Europe Biocontrol Agents Market Size, Share, Trends & Growth Forecast Report By Form, By Crop Type, and By Country (Germany, France, Spain, Italy, United Kingdom & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034 Size, Share, Trends & Growth Forecast Report By Form, By Crop Type, and By Country (Germany, France, Spain, Italy, United Kingdom & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Biocontrol Agents Market Report Summary

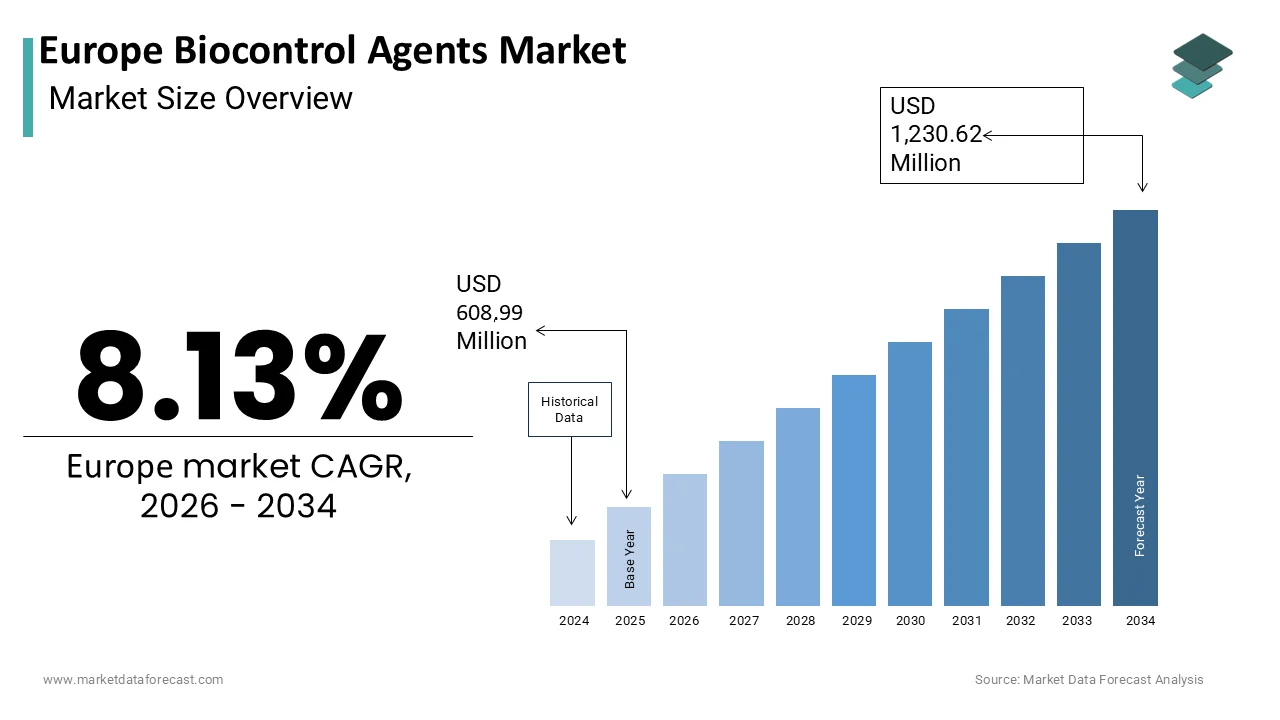

The Europe Biocontrol Agents Market was valued at USD 608.99 million in 2025 and is projected to reach USD 1,230.62 million by 2034, growing from USD 658.50 million in 2026 at a CAGR of 8.13% during the forecast period. Growth is driven by stringent regulatory bans on synthetic chemical pesticides, escalating consumer demand for residue-free produce, and integration with precision agriculture and digital monitoring. Higher costs and limited shelf life of biological products are shaping market dynamics.

