Europe Cerebral Palsy Market Size, Share, Trends & Growth Forecast Report By Type, Treatment, Medical Devices, End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis (2026 to 2034)

Europe Cerebral Palsy Market Size

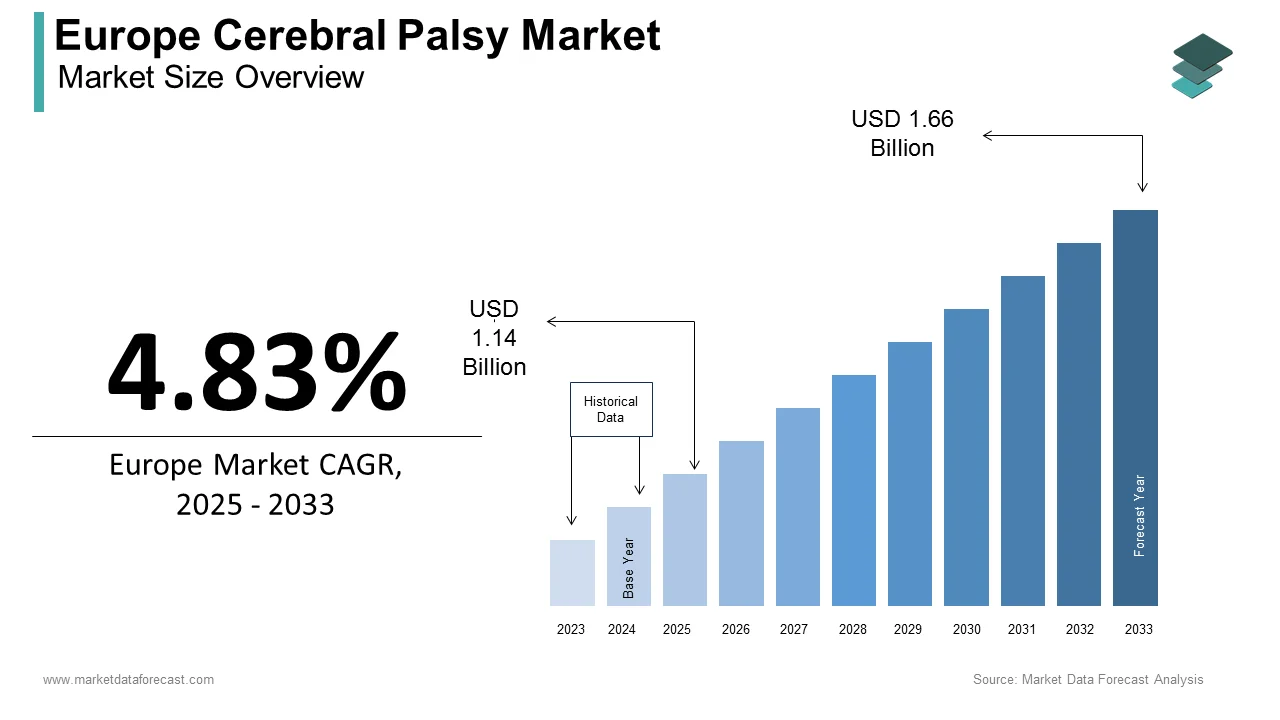

The Europe cerebral palsy market was valued at USD 1.25 billion in 2025, is estimated to reach USD 1.31 million in 2026, and is projected to reach USD 1.91 million by 2034, growing at a CAGR of 4.83% from 2026 to 2034.

The Europe Cerebral Palsy Market encompasses a broad range of therapeutic, assistive, and rehabilitative services and products aimed at managing cerebral palsy (CP), a group of neurological disorders affecting movement, muscle tone, and motor skills. Cerebral palsy is often caused by brain damage that occurs before, during, or shortly after birth. It is one of the most common childhood physical disabilities in developed regions such as Europe.

As per the European Surveillance of Cerebral Palsy (SCPE), approximately 1 in every 500 live births in Europe results in some form of cerebral palsy, making it a significant public health concern. The market includes pharmaceutical treatments, physiotherapy, speech therapy, orthopedic devices, mobility aids, surgical interventions, and advanced rehabilitation technologies tailored for individuals with CP across different age groups.

