- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

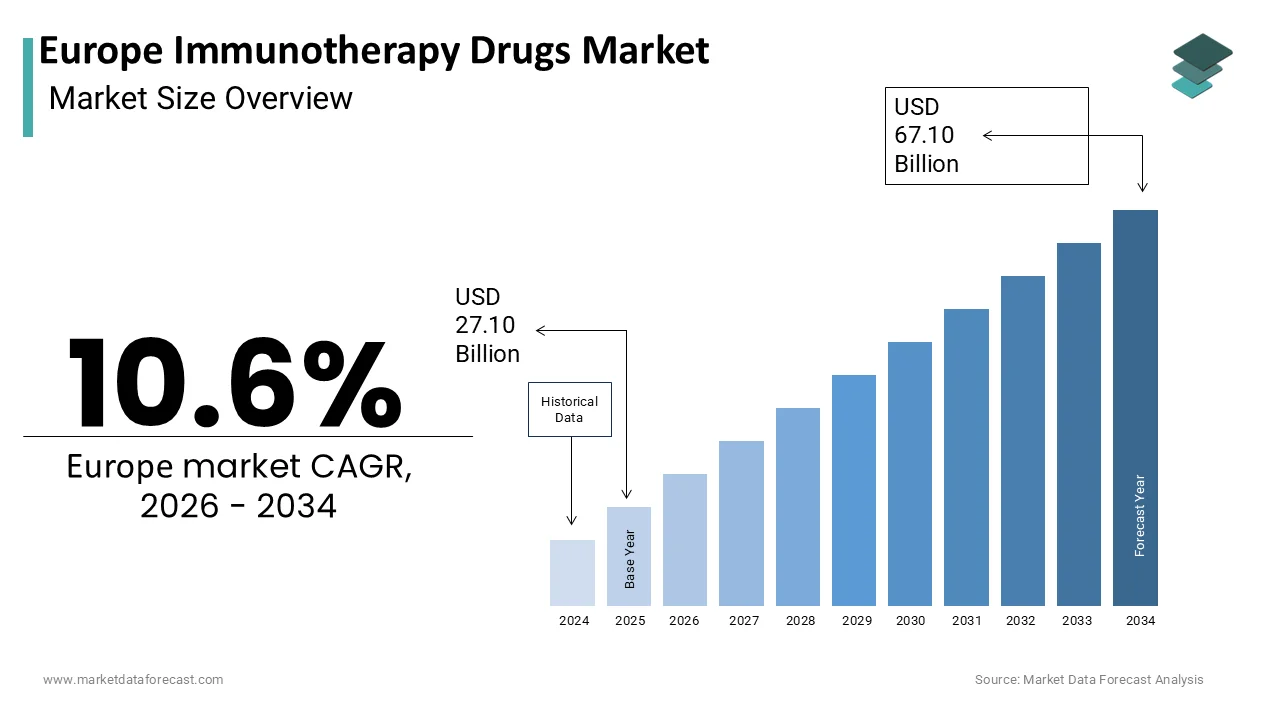

Market Size, 2025

$27.10 BnMarket Estimate, 2026

$29.97 BnMarket Forecast, 2034

$67.10 BnCAGR, 2026–2034

10.6%Europe Immunotherapy Drugs Market Summary

Market Size & Growth

- Europe immunotherapy drugs market was valued at USD 27.10 billion in 2025.

- Expected to reach USD 29.97 billion in 2026 and USD 67.10 billion by 2034, growing at a CAGR of 10.6% from 2026 to 2034.

- Germany led the market in 2025, holding 20.3% of regional market share.

Key Market Segments

- By drug type: Monoclonal antibodies, interferons, interleukins, vaccines, checkpoint inhibitors.

- By application: Lung cancer, melanoma, blood cancer, breast cancer, cervical cancer, glioblastoma, gastric cancer, prostate cancer.

- By country: UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Russia, Turkey, Czech Republic.

- Monoclonal antibodies held the largest drug-type share in 2025; checkpoint inhibitors are the fastest-growing, at a CAGR of 15.1%.

