the International Electronics Manufacturing Initiative, the production of printed circuit boards and semiconductor packages has increased by 8% annually, further fueling the need for precise drilling and milling operations. Additionally, the adoption of five axis machining centers, which rely heavily on solid tools for complex contouring, has accelerated market growth. The German Machine Tool Builders Association reports that sales of solid carbide tools have outpaced other categories in recent years, reflecting the shift towards high value added manufacturing. This segment's growth is also supported by the development of new substrate materials that enhance wear resistance and tool life, making solid round tools an increasingly viable option for demanding applications.

By Material Insights

The cemented carbide segment held the major share of the global market in 2025. The dominance of cemented carbide segment in the global market is attributed to its exceptional balance of hardness, toughness, and wear resistance, making it suitable for a wide range of machining applications. This material is composed of tungsten carbide particles bonded with a cobalt binder, providing the durability required for high speed cutting operations. The dominance of cemented carbide is driven by its extensive use in the automotive and general engineering sectors, where it offers superior performance compared to high speed steel. According to the International Tungsten Industry Association, cemented carbide accounts for over 50% of the global cutting tool material market, underscoring its indispensability in industrial manufacturing. The material's ability to maintain cutting edge integrity at elevated temperatures allows for faster machining speeds, which translates to higher productivity and lower unit costs. As per the European Powder Metallurgy Association, the production of cemented carbide tools in Europe has remained stable, with a slight increase in demand for specialized grades tailored for difficult to machine alloys. Furthermore, the recyclability of tungsten carbide supports sustainable manufacturing practices, as recovered materials can be reprocessed into new tools with minimal loss of quality. The US Geological Survey highlights that the recycling rate for tungsten carbide scrap has improved, contributing to a more secure supply chain for manufacturers. This segment's leadership is reinforced by ongoing research into nano structured carbides, which offer enhanced mechanical properties and extended tool life, ensuring that cemented carbide remains the preferred choice for diverse industrial applications.

On the other side, the polycrystalline segment is estimated to progress at a CAGR of 7.2% during the forecast period owing to the increasing use of abrasive non-ferrous materials and composites in the aerospace and automotive industries, which require cutting tools with extreme hardness and thermal conductivity. Polycrystalline diamond tools offer superior wear resistance and edge retention when machining materials such as aluminum silicon alloys, carbon fiber reinforced polymers, and ceramics. According to the Aerospace Industries Association, the adoption of composite materials in aircraft structures has increased by 15% in recent years, driving the demand for specialized cutting solutions that can handle these challenging substrates without delamination or excessive tool wear. As per the Society of the Plastics Industry, the use of reinforced plastics in automotive components has also risen, further boosting the need for polycrystalline diamond tools. The ability of these tools to operate at higher cutting speeds while maintaining precise tolerances makes them ideal for high volume production environments. According to the Industrial Diamond Association, advancements in synthetic diamond production have reduced costs, making polycrystalline diamond tools more accessible to a broader range of manufacturers. Additionally, the growing emphasis on lightweight vehicle designs to improve fuel efficiency has intensified the use of aluminum and composites, thereby sustaining the robust growth trajectory of this segment.

By Application Insights

The automotive segment accounted for the major share of the global market in 2025. The growth of the automotive segment in the global market is driven by the high volume of vehicle production and the extensive machining required for engine blocks, transmission components, and chassis parts. The demand for cutting tools in this sector is sustained by the continuous evolution of vehicle designs and the introduction of new materials to meet regulatory standards for emissions and safety. According to the International Organization of Motor Vehicle Manufacturers, global motor vehicle production reached approximately 93.5 million units in 2023, creating a substantial and consistent demand for precision machining tools. The transition towards electric vehicles has further diversified the machining requirements, as the production of battery housings and electric motor components involves complex milling and drilling operations. As per the European Automobile Manufacturers Association, investments in electric vehicle manufacturing facilities in Europe have exceeded 50 billion EUR in recent years, leading to increased procurement of advanced cutting tools. The need for high precision and surface finish quality in automotive components ensures that manufacturers prioritize high performance cutting solutions to minimize defects and rework. Furthermore, the trend towards lightweighting has increased the use of aluminum and high strength steel, which require specialized tools to machine efficiently. The American Center for Mobility highlights that the adoption of automated machining lines in automotive plants has improved productivity by 20%, reinforcing the critical role of reliable cutting tools in maintaining operational efficiency and meeting production targets in this dominant application segment.

