Europe Animation Market Size, Share, Trends, and Growth Analysis Report, Segmented by Revenue Stream and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$82 BnMarket Estimate, 2026

$86.10 BnMarket Forecast, 2034

$127.21 BnCAGR, 2026–2034

5%Europe Animation Market Report Summary

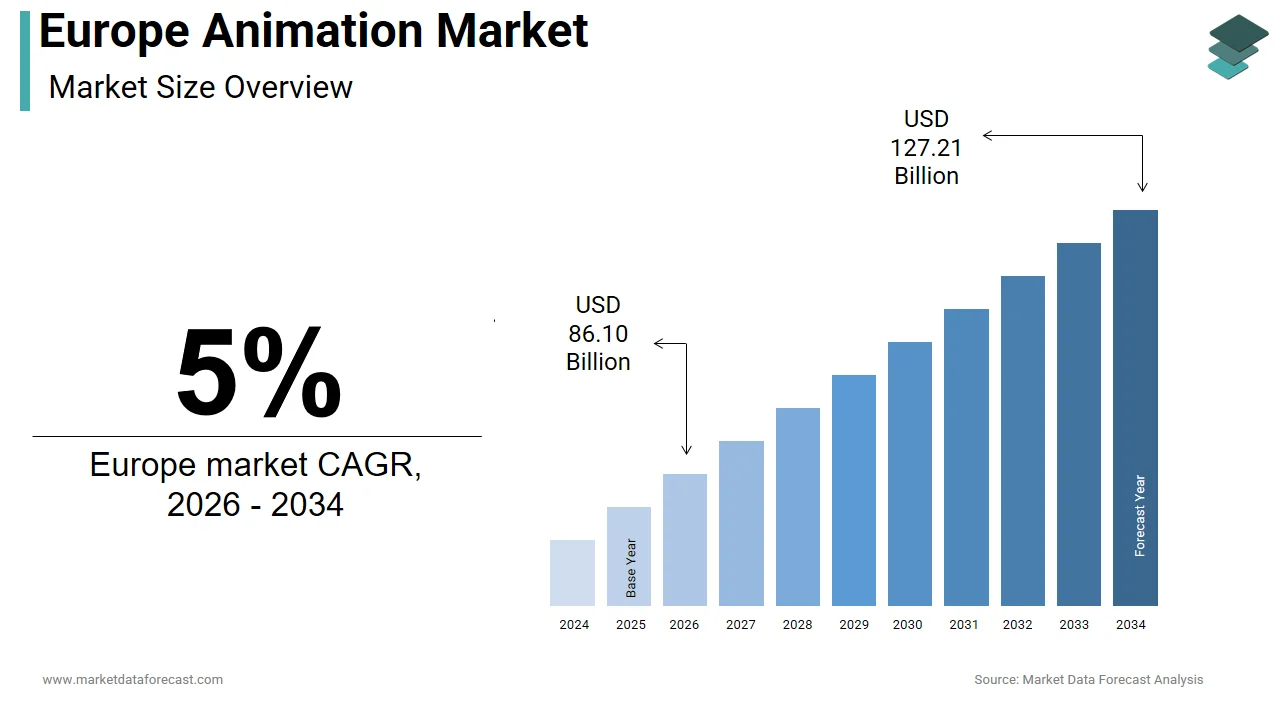

The Europe animation market was valued at USD 82 billion in 2025, is estimated to reach USD 86.10 billion in 2026, and is projected to reach USD 127.21 billion by 2034, growing at a CAGR of 5% from 2026 to 2034. Market growth is driven by rising demand for animated content across streaming platforms, increasing investment in digital entertainment, and expanding applications in film, television, gaming, and advertising. Animation plays a vital role in enhancing storytelling, audience engagement, and visual effects across media formats. Additionally, the rapid expansion of over-the-top (OTT) platforms, growing international co-productions, and technological advancements in animation software are supporting steady market growth across Europe.

Key Market Trends

- Rising demand for animated content on OTT and streaming platforms.

- Increasing investment in original animated films, series, and digital media.

- Growing use of animation in gaming, advertising, and virtual production.

- Expansion of international co-productions and global content distribution.

