Europe Luxury Clothing Market Size, Share, Trends & Growth Forecast Report By End User, By Distribution Channel, and By Country (Italy, France, United Kingdom, Germany, Switzerland & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

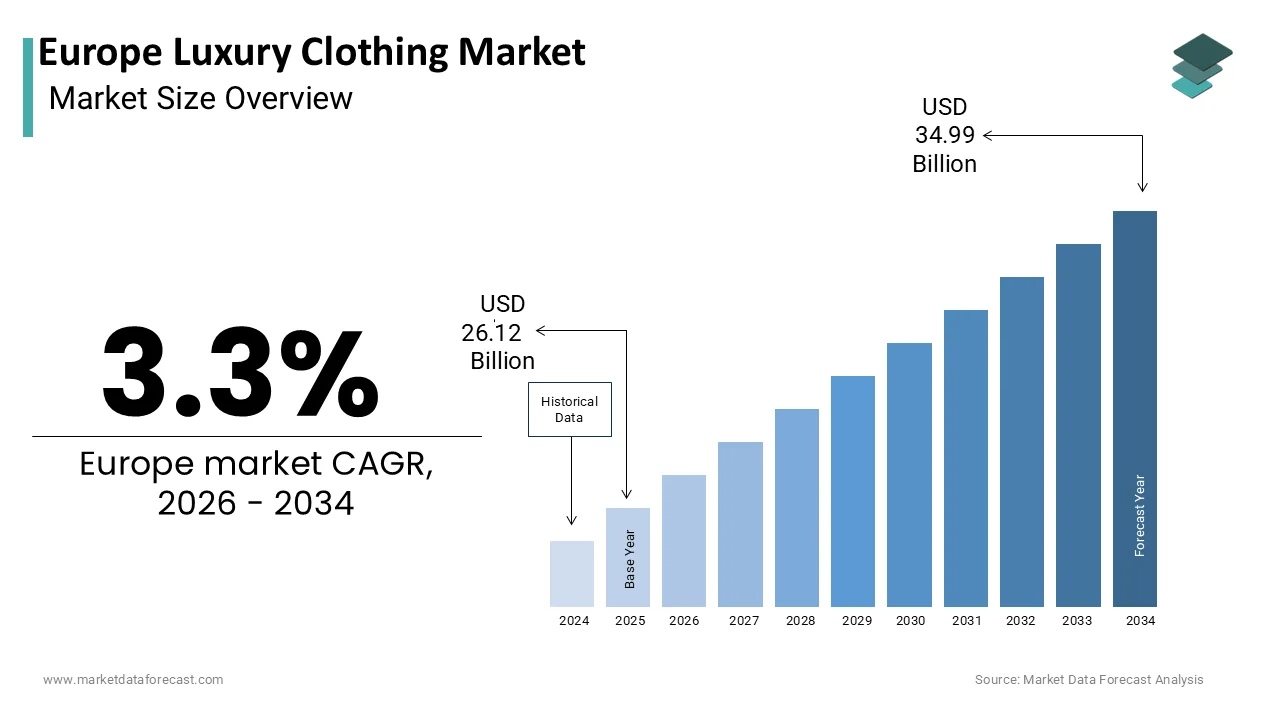

$26.12 BnMarket Estimate, 2026

$26.99 BnMarket Forecast, 2034

$34.99 BnCAGR, 2026–2034

3.30%Europe Luxury Clothing Market Size

The Europe luxury clothing market was valued at USD 26.12 billion in 2025, is estimated to reach USD 26.99 billion in 2026, and is projected to reach USD 34.99 billion by 2034, growing at a CAGR of 3.30% from 2026 to 2034.

Luxury clothing represents the apex of the global fashion industry and is defined by the creation of high-value garments that prioritize exceptional material quality, artisanal heritage, and limited availability over mass production. This sector encompasses ready-to-wear collections, haute couture, and bespoke tailoring produced primarily within the historic fashion capitals of Paris, Milan, London, and Florence. The definition extends beyond mere apparel to include an ecosystem of protected geographical indications and specialized craftsmanship clusters that have operated for centuries. In 2024, the European Union registered a significant number of protected designations of origin safeguarding the authenticity of textiles and manufacturing techniques crucial to luxury clothing production, according to the European Commission. The market is characterized by a rigorous supply chain where raw materials such as vicuña wool, Scottish cashmere, and Italian silk are sourced from specific regions to ensure unparalleled texture and durability. As per Eurostat, the textile and clothing sector in Europe employs a large workforce, with a notable concentration in high-skill roles dedicated to luxury garment assembly. This labor intensity distinguishes the market from standard fashion, as a single luxury coat may require extensive hours of manual labor by master tailors. The current scenario reflects a shift toward "slow luxury," where consumers value the narrative of creation and the longevity of the piece, driving a rejection of disposable fast fashion in favor of investment-grade clothing that retains value over time.

MARKET DRIVERS

Expansion of the Ultra-High-Net-Worth Demographic

The rapid expansion of the Ultra-High-Net-Worth Individual population in Europe is primarily driving the growth of the European luxury clothing market, which is creating a buffer against broader economic volatility. This demographic segment possesses significant disposable income that is largely immune to inflationary pressures, allowing for consistent expenditure on high-ticket garments and bespoke services. According to the Global Wealth Report published by UBS, the number of millionaires in Europe has continued to rise, with the ultra-wealthy segment showing steady annual growth. This accumulation of capital directly translates into increased purchasing power for exclusive clothing items, where price is secondary to exclusivity and brand heritage. Affluent consumers view luxury clothing not merely as attire but as a store of value and a symbol of social stratification, leading to frequent acquisitions of limited-edition collections and custom-made suits. As per private wealth management firms, the top earners in Western Europe allocate a notable portion of their discretionary spending specifically to luxury apparel and accessories. Furthermore, the migration of wealthy individuals from emerging markets to European hubs such as London, Monaco, and Geneva has intensified local demand for personalized shopping experiences.

Revival of Artisanal Craftsmanship and Heritage Value

A profound shift in consumer values towards authenticity and visible craftsmanship is significantly propelling the Europe luxury clothing market, as buyers increasingly reject homogenized mass production in favor of garments that showcase human skill. Modern luxury consumers, particularly within the Millennial and Gen Z demographics, are willing to invest heavily in clothing that features hand-stitching, intricate embroidery, and natural dyeing techniques that signify true artistry. As per Deloitte surveys, a large majority of luxury shoppers in Europe consider the story behind the product and the specific craftsmanship involved as critical factors in their purchasing decisions. This demand validates the high price points of European luxury brands, which frequently highlight their historic ateliers and master artisans in marketing narratives to emphasize exclusivity. The tangible difference in quality, durability, and fit provided by skilled craftsmen creates a compelling value proposition that machine-made alternatives cannot replicate. Furthermore, the rise of "quiet luxury" or "stealth wealth" trends emphasizes understated elegance and superior fabric quality over conspicuous branding. As per fashion institutes, demand for semi-bespoke and fully bespoke services has been increasing year over year, which reflects a desire for uniqueness and longevity.

MARKET RESTRAINTS

Volatility in Premium Raw Material Costs

The luxury clothing market in Europe faces significant headwinds due to the escalating costs and scarcity of premium raw materials, which directly impact production margins and final retail pricing. Prices for high-quality fibers such as cashmere, vicuña, and organic silk have experienced sharp increases, driven by climate change impacts on livestock and limited supply availability in key grazing regions. According to the Food and Agriculture Organization, global cashmere production has declined in recent years due to harsh weather conditions, leading to scarcity-driven price surges that affect European manufacturers disproportionately. This volatility forces luxury brands to either absorb the increased costs, thereby squeezing profitability, or pass them on to consumers, risking demand elasticity among aspirational buyers. The cost of producing fine wool in Europe has also risen significantly since 2022, exacerbated by rising energy costs required for processing and dyeing processes. Furthermore, the reliance on specific geographic regions for these materials creates supply chain vulnerabilities, as any disruption can halt production lines for entire collections. As per textile trading platforms, the price index for luxury natural fibers has reached historic highs, challenging the traditional cost structures of luxury fashion houses.

Stringent Environmental Regulations and Compliance Burdens

The implementation of the European Union's Strategy for Sustainable and Circular Textiles imposes rigorous compliance requirements, which further hamper the European luxury clothing market expansion. This legislative framework mandates extended producer responsibility, requiring brands to manage the entire lifecycle of their products, including collection, recycling, and disposal, which necessitates substantial investment in new infrastructure. According to the European Commission, new regulations introduced in 2024 require digital product passports for all textile items, detailing material composition, origin, and recyclability, forcing brands to overhaul their data management systems. Luxury clothing houses, often reliant on complex and opaque supply chains involving multiple tiers of suppliers, face immense challenges in gathering and verifying this data to ensure full compliance. As per environmental consultancies, compliance costs could increase operational expenditures considerably for mid-sized fashion brands. Furthermore, the ban on the destruction of unsold goods, a common practice in the luxury sector to maintain exclusivity, forces companies to find alternative disposal methods such as discounting or donating, which can dilute brand equity. These regulatory pressures create a high barrier to entry and expansion, slowing down the agility of the market.

MARKET OPPORTUNITIES

Integration of Digital Product Passports and Blockchain

The adoption of Digital Product Passports and blockchain technology offers a promising opportunity for the Europe luxury clothing market to enhance transparency and effectively combat counterfeiting. By embedding unique digital identifiers into garments, brands can provide consumers with immutable records of a product's journey from raw material to retail shelf, ensuring authenticity. According to the Ellen MacArthur Foundation, the implementation of such traceability systems has the potential to significantly reduce the incidence of counterfeit luxury goods by providing verifiable proof of origin and craftsmanship. This technology empowers consumers to scan a QR code and access detailed information about the garment's history, aligning with the growing demand for ethical consumption and supply chain visibility. Luxury houses leveraging blockchain have reported notable increases in consumer trust scores, as verified by brand perception studies conducted in major European capitals. Furthermore, these digital passports facilitate the resale market by maintaining a permanent history of ownership and condition, thereby supporting the circular economy model and extending the lifecycle of luxury items. As per resale platforms, items with verified digital histories tend to sell faster and at higher prices than those without.

Expansion of the Pre-Owned and Rental Luxury Sector

The burgeoning pre-owned and rental luxury market represents a substantial opportunity for European brands to tap into the circular economy and attract environmentally conscious consumers who prioritize sustainability. As sustainability becomes a core value for younger demographics, the stigma surrounding second-hand luxury is rapidly dissipating, replaced by an appreciation for vintage finds and accessible exclusivity. According to ThredUp's Resale Report, the European second-hand luxury clothing market is projected to grow significantly faster than the primary market in the coming years. Luxury houses that embrace this trend by launching their own certified pre-owned platforms or partnering with established resale sites can capture value from multiple lifecycles of a single garment, maximizing revenue potential. As per Bain & Company, a majority of Gen Z consumers in Europe are willing to buy pre-owned luxury items, viewing it as a smart and sustainable choice that aligns with their values. This shift allows brands to engage with customers who might otherwise be priced out of the primary market, fostering loyalty from an early age. The rental model also offers flexibility for special occasions, appealing to consumers who desire variety without the commitment of ownership.

MARKET CHALLENGES

Proliferation of High-Quality Counterfeit Goods

The pervasive issue of high-quality counterfeit goods is a severe challenge to the Europe luxury clothing market, eroding brand equity and siphoning off significant revenue from legitimate businesses. Advanced manufacturing technologies have enabled counterfeiters to produce "super fakes" that are nearly indistinguishable from authentic items, confusing even knowledgeable consumers and diluting exclusivity. According to the Organisation for Economic Co-operation and Development, the trade in counterfeit textiles and clothing accounts for a significant portion of global trade, with Europe being a primary target due to its concentration of luxury brands and high consumer demand. Financial estimates suggest that the luxury sector loses billions of euros annually to counterfeiting, which is a figure that continues to rise as online marketplaces and social media platforms make fake goods more accessible. As per customs enforcement agencies, seizures of counterfeit luxury clothing in EU ports have been increasing, highlighting the scale and sophistication of the problem. Combating this challenge requires constant vigilance, legal action, and technological innovation, diverting resources away from creative and strategic initiatives.

Shifting Consumer Preferences and Generational Divides

The European luxury clothing market faces the intricate challenge of bridging the widening gap between traditional brand heritage and the evolving values of younger generations who prioritize different metrics of value. Millennials and Gen Z consumers emphasize sustainability, inclusivity, and digital engagement over the legacy and exclusivity that historically defined luxury clothing. According to Boston Consulting Group, a majority of Gen Z shoppers in Europe are likely to boycott brands that do not demonstrate a clear commitment to social and environmental causes, posing a significant risk to legacy houses with opaque supply chains. As per social listening tools, sentiment towards luxury brands perceived as out of touch with modern ethical standards has declined, indicating potential loss of market share. Additionally, the preference for experiential spending over material possessions among younger demographics challenges traditional growth models of clothing brands. Balancing the expectations of older, loyal clients who value classicism with the demands of younger buyers seeking innovation creates a strategic dilemma that requires careful navigation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End User, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | LVMH Moët Hennessy Louis Vuitton SE, Kering S.A., Chanel Limited, Hermès International S.A., Prada S.p.A., Burberry Group plc, Dolce & Gabbana S.r.l., Giorgio Armani S.p.A., Hugo Boss AG, Ralph Lauren Corporation, Capri Holdings Limited, Moncler S.p.A. |

SEGMENTAL ANALYSIS

by End Use Insights

The women's segment dominated the market by holding 66.9%of the regional market share in 2025. The growth of the women’s segment in the European market is majorly driven by the wide variety of product categories available to female consumers, ranging from haute couture and ready-to-wear to seasonal essentials, which creates more frequent purchase occasions compared to other demographics. The primary driving factor is the deep cultural integration of fashion as a primary medium for self-expression and social signaling among European women, particularly in fashion capitals like Paris and Milan. According to the French Fashion Federation, women account for the majority of luxury fashion purchases in France, a trend that mirrors the broader European landscape, where wardrobe updates are a normative social behavior driven by seasonal changes and event attendance. Another critical driver is the immense influence of marketing and media ecosystems that disproportionately target female audiences with aspirational imagery and influencer collaborations. As per advertising expenditure reports, a significant portion of luxury clothing marketing budgets in Europe is allocated to campaigns featuring women's collections, reinforcing brand desirability and creating constant demand. Furthermore, the gifting culture surrounding holidays and special occasions heavily favors women's apparel, boosting sales volumes throughout the year. Continuous innovation in silhouettes, fabrics, and trends specifically designed for women ensures a perpetual cycle of demand, solidifying this segment's position as the financial backbone of the luxury clothing market.

However, the men's segment is emerging as the fastest-growing end-user category and is anticipated to expand at a CAGR of 9.1% over the forecast period, owing to a fundamental shift in societal norms where men are increasingly viewing fashion as a crucial component of their identity, professional success, and lifestyle expression. The rise of the modern masculine aesthetic, encouraged by social media influencers and celebrities, showcases bold, sophisticated, and varied styles beyond traditional suits. According to GlobalData, the European men's luxury clothing market has been expanding rapidly, with notable spikes in demand for luxury streetwear, premium casual wear, and tailored separates. Another driver is the increasing participation of men in the luxury shopping journey, moving away from reliance on partners for clothing choices to becoming active, knowledgeable, and confident consumers. As per luxury retail associations, men now spend considerably more time researching brands and products online before purchasing, indicating deeper engagement and a willingness to invest in quality. Additionally, the blurring of lines between formal and casual dress codes in the workplace has expanded the occasions for wearing luxury menswear, driving daily usage and repeat purchases. With brands launching dedicated menswear lines and flagship stores, the men's segment is positioned as the most dynamic area for future expansion.

By Distribution Channel Insights

The offline segment held the commanding lead in the Europe luxury clothing market with a share of 60.9% of the regional market in 2025. This dominance is anchored in the intrinsic need for a tactile, immersive, and highly personalized brand experience that defines the luxury purchasing journey for high-value garments. The primary driver is the unparalleled level of service and exclusivity offered in these physical environments, which allows customers to feel fabric textures, try on fits, and receive dedicated styling advice that cannot be replicated digitally. According to Bain & Company, a majority of luxury consumers in Europe prefer purchasing high-ticket clothing items in boutiques where they can engage directly with brand ambassadors and enjoy private viewing appointments. These spaces serve as brand temples that reinforce heritage and prestige, allowing customers to immerse themselves in the product narrative and history. Another driver is the assurance of authenticity and immediate possession that specialist retailers provide, mitigating the risk of counterfeits and delivery delays prevalent in other channels. As per the European Union Intellectual Property Office, unauthorized goods are significantly less common in authorized offline networks, fostering deep trust among affluent buyers. The strategic location of these stores in prestigious shopping districts creates a destination effect, drawing tourists and locals alike.

However, the online segment is experiencing the most rapid expansion and is expected to witness a CAGR of 13.3% over the forecast period, due to the digital transformation of luxury brands and the evolving shopping habits of younger, tech-savvy demographics who demand convenience, seamless integration, and instant access to global collections. The foremost driver is the significant investment by luxury houses in sophisticated e-commerce platforms that offer high-resolution imagery, 360-degree views, virtual try-on technologies, and personalized AI-driven recommendations. According to McKinsey, online luxury clothing sales in Europe have grown strongly, with mobile commerce accounting for the majority of traffic, highlighting the decisive shift towards smartphone-first shopping experiences. Another factor is the expansion of omnichannel services such as click-and-collect, virtual appointments, live chat styling, and hassle-free return policies, which bridge the gap between digital convenience and physical assurance. As per luxury e-tailers, implementing augmented reality features has reduced return rates while increasing conversion rates, addressing previous barriers to online luxury adoption regarding fit and feel. Additionally, the reach of online channels allows brands to tap into secondary cities and regions without a physical presence, unlocking vast new customer bases. The integration of social commerce, where purchases can be made directly through social media platforms, further accelerates growth, making online retail the most agile and rapidly scaling distribution channel.

COUNTRY LEVEL ANALYSIS

Italy Luxury Clothing Market Analysis

Italy stood as the paramount leader in the Europe luxury clothing market by holding a dominant share of 29.2% of the regional market in 2025. The dominance of Italy in the European market is attributed to its status as a global manufacturing and design powerhouse. The market in Italy is unique because it serves as both a primary production hub and a voracious domestic consumer base, creating a synergistic ecosystem where supply and demand reinforce each other. A key driving factor is the concentration of world-renowned fashion houses in Milan, Florence, and Rome, which attract millions of international tourists specifically for luxury clothing shopping. According to the National Chamber of Italian Fashion, the fashion system in Italy generated significant turnover in 2024, with a large portion derived from domestic luxury clothing sales and export revenue. Another critical driver is the deep-rooted cultural appreciation for "Made in Italy" craftsmanship, where local consumers prioritize quality and heritage over fleeting trends. As per ISTAT, Italian households spend considerably more on luxury clothing compared to the European average, reflecting a national commitment to dressing well as a social imperative. Furthermore, the dense network of artisanal districts ensures a steady supply of exclusive, high-quality garments.

France Luxury Clothing Market Analysis

France secured the second leading position in the regional market in 2025 due to its unparalleled heritage in haute couture and its status as the global capital of luxury branding. The market status here is characterized by the presence of the world's largest luxury conglomerates, whose headquarters in Paris dictate global trends and drive domestic consumption through flagship prestige. The primary driving factor is the immense draw of Paris as a luxury tourism destination, where visitors from Asia, the Americas, and the Middle East flock to purchase clothing directly from the source. As per the Committee for Tourism and Events in Paris, luxury shopping accounts for a substantial portion of total tourist expenditure in the city, providing a massive boost to the local clothing market. Another driver is the strong domestic culture of elegance and the "art de vivre," which compels French consumers to invest in timeless, high-quality pieces. According to INSEE, spending on luxury textiles in France remains resilient, supported by a wealthy demographic that views fashion as an essential lifestyle element.

United Kingdom Luxury Clothing Market Analysis

The United Kingdom is anticipated to register a promising CAGR in the European luxury clothing market during the forecast period, od owing to a dynamic fusion of traditional tailoring heritage and contemporary streetwear innovation centered in London. The market status in the UK is defined by its role as a global financial hub, sustaining a large population of high-net-worth individuals with significant disposable income for luxury goods. A major driving factor is the vibrancy of London Fashion Week and the city's reputation as an incubator for avant-garde design, attracting a youthful and diverse clientele eager for cutting-edge luxury clothing. According to the British Fashion Council, the fashion industry contributes substantially to the UK economy, with luxury clothing representing a growing fraction of this value. Another driver is the resilience of the British high street and the presence of iconic department stores like Harrods and Selfridges, which serve as destinations for both locals and tourists. As per the Office for National Statistics, luxury retail sales in London recovered to pre-pandemic levels by 2023, fueled by returning international visitors and strong domestic demand.

Germany Luxury Clothing Market Analysis

Germany is expected to account for a notable share of the European luxury clothing market over the forecast period due to a pragmatic yet affluent consumer base that values quality, durability, and understated elegance. The German market is distinct due to the strength of its regional economies, particularly in cities like Munich, Düsseldorf, and Hamburg, which host dense clusters of wealthy residents with high purchasing power. The primary driving factor is the robust domestic economy and low unemployment rate, which sustain high levels of consumer confidence and spending power. According to the German Retail Association, luxury clothing sales in Germany grew steadily in 2024, driven by a preference for "quiet luxury" brands that emphasize material excellence and functionality. Another driver is the growing interest in sustainable and ethically produced luxury goods, aligning with the strong environmental consciousness of the German populace. As per sustainability institutes, a majority of German luxury shoppers actively seek out brands with certified green credentials, influencing purchasing decisions significantly.

Switzerland Luxury Clothing Market Analysis

Switzerland is estimated to record a healthy CAGR in the European luxury clothing market during the forecast period due to its highest per capita spending on luxury goods in Europe, due to its exceptional wealth density, and high standard of living. The market status here is defined by a small but extremely affluent population, alongside a steady stream of high-net-worth tourists from Russia, the Middle East, and Asia. A key driving factor is the favorable currency dynamics and tax structures that often make luxury clothing more affordable for international visitors compared to neighboring EU countries. According to the Swiss State Secretariat for Economic Affairs, retail sales of luxury goods in Zurich and Geneva consistently outperform global averages, driven by the purchasing power of the local banking, pharmaceutical, and technology sectors. Another driver is the cultural alignment with precision and quality, where Swiss consumers demand the highest standards in craftsmanship and are willing to pay a premium for perfection and longevity. As per luxury consultancies, the average transaction value in Swiss boutiques is significantly higher than the European average, reflecting the ultra-premium nature of the market.

COMPETITIVE LANDSCAPE

The competition in the Europe luxury clothing market is intensely fierce,e characterized by a rivalry between historic conglomerates and agile independent houses vying for the attention of affluent global consumers. Major players leverage their heritage and brand equity to command premium prices while constantly innovating in design and customer experience to differentiate themselves. The landscape sees frequent strategic acquisitions as groups seek to diversify portfolios and secure supply chains against volatility. Competitive pressure is heightened by the need to balance tradition with digital transformation as brands race to dominate online channels without diluting their exclusive image. Sustainability has emerged as a critical battleground where companies compete to prove their ethical credentials to increasingly discerning shoppers. This dynamic environment forces continuous investment in creativi,t y technol,ogy and operational efficiency as participants strive to capture market share in a sector driven by perception and prestige.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe luxury clothing market include

- LVMH Moët Hennessy Louis Vuitton SE

- Kering S.A.

- Chanel Limited

- Hermès International S.A.

- Prada S.p.A.

- Burberry Group plc

- Dolce & Gabbana S.r.l.

- Giorgio Armani S.p.A.

- Hugo Boss AG

- Ralph Lauren Corporation

- Capri Holdings Limited (Versace, Michael Kors)

- Moncler S.p.A.

TOP LEADING PLAYERS IN THE MARKET

- LVMH stands as the undisputed giant in the Europe luxury clothing market with a portfolio that includes iconic houses like Louis Vuitton, Dior, and Celine. The group contributes significantly to the global market by setting trends in haute couture and ready-to-wear segments through its unparalleled creative direction and vertical integration. Recently, the company has strengthened its position by acquiring minority stakes in niche Italian textile manufacturers to secure supply chains for premium fabrics. They have also expanded their flagship stores in key European capitals to offer immersive brand experiences that blend physical retail with digital innovation. These strategic moves ensure control over quality and exclusivity while reinforcing their dominance in the high-end fashion landscape without relying on mass market dilution.

- Kering SA operates as a leading luxury group managing prestigious brands such as Gucci, Saint Laurent, and Bottega Veneta across the European continent. Their global contribution is defined by a strong commitment to sustainability and ethical sourcing, which has become a benchmark for the entire industry. To fortify their market stance,e the group recently launched an internal carbon fund to finance projects that reduce environmental impact within their supply chain. They have also reorganized their creative teams to foster innovation and accelerate product development cycles in response to changing consumer tastes. Furthermore, Kering has invested heavily in digital platforms to enhance direct-to-consumer sales and personalize customer interactions. These initiatives demonstrate their dedication to combining luxury aesthetics with responsible business practices to maintain relevance and leadership.

- Hermès International distinguishes itself through an unwavering focus on artisanal craftsmanship and extreme exclusivity in the Europe luxury clothing sector. The company contributes to the global market by maintaining a production model that prioritizes handmade quality over volume scaling,e nsuring each garment meets rigorous standards. Recent actions to strengthen their position include the construction of new leather and textile workshops in France to increase capacity while preserving traditional techniques. They have also enhanced their after-sales services and introduced bespoke customization options to deepen client relationships. By strictly controlling distribution channels and avoiding discounting, Hermès protects its brand equity and allure. This disciplined approach to growth and quality assurance solidifies their reputation as the pinnacle of luxury clothing manufacturing and retailing worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe luxury clothing market primarily employ strategies centered on vertical integration to control every aspect of production from raw material sourcing to final retail. Companies are heavily investing in artisanal workshops and acquiring specialized suppliers to ensure exclusive access to premium fabrics and skilled labor. Another major strategy involves the expansion of direct-to-consumer channels through flagship boutiques and enhanced e-commerce platforms to capture higher margins and gather customer data. Brands are also focusing on sustainability initiatives by launching circular economy programs and using eco-friendly materials to appeal to conscious consumers. Additionally, participants utilize limited edition releases and celebrity collaborations to generate hype and maintain brand desirability. These approaches collectively aim to preserve exclusivity while adapting to modern digital and ethical demands.

MARKET SEGMENTATION

This research report on the europe luxury clothing market is segmented and sub-segmented into the following categories.

By End User

- Women

- Men

By Distribution Channel

- Offline (Boutiques, Department Stores, Specialty Stores)

- Online (E-commerce Platforms, Brand Websites)

By Country

- Italy

- France

- United Kingdom

- Germany

- Switzerland

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com