In addition, early intervention programs have shown measurable improvements in developmental outcomes, further driving investment in specialized therapies and care systems.

With growing awareness, increasing healthcare expenditure, and advancements in medical technology, the European market is evolving rapidly, supported by government initiatives, patient advocacy groups, and cross-border collaborations focused on improving the quality of life for affected individuals.

MARKET DRIVERS

Increased Awareness and Early Diagnosis Initiatives

A primary driver of the Europe Cerebral Palsy Market is the heightened awareness and implementation of early diagnosis initiatives across the region. Governments and healthcare organizations have increasingly emphasized the importance of identifying developmental delays and neurological conditions like cerebral palsy at an early stage to improve long-term outcomes.

Also, early detection programs implemented in countries like Sweden, Germany, and the Netherlands have led to an increase in timely interventions since 2020. These programs include standardized screening tools, neonatal follow-up clinics, and training for pediatricians to recognize early signs of CP.

In the UK, the National Institute for Health and Care Excellence (NICE) issued updated guidelines in 2023 recommending routine developmental assessments for infants born preterm or with low birth weight, which are known risk factors for CP. These guidelines have contributed to a rise in early referrals for specialist evaluation in the first year following their release.

Moreover, non-profit organizations such as United Cerebral Palsy Europe and Scope have played a crucial role in educating families and caregivers about early symptoms and available support. This widespread dissemination of information has led to increased demand for diagnostic services, therapeutic interventions, and assistive technologies, directly fueling market growth.

Advancements in Medical Technology and Rehabilitation Therapies

An additional key driver of the Europe Cerebral Palsy Market is the rapid advancement in medical technology and innovative rehabilitation therapies designed to enhance mobility, communication, and independence for individuals with cerebral palsy.

Also, investments in neurotechnology and digital therapeutics have surged over the past five years, with many new assistive devices approved for use in EU member states since 2020. These include robotic exoskeletons, AI-powered speech-generating devices, and wearable sensors that monitor gait and posture in real time.

In Switzerland, leading institutions such as ETH Zurich have pioneered robotic-assisted gait training systems that are now being adopted in rehabilitation centers across Germany and France.

Moreover, hyperbaric oxygen therapy, constraint-induced movement therapy, and aquatic therapy have gained traction due to growing evidence supporting their efficacy in managing CP symptoms. These technological and therapeutic innovations are not only improving patient outcomes but also expanding the scope and scale of the cerebral palsy treatment market across Europe.

MARKET RESTRAINTS

High Cost of Long-Term Treatment and Rehabilitation

A major restraint in the Europe Cerebral Palsy Market is the high cost associated with long-term treatment and rehabilitation, which limits accessibility for many patients despite the availability of advanced therapies. Managing cerebral palsy requires a lifelong commitment involving multiple interventions such as physiotherapy, occupational therapy, speech therapy, orthopedic surgery, and assistive devices, all of which contribute to significant financial burdens.

Even in countries with robust public healthcare systems like Germany and Sweden, out-of-pocket expenditures remain substantial, particularly for private therapies and cutting-edge assistive technologies.

In Eastern Europe, where healthcare budgets are more constrained, families often face limited access to specialized care due to insufficient funding and inadequate insurance coverage. As per the European Observatory on Health Systems and Policies, nearly 40% of households in Poland and Romania report financial hardship when accessing CP-related treatments, forcing many to rely on charitable organizations or delay essential interventions.

These economic barriers hinder equitable access to comprehensive care and create disparities in treatment outcomes across different socioeconomic groups, ultimately slowing down the overall expansion of the cerebral palsy market in Europe.

Variability in Healthcare Infrastructure Across European Countries

Another critical restraint affecting the Europe Cerebral Palsy Market is the variability in healthcare infrastructure and service availability across different European countries. While Western European nations such as France, Germany, and the Netherlands benefit from well-established healthcare systems with dedicated pediatric neurology units and rehabilitation centers, Eastern and Southern European countries often struggle with fragmented services and uneven access to specialized care.

