Europe Drug Delivery Devices Market Research Report By Route Of Administration, Facility Of Use, Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe) - Industry Analysis, Size, Share, Trends and Growth Forecast (2026 to 2034)

Market Size, 2025

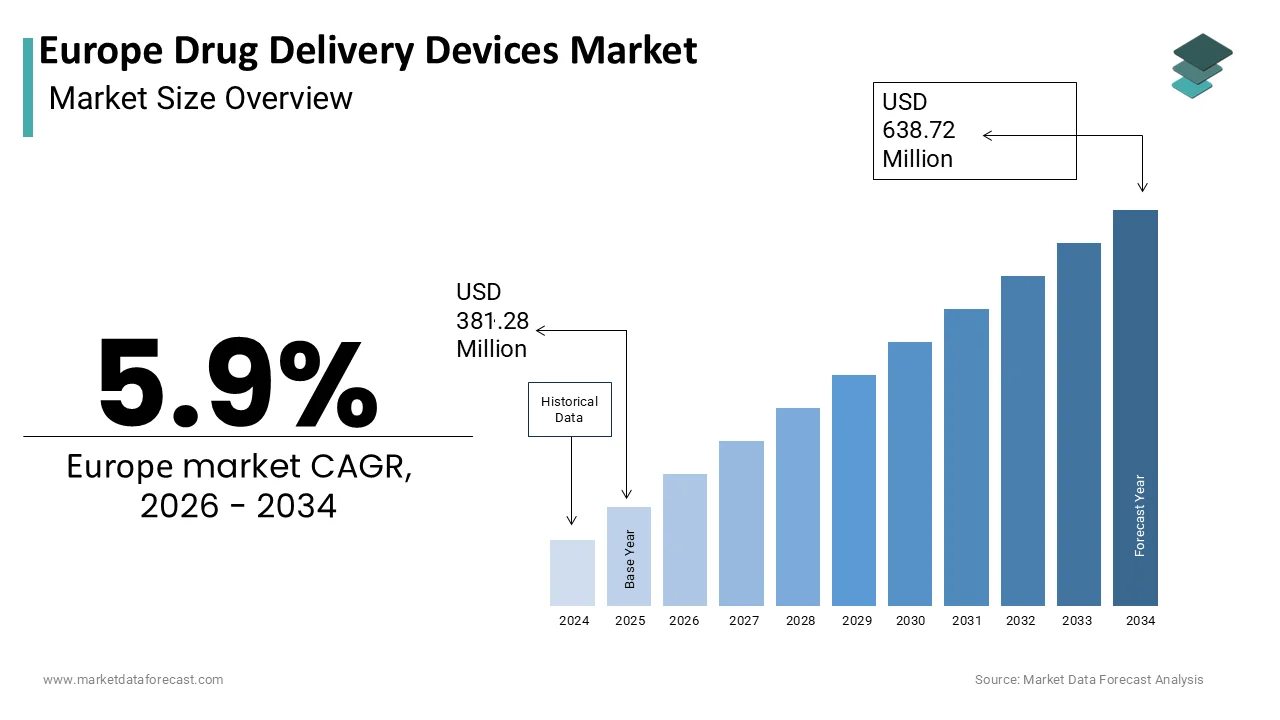

$381.28 MnMarket Estimate, 2026

$403.78 MnMarket Forecast, 2034

$638.72 MnCAGR, 2026–2034

5.9%Europe Drug Delivery Devices Market Summary

The Europe Drug Delivery Devices Market was valued at USD 360.04 million in 2024 and is estimated to reach USD 381.28 million in 2025. The market is projected to grow to USD 638.72 million by 2034, registering a CAGR of 5.9% during the forecast period.

Market Snapshot

- 2024 Market Size: USD 360.04 Million

- 2025 Market Size: USD 381.28 Million

- 2034 Market Size: USD 638.72 Million

- CAGR (2026–2034): 5.9%

Key Growth Drivers

- Rising prevalence of diabetes, respiratory diseases, and autoimmune disorders.

- Growing adoption of biologics and biosimilars requiring specialized delivery systems.

- Increasing demand for self-administration devices such as autoinjectors, insulin pens, and inhalers.

- Expansion of home healthcare and remote patient monitoring.

- Growing use of connected and digital drug delivery technologies.

Key Restraints

- Stringent regulatory requirements under the European Medical Devices Regulation (MDR).

- High costs associated with wearable and connected drug delivery devices.

- Supply chain challenges related to specialty glass, sensors, and electronic components.

- Risk of medication errors due to improper device handling.

Key Opportunities

- Expansion of smart and connected drug delivery devices.

- Increasing adoption of wearable injectors for biologic therapies.

- Growing demand for biosimilar-compatible delivery systems.

- Investments in localized manufacturing and supply chain resilience.

Segment Highlights

By Route of Administration

- Largest Segment: Injectable Drug Delivery (42.3% market share in 2025)

- Fastest-Growing Segment: Implantable Drug Delivery (14.3% CAGR)

By End User

- Largest Segment: Home Care Settings (38.2% market share in 2025)

- Fastest-Growing Segment: Ambulatory Surgical Centers (11.7% CAGR)

Country Insights

- Germany: Largest market with 22.3% share, driven by strong healthcare infrastructure and biologics adoption.

- France: Second-largest market with 18.2% share, supported by chronic disease management programs and digital health initiatives.

- United Kingdom: Strong growth driven by connected healthcare technologies and innovation programs.

- Italy: Increasing biologics use and growing demand for outpatient treatment services.

Key Companies

- Becton Dickinson and Company (BD)

- Ypsomed Holding AG

- Gerresheimer AG

- Bend Research

- Endocyte

- Microchips Inc.

- Pearl Therapeutics Inc.

- Presage Bioscience

- UCB Group

- Genentech Inc.

- Polymer Factory

- Alkermes Inc.

- BIND Biosciences Inc.

- QLT Inc.

Europe Drug Delivery Devices Market Size

The Europe Drug Delivery Devices Market is projected to grow from USD 381.28 million in 2025 to USD 403.78 million in 2026 and reach USD 638.72 million by 2034, registering a CAGR of 5.9% during the forecast period from 2026 to 2034.

The Drug delivery devices are engineered systems designed to administer therapeutic agents with precision, safety, and patient compliance across multiple routes, including subcutaneous, inhalation, transdermal, and oral. These include autoinjectors, prefilled syringes, insulin pens, metered dose inhalers, and implantable infusion pumps, among others. The European healthcare ecosystem increasingly prioritizes patient-centric therapies driven by chronic disease burdens and the shift toward home-based care. The European Medicines Agency has streamlined combination product regulations under the Medical Devices Regulation to harmonize the evaluation of drug-device co-development. Furthermore, national health systems across Germany, France, and the Netherlands now mandate health technology assessments that evaluate not just drug efficacy but also delivery system usability and error reduction potential.

MARKET DRIVERS

Surge in Chronic Diseases Necessitates Long-Term Self-Administration Solutions

The escalating prevalence of chronic conditions, such as diabetes, autoimmune disorders, and respiratory diseases, is a major factor bolstering the growth of the European drug delivery devices market. According to the European Centre for Disease Prevention and Control, over 60 million Europeans live with diabetes or prediabetes, with insulin-dependent patients requiring multiple daily injections. Similarly b, biologic therapies for rheumatoid arthritis and multiple sclerosis often demand subcutaneous self-administration every one to four weeks. As per the European Respiratory Society, over 30 million people in the EU suffer from asthma or chronic obstructive pulmonary disease,e, necessitating regular use of pressurized metered dose inhalers or dry powder devices. National health policies increasingly support home-based management to reduce hospital burden, with Germany’s Integrated Care Agreements reimbursing connected inhalers that track adherence. This long-term treatment paradigm demands intuitive error-resistant delivery systems that ensure consistent dosing and patient compliance. Consequently, device manufacturers are prioritizing ergonomic design, dose confirmation feedback, and needle shielding features validated by the European Commission’s Human Factors Guidance for medical devices. The chronic care imperative thus serves as a powerful structural driver for advanced self-use delivery platforms across the continent.

Accelerated Adoption of Biologics and Complex Molecules Drives Specialized Delivery Needs

The therapeutic pipeline is dominated by large molecule drugs, including monoclonal antibodies, peptides, and gene therapies, that cannot be administered,,d orally due to enzymatic degradation and poor bioavailability. The rising adoption of biologics and complex molecules is additionally fuelling the growth of the European drug delivery devices market. As per the European Medicines Agency, biologics accounted for many new active substance approvals in 2023 with their clinical centrality. These molecules often require high viscosity subcutaneous delivery volumes exceeding 1 milliliter or cold chain stability challenges that standard syringes cannot address. Consequently, there is a rising dependence on advanced devices, such as wearable injectors for volumes up to 10 milliliters and dual-chamber prefilled syringes that reconstitute lyophilized drugs at the point of use. A 2025 assessment by the Paul Ehrlich Institute confirmed that many newly launched biologics in Germany included proprietary delivery systems to ensure stability and dosing accuracy. Regulatory bodies now evaluate delivery compatibility as part of marketing authorization with the EMA’s Guideline on Quality of Drug Delivery Devices, requiring extensive usability testing. This molecular complexity has made specialized delivery hardware not an accessory but a core component of therapeutic efficacy and regulatory approval in Europe.

MARKET RESTRAINTS

Stringent and Evolving Combination Product Regulations Increase Development Timelines

The classification of drug delivery devices as combination products under the European Union Medical Devices Regulation and the Clinical Trials Regulation creates complex and overlapping compliance pathways that delay time. The stringent and evolving combination product regulations increase development timelines, which is one of the factors impeding the growth of the European drug delivery devices market. According to the European Medicines Agency, manufacturers must now submit separate technical documentation for both the drug and device components, with alignment on risk management, usability, and biocompatibility. A 2025 review by the European Federation of Pharmaceutical Industries and Associations found that the average approval timeline for combination products has increased by 9 to 14 months since full MDR implementation in 2021. Notified bodies face capacity constraints, with over sixty perchigh-riskgh risk device reviews backlogged as reported by the European Commission. Furthermore, national competent authorities interpret human factors validation requirements inconsistently, with Germany mandating home usability studies while Italy accepts simulated environments. These regulatory ambiguities disproportionately impact small biotech firms, which constitute 40% of novel biologic sponsors in Europe. The resulting delays and cost escalations stifle innovation, particularly for next-generation wearable and digitally connected delivery systems.

High Costs of Advanced Delivery Systems Limit Reimbursement and Patient Access

The premium pricing of smart and wearable drug delivery devices often exceeds national reimbursement thresholds, which is also hindering the growth of the European drug delivery devices market. As per a 2025 analysis by the European Observatory on Health Systems and Policies, autoinjectors with dose tracking or wearable on-body injectors cost three to eight times more than standard prefilled syringes, creating budget impact concerns for payers. In countries es as Spain and Greece, national health technology assessment bodies routinely reject reimbursement for connected delivery systems unless manufacturers provide long-term adherence and hospitalization reduction data. Even in wealthier systems, such as France’s Transparency Committee, granted only partial reimbursement for a next-generation insulin patch pump in early 2025, citing insufficient comparative effectiveness evidence.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies Enables Smart Connected Delivery Platforms

The emergence of drug delivery devices with digital health capabilities to enhance treatment adherence, real-time monitoring, and personalized care is creating new opportunities for the growth the European drug delivery devices market. Connected autoinjectors and inhalers now transmit dose timing and technique data to smartphone applications, enabling clinicians to intervene when errors or omissions occur. As per the European Commission’s Digital Transformation of Health and Care initiative, over 55% of member states have launched national digital health strategies that incentivize connected medical devices. In 2025, the UK’s National Health Service piloted a program using Bluetooth-enabled insulin pens for type 1 diabetes paBluetooth-enabledin a reduction in HbA1c variability over 6 months. Similarly, Germany’s DiGA framework fast-tracks reimbursement for delivery devices with validated digital components that improve health outcomes. The European Medicines Agency has also issued draft guidance on data standards for connected combination products, facilitating regulatory clarity.

Expansion of Biosimilars Creates Demand for Interchangeable User-Friendly Delivery Systems

The rapid uptake of biosimilars is generating significant demand for standardized intuitive delivery platforms that support seamless switching and reduce administration errors. The expansion of biosimilars creates demand for interchangeable and user-friendly delivery systems, which additionally enhance the growth of the European drug delivery devices market. Unlike originator biologics, which often use proprietary pens or injectors, biosimilar manufacturers frequently rely on universal delivery systems to accelerate entry and ensure interchangeability. This has spurred innovation in reusable multi-dose autoinjectors and prefilled syringes with universal fitment compatible across multiple biosimilar molecules. The European Directorate for the Quality of Medicines now includes device usability in its biosimilar guideline updates , emphasizing the need for a consistent user experience during switching. National formularies in the Netherlands and Sweden increasingly favor biosimilars paired with patient training on common delivery platforms, enhancing adherence.

MARKET CHALLENGES

Device Usability Failures,, Risk,, Medication Errors,, and Regulatory Non Compliance

The poor human factors design in drug non-compliance continues to pose significant patient safety risks, which is a significant factor challenging the growth of Europe. As per the European Medicines Agency, reported adverse events linked to biologics between 2021 and 2023 involved user errors such as incomplete dose delivery, incorrect injection technique, or failure to activate safety mechanisms. A 2025 study published in the European Journal of Hospital Pharmacy found that 38% of elderly patients using multi-step autoinjectors made at least one handling mistake during simulated use. These errors are particularly prevalent in high-stress or low-vision scenarios common among chronically ill populations. The Medical Devices Regulation now mandates summative usability testing with representative patient groups, yet inconsistent implementation across notified bodies leads to variable safety outcomes. In response, France’s National Agency for Medicines initiated a post-market surveillance pilot in 2023, tracking real-world injection errors through connected device data. Until human-centered design becomes universally enforced through rigorous standardized validation, these usability gaps will persist as a critical vulnerability in Europe’s drug delivery infrastructure.

Supply Chain Fragility Exposes Critical Dependencies: Single-Source Components.

The European drug delivery device manufacturing ecosystem remains vulnerable to supply chain disruptions due to concentrated sourcing of high-precision components such as glass barrels, springs, and sensors. As per the European Commission’s 2025 Critical Raw Materials and Medical Devices Report, over seventy percent of specialty glass for prefilled syringes is sourced from two non-EU suppliers, creating strategic dependency. The 2022 global glass shortage delayed launches of multiple biologic therapies in Europe, with one multinational reporting a six-month postponement due to barrel unavailability. Similarly, microelectronic components for connected injectors face lead times exceeding twenty weeks according to the European Medical Devices Industry Group. Geopolitical tensions and export controls further exacerbate this fragility, with no certified European alternative for high borosilicate glass currently available. Although the EU’s Pharmaceutical Strategy for 2025 aims to onshore medical component production, progress remains slow.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Route of Administration, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Bend Research, Endocyte, Microchips Inc., Pearl Therapeutics Inc., Presage Bioscience, UCB Group, Genentech Inc., Polymer Factory, Alkermes Inc., BIND Biosciences Inc., and QLT Inc. |

SEGMENTAL ANALYSIS

By Route Of Administration Insights

The injectable drug delivery segment accounted in holding 42.3% of the European drug delivery devices market share in 2025, owing to the continent’s accelerating adoption of biologic therapies, which require parenteral administration due to molecular instability and poor oral bioavailability. As per the European Medicines Agency, biologics constituted any new therapeutic approvals in 2023, with monoclonal antibodies alone treating Europeans for conditions like rheumatoid arthritis, psoriasis, and oncology indications. The rise of self-administered chronic care has further entrenched injectables, with over 8 million patients in Germany and France using insulin pens or autoinjectors daily, as documented by national diabetes registries. Regulatory frameworks now mandate device integration of high-value biologics, with the EMA requiring human factors validation for all subcutaneous delivery systems. Additionally, advances in wearable on-body injectors now enable delivery of high-volume vial-body formulations up to 10 milliliters, addressing a critical gap in monoclonal antibody dosing.

The implantable drug delivery segment is likely to grow at the fastest CAGR of 14.3% from 2025 to 2033, with the clinical demand for sustained localized therapy in oncology, ophthalmology, and neurology, where systemic delivery poses efficacy and toxicity challenges. In ophthalmology, intravitreal implants like dexamethasone and fluocinolone acetonide now treat over many patients annually across the EU for chronic macular edema, as per the European Society of Retina Specialists. Similarly, implantable micro pumps for intrathecal baclofen delivery have reduced spasticity hospitalizations in multiple sclerosis patients, according to a 2025 report. The European Medicines Agency has fast-tracked several implantable combination products under its PRIME scheme, recognizing their therapeutic differentiation. Moreover, innovations in biodegradable polymer matrices now enable programmable release profiles over months without surgical removal.

By End User Insights

The home care settings segment was the largest by holding 38.2% of the European drug delivery devices market share in 2025, where Europe’s strategic shift toward decentralized care models is driven by aging demographics, hospital capacity constraints, and patient preference for autonomy. As per Eurostat, the EU population aged 65 or older managed at least one chronic condition requiring regular medication. National policies actively support home-based therapy, with Germany’s Integrated Care contracts reimbursing connected insulin pens and France’s Long Term Illness scheme covering autoinjectors for autoimmune diseases. The European Commission’s Digital Health Action Plan further incentivizes remote monitoring-enabled delivery devices that transmit adherence data to care teams. This ecosystem of policy reimbursement and user-centric design has transformed the home from a passive care environment into an active therapeutic node in Europe’s healthcare continuum.

The ambulatory surgical centers segment is anticipated to witness the fastest CAGR of 11.7% ffrom2025 to 2033, with the migration of complex procedures from inpatient hospitals to outpatient settings driven by cost efficiency and infection control priorities. High number of cataract surgeries and orthopedic injectA highgh in Western Europe now occur in ambulatory centers, as documented by the OECD Health Statistics 2025. These facilities increasingly rely on single-use precision delivery systems such as ocular injectors for anti-VEGF therapy and intra-articular pen devices for viscosupplementation. The European Society of Cataract and Refractive Surgeons reported in 2025 that intravitreal injections were administered in ambulatory centers across Germany and Italy alone. Regulatory harmonization under the Medical Devices Regulation has also streamlined device procurement for these centers, enabling rapid adoption of next-generation delivery platforms.

COUNTRY LEVEL ANALYSIS

Germany Next-Generation Devices Market Analysis

Germany was the top performer of the European drug delivery devices market by capturing 22.3% of share in 2025. The country’s leadership arises from its dense network of biopharmaceutical companies, robust statutory health insurance system, and early adoption of advanced delivery technologies. Over 300 biologic therapies are commercially available in Germany, with nearly all paired with proprietary delivery systems, as per the research. The German Social Health Insurance funds fully reimburse smart pens and autoinjectors for chronic conditions under the AMNOG framework, provided manufacturers demonstrate added benefit. Furthermore, Germany hosts Europe’s highest concentration of medical device notified bodies, accelerating combination product approvals. The national Digital Health Applications Ordinance has enabled reimbursement for connected delivery devices that integrate with electronic health records.

France Drug Delivery Devices Market Analysis

France's drug delivery devices market was ranked second by holding 18.2% of the share in 2025, with its influential regulatory stance and comprehensive chronic disease management programs. The Transparency Committee’s rigorous health technology assessments shape reimbursement decisions not only domestically but across Southern Europe. France’s Long Term Illness scheme covers 100% of costs for autoinjectors used in multiple sclerosis, rheumatoid arthritis, and type 1 diabetes, benefiting over four million patients. The country also leads in digital therapeutics with the DiGA registry fast fast-tracking connected inhalers and insulin delivery systems that prove adherence improvement. As per the French Ministry of Health, mandated human factors training for all new biologic prescribers emphasizes correct device use. National disease registries such as the CRIEP provide real-world evidence on delivery system performance f,, further informing policy. This blend of regulatory rig,o,r patient access and outcome monitoring cements France’s strategic ro,, le in the European delivery device ecosystem.

United Kingdom Drug Delivery Devices Market Analysis

The United Kingdom drug delivery devices market was positioned second by holding 34.3% of share in 2025. The National Health Service remains a powerful adopter through targeted innovation pathways such as the NHS Accelerated Access Collaborative, which fast-tracks high-impact delivery technologies. As per the NHS launched a nationwide pilot for connected insulin pens in type 1 diabetes reducing HbA1c variability 6 six months, as per NHS England outcomes data. The UK continues to align its combination product guidelines with EU MDR principles, ensuring mutual recognition in clinical evidence. Moreover, the UK hosts leading academic centers like Imperial College London, pioneering microneedle and implantable delivery research funded by UK Research and Innovation. Although no longer part of the EU regulatory network,k, the UK’s scientific infrastructure, reimbursement pilots, and large chronic patient base sustain its influence and market significance in European drug delivery innovation.

Italy Drug Delivery Devices Market Analysis

Italy's drug delivery devices market growth is likely to be driven by the highest per capita biologic prescription rates in the EU. Over 1.8 million Italians receive monoclonal antibody therapies annually for autoimmune and oncology indications necessitating a robust delivery infrastructure. Regional health authorities in Lombardy and Emilia Romagna have implemented standardized training programs for autoinjector use, reducing administration errors by 30%, as per the study. Italy also leads in ophthalmic delivery with over four hundred thousand intravitreal injections administered annually in hospital, outpatient, and ambulatory settings.

TOP LEADING PLAYERS IN THE MARKET

- Becton Dickinson and Company is a global leader in drug delivery systems with a strong footprint across Europe through its portfolio of syringes, autoinjectors, and safety-engineered devices. The company supplies critical delivery platforms for biologics vaccines, e,s, and insulin to major pharmaceutical partners, and national immunization programs. In early 2025, BD launched its next-generation BD Ultra Fine Pen Needle with enhanced comfort features tailored for elderly diabetic patients in Germany and France. The firm also expanded its human factors testing center in Ireland to support EU Medical Devices Regulation compliance for combination products. Collaborations with European biotech firms on wearable injector development further reinforce BD’s role as a strategic enabler of advanced parenteral delivery across the continent.

- Ypsomed Holding AG stands as a European specialist in self-injection systems with deep integration into the chronic care ecosystem through its reusable and disposable autoinjectors and insulin pens. The company partners with leading biopharmaceutical firms to co-develop customized delivery platforms that meet stringent usability and regulatory standards. In late 2023, Ypsomed introduced its YpsoDose electronic autoinjector featuring real-time dose tracking and Bluetooth connectivity, now deployed in multiple EU countries for multiple sclerosis and rheumatoid arthritis therapies. The firm also inaugurated a new production line in Switzerland in early 2025 to meet growing demand for high-volume wearable injectors. Its focus on patient-centric engineering and digital integration cements Ypsomed’s position as a key innovation driver in Europe’s delivery device landscape.

- Gerresheimer AG contributes significantly to the European drug delivery devices market through its primary packaging and device solutions, including glass and plastic syringes,,inhalerccomponentsss nd nasal spray systems. The company supplies device-ready containers to global pharmaceutical manufacturers under strict quality and traceability protocols aligned with EU regulations. In 2025, Gerresheimer launched its Gx RTF ready-to-fill syringe platform with integrated plunger stopper and tip cap-capping assembly errors in biologic fill finish operations across European contract manufacturing sites. The firm also partnered with a Dutch biotech to develop a novel ocular delivery pen for posterior segment therapy. Continuous investment in smart manufacturing and regulatory-compliant production ensures Gerresheimer remains a backbone supplier for next-generation drug delivery systems in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European drug delivery devices market prioritize human factors engineering to ensure intuitive device performance, especially for elderly and chronically ill users. Thy invests heavily in combination product regulatory expertise to navigate the complex Medical Devices Regulation and Clinical Trials Regulation frameworks. Companies pursue strategic co-development with pharmaceutical firms to embed delivery systems early in drug development pipelines. Digital integration through connected devices and mobile health platforms enhances adherence monitoring and real-world evidence generation. Innovation focuses on high viscosity delivery, wearable injectors, nd reusable platforms to support biologics and sustainability goals. Firms also expand localized manufacturing and testing capabilities within Europe to ensure supply chain resilience and faster regulatory approval.

COMPETITIVE LANDSCAPE

The European drug delivery devices market features intense competition among multinational device specialists, European engineering fifirmsand global packaging leaders, all vying to support the biologics-driven, ven therapeutic shift. Competition is not based on price but on regulatory readiness, usability validation, manufacturing precision,n, and digital capabilities. Incumbents benefit from deep relationships with pharmaceutical partners and established quality management systems compliant with EUMDR.e, iche innovators in wearable injectable,ors mi reedles and implantable systems are gaining traction through venture funding and academic offshoots. Regulatory complexity creates high barriers to entry, favoring firms with in-house notified body experience and clinical validation infrastructure. Houseational differences in reimbursement for smart devices further fragment adoption, requiring localized market access strategies. Themoss, successful players combine engineering excellence without come-based value propositions, demonstrating reduced hospitalizations, improved adherence, or lower total cost of care.

KEY MARKET PLAYERS

Some of the Prominent Companies leading the europe device market profiled in the report are

- Bend Research

- Endocyte

- Microchips Inc.

- Pearl Therapeutics Inc.

- Presage Bioscience

- UCB Group

- Genentech Inc.

- Polymer Factory

- Alkermes Inc.

- BIND Biosciences Inc.

- QLT Inc.

MARKET SEGMENTATION

This market research report on the europe drug delivery devices market is segmented and sub-segmented into the following categories.

By Route of Administration

- Oral Drug Delivery

- Pulmonary Drug Delivery

- Injectable Drug Delivery

- Ocular Drug Delivery

- Nasal Drug Delivery

- Topical Drug Delivery

- Implantable Drug Delivery

- Tran mucosal Drug Delivery.

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Home Care settings

- Diagnostic Centers.

By Region

- UK

- France

- Spain,

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Drug Delivery Devices Market?

Chronic disease prevalence, aging populations, and demand for self-administration fuel the Europe Drug Delivery Devices Market, with technological advances in biologics delivery, smart injectors, and wearable pumps boosting adoption. Regulatory support under EU MDR and investments in home healthcare further accelerate expansion across major countries like Germany, France, UK, Italy, and Sweden.

2. Who are key players in the Europe Drug Delivery Devices Market?

Leading companies in the Europe Drug Delivery Devices Market include Pfizer Inc., Johnson & Johnson, Roche, Novartis, Bayer AG, BD, Gerresheimer AG, and Sanofi, focusing on innovative syringes, inhalers, and infusion systems. These firms drive competition through R&D in connected devices and partnerships to meet rising needs for chronic therapy delivery.

3. What is the largest segment in the Europe Drug Delivery Devices Market?

Inhalers dominate the Europe Drug Delivery Devices Market due to high respiratory disease rates, followed by injection devices showing fastest growth from biologics and self-injection trends. Other segments like nebulizers, transdermal patches, and infusion pumps also contribute significantly in hospital and ambulatory settings

4. How does regulation impact the Europe Drug Delivery Devices Market?

EU MDR compliance shapes the Europe Drug Delivery Devices Market by ensuring safety and efficacy in advanced systems like auto-injectors and smart pumps, while fostering innovation amid stricter post-market surveillance. This supports market maturity in countries like Germany and France, balancing growth with patient safety standards.

5. What role does home care play in the Europe Drug Delivery Devices Market?

Home healthcare expands the Europe Drug Delivery Devices Market through portable inhalers, pen injectors, and patch pumps enabling self-administration for chronic patients. This shift reduces hospital burdens, aligns with aging demographics, and integrates digital monitoring for better adherence across Europe.

6. Which countries lead the Europe Drug Delivery Devices Market?

Germany, France, UK, Italy, Spain, and Sweden lead the Europe Drug Delivery Devices Market, driven by advanced infrastructure, high chronic disease rates, and R&D investments. Sweden shows highest growth potential from innovation in injection and pulmonary delivery systems.

7. What innovations shape the Europe Drug Delivery Devices Market?

Connected and wearable devices, AI-integrated pumps, and nanotechnology for targeted delivery innovate the Europe Drug Delivery Devices Market, improving precision for biologics and complex therapies. These advancements enhance patient compliance and support personalized medicine trends.

8. What is the outlook for the Europe Drug Delivery Devices Market?

The Europe Drug Delivery Devices Market anticipates steady expansion from chronic disease rises, self-care trends, and tech integrations like biosimilars compatibility. Biosimilar affordability and volume growth will sustain momentum despite pricing pressures.

9. How do chronic diseases influence the Europe Drug Delivery Devices Market?

Diabetes, respiratory, and cardiovascular conditions propel the Europe Drug Delivery Devices Market by necessitating regular, precise dosing via inhalers, injectors, and infusions. Europe's 56+ million diabetes cases underscore demand for advanced, user-friendly systems.

10. What end-users dominate the Europe Drug Delivery Devices Market?

Hospitals, clinics, and ambulatory centers lead the Europe Drug Delivery Devices Market, with growing home care adoption for injectables and oral systems. This diversification supports scalable delivery amid rising outpatient procedures.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com