Europe Agriculture Nets Market Size, Share, Growth, Trends & Analysis Report Segmented By Product, Material, Form, Price Range, Distribution Channel, Application, End-user, And By Country (Germany, United Kingdom, France, Italy, Spain and the Rest of Europe), Industry Analysis From 2026 to 2034

Europe Agriculture Nets Market Report Summary

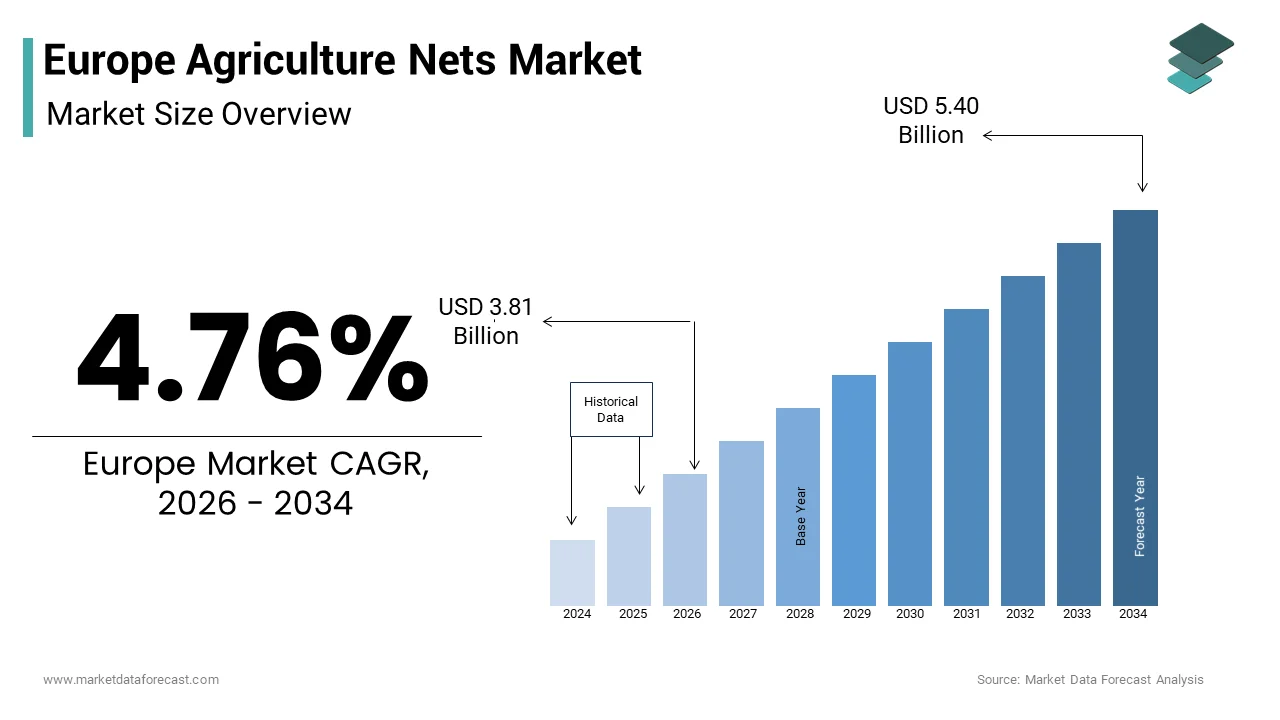

The Europe agriculture nets market was valued at USD 3.64 billion in 2025, is estimated to reach USD 3.81 billion in 2026, and is projected to reach USD 5.40 billion by 2034, registering a CAGR of 4.76% during the forecast period from 2026 to 2034. The Europe agriculture nets market is witnessing steady expansion as growers increasingly invest in crop protection technologies to improve yields, enhance produce quality, and mitigate climate-related risks. Rising concerns over extreme weather events, pest infestations, excessive solar radiation, and water conservation are accelerating the adoption of advanced agricultural netting solutions across open-field farming, orchards, vineyards, and greenhouse cultivation. Supportive government initiatives promoting sustainable agriculture, the growing demand for high-value horticultural crops, and continuous advancements in durable, UV-resistant, and recyclable net materials are further strengthening market growth. As precision agriculture and climate-resilient farming practices gain momentum across Europe, agriculture nets are becoming an essential component of modern crop management strategies.

Key Market Trends

- Climate-resilient farming practices are driving increased adoption of shading, anti-hail, insect-proof, and bird protection nets across diverse agricultural applications.

- Manufacturers are developing lightweight, UV-stabilized, and recyclable agricultural nets to improve durability while supporting sustainability objectives.

- Greenhouse cultivation and protected agriculture are expanding across Europe, increasing demand for specialized netting solutions that optimize crop growth conditions.

- Precision farming technologies are being integrated with crop protection systems to improve resource efficiency and enhance farm productivity.

- Rising production of fruits, vegetables, and vineyards is encouraging investments in customized netting solutions designed for high-value crop protection.

Segmental Insights

Based on product, the shading nets segment dominated the Europe agriculture nets market in 2025. The segment's leadership is driven by its effectiveness in reducing heat stress, regulating light intensity, minimizing moisture loss, and protecting crops from excessive solar radiation, particularly in horticulture and greenhouse farming.

Based on material, the plastic materials segment accounted for the largest share of the Europe agriculture nets market in 2025. Plastic-based nets continue to dominate due to their lightweight structure, high tensile strength, weather resistance, cost-effectiveness, and long operational lifespan across a wide range of agricultural environments.