Furthermore, as per the European Disability Forum, rural areas in countries like Greece, Croatia, and Romania face significant shortages of accessible transport, trained professionals, and equipped facilities, making it difficult for families to access ongoing therapies and interventions. This geographical imbalance results in delayed treatment initiation and inconsistent continuity of care.

Such infrastructural inequalities hinder the uniform development of the cerebral palsy market across Europe and pose a challenge for stakeholders aiming to provide standardized, high-quality care to all patients regardless of their location.

MARKET OPPORTUNITIES

Expansion of Telehealth and Digital Therapy Platforms

A potential opportunity in the Europe Cerebral Palsy Market lies in the rapid expansion of telehealth and digital therapy platforms, which are transforming how care is delivered to individuals with cerebral palsy. The adoption of remote monitoring, virtual consultations, and online rehabilitation services has surged, especially following the acceleration of digital health solutions post-pandemic.

Moreover, startups and tech firms are developing AI-driven apps that track motor development and provide personalized feedback to caregivers and clinicians. With increasing internet penetration and smartphone usage, digital therapy platforms are poised to play a pivotal role in bridging care gaps and expanding access to affordable, continuous support across Europe.

Growth of Personalized Medicine and Genetic Research

One more promising opportunity in the Europe Cerebral Palsy Market is the emergence of personalized medicine and genetic research aimed at understanding the underlying causes of cerebral palsy and tailoring interventions accordingly. Advances in genomics and biomarker identification are enabling researchers to explore potential genetic predispositions and develop targeted therapies for specific subtypes of CP.

According to the European Molecular Biology Laboratory (EMBL), recent genome-wide association studies have identified several candidate genes linked to increased risk of cerebral palsy, opening new avenues for early prediction and customized treatment planning.

In Italy, the Bambino Gesù Children's Hospital is conducting clinical trials on stem cell therapy for cerebral palsy, leveraging regenerative medicine to repair damaged neural tissues.

Also, collaborations between academic institutions, biotech firms, and regulatory bodies are accelerating the translation of research findings into clinical practice. With increased funding from Horizon Europe and other innovation grants, personalized medicine is expected to significantly influence the trajectory of cerebral palsy management across the continent.

MARKET CHALLENGES

Delayed Diagnosis and Lack of Standardized Protocols

A major challenge facing the Europe Cerebral Palsy Market is the issue of delayed diagnosis and the absence of fully standardized protocols for early identification of the condition. Despite growing awareness and improved medical capabilities, many children still go undiagnosed until they are beyond the critical window for early intervention, limiting the effectiveness of therapeutic measures.

According to the European Academy of Childhood Disability, up to 30% of children with cerebral palsy receive a formal diagnosis after the age of two, even though early indicators can often be detected within the first few months of life. This delay is partly attributed to inconsistent application of assessment tools across different healthcare settings and varying levels of expertise among primary care providers.

In countries like Portugal and Hungary, where pediatric neurology resources are limited, general practitioners and midwives may lack sufficient training to recognize early red flags. As per the European Observatory on Health Systems and Policies, disparities in neonatal follow-up programs result in missed opportunities for timely referral to specialist services.

Efforts to implement standardized screening procedures, such as the General Movements Assessment and Hammersmith Infant Neurological Examination, have been slow to gain universal adoption.

Limited Availability of Skilled Professionals and Specialist Centers

Another pressing challenge in the Europe Cerebral Palsy Market is the limited availability of skilled professionals and specialized treatment centers, particularly in rural and less-developed regions. The complexity of cerebral palsy necessitates a multidisciplinary approach involving pediatric neurologists, physiotherapists, speech therapists, occupational therapists, and orthopedic surgeons, many of whom are concentrated in urban medical hubs.

In Greece, as per the Hellenic Society of Pediatrics in 2023 that nearly half of the country’s regional hospitals lack dedicated pediatric rehabilitation units, forcing patients to travel considerable distances for treatment. Similarly, in parts of Poland and Romania, rural communities face similar challenges due to underfunded local healthcare systems and limited recruitment incentives for specialists.