Key Market Trends

- Rising withdrawal of synthetic pesticide approvals under EU Regulation EC No 1107/2009

- Growing integration of biocontrol release schedules with precision agriculture and drones

- Increasing use of microencapsulation technology to extend microbial product shelf life

- Expansion of biocontrol adoption in protected cultivation and greenhouse systems

- Rising demand for residue-free produce driven by retailer maximum residue limit standards

Segmental Insights

- Based on form, macrobials held the dominant share in 2025, driven by widespread adoption in greenhouse and protected cultivation systems.

- Based on crop type, horticultural crops held the largest share in 2025, driven by strict zero-tolerance pesticide residue policies from retailers.

- Microbials is the fastest-growing form segment, projected at a CAGR of 13.3%, driven by advances in encapsulation and formulation stability.

Regional Insights

- Germany led the market in 2025, supported by advanced precision agriculture technology and strong organic farming adoption.

- France holds a significant share, driven by the Ecophyto Plan's pesticide reduction goals and agroecological transition support.

- Spain is a prominent market supported by its intensive horticulture and protected cultivation export sector.

- Italy contributes notably due to its large organic farming area and high-value specialty crop production.

- Cash crops is the fastest-growing crop type segment, projected at a CAGR of 13.8%, driven by regulatory gaps left by withdrawn chemical seed treatments.

Competitive Landscape

The market is highly competitive, with multinational agrochemical corporations and specialized biological solution providers competing on formulation stability, technical support, and field trial credibility. Companies are investing in encapsulation technology and partnerships with seed manufacturers to integrate biocontrols into existing farming operations.

Prominent players in the market include Koppert Biological Systems, Biobest Group, and Syngenta Group.

Europe Biocontrol Agents Market Size

The Europe Biocontrol Agents Market is projected to grow from USD 608.99 million in 2025 to USD 658.50 million in 2026 and reach USD 1,230.62 million by 2034, registering a CAGR of 8.13% during the forecast period from 2026 to 2034.

Biocontrol agents are living organisms or natural substances used to manage agricultural pests and diseases, offering a sustainable alternative to synthetic chemical pesticides. This sector includes macrobials such as predatory insects and mites, microbials including bacteria, fungi, and viruses, and semiochemicals like pheromones that disrupt pest mating cycles. The adoption of these biological solutions is deeply embedded in the European Union’s regulatory framework, which prioritizes environmental protection and human health. According to Eurostat, the sales volume of pesticides in the EU in 2024 remained 12% below the 2011-2021 average, reflecting a structural shift towards integrated pest management practices. The Farm to Fork Strategy explicitly targets a 50% reduction in the use and risk of chemical pesticides by 2030, creating a favorable policy environment for biological alternatives. As per The World of Organic Agriculture 2026 report, organic farmland in the European Union reached 10.6% of the total agricultural area, with countries like Austria maintaining significant coverage exceeding 25%. This expansion necessitates reliable non-chemical crop protection tools. Furthermore, the European Food Safety Authority continues to withdraw approvals for numerous active substances due to safety concerns, leaving gaps in pest control portfolios that biocontrol agents are well positioned to fill. The market is characterized by high innovation rates and increasing collaboration between research institutions and commercial entities to develop effective strains suited to diverse European climatic conditions.

MARKET DRIVERS

Stringent Regulatory Bans on Synthetic Chemical Pesticides

The progressive withdrawal of approvals for synthetic chemical active substances is one of the major factors propelling the growth of the European biocontrol agents market. The European Union operates under Regulation EC No 1107/2009, which mandates rigorous safety assessments for all plant protection products, leading to the non-renewal of many conventional chemicals. According to the European Commission, a significant portion of previously approved pesticide active substances have been withdrawn from the market over the last decade due to failures in meeting updated safety standards regarding human health and environmental impact. Specific bans on neonicotinoids and otherbroad-spectrumm insecticides have created significant voids in pest management strategies, particularly for crops like sugar beets and oilseed rape. Farmers are compelled to seek compliant alternatives to avoid legal penalties and maintain production levels. The Sustainable Use of Pesticides Directive further reinforces this trend by requiring member states to prioritize non-chemical methods in their National Action Plans. As per data from the European Environment Agency, agricultural runoff containing pesticide residues remains a critical water quality issue, prompting stricter local regulations in vulnerable zones. This regulatory pressure ensures that biocontrol agents are increasingly mandatory components of modern crop protection programs, driving consistent demand growth among both organic and conventional growers seeking to remain compliant with evolving legislative frameworks.