Based on price range, the mid-range segment captured the highest share of the European market in 2025. Farmers increasingly prefer mid-priced agricultural nets because they offer an optimal balance between affordability, durability, and performance, making them suitable for both commercial and medium-scale farming operations.

Regional Insights

Spain held a leading position in the Europe agriculture nets market in 2025, supported by its extensive horticulture, greenhouse cultivation, and fruit production sectors that require advanced crop protection systems. Italy is expected to strengthen its market position through growing investments in protective netting for vineyards, orchards, and other high-value specialty crops. France is projected to experience steady market growth as sustainable farming practices and climate adaptation strategies continue to encourage wider adoption of agricultural nets. Germany is expected to maintain strong momentum by leveraging technological innovation and environmentally sustainable agricultural practices, while the Netherlands will remain a key innovation hub, supported by its globally recognized greenhouse technologies and expertise in protected cultivation systems.

Competitive Landscape

The Europe agriculture nets market is characterized by the presence of established agricultural textile manufacturers and specialized crop protection solution providers focused on product innovation, sustainability, and performance enhancement. Leading companies are investing in advanced polymer technologies, UV-resistant materials, recyclable netting solutions, and customized products designed for different crop types and climatic conditions. Strategic collaborations with agricultural distributors, greenhouse operators, and research institutions are helping companies expand their market reach and accelerate product development. Manufacturers are also strengthening production capabilities and incorporating environmentally responsible materials to align with Europe's sustainability goals and evolving agricultural regulations. As climate resilience and precision farming continue to shape modern agriculture, market participants are emphasizing innovation, product quality, and long-term durability to strengthen their competitive position across the European agriculture nets market.

Prominent players in the Europe agriculture nets market include Belton Industries, Smart Net Systems Ltd., Netfabrik, Raschier Group, Diatex, Garware Technical Fibres Limited, Thrace Group, Inc., Agriplast Tech India Pvt. Ltd., Agrotextiles International, Schweitzer-Mauduit International, Inc., Wellco Industries, Alphatex, Cittadini S.p.A., Zhongshan Hongjun Nonwovens Co. Ltd., and Beaulieu Technical Textiles.

Europe Agriculture Nets Market Size

The Europe agriculture nets market size was valued at USD 3.64 billion in 2025 and is anticipated to reach USD 3.81 billion in 2026 to reach USD 5.40 billion by 2034, growing at a CAGR of 4.76% during the forecast period from 2026 to 2034.

Agriculture nets are a diverse range of protective mesh structures designed to shield crops from environmental stressors, pests, and birds while optimizing microclimatic conditions for enhanced yield quality. These specialized textiles include hail protection nets, shade nets, anti-bird nets, and windbreak nets that serve critical functions across various agricultural sectors, including horticulture, viticulture, and arable farming. The European agricultural landscape is characterized by its high-value crop production where farmers prioritize premium quality outputs that command higher market prices. As per Eurostat, the European Union maintains approximately 156 million hectares of utilized agricultural area, with intensive cultivation practices prevalent in countries like Spain, Italy, and France. The region experiences an increasing frequency of extreme weather events, which necessitates robust protective measures for crop preservation. According to the European Environment Agency, the number of climate-related disasters in Europe has risen significantly over the past decade, affecting agricultural productivity and leading to higher demand for risk mitigation. Farmers are increasingly adopting precision agriculture techniques that integrate physical barriers like nets with digital monitoring systems. The shift toward organic farming practices across Europe further amplifies the demand for non-chemical pest management solutions, where agriculture nets provide effective physical barriers against insect infestations. This transition aligns with the European Green Deal objectives that aim to reduce the use and risk of chemical pesticides by 50% by 2030, as stated by the European Commission. The integration of sustainable farming practices with protective netting technologies represents a fundamental shift in how European farmers approach crop protection and yield optimization in an era of climate uncertainty.

MARKET DRIVERS

Increasing Frequency of Extreme Weather Events Drives Demand for Protective Netting Solutions

The escalating occurrence of severe weather phenomena across Europe is one of the major factors propelling the expansion of the European agriculture nets market. Climate change has intensified the frequency and severity of hailstorms, strong winds, and excessive solar radiation, which directly threaten agricultural productivity. According to recent meteorological and insurance data, hail is a major driver of economic losses for the agricultural sector, with individual severe events regularly inflicting losses in the billions of dollars across Europe. Countries like Italy, France, and Germany experience particularly devastating hail events during spring and summer months when crops are most vulnerable. Hail protection nets have demonstrated effectiveness in significantly reducing crop damage by providing a physical barrier that absorbs the impact energy of hailstones. Shade nets also play a crucial role in regions experiencing prolonged heatwaves where temperatures frequently exceed 35°C. As per the Copernicus Climate Change Service, recent years have seen record-breaking temperatures across the Mediterranean region, with averages well above historical norms. Farmers in Spain and Greece utilize shade nets to reduce ambient temperature, thereby preventing sunburn on fruits and maintaining optimal photosynthesis rates. Windbreak nets protect crops from desiccation and physical damage caused by strong gusts, which have increased in intensity due to changing atmospheric patterns. The economic imperative to safeguard high-value crops against unpredictable weather conditions continues to drive substantial investment in protective netting infrastructure across European agricultural operations.

