Global Esters Market Size, Share, Trends & Growth Forecast Report By Product Type (Dibasic Esters, Polyol Esters, Methyl Esters, Nitrate Esters, Vinyl Esters, Phosphate Esters, Acrylic Esters, Sucrose Esters, Fatty Acid Esters), End use And Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis from 2025 to 2033

Global Esters Market Summary

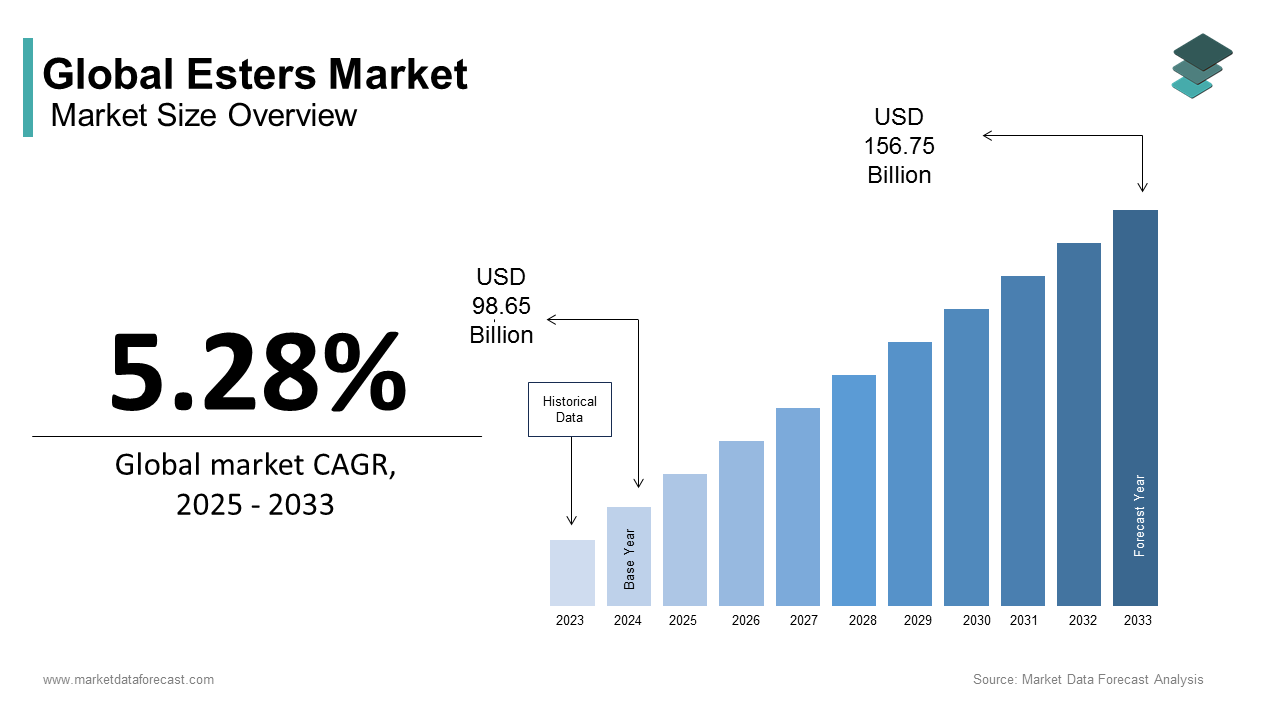

The global esters market size was valued at USD 98.65 billion in 2024, projected to reach USD 103.86 billion in 2025 and USD 156.75 billion by 2033, growing at a CAGR of 5.28% from 2025 to 2033. Market growth is driven by increasing demand for esters in plastics, polymers, personal care, and industrial applications, along with rising adoption in eco-friendly solvents and lubricants. Technological advancements in ester production and growing emphasis on sustainable chemical solutions are further boosting market expansion.

Key Market Trends

- Increasing use of fatty acid esters in lubricants, plasticizers, and personal care products

- Rising demand for biodegradable and environmentally friendly esters

- Growth in the plastics and polymers sector is driving ester consumption

- Innovations in ester synthesis and process efficiency supporting cost-effective production

Segmental Insights

- Based on product type, the fatty acid esters segment dominated in 2024 with a 32.7% share, due to its versatility across multiple industrial and consumer applications.

- Based on end-use, the plastics and polymers segment led the market with 25.8% share in 2024, driven by high demand for esters as plasticizers and processing aids.

Regional Insights

- Asia-Pacific was the top-performing region in 2024, accounting for a 42.1% share, supported by robust manufacturing, growing polymer demand, and expanding chemical production infrastructure.

- North America is expected to grow steadily, driven by advanced chemical manufacturing technologies and increasing use of esters in industrial and personal care products.

- Europe focuses on sustainable and biodegradable ester solutions, supported by strict environmental regulations and green chemistry initiatives.

- Latin America is emerging as a promising market, backed by expanding plastics, polymers, and industrial applications.

- Middle East & Africa are gradually adopting esters for industrial, lubricants, and personal care applications, driven by regional chemical industry growth.

Competitive Landscape

Key players in the global esters market include LANXESS, Teknor Apex Company, Hallstar Innovations Corp., Monument Chemical, Mitsubishi Chemical Group Corporation, Exxon Mobil Corporation, Cargill, Incorporated, The Procter & Gamble Company, Arkema Group, Evonik Industries AG, DuPont, Solvay, Huntsman International LLC, Daikin, Ashland, DAK Americas, Esterchem Ltd., Sumitomo Chemical Co., Ltd., ABITEC, ADM, BASF SE, IFFCO, AkzoNobel N.V., Biotage, Stepan Company, DSM, CEM Corporation, Fine Organics, Subhash Chemicals, Gattefosse, Croda International, NYCO, Eastman Chemical Company. These companies focus on product innovation, sustainable manufacturing, capacity expansion, and strategic partnerships to strengthen their market presence.

Global Esters Market Size

The global esters market size was calculated to be USD 98.65 billion in 2024 and is anticipated to be worth USD 156.75 billion by 2033 from USD 103.86 billion In 2025, growing at a CAGR of 5.28% during the forecast period.

Esters are the organic compounds formed through the reaction between carboxylic acids and alcohols, yielding molecules with pivotal roles across industrial, pharmaceutical, and consumer sectors. Many commercially used flavor and fragrance compounds are ester-based due to their volatility and sensory profiles. According to the European Food Safety Authority, more than 300 ester derivatives are approved as food additives within the EU, underscoring their regulatory acceptance and functional versatility. These compounds are increasingly engineered for biodegradability by aligning with environmental mandates. Their utility in green chemistry innovations, particularly in bio-based polymer synthesis, has expanded application scope beyond traditional domains.

MARKET DRIVERS

The rising demand for bio-based plasticizers in flexible pvc applications is accelerating the growth of esters market. The transition from phthalate-based to non-phthalate plasticizers has significantly amplified the demand for esters, particularly adipate and citrate esters, in flexible polyvinyl chloride (PVC) manufacturing. As per the study, non-phthalate plasticizers are growing in popularity due to health and environmental concerns, phthalates remain dominant in Europe, even in recent years. The U.S. Consumer Product Safety Commission has restricted phthalates in children’s products, accelerating the shift toward safer ester-based alternatives.

Expansion of biodiesel production utilizing Fatty Acid Methyl Esters (FAME) is additionally propelling the growth of esters market. Fatty acid methyl esters (FAME), derived from transesterification of vegetable oils or animal fats, serve as the primary constituents of biodiesel, which directly links ester chemistry to renewable fuel development. The Renewable Energy Directive II in the EU mandates that 14% of transport energy must come from renewable sources by 2030, further incentivizing FAME-based fuel integration. FAME’s compatibility with existing diesel engines and distribution infrastructure enhances its adoption, while advancements in feedstock efficiency have reduced production costs over the past years, as per the research.

MARKET RESTRAINTS

Volatility in feedstock supply for oleochemical esters is restraining the growth of esters market. The production of oleochemical esters, particularly those derived from palm, coconut, and castor oils, faces persistent instability due to fluctuations in agricultural output and geopolitical constraints. According to the study, due to the mixed results from the top producers, global palm oil supplies tightened. Apart from these, the European Commission’s deforestation regulation, set to take effect in 2025, restricts imports of commodities linked to forest loss, potentially disrupting supply chains for palm-derived esters. These supply-side constraints increase raw material costs and production uncertainty, which is impeding consistent ester manufacturing and discouraging long-term investment in oleochemical pathways.

The stringent regulatory scrutiny on synthetic ester additives in food and cosmetics is also hindering the growth of esters market. The U.S. FDA has issued warnings on certain artificial flavor esters, including ethyl butyrate, when used above threshold levels, citing potential respiratory and dermal sensitization. Furthermore, in a January 2025 report, the Clean Label Project analyzed 160 of the top-selling protein powders. It found that 47% of the tested products exceeded at least one regulatory limit for heavy metals set by California's Proposition 65, and 21% had heavy metal levels that were double those limits.

MARKET OPPORTUNITIES

The development of biodegradable lubricants using synthetic esters is greatly influencing the growth of esters market. As per the U.S. Environmental Protection Agency, ester-based lubricants exhibit biodegradation rates exceeding 80% within 21 days under OECD 301B tests, far surpassing mineral oil counterparts. The global EAL busines is projected to grow through 2033, driven by regulations such as the Vessel General Permit, which mandates biodegradable lubricants in U.S. waters. In Germany, the Blue Angel eco-label certifies ester-based hydraulic fluids, with over 120 products achieving certification by 2023, as reported by the German Federal Environment Agency.

The enzymatic catalysis is also an opportunity for the esters market growth. It is particularly using lipases and is revolutionizing ester synthesis by enabling reactions under mild conditions with minimal waste. In 2022, BASF promoted its commercial process for producing ethyl acetate using a new type of chromium-free (Cr-free) dehydrogenation catalyst. The European Green Deal supports such innovations through funding mechanisms like Horizon Europe, allocating significant amount to biocatalysis research. Furthermore, the American Chemistry Council shows that enzyme-mediated ester production generates less wastewater than traditional methods. These advancements not only lower environmental impact but also improve product purity by making enzymatically synthesized esters ideal for pharmaceuticals and food-grade applications, thereby opening high-value market segments.

MARKET CHALLENGES

The high cost of production is a major challenge for the growth of esters market. The synthesis of high-purity esters for active pharmaceutical ingredients (APIs) and prodrugs involves complex purification and stringent quality control, which is resulting in elevated manufacturing costs. As per the research, ester-based prodrugs such as oseltamivir phosphate require multi-step esterification with chiral selectivity, increasing production expenses compared to non-esterified analogs. The average cost of producing a kilogram of pharmaceutical-grade isopropyl myristate is notable, as per the study, primarily due to solvent recovery and chromatographic purification. Furthermore, the need for GMP-compliant facilities limits outsourcing options, with only a portion of global contract manufacturers certified for ester-based API synthesis.

The competition from alternative solvents in industrial applications is additionally to hinder the growth of esters market. Esters such as ethyl acetate and butyl acetate face mounting competition from non-ester green solvents like glycol ethers, terpenes, and supercritical CO₂ in coatings, inks, and cleaning formulations. While the broader market trend does show a shift toward lower VOC (volatile organic compounds) and greener alternatives. Terpene-based solvents, derived from citrus peel, capture a portion of the eco-solvent landscape, with companies reporting an annual sales increase. Additionally, Dow Chemical has commercialized a line of glycol ether solvents with lower toxicity and improved water miscibility, directly challenging ester dominance in adhesives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.28% |

| Segments Covered | By Product Type, End Use and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | LANXESS, Teknor Apex Company, Hallstar Innovations Corp., Monument Chemical, Mitsubishi Chemical Group Corporation, Exxon Mobil Corporation, Cargill, Incorporated, The Procter & Gamble Company, Arkema Group, Evonik Industries AG, DuPont, Solvay, Huntsman International LLC, Daikin, Ashland, DAK Americas, Esterchem Ltd., Sumitomo Chemical Co., Ltd., ABITEC, ADM, BASF SE, IFFCO, AkzoNobel N.V., Biotage, Stepan Company, DSM, CEM Corporation, Fine Organics, Subhash Chemicals, Gattefosse, Croda International, NYCO, Eastman Chemical Company |

SEGMENTAL ANALYSIS

By Product Type Insights

The fatty acid esters segment was accounted in holding 32.7% of the esters market share in 2024 with their extensive integration across multiple high-volume sectors in food, personal care, and biofuels. Their amphiphilic nature and biocompatibility render them ideal for emulsification, solubilization, and plasticization, enabling broad utility. Unlike more niche ester classes such as nitrate or vinyl esters, fatty acid esters benefit from scalable production via transesterification of renewable feedstocks by ensuring cost efficiency and supply resilience. Fatty acid esters, especially mono- and diglycerides, are indispensable in food processing due to their ability to stabilize emulsions in baked goods, dairy products, and margarines. According to the study, many countries permit the use of E471 (mono- and diglycerides of fatty acids) in food, with annual consumption exceeding significant metric tons globally. In the United States, as per the estimates, a notable share of commercially produced bread and rolls contain fatty acid ester emulsifiers to improve texture and shelf life. The global bakery business grew significantly which directly fuels demand for these esters. Moreover, consumer preference for longer-lasting, soft-textured products has intensified formulation reliance on these additives. The Codex Alimentarius Commission reaffirms their safety by contributing to sustained regulatory approval and formulation confidence across emerging and developed markets alike.

The sucrose esters segment is likely to grow with an estimated esters market and is projected to expand at a CAGR of 9.4% from 2025 to 2033. The growth of sucrose esters segment is driven by their unique combination of non-toxicity, biodegradability, and multifunctionality, positioning them at the intersection of health, sustainability, and performance innovation. Sucrose esters are gaining traction as natural emulsifiers in response to consumer demand for transparent ingredient lists. As per the Clean Label Project’s Food Transparency Index, many surveyed consumers prefer products with recognizable ingredients, prompting manufacturers to replace synthetic surfactants with plant-derived alternatives like sucrose esters.

By End-Use Insights

The plastics and polymers segment led esters market in 2024 and accounting for 25.8% of in 2024. The growth of plastics and polymers segment is driven by the indispensable role of esters as plasticizers, stabilizers, and co-monomers in polymer manufacturing in PVC, polyesters, and engineering resins. Esters such as dioctyl terephthalate (DOTP) and acetyl tributyl citrate (ATBC) have replaced phthalates in flexible PVC used in medical devices, toys, and construction films. As per the reserach, non-phthalate plasticizers accounted for a notable share of all plasticizer demand in Europe, with ester-based variants making up a key share of this segment. Also, the global flexible PVC landscape relies heavily on ester plasticizers for durability and compliance, ensuring sustained demand. Esters are central to the synthesis of aliphatic polyesters like polylactic acid (PLA) and polybutylene succinate (PBS), which are gaining ground as compostable alternatives to conventional plastics. According to the European Bioplastics Association, global production capacity of biodegradable plastics reached 2.18 million metric tons in 2023, with esterification being the key polymerization mechanism.

The cosmetics and personal care products segment is expected to grow with a CAGR of 8.9% from 2025 to 2033 with the rising consumer preference for multifunctional, skin-compatible ingredients, with esters fulfilling roles as emollients, viscosity modifiers, and fragrance carriers. Esters such as cetyl palmitate, isopropyl myristate, and jojoba esters are favored for their non-greasy texture and skin mimicry, enhancing product appeal. The global skincare business is increasingly targets sensitive and aging skin, where esters offer superior compatibility compared to mineral oils. Brands are reformulating to eliminate animal-derived ingredients, turning to synthetic and plant-based esters as vegan alternatives. As per the study, certified vegan cosmetic products increased, with esters replacing lanolin and beeswax.

REGIONAL ANALYSIS

Asia Pacific Esters Market Insights

Asia-Pacific was the top performer in the global esters market in 2024 and accounted for 42.1% share in 2024. The region functions as both a manufacturing powerhouse and a burgeoning consumer base, with China, India, and Southeast Asia driving production and formulation demand. Its dominance is anchored in robust chemical infrastructure, cost-efficient labor, and government-backed industrial policies that promote specialty chemical development. China led the regional landscape, contributing majorly to Asia-Pacific’s ester output. The country produced significant metric tons of ester-based plasticizers alone, as the per the study. This scale is supported by state initiatives like the 14th Five-Year Plan, which prioritizes green chemical manufacturing. Additionally, China’s dominance in rare earth processing and electronics has increased demand for phosphate esters as flame retardants in circuit boards.

Europe Esters Market Insights

Europe esters market was positioned next by holding a significant share in 2024 due to its regulatory dominance and focus on sustainability. As per the study, notable share esters placed on the EU market complied with REACH restrictions on endocrine disruptors, setting a global benchmark. Germany and the Netherlands serve as innovation hubs, with BASF and DSM investing heavily in bio-based ester R&D. The EU’s Circular Economy Action Plan has spurred an increase in biodegradable ester use since 2020, as per research. Moreover, the bloc’s ban on single-use plastics has accelerated demand for ester-based biopolymers, positioning Europe as a trendsetter in eco-conscious chemical application.

North America Esters Market Insights

North America esters market growth is likely to register a prominent CAGR during the forecast period with the advanced pharmaceutical and specialty chemical sectors. The United States accounts for a notable share of regional ester consumption, with the FDA approving several ester-based excipients for drug formulations, according to the study. The rise of biologics and mRNA vaccines has increased demand for ester-stabilized lipid nanoparticles, with Moderna and Pfizer utilizing esterified lipids in their delivery systems.

Latin America Esters Market Insights

Latin America esters market is likely to grow with the substantial cubic meters of biodiesel in 2023, primarily FAME-based, as per the study. Government mandates have raised the biodiesel blend in diesel to B15, driving ester demand. Additionally, Brazil’s cosmetics industry, the fourth-largest globally, consumed significant tons of emollient esters, according to the research. While infrastructure limitations persist, policy continuity and agricultural abundance provide a stable foundation for growth.

Middle East and Africa Esters Market Insights

Middle East and Africa is likely to grow in the esters market, with Saudi Arabia and South Africa as key nodes. The Saudi Vision 2030 initiative includes a notable investment in petrochemical diversification, including ester derivatives from crude glycerol, as per the study. In South Africa, there has been an annual increase in ester use in agrochemical formulations due to rising crop protection needs.

LEADING PLAYERS IN THE ESTERS MARKET

BASF SE

BASF has established a dominant presence in the esters market through its integrated production platforms and innovation-driven portfolio across plasticizers, cosmetic ingredients, and industrial fluids. In the Asia-Pacific region, the company operates advanced manufacturing hubs in South Korea and India, which is supplying high-purity polyol and fatty acid esters to polymer and pharmaceutical clients. The company strengthened its regional footprint by partnering with Indian agrochemical firms to supply biodegradable ester carriers.

Eastman Chemical Company

Eastman plays a pivotal role in the Asia-Pacific esters market by delivering performance-driven solutions in acetate and specialty esters for coatings, adhesives, and personal care. The company’s Singapore manufacturing facility serves as a regional export hub, producing cellulose esters and acetyl polymers with high consistency. Collaborations with Japanese cosmetic formulators have accelerated the adoption of Eastman’s diesters for sensory-enhanced skincare. These strategic moves reflect Eastman’s focus on regulatory foresight and application-specific innovation to deepen market penetration across high-growth Asian economies.

Croda International Plc

Croda has emerged as a key player in the Asia-Pacific esters market by focusing on high-value, bio-based esters for personal care and pharmaceutical applications. The company’s state-of-the-art facility in Shanghai produces emollient esters such as cetyl ethylhexanoate and caprylic/capric triglycerides, serving major Asian beauty brands. The company also initiated a collaboration with Thai biotech firms to develop sustainable surfactants from palm kernel derivatives, aligning with regional circular economy goals. Its investment in digital formulation tools enables rapid customer customization, enhancing client retention. Croda’s emphasis on green chemistry and regional innovation integration solidifies its reputation as a trusted specialty ester supplier in Asia-Pacific.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the esters market are deploying targeted strategies to consolidate their positions and respond to evolving industrial demands. Forward integration into end-use applications enables customized product development, particularly in pharmaceuticals and cosmetics. Companies are increasingly investing in bio-based and enzymatic esterification technologies to align with global sustainability mandates. Strategic collaborations with regional formulators and chemical distributors enhance market reach in high-growth areas like Asia-Pacific. Capacity expansions in emerging economies ensure supply chain resilience and cost efficiency.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players of the global esters market include LANXESS, Teknor Apex Company, Hallstar Innovations Corp., Monument Chemical, Mitsubishi Chemical Group Corporation, Exxon Mobil Corporation, Cargill, Incorporated, The Procter & Gamble Company, Arkema Group, Evonik Industries AG, DuPont, Solvay, Huntsman International LLC, Daikin, Ashland, DAK Americas, Esterchem Ltd., Sumitomo Chemical Co., Ltd., ABITEC, ADM, BASF SE, IFFCO, AkzoNobel N.V., Biotage, Stepan Company, DSM, CEM Corporation, Fine Organics, Subhash Chemicals, Gattefosse, Croda International, NYCO, Eastman Chemical Company

The competition in the esters market is characterized by technological differentiation, regulatory agility, and vertical integration rather than price dominance. Major players distinguish themselves through proprietary synthesis methods, sustainable feedstock sourcing, and application-specific formulations. The market is moderately consolidated, with multinational corporations leading in high-performance and specialty esters, while regional players dominate commodity-grade production. Innovation in green chemistry, particularly bio-based and biodegradable esters, has become a primary battleground, with companies racing to meet tightening environmental standards in Europe and North America.

MARKET SEGMENTATION

This research report on the global esters market has been segmented and sub-segmented based on product type, end use and region.

By Product Type

- Dibasic Esters

- Polyol Esters

- Methyl Esters

- Nitrate Esters

- Vinyl Esters

- Phosphate Esters

- Acrylic Esters

- Sucrose Esters

- Fatty Acid Esters

By End Use

- Chemicals

- Plastic and Polymers

- Soaps and Detergents

- Explosive

- Paints and Coatings

- Agrochemicals and Domestic Hygiene Products

- Pharmaceutical

- Industrial Chemicals

- Food

- Automotive and Aviation

- Marine

- Textiles

- Cosmetics and Personal Care Products

- General Manufacturing

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are esters and how are they produced?

Esters are organic compounds formed by the reaction of an alcohol with an acid, typically produced through esterification.

2. What are the major types of esters available in the market?

Key types include fatty acid esters, phthalate esters, polyol esters, phosphate esters, and acrylic esters.

3. Which industries are the primary consumers of esters?

Industries include lubricants, food & beverages, cosmetics & personal care, plastics, paints & coatings, and pharmaceuticals.

4. What factors are driving the growth of the global esters market?

Growing demand for bio-based esters, rising use in lubricants and food applications, and increasing cosmetic and personal care product consumption.

5. What are the key challenges faced by the esters market?

Fluctuating raw material prices, environmental regulations on certain synthetic esters, and the availability of substitutes.

6. Which region dominates the global esters market?

Asia Pacific holds the largest market share due to rapid industrialization, increasing automotive demand, and strong growth in the cosmetics and food sectors.

7. What are the emerging opportunities in the esters market?

Bio-based esters, eco-friendly plasticizers, sustainable lubricants, and expanding demand in pharmaceuticals.

8. How are bio-based esters influencing the market trend?

They are gaining traction due to environmental concerns, regulatory support, and consumer preference for sustainable products.

9. What impact does regulation have on the esters market?

Strict environmental and health regulations on phthalate esters are pushing manufacturers to develop safer, bio-based alternatives.

10. What is the growth outlook for the esters market?

The market is expected to grow steadily, driven by rising demand in eco-friendly lubricants, personal care products, and bio-based chemicals.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com