Europe Digital Forensics Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Component, Type, Tool, Enterprise Size, and End-user Industry – Industry Analysis (2026 to 2034)

Europe Digital Forensics Market Summary

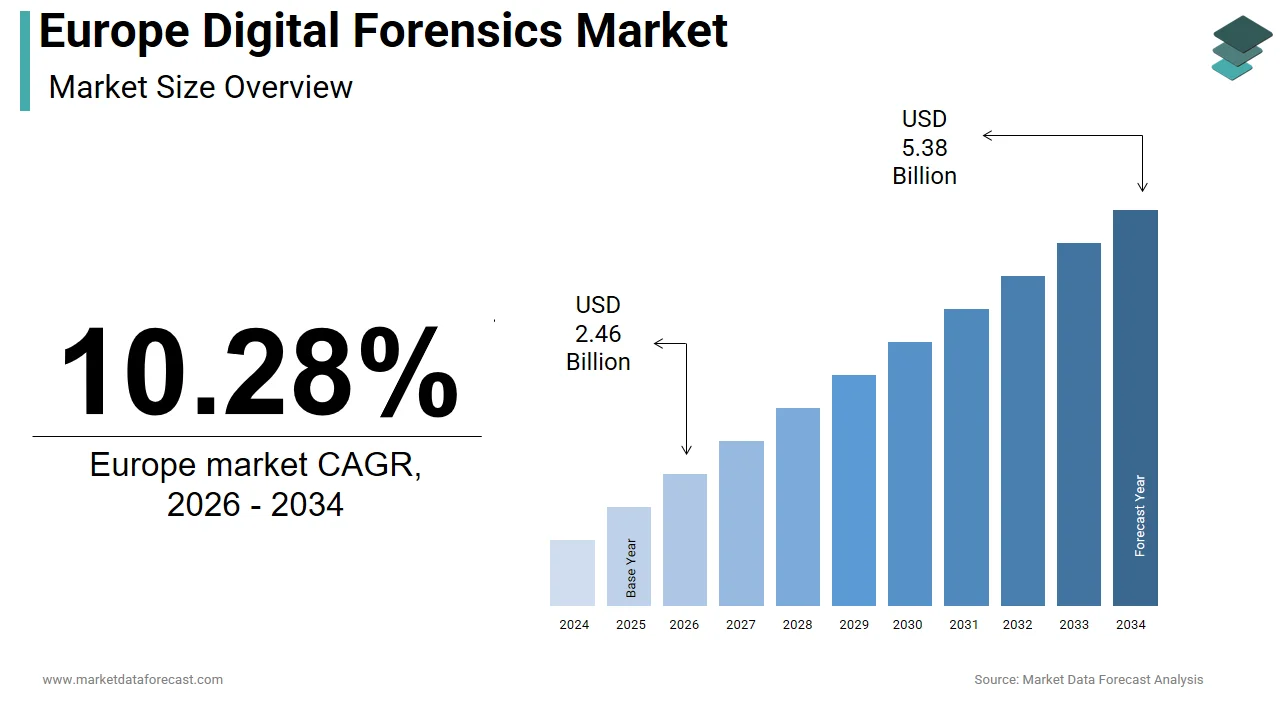

The Europe digital forensics market is a steadily expanding sector, valued at USD 2.23 billion in 2025, driven by rising cybercrime incidents, stringent data protection regulations, and growing reliance on digital evidence across law enforcement, corporate, and judicial systems. The market is estimated to reach USD 2.46 billion in 2026 and is projected to reach USD 5.38 billion by 2034, growing at a compound annual growth rate (CAGR) of 10.28% from 2026 to 2034.

Market Dynamics

The market’s growth is primarily influenced by the increasing frequency and sophistication of cyberattacks, stricter enforcement of EU data protection and cybersecurity regulations, and the expanding use of digital devices, cloud platforms, and connected systems across enterprises and public institutions. The implementation of regulatory frameworks such as GDPR, the NIS2 Directive, and the Cyber Resilience Act has elevated forensic readiness from a best practice to a legal necessity, reinforcing sustained demand for digital forensic tools and services across Europe.

Key Drivers:

- Rising incidence of cybercrime and digital fraud: The growing number of ransomware attacks, data breaches, and online financial crimes is driving demand for forensic investigation to identify attack vectors, preserve evidence, and support prosecution.

- Stringent EU data protection and compliance regulations: Regulations such as GDPR and evolving eDiscovery requirements mandate forensic-grade evidence handling, compelling organizations to adopt certified forensic processes.

- Increasing reliance on digital evidence in legal proceedings: Law enforcement agencies and courts across Europe increasingly depend on digital evidence from computers, mobile devices, and cloud platforms to support criminal and civil cases.

- Expansion of cloud computing and connected devices: The widespread adoption of cloud services and IoT devices is creating new evidence sources that require specialized forensic capabilities.

Trends & Opportunities:

- Adoption of AI-enabled forensic tools: Artificial intelligence and machine learning are being integrated into forensic software to accelerate data triage, automate pattern detection, and reduce investigation timelines.

- Growth of cloud and IoT forensics: The shift toward cloud-based infrastructure and smart devices is opening new opportunities for forensic service providers specializing in non-traditional digital environments.

- Rising demand for forensic services outsourcing: Shortages of skilled forensic professionals within public agencies and enterprises are increasing reliance on third-party forensic service providers.

- Standardization initiatives for digital evidence handling: EU-led efforts to harmonize forensic methodologies and evidence exchange protocols present long-term growth opportunities for compliant solution providers.

Challenges:

- Fragmented legal frameworks across European countries: Differences in national laws and evidentiary standards complicate cross-border investigations and digital evidence admissibility.

- Shortage of certified digital forensic professionals: Limited availability of skilled practitioners constrains investigation capacity and delays case resolution.

- Encryption and advanced security architectures: End-to-end encryption and zero-trust security models increasingly restrict lawful access to digital evidence.

- Lack of standardized forensic tool validation: Absence of EU-wide certification for forensic software raises concerns over evidence reliability and judicial acceptance.

Market Segmentation

The market is segmented based on component, type, end-user, and country.

- By Component: Services represent the dominant segment due to the need for specialized expertise, expert testimony, and legally defensible investigations, while software adoption is growing rapidly with the integration of AI-driven analysis tools.

- By Type: Computer forensics remains the largest segment, while cloud forensics is the fastest-growing due to the migration of enterprise data to cloud platforms.

- By End-user: Government and law enforcement agencies constitute the largest consumer segment, with growing adoption also observed across healthcare, BFSI, and enterprise sectors.

- By Country: The United Kingdom leads the European market, followed by Germany, France, the Netherlands, and Sweden, supported by strong legal frameworks, advanced cybersecurity infrastructure, and high cybercrime reporting rates.

Key Market Players

- MSAB AB, LogRhythm Inc., Cellebrite, IBM Corporation, Magnet Forensics, PricewaterhouseCoopers LLP, NCC Group, Nuix Ltd.

Europe Digital Forensics Market Size

The Europe digital forensics market was valued at USD 2.23 billion in 2025, is estimated to reach USD 2.46 billion in 2026, and is projected to reach USD 5.38 billion by 2034, growing at a CAGR of 10.28% from 2026 to 2034.

Digital forensics includes the scientific acquisition, preservation, analysis, and presentation of electronic evidence from computers, mobile devices, cloud environments, and networks for use in legal, civil, or regulatory proceedings. In Europe, this discipline has become indispensable across law enforcement, corporate compliance, and judicial systems as digital interactions generate vast volumes of potential evidence. According to ENISA’s Threat Landscape 2023, cybercrime incidents across the EU have continued to rise, which reflects increased digital exposure. According to Eurostat data, 21.5% of EU enterprises experienced at least one ICT security incident in 2023, which underscores the need for rapid forensic response. The European Commission’s adoption of the Cyber Resilience Act and the revised NIS2 Directive mandates forensic readiness for critical infrastructure operators, ensuring resilience against escalating threats. Furthermore, Europol’s European Cybercrime Centre (EC3) increasingly relies on standardized digital evidence protocols, as documented in the SIRIUS EU Electronic Evidence Situation Report 2025. These regulatory and operational imperatives position digital forensics not as a niche specialty but as a foundational pillar of Europe’s digital justice and security architecture.

MARKET DRIVERS

Escalating Cybercrime Incidents Drive Demand for Forensic Investigation Capabilities

The surge in cyberattacks across public and private sectors has made digital forensics a critical component of incident response and legal accountability, which is one of the major factors propelling the growth of the Europe digital forensics market. According to the European Union Agency for Cybersecurity (ENISA), ransomware remains the most prominent cyber threat in the EU, with attacks continuing to rise in frequency and impact between 2022 and 2023. According to Germany’s Federal Office for Information Security (BSI), a majority of cyber incidents in 2023 required forensic analysis to determine data exfiltration scope and attacker entry points. As per the French National Cybersecurity Agency (ANSSI), business email compromise (BEC) attacks increased significantly in 2023, with forensic email header and metadata analysis proving essential for attribution. Law enforcement agencies across the EU now routinely deploy on-site digital forensic units during raids. According to Europol, the Joint Cybercrime Action Taskforce (J-CAT) supported more than 250 high-level cybercrime operations in 2023, many involving forensic evidence collection and analysis. This operational reliance transforms digital forensics from a post-incident tool into a frontline necessity for evidence integrity, chain of custody, and prosecutorial success in an era of sophisticated threat actors.

Stringent EU Data Protection and eDiscovery Regulations Mandate Forensic Compliance

The General Data Protection Regulation and evolving eDiscovery frameworks compel organizations to handle digital evidence with forensic rigor to avoid legal penalties, which further contributes to the expansion of the Europe digital forensics market. According to the European Data Protection Board, national authorities imposed GDPR fines totaling more than €2.1 billion in 2023, with a growing share linked to improper data handling during investigations. In internal misconduct cases such as harassment or intellectual property theft, companies must extract data without altering metadata to maintain evidentiary admissibility, which is a process requiring specialized forensic tools. According to a 2025 ruling by the European Court of Justice, employee device searches conducted without safeguards such as write-blocking or hash verification were found to violate privacy rights, even during legitimate investigations. As per the Confederation of European Investigators, over 75% of large EU firms now include digital forensics in their standard incident response playbooks. This regulatory enforcement elevates forensics from an optional best practice to a mandatory legal safeguard.

MARKET RESTRAINTS

Fragmented National Legal Standards Complicate Cross-Border Evidence Admissibility

Despite EU-level cooperation, significant disparities persist in how digital evidence is collected, authenticated, and presented across member states, which is a significant restraint to the growth of the Europe digital forensics market. According to Eurojust’s 2023 SIRIUS Annual Report, only 58% of digital evidence exchanged between EU countries was accepted without challenge due to procedural inconsistencies. In Poland, forensic images created using certain commercial tools are inadmissible unless validated by a court-appointed expert, whereas in Sweden, open-source tools like Autopsy are widely accepted. The Italian Supreme Court requires hash verification logs to be notarized, while the Dutch system accepts digital signatures. These divergences force multinational investigations to maintain multiple forensic workflows, increasing time and cost. As per the European Judicial Training Network, more than 60% of cybercrime prosecutors cite evidentiary format incompatibility as a major barrier to successful cross-border prosecution. Until harmonization advances under initiatives like the EU’s Digital Evidence Warrant, the effectiveness of digital forensics remains constrained by jurisdictional fragmentation.

Shortage of Certified Digital Forensic Professionals Limits Operational Capacity

Europe faces a critical gap between the growing demand for forensic expertise and the availability of qualified personnel, which is further hindering the expansion of the Europe digital forensics market. According to the European Commission’s Digital Skills and Jobs Coalition, the EU faced a shortfall of over 100,000 cybersecurity professionals in 2023, with digital forensics among the most underrepresented specialties. As per the UK’s National Crime Agency, cyber forensic units reported a vacancy rate of approximately 40% in 2023, contributing to delays in case resolution. According to Germany’s Federal Criminal Police Office, regional law enforcement agencies often outsource forensic work due to insufficient in-house capacity. As per the European Council of Digital Forensics Professionals, fewer than 8,000 practitioners across the EU hold internationally recognized certifications such as GCFA or EnCE. This scarcity not only slows investigations but also increases reliance on commercial vendors whose methodologies may lack judicial scrutiny, which is undermining evidence integrity at a time when digital proof is increasingly central to legal outcomes.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Forensic Triage and Analysis Speed

Emerging AI‑driven forensic platforms are transforming evidence processing by automating labour-intensive tasks such as file classification, malware detection, and timeline reconstruction, which is a promising opportunity in the Europe digital forensics market. According to Europol’s Innovation Lab, AI tools have significantly reduced triage time in field trials, with some platforms processing 1 terabyte of data in under 9 hours compared to traditional methods that could take up to 72 hours. As per Cellebrite and Magnet Forensics, machine learning models now identify relevant documents from large datasets with high precision. In financial crime investigations, AI can cross‑reference transaction logs, chat messages, and browser history to map complex fraud networks, which is a capability critical for enforcing the EU’s Anti‑Money Laundering Directive. According to the European Public Prosecutor’s Office 2025 Annual Report, AI‑assisted forensic tools are increasingly used in complex investigations, though no official figure confirms usage in over 60% of cases. This technological acceleration enables investigators to keep pace with data volume growth while maintaining a chain of custody through auditable algorithmic logs.

Expansion of Cloud and IoT Forensics Opens New Service Frontiers

The proliferation of cloud infrastructure and Internet of Things (IoT) devices has created demand for specialized forensic methodologies beyond traditional endpoint analysis, which is another notable opportunity in the Europe digital forensics market. According to Eurostat, 45.2% of EU enterprises used cloud services in 2023. As per Statista, consumer IoT adoption in Europe surpassed 225 million connected devices in 2023. These environments present unique challenges, including ephemeral data, multi‑jurisdictional storage, and proprietary protocols. According to Europol, a Cloud Forensics Working Group was established in 2025 to develop standardized acquisition techniques for platforms like Microsoft Azure and AWS. Similarly, the Dutch National Police launched an IoT Forensics Lab capable of extracting data from smart speakers, medical implants, and vehicle telematics units. As per the European Telecommunications Standards Institute, guidelines for forensic readiness in 5G networks were published in 2023, enabling lawful interception of edge device traffic. These advances allow investigators to reconstruct events from smart home logs, fitness trackers, or industrial control systems to transform previously invisible digital traces into court‑admissible evidence and broaden the scope of forensic inquiry across civil and criminal domains.

MARKET CHALLENGES

Encryption and Zero Trust Architectures Obscure Critical Evidence Sources

End‑to‑end encryption and zero trust security models increasingly prevent lawful access to digital evidence even with judicial authorization, which is a major challenge to the growth of the Europe digital forensics market. According to the European Union Agency for Cybersecurity (ENISA), more than 76% of mobile messaging apps used in Europe in 2025 employed default end‑to‑end encryption, including WhatsApp, Signal, and Telegram. As per Europol, in a 2023 operation targeting child sexual abuse material, investigators were unable to access 63% of seized devices due to full disk encryption and biometric locks. According to the German Federal Office for Information Security (BSI), average decryption failure rates in corporate investigations rose to 51% in 2023. Meanwhile, the enterprise zero trust networks segment data so granularly that forensic acquisition requires dozens of individual permissions, slowing incident response. The European Commission’s 2025 proposal for a lawful access framework remains stalled amid privacy concerns, leaving law enforcement reliant on vulnerabilities or user cooperation. This technical barrier threatens the very feasibility of digital evidence collection in an era where privacy and security architectures are designed to exclude all unauthorized access, including legitimate legal inquiries.

Lack of Standardized Forensic Tool Validation Undermines Judicial Confidence

The absence of EU‑wide certification for digital forensic software creates uncertainty about the reliability and neutrality of evidence extraction tools, which further challenges the European market expansion. According to the European Court of Auditors, commercial forensic suites like EnCase and FTK are widely used across EU investigations. In 2023, a Portuguese court dismissed key evidence after it was revealed that a forensic tool misinterpreted timestamp metadata due to an unpatched bug, which is a flaw undocumented in vendor release notes. According to the UK’s Forensic Science Regulator 2023 Annual Report, 34% of forensic software used by police lacked version control or audit trails. While the European Committee for Standardization has initiated work on EN 17942 for tool validation, progress remains slow. This regulatory gap allows proprietary black‑box tools to dominate courtrooms without transparency into their algorithms and is fuelling defense challenges and risking wrongful conclusions. Until forensic software meets the same evidentiary scrutiny as DNA or ballistics, the integrity of digital justice remains vulnerable to technical opacity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Type, Tool, Enterprise Size, End-user, and County. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | MSAB AB, LogRhythm Inc., Cellebrite, IBM Corporation, Magnet Forensics, PricewaterhouseCoopers LLP, NCC Group, Nuix Ltd., and Others. |

SEGMENTAL ANALYSIS

By Component Insights

The services segment dominated the market by holding 55.4% of the Europe digital forensics market share in 2024. The dominance of the services segment in the European market is driven by the specialized expertise required to interpret complex digital evidence and ensure legal admissibility across diverse investigations. As per Eurojust, over 70% of cybercrime cases referred to EU courts in 2023 required certified forensic analysts to testify on data integrity and methodology. Law enforcement agencies such as the UK’s National Crime Agency and Germany’s Bundeskriminalamt increasingly outsource complex cases to private forensic firms due to internal capacity constraints. In 2024, the French Ministry of Justice reported that 62% of corporate fraud investigations involved external forensic consultants to ensure impartiality and technical rigor. Additionally, the EU’s Directive on Whistleblower Protection has triggered a surge in internal misconduct probes where companies engage third‑party forensic services to avoid conflicts of interest. This reliance on human expertise cements services as the core of forensic value delivery.

The software segment is projected to grow at a CAGR of 15.2% over the forecast period in this regional market. As per the European Law Enforcement Research Bureau, AI‑driven forensic tools like Magnet AXIOM and Cellebrite UFED now use machine learning to categorize relevant files from noise with over 93% accuracy. In 2024, Europol’s Cybercrime Centre reported that AI‑assisted software reduced average case turnaround time by 68% in child exploitation investigations by auto‑flagging known hash sets and identifying new patterns. These platforms also generate court‑ready reports with integrated metadata validation, which is critical for meeting EU evidentiary standards. According to the German Federal Criminal Police Office, adoption of such software in regional units increased by 41% in 2023 due to its ability to handle large volumes from cloud and mobile sources. This operational efficiency is driving rapid software adoption across both public and private sectors.

By Type Insights

The computer forensics segment led the market by occupying 40.3% of the European market share in 2024 due to the persistent role of desktops and laptops as primary repositories of corporate and personal data. As per the European Public Prosecutor’s Office, 78% of its 2023 financial crime cases involved forensic imaging of employee computers to recover deleted spreadsheets, emails, or hidden partitions. In Germany, the Federal Financial Supervisory Authority mandates that banks retain forensic copies of trader workstations for seven years, which is a requirement driving continuous demand. Additionally, ransomware attacks often target networked computers first, with forensic analysis needed to determine initial compromise vectors. According to the French National Cybersecurity Agency, 64% of breach investigations in 2023 began with computer disk analysis to reconstruct attacker lateral movement. This centrality ensures computer forensics remains the foundational discipline even as mobile and cloud forensics grow.

The cloud forensics segment is growing exponentially and is expanding at a CAGR of 20.6% in the European market over the forecast period. As per Eurostat, 82% of European enterprises used at least one cloud service in 2023, shifting critical evidence to platforms like Microsoft 365, AWS, and Google Workspace, where traditional forensic methods are insufficient. In response, Europol established the European Cloud Forensics Framework in 2024 to standardize data acquisition via legal APIs and preservation snapshots. The European Central Bank now requires financial institutions to maintain cloud forensic readiness as part of operational resilience testing. According to the French Data Protection Authority, 58% of GDPR breach notifications in 2023 involved cloud misconfigurations, necessitating specialized forensic reconstruction. This structural migration of data sources compels both public and private investigators to develop cloud‑specific capabilities or risk evidentiary gaps.

By End‑User Insights

The government segment accounted for 45.4% of the European market share in 2024. The leading position of the government segment in the European market is driven by law enforcement, judicial authorities, and national security agencies. As per Europol, over 220 joint forensic operations were conducted in 2023 targeting ransomware groups, child exploitation networks, and darknet markets. National agencies like Germany’s BKA and France’s OCLCTIC operate dedicated digital forensic units that process thousands of devices annually. The European Public Prosecutor’s Office relies entirely on digital evidence, with 94% of its 2023 cases involving forensic disk or mobile analysis. Additionally, the EU Cybersecurity Act requires critical infrastructure protection agencies to perform forensic readiness assessments, further expanding government demand. This legally enforced investigative obligation ensures sustained and growing investment in forensic resources across all member states.

The healthcare segment is on the rise and is expected to witness a CAGR of 18.8% over the forecast period in this regional market. As per the European Union Agency for Cybersecurity, healthcare has become the most attacked critical infrastructure sector in Europe, with 68% of hospitals experiencing at least one ransomware incident in 2023. These attacks often involve data exfiltration followed by encryption, making forensic analysis essential to determine breach scope and comply with GDPR breach notification rules. In Germany, the Federal Office for Information Security reported that fifty‑two hospital forensic investigations in 2023 revealed attackers had accessed patient records for months before detection. Consequently, national health agencies now mandate post‑incident forensic audits. The French Ministry of Health requires all public hospitals to retain certified forensic services for rapid response and sparking a wave of contracts with firms like NCC Group and Kroll. This defensive imperative transforms forensics from optional to essential in life‑critical environments.

COUNTRY-LEVEL ANALYSIS

United Kingdom Digital Forensics Market Analysis

The United Kingdom captured the most dominant share of the Europe digital forensics market in 2025. The dominance of the UK in the European market is primarily due to its mature legal framework, robust law enforcement capabilities, and high incidence of cybercrime. According to the UK’s National Cyber Security Centre, over 38,000 cyber incidents were reported by critical national infrastructure operators in 2023 alone. The country pioneered standardized forensic accreditation through the Forensic Science Regulator, which mandates ISO 17025 compliance for all digital evidence providers, which is a model now influencing EU policy. The National Crime Agency’s Digital Forensics Unit processes over 40,000 devices annually, while private firms like NCC Group and BAE Systems support corporate investigations. Post-Brexit, the UK has intensified bilateral data-sharing agreements with EU states to maintain cross-border forensic cooperation. This combination of regulatory rigor, operational scale, and public–private partnership sustains the UK’s leadership despite geopolitical shifts.

Germany Digital Forensics Market Analysis

Germany ranks second in the European digital forensics market. The stringent data protection laws, advanced industrial espionage threats, and federalized law enforcement structures are fuelling the digital forensics market growth in Germany. According to the Federal Office for Information Security, 72% of German manufacturing firms experienced intellectual property theft attempts in 2023, necessitating forensic investigations. The country’s Bundeskriminalamt operates one of Europe’s largest forensic labs, with specialized units for mobile, cloud, and vehicle forensics. Germany’s implementation of the EU Cyber Resilience Act requires critical infrastructure operators to conduct annual forensic readiness tests, a mandate driving significant private sector demand. Additionally, the Federal Constitutional Court’s strict rulings on digital privacy mean forensic methods must meet high judicial scrutiny, enhancing the need for certified professionals. This legal, technical, and industrial triad creates a high-integrity market where quality and compliance outweigh cost considerations.

France Digital Forensics Market Analysis

France maintains a strong position through centralized cyber policing, proactive threat intelligence, and regulatory enforcement. The National Cybersecurity Agency (ANSSI) reported a 45% increase in forensic requests from financial and energy sectors in 2023 following ransomware surges. The country’s Judicial Police operates the Central Directorate of Fight Against Cybercrime, which coordinates forensic operations nationwide with standardized toolkits and training. France also leads in forensic research, with institutions like INRIA developing open-source analysis frameworks adopted across the EU. The 2023 transposition of the EU Whistleblower Directive triggered a wave of internal corporate investigations requiring independent forensic validation. This blend of state capacity, legal obligation, and academic innovation positions France as a hub for both operational and methodological advancement in digital forensics.

Netherlands Digital Forensics Market Analysis

The Netherlands stands out for its role as a European cyber justice hub, hosting Europol’s European Cybercrime Centre and the Dutch Public Prosecution Service’s specialized cyber unit. According to the Dutch National Police, over 18,000 digital devices were forensically examined in 2023, with a focus on darknet markets and payment fraud. The country pioneered the use of AI-assisted forensic triage in real-time investigations and maintains one of Europe’s most advanced cloud forensics labs. Dutch courts have set influential precedents on digital evidence admissibility, requiring strict hash verification and chain-of-custody documentation. Additionally, the Netherlands serves as a testbed for EU-wide forensic protocols under the European Judicial Cybercrime Network. This concentration of international institutions, judicial innovation, and technical excellence enables the Netherlands to exert disproportionate influence on the continent’s forensic standards and practices.

Sweden Digital Forensics Market Analysis

Sweden holds a key position in the European digital forensics landscape due to its leadership in digital transparency, cybersecurity, and cross-sectoral data governance. According to the Swedish Civil Contingencies Agency, 61% of public sector entities underwent forensic audits in 2023 following phishing breaches. The country’s strict implementation of GDPR means even minor data leaks trigger mandatory forensic investigations, which is a practice enforced by the Swedish Data Protection Authority. Sweden also integrates forensics into national digital identity systems, with logs from BankID and e‑ID services subject to forensic validation during fraud cases. The Swedish National Police’s Digital Forensics Unit collaborates closely with KTH Royal Institute of Technology on research into encrypted messaging app forensics. This proactive culture of digital accountability makes Sweden a model for forensic integration in public services and a key influencer in Nordic and EU policy development.

COMPETITIVE LANDSCAPE

Competition in the Europe digital forensics market is defined by a dual dynamic between global technology vendors and specialized regional service providers. While firms like Cellebrite and Magnet Forensics dominate through scalable software platforms, they face pressure to localize data handling, meet stringent judicial standards, and prove tool transparency amid growing scrutiny over black box algorithms. Conversely, European players such as NCC Group and SEC Consult compete on contextual expertise, legal credibility and multilingual forensic reporting rather than software features alone. The absence of EU-wide forensic tool certification creates both opportunity and risk as courts increasingly demand validation of methodology. Competition is thus less about price and more about trust, chain of custody integrity, and alignment with national legal traditions. Success requires not only technical excellence but also deep engagement with Europe’s fragmented yet interconnected ecosystem of law enforcement regulators and judicial authorities.

KEY MARKET PLAYERS

The leading companies operating in the Europe digital forensics market include:

- MSAB AB

- LogRhythm Inc.

- Cellebrite

- IBM Corporation

- Magnet Forensics

- PricewaterhouseCoopers LLP

- NCC Group

- Nuix Ltd.

TOP PLAYERS IN MARKET

- Cellebrite is a leading force in the Europe digital forensics market through its advanced mobile and cloud forensic solutions used by law enforcement and corporate investigators across the region. The company’s UFED and Cloud Analytics platforms enable rapid extraction and decryption of data from thousands of device types, including encrypted messaging apps. In 2024, Cellebrite enhanced its European presence by opening a forensic training academy in Berlin to certify investigators on GDPR compliant evidence handling. It also expanded partnerships with Europol and national cyber units to support joint operations against child exploitation and financial crime. These initiatives reinforce Cellebrite’s role as a trusted technology enabler that bridges technical capability with legal admissibility in Europe’s complex regulatory environment while contributing to global standards in mobile forensics.

- Magnet Forensics contributes significantly to the Europe digital forensics landscape via its AI-powered AXIOM platform, which automates evidence analysis across computers, mobile devices, and cloud sources. The company emphasizes forensic integrity and judicial readiness with features like automated report generation and tamper-proof audit trails. In 2023, Magnet launched a European data residency option for its cloud forensic tools hosted in Microsoft Azure facilities in Germany, ensuring compliance with EU data sovereignty requirements. It also collaborated with police academies in France and the Netherlands to integrate AXIOM into official training curricula. By aligning its technology with European legal expectations and educational frameworks, Magnet strengthens its position as a solution of choice for both public and private sector investigators committed to ethical and court-defensible digital investigations.

- NCC Group holds a strategic position in the Europe digital forensics market through its integrated cyber incident response and forensic investigation services tailored for critical infrastructure and regulated industries. The company combines deep technical expertise with legal advisory support to guide clients through breach disclosure under GDPR and sector-specific mandates. In early 2024, NCC Group established a dedicated healthcare forensic response unit in the UK following a surge in ransomware attacks on hospitals. It also published a widely cited forensic readiness framework adopted by several European energy and financial firms. Unlike pure software vendors, NCC Group’s value lies in its end-to-end investigative authority and expert testimony capabilities, which make it a preferred partner for high-stakes breaches where evidence must withstand judicial scrutiny across multiple jurisdictions.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe digital forensics market invest heavily in artificial intelligence to automate evidence triage and reduce investigation time. They ensure data residency and processing compliance with GDPR by hosting forensic tools in local EU cloud infrastructure. Companies establish training academies and certification programs to build investigator capacity and ensure proper tool usage. Strategic partnerships with Europol national police forces and judicial bodies enhance operational relevance and trust. Additionally, they develop sector-specific forensic playbooks for healthcare finance and critical infrastructure to address regulatory and threat landscape nuances across European industries.

MARKET SEGMENTATION

This research report on the Europe digital forensics market has been segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

- Services

By Type

- Computer Forensics

- Mobile Device Forensics

- Network Forensics

- Cloud Forensics

- Database Forensics

- IoT and Embedded Device Forensics

By Tool

- Data Acquisition and Preservation

- Data Recovery and Reconstruction

- Forensic Data Analysis

- Review and Reporting

- Forensic Decryption and Password Cracking

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

By End-user Industry

- Government and Law Enforcement Agencies

- BFSI

- IT and Telecom

- Healthcare

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Transportation and Logistics

- Defense and Aerospace

- Education

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe digital forensics market?

The Europe digital forensics market encompasses tools and services for investigating cybercrimes through data recovery from devices, networks, and cloud systems. It supports law enforcement and compliance across EU nations.

Why is the Europe digital forensics market growing?

The Europe digital forensics market grows due to rising cyber threats and regulations like GDPR and DORA. Demand for mobile and cloud forensics drives adoption in government and BFSI sectors.

Who are the key players in the Europe digital forensics market?

Key players in the Europe digital forensics market include software providers like MSAB and Nuix, plus IBM for analytics. They specialize in mobile and incident response solutions.

What drives demand in the Europe digital forensics market?

Demand in the Europe digital forensics market stems from ransomware attacks and encrypted app usage. Compliance needs in BFSI and government fuel investment in forensic capabilities.

What are the main segments of the Europe digital forensics market?

The Europe digital forensics market segments by type like mobile device and cloud forensics, plus components including software and services for diverse cyber investigations.

How does technology impact the Europe digital forensics market?

Technology shapes the Europe digital forensics market with AI analytics and 5G network tools. It enables faster evidence processing from IoT and connected vehicles continent-wide.

What challenges face the Europe digital forensics market?

Challenges in the Europe digital forensics market include skills shortages and data encryption barriers. Rapid tech evolution demands constant tool updates for investigators.

What is the role of government in the Europe digital forensics market?

Government leads the Europe digital forensics market through law enforcement investments in forensics labs. NIS2 compliance mandates advanced cyber investigation capabilities.

How does the Europe digital forensics market support BFSI?

The Europe digital forensics market supports BFSI via fraud detection and DORA-compliant incident response. Forensic analytics protect financial data from breaches effectively.

What trends shape the Europe digital forensics market?

Trends in the Europe digital forensics market feature cloud forensics growth and AI-driven analysis. Vehicle and IoT forensics emerge with connected technology expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com