Europe Functional Drinks Market Size, Share, Trends & Growth Forecast Report, Segmented By Product Type (Energy Drinks, Sports Drinks, Others), Functionality, Packaging Type, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis From (2025 To 2033)

Europe Functional Drinks Market Size

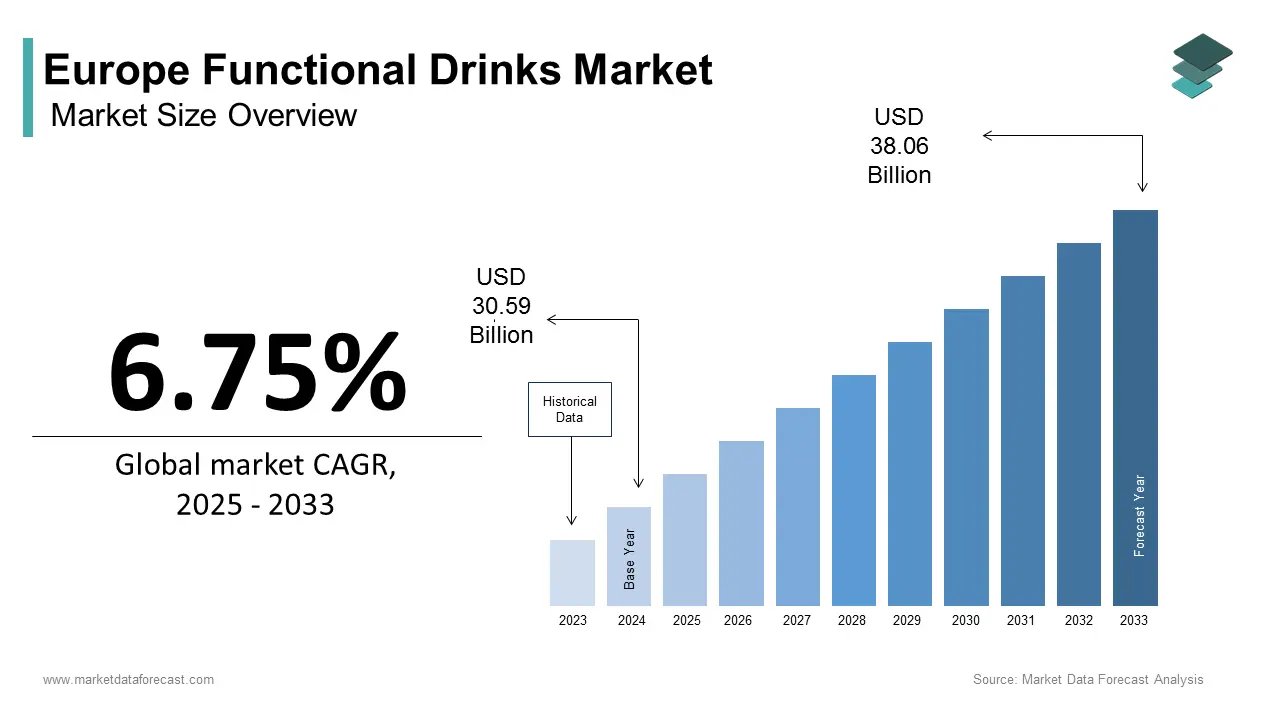

The Europe functional drinks market size was calculated at USD 30.59 billion in 2024 and is anticipated to reach USD 55.06 billion by 2033, from USD 32.65 billion in 2025, growing at a CAGR of 6.75% during the forecast period.

Functional drinks refer to the beverages formulated to deliver physiological benefits beyond basic hydration, including enhanced energy, improved digestion, immune support, cognitive performance, and stress reduction. These products span categories such as sports and energy drinks, probiotic beverages, plant-based adaptogenic tonics, fortified waters, and nootropic infusions. According to Eurostat data from 2024, more than a third of people in the EU (35.3%) reported having a long-standing (chronic) health problem. Meanwhile, the European Food Safety Authority (EFSA) has evaluated thousands of proposed health claims, with over 260 health claims approved for use in the EU by the European Commission. The European Commission’s Farm to Fork Strategy further incentivizes clean label formulations by restricting synthetic additives and promoting transparency. Unlike fleeting wellness fads, functional drinks in Europe are increasingly embedded in daily routines—from post-workout recovery to workplace focus—making them a structural component of the continent’s evolving food and health ecosystem.

MARKET DRIVERS

Rising Prevalence of Lifestyle-Related Chronic Conditions Fuels Preventive Consumption

The growing burden of non-communicable diseases linked to sedentary behavior, poor sleep, and dietary imbalances is propelling the growth of the Europe functional drinks market. This is transforming functional drinks from indulgent novelties into everyday health tools across Europe. According to the World Health Organization Regional Office for Europe, nearly 60 percent of adults in the region are overweight or obese, while one in four suffers from hypertension, creating sustained demand for beverages that support metabolic and cardiovascular wellness. In response, brands are formulating drinks with clinically backed ingredients such as green tea catechins for fat oxidation, magnesium for muscle relaxation, and plant sterols for cholesterol management. Germany and the Nordic countries lead in adoption, with pharmacies and health food stores dedicating entire aisles to functional hydration. This convergence of public health urgency and regulatory validation positions functional drinks as a scalable, palatable, and socially acceptable vehicle for preventive nutrition in an aging and metabolically stressed population.

Demand for Clean Label and Plant-Based Wellness Solutions Drives Product Innovation

European consumers increasingly reject artificial additives and synthetic stimulants in favor of transparent, plant-derived functional ingredients, which drives the expansion of the Europe functional drinks market. As per research, a share of respondents prefer products with fewer than five recognizable ingredients, and a portion actively avoids artificial colors and sweeteners. This preference has accelerated the use of natural alternatives such as stevia, monk fruit, and erythritol for sweetness and adaptogens like ashwagandha, rhodiola, and lion’s mane mushroom for stress resilience and cognitive support. In France and Italy, herbal infusions fortified with elderberry, echinacea, or ginger now dominate the immune health segment, while Scandinavian brands leverage local botanicals like sea buckthorn and cloudberry for antioxidant positioning. Companies have scaled rapidly by emphasizing minimal processing, cold brewing, and recyclable packaging, aligning functional benefits with environmental and ethical values. This clean label imperative is not merely a trend but a structural redefinition of what constitutes a trustworthy health beverage in Europe.

MARKET RESTRAINTS

Stringent EU Health Claim Regulations Limit Marketing Flexibility

The stringent regulatory regime governing nutrition and health claims in Europe acts as a significant constraint on the Europe functional drinks market. This is particularly true in how product benefits are conveyed to consumers. According to research, only a small fraction of the total claims reviewed have been approved. This means that even scientifically substantiated benefits of ingredients like turmeric for inflammation or L-theanine for relaxation cannot be explicitly referenced on packaging unless formally approved. The ambiguity dilutes consumer understanding and diminishes perceived efficacy compared to markets like the United States, where structure-function claims are permitted. Moreover, the approval process takes several months and costs upwards, which deters small and medium enterprises from pursuing legitimate innovations. The framework, while designed to protect against misinformation, inadvertently stifles category growth by limiting the ability to educate consumers on evidence-based benefits.

Sugar Content Scrutiny and Fiscal Policies Dampen Energy and Sports Drink Growth

Aggressive public health policies targeting sugar consumption further constrain the expansion of the Europe functional drinks market. As per studies, Adults in the European region generally have a very high average annual sugar consumption. In response, Several European countries have put in place specific taxes on sugar-sweetened beverages. The United Kingdom's tax successfully reduced beverage sugar content and decreased high sugar drink sales. Major brands have reformulated with artificial or natural sweeteners, yet face consumer skepticism over long-term health impacts. Consequently, companies must balance functional efficacy with nutritional compliance, a challenge that slows innovation and limits appeal among taste-driven younger demographics.

MARKET OPPORTUNITIES

Expansion into Mental Wellness and Cognitive Performance Niches

The growing recognition of mental health as integral to overall wellbeing has opened a potential opportunity for the Europe functional drinks market. This is centered on stress resilience, focus, and emotional balance. According to research, millions of people in Europe suffer from mental health disorders, with anxiety and burnout rising sharply among urban professionals and students. This has spurred demand for nootropic and adaptogenic beverages formulated with ingredients like L-theanine, bacopa monnieri, and phosphatidylserine, clinically associated with reduced cortisol and improved attention. Brands have gained traction in workplaces and universities by positioning their drinks as “brain fuel” alternatives to coffee. Retailers like E.Leclerc and DM Drogerie now feature dedicated mind care shelves. The integration of mental wellness into national health strategies further legitimizes the category. Cognitive functional drinks are poised to move from niche to mainstream as stigma declines and neuroscience literacy rises.

Integration of Functional Beverages into Clinical and Preventive Nutrition Pathways

These drinks are increasingly being incorporated into medical nutrition therapy and public health prevention programs across Europe, which creates major prospects for the expansion of the Europe functional drinks market. According to studies, Specialized oral nutritional supplements, such as protein-enriched and micronutrient-fortified beverages, are increasingly recommended in clinical settings for hospitalized elderly patients to fight malnutrition and muscle loss. In some nations like the Netherlands and Sweden, these nutritional products are routinely covered by national health services to aid post-surgical recovery and manage chronic diseases. Simultaneously, public health initiatives are piloting functional hydration in schools and workplaces. Government-led health initiatives are emerging, with countries like Finland launching pilot programs to integrate functional drinks, such as probiotics, into public institutions like high schools to improve student health. The European Commission is actively supporting numerous international research projects that test the effectiveness of functional beverages in addressing widespread health concerns like metabolic syndrome and cognitive decline. This clinical and policy endorsement elevates functional drinks from consumer choice to an evidence-based public health tool, opening new B2B revenue streams and enhancing scientific credibility.

MARKET CHALLENGES

Inconsistent National Interpretations of Novel Food and Ingredient Regulations

Significant disparities persist among member states in interpreting and enforcing regulations governing novel ingredients, which creates operational complexity and market fragmentation and thereby hinders the growth of the Europe functional drinks market. This regulatory patchwork forces manufacturers to develop multiple formulations for different markets, increasing costs and delaying pan-European launches. Moreover, the use of certain probiotic strains approved under the Qualified Presumption of Safety list may still face resistance from national food safety authorities without additional dossiers. These inconsistencies undermine the single market principle and discourage investment, particularly among small producers lacking legal resources to navigate jurisdictional variability.

Greenwashing Allegations and Sustainability Credibility Gaps

The rising environmental consciousness of European consumers, which means they are increasingly skeptical of sustainability claims from functional drink brands (especially concerning packaging recyclability and carbon footprint), hampers the expansion of the Europe functional drinks market. Many functional beverage labels utilize terms such as "eco-friendly" or "planet positive" without third-party verification or clear metrics. New European regulations now require all environmental claims to be supported by evidence, leading authorities to issue formal warnings against brands making misleading assertions like those for "biodegradable" bottles made from non-recyclable materials. Moreover, the carbon intensity of imported superfoods like maqui berry or moringa, often flown from South America or Africa, contradicts local sourcing narratives. Brands risk consumer distrust and regulatory penalties, affecting the very wellness values they seek to embody, until they adopt transparent supply chain disclosures and standardized environmental labelling.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.75% |

| Segments Covered | By Product Type, Functionality, Packaging Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Red Bull GmbH, PepsiCo, The Coca-Cola Company, Danone S.A., Nestlé S.A., Monster Beverage Corp., Keurig Dr Pepper, Suntory Holdings (Lucozade), Oatly Group, Glanbia plc, Campbell Soup Company (V8), The Kraft Heinz Company, AriZona Beverages, Califia Farms. |

SEGMENTAL ANALYSIS

By Product Type Insights

The energy drinks segment held the leading share of 42.5% of the Europe functional drinks market in 2024. The supremacy of the energy drinks segment is attributed to sustained demand among young adults and shift workers seeking alertness and mental performance enhancement. Urbanization and extended digital work hours have normalized midday consumption beyond athletic contexts. Apart from these, major brands have reformulated to comply with sugar taxes by introducing zero-calorie variants using sucralose and acesulfame K, which represent a portion of energy drink sales in taxed countries. The integration of B vitamins, taurine, and ginseng further reinforces perceived cognitive benefits. Despite regulatory scrutiny, energy drinks remain culturally entrenched as a lifestyle staple, particularly among 18- to 34-year-olds who view them as essential productivity tools in fast-paced environments.

The adaptogenic and nootropic beverages segment is estimated to register the fastest CAGR of 21.3% between 2025 and 2033 due to rising awareness of mental wellness and cognitive resilience in high-stress urban populations. These drinks feature clinically studied ingredients such as L-theanine, ashwagandha, bacopa monnieri, and lion’s mane mushroom, which are associated with reduced cortisol levels and improved focus. Brands have scaled through workplace wellness programs and university partnerships targeting students during exam periods. Retailers, including DM Drogerie and Monoprix, have created dedicated mental performance aisles with double-digit year-on-year sales growth.

By Functionality Insights

The digestive health segment was the largest in the Europe functional drinks market by capturing a 33.6% share in 2024. The supremacy of the digestive health segment is propelled by high consumer awareness of gut microbiome science and the widespread prevalence of digestive discomfort. Probiotic beverages, particularly those containing Lactobacillus and Bifidobacterium strains, have gained mainstream acceptance with the European Food Safety Authority authorizing a health claim for Lactobacillus casei Shirota in relation to improved gut transit. Major dairy and plant-based brands, including Yakult Danone and Remedy Drinks, have expanded refrigerated probiotic lines across supermarkets and pharmacies. The cultural normalization of gut health as foundational to immunity and mental well-being has transformed digestive beverages from niche wellness items into daily dietary staples across age groups.

The cognitive and mental performance support segment is anticipated to witness the fastest CAGR of 24.7% from 2025 to 2033, owing to escalating rates of workplace burnout, academic stress, and digital fatigue across Europe. As per sources, a share of employees report chronic mental exhaustion, with younger cohorts most affected. Functional beverages formulated with nootropics such as phosphatidylserine, bacopa monnieri, and L-theanine are gaining traction as non-stimulant alternatives to caffeine. Retailers have responded by launching “mind care” sections featuring chilled functional tonics. Universities have piloted the distribution of nootropic drinks during exam weeks. This segment bridges nutrition, neuroscience, and preventive care as mental wellness becomes a public health priority.

By Packaging Type Insights

The PET bottles segment led the Europe functional drinks packaging market by occupying a 58.1% share in 2024. Factors such as cost efficiency, lightweight design, and compatibility with high-speed filling lines used by major beverage manufacturers have mainly contributed to the growth of the PET bottles segment. PET is particularly favored for single-serve energy and sports drinks, which account for the bulk of functional beverage volume. The material’s transparency also allows for vibrant label designs that communicate premium functional positioning. Major brands have transitioned to recycled PET in Western Europe, complying with extended producer responsibility schemes. The material’s barrier properties also preserve the potency of sensitive ingredients like vitamins and probiotics better than aluminum in certain formulations. PET will remain the default for mass market functional hydration until alternative packaging achieves comparable economics and shelf life.

The aluminum cans segment is likely to experience the fastest CAGR of 17.8% between 2025 and 2033. The rapid expansion of the aluminum cans segment is propelled by superior recyclability, circular economy alignment, and strong consumer perception of premiumness and portability. Aluminum has a notable recycling rate in the EU, the highest of any beverage packaging material. Brands targeting health-conscious and eco-aware consumers, such as Ugly Drinks and Liquid I.V., have adopted slim cans to convey modernity and sustainability. The format is also ideal for carbonated adaptogenic and electrolyte drinks, which require pressure resistance. Additionally, cans offer better light and oxygen protection, preserving the stability of light-sensitive botanicals like curcumin and anthocyanins.

REGIONAL ANALYSIS

Germany Functional Drinks Market Analysis

Germany was the top performer in the Europe functional drinks market and accounted for a 21.7% share in 2024. The prominence of the German market is driven by high health literacy, strong purchasing power, and a culture of preventive wellness. The country leads in probiotic and plant-based functional beverages, with numerous kombucha and kefir brands available in mainstream retail. Energy drink consumption remains robust. Regulatory clarity from the Federal Office of Consumer Protection enables compliant health claims for vitamins and minerals, accelerating product development. Apart from these, Germany’s dense network of reformhäuser health food stores provides a trusted channel for premium functional hydration. The rise of workplace wellness programs in the automotive and tech sectors has further normalized functional drink consumption during work hours. With a population deeply engaged in nutritional science and sustainability, Germany sets both volume and innovation benchmarks for the broader European market.

United Kingdom Functional Drinks Market Analysis

The United Kingdom followed closely in the Europe functional drinks market by occupying a 17.3% share in 2024 because of early adoption of global wellness trends and a responsive regulatory environment. The UK was among the first European countries to implement a sugar tax, spurring rapid reformulation, with a share of energy drinks now offering sugar-free variants. London serves as a launchpad for premium nootropic and adaptogenic brands like Nootopia and Form Adaptogens, which leverage digital marketing and subscription models. The National Health Service’s focus on preventive care has indirectly validated functional hydration, with GPs increasingly discussing diet-based mental health strategies. In addition, the UK Food Standards Agency updated its guidance to facilitate novel food approvals for botanical extracts, accelerating time to market. Consumer trust in certified health claims remains high. This blend of policy innovation, entrepreneurial energy, and health-conscious consumers sustains the UK’s leadership in high-value functional beverage categories.

France Functional Drinks Market Analysis

France maintains a noteworthy player in the Europe functional drinks market, with its preference for natural botanicals and strong regulatory caution toward synthetic ingredients. French consumers favor herbal infusions fortified with elderberry, ginger, and echinacea, particularly in immune support beverages, as documented by the French Agency for Food, Environmental and Occupational Health and Safety. The country’s “Made in France” movement has boosted local production of plant-based functional drinks using regional ingredients like thyme, rosemary, and maritime pine. Major retailers dedicate significant shelf space to organic and functional hydration, with private label offerings expanding rapidly. The French National Nutrition and Health Program’s emphasis on gut microbiome health has further legitimized probiotic beverages. France exemplifies how cultural values can shape a distinct functional drink identity within the European landscape by balancing tradition with innovation.

Italy Functional Drinks Market Analysis

Italy grew steadily in the Europe functional drinks market due to Mediterranean dietary principles and rising interest in digestive wellness. The country is Europe’s largest consumer of probiotic beverages per capita, with Yakult and local brands deeply integrated into daily routines. Italian consumers prefer functional drinks that align with culinary heritage, leading to the success of beverages infused with citrus bergamot, artichoke, and olive leaf polyphenols known for metabolic benefits. Energy drink consumption remains moderate due to cultural preference for espresso, yet sports and rehydration drinks are gaining traction among fitness enthusiasts, particularly in urban centers like Milan and Rome. Italy’s market success is built on a foundation of high trust in natural remedies and a strong pharmacy distribution network, which fosters a thriving environment for authentic, efficacious, and sensorially appealing products rooted in its rich botanical and nutritional legacy.

Spain Functional Drinks Market Analysis

Spain is anticipated to grow in the Europe functional drinks market between 2025 and 2033, owing to strong demand for hydration solutions suited to its warm climate and active lifestyle. Sports and electrolyte drinks dominate with consumption peaking during summer months and major sporting events, as reported by the Spanish Soft Drinks Association. The country is also a leader in aloe vera and antioxidant fortified beverages, leveraging its abundant cultivation of citrus and grape polyphenols. Urban wellness trends in cities like Barcelona and Madrid have accelerated the adoption of nootropic and adaptogenic tonics among young professionals. Retailers such as Mercadona have launched affordable private-label functional lines, driving mass market accessibility. Spain's functional drinks market balances performance, practicality, and preventive care in a sun-drenched context, thanks to a culture that blends Mediterranean health traditions with modern fitness consciousness.

COMPETITION OVERVIEW

Competition in the Europe functional drinks market is characterized by a dynamic interplay between multinational beverage giants, regional specialists, and agile start-ups. Established players like Red Bull, Coca-Cola, and PepsiCo dominate volume through extensive distribution, brand recognition, and economies of scale, yet face mounting pressure from niche brands offering premium clean-label plant-based formulations. The market is highly fragmented, with over 500 new functional drink launches recorded in Europe in 2024 alone, according to FoodDrinkEurope, reflecting intense innovation. Differentiation hinges on scientific substantiation, ingredient transparency, and alignment with lifestyle values such as mental wellness, sustainability, and athletic performance. Regulatory complexity adds another layer as companies navigate inconsistent national interpretations of health claims and novel food rules. Despite barriers, small brands gain traction through e-commerce, specialty retail, and social media storytelling. The result is a competitive landscape where authenticity, agility, and regulatory precision are as critical as scale and marketing spend in capturing consumer trust and loyalty.

KEY MARKET PLAYERS

A few major players of the Europe functional drink market include

- Red Bull GmbH

- PepsiCo

- The Coca-Cola Company

- Danone S.A

- Nestlé S.A

- Monster Beverage Corp

- Keurig Dr Pepper

- Suntory Holdings (Lucozade)

- Oatly Group

- Glanbia plc

- Campbell Soup Company (V8)

- The Kraft Heinz Company

- AriZona Beverages

- Califia Farms

Top Strategies Used by the Key Market Participants

Key players in the Europe functional drinks market employ several strategic approaches to maintain relevance and drive growth. Product reformulation is central with companies reducing sugar, eliminating artificial additives, and incorporating clinically supported functional ingredients like probiotics, adaptogens, and electrolytes. Brand diversification allows portfolios to span energy, sports hydration, and mental wellness, addressing distinct consumer needs. Sustainability integration features prominently through the adoption of recycled packaging, lightweighting, and carbon-neutral production aligned with EU environmental mandates. Strategic partnerships with fitness centers, universities, and health professionals enhance credibility and access. Digital engagement via social media influencer collaborations and direct-to-consumer platforms builds community and loyalty. Finally, regulatory agility ensures compliance with evolving health claim and labeling laws across diverse national markets, preserving both innovation speed and legal safety.

Leading Players in the Market

Red Bull GmbH

Red Bull GmbH is a pioneering force in the Europe functional drinks market, having established the modern energy drink category through aggressive branding and lifestyle marketing. Headquartered in Austria, the company supplies its signature functional beverage across all European countries and has expanded into zero-sugar and organic variants to align with evolving health regulations. Red Bull plays a significant role globally by sponsoring extreme sports events, music festivals, and esports, which reinforces brand affinity among young consumers. It also invested in sustainable packaging by transitioning its entire European can portfolio to 100 percent recycled aluminum, strengthening its environmental credentials while maintaining product performance and appeal.

The Coca-Cola Company

The Coca Cola Company maintains a strong presence in the Europe functional drinks market through diverse brand portfolios, including Powerade for sports hydration and Relentless for energy. The company leverages its extensive distribution network and retail partnerships to ensure wide availability across supermarkets, convenience stores, and gyms. Globally Coca Coca-Cola integrates functional innovation into its core strategy by acquiring or developing science-backed beverages that address hydration recovery and mental alertness. Coca-Cola also enhanced its sustainability commitments by piloting plant-based PET bottles for functional lines in Germany and France, reinforcing brand trust through environmental responsibility and regulatory compliance.

PepsiCo Inc

PepsiCo Inc. contributes significantly to the Europe functional drinks landscape primarily through its Rockstar and Gatorade brands, which cater to energy and sports performance segments, respectively. The company combines scientific formulation with mass marketing to reach both athletic and everyday consumers. Globally, PepsiCo emphasizes functional nutrition as part of its “Winning with Purpose” agenda, focusing on products that support physical performance and metabolic health. The company also partnered with European fitness chains to offer site-to-site hydration solutions, enhancing direct consumer engagement. By aligning product development with clean label trends and sustainability goals, PepsiCo strengthens its relevance in Europe’s increasingly health-conscious beverage ecosystem.

MARKET SEGMENTATION

This research report on the Europe functional drinks market has been segmented and sub-segmented based on Product type, functionality, packaging type, and region.

By Product Type

- Energy Drinks

- Sports Drinks

- Others

By Functionality

- Digestive Health

- Immune Support

- Others

By Packaging Type

- PET/Glass Bottles

- Aluminium Cans

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What segments are included in the Europe functional drinks market?

Major segments include energy drinks, sports drinks, functional juices, ready-to-drink (RTD) teas, probiotic drinks, enhanced water, and plant-based functional beverages.

2. What is driving the growth of the Europe functional drinks market?

Key drivers include rising health consciousness, increasing demand for immunity-boosting products, growth in fitness culture, and rising urbanization and premium beverage consumption.

3. Which countries lead the functional drinks market in Europe?

The leading markets are Germany, the United Kingdom, France, Italy, and Spain.

4. Who are the key consumers of functional drinks in Europe?

Millennials, young professionals, fitness enthusiasts, athletes, and individuals seeking convenience-based nutritional options.

5. What trends are shaping the Europe functional drinks market?

Key trends include clean-label beverages, sugar-free/low-calorie drinks, plant-based functional drinks, gut-health/probiotic drinks, and natural energy formulations.

6. Which distribution channels dominate the functional drinks sector in Europe?

Supermarkets/hypermarkets, convenience stores, online retail, and fitness centers.

7. What challenges does the Europe functional drinks market face?

Challenges include stringent EU regulations, high product costs, increasing competition, and concerns about sugar/energy drink overconsumption.

8. What role does innovation play in this market?

Brands are focusing on botanical blends, nootropic drinks, protein-infused beverages, and sustainable packaging solutions to attract health-conscious consumers.

9. Which functional beverage segment is growing the fastest in Europe?

Probiotic drinks, RTD teas, and enhanced water are currently witnessing the highest growth due to strong demand for immunity and digestion support.

10. What is the future outlook for the Europe functional drinks market?

The market is expected to grow strongly due to rising health awareness, premiumization, and increasing adoption of functional beverages as part of daily lifestyle routines.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com