- Lung cancer held the largest application share in 2025; melanoma is the fastest-growing application, at a CAGR of 20.9%.

Key Drivers

- Rising incidence of cancer and immune-mediated disorders (rheumatoid arthritis, psoriasis, multiple sclerosis) across Europe.

- Accelerated EMA regulatory pathways (PRIME scheme) and public investment in translational immunology.

- Expanding non-oncologic applications, including severe asthma, chronic urticaria, and alopecia areata.

Key Players

Roche, Merck, Eli Lilly, Novartis, AstraZeneca, GlaxoSmithKline PLC, Amgen, Celgene, Bristol Myers Squibb, Seattle Genetics.

Europe Immunotherapy Drugs Market Size

The Europe Immunotherapy Drugs Market is projected to grow from USD 27.10 billion in 2025 to USD 29.97 billion in 2026 and reach USD 67.10 billion by 2034, registering a CAGR of 10.6% during the forecast period from 2026 to 2034.

Immunotherapy drugs are a transformative class of therapeutic agents that harness the body’s immune system to identify and eliminate malignant or infected cells. In Europe, this approach has increasingly become integral to oncology, rheumatology,y and infectious disease management as clinical paradigms shift from purely cytotoxic regimens toward precision immune modulation. Agents were active across the European Union in 2025, which reflects substantial scientific and regulatory momentum. According to the International Agency for Research on Cancer, the WHO Europe region recorded about 4.88 million new cancer cases in 2022, while EU‑specific estimates put new cancer cases in the EU at approximately 2.7 million in 2022, which indicates the persistent clinical urgency that drives therapeutic innovation. Unlike traditional pharmaceutical models, immunotherapy encompasses diverse modalities including immune checkpoint inhibitors, monoclonal antibodies, cancer vaccines, and cellular therapies, each tailored to modulate specific immune pathways. The European regulatory framework has notably accelerated conditional approvals and early support for breakthrough immunotherapies through the EMA’s PRIME scheme, which prioritizes medicines addressing unmet medical needs and offers enhanced interaction to speed development and evaluation. This evolving ecosystem is shaped not by market metrics but by demographic shifts, disease‑burden patterns, and institutional investment in translational immunology, all converging to redefine therapeutic standards across the continent.

MARKET DRIVERS

Rising Incidence of Immune‑Mediated and Oncologic Disorders Fuels Therapeutic Demand

The escalating burden of cancer and chronic inflammatory diseases across European nations is one of the major factors propelling the growth of the European immunotherapy drugs market. Regional cancer registries document millions of new cancer diagnoses annually across Europe, with lung, colorectal, and breast cancers among the most prevalent. This sustained oncologic pressure has intensified demand for therapies that offer durable responses beyond conventional chemotherapy. Concurrently, immune‑mediated conditions such as rheumatoid arthritis, psoriasis,s and multiple sclerosis affect large patient populations across the European Union, which is creating substantial long‑term demand for immunomodulatory treatments. These disorders often require prolonged therapy where biologic agents demonstrate superior efficacy over many small‑molecule alternatives. According to the European Society for Medical Oncology, rapid clinical assimilation of immune checkpoint inhibitors and other immunotherapies in appropriate indicatios,reflectsg changing standards of care. Furthermore, national cancer plans in Germany, France,e and the Netherlands explicitly prioritize access to immunotherapies and align reimbursement policies with clinical guidelines. This convergence of epidemiologic necessity and health‑system endorsement creates a fertile ground for continued therapeutic deployment. The persistent rise in age‑adjusted incidence for certain hematologic malignancies and solid tumours ensures that immunotherapy remains central to Europe’s therapeutic arsenal.

Accelerated Regulatory Pathways and Public Investment in Translational Immunology

Europe’s strategic emphasis on fast‑tracking innovative biologics through tailored regulatory mechanisms has significantly expanded patient access to immunotherapies, which is further supporting the growth of the European immunotherapy drugs market. The European Medicines Agency’s priority and accelerated‑assessment pathways provide regulatory support that shortens review timelines for medicines addressing unmet medical needs. Public funding and EU research programmes channel substantial resources into immuno‑oncology and translational immunology, which is supporting academic‑industry partnerships and manufacturing capacity building. National institutes and centres of excellence across member states have launched dedicated cellular‑therapy manufacturing hubs supported by public grants. Additionally, pan‑European clinical trial networks and cooperative groups facilitate multi‑country protocol harmonization and operational efficiencies that reduce development timelines. These structural enablers not only de‑risk commercialization but also ensure that academic breakthroughs translate more rapidly into clinical practice. As a result, Europe has become a leading region for early‑phase studies and first‑in‑human trials for next‑generation immunotherapies, including bispecific engagers and engineered T‑cell receptors.

MARKET RESTRAINTS

High Treatment Costs and Uneven Reimbursement Frameworks Impede Broad Accessibility

Despite scientific advances, the economic burden of immunotherapy remains a critical barrier to equitable patient access across European healthcare systems, which is hindering the growth of the European immunotherapy drugs market. Per‑patient costs for many advanced immunotherapies are very high and place substantial pressure on health‑system budgets and HTA processes. This cost strain is particularly acute in countries with more constrained public finances, where formulary inclusion and reimbursement criteria are often more restrictive. Reimbursement decisions vary significantly even among high‑income nations, with some systems imposing narrow eligibility criteria based on biomarkers or prior treatment lines, while others adopt broader coverage. Patient co‑payments and out‑of‑pocket expenses can be substantial in certain member states, creating financial toxicity and driving cross‑border care seeking that fragments clinical‑outcomes data. Moreover, conventional cost‑effectiveness thresholds and short‑term budget impact frameworks sometimes fail to capture long‑term survival benefits unique to immunotherapy, which leads to negative or conditional recommendations despite demonstrated clinical efficacy. Without more harmonized pricing and reimbursement strategies that recognize long‑term value, the full therapeutic potential of these agents will remain unevenly realized across Europe.

Complex Manufacturing and Supply‑Chain Vulnerabilities for Advanced Therapies

The growth of the European immunotherapy drugs market is also constrained by the production of cell‑ and gene‑based immunotherapies that present formidable logistical and infrastructural challenges and constrain scalability across Europe. Autologous therapies such as CAR‑T products require patient‑specific apheresis, cryopreservation, and centralized manufacturing with multi‑week vein‑to‑vein timelines reported in clinical practice analyses. The number of certified commercial manufacturing facilities and GMP‑capable sites in the EU is limited, which is restricting geographic reach and creating bottlenecks during demand surges. Temperature‑sensitive supply chains further exacerbate fragility, with cold‑chain integrity and reprocessing events documented by regulatory audits and national control authorities. Workforce shortages compound these issues as only a subset of clinical centres possesses the specialised personnel required for administration, monitoring, and toxicity management of advanced cellular therapies. Regional disparities are stark, with some countries lacking certified treatment centres despite comparable disease incidence. Additionally, dependencies on non‑European suppliers for viral vectors, cytokines,s and other critical inputs introduce geopolitical and continuity risks that have materialized during past supply disruptions. Until decentralized manufacturing models, standardized logistics protocols, ls and expanded clinical capacity are implemented, the promise of advanced immunotherapies will remain concentrated in select academic and commercial hubs rather than broadly accessible across the continent.

MARKET OPPORTUNITIES

Expanding Indications in Non‑Oncologic Immune Disorders Open New Clinical Frontiers

The therapeutic scope of immunotherapy is rapidly broadening beyond oncology into chronic inflammatory and autoimmune conditions where immune dysregulation plays a central pathogenic role, which is a major opportunity in tEuropeanope immunotherapy drugs market. Allergic diseases, including severe asthma and chronic urticaria, affect large patient populations across Europe and are increasingly managed with biologic immunomodulators. Recent regulatory approvals have extended targeted cytokine inhibitors into new indications such as refractory eosinophilic disorders, and novel agents targeting pathways like JAK–STAT have shown clinically meaningful efficacy in conditions such as alopecia areata. The economic rationale is compelling: many non‑oncologic indications entail longer treatment durations and lower manufacturing complexity than cellular therapies. National health‑technology assessment bodies are beginning to recognize this value, and real‑world evidence platforms are generating outcome data that facilitate label expansions. This diversification mitigates dependency on the oncology segment and leverages existing immunology expertise within European academic centres, which is accelerating clinical adoption across therapeutic domains.

Integration of Artificial Intelligence in Biomarker Discovery Enhances Patient Stratification

The application of artificial intelligence to multi‑omics data is transforming the identification of predictive biomarkers that maximize immunotherapy response while minimizing adverse events, which is another promising opportunity in the European immunotherapy drugs market. European research consortia and academic centres have developed machine‑learning approaches that analyse circulating tumour DNA, transcriptomic profiles, and immune‑repertoire data to forecast treatment response with promising validation results. Increasing numbers of academic medical centres now employ AI‑supported platforms to inform therapy selection in indications such as non‑small‑cell lung cancer and melanoma. Industry and public‑sector investments in digital pathology and genomic infrastructure are strengthening these capabilities. Crucially, this precision approach addresses a key limitation of immunotherapy by enabling dynamic, composite biomarker assessment rather than relying on single static tests. Regulatory bodies are adapting oversight frameworks for AI‑enabled diagnostics, positioning Europe to lead in next‑generation personalized therapy delivery.

MARKET CHALLENGES

Managing Immune‑Related Adverse Events Requires Specialized Clinical Infrastructure

The unique toxicity profile of immunotherapies, particularly immune‑related adverse events, presents significant clinical‑management challenges that strain existing healthcare capacities, which is a major challenge to the expansion of the European immunotherapy drugs market. Severe toxicities from combination checkpoint blockade can affect endocrine, gastrointestinal, and dermatologic systems and often require multidisciplinary intervention involving endocrinologists, gastroenterologists,s and dermatologists. Many community hospitals lack formal immunotherapy‑toxicity management protocols and dedicated pathways for rapid recognition and escalation. Delayed diagnosis of rare but life‑threatening complications such as myocarditis can result in high mortality if not identified and treated promptly. Training gaps in oncology and allied specialties further compound the issue, and variability in care quality contributes to treatment interruptions that undermine therapeutic benefit. Without standardized surveillance algorithms, dedicated toxicity clinics, cs and widespread clinician education, the safe, equitable rollout of advanced immunotherapies across diverse care settings will remain constrained.

Ethical and Data‑Governance Complexities in Cross‑Border Real‑World Evidence Generation

Reliance on real‑world data to evaluate long‑term immunotherapy outcomes has exposed critical gaps in Europe’s ethical and regulatory frameworks for cross‑national health‑data sharing, which is further challenging the growth of tEuropeanope immunotherapy drugs market. While initiatives such as the European Health Data Space aim to harmonize access, multiple national data‑protection regimes still govern patient‑level information and create legal uncertainty for multi‑country studies. Interoperability of oncology registries and heterogeneity in consent models vary across jurisdictions, delaying pooled analyses of rare immune‑related toxicities or late relapse patterns. These inconsistencies slow post‑marketing surveillance at a time when it is crucial for novel agents such as T‑cell engagers. Commercial partners also face heightened scrutiny under data‑protection rules when collaborating with public health systems, complicating public–private research partnerships that are essential for scalable data infrastructure. Without a unified ethical‑governance architecture and interoperable technical standards, Europe risks fragmenting its evidence base and weakening the scientific foundation needed to optimize immunotherapy deployment across diverse populations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Drug Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Market Leaders Profiled | Roche, Merck, Eli Lilly, Novartis, AstraZeneca, GlaxoSmithKline PLC |

SEGMENTAL ANALYSIS

By Drug Type Insights

The monoclonal antibodies segment commanded the leading share of the European immunotherapy drugs market in 2025 due to their versatility, broad clinical validation, and regulatory maturity across oncologic and autoimmune indications. These engineered proteins precisely target disease‑associated antigens with high specificity, minimizing off‑target effects compared to conventional cytotoxic agents. Regulatory listings and therapeutic registries show dozens of monoclonal antibody products authorised for use across the EU, with many indicated for cancer therapy and other serious diseases. Their dominance is further reinforced by established manufacturing protocols and inclusion in national treatment guidelines. For instance, the European Society for Medical Oncology recommends trastuzumab for HER2‑positive breast cancer and rituximab for CD20‑positive lymphomas as standard of care. Clinical utilisation data and health system reports indicate substantial patient exposure to monoclonal antibody‑based therapies across Europe, reflecting deep clinical penetration. Additionally, biosimilar competition has expanded access by reducing prices in several Member States, improving affordability and uptake. This combination of therapeutic efficacy, regulatory endorsement, and improved cost accessibility solidifies monoclonal antibodies as the backbone of Europe’s immunotherapy landscape.

The checkpoint inhibitors segment is among the fastest-expanding drug classes in theEuropeane immunotherapy drugs market and is expected to witness a CAGR of 15.1% over the forecast period, owing to their transformative impact in multiple solid tumours and a steady stream of new regulatory approvals and label expansions. This acceleration stems from their ability to induce durable remissions in indications where historical therapies delivered limited long‑term benefit. European regulators and national health technology assessments have approved numerous new checkpoint inhibitor indications in recent years, and real‑world evidence across registries supports meaningful survival gains in several tumour types. National health systems are responding by streamlining access and integrating companion diagnostics such as PD‑L1 testing into reimbursement pathways. Moreover, academic centres across Europe are pioneering neoadjuvant and combination checkpoint blockade protocols that reduce surgical morbidity and improve pathologic response rates. These advances collectively position checkpoint inhibitors at the vanguard of immuno‑oncology innovation in Europe.

By Application Insights

The lung cancer segment was a leading application segment for immunotherapy drugs in Europe and held the highest share of the European immunotherapy drugs market in 2025. The leading position of the lung cancer segment in the European market is driven by high disease incidence, historically limited efficacy of older therapies, and robust clinical evidence supporting immune checkpoint blockade. Europe records hundreds of thousands of new lung cancer cases annually, and immunotherapy has rapidly been integrated into first‑line and subsequent treatment pathways for non‑small cell lung cancer in many Member States. The integration of immunotherapy into first‑line treatment has been rapid in countries with established biomarker and registry infrastructure, and a large share of eligible non‑small cell lung cancer patients in several major markets now receive PD‑1 or PD‑L1 inhibitors as part of standard care. This adoption is underpinned by survival benefits demonstrated in pivotal trials and validated in European subpopulations. Additionally, comprehensive biomarker testing infrastructure in countries like Sweden and the Netherlands enables precise patient selection, maximizing therapeutic yield. The convergence of epidemiologic burden, clinical validation, and diagnostic readiness ensures lung cancer remains a primary therapeutic gateway for immunotherapy in Europe.

The melanoma segment is anticipated to grow at a CAGR of 20.9% over the forecast period in theEuropeane immunotherapy drugs market. Melanoma is a highly dynamic and fast‑growing application area for immunotherapy, propelled by the paradigm‑shifting efficacy of combination checkpoint regimens and expanding adjuvant and neoadjuvant indications. Clinical trial and registry evidence show dramatic improvements in long‑term outcomes for advanced melanoma with dual checkpoint blockade, with five‑year survival rates rising substantially and exceeding 50% in some study cohorts. Early detection initiatives and national screening or awareness programs in several countries increase the pool of patients eligible for curative‑intent and adjuvant immunotherapy, amplifying demand. Regulatory support has been strong, with multiple melanoma‑specific label expansions and guideline updates in recent years. Real‑world registries demonstrate high uptake of adjuvant anti‑PD‑1 therapy in appropriate stage III patients following resection. This synergy of survival breakthroughs, earlier diagnosis, and proactive treatment protocols drives melanoma’s position as one of Europe’s most dynamic immunotherapy application areas.

COUNTRY LEVEL ANALYSIS

Germany Immunotherapy Drugs Market Analysis

Germany led the immunotherapy drugs market in Europe in 2025 by holding 20.3% of the regional market share. The dominance of Germany in the European market can be credited to its integrated oncology care model, robust biopharmaceutical innovation ecosystem, and early adoption of advanced therapies. Germany hosts a high number of certified immunotherapy administration centers and maintains a centralized biomarker testing infrastructure that processes large volumes of PD‑L1 and other companion diagnostics annually. The statutory health insurance system covers EMA‑approved immunotherapies with limited patient cost exposure, supporting broad access. Public investment in cellular‑therapy infrastructure has increased in recent years, with federal and state funding directed to CAR‑T manufacturing and academic hospital platforms. Clinical trial participation is strong, with German sites enrolling a substantial share of European patients in late‑phase immuno‑oncology studies. This confluence of clinical capacity, regulatory efficiency, and scientific investment cements Germany’s dominance in the regional immunotherapy landscape.

United Kingdom Immunotherapy Drugs Market Analysis

The United Kingdom is a leading market in Europe with rapid uptake of high‑value immunotherapies driven by centralized health‑technology assessment and NHS commissioning pathways. The NHS has treated a growing number of cancer patients with immune‑checkpoint inhibitors as indications expand across tumor types. The UK also leads in real‑world evidence generation through national registries that link treatment and outcome data for the vast majority of diagnosed cases. The Medicines and Healthcare products Regulatory Agency operates innovation and early‑access mechanisms that have accelerated the availability of promising immunotherapies, and strong academic research capacity continues to feed clinical adoption and trial activity. These structural advantages ensure the UK remains a top‑tier immunotherapy market in Europe.

France Immunotherapy Drugs Market Analysis

France is a major European market for immunotherapies, supported by proactive national cancer strategies, centralized reimbursement mechanisms, and high clinical‑trial density. National cancer plans prioritize equitable access to advanced therapies and have mobilized multi‑year funding to expand treatment capacity in underserved regions. A large proportion of French oncology departments are certified to administer complex immunotherapies, including cellular therapies, and the national appraisal and reimbursement pathways have been streamlined to shorten the time to patient access. France’s extensive trial network enables rapid translation of research into practice, reinforcing its sustained leadership in the European immunotherapy domain.

Italy Immunotherapy Drugs Market Analysis

Italy is an important and expanding immunotherapy market driven by regional oncology networks, national efforts to standardize biomarker testing, and growing clinical capacity. Standardized PD‑L1 and other biomarker protocols have been implemented nationally to improve patient identification for checkpoint inhibitors and targeted immunotherapies. The Italian health system now funds approved immunotherapies for on‑label indications, and academic reference centers play a leading role in cellular‑therapy trials and capability building. Demographic trends and an aging patient population further support rising demand for less‑toxic immunotherapeutic regimens. These systemic adaptations position Italy as a resilient and growing market for immunotherapy drugs.

Spain Immunotherapy Drugs Market Analysis

Spain is a significant market for immunotherapies in Europe, underpinned by a national precision‑medicine strategy, coordinated diagnostic infrastructure, and expanding clinical research output. Nationwide genomic and molecular profiling programs have increased routine assessment of PD‑L1 and other biomarkers in major hospitals, directly supporting immunotherapy selection. Spanish oncology centers have scaled immunotherapy delivery across multiple tumor types following recent approvals, and strategic public investment has targeted infusion‑facility upgrades and specialist nursing training for immune‑related toxicity management. Active participation in multinational research consortia and EU‑funded projects further strengthens Spain’s role among Europe’s top immunotherapy markets.

COMPETITIVE LANDSCAPE

Competition in Europeanrope immunotherapy drugs market is characterized by intense scientific differentiation, strategic partnerships,s and regulatory agility among global pharmaceutical leaders. Companies prioritize clinical validation through region-specific trials to align with the European Medicines Agency’s stringent evidence requirements. The landscape is further shaped by collaborations between industry and public research institutions to accelerate biomarker discovery and therapy personalization. While large firms dominate therapeutic innovation, mid-sized biotechs contribute disruptive modalities such as engineered cytokines and neoantigen vaccines. Pricing pressures and fragmented reimbursement policies compel manufacturers to demonstrate long term value through real-world evidence generation. Simultaneously, workforce training and infrastructure development remain competitive differentiators,s particularly for complex therapies like CAR T cells. This dynamic environment fosters continuous innovation but demands deep integration with Europe’s healthcare ecosystems to achieve sustainable market success.

KEY MARKET PLAYERS

Top Companies leading the europe immunotherapy drugs market Profiled in the Report are

- Roche

- Merck

- Eli Lilly

- Novartis

- AstraZeneca

- GlaxoSmithKline PLC

- Amgen

- Celgene

- Bristol Myers Squibb

- Seattle Genetics

TOP LEADING PLAYERS IN THE MARKET

- Roche maintains a prominent position in the European immunotherapy drugs market through its foundational role in developing monoclonal antibodies and immune checkpoint inhibitors. The company’s anti-PD L1 agent atezolizumab is widely used across European oncology centers for bladder and lung cancers. Roche recently expanded its immuno-oncology pipeline by initiating phase III trials for a novel T cell-engaging bispecific antibody targeting solid tumors in collaboration with European academic institutions. It also reinforced its European manufacturing footprint by upgrading its Basel facility to support commercial-scale production of next-generation immunotherapies. These actions underscore Roche’s commitment to advancing immune-based cancer treatment and enhancing therapeutic accessibility across the region through scientific innovation and infrastructure investment.

- Bristol Myers Squibb is a key contributor to the European immunotherapy drugs market with its pioneering checkpoint inhibitors nivolumab and ipilimumab, which have redefined melanoma and renal cell carcinoma care across the continent. The company has deepened its European engagement by establishing a Center of Excellence for Cellular Therapy in Amsterdam to support CAR T cell delivery and post treatment monitoring. In 202,4 it launched a pan-European real-world evidence program in partnership with seven national cancer registries to evaluate long term outcomes of combination immunotherapy. Additionally, Bristol Myers Squibb increased its investment in biomarker research through collaborations with the European Organisation for Research and Treatment of Cancer to refine patient selection criteria and optimize therapeutic efficacy across diverse populations.

- Merck KGaA exerts significant influence in the European immunotherapy drugs market through its anti-PD-L1 antibody avelumab, approved for Merkel cell carcinoma and urothelial cancer. The company has intensified its regional presenby co-developingngg novel immunotherapies with European biotech firms focusing on tumor microenvironment modulation. In 2025, Merck KGaA inaugurated a dedicated immunotherapy research hub in Darmstadt to acceleratethe discovery of next-generation checkpoint targets. It also expanded access programs in Southern and Eastern Europe to ensure equitable availability of its agents in resource-constrained settings. By aligning its innovation strategy with Europe’s public health priorities and scientific ecosystem, Merck KGaA continues to strengthen its role as a trusted partner in advancingimmune-mediatedd cancer therapies across the continent.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European immunotherapy drugs market primarily employ four strategic approaches to reinforce their presence. First, they invest heavily in clinical research through partnerships with European academic and oncology networks to generate region-specific evidence. Second, they expand manufacturing and logistics capabilities within the European Union to ensure a reliable supply of temperature-sensitive biologics. Third, they engage proactively with national health technology assessment bodies to facilitate timely reimbursement decisions. Fourth, they develop companion diagnostic tools in coordination with regulatory agencies to enhance patient selection precision. Additionally, companies pursue targeted acquisitions of European biotech startups to access novel immune targets and platform technologies. These strategies collectively enhance scientific credibility,y market access, ss and therapeutic impact across diverse healthcare systems in Europe.

MARKET SEGMENTATION

This research report on the europe immunotherapy drugs market has been segmented and sub-segmented into the following categories.

By Drug Type

- Monoclonal antibodies

- Interferons

- Interleukins

- Vaccines

- checkpoint inhibitors

By Application

- Blood Cancer

- Cervical Cancer

- Breast Cancer

- Glioblastoma

- Lung Cancer

- Gastric Cancer

- Prostate Cancer

- Melanoma

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe