Europe Dental Floss Market Size, Share, Trends & Growth Forecast Report By Product, Sales Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) – Industry Analysis From 2026 to 2034

Market Size, 2025

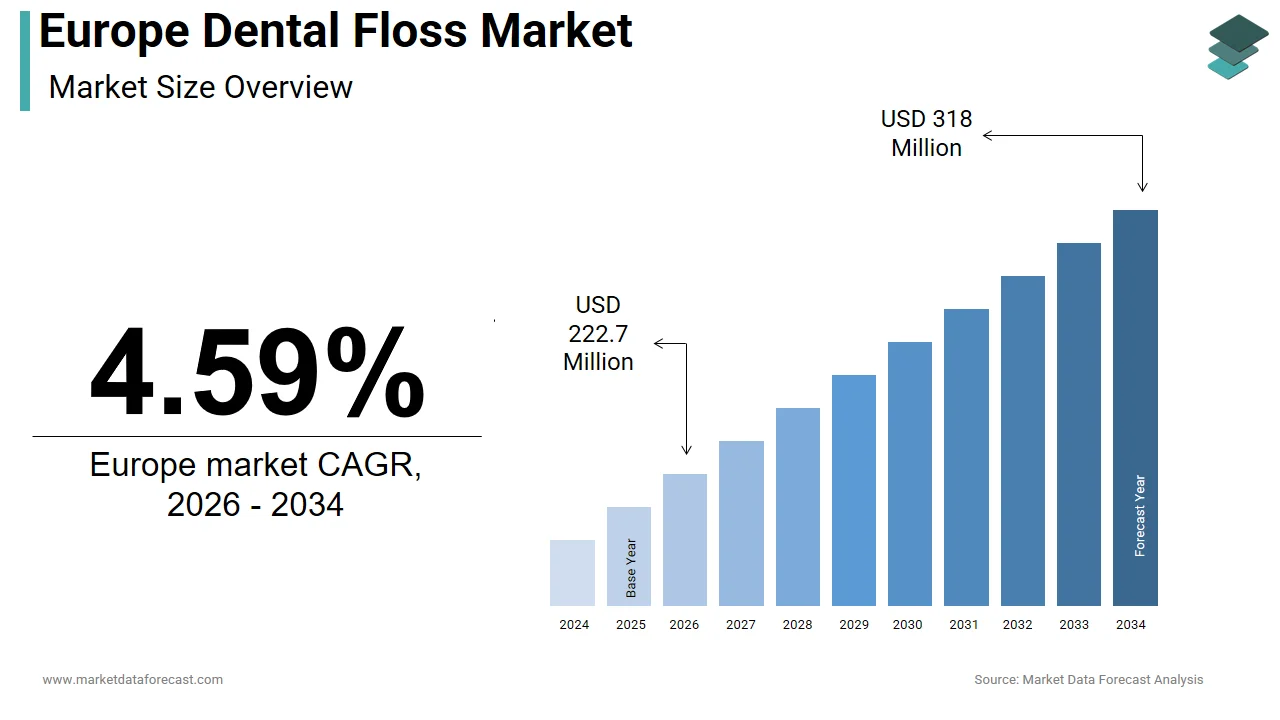

$212.32 MnMarket Estimate, 2026

$222.7 MnMarket Forecast, 2034

$318 MnCAGR, 2026–2034

4.59%Europe Dental Floss Market Report Summary

The Europe dental floss market was valued at USD 212.32 million in 2025, is estimated to reach USD 222.7 million in 2026, and is projected to reach USD 318 million by 2034, growing at a CAGR of 4.59% from 2026 to 2034. Market growth is driven by increasing awareness of oral hygiene, rising prevalence of periodontal diseases, and growing adoption of preventive dental care practices across Europe. Consumers are increasingly prioritizing daily interdental cleaning as part of comprehensive oral care routines. Expansion of premium and specialized floss products, including flavored, biodegradable, and orthodontic-friendly variants, is further supporting market growth.

Key Market Trends

- Rising awareness of preventive oral healthcare and gum disease management.

- Increasing demand for waxed and easy-glide dental floss variants.

- Growing popularity of eco-friendly and biodegradable floss products.