- Increasing adoption of advanced animation technologies and visual effects tools.

Segmental Insights

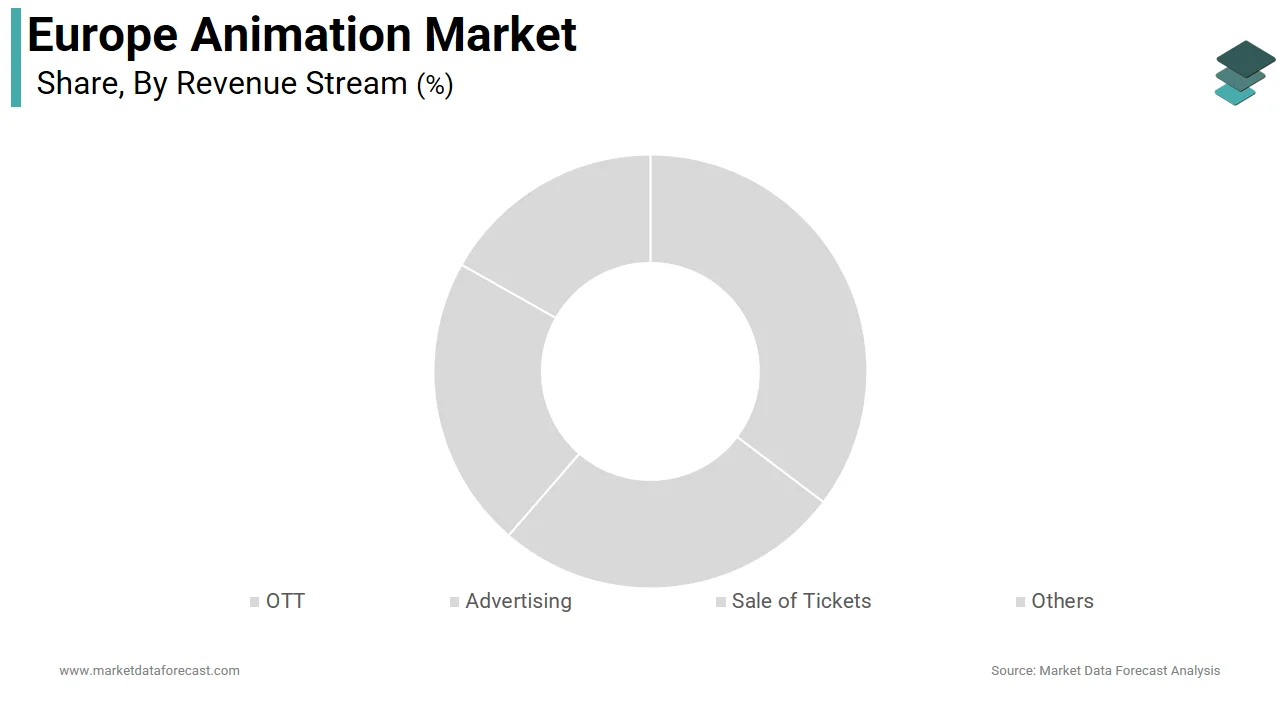

- Based on revenue stream, the OTT platforms segment dominated the Europe animation market by accounting for 40.9% share in 2025, driven by increasing consumption of streaming content and rising investment in original animated programming by digital platforms.

Regional Insights

The Europe animation market is witnessing steady growth across major countries, supported by strong creative industries, government funding, and expanding digital content production.

- France led the market by capturing 23.3% share in 2025, driven by strong government support, tax incentives, and globally recognized animation studios and production houses.

- The United Kingdom held a significant share, supported by leadership in English-language animation production, strong technical innovation, and international co-production collaborations.

- Germany is expected to register a healthy CAGR during the forecast period, supported by public broadcasting mandates, regional film funding programs, and increasing investment in animation production.

Competitive Landscape

The Europe animation market is highly competitive, with global media companies, animation studios, and digital content creators focusing on expanding content portfolios, improving animation quality, and strengthening international distribution networks. Market participants are investing in advanced animation technologies, OTT partnerships, and original content development to enhance audience reach and engagement.

