Europe Field Service Management Market Size, Share, Trends, and Growth Analysis Report, Segmented by Deployment Type, Organization Size, Solution & Service Type, End-user Vertical, and Country – Industry Forecast From 2026 to 2034

Europe Field Service Management Market Report Summary

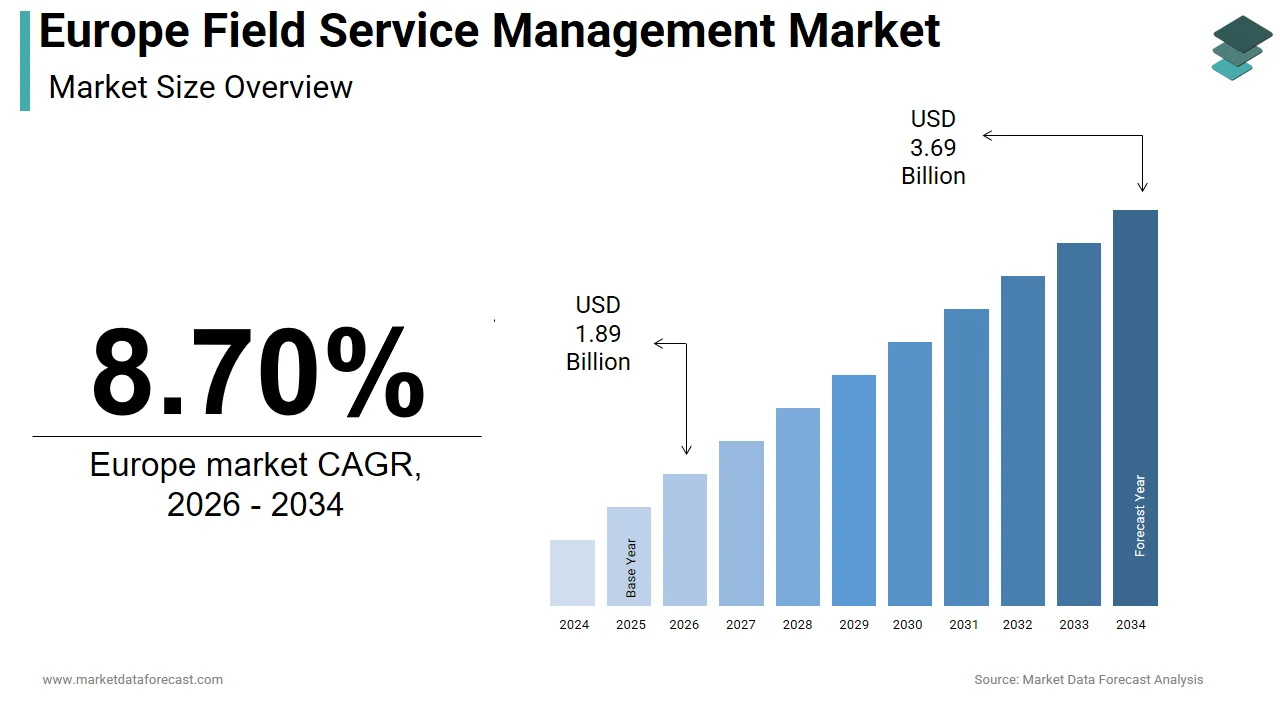

The Europe field service management market was valued at USD 1.74 billion in 2025 and is projected to grow from USD 1.89 billion in 2026 to USD 3.69 billion by 2034, expanding at a CAGR of 8.70% from 2026 to 2034. Market growth is driven by increasing demand for real-time workforce optimization, predictive maintenance, remote diagnostics, and mobile-first service platforms across industrial, utility, telecom, and facilities sectors. The rapid adoption of cloud computing, AI-driven scheduling, and IoT-enabled asset monitoring is accelerating the digital transformation of field operations across Europe.

Key Market Trends

- Rising adoption of cloud-based and mobile FSM platforms

- Integration of IoT and predictive analytics for proactive maintenance

- Growing demand for remote service and augmented reality support tools

- Expansion of AI-powered dispatching and route optimization

- Increasing focus on service-level agreement (SLA) compliance and customer experience

Segmental Insights

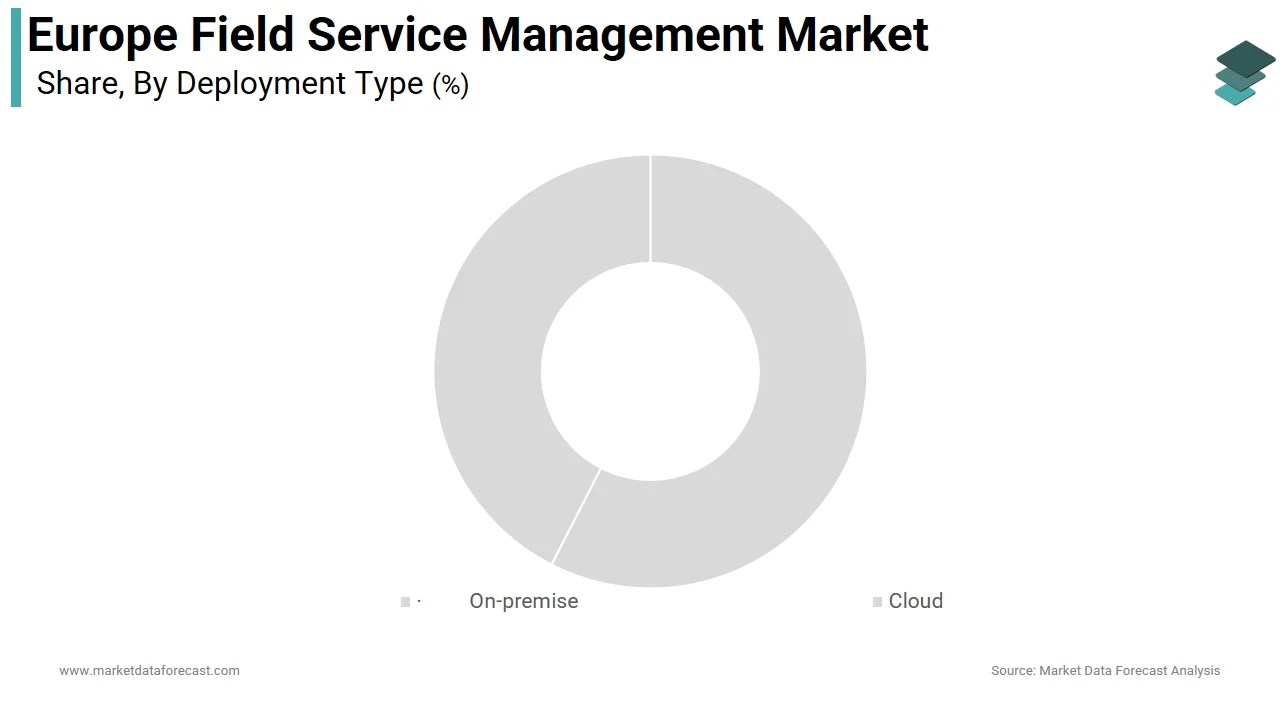

- Based on deployment type, the cloud deployment segment dominated the market with 66.9% share in 2025, driven by scalability, lower infrastructure costs, faster deployment, and seamless integration with enterprise systems

- Based on organization size, the large enterprises segment led the market with 60.5% share in 2025, supported by high service volumes, complex asset networks, and strong investment capacity.

- Based on end-user vertical, the facilities management segment held the largest share at 33.8% in 2025, driven by the growing outsourcing of building maintenance, HVAC services, and smart infrastructure management.

Regional Insights

The European field service management market shows strong concentration in major industrial and service-driven economies.

- Germany led the market with 23.3% share in 2025, supported by its strong manufacturing base, industrial automation adoption, and emphasis on operational efficiency.

- The United Kingdom accounted for 15.8% share, driven by telecom, utilities, and facilities outsourcing sectors.

- France is expected to register the fastest growth during the forecast period, supported by smart infrastructure investments, public sector digitization, and industrial modernization programs.

Competitive Landscape

The Europe field service management market is highly competitive and technology-driven, dominated by global enterprise software providers and specialized FSM vendors. Competition centers on AI-driven scheduling, mobile workforce enablement, system integration, and analytics capabilities. Leading vendors are expanding their portfolios through cloud-native architectures, industry-specific modules, and ecosystem partnerships. Integration with ERP, CRM, and IoT platforms has become a critical differentiator. Vendors are also investing in augmented reality, remote assistance, and automation tools to enhance technician productivity and reduce service costs.

Key players operating in the market include Oracle, ServiceNow, Salesforce, Microsoft, SAP, IFS, and others.

Europe Field Service Management Market Size

The size of the Europe field service management market was worth USD 1.74 billion in 2025. The regional market is anticipated to grow at a CAGR of 8.70% from 2026 to 2034 and be worth USD 3.69 billion by 2034 from USD 1.89 billion in 2026.

Field service management refers to the orchestration and optimization of on-site technical operations through digital platforms that coordinate workforce deployment, scheduling, inventory tracking, and customer engagement. The market has evolved beyond basic dispatch tools into integrated ecosystems powered by artificial intelligence, Internet of Things connectivity, and real-time analytics. As European economies prioritize operational resilience and service excellence, industries such as utilities, telecommunications, healthcare, and industrial manufacturing increasingly rely on field service solutions to maintain asset uptime and meet stringent regulatory expectations. As per Eurostat, the total employment in the European Union reached more than 160 million persons in 2024, which is showing steady growth compared to previous years. According to the European Commission, small and medium-sized enterprises account for nearly 99% of all businesses in the EU and provide jobs to more than 85 million citizens. This dense network of service-dependent enterprises underpins the structural relevance of field service management across the region.

MARKET DRIVERS

Accelerated Adoption of Predictive Maintenance Technologies

European industries are rapidly integrating predictive maintenance strategies to minimize unplanned downtime and extend asset life cycles, which is significantly driving the European field service management market. Predictive maintenance relies heavily on field service management platforms to translate sensor-driven insights into actionable technician workflows. As per the International Energy Agency, industrial facilities in Europe lose a significant share of their total energy consumption due to inefficient or poorly maintained equipment, which translates into billions of euros in avoidable costs annually. In response, manufacturers and utilities are deploying condition monitoring systems that feed data directly into field service software, which is enabling dynamic work order generation. Germany, for instance, hosts over 170,000 medium-sized industrial firms known as the Mittelstand, many of which have adopted Industry 4.0 protocols that embed predictive diagnostics into daily operations. As per the Fraunhofer Institute, German manufacturers using predictive maintenance reported notable reductions in machine failures and maintenance expenses within two years. This shift not only increases demand for intelligent field service platforms but also necessitates seamless integration with enterprise asset management and ERP systems. Consequently, vendors offering AI-enabled forecasting and automated technician dispatch capabilities are gaining traction, particularly in sectors where equipment reliability directly impacts safety and compliance, such as energy and healthcare.

Escalating Labor Shortages in Skilled Technical Roles

Europe faces a deepening shortage of qualified field technicians, which intensifies reliance on digital coordination tools to maximize workforce productivity, which is further supporting the expansion of the European field service management market. As per Eurofound, many European companies in construction, manufacturing, and utilities reported difficulties filling skilled trades positions, with the gap most acute in Germany, France, and Italy. This scarcity stems from demographic shifts, including an aging workforce and insufficient vocational training pipelines. In Germany, the Federal Employment Agency estimates that by 2030 the country will face a shortfall of more than 250,000 skilled maintenance workers. Field service management systems mitigate this constraint by optimizing route planning, automating knowledge transfer through augmented reality manuals, and enabling remote diagnostics that reduce the need for physical site visits. As per TNO, the Netherlands Organisation for Applied Scientific Research, technicians in the Netherlands can now resolve a considerable share of HVAC issues remotely using guided troubleshooting modules embedded in field service applications. These capabilities allow fewer technicians to manage larger service territories while maintaining service level agreements. Consequently, organizations are investing in platforms that support upskilling through in-app training modules and real-time expert collaboration features, thereby transforming field service management from a logistical tool into a strategic workforce augmentation platform.

MARKET RESTRAINTS

Data Privacy and Cross-Border Compliance Complexities

The fragmented regulatory landscape governing data handling across European jurisdictions poses a significant barrier to unified field service operations. While the General Data Protection Regulation establishes baseline privacy standards, national interpretations and sector-specific mandates create compliance friction, especially for multinational service providers. According to the European Data Protection Board, hundreds of cross-border GDPR enforcement actions were initiated between 2023 and 2025, with fines exceeding billions of euros collectively. Field service platforms routinely process sensitive information, including customer locations, biometric verification data, and equipment telemetry, which may be classified as personal data under local laws. In France, the National Commission on Informatics and Liberty requires explicit consent for geolocation tracking of service personnel, while in Sweden, the Data Inspection Authority mandates on-premises data storage for public sector contracts. These divergences compel vendors to develop region-specific configurations, increasing deployment costs and delaying time to value. As per the Centre for European Policy Studies, a majority of European service firms operating in three or more countries reported having to modify their digital workflows to satisfy local data residency requirements. Such fragmentation discourages smaller providers from scaling across borders and forces enterprises to maintain parallel systems, undermining the efficiency gains promised by cloud-based field service management. Until harmonization advances, compliance overhead will remain a persistent restraint on market cohesion and innovation velocity.

High Integration Costs with Legacy Enterprise Systems

Many European organizations operate on decades-old enterprise resource planning and customer relationship management infrastructures that lack native compatibility with modern field service platforms, which is further impeding the growth of the European field service management market. Replacing these systems is often prohibitively expensive or operationally disruptive, particularly in capital-intensive sectors like utilities and rail transport. As per the European Investment Bank, a large share of industrial firms in Central and Eastern Europe still relies on ERP systems installed before 2010, with limited API support. Integrating contemporary field service solutions with such environments demands custom middleware, extensive testing, and prolonged change management cycles. For instance, Deutsche Bahn, the German national railway operator, spent more than 18 months and 45 million euros integrating its field maintenance operations with a new digital platform due to dependencies on legacy mainframe systems. As per the VDMA, the German Mechanical Engineering Industry Association, many mid-sized manufacturers delayed field service digitization because integration costs exceeded initial software licensing expenses by a factor of three or more. These financial and temporal burdens disproportionately affect small and medium enterprises, which lack dedicated IT transformation budgets. Consequently, adoption remains uneven, with early movers concentrated in digitally mature markets like the Nordics, while others lag despite recognizing the operational benefits. Until low-code integration frameworks and standardized industrial data protocols gain wider adoption, this technical inertia will continue to suppress market penetration.

MARKET OPPORTUNITIES

Expansion of Circular Economy Mandates Driving Service-Centric Business Models

European Union policies promoting product longevity and resource efficiency are compelling manufacturers to shift from transactional sales to outcome-based service contracts, which is a promising opportunity in the European field service management market. Under the EU Circular Economy Action Plan, companies are incentivized to retain ownership of products and deliver performance as a service, which inherently increases demand for sophisticated field service coordination. As per the European Environment Agency, a large share of electrical and electronic equipment placed on the EU market in 2024 was covered by extended producer responsibility schemes requiring manufacturers to manage end of life recovery and, in many cases, ongoing maintenance. This paradigm shift is evident in sectors like industrial machinery, where companies such as Siemens and Schneider Electric now offer availability-based contracts guaranteeing uptime rather than selling standalone hardware. To fulfil these commitments, firms deploy field service management systems that track asset health, schedule preventive interventions, and document compliance with environmental regulations. In the Netherlands, the government reported that many manufacturing firms introduced product-as-a-service models between 2022 and 2025, directly linked to national circular economy roadmaps. These arrangements generate recurring service events and necessitate granular visibility into technician performance, parts usage, and customer satisfaction metrics. Consequently, field service platforms that support contract lifecycle management and sustainability reporting are emerging as critical enablers of regulatory alignment and competitive differentiation in Europe’s evolving industrial landscape.

Rise of Distributed Renewable Energy Infrastructure Requiring Agile Field Coordination

The rapid decentralization of Europe’s power grid, which is driven by rooftop solar, community wind farms, and battery storage hubs, has created a vast new domain for field service operations, and this is another potential opportunity in the European field service management market. Unlike centralized fossil fuel plants, renewable assets are geographically dispersed, often located in remote or residential areas, demanding highly responsive and geospatially intelligent service models. According to the European Network of Transmission System Operators for Electricity, millions of distributed energy resources were connected to European grids by 2025, which is representing a sharp increase since 2020. Each installation requires periodic inspection, firmware updates, and fault resolution, often within strict service windows to maintain grid stability and subsidy eligibility. In Spain, the Ministry for Ecological Transition mandates that solar inverter faults be addressed promptly to avoid penalties under renewable incentive programs. This operational tempo necessitates field service platforms capable of dynamic scheduling, weather-aware routing, and integration with grid management software. Companies like Enel and Ørsted now manage technician fleets across thousands of micro sites using AI-driven dispatch engines that adjust in real time to outage alerts and traffic conditions. As per the International Renewable Energy Agency, European utilities employing advanced field coordination reported significant reductions in mean time to repair for distributed assets compared to manual scheduling. As the EU targets 45% renewable electricity by 2030, this infrastructure sprawl will continue to fuel demand for scalable, intelligent field service solutions tailored to the unique rhythms of clean energy maintenance.

MARKET CHALLENGES

Persistent Fragmentation of Regional Service Standards and Certification Requirements

Despite efforts toward harmonization, European countries maintain distinct technical certification regimes for field personnel, particularly in regulated domains such as gas utilities, medical equipment, and high voltage electrical systems, which is a major challenge to the growth of the European field service management market. A technician certified in Belgium may not be legally permitted to perform identical work in Poland without undergoing redundant assessments, which creates inefficiencies for pan-European service providers. According to the European Federation of National Engineering Associations, only a minority of technical occupational standards are mutually recognized across EU member states as of 2025. This patchwork forces companies to either maintain localized technician pools or invest in continuous re-certification programs, which inflate operational costs and delay service delivery. For example, a multinational HVAC provider operating in five EU countries reported that a notable share of its annual training budget was devoted solely to compliance with divergent national safety accreditations, as documented in an internal audit shared with the European Social Fund. Moreover, the lack of standardized digital credentialing impedes real-time verification of technician qualifications within field service platforms, leading to manual oversight and potential compliance breaches. Until the European Commission advances mutual recognition directives under the Professional Qualifications Directive, this regulatory heterogeneity will constrain workforce mobility and limit the scalability of centralized field service operations, particularly for industries where safety certifications are non-negotiable.

Inconsistent Digital Literacy Among Aging Field Workforces

A significant portion of Europe’s frontline service technicians belongs to an aging demographic less familiar with mobile applications, cloud interfaces, and data-driven workflows, which is further challenging the European field service management market expansion. As per Eurostat, a considerable share of skilled tradespeople in the EU are aged 50 or older, with the highest concentrations in Southern and Eastern Europe. This generational gap creates resistance to adopting digital field service tools, even when organizational leadership mandates their use. A field study conducted by the German Institute for Economic Research found that technicians over 55 required more training hours to achieve proficiency with new mobile work order systems compared to colleagues under 35. Moreover, error rates during initial deployment phases were higher among older cohorts, leading to duplicated visits and customer dissatisfaction. While some firms deploy simplified user interfaces and voice-enabled assistants to bridge this divide, such accommodations often compromise functionality or require costly customization. In Italy, Confindustria reported that many small maintenance firms abandoned digital transformation initiatives due to workforce pushback and inadequate change management resources. This human factor challenge is compounded by limited access to adult digital upskilling programs outside major urban centers. Until public-private partnerships expand targeted reskilling pathways and software vendors prioritize intuitive design for non-digital native users, the full potential of field service management platforms will remain unrealized across large segments of the European service economy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Deployment Type, Organization Size, Solution & Service Type, End-user Vertical, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Oracle Corp. (Oracle Field Service), ServiceNow, Salesforce Inc. (Field Service), Microsoft Corp. (Dynamics 365 Field Service), SAP SE (Coresystems), IFS AB, and Others. |

SEGMENTAL ANALYSIS

By Deployment Type Insights

The cloud deployment segment dominated the Europe field service management market by accounting for 66.9% of the regional market share in 2025. The dominance of the cloud segment in this regional market is driven by the operational agility and cost efficiency that cloud-based solutions offer to businesses navigating Europe’s dynamic regulatory and competitive landscape. European enterprises increasingly operate across multiple jurisdictions, requiring field service platforms that can scale rapidly without heavy infrastructure investment. Cloud deployments enable real-time access to centralized data from any location, which is critical for firms managing dispersed technician teams. As per the European Commission, a majority of EU-based service companies with operations in three or more member states reported using cloud-based field service tools to maintain workflow consistency. The ability to onboard new users, update software, and integrate with local compliance modules without on-site IT intervention significantly reduces time to value. In Germany, where cross-border logistics are routine for industrial service providers, cloud platforms have cut average deployment cycles compared to on-premises alternatives as documented by Bitkom, the German Association for Information Technology, Telecommunications, and New Media. This flexibility is especially valuable in sectors like utilities and telecom, where service demands fluctuate seasonally and geographically.

By Organization Size Insights

The large enterprises segment led the Europe field service management market by capturing 60.5% of the regional market share in 2025. The dominating position of the large enterprises segment in the European market is attributed to the complex service networks, extensive asset portfolios, and stringent compliance obligations that necessitate sophisticated coordination platforms. Large enterprises in Europe often manage thousands of assets across dozens of countries, requiring centralized visibility into maintenance status, technician performance, and parts inventory. Field service management systems provide the orchestration layer needed to unify these operations under a single governance framework. As per the European Investment Bank, large industrial firms with more than 250 employees account for a significant share of total maintenance expenditures in the EU manufacturing sector. For instance, Siemens operates more than 400 production and service sites across Europe and relies on an integrated field service platform to coordinate thousands of technicians, ensuring adherence to ISO 55000 asset management standards. Without such systems, manual tracking would introduce unacceptable delays and compliance risks, particularly in safety-critical industries like energy and rail transport, where the European Union Agency for Railways mandates detailed service logs for every intervention.

The small and medium enterprises segment is estimated to witness a promising CAGR of 16.6% over the forecast period. A new generation of industry-tailored cloud-based field service applications has dramatically lowered adoption barriers for SMEs. Unlike generic enterprise platforms, these solutions offer pre-configured workflows for sectors like HVAC, plumbing, and electrical contracting at affordable monthly subscription rates. As per the European DIGITAL SME Alliance, many European service-oriented SMEs adopted specialized field service software between 2023 and 2025, citing ease of use and immediate return on investment. In Italy, where most businesses are SMEs, the National Confederation of Crafts and Small Enterprises reported that digitized field operations reduced administrative overhead on average, allowing owners to redirect staff from paperwork to revenue-generating tasks. This product market fit has transformed field service tools from luxury investments into essential productivity enablers for Europe’s backbone of micro and small service providers.

By End User Vertical Insights

The facilities management commanded the highest share of 33.8% of the regional market in 2025. The growth of the facilities management segment in this regional market is driven by the sector’s labor intensity, asset diversity, and contractual obligation to deliver measurable service levels. Facilities management contracts in Europe increasingly tie payments to quantifiable performance metrics such as response time, first-time fix rate, and customer satisfaction scores. Field service management systems provide the real-time tracking and automated reporting necessary to prove compliance and avoid penalties. As per the Royal Institution of Chartered Surveyors, most hard facilities management contracts signed in the EU in 2024 included digitally verifiable KPIs enforceable through integrated field platforms. In the United Kingdom, major providers like Mitie and ISS embed GPS timestamped photo evidence and technician notes directly into client dashboards, reducing billing disputes as reported by the British Institute of Facilities Management. This shift from relationship-based to data-driven accountability has made field service software indispensable for winning and retaining large commercial contracts across office, retail, and healthcare real estate portfolios.

The IT and telecom segment is a promising segment and is predicted to register a CAGR of 16.6% over the forecast period. Europe’s aggressive broadband expansion mandates have triggered unprecedented deployment activity for telecom operators. The European Electronic Communications Code requires member states to achieve gigabit connectivity for all households by 2030, driving massive investments in fiber and 5G infrastructure. Each installation involves multiple field visits for surveying, trenching, splicing, and testing, all of which must be synchronized across subcontractors and municipal permits. As per the Body of European Regulators for Electronic Communications, millions of new fiber connections were activated in the EU in 2024. To manage this complexity, Orange in France deployed a cloud-based field service platform that reduced technician idle time through AI-optimized scheduling as validated by ARCEP, the French telecom regulator. Similarly, Deutsche Telekom uses real-time asset mapping to prevent duplicate excavations, saving significant amounts annually in civil works costs. The sheer volume and precision required in network builds make advanced field coordination not optional but foundational to national digital strategies.

COUNTRY-LEVEL ANALYSIS

Germany Field Service Management Market Analysis

Germany occupied the major share of 23.3% of the regional market in 2025. The leading position of Germany in the European market is attributed to its dense industrial base, rigorous engineering culture, and leadership in Industry 4.0 adoption. Germany hosts over 170000 Mittelstand companies, which form the backbone of European manufacturing and rely heavily on precision maintenance to sustain export competitiveness. As per the Federal Ministry for Economic Affairs and Climate Action, a majority of German industrial firms implemented digital field service solutions by 2024 to comply with DIN SPEC 91364 standards for predictive maintenance interoperability. The automotive sector alone accounts for nearly 30% of field service activity, with OEMs like BMW mandating real-time technician reporting across their global supplier network. Furthermore, Germany’s Energiewende energy transition policy has spurredthe deployment of millions of distributed renewable assets each requiring scheduled servicing coordinated through cloud platforms. As per the Fraunhofer Institute, digital field coordination has reduced unplanned downtime in German factories since 2020, making the country not just the largest but also the most technologically advanced market for field service management in Europe.

United Kingdom Field Service Management Market Analysis

The United Kingdom held 15.8% of the European field service management market share in 2025. Despite Brexit-related uncertainties, the UK maintains a strong demand driven by its mature facilities management sector and robust digital infrastructure. London alone accounts for a significant share of national FM contracts, which increasingly stipulate digital proof of service delivery. As per the Office for National Statistics, many UK-based service firms with more than 50 employees used field service management software in 2024, showing strong growth compared to 2020. The National Health Service has been a major catalyst in deploying field platforms across hundreds of acute hospitals to manage biomedical equipment maintenance under strict MHRA regulations. Additionally, the UK’s commitment to net zero by 2050 has accelerated heat pump installations, with Ofgem reporting large-scale deployments in 2024 each requiring certified technician visits tracked via digital workflows. The presence of global vendors like ServiceNow and Salesforce with regional headquarters in London further reinforces ecosystem maturity, making the UK a high-value, stable market despite macroeconomic headwinds.

France Field Service Management Market Analysis

France is predicted to witness a promising CAGR in the European field service management market during the forecast period. The country’s strength lies in its centralized utility sector and aggressive public digitization agenda. EDF, Engie, and Veolia collectively manage millions of customer touchpoints annually, requiring sophisticated field coordination to meet state-mandated service standards. As per France Stratégie, the government’s economic planning agency, a large share of French public service providers adopted AI-enhanced field platforms between 2022 and 2024 under the France Relance recovery plan. The nuclear energy fleet alone comprises dozens of reactors, each undergoing rolling maintenance campaigns that involve hundreds of technicians whose certifications and task completions must be digitally verified per ASN safety directives. Moreover, France’s Loi Climat et Résilience law requires all buildings over 1000 square meters to undergo energy retrofits by 2030, triggering a wave of HVAC and insulation projects managed through field service apps. As per INSEE, construction-related field service activity grew in 2024, underscoring how regulatory policy directly fuels platform adoption across both public and private domains.

Italy Field Service Management Market Analysis

Italy is projected to account for a notable share of the European field service management market over the forecast period. Its market is characterized by a vast network of artisanal service providers and a late but accelerating digital transition. Over 4 million microenterprises dominate the Italian economy, many of which historically relied on paper-based scheduling. However, recent EU cohesion funds have catalyzed change with the National Recovery and Resilience Plan allocating billions of euros specifically for SME digitization in 2024. As per ISTAT, Italy’s national statistics institute, more than half of maintenance businesses with 10 to 49 employees adopted cloud field tools in 2024, showing sharp growth compared to 2021. The tourism sector has been a key driver, with tens of thousands of hotels upgrading HVAC and plumbing systems to meet new EU energy labeling requirements tracked via digital work orders. Additionally, Italy’s aging building stock requires constant retrofitting, creating steady demand for skilled trades coordinated through mobile platforms. While still behind Northern peers, Italy’s growth trajectory is steep, fueled by both necessity and targeted public investment.

Netherlands Field Service Management Market Analysis

The Netherlands is anticipated to register a healthy CAGR in the European field service management market during the forecast period. The country’s leadership stems from its role as a European logistics and sustainability pioneer. Dutch firms operate under some of the continent’s strictest environmental and labor regulations, making digital compliance non-negotiable. As per Statistics Netherlands, a large share of service companies in the Randstad region uses field platforms that auto-log technician hours, carbon mileage, and material usage to satisfy corporate sustainability reporting mandates. The port of Rotterdam, the largest in Europe, deploys field service systems across thousands of assets, including cranes, pumps, and refrigeration units with real-time health monitoring, preventing costly cargo delays. Furthermore, the Netherlands’ ambitious climate agreement targets millions of heat pump installations by 2030, a goal driving unprecedented field activity coordinated through platforms that integrate with national subsidy portals. As per TNO, Dutch utilities using AI-driven field dispatch reduced technician travel distance in 2024, lowering both costs and emissions. This fusion of logistical excellence, regulatory rigor, and green ambition positions the Netherlands as a high-efficiency innovation hub within the European field service landscape.

COMPETITIVE LANDSCAPE

The Europe field service management market features intense competition among global software vendors, niche European specialists, and emerging AI-driven startups. Established players leverage scale, interoperability, and compliance expertise to retain large enterprise clients while agile regional providers differentiate through vertical depth and multilingual support. Competition centers not on price but on functional sophistication, integration ease, and adherence to evolving EU regulations, including GDPR, digital operational resilience, and green transition policies. Vendors continuously enhance mobile capabilities, offline access, and real-time analytics to address fragmented technician demographics and infrastructure variability across Northern, Southern, and Eastern Europe. The absence of a dominant standard has spurred platform wars where ecosystem alliances, API openness, and partner networks increasingly determine market influence. As service-centric business models expand, competition is shifting from feature parity to outcome delivery measured through uptime, sustainability, and customer satisfaction.

KEY MARKET PLAYERS

The leading companies operating in the Europe field service management market include:

- Oracle Corp. (Oracle Field Service)

- ServiceNow

- Salesforce Inc. (Field Service)

- Microsoft Corp. (Dynamics 365 Field Service)

- SAP SE (Coresystems)

- IFS AB

TOP PLAYERS IN THE MARKET

- ServiceNow plays a pivotal role in the Europe field service management market through its cloud native Now Platform, which integrates field workflows with enterprise service management. The company has deepened its European footprint by expanding data residency options in Germany and the Netherlands to comply with GDPR and sector-specific regulations. In 2024, ServiceNow enhanced its Field Service Management application with generative AI capabilities, enabling technicians to receive real-time troubleshooting guidance and automated work order summaries. It also forged strategic partnerships with major European utilities and telecom operators to embed predictive maintenance logic into service delivery. These initiatives reinforce its position as a preferred platform for large enterprises seeking scalable, intelligent, and compliant field operations across the region.

- Salesforce contributes significantly to the European field service landscape via its Field Service Lightning solution, which unifies customer relationship management with mobile workforce orchestration. The company has invested heavily in localized language support and regulatory compliance features tailored for EU markets, including right to repair documentation and sustainability reporting modules. In 2024, Salesforce launched an industry-specific accelerator for renewable energy service providers, enabling dynamic scheduling around weather forecasts and grid availability. It also integrated its platform with leading European IoT ecosystems such as Bosch IoT Suite to facilitate real-time asset monitoring. These moves demonstrate Salesforce’s commitment to embedding field service within broader customer success and sustainability strategies across Europe.

- IFS maintains strong relevance in the Europe field service management market, particularly within asset-intensive sectors such as aerospace, energy, and manufacturing. Its IFS Field Service Management solution is engineered for complex multi-skilled dispatch and contract compliance common in European industrial environments. In 2024, IFS introduced native mobile offline capabilities and augmented reality work instructions to support technicians in remote or low connectivity areas typical of Nordic and Eastern European operations. The company also expanded its partnership with Microsoft to deliver seamless integration between IFS Cloud and Dynamics 365 Field Service, enhancing interoperability for joint customers. By focusing on deep vertical functionality and operational resilience, IFS continues to serve as a critical enabler for mission-critical field operations across the continent.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe field service management market primarily pursue product innovation through artificial intelligence and Internet of Things integration to enhance predictive dispatch and technician enablement. They invest in cloud infrastructure with regional data centers to meet strict European data sovereignty requirements. Strategic partnerships with local system integrators and industry-specific technology providers help tailor solutions for regulated sectors such as energy, healthcare, and utilities. Companies also focus on user experience simplification to accelerate adoption among aging technician workforces. Additionally, they align their platforms with European sustainability mandates by embedding carbon tracking service longevity metrics and circular economy workflows into core functionality to support compliance and corporate responsibility goals.

MARKET SEGMENTATION

This research report on the Europe field service management market has been segmented and sub-segmented into the following categories.

By Deployment Type

- On-premise

- Cloud

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By FSM Solution and Service Type

- Solutions

- Scheduling, Dispatch, and Route Optimization

- Service Contract Management

- Work-order Management

- Customer Management

- Inventory Management

- Other Software (Billing, Invoicing, Warranty)

- Services

- Integration

- Implementation

- Support

By End-user Vertical

- Facilities Management (Hard-FM and Soft-FM)

- IT and Telecom

- Healthcare and Life Sciences

- Energy and Utilities

- Oil and Gas

- Manufacturing

- Transportation and Logistics

- Real Estate and Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe field service management market?

The Europe field service management market delivers software coordinating mobile technicians for installation, maintenance, and repairs. Cloud platforms optimize scheduling across industries.

What drives the Europe field service management market?

Automation demands and efficiency needs propel the Europe field service management market. Digital transformation in utilities and telecom accelerates FSM adoption continent-wide.

How is the Europe field service management market segmented?

The Europe field service management market segments by solution like scheduling, work orders, analytics, plus deployment as cloud or on-premises for varied enterprise sizes.

Which countries lead the Europe field service management market?

Germany, UK, and France dominate the Europe field service management market with mature manufacturing and telecom sectors demanding advanced FSM capabilities.

Why cloud solutions grow in the Europe field service management market?

Cloud FSM platforms expand rapidly in the Europe field service management market offering scalability and real-time data for SMEs and large enterprises alike.

What role does AI play in the Europe field service management market?

AI enables predictive dispatch in the Europe field service management market forecasting failures and optimizing technician routes for reduced downtime.

Which industries use the Europe field service management market?

Telecom, utilities, manufacturing lead adoption in the Europe field service management market streamlining field operations across diverse service environments.

What challenges face the Europe field service management market?

Data privacy regulations challenge the Europe field service management market requiring secure cloud solutions compliant with GDPR standards across member states.

How does regulation impact the Europe field service management market?

GDPR shapes the Europe field service management market favoring secure on-premises and hybrid deployments protecting customer data in field operations.

Why SMEs adopt the Europe field service management market?

SMEs leverage cost-effective FSM in the Europe field service management market gaining mobile apps and analytics without heavy infrastructure investments.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com