This uneven distribution of expertise and infrastructure hampers the delivery of timely, coordinated interventions and creates disparities in treatment quality across Europe, ultimately constraining the broader market’s growth potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2024 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Treatments, End-Users, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered

| (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | Abbott Laboratories (US), AbbVie Inc. (US), Acorda Therapeutics, Inc. (US), Allergan Plc (Ireland), AstraZeneca Plc (UK), Bayer AG (Germany), Biogen Inc. (US), Boston Scientific Corporation (US), Bristol-Myers Squibb Company (US), Eli Lilly and Company (US), GlaxoSmithKline Plc (UK), Ipsen (France), Johnson & Johnson (US), Medtronic Plc (Ireland), Merck & Co., Inc. (US), Merck KGaA (Germany), Novartis International AG (Switzerland), Pfizer Inc. (US), Roche Holding AG (Switzerland), Sanofi SA (France), Stryker Corporation (US) and Teva Pharmaceutical Industries Ltd. (Israel).. |

SEGMENTAL ANALYSIS

By Type Insights

Congenital cerebral palsy was the largest segment in the Europe Cerebral Palsy Market in 2024, accounting for 42.3% of total cases. This dominance is due to its high prevalence among diagnosed cases, as congenital CP accounts for the majority of all types, typically resulting from brain damage occurring before or during birth.

The early onset of this type necessitates long-term medical intervention, which significantly boosts demand for therapeutic, diagnostic, and assistive services.

In Germany, neonatal complications such as hypoxia, infections, and preterm birth remain leading causes of congenital CP.

In addition, public health initiatives aimed at improving maternal and neonatal care have led to better detection and documentation of congenital cases.

Hypotonic cerebral palsy is emerging as the fastest-growing segment in the Europe Cerebral Palsy Market, registering a CAGR of 7.2% over recent years. Although less common than other forms, its rising incidence and increased recognition are contributing to its accelerated growth trajectory.

Hypotonia, characterized by poor muscle tone and delayed motor development, often presents challenges in early diagnosis, but recent advancements in screening protocols have enabled earlier identification.

Also, new physiotherapeutic approaches tailored specifically for hypotonic patients have resulted in better patient outcomes, increasing treatment adoption.

Moreover, the Netherlands has seen a surge in referrals to multidisciplinary clinics specializing in rare CP subtypes, supported by national funding for rare disease research under the Horizon Europe framework. These developments are fueling both clinical engagement and market expansion for hypotonic cerebral palsy management across Europe.

By Treatments Insights

Therapy constitutes the prominent segment in the Europe Cerebral Palsy Market, holding a share of 35.1%. This includes physiotherapy, occupational therapy, speech therapy, and behavioral interventions, which form the cornerstone of long-term management for individuals with cerebral palsy. These therapies are often integrated into school-based programs and home care routines, ensuring sustained engagement throughout developmental years.

Additionally, in Denmark, where early intervention models are well-established. The country’s strong emphasis on inclusive education further reinforces the necessity of ongoing therapeutic support.

With growing evidence supporting the efficacy of early and continuous therapy, governments and private institutions across Europe are investing heavily in expanding therapeutic infrastructure, making it the most dominant treatment segment in the cerebral palsy market.

Imaging tests represented the fastest-growing segment in the Europe Cerebral Palsy Market, recording a CAGR of approximately 8.4% in recent years. This rapid growth is attributed to the increasing reliance on neuroimaging technologies such as MRI, CT scans, and ultrasound for early and precise diagnosis of cerebral palsy.

According to the European Society of Neuroradiology (ESNR), the use of brain imaging in neonatal intensive care units has risen since 2020, driven by technological advancements and the integration of AI-assisted diagnostics. Early imaging enables clinicians to detect structural brain abnormalities associated with CP, facilitating timely intervention.

Furthermore, as per the European Reference Network for Rare Neurological Diseases (ERN-RND), the number of cross-border referrals for advanced imaging diagnostics has surged by 22% in the last three years, reflecting growing collaboration and resource-sharing among EU nations. These developments underscore the critical role of imaging tests in shaping modern cerebral palsy management strategies, driving their rapid adoption across the region.

By End-Users Insights

Physiotherapy centers prevailed in the Europe Cerebral Palsy Market, capturing 28.3% of the total end-user base. These centers play a pivotal role in delivering structured, long-term physical rehabilitation programs tailored to the specific needs of individuals with cerebral palsy. These facilities are often equipped with state-of-the-art equipment and staffed by certified specialists who collaborate with families and schools to ensure holistic development. This widespread accessibility ensures continuity of care and enhances patient retention rates.

Similarly, in the UK, as per the Chartered Society of Physiotherapy (CSP), community-based physiotherapy clinics have expanded significantly, especially in London and Manchester, where waiting times for NHS services are longer. Private centers are increasingly filling the gap by offering flexible appointment schedules and personalized therapy plans.

The combination of institutional support, professional expertise, and patient-centric approaches positions physiotherapy centers as the leading end-user segment in the European cerebral palsy market.

Home care is the booming end-user segment in the Europe Cerebral Palsy Market, exhibiting a CAGR of 9.1% in recent years. This trend reflects a shift toward decentralized care models that emphasize convenience, cost-effectiveness, and family involvement in managing CP-related conditions.

Home care allows patients to receive physiotherapy, occupational therapy, and nursing assistance without the logistical burden of frequent hospital visits, particularly beneficial for rural populations.

Additionally, in Poland, where institutional healthcare resources are unevenly distributed, home care services have expanded rapidly, supported by non-governmental organizations and private insurers. According to the Polish Cerebral Palsy Foundation, nearly 30% of CP patients now receive some form of home-based rehabilitation, up from 18% in 2020.

This growing preference for home-based interventions is reshaping the delivery of cerebral palsy care, accelerating the expansion of the home care segment across Europe.

COUNTRY-WISE ANALYSIS

Germany Cerebral Palsy Market Insights

Germany secured the top position in the Europe Cerebral Palsy Market, commanding 18.1% of the regional market share. As Europe’s largest economy and a leader in healthcare innovation, Germany offers comprehensive diagnostic and therapeutic services for individuals with cerebral palsy. The country’s robust statutory health insurance system ensures broad coverage for essential treatments, including physiotherapy, orthopedic surgery, and assistive devices.

In addition, Germany is at the forefront of research into novel therapies, with institutions like the University Medical Center Göttingen conducting clinical trials on stem cell applications and neuromodulation techniques. The presence of world-class pediatric neurology departments and a well-established network of rehabilitation clinics further strengthens Germany’s leadership position in the European cerebral palsy landscape.

United Kingdom Cerebral Palsy Market Insights

The United Kingdom remains a significant player in the Europe Cerebral Palsy Market. The UK’s market status is shaped by its commitment to integrated healthcare models that combine early diagnosis, specialist treatment, and community-based support.

According to Public Health England, approximately 1 in 400 children in the UK is diagnosed with cerebral palsy annually, translating to roughly 1,800 new cases each year. The National Health Service (NHS) provides comprehensive care pathways, including access to physiotherapy, speech therapy, and surgical interventions.

The National Institute for Health and Care Excellence (NICE) has issued detailed guidelines emphasizing early detection and coordinated care planning. As per the UK Cerebral Palsy Register, adherence to these guidelines has improved early referral rates and treatment consistency across regions.

Also, charitable organizations such as Scope and Action Cerebral Palsy actively support research and advocacy efforts, enhancing awareness and policy development. With continued investment in digital health platforms and home-based care services, the UK remains a key contributor to the advancement of cerebral palsy treatment in Europe.

France Cerebral Palsy Market Insights

France occupied a prominent position in the Europe Cerebral Palsy Market. The country’s healthcare system places a strong emphasis on pediatric rehabilitation, ensuring that children with CP receive early and sustained therapeutic interventions. Moreover, France is home to several academic institutions conducting cutting-edge research on neuroplasticity and adaptive therapies. With a well-developed healthcare infrastructure and a focus on quality of life improvements, France continues to be a major player in the European cerebral palsy market.