Leading companies operating in the Europe animation market include Warner Bros. Discovery, Sony Pictures Entertainment, DreamWorks Animation, The Walt Disney Company, Paramount Global, Netflix, Toei Animation, and Xilam Animation.

Europe Animation Market Size

The Europe animation market was valued at USD 82 billion in 2025, is estimated to reach USD 86.10 billion in 2026, and is projected to reach USD 127.21 billion by 2034, growing at a CAGR of 5% from 2026 to 2034.

Animation encompasses the creation, production, and distribution of animated content across film, television, streaming platforms, advertising, gaming, and immersive media such as virtual and augmented reality. This creative sector blends artistic storytelling with advanced digital technologies, including 2D hand-drawn, 3D computer-generated imagery, stop-motion, and real-time rendering to serve both entertainment and functional applications like education, simulation, and medical visualization. The market’s vitality is anchored in Europe’s rich legacy of visual arts and public support for cultural expression. As per Eurostat, the EU’s audiovisual and related sectors employ a significant workforce, with animation studios forming a critical node in this ecosystem. Concurrently, according to the European Audiovisual Observatory, European countries continue to produce a substantial number of animated feature films and short animations, which reflects sustained creative output. This cultural industrial complex operates within a unique policy environment where artistic merit, linguistic diversity, and technological innovation are actively nurtured through national film institutes and EU funding mechanisms like Creative Europe, which distinguishes it from purely commercial markets.

MARKET DRIVERS

EU Policy Support Through Creative Europe Is Sustaining Independent Production

The growth of the European animation market is primarily driven by the European Union’s Creative Europe program, which remains a cornerstone of animation financing, allocating over 260 million euros annually to cross-border audiovisual projects, with animation consistently receiving a disproportionate share due to its high production costs and cultural value. As per the European Commission, animation has received significant support through MEDIA sub-program grants, enabling studios in Belgium, Ireland, and Estonia to produce internationally competitive works without relying solely on commercial returns. This public funding de-risks experimentation, allowing creators to explore non-mainstream narratives and indigenous languages such as Catalan, Welsh, or Sami that would otherwise be economically unviable. The program also mandates co-production among at least two EU countries, fostering talent exchange and technical collaboration. This institutional scaffolding ensures a steady pipeline of European-authored animation that preserves cultural identity while achieving global festival recognition and distribution.

Rising Demand for Animated Content on Global Streaming Platforms Is Expanding Commissioning Opportunities

The aggressive content acquisition strategies of major streaming services have created unprecedented demand for original animated series tailored to European audiences, which is further contributing to the expansion of the European market. According to the European Audiovisual Observatory, global streamers have increasingly commissioned European-produced animated series, reflecting growing interest in the region’s creative output. Platforms like Netflix, Amazon Prime Video, and Disney+ now operate dedicated regional development teams in London, Paris, and Madrid, seeking locally resonant stories with global appeal. For instance, Netflix’s “Lupin” spin-off animated shorts and Amazon’s investment in French-Belgian co-productions reflect a strategic pivot toward culturally specific IP. This shift provides European studios with stable pre-sales and higher budgets, enabling them to retain creative control while accessing worldwide audiences. The result is a virtuous cycle where local authenticity meets global scale, transforming European animation from a niche art form into a commercially viable export sector.

MARKET RESTRAINTS

Fragmented Language Markets Inhibit Economies of Scale and Broad Commercial Viability

Europe’s linguistic diversity, with over 24 official EU languages and numerous regional dialects, creates significant barriers to achieving the audience scale necessary for profitable animation production. Unlike the United States or Japan, where a single language enables mass-market returns, a French-language animated series may struggle to recoup costs beyond France, Belgium, and Switzerland, limiting its budget ceiling. As per the European Film Academy, European animated features generally operate with lower production budgets compared to U.S. projects. This financial constraint forces studios to rely heavily on public subsidies or international co-productions, which introduce creative compromises and scheduling complexities. The need for dubbing or subtitling further fragments viewership and delays release windows, reducing marketing impact and merchandising potential. Consequently, even critically acclaimed works often fail to achieve commercial sustainability without continuous public support.

Intense Global Competition for Skilled Animators Is Driving Up Labor Costs and Causing Talent Drain

European animation studios face mounting pressure from North American and Asian studios that offer significantly higher salaries and access to cutting-edge pipelines, which is also hindering the expansion of the animation market in Europe. According to the International Animated Film Association, a notable share of senior animators trained in European academies have relocated to Canada, the United States, or South Korea, attracted by better compensation packages. This brain drain is particularly acute in specialized fields like rigging, simulation, and real-time engine animation, where demand outstrips local supply. In response, European studios must either raise wages, eroding already thin margins, or outsource key sequences, compromising artistic cohesion. The shortage is exacerbated by underfunded vocational programs. As per CILECT, the International Association of Film and Television Schools, many graduates lack industry-ready technical skills despite high enrollment in animation degrees. This human capital gap constrains production capacity and innovation.

MARKET OPPORTUNITIES

Integration of Real-Time Rendering Engines Is Democratizing High-Quality Production

The adoption of game-engine technologies like Unreal Engine and Unity is revolutionizing European animation workflows by enabling real-time visualization, virtual cinematography, and rapid iteration, which is a notable opportunity in the European animation market. As per Epic Games, independent animation studios across Europe have increasingly adopted real-time tools for pre-visualization and final rendering, which has streamlined production processes. This shift lowers entry barriers for small studios, allowing them to produce broadcast-quality content with leaner teams and modest budgets. Moreover, these engines facilitate seamless crossover into immersive media such as virtual production for live-action hybrids or interactive museum exhibits, opening new revenue streams beyond traditional broadcasting. The EU’s Horizon Europe program has also funded several pilot projects integrating real-time animation into educational and cultural heritage applications, positioning European creators at the forefront of next-generation storytelling.

Growing Use of Animation in Non-Entertainment Sectors Is Diversifying Revenue Streams

Beyond film and television, European animation studios are increasingly engaged in functional applications across healthcare, architecture, defense, and scientific communication, which is another prominent opportunity in the European animation market. In the medical field, studios in Germany and Sweden collaborate with universities to create 3D animated simulations of cellular processes for patient education and surgical training. According to the European Health Telematics Observatory, medical animation has witnessed notable growth driven by demand for clear visual explanations of complex treatments. Similarly, architectural firms commission animated walkthroughs for urban planning approvals, while defense contractors use simulation-based animation for personnel training. These B2B contracts provide stable, year-round income that offsets the seasonal volatility of entertainment production. By leveraging their narrative and visualization expertise in high-value professional services, European animators are building resilient, diversified business models less dependent on box office or streaming metrics.

MARKET CHALLENGES

Inadequate Access to Risk Capital Limits Scaling Beyond Public Funding Models

Despite strong creative output, European animation studios struggle to attract private equity or venture investment due to perceived high risk and long payback periods, which is a key challenge to the growth of the European animation market. As per the European Venture Capital Association, only a small portion of media-tech investments have targeted pure-play animation studios, with most capital flowing to platform or tool developers instead. This gap forces producers to rely on fragmented public grants, pre-sales, and broadcaster licenses, which rarely cover full production costs and impose rigid delivery schedules. The absence of scalable financing mechanisms prevents studios from building owned intellectual property portfolios or investing in proprietary technology, leaving them as service providers rather than rights holders. Without a robust private investment ecosystem akin to Hollywood’s studio system or Silicon Valley’s tech incubators, European animation remains vulnerable to policy shifts and unable to compete in global IP-driven markets where ownership dictates long-term value.

Evolving Audience Expectations for Interactive and Personalized Content Require New Skill Sets