Escalating Consumer Demand for Residue-Free Produce

Growing consumer awareness regarding food safety and environmental sustainability is further contributing to the European biocontrol agents market expansion. Shoppers are increasingly scrutinizing product labels and preferring fruits and vegetables grown without synthetic chemical residues, which they perceive as healthier and more environmentally friendly. According to recent market data, the retail market for organic food in the EU reached approximately 55 billion euros, demonstrating robust consumer willingness to pay premium prices for sustainably produced goods. Major supermarket chains and retailers have established private standards for maximum residue limits that are often stricter than legal requirements, forcing suppliers to adopt biological crop protection methods. A survey by the European Consumer Organisation indicated that over 70% of Europeans are willing to pay more for sustainably and locally sourced food products. This market pull encourages conventional farmers to integrate biocontrol agents into their production systems to access lucrative retail contracts and maintain brand reputation. High-value crops such as berries, leafy greens, and tomatoes are particularly sensitive to chemical residues, making them ideal candidates for biological pest management. The economic incentive provided by premium pricing and guaranteed market access ensures that growers view biocontrol agents as essential tools for business viability, thereby sustaining strong market momentum.

MARKET RESTRAINTS

Higher Cost Structure Compared to Synthetic Alternatives

The elevated cost of biocontrol agents relative to conventional synthetic pesticides is significantly hampering the European biocontrol agents market growth. Biological products often require more complex manufacturing processes involving live organism cultivation, stringent quality control, and specialized storage conditions, which drive up production expenses. According to agricultural economic studies, biocontrol treatments can be 20% to 30% more expensive per hectare than standard chemical applications,s depending on the crop and pest pressure. For large-scale conventional farmers operating on thin margins, this price differential presents a substantial financial barrier, especially when synthetic options remain available and affordable. The need for repeated applications to maintain efficacy further increases labor and material costs, exacerbating the total expense. As per economic research, small and medium-sized farms lack the financial buffer to absorb these higher input costs without guaranteed yield improvements or premium market access. Government subsidies for synthetic fertilizers and pesticides in certain member states distort the pricing landscape, making it difficult for biological alternatives to compete on a level playing field. Although long-term benefits such as improved soil health and resistance management exist, the immediate cash flow impact discourages many growers from switching.

Limited Shelf Life and Complex Storage Requirements

The inherent biological nature of biocontrol agents imposes strict limitations on shelf life and storage conditions that complicate logistics and distribution across Europe and impede regional market expansion. Unlike stable chemical formulations, live macrobials and microbials require specific temperature, humidity, and light conditions to maintain viability and efficacy during transport and warehousing. Most predatory insects and mites have a short shelf life, requiring rapid delivery from manufacturer to field, which challenges existing supply chain infrastructure. According to supply chain assessments, inconsistent cold chain facilities in rural areas lead to significant product mortality and reduced field performance, undermining farmer confidence. Fungal and bacterial agents are also sensitive to extreme temperatures and UV exposure, requiring specialized packaging and handling protocols that increase operational costs. As per distributor reports, product wastage due to improper storage or delayed delivery remains a persistent issue affecting profitability and reliability. Farmers often hesitate to invest in biological inputs when faced with uncertainty regarding organism viability at the time of application, preferring the predictable potency of chemical pesticides. The lack of standardized preservation technologies across different formulation types creates variability in product quality, further complicating inventory management for retailers.

