- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

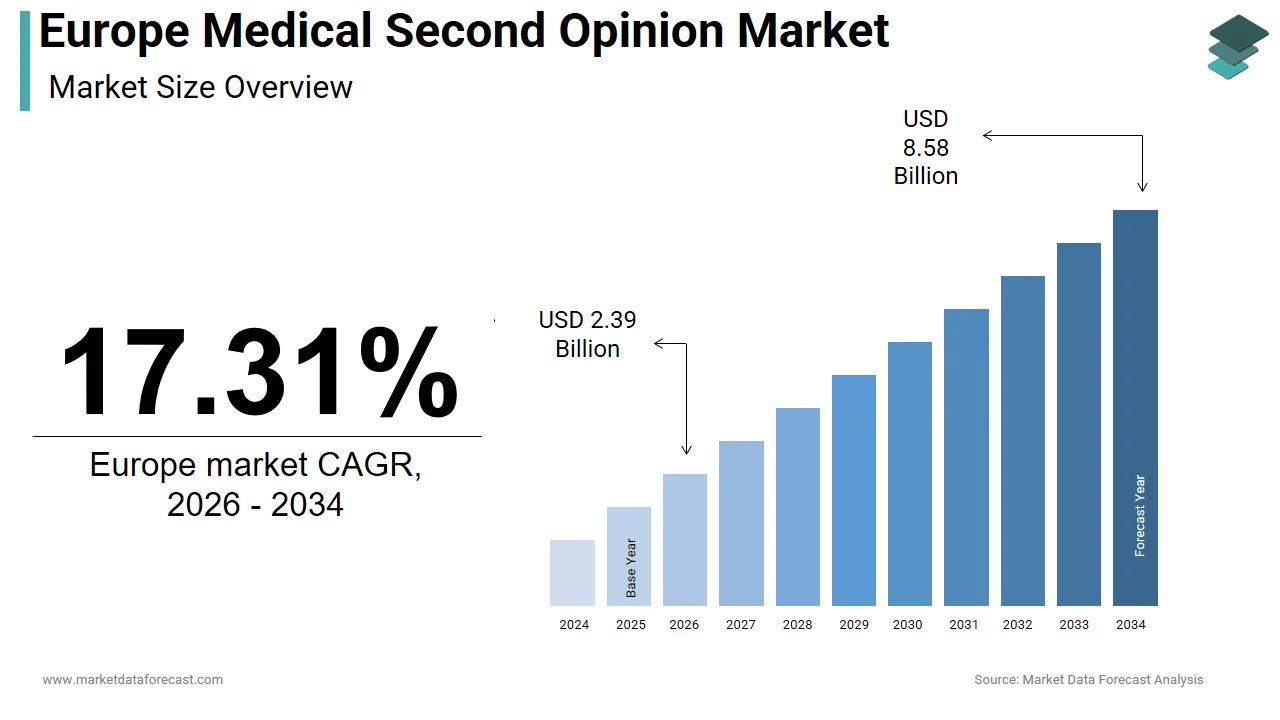

Market Size, 2025

$2.04 BnMarket Estimate, 2026

$2.39 BnMarket Forecast, 2034

$8.58 BnCAGR, 2026–2034

17.31%Europe Medical Second Opinion Market Size

The size of the Europe medical second opinion market was valued at USD 2.04 billion in 2025. This market is expected to grow at a CAGR of 17.31% from 2026 to 2034 and be worth USD 8.58 billion by 2034 from USD 2.39 billion in 2026.