On the other end, the aerospace and defense segment is predicted to expand at a healthy CAGR of 6.2% during the forecast period owing to the extensive use of advanced materials such as titanium alloys, nickel based superalloys, and carbon fiber composites, which require specialized cutting tools for effective machining. According to the Aerospace Industries Association, global aerospace revenues are projected to exceed 900 billion USD by 2025, reflecting strong order backlogs for new aircraft models and increased maintenance activities. The introduction of next generation aircraft, which incorporate higher proportions of composite materials, has intensified the demand for polycrystalline diamond and cubic boron nitride tools that can handle abrasive textures without causing damage. As per the European Association of Aerospace Industries, the sector is investing heavily in sustainable aviation technologies, which involve the development of lightweight structures that require intricate machining processes. The defense sector also contributes to this growth, with governments worldwide upgrading their military hardware and investing in advanced manufacturing capabilities. The US Department of Defense reported an increase in procurement budgets for aerospace components, further stimulating the demand for high precision cutting tools. Additionally, the need for strict quality control and certification in aerospace manufacturing ensures that only high performance tools are used, supporting the premium segment of the market and driving continuous innovation in tooling technologies.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific dominated the cutting tools market worldwide in 2025 with 40.4% of the global market share. The manufacturing sector in major Asia Pacific countries is expected to experience robust growth for the next few years, which will continue to strengthen its role as the dominant contributor to global industrial demand. The region's dominance is underpinned by its status as the world's factory, with extensive production capabilities in automotive, electronics, and machinery sectors. According to the National Bureau of Statistics of China, the country's manufacturing output grew by 4.6% in 2023, sustaining high demand for industrial cutting tools. Japan remains a key player due to its advanced technological capabilities and presence of major tool manufacturers, contributing significantly to regional innovation. As per the Japan Machine Tool Builders Association, domestic orders for cutting tools have remained stable, supported by exports to neighboring countries. India is emerging as a significant growth engine, with the government's Make in India initiative boosting local manufacturing. The Ministry of Commerce and Industry in India reported a 10% increase in manufacturing sector investments, leading to higher adoption of automated machining solutions. The presence of low cost labor and favorable government policies further attracts foreign direct investment, enhancing the region's production capacity. Additionally, the rapid urbanization and infrastructure development in Southeast Asian countries are driving demand for construction equipment, which requires precision machined components. This combination of established industrial bases and emerging markets ensures that Asia Pacific continues to lead the global cutting tools landscape.

North America Market Analysis

The industrial ecosystem in North American countries is likely to accelerate its digital transformation for the next few years, heavily boosting domestic high precision manufacturing investments. North America maintains a strong position in the global cutting tools market, characterized by high adoption of advanced manufacturing technologies and a focus on precision engineering. The region benefits from a mature industrial base, particularly in the United States, where the aerospace, automotive, and medical device sectors drive demand for high performance tools. According to the US Census Bureau, the manufacturing sector in the United States contributed approximately 2.8 trillion USD to the economy, highlighting its significance. The resurgence of domestic manufacturing, supported by initiatives such as the CHIPS and Science Act, has spurred investments in semiconductor and electric vehicle production, increasing the need for specialized cutting solutions. As per the National Association of Manufacturers, US manufacturers are increasingly adopting Industry 4.0 technologies, including smart tools and predictive maintenance systems, to enhance efficiency. Canada also contributes to the regional market, with a growing aerospace sector in Quebec and Ontario. The Aerospace Industries Association of Canada noted a 5% growth in aerospace exports, driving demand for precision machining tools. The region's emphasis on innovation and quality ensures that premium cutting tools are preferred, supporting higher average selling prices. Furthermore, the presence of leading tool manufacturers and distributors facilitates easy access to advanced products, reinforcing North America's competitive position in the global market.

