- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

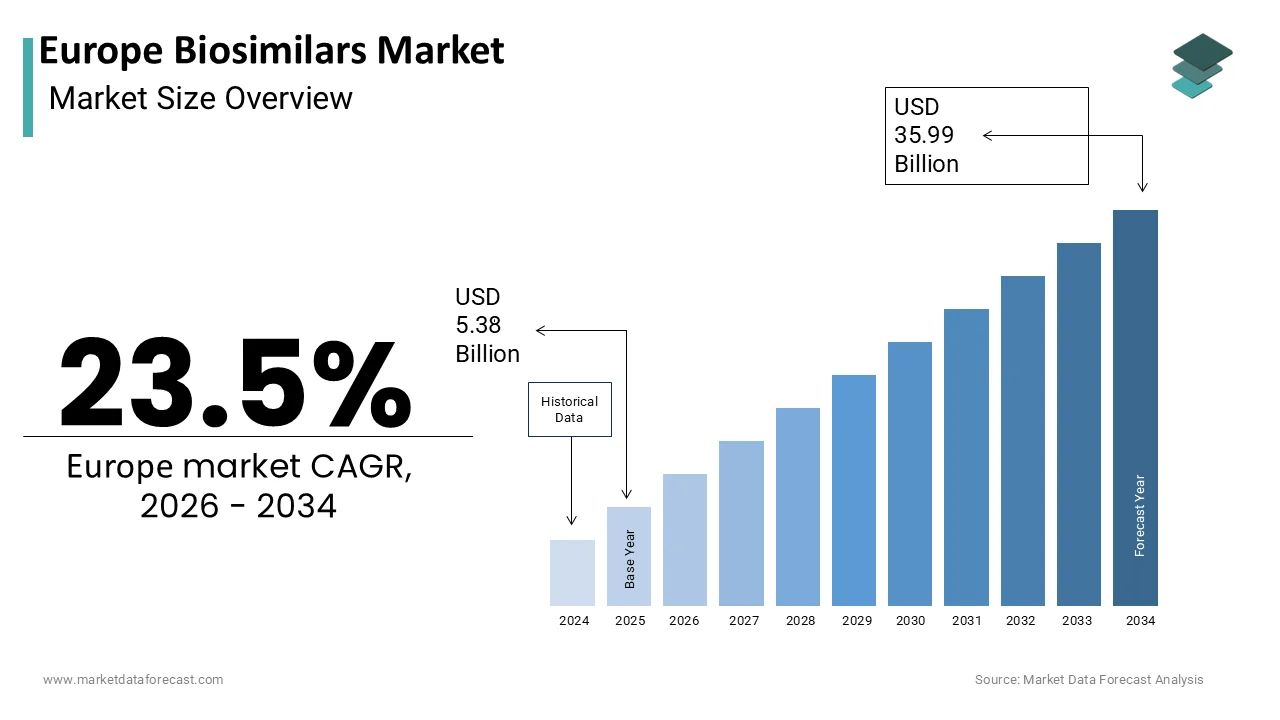

Market Size, 2025

$5.38 BnMarket Estimate, 2026

$6.65 BnMarket Forecast, 2034

$35.99 BnCAGR, 2026–2034

23.5%Europe Biosimilars Market Summary

Market Size & Growth

- The Europe Biosimilars Market was valued at USD 5.38 billion in 2025.

- Expected to reach USD 6.65 billion in 2026 and USD 35.99 billion by 2034, growing at a CAGR of 23.5% from 2026 to 2034.

- Germany leads the regional market, accounting for 23.4% of European market share in 2025.

Key Market Segments

- By Product Type: Monoclonal Antibodies (largest share), Recombinant Glycosylated Proteins (fastest-growing, 15.4% CAGR)

- By Technology: Recombinant DNA Technology (largest share), Mass Spectroscopy (fastest-growing)

- By Disease: Chronic and Autoimmune Diseases (largest share), Oncology (fastest-growing, 17.7% CAGR)

- By Country: Germany leads; France holds second-largest share; United Kingdom, Italy, and Sweden are prominent markets.

Key Drivers

- Stringent EMA regulatory framework and early adoption by public payers, with biosimilar penetration exceeding 90% for infliximab and etanercept in Germany by 2023.

- Expiring patents on blockbuster biologics (trastuzumab, adalimumab, rituximab) between 2018 and 2023, opening EU sales exceeding €12 billion annually.

- Adoption of interchangeability and automatic substitution policies in Denmark, Sweden, and the Netherlands.

Key Players

Sandoz International GmbH, Wockhardt Ltd, Hospira Inc., Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories, Biocon Limited, Mylan Inc., Zydus Cadila, Celltrion Inc., Roche Diagnostics, Cipla Ltd.

Europe Biosimilars Market Size

The Europe Biosimilars Market is projected to grow from USD 5.38 billion in 2025 to USD 6.65 billion in 2026 and reach USD 35.99 billion by 2034, registering a CAGR of 23.5% during the forecast period from 2026 to 2034.

Biosimilars are biological medicinal products highly similar to an already authorized reference biologic in terms of quality, safety,y and efficacy but developed after the expiration of the originator’s patent protection. In Europe, they represent a critical instrument for expanding access to advanced therapies while containing healthcare expenditure across public systems. Unlike generic small molecule drugs,s biosimilars require comprehensive analytical and clinical comparability exercises due to the complexity of their large protein structures. According to the European Medicines Agency, more than 90 biosimilars have received marketing authorization in the European Union since 2006, covering therapeutic areas such as oncology, immunology, and endocrinology. The European Commission’s Pharmaceutical Strategy for Europe explicitly endorses biosimilars as instruments to foster competition and sustainability, with a target of achieving 80% biosimilar uptake in eligible categories by 2025. National health systems, including those in Germany, France, and the Netherlands, have implemented mandatory substitution policies and tendering frameworks to accelerate adoption. This regulatory maturity, combined with strong scientific oversight and public payer incentives, defines Europe as the world’s most advanced and influential biosimilars market.

MARKET DRIVERS

Stringent Regulatory Framework and Early Adoption by Public Payers

Europe’s leadership in biosimilars stems from its pioneering and scientifically rigorous regulatory pathway established by the European Medicines Agency (EMA), which is one of the major factors driving the growth of the European biosimilars market. The EU was the first jurisdiction to approve a biosimilar in 2006 (somatropin/Omnitrope), and has since accumulated the world’s most extensive experience in evaluating complex biologics. This regulatory clarity gives prescribers and payers high confidence in biosimilar interchangeability. National health systems have capitalized on this by implementing aggressive uptake strategies. Germany’s statutory health insurers achieved biosimilar penetration rates above 90% for infliximab and etanercept by 2023 through mandatory price referencing. In France, the Haute Autorité de Santé requires hospitals to switch at least 80% of new patients to biosimilars within six months of market entry. The Netherlands uses centralized tenders that often allocate 100% of volume to the lowest‑priced biosimilar. As per the estimations of the European Commission, these policy mechanisms collectively saved EU payers more than €35 billion between 2007 and 2023.

Expiring Patents of High‑Revenue Biologics Drive Pipeline Expansion

The expiration of patents on blockbuster biologics has created a fertile pipeline for biosimilar development in Europe, particularly in oncology and autoimmune diseases, which is further boosting the biosimilars market expansion in Europe. According to the European Commission’s 2023 Pharmaceutical Watch report, originators such as trastuzumab, adalimumab, and rituximab lost exclusivity between 2018 and 2023, opening access to therapies with combined annual EU sales exceeding €12 billion. This has spurred intense developer interest, with more than 60 biosimilar candidates under EMA evaluation in 2023. EFPIA and IQVIA note that biosimilar developers invested over €4 billion in clinical and analytical studies in Europe between 2021 and 2023. National cancer plans further amplify demand. Germany’s National Decade Against Cancer and Italy’s Oncology Network prioritize cost‑effective biologics to expand treatment access. With ~4 million new cancer cases annually in Europe (ECIS, 2023), the need for affordable monoclonal antibodies ensures continuous pipeline momentum and market entry of novel biosimilars well into the next decade.