- Expansion of aesthetic dentistry and orthodontic treatments.

- Strengthening retail presence through pharmacies and supermarkets.

Segmental Insights

- Based on product, the waxed floss segment dominated the market in 2025 by holding 58.4% share, driven by its smoother glide, reduced shredding, and ease of use for consumers with tightly spaced teeth.

- Based on sales channel, the retail pharmacies segment led the market by capturing 49.1% share in 2025, supported by strong consumer trust, pharmacist recommendations, and wide product availability.

Regional Insights

The Europe dental floss market is witnessing steady growth across major economies, supported by preventive healthcare policies and increasing dental awareness campaigns.

- Germany led the regional market in 2025 with 22.6% share, driven by strong oral healthcare awareness and high consumer spending on personal care products.

- The United Kingdom followed with 17.8% share in 2025, supported by structured preventive dentistry programs and strong retail distribution networks.

- France maintains a significant position, supported by a blend of aesthetic dentistry culture and state-supported preventive oral healthcare initiatives.

Competitive Landscape

The Europe dental floss market is characterized by the presence of established oral care brands competing on product innovation, sustainability, and retail expansion. Market players are focusing on premium formulations, biodegradable materials, and orthodontic-friendly solutions to differentiate their offerings. Strategic marketing campaigns and expanded pharmacy partnerships are shaping competitive dynamics across the region.

Prominent companies operating in the Europe dental floss market include Procter & Gamble Co., Johnson & Johnson Services, Inc., Colgate-Palmolive Company, GlaxoSmithKline plc, Sunstar Group, and Dentek Oral Care, Inc..

Europe Dental Floss Market Size

The Europe dental floss market was valued at USD 212.32 million in 2025, is estimated to reach USD 222.7 million in 2026, and is projected to reach USD 318 million by 2034, growing at a CAGR of 4.59% from 2026 to 2034.

Dental floss refers to interdental cleaning devices designed to remove plaque and food debris from between teeth, where brushing alone is insufficient. Available in multifilament nylon, monofilament polytetrafluoroethylene (PTFE), and increasingly biodegradable formats such as silk or plant-based polymers, these products are categorized as medical devices under the European Union’s Medical Devices Regulation (MDR) 2017/745 when making preventive health claims. The market encompasses traditional string floss, floss picks, and water flosser-compatible refills, with growing emphasis on sustainability and user compliance. According to sources, a significant majority of the European adult population exhibits symptoms of gum inflammation, a condition that can typically be managed through regular cleaning between the teeth. Despite guidance from dental professionals, only a minority of adults in Germany maintain a consistent daily routine of cleaning between their teeth. As per research, Household spending on health-related goods and services has been increasing, suggesting that consumers are placing a higher priority on products that support their overall well-being. This evolving landscape, shaped by clinical evidence, regulatory classification, and shifting consumer habits, positions dental floss not merely as a hygiene tool but as a critical component of preventive healthcare across Europe.

MARKET DRIVERS

Growing Clinical Emphasis on Interdental Cleaning in Preventive Dentistry

European dental associations have intensified their advocacy for daily flossing as a non-negotiable element of oral hygiene, which in turn drives the growth of the Europe dental floss market. This shift is driven by robust epidemiological evidence linking interdental plaque to periodontal disease and systemic conditions like cardiovascular disorders. The European Federation of Periodontology’s top-tier clinical guidelines emphasize that standard toothbrushing cannot adequately clean all tooth surfaces, making the use of additional interdental tools essential for effective plaque management. National bodies have followed suit; the British Society of Periodontology now includes flossing instructions in all routine check-ups, while France’s Order of Dentists mandates interdental cleaning education during public school dental screenings. Research indicates that patients who receive direct, personalized instruction from dental professionals on how to clean between their teeth are significantly more consistent in maintaining their oral hygiene routines over time. This institutional push transforms floss from a discretionary purchase into a prescribed behavior, directly stimulating demand. Dental professionals increasingly dispense branded floss samples during visits, creating trusted entry points for consumers and reinforcing clinical legitimacy over retail marketing.