Modern viewers, particularly younger demographics, increasingly expect animated content to be interactive, adaptive, or integrated into social media ecosystems, trends that demand competencies beyond traditional frame-by-frame animation, which is further challenging the expansion of the European animation market. Creating choose-your-own-adventure narratives, AI-driven character responses, or TikTok-native micro-animations requires proficiency in programming, user experience design, and data analytics. According to the European Youth Forum, younger audiences show a strong preference for animated content that allows interaction or personalization. Yet, most European animation schools still emphasize classical techniques, leaving graduates unprepared for this paradigm shift. Studios that attempt to pivot must either retrain existing staff, a costly and time-consuming process, or hire from adjacent tech sectors, disrupting creative workflows. This skills mismatch threatens to marginalize traditional studios unless they rapidly reinvent their production philosophies and talent development strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Revenue and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Warner Bros. Discovery, Inc, Sony Pictures Digital Productions Inc., DREAMWORKS ANIMATION, TOEI ANIMATION CO., LTD., Disney, Paramount, NETFLIX, AARDMAN ANIMATIONS LTD, OLM, Inc., Madman Entertainment Pty. Ltd., Cartoon Saloon, Kyoto Animation Co., Ltd., Xilam Animation SA, Pierrot Co., Ltd., Blublu Studios, NIPPON ANIMATION CO., LTD., SUNRISE, Pixeldust Framestore, Illumination Mac Guff, LAIKA, LLC, and MPC Film. |

SEGMENTAL ANALYSIS

By Revenue Stream Insights

The Over-the-top (OTT) platforms segment led the market by capturing 40.9% of the European market share in 2025. The dominance of the OTT platforms segment in the European market is driven by two structural shifts in content consumption and financing. The first is the strategic pivot of global streamers toward local original content. As per the European Commission, Netflix, Amazon Prime Video, and Disney+ have collectively invested heavily in European-produced animated series, with exclusive licensing deals providing studios with predictable upfront payments. This model replaces the volatile box office and advertising-dependent revenues of the past, enabling longer production cycles and higher artistic ambition. The second driver is changing viewer behavior. According to Eurostat, a significant share of European households subscribed to at least one streaming service in 2025, with animated content being among the most-watched genres for both children and adults. The on-demand nature of OTT aligns perfectly with fragmented viewing habits, ensuring consistent viewership and justifying continued commissioning.

The advertising-supported animation segment is estimated to witness a CAGR of 10.5% over the forecast period in the European animation market. The brands’ urgent need to engage younger audiences who actively avoid traditional commercials is one of the major factors propelling the growth of the advertising-supported animation segment in the European market. Animated short-form content, particularly on social media platforms like YouTube Shorts, Instagram Reels, and TikTok, offers high shareability and emotional resonance without triggering ad-blockers. A second major factor is the rise of branded entertainment studios within advertising agencies. In France and the UK, many top-tier agencies now operate in-house animation units producing narrative-driven campaigns for clients in gaming, fashion, and sustainable tech. As per the European Interactive Advertising Bureau, animated brand films have demonstrated stronger viewer engagement compared to live-action equivalents among younger audiences. This performance metric, combined with lower production costs and faster turnaround, makes animation an indispensable tool in modern digital marketing, transforming it from a children’s medium into a sophisticated brand communication channel.

COUNTRY-LEVEL ANALYSIS

France Animation Market Analysis

France held the leading position in the European animation market in 2025 with 23.3% of the European market share. The dominance of France in the European market is attributed to its historic commitment to audiovisual sovereignty and artistic excellence. Its market status is defined by a robust ecosystem of independent studios, public broadcasters, and state-backed financing mechanisms. As per the Centre national du cinéma et de l’image animée (CNC), significant funding has been allocated to animation projects with cultural and linguistic criteria that prioritize French-language creation. This support has nurtured globally acclaimed studios like Folivari and Xilam, whose works regularly feature at Annecy and win international awards. Additionally, France mandates that broadcasters dedicate 60% of children’s programming to European productions, ensuring consistent domestic demand. The convergence of public policy, creative talent, and institutional infrastructure makes France not just a production hub but a standard-bearer for culturally rooted animation in Europe.

United Kingdom Animation Market Analysis

The United Kingdom held a prominent share of the European animation market in 2025 due to its strength in English-language co-productions and technical innovation. Its market status is shaped by world-class studios such as Aardman Animations and Blue-Zoo, which blend artistic storytelling with cutting-edge digital pipelines. The key driver is access to global capital and distribution. As per the British Film Institute, a majority of UK animated features in 2025 were co-financed with partners from Canada, France, or South Korea. Furthermore, the UK’s National Lottery distributes substantial funding annually to animation through the BFI Film Fund, supporting both auteur-driven shorts and commercially viable series. This hybrid model of public-private financing sustains a diverse and internationally competitive animation sector.