Medical Second Opinion refers to the clinical services wherein patients obtain an independent evaluation from a qualified specialist following an initial diagnosis or treatment recommendation. This practice is increasingly institutionalized across European healthcare systems as a mechanism to enhance diagnostic accuracy, align therapeutic strategies with best practices, and uphold patient autonomy. Rooted in the principles of shared decision making and clinical transparency, second opinions are particularly prevalent in high-stakes medical domains such as oncology, neurology, and complex surgical planning. Apart from these, the OECD has pointed out a high demand for second opinions in Germany for major conditions like cancer and surgery, but without specifying a precise percentage. This demand has led to the legal implementation of second opinion directives in Germany for certain elective surgeries, indicating an ongoing trend toward formalizing access to second opinions. Enabled by EU cross-border healthcare directives and digital health integration, the market reflects a convergence of ethical imperatives, clinical necessity, and technological advancement.

MARKET DRIVERS

Rising Prevalence of Complex Chronic Conditions Drives Demand for Expert Validation

Region’s demographic transition toward an older population has intensified the burden of multimorbidity, which fuels the growth of the Europe medical second opinion market. According to the European Commission, individuals aged sixty-five and above constitute a portion of the EU population, with many managing two or more chronic conditions simultaneously. This complexity frequently leads to diagnostic ambiguity or suboptimal treatment pathways in primary or secondary care settings. Furthermore, as per sources, around fifteen percent of initial cancer diagnoses across Europe undergo significant modification after external pathology assessment or multidisciplinary tumor board input. These recalibrations often alter staging, prognosis, or therapeutic direction, directly influencing survival and quality of life. Consequently, the growing volume of patients presenting with intersecting chronic diseases sustains robust demand for authoritative external validation, especially in tertiary referral centers where precision directly correlates with clinical outcomes.

Expansion of Digital Health Infrastructure Enables Scalable Second Opinion Access

The maturation of the region’s digital health infrastructure has removed longstanding logistical and geographic barriers, and this propels the expansion of the Europe medical second opinion market. As per studies, many EU member states have increased their use of digital health technologies, including remote consultations, since the COVID-19 pandemic; the extent varies widely. Nations such as Estonia and Denmark have achieved near universal adoption of interoperable electronic health records, allowing seamless and secure transmission of radiological images, genomic data, and clinical notes to external specialists. As per research, Cross-border telemedicine and patient mobility are indeed growing, and the Cross-border Healthcare Directive provides a framework for this. Furthermore, national platforms ensure end-to-end encryption and General Data Protection Regulation compliance by alleviating patient and provider concerns about data privacy. This digital enablement not only accelerates decision making in time-sensitive conditions, such as suspected glioblastoma or acute coronary syndromes, but also democratizes access to elite clinical expertise regardless of a patient’s location, thereby expanding the market’s reach and relevance.

MARKET RESTRAINTS

Fragmented Reimbursement Policies Across EU Member States Limit Market Penetration

The absence of consistent public reimbursement frameworks is an impediment to the growth of the Europe medical second opinion market. According to sources, the funding and coverage for second medical opinions vary widely across EU countries. Some public health systems explicitly cover second opinions for specific. In Italy and Spain, patients often seek second medical opinions through private providers due to long public-sector waiting lists, as per research. The lack of standardized billing codes further discourages physician participation, as clinicians cannot reliably claim compensation for the time intensive process of reviewing external cases. Moreover, due to high workloads and a lack of compensation for second medical opinions in some public healthcare systems, some physicians may decline such requests. This financial barrier disproportionately affects low-income populations, which strengthens health inequities and prevents second opinions from becoming a routine element of care rather than a privilege for the affluent.

Regulatory Ambiguity Surrounding Cross-Border Clinical Liability Deters Specialist Participation

Unresolved legal uncertainties around professional liability inhibit specialist engagement in transnational second opinion services, and this constrains the expansion of the Europe medical second opinion market. As per the European Union Agency for Fundamental Rights, liability for clinical advice rendered remotely remains tethered to the physician’s country of licensure, yet the clinical consequences manifest in the patient’s home jurisdiction by creating a jurisdictional mismatch that exposes providers to unpredictable legal risk. For instance, a Belgian radiologist offering a second opinion to a patient in Croatia may be subject to Croatian malpractice laws if an adverse outcome occurs, even if the interpretation adheres to Belgian standards. The absence of a unified EU liability framework creates a legal gray zone that will continue to stifle specialist availability and divide the talent pool, which weakens a potential pan-continental market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Diagnostic Triage Creates New Service Models