Rise of Eco-Conscious Consumerism and Demand for Sustainable Oral Care

European consumers are increasingly rejecting single-use plastics in personal care, which enables innovation in biodegradable and refillable dental floss formats, and thereby fuels the expansion of the Europe dental floss market. The EU’s Single-Use Plastics Directive has heightened scrutiny on conventional nylon floss spools and plastic floss picks, prompting brands to adopt compostable materials like silk, bamboo fiber, and polylactic acid (PLA). The Western European dental floss market is experiencing a significant shift toward sustainable packaging solutions, with an increasing number of new products adopting refill systems or certified compostable materials to meet environmental regulations. Countries like Sweden and Germany lead this shift. A substantial portion of young consumers in Germany shows a strong willingness to pay a premium for plastic-free dental floss, reflecting a growing demand for eco-friendly, zero-waste oral care products. Brands such as Georganics and Hydrophil have gained traction by offering glass dispensers with silk floss refills, aligning with zero-waste lifestyles. This environmental imperative, reinforced by municipal waste reduction policies and retailer sustainability pledges, is reshaping product design and creating new value propositions centered on planetary health alongside oral health.

MARKET RESTRAINTS

Persistent Low Compliance Rates Despite Clinical Recommendations

Daily flossing adherence remains stubbornly low across the region, despite decades of professional endorsement, which fundamentally limits the Europe dental floss market growth. The Fifth German Oral Health Study highlighted that while toothbrushing is common, regular interdental cleaning, such as flossing, is practiced by only a minority of adults in Germany, a trend that appears to be similarly low across other European nations like France and Italy. Behavioral research identifies key barriers: perceived complexity, time constraints, and discomfort, particularly among individuals with tight interdental spaces or orthodontic appliances. A 2024 investigation into dental behaviors indicated that physical discomfort, such as pain or floss getting stuck, remains a major barrier for adults who do not regularly floss. Unlike toothbrushing, which is habitualized early in life, flossing lacks cultural reinforcement and is often introduced too late. Public health campaigns have struggled to overcome this inertia; even in countries with universal dental coverage like Sweden, compliance plateaus below 40 percent. Mass adoption requires behavioral change, not just supply-side innovation, as the market is restricted by how people use products, not just how they are made.

Regulatory Ambiguity Around Biodegradability Claims and Material Standards

The surge in eco-friendly floss has exposed a lack of harmonized EU standards for biodegradability and compostability in oral care products, which leads to consumer confusion and greenwashing risks. This impedes the expansion of the Europe dental floss market. EU Ecolabel certification lacks specific criteria for dental floss, permitting brands to make unverified 'eco' or 'natural' claims. A European Commission analysis of online "green" claims found that a large portion of environmental assertions, including those for products marketed as biodegradable, were vague or lacked accessible, substantiated evidence. Furthermore, materials like PLA, marketed as compostable, require industrial facilities to break down, which are unavailable in most European municipalities. Studies indicate that PLA-based products, including floss, often fail to break down in home composting conditions, remaining largely intact over several months due to the absence of the high-temperature environment required for degradation. This regulatory gap erodes trust and complicates procurement for retailers like Ecover or dm-drogerie, which enforce strict sustainability criteria. The market for sustainable floss is hindered by poor labeling and unverified claims, pending the establishment of enforced standards.

MARKET OPPORTUNITIES

Integration with Digital Oral Health Platforms and Smart Devices

The convergence of connected health and preventive dentistry offers a significant opportunity for dental floss to evolve beyond a passive tool into an integrated component of digital wellness ecosystems, which is expected to boost the growth of the Europe dental floss market. Emerging smart toothbrushes from brands like Oral-B and Philips Sonicare now include app-based coaching that tracks brushing coverage and prompts interdental cleaning based on individual risk profiles. In addition, Oral-B launched a feature that syncs with floss usage logs via manual input, offering personalized feedback and reminders. Startups like Beam Brush are piloting AI-driven platforms that analyze intraoral scans to identify high-risk interdental zones and recommend specific floss types. Increased digital health adoption across Europe and a greater focus on preventative oral care are creating a receptive audience for integrated digital dental health solutions. Integrating smart flossing into digital oral care routines enables manufacturers to boost compliance, capture usage analytics, and establish subscription-based replenishment, evolving a staple product into a service-enabled health solution in line with Europe’s digital transformation.

Expansion into Medicated and Therapeutic Floss Variants

There is growing potential to develop dental floss infused with active pharmaceutical ingredients to address specific oral pathologies, which paves the way for potential prospects for the Europe dental floss market. This shifts the category from mechanical cleaning to targeted therapy. Chlorhexidine-coated floss, for instance, has demonstrated efficacy in reducing gingival inflammation in post-surgical patients. Similarly, floss impregnated with xylitol or fluoride offers sustained release to high-caries-risk sites, particularly beneficial for orthodontic patients. The European Medicines Agency permits such products under the medical device framework if they deliver localized effects without systemic absorption. Due to the high prevalence of periodontal disease among middle-aged and older European adults, professional guidelines increasingly advocate for the routine inclusion of interdental cleaning, such as therapeutic floss, as a key component of standard clinical oral health management. Partnerships between dental brands and pharmaceutical companies, such as Colgate’s collaboration with Sanofi on antimicrobial delivery systems, signal this shift. Utilizing dental floss for drug delivery opens up high-margin, clinically validated market segments that were previously held by gels and rinses.

MARKET CHALLENGES

Intensifying Competition from Alternative Interdental Cleaners

Mounting competitive pressure from alternative interdental devices, which offer greater ease of use and perceived efficacy, particularly among aging populations and orthodontic patients, is constraining the growth of the European dental floss market. Water flossers, for example, have gained significant traction. In Germany, a growing number of individuals starting interdental cleaning are choosing water flossers over traditional string floss, driven by increased user comfort and better accessibility for specialized needs. Interdental brushes, endorsed by the European Federation of Periodontology as first-line for patients with gum recession, now outsell floss in Nordic countries. Research indicates a growing adoption of interdental brushes in Sweden, while traditional floss consumption remains flat. These alternatives benefit from strong clinical backing, ergonomic advantages, and compatibility with dexterity limitations common in older adults, the fastest-growing demographic in Europe. Unless floss innovates in usability, through pre-threaded handles, softer textures, or guided systems, it risks further displacement in a market increasingly oriented toward user-friendly, evidence-backed tools.

Supply Chain Vulnerabilities in Specialty Polymer Sourcing

The production of high-performance dental floss relies on specialized polymers like PTFE and nylon 6/6, whose supply chains are susceptible to geopolitical and environmental disruptions, thereby inhibiting the expansion of the European dental floss market. PTFE, valued for its shred resistance and glide, is derived from fluorspar, a mineral heavily concentrated in China and Mexico. Stricter environmental regulations and ongoing regulatory evaluations of PFAS by European authorities are creating long-term uncertainty for the PTFE market, leading to increased price volatility. Similarly, nylon production is energy-intensive and tied to petrochemical markets, exposing manufacturers to oil price volatility. Biodegradable alternatives like PLA provide a solution, yet they are limited by their dependence on climate-sensitive crops. Severe drought conditions in parts of Europe during 2024 constrained corn supplies, contributing to higher raw material costs and reduced availability in the region. These dependencies constrain cost predictability and force reformulations that may compromise performance. The market's exposure to shocks that jeopardize product consistency and affordability will persist unless investments are made in circular material systems and regional bio-polymer production.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Sales Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Procter & Gamble Co., Johnson & Johnson Services, Inc., Colgate-Palmolive Company, GlaxoSmithKline plc, Sunstar Group, and Dentek Oral Care, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The waxed floss segment secured the majority share of 58.4% of the Europe dental floss market in 2025. The supremacy of the waxed floss segment is attributed to superior user experience, particularly ease of insertion between tight interdental spaces, and reduced fraying during use compared to unwaxed alternatives. The wax coating, typically derived from natural carnauba or synthetic polymers, enhances glide without compromising cleaning efficacy, making it the preferred choice for first-time users and those with crowded dentition. Many dental professionals in Europe often recommend waxed dental floss to patients during initial education because its coating allows for easier maneuvering between teeth, which can improve patient compliance. In countries like Italy and Spain, where orthodontic treatment is prevalent among adolescents, waxed floss is often bundled with braces kits to prevent plaque accumulation around brackets. Additionally, major brands such as Oral-B and Colgate have optimized their flagship floss lines around waxed variants, ensuring wide retail availability and consistent consumer familiarity. This combination of clinical endorsement, functional advantage, and market entrenchment solidifies waxed floss as the cornerstone of daily interdental care across Europe.

The other products segment is likely to experience the fastest CAGR of 8.6% from 2026 to 2034 due to demand for convenience, sustainability, and compatibility with modern lifestyles. Floss picks, in particular, appeal to on-the-go users and caregivers assisting children or elderly relatives. A rising number of young adults in Germany are adopting floss picks as their primary interdental cleaning method, driven by the convenience and portability of the products. Simultaneously, eco-conscious consumers are adopting refillable silk floss systems with compostable packaging, especially in Nordic countries. Following tighter regulations on single-use items in Sweden, there is a significant, accelerated shift in consumer demand toward sustainable, plastic-free interdental products. Furthermore, the rise of smart oral care ecosystems has spurred demand for specialized refills compatible with connected water flossers. This diversification beyond traditional string formats reflects a broader shift toward user-centric, environmentally responsible, and technologically integrated oral hygiene solutions.

By Sales Channel Insights

The retail pharmacies segment dominated the Europe Dental Floss Market by holding a 49.1% share in 2025. The dominance of the retail pharmacies segment is credited to high foot traffic, trusted health-focused environments, and strategic product placement alongside toothbrushes and toothpaste. Chains like Boots in the UK, dm-drogerie in Germany, and parapharmacies in France curate oral care sections that emphasize professional-grade products, fostering consumer confidence in quality and efficacy. According to sources, a significant share of EU households visit a pharmacy at least once a month, providing unmatched exposure for essential hygiene items. Pharmacists often serve as informal health advisors; in countries like Italy and Spain, they routinely recommend specific floss types based on patient needs, reinforcing clinical credibility. Additionally, retail pharmacies offer immediate purchase without delivery delays, catering to impulse buys and replenishment cycles. This blend of accessibility, authority, and convenience ensures that brick-and-mortar pharmacies remain the primary gateway for mainstream floss adoption across Europe.

The online pharmacies segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 11.2% over the forecast period, owing to digital health adoption, subscription models, and the ability to access niche or premium floss variants not available in physical stores. Platforms like Apotheka in Sweden and DocMorris in Germany offer curated oral care bundles with auto-replenishment, reducing purchase friction and ensuring consistent usage. European consumers are increasingly adopting digital channels to purchase personal health, wellness, and oral hygiene products, with online platforms becoming a primary, convenient alternative to traditional retail. Online pharmacies also provide detailed ingredient transparency and customer reviews, critical for eco-conscious buyers evaluating biodegradability claims. Moreover, tele-dentistry integrations allow virtual consultations to result in direct floss prescriptions delivered to the doorstep. Online pharmacies are making interdental care more accessible and personal, using faster urban delivery and improved logistics to build stronger consumer trust.

COUNTRY-LEVEL ANALYSIS

Germany Dental Floss Market Analysis

Germany led the Europe Dental Floss Market by accounting for a 22.6% share in 2025. The leading position of the German market is attributed to its robust healthcare infrastructure, high oral health literacy, and strong regulatory environment. The country mandates regular dental check-ups under statutory health insurance, creating consistent touchpoints for professional floss recommendations. According to a study, a significant share of adults receive personalized interdental cleaning advice during annual visits, driving habitual use. Retail chains like dm-drogerie and Rossmann dedicate extensive shelf space to premium and eco-friendly floss, reflecting consumer demand for quality and sustainability. Additionally, Germany’s engineering culture extends to oral care, with high adoption of advanced tools like water flossers whose refills contribute to market growth. This ecosystem of preventive healthcare, retail sophistication, and technical affinity positions Germany as the continent’s most mature and influential dental floss market.