Germany Animation Market Analysis

Germany is estimated to grow at a healthy CAGR in the European animation market over the forecast period, owing to the strong public broadcasting mandates and regional film funding bodies. Its market status is characterized by stable, non-commercial production driven by educational and cultural objectives. As per the German Federal Film Board, animation has consistently received a notable share of development funding, reflecting its perceived cultural value. Public broadcasters ARD and ZDF allocate significant airtime to domestically produced children’s animation, with minimum quotas for European origin. Germany’s federal structure empowers 16 regional film boards, such as those in Bavaria and North Rhine-Westphalia, to offer grants covering substantial portions of production costs for qualifying projects. This decentralized yet consistent support system ensures steady output even during commercial downturns.

Spain Animation Market Analysis

Spain is expected to exhibit a notable CAGR in the European animation market during the forecast period. Spain is emerging as a dynamic hub for digital-native creators and cost-efficient production. Its market status is defined by a surge in short-form and web-based animation fueled by a young, tech-savvy workforce. As per Spain’s Ministry of Culture, the country hosts a large number of animation studios, many specializing in outsourced sequences for international features or original IP for platforms like YouTube and Netflix. Government incentives, including a 30% cash rebate on animation production costs introduced in 2023, have further attracted foreign commissions. The combination of affordable talent, modern infrastructure, and fiscal support positions Spain as a high-growth, export-oriented node in Europe’s animation network.

Ireland Animation Market Analysis

Ireland is anticipated to account for a substantial share of the European animation market over the forecast period. Ireland is disproportionate to its size, due to its concentration of high-end studios and favorable tax policies. Its market status is exemplified by Cartoon Saloon and Boulder Media, whose Oscar-nominated works blend Irish folklore with universal themes. The primary driver is Section 481 of the Irish Taxes Consolidation Act, which provides a 32% refundable tax credit on eligible animation expenditures, making Ireland one of Europe’s most attractive production destinations. As per Screen Ireland, this incentive supported numerous feature-length and series projects in 2025. Additionally, Ireland’s English-speaking workforce and time zone alignment with both Europe and North America facilitate seamless collaboration with global partners. The government’s targeted investment in studio infrastructure, such as the Limerick Digital Hub, further enhances capacity. This strategic blend of fiscal advantage, creative excellence, and logistical convenience cements Ireland’s role as a premium animation powerhouse.

COMPETITIVE LANDSCAPE

The competition in the Europe animation market is defined by a dual structure comprising globally recognized studios and a vibrant network of small independent creators. Large players compete on brand recognition, technical sophistication, and access to international financing, often leveraging public subsidies to produce high-budget features and series. Simultaneously, micro-studios thrive by specializing in niche aesthetics, regional storytelling, or short-form digital content tailored for social media. The primary battleground is not just audience attention but access to skilled animators, public funding, and global distribution windows. While U.S. and Asian studios dominate commercial scale, European competitors differentiate through cultural authenticity, artistic experimentation, and policy-supported creative autonomy. However, the market remains fragmented by language, funding cycles, and talent mobility, creating both opportunities for uniqueness and challenges in achieving sustainable scale without strategic partnerships or diversified revenue models.

KEY MARKET PLAYERS

The leading companies operating in the Europe animation market include:

- Warner Bros. Discovery, Inc

- Sony Pictures Digital Productions Inc.

- DREAMWORKS ANIMATION

- TOEI ANIMATION CO., LTD.

- Disney

- Paramount

- NETFLIX

- AARDMAN ANIMATIONS LTD

- OLM, Inc.

- Madman Entertainment Pty. Ltd.

- Cartoon Saloon

- Kyoto Animation Co., Ltd.

- Xilam Animation SA

- Pierrot Co., Ltd.

- Blublu Studios

- NIPPON ANIMATION CO., LTD.