Italy Cerebral Palsy Market Insights

Italy is positioning itself as a key growth market in Southern Europe. The country’s evolving healthcare landscape and increasing adoption of assistive technologies are driving demand for advanced CP management solutions.

The Italian National Health Service (SSN) covers a wide range of rehabilitative services, including speech therapy, occupational therapy, and orthopedic interventions.

In recent years, there has been a notable rise in the use of robotic-assisted therapy and AI-driven mobility aids, particularly in cities like Milan and Rome.

Moreover, the Italian Ministry of Health has introduced policies promoting inclusive education and workplace adaptation for individuals with disabilities, encouraging broader societal integration. With growing awareness and technological advancements, Italy is strengthening its role in the European cerebral palsy care ecosystem.

Sweden Cerebral Palsy Market Insights

Sweden plays a vital role in the Europe Cerebral Palsy Market. Known for its advanced healthcare system, Sweden excels in early diagnosis, neonatal care, and long-term rehabilitation for cerebral palsy patients. The country’s universal healthcare model ensures equitable access to diagnostic imaging, genetic screening, and neurodevelopmental assessments.

The Karolinska Institute and Uppsala University are actively engaged in cerebral palsy research, exploring biomarkers and regenerative medicine approaches. Furthermore, Sweden’s progressive disability policies promote inclusion and independent living, fostering a supportive environment for individuals with cerebral palsy. These factors contribute to Sweden’s strong market position and continued leadership in innovative CP care across Europe.

KEY MARKET PARTICIPANTS

Companies that play a notable role in the Europe cerebral palsy market include Abbott Laboratories (US), AbbVie Inc. (US), Acorda Therapeutics, Inc. (US), Allergan Plc (Ireland), AstraZeneca Plc (UK), Bayer AG (Germany), Biogen Inc. (US), Boston Scientific Corporation (US), Bristol-Myers Squibb Company (US), Eli Lilly and Company (US), GlaxoSmithKline Plc (UK), Ipsen (France), Johnson & Johnson (US), Medtronic Plc (Ireland), Merck & Co., Inc. (US), Merck KGaA (Germany), Novartis International AG (Switzerland), Pfizer Inc. (US), Roche Holding AG (Switzerland), Sanofi SA (France), Stryker Corporation (US) and Teva Pharmaceutical Industries Ltd. (Israel).

TOP LEADING PLAYERS IN THE MARKET

Medtronic PLC

Medtronic is a global leader in medical technology and plays a significant role in the Europe Cerebral Palsy Market by offering advanced therapeutic solutions, particularly in neuromodulation and orthopedic interventions. The company provides implantable devices such as baclofen pumps that help manage spasticity associated with cerebral palsy. Their focus on innovation, combined with strong partnerships with European healthcare providers, has enabled them to deliver life-changing technologies to patients across the region.

Abbott Laboratories

Abbott contributes to the Europe Cerebral Palsy Market through its nutritional and pharmaceutical offerings tailored for individuals with neurological conditions. The company develops specialized nutritional formulas that support growth and development in children with CP who face feeding difficulties. Abbott’s commitment to research and patient-centric care enhances its presence in the market, especially in rehabilitation centers and home care settings where long-term dietary support is essential.

Otto Bock HealthCare GmbH

Otto Bock is a leading provider of assistive technologies and mobility solutions for people with disabilities, including those affected by cerebral palsy. Based in Germany, the company designs and manufactures prosthetics, orthotics, and mobility aids that significantly improve the quality of life for CP patients. With a strong distribution network and continuous product innovation, Otto Bock plays a crucial role in enabling independence and accessibility for individuals with cerebral palsy across Europe.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by key players in the Europe Cerebral Palsy Market is product innovation and technological advancement. Companies are continuously developing new assistive devices, implantable therapies, and digital health tools to improve patient outcomes and enhance treatment efficacy. These innovations not only differentiate their offerings but also align with evolving clinical needs.

Another important strategy is strategic collaborations and partnerships with healthcare institutions, research organizations, and patient advocacy groups. By working closely with stakeholders, companies can better understand patient requirements, accelerate clinical trials, and ensure broader adoption of their products within the healthcare ecosystem.