United Kingdom Dental Floss Market Analysis

The United Kingdom followed closely in the Europe dental floss market by capturing a 17.8% share in 2025. The expansion of the UK market is fuelled by its National Health Service–linked preventive dentistry programs and strong e-commerce penetration. NHS guidelines explicitly recommend daily flossing, and dental hygienists routinely demonstrate techniques during free check-ups for children and seniors. The UK government, through OHID and partnerships with dental care providers, is delivering millions of toothbrushing packs to young children in underserved areas of England to promote daily oral hygiene and prevent decay. Simultaneously, online channels thrive. Retailers like Boots and Amazon UK are experiencing increased demand for personal dental hygiene products, with consumers turning to subscription models to maintain regular, direct-to-door deliveries of oral care items. The UK also leads in sustainable innovation, with London-based startups like Georganics pioneering refillable glass floss dispensers. This dual engine of public health policy and digital commerce creates a dynamic market where awareness translates directly into consistent household consumption.

France Dental Floss Market Analysis

France occupies a major share of the European market due to a unique blend of aesthetic dentistry culture and state-supported preventive care. The French national dental screening program, M’T Dents, provides free check-ups at ages 6, 9, 12, and 15, during which interdental hygiene is emphasized. The French national health system is strengthening preventative dental care for younger populations by increasing access to free check-ups and enhancing public health initiatives focused on hygiene and oral health. Parapharmacies, specialized beauty-health retailers like Marionnaud and Pharma GDD, dominate distribution, offering premium floss alongside cosmetic dental products, aligning oral care with personal grooming. French consumers favor flavored and waxed variants, with mint and cinnamon being top sellers. This integration of dental hygiene into broader self-care rituals, supported by institutional outreach, sustains steady demand across age groups.

Sweden Dental Floss Market Analysis

Sweden is a lucrative region in the Europe dental floss market and is emerging as a leader in sustainable and preventive oral care. The country’s publicly funded dental system includes free check-ups until age 23 and subsidized cleanings for adults, fostering lifelong flossing habits. According to sources, a significant portion of young adults report daily interdental cleaning, the highest rate in Europe. Eco-consciousness further shapes the market. Retailers like Matas and Apoteket prioritize certified compostable floss, and municipal waste policies discourage single-use plastics. Startups such as Hydrophil have gained national traction with bamboo-based floss in recyclable packaging. This alignment of universal healthcare access, environmental policy, and consumer ethics makes Sweden a bellwether for future market evolution toward green, habitual interdental care.

Italy Dental Floss Market Analysis

Italy is anticipated to expand in the Europe Dental Floss Market during the forecast period owing to high orthodontic prevalence and family-oriented oral hygiene practices. A portion of Italian adolescents undergo braces treatment, creating sustained demand for shred-resistant waxed floss and floss threaders. Family pharmacies (farmacie) play a central role, with pharmacists often advising multi-generational households on oral care routines. Additionally, Italy’s strong regional food culture, rich in fibrous vegetables and aged cheeses, increases awareness of interdental debris, prompting proactive cleaning. Brands like Curaprox have succeeded by offering ultra-thin floss tailored to Mediterranean dental anatomy. This confluence of clinical need, familial health guidance, and dietary habits sustains consistent, culturally embedded floss usage across the Italian population.

COMPETITIVE LANDSCAPE

Competition in the Europe Dental Floss Market is characterized by a three-tier structure comprising global consumer health giants, specialized oral care innovators, and private-label retailers. Differentiation hinges not on price alone but on material science, sustainability credentials, and integration with broader oral health routines. Established brands like Oral-B and Colgate compete through clinical validation, retail scale, and digital ecosystem integration, while niche players such as Sunstar and Georganics focus on ergonomic design and eco-innovation to capture premium segments. Regulatory pressures under the EU Medical Devices Regulation and Single-Use Plastics Directive have raised compliance barriers, favoring companies with robust R&D and supply chain transparency. Meanwhile, supermarket own-brands offer basic floss at lower prices, compressing margins in the value segment. Ultimately, success depends on balancing performance, environmental responsibility, and behavioral science to overcome persistent low compliance rates and convert clinical recommendations into habitual use across diverse European consumer landscapes.

KEY MARKET PLAYERS

The leading companies operating in the Europe dental floss market include:

- Procter & Gamble Co.

- Johnson & Johnson Services, Inc.

- Colgate-Palmolive Company

- GlaxoSmithKline plc

- Sunstar Group

- Dentek Oral Care, Inc.

TOP PLAYERS IN THE MARKET

- Procter & Gamble, through its Oral-B brand, maintains a strong presence in the Europe Dental Floss Market with a portfolio that includes Glide floss and integrated interdental solutions. The company leverages its global R&D capabilities to develop high-performance PTFE-based floss known for shred resistance and smooth glide, particularly valued in markets with high orthodontic usage. In recent years, P&G has reinforced its European position by aligning product innovation with sustainability goals, introducing recyclable packaging, and reducing plastic content in floss dispensers. It has also deepened integration with its smart toothbrush ecosystem, offering bundled recommendations via the Oral-B app to encourage consistent interdental care. These initiatives reflect a strategic shift from standalone products to holistic oral health systems, enhancing consumer engagement and loyalty across the continent.

- Colgate-Palmolive plays a pivotal role in the Europe Dental Floss Market through its Total and Dental Floss lines, which emphasize clinical efficacy and accessibility. The company partners extensively with dental professionals and national health programs to promote interdental hygiene as part of preventive care. Recently, Colgate has expanded its eco-friendly offerings in Europe, launching plant-based waxed floss in compostable cardboard packaging across Germany, France, and the UK. It also enhanced flavor profiles using natural mint oils to improve the sensory experience without artificial additives. Colgate boosts its image as a trusted, health-focused brand by combining scientific innovation with EU clean-label trends, effectively connecting everyday consumers with professional recommendations.

- Sunstar Group, a Swiss-Japanese oral care innovator, holds a distinctive position in the Europe Dental Floss Market through its GUM brand, renowned for specialized interdental products. Sunstar focuses on precision engineering, offering ultra-thin floss, floss threaders, and biodegradable variants tailored for sensitive gums and tight spaces. The company has intensified its European footprint by collaborating with dental hygienist associations in Sweden and the Netherlands to co-develop educational materials on proper flossing technique. Sunstar’s commitment to clinical collaboration, ergonomic design, and sustainable innovation allows it to command premium positioning while addressing unmet needs in therapeutic and eco-conscious segments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Dental Floss Market are reformulating products to eliminate synthetic waxes and incorporate plant-based or biodegradable materials in response to EU sustainability mandates. They are integrating floss into connected oral care ecosystems by linking usage recommendations to smart toothbrush apps and tele-dentistry platforms. Companies are partnering with national dental associations to embed floss education into public health programs and school screenings. Strategic investments in refillable and plastic-free packaging systems are being made to appeal to zero-waste consumers in Northern and Western Europe. Additionally, firms are expanding flavor and texture variants using natural ingredients to enhance sensory acceptance and reduce user discomfort during daily use.

MARKET SEGMENTATION

This research report on the Europe dental floss market has been segmented and sub-segmented into the following categories.

By Product

- Waxed floss

- Un-waxed floss

- Other Products

By Sales Channel

- Retail Pharmacies

- Online Pharmacies

- Other Sales Channels

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe dental floss market?

The Europe dental floss market offers interdental cleaning products preventing plaque and gum disease across retail channels.

Why is the Europe dental floss market growing?

The Europe dental floss market expands through oral hygiene awareness and eco-friendly product innovations.

What types dominate the Europe dental floss market?

Waxed, unwaxed, and floss picks lead the Europe dental floss market for consumer convenience and effectiveness.

Who leads the Europe dental floss market?

Procter & Gamble, Colgate-Palmolive, and Johnson & Johnson drive the Europe dental floss market innovations.

What trends shape the Europe dental floss market?

Trends feature biodegradable floss in the Europe dental floss market sustainable oral care demands.

How does waxed floss benefit users in the Europe dental floss market?

Waxed floss glides smoothly between teeth in the Europe dental floss market reducing shredding issues.

What role do floss picks play in the Europe dental floss market?

Floss picks offer convenience for on-the-go use in the Europe dental floss market travel segments.

Which countries lead the Europe dental floss market?

Germany and UK dominate the Europe dental floss market advanced dental care infrastructures.

What materials compose floss in the Europe dental floss market?

Nylon, PTFE, and silk materials prevail in the Europe dental floss market diverse product offerings.

How does floss prevent gum disease in the Europe dental floss market?

Floss removes interdental plaque crucial for gingivitis prevention in the Europe dental floss market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com