Stringent Regulations on Chemical Pesticide Usage Accelerate Adoption of Physical Barrier Methods

The European Union’s rigorous regulatory framework governing pesticide application has fundamentally altered pest management strategies, which is prompting widespread adoption of agriculture nets as viable non-chemical alternatives and further boosting the European agriculture nets market growth. The Farm to Fork Strategy launched by the European Commission mandates a 50% reduction in chemical pesticide usage by 2030 alongside a 25% increase in organic farming area. As per Eurostat, organic farmland in the EU reached 16.9 million hectares in 2022, which is representing 10.5% of total agricultural area. This regulatory pressure compels conventional farmers to explore integrated pest management solutions that minimize chemical dependency while maintaining crop protection standards. Anti-insect nets create physical barriers that prevent pest infiltration without resorting to synthetic chemicals, thereby aligning with both regulatory requirements and consumer preferences for residue-free produce. According to sources, fine mesh nets can effectively reduce aphid and whitefly populations in greenhouse vegetable production. Bird netting addresses another significant challenge, as bird presence in agricultural landscapes is high, and protective measures are necessary to prevent crop loss. Traditional deterrent methods often involve harmful chemicals or noise devices that face increasing restrictions under environmental protection laws. Agriculture nets provide a sustainable solution that protects crops throughout the growing season without ecological side effects. The rising consumer awareness regarding food safety and environmental sustainability further reinforces this trend, with a significant majority of European consumers expressing a willingness to pay premium prices for organically produced fruits and vegetables. This market dynamic creates compelling economic incentives for farmers to invest in protective netting systems that ensure compliance with evolving regulatory standards while meeting consumer expectations for clean and safe produce.

MARKET RESTRAINTS

High Initial Investment Costs Restrict Market Penetration among Small Scale Farmers

The substantial capital expenditure required for installing comprehensive agriculture netting systems presents a significant barrier for the European agriculture nets market expansion, particularly for small and medium-sized farming operations that dominate the European agricultural landscape. A complete hail protection system for orchards requires a significant upfront investment in materials and installation, which can represent a considerable financial burden for farmers operating on thin margins. The European CAP Network reports that nearly two-thirds of all holdings in the EU are small, covering less than 5 hectares of agricultural land. These smaller operations often lack access to favorable financing options or government subsidies that could offset installation costs. While larger commercial enterprises can amortize these expenses over extensive cultivated areas, smallholders struggle to justify the investment given their limited scale of production. The return on investment period typically spans 3 to 5 years, which requires stable market conditions and consistent crop yields to realize projected benefits. Economic volatility, exacerbated by recent energy crises and inflationary pressures, has further constrained farm budgets, with agricultural input costs rising by 30% in 2022 as per Eurostat. Many farmers prioritize immediate operational needs over long-term infrastructure improvements when faced with cash flow constraints. The fragmented nature of European agriculture, with millions of small family-owned farms, complicates economies of scale that could potentially reduce per-unit costs. Additionally, maintenance requirements, including periodic repairs, replacement of damaged sections, and structural reinforcements, add recurring expenses that deter budget-conscious farmers. Without adequate financial support mechanisms or innovative leasing models, the high entry cost continues to limit widespread adoption, particularly among the demographic segment that constitutes the majority of European agricultural producers.

Complex Installation Requirements and Technical Expertise Gaps Impede Widespread Deployment

The technical complexity associated with proper installation and maintenance of agriculture nets creates substantial operational challenges that hinder efficient market penetration across diverse farming communities, which is further impeding the regional market expansion. Professional installation of large-scale netting systems requires specialized equipment, engineering knowledge, and experienced labor forces that are not readily available in many rural European regions. According to safety and agricultural associations, improper installation often leads to premature degradation and reduced protective efficacy. The structural integrity of netting systems depends on precise tensioning, appropriate pole spacing, and secure anchoring methods that demand technical proficiency beyond typical farming skills. Many farmers lack access to qualified installers, particularly in remote agricultural areas where service providers are scarce. The shortage of skilled agricultural technicians remains a challenge, as the number of farm managers with full agricultural training is relatively low across the EU. DIY installation attempts often result in suboptimal performance, including sagging nets, inadequate coverage, and vulnerability to wind damage. Maintenance activities, such as debris removal, tension adjustment, and damage repair, require regular attention that competes with other critical farm operations during peak seasons. The learning curve associated with managing netting systems discourages adoption among older farmers who constitute a large portion of the EU agricultural workforce as per Eurostat statistics. Training programs specifically focused on netting installation and maintenance remains insufficient in many regions, with limited access to dedicated modules in agricultural extension services. This knowledge gap results in inefficient utilization of installed systems, reduced lifespan of materials, and diminished confidence in the technology overall.

MARKET OPPORTUNITIES

Integration with Precision Agriculture Technologies Creates New Growth Avenues

The convergence of agriculture nets with digital farming technologies is a promising opportunity for the European agriculture nets market. Smart netting systems equipped with embedded sensors can monitor microclimatic conditions, including temperature, humidity, light intensity, and wind speed, providing real-time data that optimizes crop management strategies. According to industry reports, the precision farming market in Europe is growing at a significant rate, creating a receptive market for integrated netting solutions. These intelligent systems enable farmers to adjust shading levels dynamically based on solar radiation measurements, improving photosynthesis efficiency. Internet of Things-enabled nets can detect structural stress points and predict maintenance needs before failures occur, reducing downtime and extending product lifespan. The European Commission’s digital initiatives aim to improve connectivity in rural areas, facilitating the seamless integration of sensor networks within protective structures. Data analytics platforms process information collected from net-mounted sensors to generate actionable insights regarding irrigation scheduling, pest activity patterns, and harvest timing optimization. Vertical farming operations in urban environments increasingly combine layered netting systems with automated climate control, creating highly controlled production environments that maximize yield per square meter. The growing emphasis on sustainable intensification drives demand for technologies that enhance productivity without expanding land use. Collaborative projects between technology providers and net manufacturers are developing standardized communication protocols, ensuring interoperability between different farming equipment brands. This technological synergy positions agriculture nets as central components of next-generation farming infrastructure rather than standalone protective measures.

Expansion of Organic Farming Practices Opens Untapped Market Segments

The rapid expansion of organic agriculture across Europe creates substantial growth opportunities for agriculture net manufacturers targeting farmers who prioritize chemical-free pest management solutions. Organic farmland in the European Union has reached 16.9 million hectares, reflecting a steady growth trajectory. This expansion aligns with the European Green Deal target of dedicating 25% of agricultural land to organic production by 2030. Organic certification standards strictly prohibit synthetic pesticide usage, making physical barriers like anti-insect nets essential components of compliant farming systems. The organic fruit and vegetable sector particularly benefits from netting applications, as growers look for effective alternatives to synthetic sprays. Premium pricing for organic produce provides farmers with additional revenue streams that justify investments in high-quality protective infrastructure. Consumer demand for organic products continues to strengthen, with retail sales reaching tens of billions of euros across the EU. Specialized netting products designed specifically for organic operations feature durable materials and non-toxic treatments that meet stringent certification requirements. The development of compostable nets made from plant-based polymers addresses end-of-life disposal concerns while maintaining protective performance standards. Research institutions across Europe are collaborating with manufacturers to develop next-generation materials that decompose naturally after specified usage periods. Government subsidy programs supporting organic conversion often include provisions for infrastructure improvements, creating favorable purchasing conditions for farmers transitioning to organic methods. This financial backing reduces adoption barriers and accelerates market penetration among conventional farmers considering organic conversion. The alignment between regulatory frameworks, consumer preferences, and technological capabilities positions agriculture nets as indispensable tools for the expanding organic sector.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Price Fluctuations Disrupt Production Stability

The supply chain disruptions and volatile raw material costs that undermine production planning and pricing stability for manufacturers are likely to challenge to the European agriculture nets market expansion. The primary materials used in net production, including polyethylene, polypropylene, and specialized polymers, are derived from petroleum-based feedstocks whose prices fluctuate dramatically in response to global energy market dynamics. According to European industry associations, raw material costs for agricultural plastics have experienced significant volatility driven by energy price spikes and geopolitical tensions affecting supply routes. Manufacturing facilities across Europe have occasionally experienced production delays during peak demand seasons as suppliers struggled to secure consistent material deliveries. The dependency on imported raw materials exposes European manufacturers to currency exchange rate risks and international trade policy changes. Transportation costs for distributing finished products remain a significant factor, compressing profit margins for net producers. Labor shortages in manufacturing sectors further compound these challenges. Small and medium-sized manufacturers often lack the bargaining power to negotiate favorable terms with raw material suppliers, leaving them vulnerable to price shocks. Inventory management becomes increasingly complex as companies balance the need for adequate stock levels against the risk of holding depreciating assets during price declines. Quality consistency can suffer when manufacturers substitute materials to control costs, potentially compromising product performance and customer satisfaction. The cumulative effect of these supply chain pressures often forces producers to pass costs onto farmers who already operate under tight financial constraints. Long-term contracts with fixed pricing become difficult to sustain in such volatile conditions, creating uncertainty for both suppliers and buyers throughout the value chain.

Environmental Concerns Regarding Plastic Waste and Recycling Infrastructure Deficiencies

The environmental footprint of plastic-based agriculture nets generates growing scrutiny from regulators, consumers, and environmental organizations, which is further challenging the regional market growth. Traditional polyethylene and polypropylene nets persist in the environment for decades if not properly collected and recycled, contributing to soil contamination and microplastic pollution. According to the European Environmental Agency, current recycling rates for agricultural plastic waste vary significantly across the EU, with significant amounts still ending up in landfills or incineration facilities. Farmers face logistical challenges in removing used nets from fields, cleaning them of soil and organic debris, and transporting them to designated recycling centers. Contamination with pesticides, fertilizers, and plant residues complicates the recycling process, requiring specialized washing facilities that are not universally available. The European Commission’s Single-Use Plastics Directive increasingly targets agricultural applications, prompting manufacturers to reformulate products with recyclable or biodegradable alternatives. However, these sustainable materials often face challenges in matching the mechanical properties and lifespans of conventional plastics. Public awareness campaigns highlighting plastic pollution in agricultural landscapes have intensified pressure on farmers to adopt environmentally responsible practices. Retailers and food processors implementing sustainability criteria in their supply chains increasingly require proof of proper net disposal from their agricultural suppliers. The lack of standardized labeling and tracking systems makes it difficult to verify recycling claims and ensure accountability throughout the product lifecycle. Manufacturers investing in circular economy initiatives face higher production costs that must be balanced against market willingness to pay premium prices for eco-friendly alternatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.76% |

| Segments Covered | By Product, Material, Form, Price Range, Distribution Channel, Application, End-user, Country |

| Various Analyses Covered | Global, Regional, and country Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | Belton Industries., Smart Net Systems Ltd., Netfabrik, Raschier Group, Diatex, Garware Technical Fibres Limited, Thrace Group, Inc., Agriplast Tech India Pvt. Ltd., Agrotextiles International, Schweitzer-Mauduit International, Inc., wellcoindustries, Alphatex, Cittadini S.p.A, Zhongshan Hongjun Nonwovens Co. Ltd., Beaulieu Technical Textiles |

SEGMENTAL ANALYSIS

By Product Insights

The shading nets segment dominated the market by holding the highest share of the European market in 2025 due to their critical role in mitigating heat stress and optimizing light exposure for high-value crops and the increasing frequency of extreme temperature events across Southern and Central Europe, which necessitates precise microclimate control. According to the Copernicus Climate Change Service, average summer temperatures in Mediterranean regions have risen significantly over the past decade, leading to widespread sunburn damage in fruit orchards. Shading nets reduce solar radiation by 30% to 70%, depending on mesh density, thereby preventing thermal stress and maintaining photosynthetic efficiency. As per Eurostat, horticultural production in Spain and Italy accounts for a substantial portion of total European fruit and vegetable output, which is making these nations primary adopters of shading technologies. The versatility of shading nets allows application across diverse crops, including berries, grapes, and ornamental plants, which require specific light conditions for optimal quality. Proper shading can improve water use efficiency by reducing evapotranspiration rates during peak heat periods, which aligns with European Union water scarcity directives that mandate sustainable irrigation practices. Furthermore, the aesthetic quality of produce, such as uniform coloration in apples and peppers, is significantly enhanced under controlled light conditions, driving premium pricing for shaded crops. The economic return on investment for shading systems is typically realized within two growing seasons due to reduced crop loss and improved marketability. Manufacturers continue to innovate with adjustable shading systems that respond to real-time weather data, further cementing the dominance of this segment in the European agricultural landscape.

However, the anti-insect nets segment represent the fastest-growing segment in the Europe agriculture nets market and is estimated to record a promising CAGR of 6.2% over the forecast period owing to the stringent regulatory frameworks targeting chemical pesticide reduction and the simultaneous rise in organic farming adoption. The European Commission’s Farm to Fork Strategy mandates a 50% reduction in chemical pesticide usage by 2030, compelling conventional farmers to adopt physical barrier methods for pest management. As per Eurostat, the area under organic cultivation in the European Union continues to grow, reflecting a consistent increase in certified organic land. Anti-insect nets provide an effective non-chemical solution that prevents pest infiltration while allowing adequate air circulation and pollination. Research published by agricultural journals demonstrates that fine mesh nets can effectively reduce pest populations in greenhouse environments. The growing consumer preference for residue-free produce further accelerates demand, with a significant majority of European shoppers willing to pay premium prices for organically certified fruits and vegetables. Additionally, the emergence of invasive species has heightened the need for robust physical barriers that traditional chemical controls struggle to address effectively. Technological advancements in net manufacturing have produced ultra-fine meshes that block even the smallest pests without compromising structural integrity or light transmission. These factors collectively position anti-insect nets as the most dynamic growth segment in the European agricultural protection market.

By Material Insights

The plastic materials segment led the market by holding the largest share of the European market in 2025 due to their superior durability, cost-effectiveness, and versatility in application. Polyethylene and polypropylene remain the predominant materials owing to their resistance to ultraviolet radiation, moisture, and mechanical stress. The agricultural sector consumes over 1 million tons of plastic films and nets annually in the European Union, representing a significant portion of total agricultural plastic usage. The lightweight nature of plastic nets facilitates easy installation and reduces structural support requirements compared to heavier alternatives like metal. Manufacturing processes for plastic nets have achieved high levels of standardization, enabling mass production at competitive prices that appeal to both large commercial farms and smallholders. Conventional plastic nets typically offer a lifespan ranging from 5 to 10 years, depending on environmental conditions, providing long-term value for farmers. The recyclability of certain plastic types, although currently limited by infrastructure constraints, offers potential for circular economy integration, which aligns with European sustainability goals. Advances in polymer technology have introduced stabilized formulations that resist degradation from prolonged sun exposure, extending product longevity and reducing replacement frequency. The adaptability of plastic materials allows for customization of mesh size, color, and tensile strength to meet specific crop protection needs. Furthermore, the established supply chain for raw materials ensures consistent availability across European markets, minimizing procurement delays. These combined advantages solidify the position of plastic as the dominant material choice for agricultural netting applications throughout the region.

By Price Range Insights

The mid-range price segment held the major share of the European market in 2025 due to its optimal balance between quality, durability, and affordability for the majority of farmers. This segment caters to conventional farmers who require reliable protection without the premium costs associated with high-end specialized products. Small and medium-sized enterprises constitute the majority of all agricultural holdings in the European Union, making cost-effective solutions essential for operational viability. Mid-range nets typically offer a lifespan of 5 to 7 years, with adequate ultraviolet stabilization and tensile strength to withstand moderate weather conditions. As per Eurostat, the average annual income per farm in the EU varies significantly but remains constrained for many operations, necessitating prudent capital expenditure decisions. The mid-range segment benefits from established distribution channels and widespread availability, ensuring that farmers can access products without lengthy procurement delays. Manufacturers in this segment focus on standardized specifications that meet general protection needs for common crops such as vegetables, fruits, and ornamentals. The competitive landscape encourages continuous improvement in material quality while maintaining accessible pricing structures. Bulk purchasing agreements and cooperative buying arrangements among farmer associations further enhance the attractiveness of mid-range products by offering volume discounts. This segment also benefits from moderate maintenance requirements that do not demand specialized technical expertise, reducing overall ownership costs. The alignment between performance expectations and budgetary constraints makes the mid-range segment the preferred choice for the broadest demographic of European agricultural producers seeking dependable crop protection solutions.

On the other side, the premium price segment is the fastest-growing category in the Europe agriculture nets market and is predicted to showcase a CAGR of 10.5% over the forecast period owing to the increasing demand for high-performance specialized solutions, the expansion of high-value crop production, where marginal improvements in yield quality justify substantial investments in superior protective infrastructure. Premium fruits such as berries, cherries, and exotic varieties command prices that are 30% to 50% higher than standard produce, creating economic incentives for advanced protection systems. Premium nets feature enhanced ultraviolet stabilization, superior tensile strength, and specialized coatings that extend lifespan beyond 10 years while providing optimized microclimatic control. Advanced shading nets with adjustable light transmission capabilities can improve photosynthetic efficiency, directly impacting yield volume and quality. Large-scale commercial operations and integrated agricultural enterprises are primary adopters of premium products, as they prioritize long-term asset value and operational efficiency. The integration of smart technologies, such as embedded sensors for real-time monitoring, further distinguishes premium offerings, appealing to technologically advanced farming operations. Government grants supporting innovation in agricultural technology often cover portions of premium equipment costs, reducing financial barriers for early adopters. The growing emphasis on precision agriculture and sustainable intensification drives demand for premium products that offer superior return on investment through durability and advanced technical features.

COUNTRY LEVEL ANALYSIS

Spain Agriculture Nets Market Analysis

Spain held a prominent position in the Europe agriculture nets market in 2025 as the largest producer of fruits and vegetables in the European Union. According to the European Commission, the country accounts for approximately 12% of total European horticultural output, making protective netting essential for maintaining crop quality and yield. The Mediterranean climate exposes Spanish agriculture to intense solar radiation, hailstorms, and pest pressures, particularly in regions like Andalusia and Murcia where intensive farming prevails. Shading nets are extensively used in citrus orchards and berry plantations to prevent sunburn and optimize ripening conditions. According to the Spanish Ministry of Agriculture, Fisheries and Food, hail protection nets cover a significant portion of fruit trees, reflecting the severity of weather-related risks. The expansion of organic farming in Spain has accelerated demand for anti-insect nets, with organic farmland increasing at a notable rate as the country now boasts over 2.9 million hectares of organic land. Government initiatives under the National Strategic Plan for the Common Agricultural Policy provide subsidies for sustainable infrastructure, including protective netting systems. The export-oriented nature of Spanish agriculture requires premium quality produce that meets strict international standards, driving investment in advanced netting technologies. Local manufacturers have developed specialized products suited to regional climatic conditions, creating a robust domestic supply chain. The integration of precision agriculture technologies with netting systems is gaining traction among large commercial operations seeking to optimize resource use. Spain’s strategic location and favorable growing conditions ensure continued leadership in high-value crop production, sustaining strong demand for agriculture nets across multiple segments.

Italy Agriculture Nets Market Analysis

Italy is expected to strengthen its market position over the next few years by focusing on specialized protection for its high-value viticulture and fruit sectors. The country is renowned for viticulture, olive cultivation, and fruit production, which require specialized protective measures to ensure premium quality outputs. According to the Italian Ministry of Agriculture, the country utilizes extensive protective netting, primarily for hail protection in northern regions and shade management in southern areas. The Po Valley experiences frequent hailstorms during spring and summer, causing substantial damage to apple, pear, and peach orchards, necessitating robust hail nets. As per industry reports, investment in protective agricultural infrastructure in Italy has grown steadily, reflecting the increasing awareness of climate-related risks. The expansion of organic farming in Italy, with over 2.1 million hectares under organic certification, drives demand for anti-insect nets that comply with strict regulatory standards. Regional governments in Lombardy, Emilia-Romagna, and Veneto offer financial incentives for farmers adopting sustainable protection methods. The prevalence of small and medium-sized family farms presents challenges in terms of initial investment costs, but cooperative purchasing models help mitigate financial barriers. Italian manufacturers are leaders in designing aesthetically pleasing netting systems that blend with scenic landscapes, particularly in wine-producing regions. The emphasis on geographical indication labels for Italian produce requires consistent quality that protective nets help maintain. Continued innovation in material science and installation techniques supports Italy’s strong position in the European agriculture nets market.

France Agriculture Nets Market Analysis

France is likely to see steady growth in its agriculture nets market over the next few years as it continues to prioritize sustainable and agroecological farming practices. The country produces a wide range of crops including grapes, apples, stone fruits, and vegetables that benefit from protective netting applications. According to the French Ministry of Agriculture, tens of thousands of hectares of orchards are equipped with hail protection nets, particularly in regions prone to severe weather such as Alsace and Aquitaine. The French government’s National Strategy for Agroecology promotes reduced pesticide usage, encouraging the adoption of physical barriers like anti-insect nets. As per official agricultural data, organic farmland in France has expanded significantly, representing a growing percentage of the total agricultural area. This growth drives demand for certified organic-compliant netting solutions that prevent pest infestations without chemical interventions. Viticulture represents a significant application area where bird nets protect grape clusters from damage during ripening periods. The Champagne and Bordeaux regions extensively utilize bird netting to safeguard premium wine production. French manufacturers focus on developing durable and aesthetically discreet netting systems that preserve landscape integrity. Subsidies under the European Agricultural Fund for Rural Development support infrastructure improvements, including protective netting installations. The strong cooperative structure in French agriculture facilitates collective investment in shared protective infrastructure, reducing individual financial burdens. Climate change impacts, including the increased frequency of extreme weather events, continue to drive the adoption of comprehensive protection systems across French agricultural operations.

Germany Agriculture Nets Market Analysis

Germany is anticipated to maintain a strong trajectory in the agriculture nets market by leveraging technological advancements and meeting strict environmental sustainability targets in the coming years. The country focuses on high-value crops such as hops, berries, and vegetables that require precise protection to maintain quality standards. According to the Federal Statistical Office of Germany, the number of agricultural holdings utilizing protective structures has seen consistent growth, reflecting increasing investment in crop protection. Hail protection is particularly critical in southern regions like Bavaria and Baden-Württemberg, where severe storms frequently damage fruit orchards. As per the German Agricultural Society, anti-insect nets are increasingly adopted in greenhouse vegetable production to comply with strict pesticide reduction targets. The German government’s National Action Plan on the Sustainable Use of Plant Protection Products mandates significant reductions in chemical usage, driving demand for physical barrier methods. Organic farming in Germany covers approximately 1.6 million hectares, representing 11% of total agricultural land, according to the Federal Ministry of Food and Agriculture. This expansion fuels demand for certified organic-compliant netting solutions. German engineering excellence contributes to the development of sophisticated netting systems integrated with automation and sensor technologies. The country’s strong manufacturing base supports local production of high-quality nets, reducing dependency on imports. Cooperative structures among German farmers facilitate knowledge sharing and collective procurement, enhancing market penetration. The emphasis on sustainability and technological innovation ensures Germany’s continued relevance in the European agriculture nets market.

Netherlands Agriculture Nets Market Analysis

The Netherlands is expected to remain a global hub for innovative agricultural netting solutions as it continues to export its advanced greenhouse technology over the next few years. The country accounts for a disproportionate share of European greenhouse vegetable and flower production, requiring advanced climate control and protective solutions. According to Statistics Netherlands, thousands of hectares of greenhouse area utilize sophisticated shading and screening systems that function similarly to agriculture nets. The Dutch approach emphasizes precision agriculture, integrating netting with automated climate control systems to optimize growing conditions. As per academic research from Wageningen University, greenhouse operators achieve significant resource use efficiency improvements through integrated shading and ventilation strategies. The high intensity of production necessitates durable and high-performance materials that withstand continuous operation. Anti-insect nets are essential in Dutch greenhouse complexes to prevent pest entry while maintaining adequate ventilation. The Netherlands serves as a testing ground for innovative netting technologies, including smart nets with embedded sensors for real-time monitoring. The export of Dutch agricultural technology, including netting systems, to other European countries strengthens its market influence. Government support for sustainable greenhouse horticulture through subsidies and research funding drives continuous innovation. The concentration of expertise in horticultural engineering positions the Netherlands as a key influencer in setting technical standards for agriculture nets across Europe. The focus on circular economy principles encourages the development of recyclable and biodegradable netting materials.

COMPETITIVE LANDSCAPE

The competition in the Europe agriculture nets market is characterized by a mix of established manufacturers and emerging innovators striving to differentiate through technology and sustainability. Leading companies compete primarily on product quality durability and adherence to environmental standards rather than price alone. The market features moderate consolidation with key players expanding their geographic footprint through strategic acquisitions and partnerships. Innovation drives competitive advantage as firms introduce smart netting systems integrated with digital monitoring tools for precision agriculture. Regulatory compliance serves as a significant barrier to entry favoring established entities with resources to meet stringent European Union directives on plastic waste and pesticide reduction. Regional players maintain strong positions by offering localized solutions tailored to specific climatic conditions and crop requirements. The threat of substitute products remains low due to the unique effectiveness of physical barriers in organic and sustainable farming systems. Competitive intensity is heightened by the growing demand for eco friendly alternatives prompting continuous investment in biodegradable materials. Customer loyalty is increasingly influenced by after sales support and technical assistance ensuring optimal product performance.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe agriculture nets market are

- Belton Industries.

- Smart Net Systems Ltd.

- Netfabrik

- Raschier Group

- Diatex

- Garware Technical Fibres Limited

- Thrace Group, Inc.

- Agriplast Tech India Pvt. Ltd.

- Agrotextiles International

- Schweitzer-Mauduit International, Inc.

- Wellcoindustries

- Alphatex

- Cittadini S.p.A

- Zhongshan Hongjun Nonwovens Co. Ltd.

- Beaulieu Technical Textiles

Top Players In The Market

- Raschier Group stands as a prominent manufacturer specializing in high quality agricultural protection solutions across European markets. The company focuses on producing durable hail nets shade nets and anti insect nets using advanced polymer technologies. Raschier has recently expanded its production capacity in Italy to meet growing demand for sustainable farming inputs. Their commitment to innovation involves developing biodegradable netting options that align with European environmental regulations. The company actively collaborates with research institutions to enhance product durability and ultraviolet resistance. By offering customized solutions for various crops including fruits vegetables and ornamentals Raschier strengthens its reputation for reliability. Recent investments in automated manufacturing processes have improved efficiency and reduced lead times for customers. This strategic focus on quality and sustainability ensures Raschier remains a preferred partner for farmers seeking long term crop protection systems that support both productivity and ecological responsibility.

- Netfabrik operates as a key supplier of specialized agricultural nets serving diverse farming sectors throughout Europe. The company distinguishes itself through rigorous quality control and extensive product testing under real world conditions. Netfabrik recently launched a new line of smart shading nets equipped with sensor integration capabilities for precision agriculture applications. This innovation allows farmers to monitor microclimatic data directly through their protective structures. The firm has strengthened its distribution network by partnering with local agricultural cooperatives in Spain and France. Netfabrik emphasizes customer education by providing technical support for proper installation and maintenance procedures. Their recent expansion into Eastern European markets demonstrates a commitment to broadening geographic reach. By focusing on technological advancement and customer service Netfabrik enhances its competitive position. The company continues to invest in research and development to create next generation materials that offer superior performance while minimizing environmental impact.

- Agrotextiles International is a leading provider of comprehensive crop protection solutions with a strong presence in Western and Central Europe. The company offers a wide range of products including windbreak nets bird nets and hail protection systems tailored to specific regional needs. Agrotextiles recently introduced a recycling program for used agricultural nets addressing growing concerns about plastic waste management. This initiative supports circular economy principles and enhances brand loyalty among environmentally conscious farmers. The firm has upgraded its manufacturing facilities to incorporate energy efficient production methods reducing its carbon footprint. Strategic partnerships with agricultural universities enable Agrotextiles to stay at the forefront of scientific advancements in crop protection. Their recent marketing campaigns highlight the economic benefits of using premium quality nets for high value crops. By combining product innovation with sustainable practices Agrotextiles International solidifies its role as a trusted advisor and supplier in the evolving European agricultural landscape.

Top Strategies Used By Key Market Participants

Key players in the Europe agriculture nets market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation remains central as companies develop advanced materials with enhanced durability and environmental compatibility. Manufacturers invest heavily in research and development to create biodegradable and recyclable netting solutions that comply with stringent European regulations. Strategic partnerships with agricultural research institutions facilitate the creation of technologically advanced products such as smart nets with embedded sensors. Expansion of distribution networks through collaborations with local cooperatives and distributors ensures broader market reach particularly in emerging regions. Companies also focus on customer education and technical support services to improve installation quality and product lifespan. Sustainability initiatives including recycling programs and eco friendly manufacturing processes strengthen brand reputation among environmentally conscious consumers. Diversification of product portfolios to address specific crop needs and regional climatic conditions allows firms to capture niche market segments effectively.

MARKET SEGMENTATION

This research report on the Europe agriculture nets market is segmented and sub-segmented into the following categories.

By Product Type

- Shading Nets

- Anti-Hail

- Anti-Insects

- Windbreak

- Others

By Material Type

- Plastic

- Metal

- Rubber

- Others

By Form

- Woven

- Non-Woven

By Price Range

- Economy

- Mid-Range

- Premium

By Distribution Channel

- Online

- Offline

By Application

- Horticulture And Floriculture

- Farming Area

- Animal Husbandry

- Aquaculture

By End Use

- Industrial Agriculture

- Sustainable Agriculture

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

Why is the Europe agriculture nets market experiencing steady growth?

The market is expanding due to increasing adoption of protected cultivation, rising demand for high-quality crops, and growing investments in sustainable farming practices across Europe.

What are agriculture nets and how are they used in farming?

Agriculture nets are protective coverings used to shield crops from excessive sunlight, insects, birds, hail, wind, and adverse weather while improving growing conditions.

Which product segment accounts for the largest share of the Europe agriculture nets market?

Shading nets account for the largest market share due to their widespread use in greenhouses, nurseries, horticulture, and open-field cultivation.

How do agriculture nets improve crop productivity and quality?

They regulate light intensity, reduce crop damage, protect against pests and weather, improve microclimatic conditions, and enhance overall crop yield and quality.

What factors are driving the growth of the Europe agriculture nets market?

Increasing greenhouse cultivation, rising horticultural production, growing demand for climate-resilient farming, and government support for sustainable agriculture are driving market growth.

Which agricultural sectors generate the highest demand for agriculture nets?

Horticulture, fruit cultivation, vegetable farming, floriculture, nurseries, vineyards, and greenhouse farming are the primary end users.

What trends are shaping the future of the Europe agriculture nets market?

UV-stabilized netting, recyclable materials, smart agriculture, precision farming, climate-adaptive cultivation, and sustainable crop protection solutions are shaping the market.

How are manufacturers improving agriculture net products?

Manufacturers are developing lightweight, durable, UV-resistant, recyclable, and weather-resistant nets with enhanced protection and longer service life.

What challenges could affect the growth of the Europe agriculture nets market?

High installation costs, fluctuating raw material prices, disposal of plastic materials, changing weather conditions, and varying adoption among small-scale farmers could affect market growth.

Which countries are expected to lead the Europe agriculture nets market?

Spain, Italy, France, Germany, and the Netherlands are leading markets due to extensive greenhouse farming, advanced horticulture, and strong investments in protected agriculture.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com