MARKET OPPORTUNITIES

Integration with Precision Agriculture and Digital Monitoring

The convergence of biocontrol agents with precision agriculture technologies offers a substantial opportunity for the European biocontrol agents market growth. Advanced sensors, drones, and digital monitoring platforms enable growers to track pest populations and environmental conditions in real time, allowing for targeted and timely deployment of biological agents. According to industry analysis, the adoption of digital tools in large-scale farming is accelerating, with over 30% of large farms in major agricultural regions utilizing precision agriculture techniques. Integrating biocontrol release schedules with predictive pest models helps farmers apply agents when pest thresholds are reached and environmental conditions favor organism survival, maximizing efficacy and minimizing waste. Drone-based dispersal systems offer novel delivery methods for releasing predatory mites or applying microbial sprays over large areas, reducing labor costs and improving coverage uniformity. As per industry trends, the synergy between biological inputs and digital data enhances the credibility of biocontrol among tech-savvy younger farmers who prioritize measurable outcomes. This technological integration also facilitates traceability and documentation required for organic certification and sustainability reporting, adding value to the overall farming operation.

Expansion into Protected Cultivation and Greenhouse Systems

The extensive protected cultivation sector in Europe, particularly in countries like Spain, the Netherlands, and Italy, presents a significant opportunity for the biocontrol agents market. Greenhouses and tunnel farming create controlled environments where temperature, humidity, and light can be optimized for the survival and activity of beneficial organisms, making them ideal settings for biological pest management. According to industry reports, over 90% of greenhouse vegetable production in the Netherlands utilizes integrated pest management strategies dominated by biological controls. The closed nature of these systems prevents the escape of released agents and minimizes interference from weather conditions, ensuring higher efficacy compared to open-field applications. High-value crops grown in protected environments are highly susceptible to pests such as whiteflies, thrips, and spider mites, which can cause rapid crop loss if not managed effectively. Biocontrol agents offer a safe and efficient solution that avoids chemical residues on premium produce destined for export markets with strict maximum residue limits. As per market analysis, the density of greenhouse production allows for economies of scale in biocontrol application, making it cost-competitive with chemical alternatives. The growing investment in vertical farming and urban agriculture further expands the addressable market for biocontrol solutions.

MARKET CHALLENGES

Variable Efficacy Due to Environmental Sensitivity

The susceptibility of biocontrol agents to fluctuating environmental conditions poses a significant challenge to their consistent performance and reliability in European agricultural settings. Unlike synthetic chemicals, which provide predictable knockdown effects regardless of weather, biological agents require specific temperature, humidity, and light levels to thrive and exert control. For instance, predatory mites may become inactive below certain temperatures, while fungal pathogens require high humidity to infect pest populations. According to agronomic studies, efficacy rates of biocontrol agents can vary significantly between seasons and regions, leading to unpredictable results that frustrate farmers accustomed to chemical certainty. Climate change exacerbates this issue by introducing more extreme weather events,s such as heatwaves or heavy rains, that can wash away or kill beneficial organisms. As per field trial data, inconsistent performance during critical pest outbreaks can lead to crop damage and economic losses, discouraging growers from relying solely on biological methods. The complexity of matching specific agent strains to local microclimates requires advanced technical knowledge that many farmers lack. This variability creates a perception of unreliability that hinders widespread adoption among risk-averse conventional farmers who prioritize immediate and guaranteed pest suppression.

Complex Regulatory Approval Processes for Novel Strains

Navigating the complex and lengthy regulatory approval process for new biocontrol agents remains a major challenge for manufacturers seeking to introduce innovative strains to the European market. While the EU supports low-risk products, the authorization procedure under Regulation EC No 1107/2009 requires extensive data on efficacy, safety, and environmental impact, which can be costly and time-consuming to generate. According to industry estimates, the average time to register a new biologically active substance can reach 3 years, with costs varying significantly based on dossier complexity. This lengthy timeline delays product commercialization and reduces the window for patent protection, discouraging investment in research and development, particularly for small andmedium-sizedd enterprises. The lack of harmonization in data interpretation across member states further complicates the process, creating market fragmentation and additional administrative burdens. As per industry feedback, the uncertainty surrounding regulatory outcomes and potential changes in data requirements creates financial risks for developers. Additionally, the periodic re-evaluation of approved substances adds ongoing compliance costs for manufacturers. Until the regulatory framework becomes more streamlined and predictable for biologicals, the pace of innovation and market entry will remain constrained.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Form, Crop Type, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, Germany, France, Italy, Spain, Netherlands, Belgium, Sweden, Rest of Europe |

| Market Leaders Profiled | BASF SE, Bayer AG, Syngenta AG, Corteva Agriscience, Koppert Biological Systems, Certis Belchim B.V., Biobest Group NV, Andermatt Biocontrol AG, Bioline AgroSciences Ltd. (InVivo Group), Valent BioSciences LLC, Novonesis A/S, UPL Limited. |

SEGMENTAL ANALYSIS

By Form Insights

The macrobials segment held the dominant share of the European market in 2025 due to their widespread adoption in protected cultivation systems such as greenhouses and polytunnels, where environmental conditions can be controlled to optimize biological activity. Predatory mites, insects, and nematodes are highly effective against common greenhouse pests like whiteflies, thrips, aphids, and spider mites,s which thrive in warm, rm humid environments. According to industry data, over 90% of greenhouse vegetable production in countries like the Netherlands and Spain utilizes microbial agents as the primary pest management strategy. The high economic value of crops such as tomatoes, peppers, cucumbers, and ornamental flowers justifies the higher cost of macrobials compared to chemical alternatives. Farmers in these sectors prioritize residue-free produce to meet strict retailer standards and export requirements, making macrobials an essential tool for maintaining market access. The visible nature of microbial efficacy allows growers to monitor pest suppression directly, fostering trust and continued usage. As per industry surveys, the reliability of established microbial species has created a loyal customer base among professional greenhouse operators. The mature supply chain and technical support infrastructure for macrobials further reinforce their dominant position.

However, the microbials segment is expected to register the fastest CAGR of 13.3% over the forecast period in the European market owing to the significant advancements in formulation technologies that enhance product stability and shelf life. Traditional microbial products suffered from short viability periods and sensitivity to environmental stressors, but recent innovations in encapsulation and drying techniques have improved their robustness. According to agricultural research, new microencapsulation methods protect bacterial and fungal spores from UV radiation and desiccation, extending shelf life significantly. These technological improvements allow for broader distribution and storage in standard warehouse conditions, reducing logistical constraints. The development of liquid formulations compatible with standard spraying equipment simplifies application for large-scale field crops, making microbials more accessible to conventional farmers. As per industry reports, the introduction of ready-to-use microbial products has increased adoption rates in recent years. Manufacturers are also investing in strain selection to identify variants with higher tolerance to temperature fluctuations and pH variations, ensuring consistent performance across diverse European climates. These scientific breakthroughs address previous limitations and build confidence among growers who previously hesitated to use microbial inputs due to reliability concerns.

By Crop Type Insights

The horticultural crops segment held the largest share of the European market in 2025 due to their high economic value and strict zero-tolerance policies for pesticide residues. Consumers and retailers demand fresh produce that is safe and free from chemical contaminants, driving growers to adopt biological control methods. According to industry associations, a vast majority of supermarket contracts now include stringent maximum residue limit clauses that are often tighter than legal requirements. Biocontrol agents offer a compliant solution that ensures produce meets these high standards without compromising quality or yield. The intensive nature of horticultural production, particularly in protected environments, creates ideal conditions for pest outbreaks, necessitating effective and safe management tools. Macrobials and microbials are widely used in strawberry, tomato, and pepper production where pest pressure is high and harvest intervals are short. As per industry data, the use of biocontrols in horticulture has become standard practice in many regions, with adoption rates exceeding 70% in major producing areas. The premium prices commanded by residue-free produce provide financial incentives for growers to invest in biocontrol technologies.