Europe Market Analysis

European countries are anticipated to focus intensely on green manufacturing and supply chain resilience for the next few years, steering industrial growth toward high precision sustainable tooling. Europe holds a significant share of the cutting tools market, driven by its strong engineering heritage and leadership in high value added manufacturing sectors such as automotive and aerospace. Germany, Italy, and France are key contributors, hosting numerous original equipment manufacturers that require precision machining solutions. According to Eurostat, the manufacturing industry in the European Union accounted for 15% of the total value added, underscoring its economic importance. Germany, as the largest economy in the region, relies heavily on advanced cutting tools for its automotive and machinery sectors. As per the Federal Ministry for Economic Affairs and Climate Action, German machine tool orders increased by 3%, reflecting steady demand from domestic and international customers.

COMPETITIVE LANDSCAPE

The competition in the global cutting tools market is characterized by intense rivalry among established multinational corporations and emerging regional manufacturers. Leading companies differentiate themselves through continuous innovation in material science and digital technologies rather than competing solely on price. The market features a mix of premium brands offering high performance specialized tools and cost effective providers catering to standard applications. Technological advancement serves as a primary competitive lever with firms investing in smart tooling solutions and automated manufacturing processes. Strategic collaborations with machine tool builders and end users facilitate the development of integrated systems that enhance productivity. Geographic expansion remains a key strategy as companies seek to capture growth in emerging markets such as Asia Pacific and Latin America. Supply chain resilience has become critical with manufacturers diversifying sourcing to mitigate risks associated with raw material volatility. Customer service and technical support are vital differentiators that influence purchasing decisions in high value segments. The presence of numerous small and medium sized enterprises adds to the fragmented nature of the market particularly in standard tool categories. Overall the competitive landscape demands constant adaptation to technological trends and shifting customer preferences to sustain long term success.

KEY MARKET PLAYERS

A few of the market players in the global cutting tools market include

- Sandvik AB

- Kennametal Inc.

- Robert Bosch GmbH

- Stanley Black & Decker Inc.

- Mitsubishi Materials Corporation

- OSG Corporation

- Kyocera Corporation

- Guhring KG

- ISCAR LTD

- Seco Tools AB

Top Players In The Market

- Sandvik Coromant stands as a premier innovator in the field of metal cutting solutions and digital manufacturing technologies. The company consistently invests in research and development to introduce advanced tooling systems that enhance productivity and sustainability for industrial clients globally. Recent initiatives include the expansion of its CoroPlus digital platform which enables connected machining processes and data driven decision making for optimized performance. Sandvik Coromant actively collaborates with automotive and aerospace manufacturers to develop customized solutions that address specific machining challenges. Their commitment to sustainability is evident through the introduction of eco friendly tool designs and recycling programs for carbide materials. By focusing on high value applications and technological integration the company strengthens its leadership position while supporting customers in achieving greater efficiency and reduced environmental impact in their production operations worldwide.

- Kennametal Inc delivers specialized engineering solutions that serve diverse industries including transportation infrastructure and general engineering sectors. The company leverages its extensive material science expertise to create durable cutting tools that withstand rigorous operating conditions. Recent strategic actions involve optimizing its global supply chain to ensure reliable product availability and faster delivery times for key markets. Kennametal has also focused on expanding its portfolio of indexable inserts and solid carbide tools tailored for high speed machining applications. The organization emphasizes customer centric innovation by providing technical support and application engineering services to improve machining outcomes. Through continuous improvement in manufacturing processes and the adoption of digital tools Kennametal enhances operational efficiency and maintains a competitive edge in the global marketplace.