- SUNRISE

- Pixeldust Framestore

- Illumination Mac Guff

- LAIKA, LLC

- MPC Film

TOP PLAYERS IN THE MARKET

- Aardman Animations is a British studio globally renowned for its stop-motion and CGI hybrid productions such as Wallace & Gromit and Shaun the Sheep. The company contributes significantly to the European animation market by championing artisanal techniques while embracing digital innovation. Aardman maintains strong partnerships with the BBC, Netflix, and StudioCanal, ensuring the wide distribution of its culturally distinctive content. Recently, the studio expanded its real-time rendering capabilities and launched an immersive storytelling division focused on virtual reality experiences based on its iconic characters. This strategic diversification strengthens its position by extending intellectual property into experiential media and educational platforms, reinforcing its global reputation for narrative excellence and technical craftsmanship rooted in European creative values.

- Xilam is a leading French animation studio known for internationally successful series like Oggy and the Cockroaches and Zig & Sharko. The company plays a pivotal role in the European market by producing multilingual, visually driven content that transcends language barriers. Xilam has built a robust global licensing and merchandising operation, with its shows broadcast in over 180 countries. In recent years, Xilam has invested heavily in in-house 3D production pipelines and established a dedicated gaming division to adapt its franchises into interactive formats. It also co-founded a pan-European animation incubator to nurture emerging talent. These initiatives enhance its creative autonomy and revenue resilience while promoting European animation aesthetics on the world stage.

- Cartoon Saloon is an Irish studio celebrated for its hand-drawn feature films, including The Secret of Kells and Wolfwalkers, which have received multiple Academy Award nominations. The studio’s contribution lies in its fusion of Celtic folklore with universal coming-of-age themes, offering a distinct European voice in global cinema. Cartoon Saloon actively collaborates with international co-producers while maintaining creative control from its base in Kilkenny. Recently, the studio secured long-term development deals with Apple TV+ and expanded its educational outreach through animated shorts addressing climate and social issues. By balancing artistic integrity with strategic streaming partnerships, Cartoon Saloon elevates the profile of independent European animation and demonstrates that culturally specific stories can achieve worldwide resonance.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe animation market are increasingly developing owned intellectual property to retain long term rights and maximize revenue from licensing, merchandising, and spin-offs. They are investing in real-time rendering and game engine technologies to reduce production costs and enable crossover into interactive and immersive media. Studios are forming strategic co-production alliances across EU countries to access public funding and pool creative talent. Companies are also expanding into branded entertainment and educational content to diversify income beyond traditional broadcasting. Additionally, firms are establishing in-house digital distribution channels and social media teams to engage directly with global audiences and build franchise loyalty outside conventional platform dependencies.

MARKET SEGMENTATION

This research report on the Europe animation market has been segmented and sub-segmented into the following categories.

By Revenue Stream

- OTT

- Advertising

- Sale of Tickets

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe animation market?

The Europe animation market produces films, series, and commercials using 2D, 3D, and stop-motion techniques. France and UK lead with diverse studios serving global platforms.

How does the Europe animation market operate?

The Europe animation market operates through studios handling pre-production to delivery. Pipelines integrate modeling, rigging, and rendering for efficient project workflows.

Who are the key players in the Europe animation market?

Key players in the Europe animation market include StudioCanal, Aardman, and Cartoon Saloon. They excel in feature films, series, and international co-productions effectively.

What trends shape the Europe animation market?

Trends in the Europe animation market feature VR experiences, real-time rendering, and AI-assisted animation. Streaming deals drive diverse content for global audiences.

What types dominate the Europe animation market?

3D CGI dominates the Europe animation market for films and games, while 2D excels in series. Motion graphics thrive in advertising and digital media applications.

How does regulation affect the Europe animation market?

Regulation supports the Europe animation market via tax incentives and content quotas. EU funding programs boost co-productions and cultural animation projects.

What role does gaming play in the Europe animation market?

Gaming drives the Europe animation market demanding character assets and cinematics. Studios adapt pipelines for real-time engines like Unreal and Unity effectively.

How does streaming impact the Europe animation market?

Streaming platforms expand the Europe animation market commissioning original series. Netflix and Disney+ deals increase budgets for high-quality European content.

What challenges face the Europe animation market?

Challenges in the Europe animation market include talent shortages and tight deadlines. International collaborations help studios scale production capacity efficiently.

How has technology transformed the Europe animation market?

Technology revolutionizes the Europe animation market with cloud rendering and motion capture. Real-time tools accelerate iteration from concept to final output.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com