Artificial intelligence is emerging as a powerful enabler of efficient and targeted second opinion delivery across the region, which is setting up new opportunities for the Europe medical second opinion market growth. The European Society of Radiology has published extensively on AI in diagnostic imaging by emphasizing its potential while noting that performance can vary depending on the specific application. This capability allows health systems to triage cases, directing only high-risk or ambiguous findings to human specialists. In Sweden, studies led by institutions like the Karolinska Institute have shown that AI tools can assist in dermatology referrals and skin cancer diagnosis, with research demonstrating improved diagnostic accuracy with AI assistance, according to sources. Moreover, under the EU's Medical Device Regulation, medical devices that incorporate AI can receive the CE mark, a regulatory step that enables their legal sale in the European Economic Area. Hundreds of AI-based medical devices have received the CE mark since 2015. These technologies automate preliminary analysis, freeing expert human reviewers to focus their skills on complex cases where their judgment is most valuable.

Growing Emphasis on Value-Based Healthcare Aligns with Second Opinion Outcomes

Its strategic pivot toward value-based healthcare offers potential prospects for the expansion of the Europe medical second opinion market. According to studies, many European countries are exploring and piloting innovative payment models, including value-based and outcome-based payment, to move away from fee-for-service systems. Second opinions directly support this shift by curbing misdiagnosis-driven complications and unnecessary procedures. Second opinion services have a clear strategic advantage for inclusion in bundled payment and integrated care contracts across the continent, especially as payers demand interventions that provide proven value and cost control.

MARKET CHALLENGES

Persistent Shortage of Subspecialist Physicians Constrains Service Scalability

A shortage of subspecialist clinicians qualified to deliver high-fidelity external reviews slows down the growth of the Europe medical second opinion market. According to a 2023 report from the European Commission in collaboration with the OECD and European Observatory on Health Systems and Policies (State of Health in the EU Report), Europe faces significant health workforce challenges, including a projected deficit of hundreds of thousands of physicians by 2030. Geographic disparities compound this shortage. As per the World Health Organization’s European Regional Office, significant disparities in healthcare workforce distribution within countries like Romania and Bulgaria. This scarcity translates into prolonged wait times; the median turnaround for oncology second opinions exceeds fourteen days in many regions, which affects their utility in urgent clinical contexts. The market's ability to meet rising demand is fundamentally constrained by a lack of coordinated investment in subspecialty training, mutual credential recognition across borders, and the delegation of tasks to allied experts.

Patient Hesitancy Stemming from Perceived Threat to Primary Physician Relationship

Patient reluctance driven by concerns about damaging trust with their primary physician hampers the expansion of the Europe medical second opinion market. The hesitation is especially pronounced in countries with hierarchical healthcare traditions. The European Health Consumer Index further correlates low patient empowerment scores in nations like Portugal and Slovakia with markedly lower second opinion utilization rates, despite comparable disease burdens. Patient demand for second opinions will stay artificially suppressed, despite advances in technology or policy, as long as healthcare systems fail to reframe them as collaborative quality assurance and train clinicians to embrace them.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Disease, Supply Provider, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Second Opinion International, Elite Medical Services, Helsana, Cigna, WorldCare, Medix, 2nd.MD (Innovation Specialists LLC), and AXA |

SEGMENTAL ANALYSIS

By Disease Insights

The cancer segment continues to hold the largest share of 42.5% share of the Europe medical second opinion market in 2024. The high-stakes nature of cancer diagnosis and treatment, where misclassification can lead to inappropriate therapy, reduced survival, or unnecessary toxicity, has significantly boosted the growth of the growth of the cancer segment in the regional market. A significant proportion of initial cancer diagnoses in Europe undergo substantive revision upon expert review, supporting the clinical necessity of second opinions. In breast cancer, as per sources, a portion of hormone receptor or HER2 status assessments were corrected following centralized review. These changes directly impact treatment eligibility for targeted therapies or immunotherapies. This diagnostic volatility, coupled with rapid advances in genomic profiling and precision oncology, sustains unparalleled demand for expert validation in this segment.

In several European countries, second opinions in oncology are not merely optional but embedded in national clinical governance frameworks. Patient advocacy groups such as Europa Donna and the European Cancer Patient Coalition have also successfully lobbied for legal recognition of second opinion rights, which influences policy in countries like Italy and the Netherlands. The tight link between treatment accuracy and cancer survival rates means that institutional and societal factors drive patients to seek second opinions, which in turn reinforces oncology's dominance in the market.

The cardiac disorders segment is likely to experience the fastest CAGR of 11.3% from 2025 to 2033. The growth of the cardiac disorders segment is driven by the rising diagnostic complexity in cardiovascular care and increasing patient awareness of treatment variability. Heart failure with preserved ejection fraction now accounts for over fifty percent of all heart failure cases in Europe, yet its diagnosis remains notoriously challenging due to nonspecific symptoms and overlapping comorbidities. As per sources, a portion of heart failure diagnoses in primary care settings are inaccurate, which often misclassifies patients as having diastolic dysfunction when alternative etiologies such as pulmonary hypertension or valvular disease are present. This diagnostic uncertainty drives demand for cardiology second opinions, particularly from specialized heart failure clinics. The integration of advanced imaging and biomarker analysis in tertiary centers further incentivizes referral for external validation, fueling segment growth. Significant variation exists in recommendations for coronary revascularization, such as stenting or bypass surgery, between community hospitals and academic cardiology centers. Heightened patient awareness, driven by public health campaigns from bodies like the European Heart Network, has increased scrutiny of procedural indications, which prompts more individuals to seek independent cardiology opinions before consenting to surgery. This trend toward informed consent and procedural appropriateness emphasizes the segment’s rapid expansion.

By Supply Provider Insights

The hospitals led the Europe medical second opinion market and occupied 46.5% share in 202. Their integration with academic medical centers, access to multidisciplinary expertise, and alignment with national healthcare pathways propel the growth of the hospitals segment.

In most European countries, second opinions are formally routed through public hospital networks, particularly for high-complexity conditions. These institutions house specialized diagnostic units, such as molecular pathology labs or cardiac imaging cores, that are inaccessible to private or digital providers. This structural integration ensures that hospitals remain the default destination for clinically validated second opinions, especially when public reimbursement is involved. Their role as training grounds for specialists further concentrates expertise, which strengthens their centrality in the second opinion ecosystem. Hospitals uniquely offer coordinated second opinion mechanisms through formalized structures like tumor boards or heart teams, which synthesize input from radiologists, pathologists, surgeons, and medical specialists. These collaborative models enhance diagnostic reliability and treatment alignment by making hospital-based second opinions not just supplementary but foundational to high-quality care. The growing practice among European health authorities of tying hospital accreditation to multidisciplinary review compliance reinforces the dominant position of hospitals in the supply landscape.

The online and offline medical second opinion provider segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 14.7% from 2025 to 2033. The expansion of the online and offline medical second opinion provider segment is propelled by digital transformation, patient empowerment, and cross-border care facilitation. The implementation of the EU Cross-Border Healthcare Directive has caused the rise of digital second opinion platforms by legally enabling patients to seek expert assessments from specialists in other member states and claim partial reimbursement. Platforms have integrated second opinion modules that connect patients with specialists from top European hospitals, bypassing traditional referral barriers. The directive’s provision for prior authorization and cost reimbursement, up to the level of domestic care, reduces financial barriers, which makes these services accessible to a broader demographic. This regulatory tailwind, combined with standardized data exchange protocols under the European Health Data Space initiative, positions digital providers as agile intermediaries in a fragmented healthcare landscape. A growing number of European corporations are partnering with digital second opinion providers to offer these services as part of employee wellness packages. Companies provide employees with prepaid access to platforms such as Best Doctors Europe, which connects users to a curated network of over five thousand specialists across the continent. This B2B channel not only ensures recurring revenue for digital providers but also normalizes second opinions as a standard component of health management rather than a crisis response. The expansion of employer-sponsored health benefits in Northern and Western Europe is driving this partnership model, which enables it to rapidly gain market share beyond what was possible through standard patient acquisition methods.

COUNTRY LEVEL ANALYSIS

Germany Market Analysis

Germany dominated the Europe medical second opinion market in 2024 and held a 22.5% share. The prominence of Germany is because of a robust statutory health insurance system that explicitly covers second opinions for major diagnoses and a dense network of university hospitals with specialized review units. Most people in Germany are enrolled in public health insurance plans that include the right to obtain a second medical opinion in specialized areas such as oncology, cardiology, and orthopedic care, according to sources. As per research, a significant number of patients request secondary evaluations each year, with cancer-related consultations representing a major portion. This combination of legal entitlement, infrastructure readiness, and clinical culture of diagnostic verification strengthens Germany’s dominance in the regional market.

France Market Analysis

France is the next prominent region in the Europe medical second opinion market by capturing 18.5% share in 2024. The growth of France is due to centralized clinical governance and patient rights legislation that enshrines access to external medical review. The French Public Health Code guarantees every patient the right to a second opinion without requiring physician referral, and national cancer and cardiac plans mandate multidisciplinary review for complex cases. Besides, France’s Carte Vitale system enables real-time billing and partial reimbursement, minimizing out-of-pocket costs. High health literacy rates further drive proactive patient engagement. These systemic enablers create a mature and high-volume second opinion environment that supports France’s position as the continent’s second-largest market.

United Kingdom Market Analysis

The United Kingdom experienced steady growth in the Europe medical second opinion market. Even in a public healthcare system, patients can get a second opinion because of patient choice policies and specific commissioning pathways. NHS England’s Right to Choose framework allows patients to select providers for diagnostic and specialist services, including second opinions, fostering competition among hospital trusts. The UK also hosts globally recognized centers of excellence, such as The Royal Marsden for oncology and Papworth Hospital for cardiology, that attract domestic and international referrals. Although public funding for second opinions is limited to specific scenarios, the strong private insurance market sustains robust demand. This hybrid public-private dynamic emphasizes the UK’s consistent market presence.

Italy Market Analysis

Italy is expanding steadily in the Europe Medical Second Opinion Market due to regional healthcare autonomy and growing patient awareness, particularly in oncology. The national right to a second opinion is implemented inconsistently across the country, with structured pathways and partial reimbursement in Lombardy and Emilia Romagna, but lagging access in southern regions. Cross-border referrals to German and Swiss centers are common, facilitated by EU regulations. Furthermore, private clinics in Milan and Rome have developed premium second opinion services targeting affluent patients and medical tourists. Despite systemic fragmentation, Italy’s large population and rising demand for diagnostic certainty sustain its position as a key market.

Switzerland Market Analysis

Switzerland is likely to grow in the Europe medical second opinion market from 2025 to 2033. Though not an EU member, Switzerland’s high-income healthcare system and reputation for clinical excellence make it a magnet for second-opinion seekers. In Switzerland, the vast majority of residents are enrolled in private health insurance plans that include coverage for external medical assessments, according to sources. Leading hospitals offer internationally recognized second opinion programs, attracting both domestic and foreign patients. Switzerland’s neutrality, multilingual expertise, and adoption of cutting-edge diagnostics, such as liquid biopsy and AI-assisted imaging, enhance its appeal. Furthermore, the absence of waiting lists and rapid turnaround times, often under seventy-two hours, differentiates its offering in a time-sensitive care environment, which secures its place among Europe’s top five markets.

COMPETITIVE LANDSCAPE

The Europe Medical Second Opinion Market features a dynamic competitive landscape characterized by the coexistence of global telehealth giants, regional digital health startups, and elite academic medical centers. Competition centers not on price but on clinical credibility, turnaround speed, data security, and integration with existing care pathways. Established players leverage partnerships with national health services and private insurers to gain institutional legitimacy while newer entrants differentiate through artificial intelligence-driven triage, multilingual support, and blockchain-based data verification. Geographic reach is a key differentiator, with some providers focusing on domestic markets while others build pan-European networks through cross-border collaborations. Regulatory navigation, particularly around liability and data privacy, remains a vital capability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe medical second opinion market include

- Second Opinion International

- Elite Medical Services

- Helsana

- Cigna

- WorldCare

- Medix

- 2nd.MD (Innovation Specialists LLC)

- AXA

Top Players in the Market

- Best Doctors Europe is a leading provider of medical second opinion services across the continent, operating under the Teladoc Health umbrella. The company connects patients with a curated network of over five thousand specialists from top European hospitals, enabling expert reviews in oncology, cardiology, and rare diseases. In recent years, Best Doctors Europe has expanded its digital platform to integrate artificial intelligence for case triage and launched employer-sponsored programs with multinational corporations in Germany, France, and the Netherlands. These initiatives enhance accessibility and position the company as a strategic partner in value-based healthcare delivery across public and private sectors.

- Cleveland Clinic London serves as an important node in the transatlantic second opinion ecosystem, offering European patients access to US-based clinical expertise through its UK hub. The institution provides comprehensive remote second opinions leveraging multidisciplinary teams from its global network. In 2023, Cleveland Clinic London enhanced its digital infrastructure to support the real-time, secure exchange of imaging and genomic data with its main campus in Ohio. This integration allows European patients to receive consensus opinions from world-renowned specialists without travel. The clinic also partnered with UK private insurers to streamline reimbursement, further embedding its services into local care pathways.

- Medix is an international medical review and case management company with a strong footprint in Western and Southern Europe. It specializes in delivering independent second opinions for complex oncological, hematological, and neurological conditions through a network of academic physicians. Medix has recently invested in blockchain-enabled health data verification tools to ensure the integrity of patient records during remote reviews. These innovations support Medix’s role as a trusted intermediary between patients, insurers, and specialist centers in a fragmented European landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe Medical Second Opinion Market prioritize strategic partnerships with national health systems and private insurers to embed their services into routine care pathways. They invest heavily in secure digital platforms that comply with the General Data Protection Regulation and support interoperability with hospital electronic records. Many firms integrate artificial intelligence to triage cases and prioritize high-risk diagnoses for human review. Expansion through employer-sponsored health programs is another core tactic targeting corporate clients across Northern and Western Europe. Apart from these, companies actively pursue cross-border credentialing and liability frameworks to facilitate specialist participation across jurisdictions, enhancing service scalability and clinical credibility.

EUROPE MEDICAL SECOND OPINION MARKET NEWS

- In January 2023, the Cleveland Clinic launched a project for virtual treatment by the healthcare system, and telehealth company Amwell partnered with digital health company Transparent. Transparent members will be qualified to have a diagnosis or treatment plan reviewed and to receive a second opinion.

- In January 2021, the medical opinion platform MD was acquired by Lybrate, which assists patients in understanding their health benefits. This goal is to guide patients in making important health decisions to have surgery; the goal is to offer them access to a second opinion.

MARKET SEGMENTATION

This Europe medical second opinion market research report is segmented and sub-segmented into the following categories.

By Disease

- Cancer

- Cardiac Disorders

- Diabetes

- Injuries

By Supply Provider

- Hospitals

- Health Insurance Players

- Online and Offline Medical Second Opinion Providers

- Private clinics

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe