Europe Fish Processing Market Research Report Segmented By Category (Frozen, Preserved And Others), Application (Food, Non-Food), Source (Marine And Inland), Species (Fish, Crustaceans, Mollusks And Others), Equipment (Slaughtering, Gutting, Scaling, Filleting, Deboning, Skinning, Smoking And Others), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic And Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Fish Processing Market Size

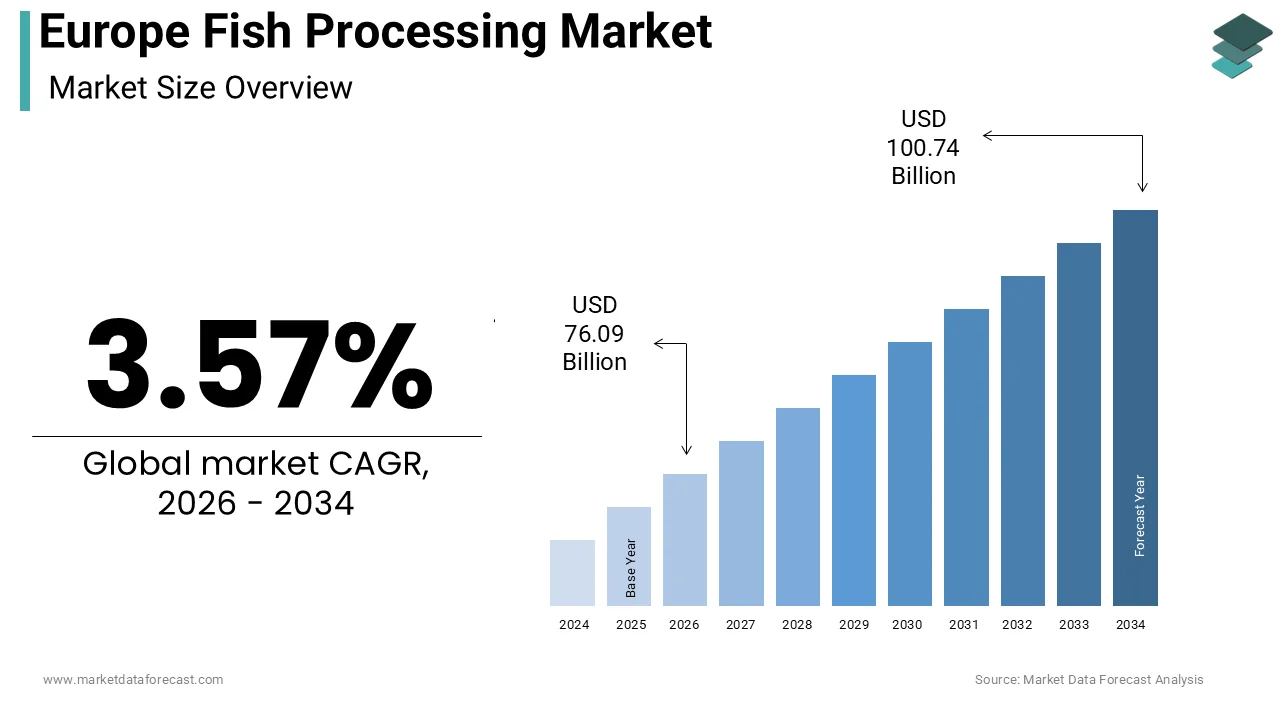

The size of the European fish processing market was expected to be worth USD 73.47 billion in 2025 and is anticipated to be worth USD 100.74 billion by 2034 from USD 76.09 billion in 2026, growing at a CAGR of 3.57% during the forecast period.

Fish processing encompasses the comprehensive industrial ecosystem dedicated to transforming raw aquatic harvest into consumable products through methods such as freezing, smoking, curing, canning, and value-added preparation. This sector serves as a critical bridge between marine capture fisheries, aquaculture production, and the final consumer, ensuring food safety, extending shelf life, and enhancing nutritional accessibility. The definition extends beyond simple preservation to include sophisticated supply chain logistics that adhere to some of the world's most rigorous hygiene and traceability standards. As per the European Food Safety Authority, the region maintains strict controls on contaminants and microbiological hazards in seafood, which mandates robust processing protocols that define market entry barriers. Furthermore, the European Union stands as one of the largest importers of fishery products globally, relying heavily on processed imports to meet domestic consumption needs that local catches cannot satisfy. According to Eurostat, the average annual consumption of fishery and aquaculture products per capita in the European Union exceeds twenty kilograms, which indicates the sector's vital role in regional food security. The market is characterized by a diverse array of operators ranging from large multinational corporations to small artisanal producers, all navigating a complex regulatory landscape designed to protect both public health and marine resources. This intricate balance between industrial efficiency, sustainability mandates, and consumer demand shapes the unique contours of the European fish processing market.

MARKET DRIVERS

Rising Consumer Preference for Convenient and Ready-to-Eat Seafood

The shifting lifestyle dynamics across Europe, characterized by increasing urbanization and dual-income households, have catalyzed a surging demand for convenient, ready-to-eat, and ready-to-cook seafood products, which is primarily driving the European fish processing market expansion. Modern consumers increasingly prioritize time-saving meal solutions without compromising on nutritional quality, driving processors to innovate with pre-marinated fillets, breaded items, and microwaveable seafood meals. As per data from the European Commission, the share of household expenditure on food consumed away from home or prepared via convenience formats has risen steadily, reflecting a broader societal shift toward efficiency. The aging population in countries like Germany and Italy further amplifies this trend, as older demographics often seek easy-to-prepare protein sources that are rich in essential nutrients like omega-3 fatty acids. According to the European Association of Fish Producers Organizations, retailers have responded by expanding their chilled and frozen seafood aisles with value-added products that offer restaurant-quality experiences at home. This demand for convenience compels processors to invest in advanced packaging technologies and automation to maintain product freshness while reducing preparation time for the end user. The ability to offer diverse flavor profiles and ethnic cuisines through processed seafood formats also appeals to the multicultural demographic of modern Europe. Consequently, the drive for convenience acts as a primary engine for market growth, pushing manufacturers to move beyond commodity sales toward high-margin, differentiated product portfolios that align with contemporary living patterns.

Heightened Awareness of Health Benefits Associated with Seafood Consumption

The growing scientific consensus and public awareness regarding the profound health benefits of seafood consumptionares further contributing to the growth of the European fish processing market. Consumers are increasingly educated about the role of marine proteins in preventing cardiovascular diseases, supporting cognitive function, and providing essential vitamins and minerals, which is leading to a deliberate shift in dietary choices. As per the European Society of Cardiology, regular consumption of fatty fish is strongly linked to reduced risks of heart disease, which is a message that has been effectively disseminated through public health campaigns across the continent. This health consciousness is particularly pronounced among millennials and Gen Z consumers who actively seek functional foods that contribute to long-term wellness. According to the European Food Information Council, surveys indicate that a significant majority of Europeans consider seafood a healthy choice, which is prompting them to incorporate it into their diets more frequently despite higher price points compared to other proteins. Processors capitalize on this trend by developing fortified products, low-sodium options, and clean-label items that cater to specific health goals such as weight management or muscle building. The endorsement of seafood by nutritionists and dietitians further validates these choices, creating a stable and expanding demand base. This alignment of consumer behavior with medical recommendations ensures that the market continues to grow as health becomes a central pillar of food purchasing decisions in Europe.

MARKET RESTRAINTS

Volatility in Raw Material Supply and Fluctuating Catch Quotas

The inherent instability of raw material supply due to fluctuating fish stocks and stringent catch quotas imposed by regulatory bodieisre hindering the fish processing market growth in Europe. The regional market relies heavily on wild-caught species whose availability is subject to natural cycles, climate change impacts, and political negotiations regarding fishing rights. As per the International Council for the Exploration of the Sea, many commercial fish stocks in European waters face pressure, leading the European Union to adjust Total Allowable Catches annually, often resulting in reduced volumes for key species like cod and hake. These quota restrictions create supply bottlenecks that force processors to operate below capacity or seek expensive alternatives from distant waters, thereby squeezing profit margins. According to the European Commission's Common Fisheries Policy, the mandate to achieve Maximum Sustainable Yield means that overfished stocks must be allowed to recover, which temporarily limits the raw material available for processing. Furthermore, geopolitical tensions and Brexit have complicated access to traditional fishing grounds, exacerbating supply chain uncertainties. The reliance on imports to fill gaps introduces additional risks related to currency fluctuations and international trade disputes. This unpredictability in raw material availability hampers long-term planning and investment in processing infrastructure, as companies struggle to guarantee consistent product flow to retailers and food service clients in a market defined by biological and regulatory constraints.

Stringent Regulatory Compliance and Traceability Requirements

The rigorous regulatory framework governing food safety, labeling, and traceability in Europe is another significant impediment to the regional market growth. The European Union enforces some of the strictest standards globally, requiring comprehensive documentation from the point of catch to the final retail shelf to combat illegal fishing and ensure consumer safety. As per the European Food Safety Authority, processors must adhere to detailed Hazard Analysis and Critical Control Points protocols, which necessitate significant investment in quality control systems, testing laboratories, and specialized staff. The requirement for full traceability under the EU Control Regulation means that every batch of fish must be tracked through complex supply chains, imposing heavy administrative burdens on companies, particularly small and medium-sized enterprises. According to the European Commission, non-compliance can result in severe penalties, product recalls, and reputational damage, forcing firms to adopt conservative operational strategies that may limit innovation speed. The need to constantly update labeling to reflect new allergen information, origin details, and sustainability certifications adds further cost and logistical challenges. These regulatory demands, while essential for protecting public health and marine resources, increase the cost of production and create high barriers for new entrants, thereby restraining the overall agility and growth potential of the market in a highly competitive environment.

MARKET OPPORTUNITIES

Expansion of Sustainable and Eco-Labelled Product Lines

The burgeoning consumer demand for sustainably sourced and eco-certified seafood products is a promising opportunity for the European fish processing market to differentiate itself and capture premium market segments. As environmental consciousness rises, European shoppers are increasingly scrutinizing the origin and harvesting methods of their food, favoring products bearing recognized sustainability labels such as the Marine Stewardship Council or Aquaculture Stewardship Council. As per the Global Sustainable Seafood Initiative, the sales of certified sustainable seafood in Europe have shown robust growth, with consumers willing to pay a price premium for goods that guarantee responsible fishing and farming practices. Processors have the opportunity to align their supply chains with these standards, securing long-term contracts with retailers who have committed to sourcing only sustainable seafood. This shift also opens doors to innovative product development using underutilized or invasive species that are abundant but less known, thereby relieving pressure on popular stocks while offering unique culinary experiences. According to the European Commission's Green Deal, there is strong political and financial support for initiatives that promote circular economy principles in the food sector, including the utilization of fish by-products for human consumption or other valuable applications. By embracing sustainability as a core business strategy, companies can build brand loyalty, mitigate supply risks, and access new distribution channels that prioritize ethical sourcing, driving significant value growth in an increasingly conscientious market.

Utilization of Fish By-Products for High-Value Applications

The strategic utilization of fish by-products that traditionally constitute a significant portion of waste offers a substantial opportunity for the European fish processing market. Advances in biotechnology and extraction techniques now enable processors to convert heads, bones, skins, and viscera into high-value ingredients such as collagen, gelatin, omega-3 supplements, and bioactive peptides. As per the European Fisheries and Aquaculture Advisory Council, up to 60% of a fish can end up as by-product, representing a massive untapped resource that, if valorized, can significantly improve the economic efficiency of processing operations. The growing demand for natural ingredients in the pharmaceutical, cosmetic, and nutraceutical industries creates a lucrative outlet for these extracted compounds. According to research from the European Marine Board, the development of biorefineries integrated with fish processing plants can transform waste streams into valuable assets, aligning with the European Union's zero-waste targets. This approach not only generates additional revenue streams but also reduces disposal costs and environmental impact, enhancing the overall sustainability profile of the company. Companies that invest in technologies to efficiently separate and process these by-products can position themselves as leaders in the circular bioeconomy, accessing new markets beyond traditional food retail and creating a more resilient business model against fluctuations in primary product prices.

MARKET CHALLENGES

Impact of Climate Change on Fish Stock Distribution and Quality

The accelerating effect of climate change is a major challenge to the European fish processing market. Rising sea temperatures and ocean acidification are causing migratory shifts in marine species, moving them away from traditional fishing grounds and disrupting established supply chains that processors rely on. As per the Intergovernmental Panel on Climate Change, many commercially important species in European waters are moving northward or into deeper waters, forcing fleets to travel further and incur higher fuel costs to maintain catch volumes. These changes also affect the biological quality of the fish, potentially impacting texture, fat content, and shelf life, which complicates processing parameters and product consistency. According to the European Environment Agency, extreme weather events and changing ocean currents can lead to unpredictable catches and seasons, which makes it difficult for processors to plan production schedules and manage inventory effectively. The uncertainty regarding future stock availability threatens the viability of processing facilities located in regions that may lose access to their primary raw materials. Adapting to these shifts requires significant investment in flexible supply chains and alternative sourcing strategies, yet the pace of environmental change often outstrips the industry's ability to adjust. This ecological volatility creates a persistent risk factor that undermines long-term stability and profitability for the entire sector.

Escalating Energy Costs and Operational Expenses

The sharp escalation in energy costs and general operational expenses is further challenging the expansion of the European fish processing market. The European market is highly energy-intensive, relying heavily on electricity and fuel for freezing, cold storage, cooking, and transportation processes, making it particularly vulnerable to fluctuations in energy prices. As per Eurostat, energy prices in Europe have experienced unprecedented volatility in recent years, driven by geopolitical tensions and supply constraints, which have significantly inflated the cost base for processors. The necessity of maintaining unbroken cold chains from catch to consumer means that even brief spikes in energy costs can erode thin profit margins, forcing companies to either absorb losses or pass costs onto consumers, risking demand destruction. According to the European Association of Fish Producers Organizations, many small and medium-sized processors face existential threats as they lack the financial resilience to hedge against such cost surges or invest in energy-efficient technologies. Furthermore, rising labor costs and inflationary pressures on packaging materials compound the financial strain. The imperative to reduce carbon footprints adds another layer of cost, as firms must invest in renewable energy sources and efficient equipment to meet regulatory and consumer expectations. Balancing these mounting expenses while maintaining product affordability and quality remains a daunting hurdle for market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.57% |

| Segments Covered | By Category, Source, Equipment, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Leroy, Pelagia AS, Maruha Nichiro Corporation, Pescanova USA, Royal Greenland A / S, Thai Union Group Public Company Limited, High Liner Foods, NISSUI, Channel Fish Processing Company Inc, Charoen Pokphand Foods PCL, and Marine Harvest ASA. |

SEGMENTAL ANALYSIS

By Category Insights

The frozen segment led the market by holding the largest share of the European fish processing market in 2025 due to its unparalleled ability to extend shelf life while retaining nutritional value and sensory qualities comparable to fresh products. The logistical necessity of transporting seafood from distant fishing grounds or aquaculture sites to inland consumption centers without spoilage is further contributing to the dominance of the frozen segment in the European market. As per the European Commission, the European Union relies heavily on imports to meet its seafood demand, with over 60% of consumed fishery products originating from outside the region, which is making freezing an essential preservation method for long-distance trade. The versatility of frozen formats allows retailers to offer a wide variety of species year-round, independent of seasonal catch fluctuations, which appeals to modern consumers seeking consistency. According to Eurostat, household expenditure on frozen food has seen steady growth as consumers increasingly stock up on convenient protein sources that reduce food waste. Furthermore, advancements in Individual Quick Freezing technology have minimized ice crystal formation, which preserves the texture and cellular integrity of the fish, thereby overcoming historical consumer perceptions regarding quality loss. The ability of frozen products to serve as raw material for further processing into value-added items like breaded fillets or ready meals also cements their position as the backbone of the industrial supply chain. This combination of logistical efficiency, product availability, and technological improvement ensures the frozen segment remains the market leader.

On the other hand, the preserved segment is anticipated to record the fastest CAGR in the European fish processing market over the forecast period, owing to a resurgence in appreciation for traditional flavors and the demand for ultra-convenient pantry staples. The evolving culinary landscape, where consumers seek authentic, gourmet experiences that require minimal preparation time, such as high-quality smoked salmon or artisanal tinned sardines, is further boosting the expansion of the preserved segment in the European market. As per data from the European Canned Food Federation, the sales of canned fish have rebounded strongly as shoppers recognize their long shelf life and nutritional density as key advantages during times of economic uncertainty and supply chain volatility. The trend toward "clean label" products has prompted manufacturers to reformulate preserved items with natural ingredients, sea salt, and olive oil, shedding the image of overly processed food and attracting health-conscious demographics. According to industry reports from major European retailers, the premiumization of preserved seafood, particularly in the smoking and curing categories, has opened new revenue streams driven by gift-giving occasions and upscale dining at home. The portability and non-perishable nature of these products also make them ideal for the growing outdoor recreation and camping sectors in Europe. This convergence of tradition, convenience, and premium positioning positions the preserved segment as the fastest-growing component of the market.

By Source Insights

The marine segment held the dominant position in the Europe fish processing market by capturing the major share of the European market in 2025 due to the cultural preference for saltwater species such as cod, haddock, tuna, and salmon, which constitute the staple diet in many European nations. As per the Food and Agriculture Organization of the United Nations, marine capture fisheries in European waters continue to yield millions of tonnes annually, which provides a massive and consistent raw material base for processors. The extensive coastline of Europe, stretching from the Arctic Ocean to the Mediterranean Sea, supports a diverse range of marine ecosystems that sustain large-scale commercial fishing fleets. According to the European Maritime and Fisheries Fund reports, significant public investment is directed toward modernizing the marine fleet and ports to ensure sustainable harvest levels, which is reinforcing the sector's capacity. Furthermore, the global trade in marine products is far more developed than that of inland species, with established cold chains and import networks bringing tropical and deep-sea species to European markets. The sheer scale of marine aquaculture, particularly in Norway and Scotland for salmon, adds substantial volume that inland freshwater farming cannot match. This abundance of resources, combined with deep-rooted consumer habits and robust infrastructure, ensures the marine segment remains the primary driver of market volume.

On the other hand, the inland segment is anticipated to witness the fastest CAGR in the European market over the forecast period owing to the strategic initiatives to enhance food security, reduce the carbon footprint of transportation, and diversify protein sources through sustainable freshwater aquaculture. The rising focus on local production to mitigate reliance on volatile global supply chains and imported marine stocks is also aiding the expansion of the inland segment in the European market. As per the European Alliance for Aquaculture, there is a concerted push by EU member states to expand inland fish farming operations for species like trout, carp, and catfish, which are well-suited to recirculating aquaculture systems that minimize environmental impact. The growing consumer preference for locally sourced and traceable food products favors inland producers who can offer shorter supply chains and fresher delivery times to central European markets. According to the European Commission's Strategic Guidelines for Aquaculture, specific funding and regulatory support are being allocated to promote organic inland fish farming and innovate in feed efficiency, making these operations more economically viable. Additionally, the rise of niche markets for indigenous freshwater species and the development of value-added processed products from inland catches are attracting new consumer segments. The ability of inland aquaculture to operate independently of oceanic climate changes and overfishing concerns provides a stable growth trajectory. This alignment with sustainability goals and localism trends ensures the inland segment will outpace marine sources in terms of growth velocity.

By Equipment Insights

The filleting equipment segment dominated the market by capturing the highest share of the European fish processing market in 2025. The leading position of the filleting equipment segment in the European market is driven by the critical mechanized step that transforms whole fish into the primary cut demanded by retailers and food service operators. The intense labor shortages in the European processing sector and the need for high precision to maximize yield from expensive raw materials are further contributing to the dominance of the filleting equipment segment in the regional market. As per the European Association of Fish Producers Organizations, the cost of labor in Europe has risen significantly, which is making manual filleting economically unviable for high-volume operations and requiring the adoption of automated filleting machines that can process thousands of fish per hour with minimal waste. Modern filleting equipment utilizes advanced vision systems and adaptive cutting technologies to navigate the unique anatomy of each fish to ensure optimal meat recovery and consistent product quality. For instance, the return on investment for automated filleting lines is rapid due to the reduction in product giveaway and the ability to operate continuously without fatigue. The versatility of these machines to handle various species, from delicate whitefish to oily salmon, makes them indispensable in multi-species processing plants. Furthermore, strict hygiene regulations in Europe favor enclosed, easy-to-clean automated systems over manual stations, which are further driving adoption. The centrality of the fillet as the most valuable product form ensures that investment in filleting technology remains the top priority for processors seeking efficiency and profitability.

On the other hand, the smoking equipment segment is anticipated to record a promising CAGR in the European fish processing market during the forecast period, owing to the escalating consumer demand for premium, flavor-enhanced seafood products and the expansion of the ready-to-eat category. The trend toward gourmet home dining and the popularity of smoked salmon, trout, and mackerel as luxury breakfast and appetizer items across Europe is further propelling the growth of the smoking equipment segment in the European market. As per market observations from food processing equipment suppliers, manufacturers are increasingly investing in advanced smoking kilns that offer precise control over temperature, humidity, and smoke density to create distinct flavor profiles while ensuring food safety and extending shelf life naturally. The shift toward continuous smoking lines allows processors to scale up production to meet surging retail demand without compromising the artisanal quality that consumers expect. According to the European Smoked Fish Association, the value of smoked fish products has grown double-digits in recent years, prompting processors to upgrade from traditional batch smokers to high-capacity, energy-efficient units that reduce operating costs. The integration of digital monitoring systems in modern smoking equipment enables real-time adjustments and data logging for compliance with strict EU food safety standards. Additionally, the versatility of new smoking technologies to handle plant-based alternatives alongside fish opens new application avenues. This convergence of premiumization, automation, and regulatory compliance ensures the smoking equipment segment will experience the highest growth rates.

REGIONAL ANALYSIS

Norway Fish Processing Market Analysis

Norway held the dominant position in the Europe fish processing market by holding the leading share of the regional market in 2025. The dominating position of Norway in the European market is attributed to its massive aquaculture industry, particularly in Atlantic salmon, and its highly advanced processing infrastructure. The status of Norway as the world's second-largest seafood exporter, with a domestic processing sector that is synonymous with innovation, quality, and sustainability, is also aiding the dominance of Norway in the European market. As per Statistics Norway, the seafood industry constitutes a pillar of the national economy, with export values reaching record highs driven by processed salmon products destined for European tables. The Norwegian processing sector is characterized by widespread adoption of robotics and automation to address labor constraints and ensure hygienic standards that exceed global benchmarks. According to the Norwegian Seafood Council, the industry has invested heavily in value-added processing facilities that produce fillets, portions, and ready-to-eat meals, moving beyond simple head-and-gut exports. The country's rigorous regulatory framework and commitment to sustainable farming practices enhance the global reputation of its processed goods, commanding premium prices. Furthermore, Norway's strategic location and efficient logistics network facilitate the rapid delivery of fresh and frozen products to key European markets. The continuous R&D focus on by-product utilization and energy-efficient processing technologies ensures Norway maintains its top position through a synergy of natural resources and technological excellence.

Spain Fish Processing Market Analysis

Spain accounted for the second-largest share of the European fish processing market in 2025 due to its rich maritime heritage, extensive fishing fleet, and world-renowned expertise in preserving and canning technologies. The Spanish market is characterized by a dense cluster of processing industries in regions like Galicia and Andalusia, which specialize in high-value canned tuna, mussels, and octopus products that are exported globally. As per data from the Spanish Ministry of Agriculture, Fisheries and Food, the country is a leading producer of canned fish in Europe, with a tradition of craftsmanship that blends seamlessly with modern industrial efficiency. The strong domestic consumption of seafood, deeply embedded in the Mediterranean diet, provides a robust baseline demand for processed products ranging from frozen hake to smoked delicacies. According to the Spanish National Federation of Canned Fish Industries, the sector has successfully pivoted toward premiumization, launching gourmet lines that appeal to discerning consumers willing to pay for quality and origin certification. The presence of major international fishing companies headquartered in Spain facilitates a steady supply of raw materials from global waters, ensuring year-round processing activity. Additionally, significant investments in port infrastructure and cold chain logistics enhance the competitiveness of Spanish processors. The combination of traditional know-how, diverse product portfolios, and strong export orientation ensures Spain remains a critical and dynamic market for fish processing in Europe.

France Fish Processing Market Analysis

France is estimated to register a promising CAGR in the European fish processing market over the forecast period, owing to its sophisticated consumer base that drives demand for high-quality, value-added, and gourmet seafood preparations. The French market is propelled by a strong culinary culture that prizes convenience without sacrificing taste, which is leading to a thriving sector for marinated, smoked, and ready-to-cook fish products. As per the French Office for Seafood, the nation is one of the largest consumers of seafood in Europe, with a particular affinity for premium species like salmon, cod, and shellfish that are often sold in processed forms. The French market focuses heavily on innovation, developing products that align with health trends such as low-sodium options and organic certifications. According to FranceAgriMer, the processed seafood sector has seen consistent growth in the retail channel, supported by aggressive marketing campaigns that highlight the nutritional benefits and French savoir-faire. The presence of large cooperative groups allows small-scale fishermen to access industrial processing capabilities, ensuring a steady flow of local catch into the value chain. Furthermore, France's strict adherence to labeling and origin tracing builds immense consumer trust, fostering loyalty to domestic brands. The strategic emphasis on terroir and gastronomic excellence differentiates French processed fish in the competitive European landscape, securing its status as a key market leader.

United Kingdom Fish Processing Market Analysis

The United Kingdom is expected to exhibit a healthy CAGR in the European fish processing market over the forecast period, owing to its significant role in the primary processing of whitefish and its global reputation for high-quality smoked salmon and kippers. The British market is driven by a strong retail sector that demands a consistent supply of frozen and chilled fillets, supported by a well-established network of processing plants in Scotland, England, and Northern Ireland. As per the Seafood Industry Authority, the UK processes a substantial volume of both domestically caught fish and imports, acting as a gateway for seafood entering the European market. The smoking sector in the UK is particularly renowned, with traditional methods combined with modern hygiene standards producing premium products that are exported worldwide. According to Seafish, the industry body for the UK seafood sector, there is a growing trend toward convenience foods, driving investment in ready-meal production and portion-controlled packs. The post-Brexit landscape has prompted processors to optimize supply chains and explore new export markets while maintaining high standards of food safety and sustainability. The concentration of processing facilities near major ports ensures efficient handling of fresh catches, minimizing time to market. The blend of traditional craftsmanship in smoking and advanced capabilities in freezing and filleting ensures the UK remains a pivotal player in the European fish processing ecosystem.

Denmark Fish Processing Market Analysis

Denmark is estimated to account for a notable share of the European fish processing market during the forecast period due to its advanced aquaculture sector, strong focus on sustainability, and leadership in developing innovative ready-to-eat seafood meals. The Danish market is characterized by a high degree of vertical integration, where companies control the entire value chain from breeding to processing, ensuring exceptional quality and traceability. As per Statistics Denmark, the country is a major exporter of processed fish products, particularly trout and salmon, leveraging its reputation for clean production environments and animal welfare standards. The Danish processing industry is at the forefront of automation, utilizing state-of-the-art machinery to maximize yield and minimize waste, setting benchmarks for efficiency in Europe. According to the Danish AgriFish Agency, there is significant government support for research into new product formulations, including plant-seafood hybrids and functional foods enriched with omega-3. The strong domestic culture of healthy eating fuels demand for convenient, nutritious seafood options available in supermarkets. Furthermore, Denmark's strategic location serves as a logistics hub for distributing processed fish to neighboring Germany and Scandinavia. The commitment to circular economy principles, whereby by-products are converted into valuable ingredients, enhances the sustainability profile of Danish processors. This fusion of technological innovation, sustainable practices, and product development ensures Denmark's continued significance as a top-tier market in the European fish processing industry.

COMPETITION OVERVIEW

The competition in the Europe Fish Processing Market is characterized by intense rivalry among large multinational corporations and specialized regional processors vying for dominance through quality, sustainability, and innovation. Major corporations leverage their extensive global supply chains and economies of scale to offer competitive pricing and consistent product availability to major retail chains. The market sees fierce competition in terms of product differentiation, where factors like organic certification, sustainable sourcing labels, and unique flavor profiles determine brand preference among discerning consumers. Companies are increasingly competing on transparency credentials, with many striving to provide full traceability from boat to plate to build consumer trust. Price competition remains moderate as the critical nature of food safety and quality prioritizes reliability over cost savings for most buyers. Strategic collaborations with fishing fleets and aquaculture farms allow players to secure stable raw material supplies amidst fluctuating quotas. The pressure to continuously innovate with convenient and healthy product formats drives the competitive intensity across the region. Overall, the landscape is dynamic with continuous efforts to balance industrial efficiency with artisanal quality perception,s driving the market forward.

KEY MARKET PLAYERS

A few major players of the Europe fish processing market include

- Leroy

- Pelagia AS

- Maruha Nichiro Corporation

- Pescanova USA

- Royal Greenland A / S

- Thai Union Group Public Company Limited

- High Liner Foods

- NISSUI

- Channel Fish Processing Company Inc

- Charoen Pokphand Foods PCL

- Marine Harvest ASA

Top Strategies Used by the Key Market Participants

Key players in the Europe Fish Processing Market primarily employ vertical integration as a central strategy to control the entire supply chain from aquaculture or capture to the final processed product, ensuring quality and consistency. Companies frequently invest in advanced automation and robotics to overcome labor shortages and improve processing efficiency while maintaining high hygiene standards. Strategic acquisitions of local brands represent another vital approach, allowing firms to expand their product portfolios and gain immediate access to established distribution networks. Partnerships with certification bodies and sustainability organizations help manufacturers validate their eco-friendly practices and appeal to environmentally conscious consumers. Expanding value-added product lines such as ready-to-eat meals and gourmet smoked items serves as a critical tactic to drive higher margins and meet demand for convenience. Additionally, firms focus on digital transformation by implementing traceability systems that provide real-time data on product origin and journey. Sustainability initiatives are also gaining traction as companies strive to reduce waste and optimize energy usage in their operations.

Leading Players in the Europe Fish Processing Market

- Mowi ASA stands as a preeminent force in the Europe Fish Processing Market by operating the largest integrated salmon farming and processing company globally with significant European facilities. The company contributes significantly to the global market by setting benchmarks for sustainability, traceability, and quality in farmed salmon production. Recently, Mowi has focused on expanding its value-added product portfolio, including ready-to-eat meals and smoked range,s to capture higher margins. They have invested heavily in automation and robotics within their processing plants to enhance efficiency and address labor shortages. Their strategic acquisition of smaller local brands allows them to diversify offerings and penetrate niche markets across the continent. This commitment to vertical integration from feed to fork solidifies their leadership position without relying on market share metrics. The continuous innovation in packaging and product development ensures they remain aligned with evolving consumer preferences for convenience and health.

- Thai Union Group PCL operates as a pivotal player in the Europe Fish Processing Market through its extensive network of facilities specializing in canned tuna, frozen seafood, and chilled products under renowned local brands. The company plays a crucial role globally by supplying sustainable seafood solutions that meet the rigorous standards of European retailers and consumers. Recent actions include the acceleration of their SeaChange sustainability strategy, which focuses on reducing environmental impact and improving supply chain transparency. They have launched new plant-based seafood alternatives and expanded their premium chilled food lines to cater to health-conscious demographics. Thai Union actively collaborates with European NGOs and research institutions to advance ocean health and responsible sourcing practices. Their investment in smart manufacturing technologies enhances product safety and operational agility. These strategic moves ensure they remain a trusted partner for major retail chains and food service providers across the region.

- Findus Group Limited maintains a strong presence in the Europe Fish Processing Market by delivering a wide array of frozen fish products, including breaded fillets, fish sticks, and ready meals that are household names across the continent. The company makes a substantial global contribution by pioneering innovations in frozen food technology and sustainable sourcing initiatives. Recently, they have focused on reformulating products to reduce salt and saturated fat content while improving nutritional profiles to align with public health goals. Their strategy involves securing long-term supply contracts with certified fisheries to ensure consistent raw material quality and availability. Findus has also upgraded its processing facilities with energy-efficient equipment to lower carbon emissions and operational costs. They prioritize clear labeling and transparent sourcing information to build consumer trust and loyalty. This dedication to product quality, sustainability, and nutritional excellence strengthens their competitive stance and fosters long-term growth in a dynamic market.

MARKET SEGMENTATION

This research report on the Europe fish processing market has been segmented and sub-segmented based on category, source, equipment & region.

By Category

- Frozen

- Preserved

- Others

By Source

- Marine

- Inland

By Equipment

- Slaughtering

- Gutting

- Scaling

- Filleting

- Deboning

- Skinning

- Smoking

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of this market?

Rising seafood consumption, health awareness, and demand for convenience foods are key drivers.

2. What types of fish products are processed in Europe?

Processed products include frozen fish, canned fish, smoked fish, and ready-to-eat seafood.

3. Which processing methods are commonly used?

Common methods include freezing, curing, smoking, canning, and drying.

4. What are the major end-users of processed fish products?

Retail consumers, restaurants, foodservice providers, and food manufacturers are key end-users.

5. What are the key benefits of processed fish products?

They offer longer shelf life, convenience, and ease of transportation.

6. What challenges does the market face?

Challenges include fluctuating raw fish supply, strict regulations, and sustainability concerns.

7. How is sustainability impacting the market?

There is growing demand for sustainably sourced seafood and eco-friendly processing practices.

8. What role does technology play in fish processing?

Automation, advanced freezing, and packaging technologies improve efficiency and quality.

9. What distribution channels are used?

Supermarkets, hypermarkets, online platforms, and foodservice channels dominate distribution.

10. What is the future outlook of the Europe fish processing market?

The market is expected to grow steadily due to rising seafood demand and innovation in processing technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com