- Mitsubishi Materials Corporation is a leading provider of high performance cutting tools known for their precision and reliability in demanding industrial environments. The company integrates advanced material technologies such as cemented carbide and cermet to produce tools that offer superior wear resistance and longevity. Recent efforts include the launch of new product series designed for efficient machining of difficult to cut materials like titanium and heat resistant alloys. Mitsubishi Materials actively engages in partnerships with machine tool builders to develop integrated solutions that maximize machining performance. The company also invests in automation technologies to streamline production and reduce lead times for custom orders. By prioritizing quality and innovation Mitsubishi Materials continues to expand its global footprint and support manufacturers in achieving higher productivity and cost effectiveness in their machining operations.

Top Strategies Used By Key Market Participants

Key players in the cutting tools market primarily focus on product innovation and technological integration to maintain competitive advantage. Companies invest heavily in research and development to create advanced materials and coatings that enhance tool life and performance. Strategic acquisitions are frequently employed to expand geographic reach and diversify product portfolios. Partnerships with original equipment manufacturers enable the development of customized solutions tailored to specific industry needs. Digitalization strategies involve the incorporation of Internet of Things sensors into tools for real time monitoring and predictive maintenance. Sustainability initiatives are increasingly central with firms developing eco friendly products and recycling programs to meet regulatory requirements. Customer centric approaches include providing comprehensive technical support and training services to optimize tool usage. These strategies collectively drive growth and strengthen market positions by addressing evolving industrial demands and enhancing operational efficiency for clients across various sectors globally.

MARKET SEGMENTATION

This research report on the global cutting tools market has been segmented and sub-segmented based on type, material, application, and region.

By Type of Tools

- Indexable Inserts

- Solid Round Tools

By Material

- Exotic Materials

- Cubic Boron Nitride

- Stainless Steel

- Ceramics

- High-Speed Steel

- Cemented Carbide

- Polycrystalline Diamond

By Application

- Electronics

- Automotive

- Construction

- Aerospace and Defense

- Wood

- Die & Mold

- Oil & Gas

- Power Generation

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

What are the primary drivers of growth in the cutting tools market?

Key drivers include technological advancements in manufacturing processes, increasing demand from the automotive and aerospace sectors, and the growth of the industrial and construction sectors globally.

How is the market segmented in terms of product types?

The market is segmented into milling tools, drilling tools, turning tools, grinding tools, and others. Among these, milling tools hold the largest share due to their extensive use in various applications.

How is the automotive industry influencing the cutting tools market?

The automotive industry significantly influences the market as it requires precise and efficient cutting tools for manufacturing complex components. The push towards electric vehicles (EVs) is also driving demand for specialized cutting tools.

What are the emerging trends in the cutting tools market?

Emerging trends include the adoption of advanced coatings to extend tool life, the use of AI and IoT for predictive maintenance and tool management, and a shift towards sustainable and environmentally friendly manufacturing processes.

What is driving growth in the global cutting tools market?

Rising demand from automotive, aerospace, and manufacturing sectors—coupled with advancements in material science and smart tooling—is fueling market expansion. Industry 4.0 adoption and precision machining needs further accelerate this trend.

Which region dominates the cutting tools market?

Asia-Pacific leads due to robust industrialization, especially in China, Japan, and India, supported by strong manufacturing bases and government initiatives promoting advanced machining.

How are sustainability trends affecting cutting tool manufacturers?

Companies are increasingly developing eco-friendly, long-life tools and recyclable carbide inserts to meet regulatory standards and customer ESG goals without compromising performance.

What role does material innovation play in cutting tool performance?

Advanced materials like polycrystalline diamond (PCD), cubic boron nitride (CBN), and nano-coated carbides significantly enhance tool durability, heat resistance, and cutting efficiency.

Are digitalization and IoT impacting the cutting tools industry?

Yes—smart cutting tools with embedded sensors enable real-time monitoring of wear, temperature, and vibration, improving predictive maintenance and reducing unplanned downtime in smart factories.

Who are the key players in the global cutting tools market?

Major companies include Sandvik AB, Kennametal Inc., Mitsubishi Materials Corporation, Iscar (IMC Group), and Walter AG—known for R&D investment, global reach, and high-performance tooling solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com