On the other side, the cash crops segment is predicted to record a promising CAGR of 13.8% over the forecast period in the European biocontrol agents market owing to the regulatory pressure and the need for resistance management. The withdrawal of key chemical pesticides due to safety concerns has left gaps in pest control portfolios for these large-scale crops, compelling farmers to seek alternative solutions. According to agricultural research, the restriction of certain chemical seed treatments has increased vulnerability to vectors, necessitating the use of microbial and semiochemical controls. Biocontrol agents offer a viable alternative that helps manage pest populations while preserving the efficacy of remaining chemical options through rotation. The large acreage dedicated to cash crops provides significant volume potential for biocontrol manufacturers, encouraging investment in scalable production technologies. As per agricultural policy reports, the European Union’s push for sustainable intensification mandates reduced chemical inputs in arable farming, creating opportunities for biobased solutions. Farmers are increasingly adopting integrated approaches that combine biocontrols with precision agriculture to optimize input use and minimize environmental impact.

COUNTRY LEVEL ANALYSIS

Germany Biocontrol Agents Market Analysis

Germany captured the leading share of the European biocontrol agents market in 2025 and is expected to witness steady growth in its biocontrol sector over the next few years as it further aligns its advanced precision agriculture technology with organic farming needs. Germany holds a prominent position in the Europe biocontrol agents market, driven by its advanced agricultural technology sector and strong commitment to environmental sustainability. The country is a leader in organic farming adoption, with over 11.5% of its agricultural land under organic management, creating substantial demand for biological inputs. German farmers are increasingly integrating precision agriculture tools with biocontrol applications to optimize efficacy and comply with strict environmental regulations. The Federal Ministry of Food and Agriculture provides significant financial support for sustainable farming practices, including the adoption of biocontrol agents. The presence of major agrochemical companies and research institutions in Germany fosters innovation in microbial formulation technologies, enhancing product efficacy and market acceptance. The country's robust distribution network ensures wide availability of biocontrol products across diverse farming regions. Consumer demand for organic and sustainably produced food in Germany is among the highest in Europe, driving retailers to source from farms using biological inputs.

France Biocontrol Agents Market Analysis

France is poised for continued expansion in its biological inputs market as it scales its agroecological initiatives over the next few years. France stands as a major contributor to the Europe biocontrol agents market, characterized by its extensive agricultural land and strong policy support for agroecological transitions. The country is one of the largest agricultural producers in the European Union, with significant areas dedicated to cereals, wine grapes, and vegetables. The French Ecophyto Plan aims to reduce pesticide use, indirectly promoting the adoption of biological inputs that enhance plant health. According to national agricultural statistics, the area under organic farming has reached over 2.8 million hectares, which drives demand for compliant pest management solutions. French farmers are increasingly aware of the benefits of soil health management, leading to greater interest in microbial inoculants. The country hosts several leading biocontrol manufacturers and research centers that develop strains suited to local soil conditions. Government subsidies for organic conversion and sustainable practices provide financial incentives for farmers to adopt biocontrols. The strong cooperative structure in French agriculture facilitates knowledge sharing and bulk purchasing of bio inputs, accelerating market penetration.

Spain Biocontrol Agents Market Analysis

Spain is likely to strengthen its leadership in biocontrol adoption within the protected cultivation sector throughout the next few years. Spain is a key player in the Europe biocontrol agents market, particularly known for its intensive horticulture and protected agriculture sectors. The country is a major exporter of fresh fruits and vegetables to the rest of Europe, requiring high standards of produce quality and safety that drive the adoption of residue-free production methods. Biocontrol agents are widely used in Spanish greenhouses and open-field vegetable production to control pests such as whiteflies and thrips without chemical residues. According to the Ministry of Agriculture, Fisheries and Food, Spain has seen significant growth in the area of organic farming. The arid and semi-arid conditions in many parts of Spain make efficient pest management critical, as biocontrol agents offer targeted control with minimal water usage. The intensive nature of Spanish horticulture allows for frequent monitoring and adjustment of pest control inputs, facilitating the integration of biocontrols into precision farming systems. Export markets impose strict maximum residue limits, compelling Spanish growers to minimize chemical input use.

Italy Biocontrol Agents Market Analysis

Italy is projected to expand its reliance on biological pest control as it integrates its specialty crop production with sustainable Mediterranean farming practices over the next few years. Italy occupies a significant share in the Europe biocontrol agents market, driven by its diverse agricultural landscape and high-value specialty crop production. The country is a leading producer of fruits, vegetables, and wine, sectors that are increasingly adopting organic and sustainable practices to meet premium market demands. Italian farmers face challenges related to climate change-induced disease pressure, making effective biological control agents highly relevant. According to national data, Italy has one of the largest organic farming areas in the European Union, with over 2 million hectares under organic management. This extensive organic sector creates a ready market for biological pest control agents that are permitted under organic certification standards. The Mediterranean climate in many parts of Italy supports year-round cultivation, allowing for multiple applications of biocontrols and sustained demand. Italian consumers are highly conscious of food quality and origin, driving retailers to prefer suppliers using sustainable production methods.

United Kingdom Biocontrol Agents Market Analysis

The United Kingdom is expected to see a gradual increase in the adoption of biological inputs as it advances its regenerative agriculture policies in the coming years. The United Kingdom maintains a steady presence in the Europe biocontrol agents market, influenced by its post Brexit agricultural policies and strong organic sector. The UK government has introduced the Environmental Land Management scheme, which rewards farmers for adopting sustainable practices, including the use of biological inputs that improve soil health and reduce chemical reliance. According to the Department for Environment, Food and Rural Affairs, the UK has a well-established organic farming community with consumer demand for organic products remaining robust. British farmers are increasingly focused on regenerative agriculture principles,s which emphasize soil biology and minimal chemical intervention, creating favorable conditions for biocontrol adoption. The country's temperate climate supports a wide range of crops, ps including cereals, oilseeds, and vegetables, all of which can benefit from biological pest control. Research institutions in the UK are actively studying the efficacy of microbial inoculants in local soil conditions, providing evidence-based recommendations to farmers.

COMPETITIVE LANDSCAPE

The competition in the Europe biocontrol agents market is characterized by a mix of established multinational agrochemical corporations and specialized niche biological solution providers. Multinational companies leverage their extensive distribution network, brand recognition,n and financial resources to introduce biocontrols as part of integrated crop management portfolios. These large players often compete based on product stability, formulation technology,y and seamless integration with existing chemical inputs. Specialized firms differentiate themselves through deep technical expertise, high-quality microbial strains, and personalized customer support services. They focus on building trust with organic and progressive conventional farmers by providing evidence-based results from local field trials. The market sees intense competition in innovation with companies constantly developing novel carrier materials and consortium formulations to enhance efficacy and shelf life. Regulatory compliance serves as a significant barrier to entry, favoring established players with resources to navigate complex approval processes. Price competition remains moderate as buyers prioritize product reliability and performance over cost alone. Strategic alliances between biocontrol manufacturers and seed companies or precision agriculture tech firms are becoming common to create comprehensive value propositions. The fragmented nature of European agriculture means that regional players also hold strong positions in specific countries,s leveraging local knowledge and relationships to compete effectively against global giants.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Biocontrol Agents Market include

- BASF SE

- Bayer AG

- Syngenta AG

- Corteva Agriscience

- Koppert Biological Systems

- Certis Belchim B.V.

- Biobest Group NV

- Andermatt Biocontrol AG

- Bioline AgroSciences Ltd. (InVivo Group)

- Valent BioSciences LLC

- Novonesis A/S

- UPL Limited

TOP LEADING PLAYERS IN THE MARKET

- Koppert Biological Systems is a global leader in natural pest management and pollination with a strong footprint across Europe. The company specializes in producing high-quality macrobials and microbials for greenhouse and open-field applications. Koppert focuses on integrated solutions that combine biological agents with digital monitoring tools to optimize pest control efficiency. Recent actions include expanding its production facilities in Spain and the Netherlands to meet growing demand for predatory mites and beneficial insects. The company actively collaborates with research institutions to develop new strains tailored to specific European climatic conditions. By providing extensive technical support and training programs, Koppert strengthens farmer confidence and adoption rates. Its commitment to sustainability and innovation solidifies its position as a trusted partner for professional growers seeking reliable and effective biocontrol solutions throughout the continent.

- Biobest Group is a prominent player in the Europe biocontrol agents market,t known for its comprehensive portfolio of biological solutions for horticulture and agriculture. The company offers a wide range of predatory insects, mites,tes and microbial products designed to manage key pests and diseases. Biobest emphasizes sustainable farming practices and works closely with farmers to implement integrated pest management strategies. Recent initiatives involve launching new microbial formulations with enhanced stability and shelf life for broader application scenarios. The company has expanded its distribution network across Southern and Central Europe to improve accessibility and service delivery. Biobest invests heavily in research and development to discover novel active substances and improve existing product efficacy. The customer-centric approach and focus on practical field results drive strong loyalty among European growers and reinforce their competitive standing in the dynamic biocontrol sector.

- Syngenta Group leverages its vast agricultural expertise to expand its biological portfolio in the European market through strategic acquisitions and internal innovation. The company integrates biocontrol agents into its broader crop protection offerings, providing holistic solutions for conventional and organic farmers. Syngenta focuses on developing scalable microbial products that can be easily integrated into existing farming operations. Recent actions include the launch of advanced seed treatment technologies containing beneficial microbes to protect crops from early-stage diseases. The company collaborates with local distributors and agronomists to promote the benefits of biological inputs and provide technical guidance. Syngenta’s strong brand recognition and extensive supply chain enable rapid market penetration and widespread availability of its biocontrol products. By combining chemical and biological expertise, Syngenta addresses diverse pest management needs and supports the transition towards more sustainable agricultural practices across Europe.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe biocontrol agents market primarily employ strategic partnerships and collaborations to expand their distribution networks and enhance product credibility. Companies frequently partner with seed manufacturers to integrate microbial inoculants directly into seed coatings,s ensuring early root colonization and ease of use for farmers. Research and development investments focus on improving formulation stability through advanced encapsulation technologies that extend shelf life and protect organism viability during storage and transport. Market participants also engage in extensive field trials and demonstration projects to generate local data proving efficacy under diverse European soil and climatic conditions. Educational initiatives targeting farmers and agronomists are crucial to overcoming knowledge gaps and promoting proper application techniques. Additionally, our companies pursue regulatory approvals under the European Plant Protection Product Regulation to facilitate cross-border trade and market access. Mergers and acquisitions allow larger firms to acquire specialized microbial strains and technical expertise, strengthening their product portfolios. Digital integration strategies involve combining biocontrol recommendations with precision agriculture tools to optimize application timing and dosage for maximum efficiency.

MARKET SEGMENTATION

This research report on the europe biocontrol agents market is segmented and sub-segmented into the following categories.

By Form

- Macrobials

- Microbials

By Crop Type

- Horticultural Crops

- Cash Crops

By Country

- Germany

- France

- Spain

- Italy

- United Kingdom

- Rest of Europe

Frequently Asked Questions

1. What is driving growth in Europe?

.

Growth is driven by EU regulations and the Farm to Fork Strategy to cut chemical pesticide use, rising organic farming, consumer demand for safer food, and greater awareness of environmental and biodiversity concerns

2. Which product types are most important?

Key product types include beneficial insects (predators and parasitoids), microbial pesticides, and biopesticides, with each playing a major role in integrated pest management.

3. Which crops use biocontrol agents most?

They are widely used in vegetables, fruits, and other high‑value crops, especially in protected and greenhouse cultivation where precision pest control is critical

4. Which countries lead the market?

Western European countries such as Germany, France, Italy, and Spain are leading markets due to advanced agriculture, strong organic adoption, and proactive sustainability policies.

5. Who are the major players?

Key players include Koppert Biological Systems, Bioline AgroSciences, Biobest, Andermatt Biocontrol, BASF, Bayer, Syngenta, Corteva, Novozymes, Marrone Bio Innovations, and others.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com