Europe Empty Capsules Market Research Report By Product, Therapeutic Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

Europe Empty Capsules Market Summary

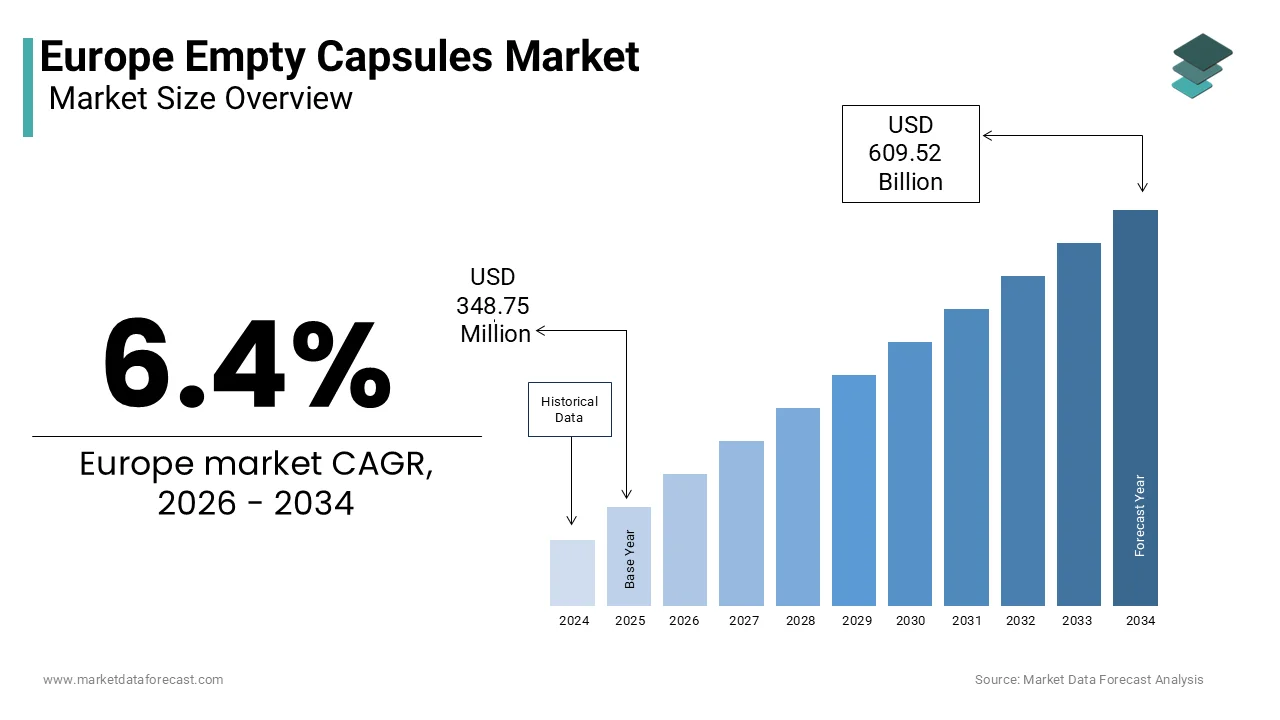

The Europe empty capsules market was valued at USD 348.75 million in 2025, is estimated to reach USD 371.07 million in 2026, and is projected to grow to USD 609.52 million by 2034, registering a CAGR of 6.4% from 2026 to 2034, driven by rising personalized medicine demand, expansion of nutraceutical private labels, growing adoption of plant-based capsules, and strict pharmacopoeial compliance across EU pharmaceutical production.

Key Market Highlights

- 2025 Market Size: USD 348.75 million

- 2026 Estimate: USD 371.07 million

- 2034 Forecast: USD 609.52 million

- CAGR (2026–2034): 6.4%

- Core Materials: Gelatin, HPMC (Hypromellose), Pullulan

- Primary End Users: Pharmaceutical manufacturers, Nutraceutical brands, Compounding pharmacies

Quick Growth Drivers

- Rapid expansion of personalized and compounded medicine across EU hospital pharmacies

- Strong shift toward plant-based HPMC capsules due to vegan, halal, and kosher demand

- Growth in private-label nutraceuticals across European retail chains

- Increasing elderly population requiring capsule-based easy-to-swallow formulations

- EMA and European Pharmacopoeia compliance strengthening standardized capsule demand

Principal Restraints

- Strict EU sourcing regulations for bovine gelatin under TSE frameworks

- Volatility in gelatin and cellulose pulp prices impacting cost predictability

- Limited global supply of EU-compliant bovine raw materials

- Pricing pressure from long-term pharmaceutical supply contracts

High-Value Opportunities

- Expansion of modified-release and dual-compartment capsule systems

- Growth of plant-based capsules in OTC and private-label supplements

- Capsule innovation for biologics and moisture-sensitive APIs

- Rising demand for halal- and kosher-certified capsule formats

- Increasing use of capsule delivery in antimicrobial stewardship programs

Key Market Challenges

- Limited EU manufacturing capacity for enteric-coated and barrier capsules

- High capital cost for advanced capsule coating infrastructure

- Fragmented religious certification standards across EU member states

- Regulatory complexity for pan-European product labeling

Fastest-Growing Segments

- Non-Gelatin Capsules: 10.5% CAGR — driven by vegan, halal, and clean-label adoption

- Nutraceutical End User: 11.4% CAGR — rapid retail and e-commerce supplement expansion

- Antibiotic & Antibacterial Applications: 8.84% CAGR — antimicrobial resistance strategies

- Vitamins & Dietary Supplements: Largest therapeutic share (35.9% in 2025)

- Pharmaceutical Industry: Largest end user (50.9% share in 2025)

Regional Leadership & Dynamics

- Germany (24.4%) — largest pharmaceutical production hub; strong compounding ecosystem

- United Kingdom — advanced nutraceutical retail chains; post-Brexit regulatory agility

- France — centralized healthcare model; halal-certified capsule demand growth

- Italy — high supplement consumption and aging population

- Spain — rapid private-label supplement expansion and vitamin demand

What Wins Commercially (Competitive Edge)

- Compliance with European Pharmacopoeia and EMA standards

- Expanded HPMC and pullulan portfolios

- Moisture-resistant and enteric-coated capsule technologies

- Strong distribution hubs within EU to ensure supply resilience

- Halal, kosher, and vegan certification transparency

Top Strategic Ask for Executives

- Expand plant-based capsule production capacity within Europe

- Invest in advanced modified-release and moisture-barrier capsule systems

- Secure diversified raw material sourcing to mitigate gelatin and HPMC volatility

- Align certification standards for broader pan-European labeling acceptance

- Target nutraceutical private-label growth channels for scalable volume demand

Leading Players

Some of the companies that are playing a dominating role in the Europe empty capsules market include:

- Lonza Group AG

- ACG Worldwide

- Qualicaps

- Suheung Co., Ltd.

- Bright Pharmacaps Inc.

- Medi-Caps Ltd.

- Sunil Healthcare Limited

Europe Empty Capsules Market Size

The Europe Empty Capsules Market was valued at USD 348.75 million in 2025, is expected to have 6.4% CAGR from 2026 to 2034, and be worth USD 609.52 million by 2034 from USD 371.07 million in 2026.

Empty capsules are shell containers primarily made from gelatin, hypromellose (HPMC), or pullulan and used to encapsulate solid or semi-solid pharmaceutical and nutraceutical formulations for oral delivery. Isemi-solidthey serve as a critical dosage form enabling precise dosing, masking of unpleasant tastes, and enhanced stability of active ingredients. The market operates under stringent regulatory oversight by the European Medicines Agency and national competent authorities, which mandate compliance with pharmacopoeial standards such as those outlined in the European Pharmacopoeia for capsule integrity, dissolution, and microbiological safety. According to the European Directorate for the Quality of Medicines, a large number of medicinal products authorized in the EU utilize hard capsules as their primary delivery system, spanning prescription drugs, over-the-counter remedies, and bespoke formulations from hospital pharmacies. Over-the-counter, Europe is home to thousands of compounding pharmacies, many of which rely on empty capsules for personalized medicine preparations. The shift toward plant-based alternatives has accelerated due to religious dietary laws, vegetarian consumer trends, and concerns over bovine spongiform encephalopathy, which is leading to the rapid adoption of HPMC capsules. With Europe accounting for a significant share of global pharmaceutical production, and a growing emphasis on patient-centric drug delivery, the empty capsules market functions as an essential therapeutic efficacy, regulatory compliance, and formulation innovation across the continent’s healthcare ecosystem.

MARKET DRIVERS

Rising Demand for Personalized and Compounded Medications Drives Capsule Consumption

The expansion of hospital and community-based compounding pharmacies across Europe has significantly increased demand for empty capsules as a versatile vehicle for personalized therapeutics, which is significantly fuelling the European empty capsules market growth. According to the European Association of Hospital Pharmacists, thousands of hospital pharmacies in the EU now offer compounding services, preparing tailored formulations for patients with rare diseases, allergies, or specific dosing needs. As per the French National Agency for Medicines and Health Products Safety, individualized capsule prescriptions dispensed by community compounding pharmacies have grown notably in recent years. These capsules often contain modified-release blends, hormone replacements, or pediatric formulations that are not commercially available. The European Pharmacopoeia mandates that all compounded capsules meet strict standards for uniformity, disintegration, and microbial limits, which is needing high quality empty shells. Additionally, countries like Germany and Italy have updated national regulations to support the use of compounded medicines in palliative and geriatric care, where swallowing whole tablets is challenging. This institutional endorsement, coupled with an aging population as per Eurostat, ensures sustained and growing reliance on empty capsules as a foundational tool in precision medicine delivery across Europe.

Growing Consumer Preference for Plant-Based and Clean Label Dosage Forms Accelerates HPMC Adoption

The increasing prevalence of vegetarianism, veganism, and religious dietary restrictions in Europe has catalysed a structural shift from animal-derived gelatin capsules to plant-based alternatives, primarily hypromanimal-derived which is further boosting the European empty capsules market expansion. According to the European Vegetarian Union, a large share of Europeans now identify as flexitarian, vegetarian, or vegan, with Germany, the United Kingdom, and Sweden leading adoption. This demographic trend directly influences pharmaceutical and nutraceutical formulation choices. The European Medicines Agency has approved HPMC capsules as bioequivalent to gelatin for most applications, enabling seamless substitution in both prescription and over-the-counter products. As per the Italian Ministry of Health, publicly funded nutraceuticals are now required to include a plant-based capsule option, impacting numerous product lines. Similarly, major pharmacy chains in the UK and Germany prioritize HPMC capsules in private label supplement ranges. Additionally, concerns about bovine spongiform encephalopathy and religious certification have made gelatin increasingly untenable for mass market products. As a result, manufacturers are reformulating across categories, driving robust demand for high-performance, pharmacopoeia-compliant empty HPMC capsules throughout the European health and wellness sector.

MARKET RESTRAINTS

Stringent Regulatory Requirements for Bovine Sourcing Limit Gelatin Capsule Availability

The European Union’s rigorous controls on animal-derived materials, particularly bovine gelatin, impose significant animal-derived constraints that restrict the availability and increase the cost of traditional empty capsules, which is a significant restraint to the growth of the European empty capsules market. According to the European Commission’s Regulation (EC) No 999/2001 on transmissible spongiform encephalopathies, gelatin used in pharmaceuticals must originate from countries classified as having negligible or controlled bovine spongiform encephalopathy risk, and from specified low-risk tissues. As per the European Food Safety Authority, only a limited nlow-risk countries worldwide meet the EU’s highest safety tier for bovine material import, which is reducing sourcing flexibility. Furthermore, each gelatin batch requires full traceability from slaughterhouse to capsule production, documented through veterinary health certificates and TSE declarations. The German Federal Institute for Drugs and Medical Devices has reported rejections of gelatin capsule imports due to incomplete documentation or origin from non-approved regions. These regulatory hurdles increase lead times and production costs, discouraging smaller supplement brands from using gelatin. While alternatives exist, the dependency on a narrow global supply of compliant bovine material creates ongoing vulnerability, particularly during geopolitical or health crises that disrupt trade flows.

Volatility in Raw Material Prices Impacts Production Cost Stability

The European empty capsules market faces persistent pressure from fluctuating prices of key raw materials, particularly gelatin and hypromellose, which are subject to agricultural, energy, and geopolitical influences. According to the European Gelatin Manufacturers Association, bovine hide prices have risen significantly in recent years, directly increasing gelatin production costs. Simultaneously, HPMC prices have surged due to rising cellulose pulp costs linked to energy-intensive processing and supply chain disruptions in wood fiber markets. As per the European Chemicals Agency, HPMC import costs from key Asian suppliers have increased notably due to export restrictions and shipping bottlenecks. These price swings are difficult to absorb in a competitive market where capsule pricing is often fixed under long-term contracts with pharmaceutical clients. Smaller European capsule fillers, which lack the scale to hedge or vertically integrate, are particularly vulnerable. As a result, some manufacturers have reduced product variety or delayed plant-based capsule expansion, slowing innovation and limiting formulator options. Until raw material sourcing stabilizes or alternative polymers achieve cost parity, price volatility will remain a structural restraint on market predictability and growth.

MARKET OPPORTUNITIES

Expansion of Modified Release and Combination Drug Formulations Creates New Capsule Applications

The pharmaceutical industry’s shift toward advanced drug delivery systems is opening significant opportunities for specialized empty capsules capable of modified release, dual compartment filling, or enhanced stability. According to the European Medicines Agency, a considerable share of new molecular entities approved in the EU in recent years utilized hard capsules for controlled or delayed release, leveraging technologies such as enteric coatings, pellet blends, or moisture barrier shells. Companies like Capsugel (now Lonza) and ACG have developed capsules with tailored disintegration profiles to protect acid-sensitive drugs or enable targeted intestinal delivery. As per the Europacid-sensitive, initiatives under Horizon Europe are supporting the development of capsules that release APIs in response to pH or enzymatic triggers, particularly for biologics and peptides. Additionally, dual-chamber capsules are gaining traction for antibiotic combinations and dual-chamber blends. With Europe hosting a majority of global clinical trials involving novel oral delivery systems, as per the European Clinical Research Infrastructure Network, the demand for high-precision, functionally enhanced empty capsules is set to grow substantially in the innovator and generic sectors.

Growth of Private Label Nutraceuticals in Retail Channels Boosts Standard Capsule Demand

The proliferation of store-brand vitamins, minerals, and herbal supplements across European supermarkets and pharmacies is creating a high volume, consistent demand stream for standard empty capsules, particularly in plant-based formats, which is another promising opportunity in the European empty capsules market. According to the European Specialist Dietary Food Association, private label nutraceutical sales have grown significantly, with major retailers like Carrefour, Tesco, and dm-drogerie expanding their supplement portfolios as proprietary brands. These products predominantly use size zero or size one HPMC capsules due to their visual clarity, stability, and consumer acceptance. The shift is driven by margin optimization and consumer trust in retailer quality control. As per the European Consumer Organisation, a majority of supplement buyers perceive private label capsules as equally effective as national brands. Retailers collaborate with contract fillers who source empty capsules in bulk, creating economies of scale that favor standardized sizes and shell types. This channel not only absorbs significant capsule volume but also accelerates the normalization of plant-based delivery forms among mainstream consumers. As health consciousness rises and retail competition intensifies, private label expansion will continue to serve as a resilient demand engine for the European empty capsules market.

MARKET CHALLENGES

Shortage of Specialized Manufacturing Capacity for Advanced Capsule Types Limits Innovation Uptake

Despite growing demand for functional capsules, Europe faces a critical bottleneck in specialized production infrastructure capable of manufacturing these advanced shells at scale, which is a significant challenge to the growth of the European empty capsules market. According to the European Federation of Pharmaceutical Industries and Associations, only a limited number of capsule manufacturers in the EU possess the technology to produce enteric or barrier-coated empty capsules, with most capacity concentrated in a few countries. This scarcity forces drug developers to rely on a restricted pool of suppliers, leading to extended lead times for custom orders. As per the Dutch Medicines Evaluation Board, marketing authorization applications for modified release products have experienced delays due to capsule supply constmodified-releaseally, the high capital cost of coating and encapsulation lines deters new entrants, especially in Southern and Eastern Europe. While demand for differentiated delivery systems rises, the lack of accessible, GMP-compliant manufacturing capacity for advanced capsules constrains formula development and slows time to market for next-generation oral therapeutics across the region.

Inconsistent Religious and Ethical Certification Standards Fragment Consumer Trust

The absence of harmonized halal, kosher, and vegan certification frameworks for empty capsules across Europe undermines consumer confidence and complicates cross-border product launches, which further challenges the expansion of the European empty capsules market. According to the European Halal Development Agency, millions of Muslims in the EU require halal-certified medicines, yet no single EU-wide standard exists for gelatin halal-certifying verification. Similarly, kosher certification is managed by disparate rabbinical authorities in France, the UK, and Germany, each with varying requirements for equipment segregation and ingredient scrutiny. Even for HPMC capsules, vegan claims lack a legal definition under EU Regulation (EC) No 1169/2011, allowing inconsistent labeling practices. As per the European Consumer Organisation, a notable share of plant-based capsules marketed as “vegan” lacked third-party certification, leading to consumer skepticism. Pharmaceutical companies, therefore, navigate a patchwork of national and religious standards, increase compliance costs, and limitpan-Europeann branding. Until the European Commission establishes u,nified guipan-Europeanethical capsule labeling, market fragmentation and trust gaps will persist, hindering the full potential of inclusive dosage form adoption across diverse European populations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Therapeutic Application, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Capsugel, ACG Worldwide, Suheung Co Ltd., Bright Pharmacaps Inc., Capscanada Corporation, Medi-Caps Ltd., Qualicaps, Roxlor, LLC, Snail Pharma Industry Co.Ltd, and Sunil Healthcare Limited. |

SEGMENTAL ANALYSIS

By Product Insights

The gelatin capsules segment held 55.9% of the European market share in 2025. The dominating position of gelatin capsules in the European market is driven by their superior mechanical properties, decades-long regulatory acceptance, and widespread use in pharmaceutical form. Despite ethical and dietary concerns, gelatin remains the gold standard for capsule performance due to its excellent film-forming ability, rapid dissolution in gastric fluid, and high compatibility with active ingredients. According to the European Pharmacopoeia, thousands of monographs for solid oral dosage forms specify gelatin as the preferred shell material, reflecting its entrenched position in drug development pipelines. Major European pharmaceutical manufacturers, including Novartis and Sanofi, continue to rely on gelatin for antibiotics, cardiovascular drugs, and hormone therapies where stability and bioavailability are critical. The European Medicines Agency has not identified safety issues with pharmaceutical-grade gelatin sourced from TSE-controlled regions, ensuring copharmaceutical-grade gelatin is significantly more cost-effective than plant-based alternatives, which makes them indispensable volume generic drugs. This combination of performance, regulatory validation, and economic efficiency maintains gelatin as the dominant product type across Europe’s pharmaceutical landscape.

The non- gelatin capsules segment represents the fastest growing segment and is estimated to record a CAGR of 10.5% over the forecast period, owing to the rising consumer demand for vegetarian, vegan, halal, and kosher compliant dosage forms, amplified by regulatory and retail trends. According to the European Vegetarian Union, the number of Europeans identifying as vegan or vegetarian has increased significantly, with Germany, Sweden, and the Netherlands leading adoption. In response, major pharmacy chains like dm in Germany and Boots in the United Kingdom now require all private label supplements to use hypromellose (HPMC) capsules. The European Commission’s update to the Nutraceutical Guidelines encourages clear labeling of capsule origin, indirectly promoting plant-based options. Religious communities are also exerting influence, with halal and kosher compliance driving demand for non-gelatin shells. Innovations in HPMC technology have narrowed the performnon-gelatinth gelatin, enabling broader pharmaceutical use. As ethical consumption and inclusivity become non-negotiable in European health markets, non-gelatin capsules are transitioning from niche alternatives to mainstream standards.

By Therapeutic Application Insights

The vitamins and dietary supplements segment occupied 35.9% of the regional market share in 2025. The leading position of the vitamins and dietary supplements segment in the European market is attributed to the region’s robust nutraceutical industry and growing consumer focus on preventive health. According to the European Specialist Dietary Food Association, the EU nutraceutical market is valued at tens of billions of euros, with a majority of products delivered in capsule form due to ease of swallowing, taste masking, and dose precision. According to the European Consumer Organisation, a significant share of adults in Western Europe regularly consume dietary supplements, with multivitamins, omega-3, and vitamin D being the most popular. Retailers have capitalized on this trend, with Carrefour in France and Tesco in the UK allocating entire aisles to private label capsules, which is driving bulk procurement of empty shells. Additionally, the rise of personalized nutrition has spurred demand for compounding pharmacies to fill custom vitamin blends into empty capsules. The European Food Safety Authority has validated capsule delivery as optimal for fat-soluble vitamins like A, D, and E. This convergence of public health awarfat-solubleil strategy, and scientific endorsement ensures vitamins and dietary supplements remain the dominant therapeutic application segment.

The antibiotic and antibacterial drugs segment is the fastest-growing therapeutic segment and is anticipated to register a CAGR of 8.84% over the forecast period, owing to Europe’s intensified efforts to combat antimicrobial resistance through optimized dosing and patient adherence, where capsules play a critical role. According to the European Centre for Disease Prevention and Control, infections caused by antibiotic-resistant bacteria remain a major public health challenge, promptiantibiotic-resistantlans that emphasize precise dosing and complete treatment courses. Capsules enable accurate delivery of narrow-spectrum antibiotics, reducing side effects and improving compliance. Narrow-spectrumols in countries like Italy and Spain now mandate capsule-based formulations for outpatient antibiotic therapy to minimize dosicapsule-basedrthermore, the European Medicines Agency’s guidance on pediatric antimicrobials recommends capsule sizes tailored for age-appropriate dosing, driving reformulation of existing products. With the EU allocating significant funding under the One Health Action Plan to strengthen antimicrobial stewardship, capsule-based antibiotic delivery is becoming a strategic tool in public healcapsule-basedich is, fuelling sustained demand across Europe.

By End User Insights

The pharmaceutical segment dominated the European empty capsules market in 2025 with 50.9% of the regional market share. Europeanominance of the pharmaceutical segment in the European market is driven by stringent regulatory requirements, high volume production, and the irreplaceable role of capsules in drug delivery. According to the European Medicines Agency, a large share of new oral solid dosage forms approved in the EU in recent years utilized hard capsules, particularly for drugs requiring taste masking, moisture protection, or modified release profiles. Major manufacturers like Novartis in Switzerland, Bayer in Germany, and Servier in France operate dedicated capsule filling lines producing billions of units annually for both branded and generic products. The European Pharmacopoeia mandates rigorous testing for capsule disintegration, content uniformity, and microbial limits, ensuring consistent demand for high-quality empty shells. Furthermore, hospital pharmacies across the EU relhigh-qualihigh-qualityapsules for compounding personalized therapies. The industry’s commitment to patient-centric design, especially for geriatric and pediatric populations with patient-centric tablets, reinforces capsules as a preferred dosage form. This regulatory, therapeutic, and demographic foundation solidifies the pharmaceutical sector as the primary end user in the European market.

The nutraceutical segment is the fastest-growing end-user segment and is projected to grow at a CAGR of 11.4% fastest-growing end-user, owing to the rising health consciousness, preventive care trends, and the exponential growth ofprivate-labell supplements in retail and e-commerce channels. According to the European Health and Fitness Association, a majority of Europeans now prioritize daily supplementation for immunity, energy, and longevity, with capsules being the preferred format due to convenience and perceived purity. Major retailers have responded aggressively, with dm-drogerie in Germany launching numerous new HPMC capsule-based supplements, while Holland & Barrett in the Netherlands has experienced growth in plant-based capsule sales. The European Commission’s Nutraceutical Transparency Initiative mandates clearer labeling of capsule composition, accelerating the shift to non-gelatin options. Additionally, the rise of personalized nutrition platfornon-gelatinthose offered by ZOE in the UK, uses empty capsules to deliver custom microbiome-tailored blends. As wellness becomes embedded in everyday consumermicrobiome-tailoredaceutical sector is emerging as the most dynamic and rapidly expanding end user of empty capsules in Europe.

COUNTRY LEVEL ANALYSIS

Germany Empty Capsules Market Analysis

Germany led the European empty capsules market with 24.4% of the regional market share in 2025. The dominance of Germany in the European market is attributed to its status as the continent’s largest pharmaceutical producer and a hub for compounding pharmacies. The country hosts numerous pharmaceutical manufacturing sites, including global leaders like Bayer and Merck, which consume billions of empty capsules annually for prescription drugs and over-the-counter medicines. According to the German Federal Institute for Drugs and Medical Devices, thousands of hospital and community pharmacies engage in compounding, preparing large volumes of individualized capsule prescriptions each year. Germany enforces strict quality standards under the German Medicinal Products Act, requiring all capsules to comply with European Pharmacopoeia specifications. The rise of veganism has accelerated the adoption of HPMC capsules in both the pharma and supplement sectors. With robust manufacturing infrastructure, regulatory rigor, and evolving consumer preferences, Germany remains the anchor market for empty capsules in Europe.

United Kingdom Empty Capsules Market Analysis

The United Kingdom held the second-largest share of the European empty capsules market in 2025. The growtsecond-largest the second-largest European market can be credited to its advanced nutraceutical sector, strong retail pharmacy networks, and post Brexit regulatory autonomy. According to the UK’s Office for National Statistics, a majority of adults regularly consume dietary supplements, with capsules representing most of the format mix. Major chains like Boots and Holland & Barrett have shifted their private label ranges entirely to non-gelatin capsules, citing consumer demand for ethical and allergen-free options. The Medicines and Healthcare products Regulatory Agency maintains alignment with European Pharmacopoeia standards while allowing faster approval of novel capsule types, enabling innovation. The National Health Service has expanded compounding services for hormone replacement and pediatric therapies, increasing demand for high-quality empty shells. Additionally, the UK’s departure from the EU has shigh-qualitytic capsule manufacturing investments to ensure supply chain resilience. This blend of consumer behavior, retail influence, and regulatory agility sustains the United Kingdom’s position as a high-growth and high-adoption market.

France Empty Capsules Market Analysis

Fhigh-growthtimated to showcase a promising CAGR in the European empty capsules market during the forecast period, owing to its centralized healthcare system and strong emphasis on pharmaceutical quality. According to the French National Agency for Medicines and Health Products Safety, compounded capsule prescriptions are dispensed in large volumes annually, primarily for dermatological, hormonal, and pediatric applications. France is also home to major pharmaceutical companies like Sanofi and Ipsen, which rely on gelatin and HPMC capsules for global drug portfolios. The French government’s Nutraceutical Charter mandates clearer labeling of capsule origin, accelerating the transition to plant-based shells in supplements. Retailers such as Monoprix and Pharmacie Principale now require third-party certification for all capsule-based products, enhancing consumerthird-partythermore, France’s Muslicapsule-baseddrives demand for halal-certified non-gelatin capsules. This intersection of public health policy, religious inclusivity, and industrial scale ensures France’s continued relevance in the European empty capsules landscape.

Italy Empty Capsules Market Analysis

Italy is predicted to record a healthy CAGR in the European market during the forecast period. Italy is distinguished by its high supplement consumption and aging population. According to the Italian National Institute of Statistics, a majority of older adults use daily vitamins or mineral supplements, with capsules being the preferred format due to ease of swallowing. Italy also has one of Europe’s highest densities of pharmacies, many of which offer compounding services for customized therapies. The Italian Medicines Agency has reported that antibiotic capsules represent a fast-growing prescription segment due to national antimicrobial stewardship programs. Additionally, Italy’s Catholic and Muslim communities influence capsule selection; while gelatin remains common, demand for certified non-gelatin options is rising rapidly in urban centers. The Ministry of Health’s guidelines on nutraceutical transparency further support clear labeling, benefiting plant-based capsule producers. With deep-rooted health traditions and demographic pressures, Italy maintains a consistent and evolving demand for both traditional and innovative empty capsules.

Spain Empty Capsules Market Analysis

Spain is expected to account for a notable share of the European empty capsules market over the forecast period. Spain is experiencing accelerated growth due to rising health awareness and retail-driven supplement adoption. According to the Spanish Agency for Medicines and Medical Devices, millions of Spaniards regularly consume dietary supplements, with private label capsules from chains like Farmacity and Druni dominating sales. The country’s warm climate and aging population drive high demand for vitamin D and antioxidant formulations, almost exclusively delivered in capsule form. Spain also has a significant Muslim community, driving demand forhalal-certified non-gelatinn capsules. The Ministry of Health has updated its compounding regulations to support personalized medicine in chronic disease management, boosting hospital pharmacy capsule use. Additionally, Spain’s role as a tourist destination has spurred hotel and wellness center partnerships with local supplement brands, creating new distribution channels. With improving health literacy and diversifying consumer needs, Spain is emerging as a dynamic and expanding market for empty capsules in Southern Europe.

COMPETITIVE LANDSCAPE

Europeanrope empty capsules market features a competitive landscape shaped by stringent quality standards,s evolving consumer preferences, es and technological differentiation. Global leaders, ers like Lonza ACG and Catale, n dominate due to their integrated manufacturing capabilities, regulatory expertise,e and broad product portfolios. Competition isno price-basedd but centers on shell performance, reliability, and compliance with European Pharmacopoeia and EMA guidelines. The market i,s bifurcated between traditional gelatin capsules valued for their dissolution and cost efficiency and plant-based alternatives driven by vegetari, an v e, gan and religious demands. Small and mid-sized manufacturers struggle to match the scale and certification depth of incumbents, ts particularly in advanced segments, moisture-resistant or modified r,elease capsules. Regulatory fragmentation adds complexity but also creates opportunities for agile players with localized compliance strategies. Innovation is increasingly focused on functional enhancements and sustainable sourcing as Europe prioritizes patient-centric, inclusive,e and environmentally responsible healthcare solutions. This dynamic environme,nt rewards companies that balance scientific rigor with market responsiveness.

KEY MARKET PLAYERS

A few noteworthy companies operating in the European empty capsules market profiled in this report are

- Capsugel

- ACG Worldwide

- Suheung Co. Ltd.

- Bright Pharmacaps Inc.

- Capscanada Corporation

- Medi-Caps Ltd.

- Qualicaps

- Roxlor, LLC

- Snail Pharma Industry Co., Ltd.

- Sunil Healthcare Limited

TOP LEADING PLAYERS IN THE MARKET

- Lonza Group AG is a Swiss-headquartered global leader in capsule technology, renowned for its CapSwiss-headquarteredffers a comprehensive portfolio of gelatin, HPMC, and specialty empty capsules. The company supplies pharmaceutical and nutraceutical customers across Europe with high-quality shells compliant with European Pharmacopoeia and FDA standards. high-quality expanded its plant-based capsule production capacity at its Colmar, France,e, facility to meetplant-basedand for vegan halal-certified dosage forms. The company also launched a new line of moisture-resistant HPMC capsules designed for hygroscopic actives, addressingmoisture-resistant challenge. Through continuous innovation in shell performance, regulatory engagement, and sustainable sourcing, Lonza reinforces its position as a trusted partner in advanced oral drug delivery across the European market.

- ACG Worldwide maintains a strong presence in the European capsules market through its ACG Capsules division, offering both European shells manufactured in GMP-certified facilities in India. ACG CCapsules catersto pharmapharmaceuticalcompounding pharmacy clients with a focus on quality, consistency,y and technical support. In 2023, ACG introduced a new transparent HPMC capsule with enhanced mechanical strength and improved sealing technology to preventleakage off semi-solid fillings. The firm also strengthened its European distribution network by establishing a dedicated logistics hub in the Netherlands to ensure rapid delivery and supply chain resilience. By combining manufacturing excellence with responsive service, ACG continues to gain traction among mid-sized and specialty formulators across the region.

- Catalent Inc leverages its global drug delivery expertise to serve the European empty capsules market with a focus on advanced formulations and integrated solutions. The company offers a range of gelatin and plant-based capsules, including specialized formats for modified release and dual-compartment delivery. In early 2024, Catalent enhanced its European capsule filling capabilities at its facility in Belgium to support clinical and commercial programs requiring high containment or potent compounds. The firm also collaborates with European biotech firms to develop capsule-based delivery systems for peptide and small-molecule therapeutics. Through vertical integration from capsule manufacturing to final packaging, Catalent provides end-to-end solutions that align with Europe’s emphasis on quality, innovationend-to-endent centric design in oral dosage forms.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European empty capsules market focus on product diversification, regulatory compliance, and sustainable innovation to strengthen their positions. Companies invest in expanding plant-based capsule portfolios, including HPMC and pullulan, to meet ethical and religious consumer demands. They enhance shell function,ality through moisture barrier technology, enteric coatings, and improved sealing mechanisms to support complex formul,ations. Strategies and capacity expansions in Europe ensure supply chain security and faster delivery. Collaboration with pharmaceutical and nutraceutical clients enables co-development of customized capsule solutions. Compliance with European Pharmacopoeia, EM, A, and national regulatory standards remains paramount. Additionally, firms, pu,rsue sustainability through traceable raw material sourcing and reduced environmental impact in manufacturing. These strategies collectively address Europe’s evolving needs for quality, ty inclusiv,ity and therapeutic efficacy in oral solid dosage forms.

MARKET SEGMENTATION

This research report on the European empty capsules market has been segmented and sub-segmented into the following categories.

By Product

- Gelatin Capsules

- Non-Gelatin Capsules

By Therapeutic Application

- Antibiotic And Antibacterial Drugs

- Vitamins And Dietary Supplements

- Antacid And Antiflatulent Preparations

- Antianemic Preparations

- Anti-Inflammatory Drugs

- Cardiovascular Therapy Drugs

- Cough And Cold Preparations

- Other Therapeutic Application

By End User

- Pharmaceutical Industry

- Nutraceutical Industry

- Cosmetics Industry

- Research Laboratories

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the main types in the Europe Empty Capsules Market?

In the Europe Empty Capsules Market, primary types include gelatin capsules, which dominate due to their established use, and non-gelatin or vegetarian capsules made from HPMC or plant-based materials. Gelatin offers superior performance in dissolution, while vegetarian options cater to vegan preferences and allergen-free needs in the pharmaceutical sector.

2. Who are the leading players in the Europe Empty Capsules Market?

Leading players in the Europe Empty Capsules Market include Lonza/Capsugel, Qualicaps Europe, and various regional manufacturers focusing on pharmaceutical-grade capsules. These companies maintain production sites across Europe, emphasizing quality standards and innovations in vegetarian capsules for nutraceutical applications. They compete through capacity expansion and regulatory compliance.

3. What drives the Europe Empty Capsules Market?

The Europe Empty Capsules Market is driven by rising demand in pharmaceuticals for capsule-based formulations and growth in nutraceuticals for health supplements. Factors include increasing chronic disease prevalence requiring easy-to-swallow dosage forms and preference for clean-label products. Pharmaceutical contract manufacturing also boosts usage across the EU.

4. Which countries lead the Europe Empty Capsules Market?

Germany leads the Europe Empty Capsules Market, followed by the UK, France, Italy, and Spain, due to strong pharmaceutical infrastructure and nutraceutical production. The Netherlands shows rapid growth from contract services. Rest of Europe contributes significantly through diverse operations.

5. What is the difference between gelatin and vegetarian capsules in the Europe Empty Capsules Market?

In the Europe Empty Capsules Market, gelatin capsules from animal sources provide excellent dissolution and cost-effectiveness for pharmaceuticals, while vegetarian capsules use HPMC for plant-based, allergen-free options popular in nutraceuticals. Vegetarian variants grow faster due to vegan trends and clean-label demands.

6. What applications dominate the Europe Empty Capsules Market?

Pharmaceuticals dominate the Europe Empty Capsules Market as the primary end-user, followed by nutraceuticals, cosmetics, and research. Capsules enable taste-masking for drugs and delivery of dietary supplements, with emphasis on generics and high-quality formulations.

7. Why prefer vegetarian capsules in the Europe Empty Capsules Market?

Vegetarian capsules in the Europe Empty Capsules Market appeal due to their plant-based composition, suiting vegan consumers and avoiding allergens like pork or beef gelatin. They offer similar performance in dissolution and are increasingly adopted in nutraceuticals and pharmaceuticals for clean-label compliance.

8. How does regulation impact the Europe Empty Capsules Market?

Strict EU regulations ensure safety and quality in the Europe Empty Capsules Market, covering material sourcing, manufacturing standards, and labeling for pharmaceutical use. Compliance with EMA guidelines supports trust in capsules for drugs and supplements, influencing manufacturer investments.

9. What role do nutraceuticals play in the Europe Empty Capsules Market?

Nutraceuticals significantly contribute to the Europe Empty Capsules Market by using capsules for vitamins, herbal extracts, and dietary supplements. Rising health consciousness drives demand for convenient, masked-taste formats in this fast-growing segment alongside pharmaceuticals.

10. Are there innovations in the Europe Empty Capsules Market?

Innovations in the Europe Empty Capsules Market include advanced vegetarian formulations, improved dissolution rates, and sustainable plant-based materials. Manufacturers invest in automation and specialized sizes for better pharmaceutical compatibility and nutraceutical delivery.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com