Lastly, expanding access through personalized and home-based care solutions is gaining traction. Market participants are focusing on telehealth integration, remote monitoring, and customized rehabilitation programs to make therapies more accessible and convenient, particularly in rural and underserved regions across Europe.

COMPETITION OVERVIEW

The competition in the Europe Cerebral Palsy Market is characterized by a mix of established global healthcare companies and emerging regional players striving to expand their influence in this highly specialized sector. As awareness about early diagnosis and intervention grows, so does the demand for innovative therapies, assistive technologies, and comprehensive rehabilitation services. This has led to an increasingly dynamic market landscape where differentiation through product innovation, service delivery models, and patient engagement strategies is key.

Major players are leveraging their global expertise to introduce cutting-edge treatments and adaptive technologies tailored for European patients. Simultaneously, local firms are capitalizing on deep-rooted relationships with healthcare systems and regulatory bodies to offer cost-effective and culturally relevant solutions. The emphasis on multidisciplinary care and integrated treatment plans has further intensified competition, prompting companies to invest heavily in research, digital health platforms, and direct-to-consumer outreach initiatives.

Moreover, the growing influence of patient advocacy groups and increasing public funding for disability care are reshaping competitive dynamics. Companies that demonstrate a strong commitment to improving quality of life while maintaining compliance with stringent EU regulations are likely to maintain a strong foothold in this evolving market.

RECENT MARKET DEVELOPMENTS

- In February 2023, Medtronic launched a new line of programmable intrathecal baclofen pumps specifically designed for pediatric cerebral palsy patients in Germany, aiming to provide targeted muscle spasticity management.

- In July 2023, Abbott expanded its partnership with several European hospitals to supply specialized nutrition formulas for children with neurological disorders, including cerebral palsy, enhancing its presence in clinical nutrition.

- In November 2023, Otto Bock introduced a next-generation range of lightweight orthotic braces tailored for young cerebral palsy patients, focusing on mobility and comfort, with initial rollout in France and the Netherlands.

- In March 2024, a major Swedish biotech firm entered into a licensing agreement with a UK-based neurotech startup to co-develop wearable sensors that monitor motor function in cerebral palsy patients.

- In June 2024, a German-based digital health company partnered with a leading Dutch university hospital to pilot an AI-driven therapy tracking app for cerebral palsy patients undergoing physiotherapy at home.

MARKET SEGMENTATION

This research report on the Europe cerebral palsy market has been segmented and sub-segmented based on the following categories.

By Type

- Ataxia

- Spastic

- Dyskinetic

- Athetoid

- Postnatal

- Congenital

- Hemiparesis

- Hypotonic

- Diplegia

By Treatments

- Surgery

- Medication

- Therapy

- Diagnosis

- Laboratory Tests

- Imaging Tests

- Others

By Medical Devices

- Orthotic Devices

- ENT Devices

- Eye-tracking Devices

By End-users

- Physiotherapy Centers

- Hospitals

- Specialty Clinics

- Home Care

- Pathology Centers

- Ambulatory

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

What was the size of the cerebral palsy market in Europe in 2024?

The Europe cerebral palsy market was valued at USD 1.09 billion in 2024.

Which are the leading countries in the Europe cerebral palsy market?

The UK and Germany are playing a major role in the European market.

Who are the companies playing a key role in the Europe cerebral palsy market?

Abbott Laboratories (US), AbbVie Inc. (US), Acorda Therapeutics, Inc. (US), Allergan Plc (Ireland), AstraZeneca Plc (UK), Bayer AG (Germany), Biogen Inc. (US), Boston Scientific Corporation (US), Bristol-Myers Squibb Company (US), Eli Lilly and Company (US), GlaxoSmithKline Plc (UK), Ipsen (France), Johnson & Johnson (US), Medtronic Plc (Ireland), Merck & Co., Inc. (US), Merck KGaA (Germany), Novartis International AG (Switzerland), Pfizer Inc. (US), Roche Holding AG (Switzerland), Sanofi SA (France), Stryker Corporation (US) and Teva Pharmaceutical Industries Ltd. (Israel) are leading companies in the Europe cerebral palsy market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com