MARKET RESTRAINTS

Physician and Patient Hesitancy Despite Regulatory Endorsement

Despite robust regulatory validation, skepticism among prescribers and patients continues to impede biosimilar uptake in several European countries, which is majorly impeding the biosimilars market growth in Europe. As per a 2025 survey presented at ESMO, ~38% of oncologists in Southern and Eastern Europe remain reluctant to switch stable patients to biosimilars. Similarly, EULAR surveys show ~40–42% of rheumatologists in Italy and Spain prefer originators for new starts despite biosimilar availability. Patient advocacy groups echo this caution. As per the European Patient Forum and EMA surveys, more than half of patients (≈55%) fear reduced effectiveness or increased side effects. These perceptions persist despite extensive real‑world evidence, including a Nordic registry study of over 1,300 patients, which shows identical two‑year retention rates between originator infliximab and biosimilars. Without targeted education and transparent communication, these attitudinal barriers delay savings and restrict equitable access, particularly in regions with weaker policy enforcement.

Legal and Patent Evergreening Tactics by Originator Companies

Originator biopharmaceutical companies frequently deploy complex legal and secondary patent strategies to delay biosimilar market entry in Europe, which is further hindering the biosimilars market growth in Europe. According to the European Commission’s 2023 antitrust review, more than 70% of high‑value biologics faced supplementary patents on formulation, delivery devices, or dosing regimens after core patent expiry. These evergreening tactics trigger prolonged litigation, as seen in the adalimumab market, where biosimilar launches in France and Spain were delayed by 18–24 months due to injunctions on device patents. The European Court of Justice noted in 2025 that such strategies cost EU health systems an estimated €4.2 billion in avoidable spending between 2020 and 2023. Furthermore, originators often enter settlement agreements with biosimilar applicants that include reverse payments or delayed entry clauses, now scrutinized under EU competition law. These maneuvers fragment market access, create country‑level disparities, and erode the predictability that once defined Europe’s biosimilar landscape.

MARKET OPPORTUNITIES

Expansion into Complex and High‑Value Oncology Indications

The next frontier for biosimilars in Europe lies in complex oncology biologics such as trastuzumab and rituximab biosimilars, with developers now exploring enhanced delivery mechanisms and antibody‑drug conjugate formats, which is a major opportunity in the European biosimilars market. According to EMA, the agency received its first biosimilar application for a monoclonal antibody drug conjugate in late 2023, whichreflectsg growing technical confidence among developers. According to the European Organisation for Research and Treatment of Cancer, biosimilar trastuzumab now accounts for more than 80–85% of HER2‑positive breast cancer treatments in Germany and the Netherlands, enabling expanded access to combination regimens. Furthermore, the European Commission’s Beating Cancer Plan allocates dedicated funding to support biosimilar adoption in national cancer control programs, which recognizes their role in sustaining innovation while managing costs. Real‑world data from Sweden confirm that biosimilar rituximab achieved equivalent two‑year progression‑free survival in diffuse large B‑cell lymphoma compared to the originator. With over 1.5 million patients receiving biologic cancer therapies annually in Europe (ECIS, 2023), oncology represents the highest‑value opportunity for next‑generation biosimilars.

Adoption of Interchangeability and Automatic Substitution Policies

Several European countries are advancing beyond initial biosimilar use to implement formal interchangeability and automatic pharmacy‑level substitution policies, which are significantly deepening market penetration. According to the European Commission’s 2025 Pharmaceutical Strategy Implementation Report, Denmark, Sweden, and the Netherlands now permit pharmacists to substitute originator biologics with approved biosimilars without physician consent, provided the patient is treatment‑naïve. These policies are supported by national registries. According to the Danish National Patient Registry, no difference in hospitalization rates between originator and biosimilar erythropoietin users over five years. In Germany, the GKV Spitzenverband introduced mandatory biosimilar substitution for hospital outpatient prescriptions in 2023, covering more than 200,000 patients annually. Additionally, EMA updated its 2023 guideline to clarify that repeated switching between biosimilars and originators does not increase immunogenicity risk, providing scientific backing for substitution. As more countries adopt these measures, biosimilar utilization is expected to exceed 90% in mature categories, which is creating a self‑reinforcing cycle of affordability, access, and trust across Europe’s health systems.

MARKET CHALLENGES

Lack of Harmonized Naming and Prescribing Conventions

Despite EU‑level regulatory approval, inconsistent national approaches to naming, prescribing, and dispensing biosimilars create confusion and hinder seamless adoption, which is a major challenge to the expansion of the European biosimilars market. According to EFPIA, 14 member states use national non‑proprietary names that differ from the international non‑proprietary name (INN), leading to formulary misalignment and prescription errors. In Italy, biosimilars are listed under distinct brand plus INN combinations, whereas Germany uses only the INN, which is causing interoperability issues in cross‑border care. Furthermore, a 2023 audit by France’s Haute Autorité de Santé found that hospital electronic prescribing systems often default to originator products unless manually overridden. EMA advocates for INN‑only prescribing, yet implementation remains voluntary. Without mandatory harmonization, prescribers face administrative burden,s and pharmacovigilance becomes fragmented as adverse events may be misattributed. This regulatory patchwork undermines the single‑market principle and delays the full realization of biosimilar benefits across Europe.

Supply Chain Fragility and Manufacturing Complexity

The production of biosimilars involves highly specialized bioreactor facilities, stringent quality control, and complex cold‑chain logistics, whicareis creating vulnerabilities in supply continuity and further challenging the growth of the European market. According to EMA, more than 60% of EU‑approved biosimilars are manufactured in only three countries,ies creating geographic concentration risk. A 2025 inspection report by the Paul Ehrlich Institute revealed that 22% of biosimilar manufacturing sites experienced at least one critical deviation related to protein folding or glycosylation patterns, requiring batch recalls. Additionally, the European Commission’s Health Emergency Preparedness and Response Authority noted that pandemic‑related disruptions in 2022 caused temporary shortages of biosimilar rituximab in five member states due to single‑source dependency on a Belgian fill‑finish facility. Unlike small‑molecule generics, biosimilars cannot be rapidly switched between suppliers because each product is tied to a specific manufacturing process approved as part of its dossier. This lack of interchangeability at the manufacturing level heightens systemic risk and underscores the need for diversified production networks and strategic stockpiling to ensure therapy continuity across European health systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Technology, Disease, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Sandoz International GmbH, Wockhardt Ltd, Hospira, Inc., Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories, Biocon Limited, Mylan, Inc., Zydus Cadila, Celltrion Inc., Roche Diagnostic,s and Cipla Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The monoclonal antibodies segment had the largest share of the European biosimilars market in 2025. The dominance of the monoclonal antibodies segment in this regional market is driven by the high cost, patent expiration, and widespread clinical use of originator biologics such as infliximab, adalimumab, rituximab, and trastuzumab. According to the European Medicines Agency (EMA), over 30 monoclonal antibody biosimilars have received marketing authorization in the EU since 2013, representing more than 65% of all biosimilar approvals. These agents are central to managing chronic autoimmune conditions and oncologic diseases, which collectively affect over 20 million Europeans. According to the European Commission’s 2023 Pharmaceutical Expenditure Report, monoclonal antibody therapies accounted for 58% of total biologic spending in public health systems before biosimilar entry. The European Observatory on Health Systems and Policies highlights that biosimilar infliximab achieved 95% market penetration in Germany and the Netherlands by 2023 through mandatory hospital tendering. Furthermore, national treatment guidelines from the European Society for Medical Oncology (ESMO) and the European Alliance of Associations for Rheumatology (EULAR) now preferentially recommend biosimilars for new patients. This convergence of therapeutic necessity, regulatory maturity, and policy enforcement ensures monoclonal antibodies remain the dominant biosimilar product category across Europe.

The recombinant glycosylated proteins segment is the fastest-growing product segment in the European biosimilars market and is expected to exhibit a CAGR of 15.4% over the forecast period. The approval of complex biosimilars for erythropoiesis‑stimulating agents and monoclonal antibodies that require precise glycosylation patterns to ensure biological activity and safety is fuelling the growth of the recombinant glycosylated proteins segment in this regional market. As per EMA, three biosimilars of darbepoetin alfa and etanercept, a heavily glycosylated fusion protein,n received approval in 2023 following extensive comparability studies on glycan profiles. The European Federation of Biotechnology reports that advances in glycoengineering now allow biosimilar developers to replicate human‑like glycosylation in Chinese hamster ovary cell lines with over 95% fidelity. This technical milestone reduces immunogenicity risks and aligns with EMA’s 2022 guideline on glycosylation analysis in biosimilar development. Demand is further amplified by aging populations, with a rising incidence of anemia in chronic kidney disease and rheumatoid arthritis. Eurostat confirms that over 90 million Europeans are aged 65 and above, ensuring robust growth in this technically advanced segment.

By Technology Insights

The recombinant DNA segment captured the leading share of the European biosimilars market in 2025. The leading position of recombinant DNA segments in this regional market is attributed to the precise replication of complex human proteins in microbial or mammalian expression systems. As per EMA, all approved biosimilars in the EU rely on recombinant DNA methods to produce the target molecule with high fidelity to the reference product. This technology allows for the insertion of human gene sequences into host cells such as E. coli, yeast, or Chinese hamster ovary cells, which then synthesize the therapeutic protein under controlled bioreactor conditions. The European Commission’s 2023 Biomanufacturing Review states that over 85% of biosimilar production facilities in Europe use mammalian cell lines cultivated through recombinant DNA platforms due to their ability to perform human‑like post‑translational modifications. Regulatory acceptance is universal, as the European Pharmacopoeia includes detailed monographs on recombinant protein quality attributes, including sequence integrity, folding, and purity. Academic institutions such as the Technical University of Munich and ETH Zurich continue to refine vector design and promoter systems to enhance yield and consistency. This scientific maturity and regulatory integration make recombinant DNA technology the indispensable backbone of Europe’s biosimilar manufacturing ecosystem.

The mass spectroscopy segment is the fastest growing technology segment in theEuropeane biosimilars market over the forecast period, owing to its critical role in higher‑order structure characterization and post‑translational modification mapping during biosimilar development. As per EMA, mass spectroscopy is now mandatory for demonstrating primary structure identity and quantifying critical quality attributes such as deamidation, oxidation, and glycosylation site occupancy. The European Directorate for the Quality of Medicines reports that over 200 biosimilar dossiers submitted between 2021 and 2023 included high‑resolution mass spectrometry data as a core analytical pillar. Technological advances such as native mass spectrometry and ion mobility now enable assessment of quaternary structure and aggregation propensity,y as these are key factors in immunogenicity risk. Companies such as Thermo Fisher and Waters have established dedicated biosimilar application labs in Germany and the UK to support European developers. Additionally, Horizon Europe allocated €45 million in 2023 to standardize mass spectrometry protocols across national reference laboratories. This analytical indispensability ensures mass spectroscopy’s rapid adoption as the gold standard for biosimilar comparability in Europe.

By Disease Insights

The chronic and autoimmune diseases segment occupied the leading share of the European biosimilars market in 2025. The growth of the chronic and autoimmune diseases segment in this regional market is majorly due to the high prevalence of conditions such as rheumatoid arthritis, psoriasis, Crohn’s disease, and ankylosing spondylitis, which are routinely managed with biologic therapies. As per the European Centre for Disease Prevention and Control (ECDC), over 25 million Europeans live with autoimmune disorders requiring long‑term treatment. EMA notes that biosimilars of infliximab, adalimumab, and etanercept collectively account for over 70% of all biosimilar sales in Europe, with rheumatology indications driving volume. National health systems prioritize these areas for cost containment, as biologics previously consumed up to 40% of hospital pharmacy budgets in immunology (European Observatory on Health Systems and Policies). In Germany and the Netherlands, biosimilar uptake in autoimmune diseases exceeds 90% due to mandatory hospital tenders and physician education campaigns by the German Society for Rheumatology. Furthermore, EULAR updated its 2023 treatment guidelines to state that biosimilars are therapeutically equivalent to originators for both treatment initiation and switching. This combination of disease burden, policy focus, and clinical endorsement solidifies chronic and autoimmune diseases as the dominant biosimilar application area.

The oncology segment is the fastest-growing disease segment in the European biosimilars market and is estimated to register a CAGR of 17.7% over the forecast period, owing to the patent expiry of high‑cost monoclonal antibodies such as trastuzumab, rituximab, and bevacizumab, which are foundational in breast, lymphoma, and colorectal cancer regimens. As per the European Cancer Information System, over 1.8 million new patients received biologic cancer therapy in Europe in 2023, creating immense fiscal pressure on public payers. The European Organisation for Research and Treatment of Cancer (EORTC) reports that biosimilar trastuzumab achieved 88% hospital penetration in Sweden and Denmark within two years of launch, enabling expanded access to dual HER2 blockade. Furthermore, EMA approved the first biosimilar of rituximab for subcutaneous use in 2025, reducing administration time and clinic burden. National cancer plans in France and Italy now mandate biosimilar use for all new patients unless contraindicated. With over 3.9 million new cancer cases annually in Europe (IARC), the oncology biosimilar market is poised for rapid and sustained expansion.

COUNTRY LEVEL ANALYSIS

Germany Biosimilars Market Analysis

Germany dominated the market by accounting for 23.4% of the European market share in 2025. The leading position of Germany in this regional market is attributed to its early adoption of mandatory hospital tenders, reference pricing, and physician incentive programs that collectively drive biosimilar uptake. As per the GKV Spitzenverband, statutory health insurers achieved over 90% biosimilar penetration for infliximab and etanercept by 2023. Germany also hosts Europe’s highest concentration of biosimilar manufacturing facilities, including plants operated by STADA and Hexal, ensuring supply security. The Paul Ehrlich Institute actively supports developers through scientific advice programs that have reduced approval timelines by 30%. Additionally, national treatment guidelines from the German Society of Hematology and Oncology require biosimilar use in all new cancer patients unless clinically justified otherwise. This ecosystem of policy enforcement, industrial capacity, and clinical alignment ensures Germany remains the cornerstone of Europe’s biosimilar landscape.

France Biosimilars Market Analysis

France held the second-largest share of the European biosimilars market in 2025. The nation’s strong position is anchored in its centralized health technology assessment system, aggressive substitution policies, and hospital governance reforms. The Haute Autorité de Santé mandates that hospitals switch at least 80% of new patients to biosimilars within six months of market entry. As a result, biosimilar adalimumab reached 85% market share in rheumatology by 2023, according to the French National Authority for Health. France also leads in oncology biosimilar adoption, with trastuzumab biosimilars used in over 90% of new HER2‑positive breast cancer cases. The government’s 2023 biosimilar roadmap allocates €120 million to support regional switching programs and physician education. Furthermore, France hosts key manufacturing sites for laboratories such as Biogaran and Teva, which supply biosimilars across Southern Europe. This blend of top‑down policy, scientific rigor, and industrial capability sustains France’s role as a high‑impact biosimilar market.

United Kingdom Biosimilars Market Analysis

The United Kingdom is expected to account for a prominent share of the European biosimilars market over the forecast period. Despite post‑Brexit regulatory divergence, the UK maintains scientific alignment with EMA biosimilar standards through the MHRA. The NHS achieved 95% biosimilar infliximab penetration in England by 2023 through its national commissioning framework, which includes financial incentives for clinical commissioning groups. NICE recommends biosimilars as first‑line in all eligible indications, including oncology and rheumatology. Academic centers such as the University of Leeds lead real‑world evidence generation, with the British Society for Rheumatology’s registry tracking over 50,000 patients on biosimilar therapies. Additionally, the UK’s Innovative Licensing and Access Pathway fast‑tracks promising biosimilars with reduced evidence requirements for unmet needs. This combination of national coordination, clinical trust, and regulatory agility ensures the UK remains a top‑tier biosimilar market in Europe.

Italy Biosimilars Market Analysis

Italy is predicted to witness a healthy CAGR in the European biosimilars market over the forecast period. The country’s market strength arises from its regional healthcare autonomy, high biologic utilization, and recent policy reforms to accelerate biosimilar adoption. The National Oncology Network mandated biosimilar trastuzumab for all new breast cancer patients in 2023, leading to 82% uptake within one year. Similarly, the Italian Medicines Agency introduced price linkage that automatically reduces originator reimbursement when biosimilars enter the market. However, regional disparities persist, with biosimilar use in the South lagging 25 percentage points behind the North, according to ISTAT. To address this, the Ministry of Health launched a 2025 national biosimilar education program targeting prescribers in underserved areas. Italy also hosts major production facilities for companies such as Zentiva and Mundipharma, supporting domestic supply. This mix of national ambition, regional variation, and industrial presence defines Italy’s evolving biosimilar landscape.

Sweden Biosimilars Market Analysis

Sweden is estimated to hold a notable share of the European market over the forecast period. The country’s outsized influence stems from its universal healthcare system, centralized procurement, and pioneering role in real‑world evidence generation. Sweden achieved 100% biosimilar substitution for erythropoietin and filgrastim by 2022 through national pharmaceutical benefits agency decisions that delist originators after biosimilar entry. The Swedish Rheumatology Quality Register shows identical drug survival rates between originator and biosimilar adalimumab over five years, providing robust clinical reassurance. Additionally, Sweden participates in the Nordic Biosimilar Collaboration, which harmonizes health technology assessments across five countries, accelerating regional uptake. The Karolinska Institute leads research on immunogenicity monitoring using national health registries linking over 10 million patients. With strong public trust in health authorities and minimal private sector interference, Sweden exemplifies how transparent policy and data‑driven governance can maximize biosimilar value across a national health system.

COMPETITIVE LANDSCAPE

Competition in the European Biosimilars Market is characterized by scientific rigor, regulatory sophistication, and strategic alignment with public health priorities among a mix of established pharmaceutical firms and specialized biotech developers. Unlike generic markets, where price dominates,s value is determined by analytical depth, clinical validation,n manufacturing consistency,y and post-launch surveillance. The European Medicines Agency’s centralized approval process ensures a high entry barrier, favoring companies with extensive biologics experience. Incumbents like Sandoz and Fresenius Kabi compete on portfolio breadth, supply reliability, and hospital integration, while newer entrants such as Biocon Biologics differentiate through cost efficiency and emerging molecule pipelines. National tender systems intensify price competition but also reward quality assurance and service continuity. Legal challenges from originators further complicate entry, requiring robust patent clearance strategies. As the market matures,s competition is shifting toward next-generation biosimilars for complex oncology agents and enhanced real-world data generation. Success in this environment demands scientific excellence, regulatory agility,y and deep collaboration with European healthcare institutions.

KEY MARKET PLAYERS

Some of the promising companies operating in the europe biosimilars market profiled in this report are

- Sandoz International GmbH

- Wockhardt Ltd

- Hospira, Inc.

- Teva Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories

- Biocon Limited

- Mylan, Inc.

- Zydus Cadila

- Celltrion Inc.

- Roche Diagnostics

- Cipla Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Sandoz is a global pioneer in the biosimilars space and a cornerstone of theEuropeane Biosimilars Market with a portfolio spanning oncology,y immunology, and supportive care. The company launched the world’s first biosimilar in Europe in 2006 and continues to lead in scientific validation and regulatory engagement. In 2025, Sandoz received European Medicines Agency approval for a biosimilar of ustekinumabb expanding access to psoriasis and Crohn’s disease treatment. It also strengthened its European manufacturing footprint by upgrading its biosimilar production facility in Kundl, Austria, to support higher capacity and next-generation molecules. Through partnerships with national health systems and professional societies, Sandoz reinforces trust in biosimilar switching and long-term safety across Europe.

- Fresenius Kabi plays a significant role in the European Biosimilars Market with a focused portfolio of monoclonal antibodies and supportive care biosimilars used in hospital settings. The company leverages its integrated healthcare infrastructure to ensure seamless distribution and clinical adoption. In early 2025, Fresenius Kabi launched a biosimilar of bevacizumab in multiple European countries following successful phase III trials in metastatic colorectal cancer. It also enhanced its pharmacovigilance network across 25 European nations to monitor real-world safety outcomes post launch. By aligning its biosimilar strategy with hospital tendering requirements and oncology treatment guidelines, Fresenius Kabi strengthens its position as a reliable supplier of cost-effective biologics in Europe’s public health systems.

- Biocon Biologics exerts growing influence in theEuropeane Biosimilars Market through its scientifically rigorous and affordable monoclonal antibody biosimilars developed in partnership with global pharmaceutical leaders. The company’s trastuzumab and bevacizumab biosimilars are widely used in oncology centers across Southern and Eastern Europe. In 202,4 Biocon Biologics expanded its European regulatory presence by establishing a dedicated scientific affairs office in Amsterdam to engage with health technology assessment bodies. It also initiated a real-world evidence study with academic hospitals in Spain and Poland to evaluate long-term outcomes in breast cancer patients. These actions demonstrate Biocon’s commitment to scientific credibility and sustainable access in Europe’s evolving biosimilar ecosystem.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Biosimilars Market employ four primary strategies to sustain competitive advantage. First, they invest in robust analytical and clinical comparability programs to meet the European Medicines Agency’s stringent requirements and build prescriber confidence. Second, they secure localized manufacturing and supply chain infrastructure within Europe to ensure reliability and comply with pharmacovigilance obligations. Third, they engage proactively with national health technology assessment bodies and hospital tender committees to facilitate rapid reimbursement and volume procurement. Fourth, they generate real-world evidence through post-marketing studies and disease registries to validate long term safety and support switching protocols. Additionally, companies conduct targeted physician education initiatives to address therapeutic misconceptions and promote biosimilar adoption across specialties. These strategies collectively enhance regulatory credibility, market access,s and clinical trust in Europe’s highly scrutinized biosimilar landscape.

MARKET SEGMENTATION

This research report on the europe biosimilars market has been segmented and sub-segmented into the following categories.

By Product Type

- Protein

- Insulin

- Human Growth Hormones

- Granulocyte Colony-stimulating Factor (G-CSF)

- Interferons

- Recombinant Glycosylated Proteins

- Erythropoietin

- Monoclonal Antibodies

- Follitropin

- Recombinant Peptides

- Glucagon

By Technology

- Mass Spectroscopy

- Chromatography

- Monoclonal Antibody Technology

- Recombinant DNA Technology

- Nuclear Magnetic resonance (NMR) technology

- Electrophoresis

- Bioassay

By Disease

- Oncology Diseases

- Blood Disorders

- Growth hormone deficiencies

- Chronic and autoimmune diseases

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe