Europe Mulch Films Market Size, Share, Trends & Growth Forecast Report By Material Type, By Crop Type, and By Country (Spain, Italy, France, Germany, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034 Size, Share, Trends & Growth Forecast Report By Material Type, By Crop Type, and By Country (Spain, Italy, France, Germany, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Mulch Films Market Report Summary

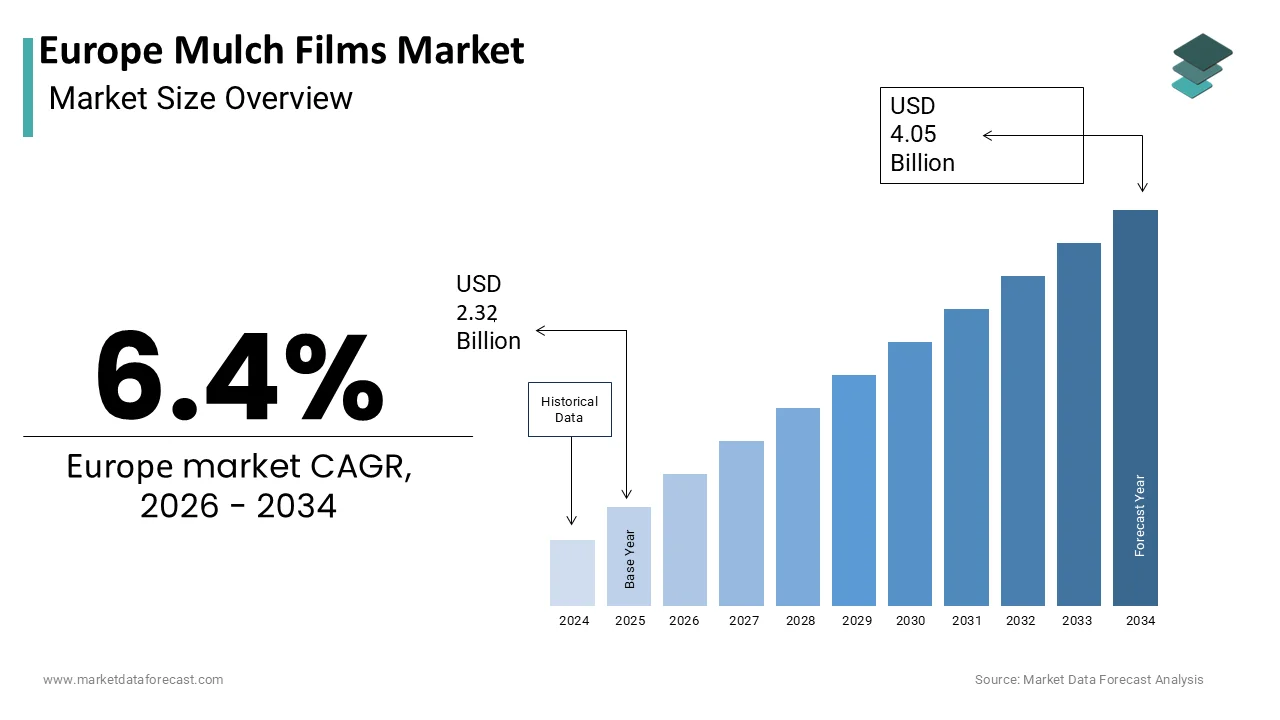

The Europe Mulch Films Market was valued at USD 2.32 billion in 2025 and is projected to reach USD 4.05 billion by 2034, growing from USD 2.47 billion in 2026 at a CAGR of 6.4% during the forecast period. Growth is driven by increasing adoption of precision agriculture, stringent environmental regulations promoting biodegradable alternatives, and expansion of organic farming and high-value crop cultivation. High costs of biodegradable films and complex recycling logistics are shaping market dynamics.

Key Market Trends

- Rising shift toward biodegradable films under EN 17033 standardization and microplastic mitigation targets

- Growing development of advanced bio-based materials from corn starch, cellulose, and algae

- Increasing mechanization of mulch film application amid agricultural labor shortages

- Expansion of infrared-transmitting films for early-season temperature optimization

- Rising retailer sustainability requirements are pushing farmers toward eco-friendly mulch inputs

Segmental Insights

- Based on material type, conventional mulch films held the majority share in 2025, driven by cost-effectiveness and established manufacturing infrastructure.

- Based on crop type, vegetables held the largest share in 2025, driven by intensive cultivation practices in Southern Europe requiring precise soil control.

- Biodegradable mulch films are the fastest-growing material segment, projected at a CAGR of 12.5%, driven by regulatory pressure and soil-protection initiatives.

Regional Insights

- Spain led the market in 2025, supported by its extensive horticultural sector and protected cultivation area exceeding 60,000 hectares.

- Italy holds a significant share, driven by strong regulatory leadership in biodegradable agricultural film adoption.

- France is a prominent market supported by strict microplastic mitigation objectives and strong retailer sustainability commitments.

- Netherlands contributes notably due to its advanced greenhouse technology and integration of mulch films with automated climate control.

- Fruits are the fastest-growing crop type segment, projected at a CAGR of 11.8%, driven by berry cultivation expansion and climate adaptation needs.

Competitive Landscape

The market is highly competitive, with multinational manufacturers and specialized regional producers competing on product quality, regulatory compliance, and environmental stewardship. Companies are investing in bio-based formulations and recycling infrastructure to align with EU circular economy goals.

Prominent players in the market include Berry Global Inc., BASF SE, Novamont S.p.A., RKW Group, Coveris Holdings S.A., Armando Alvarez Group, Trioplast Industrier AB, Ab Rani Plast Oy, Polythene UK Ltd., AEP Industries Inc., Ginegar Plastic Products Ltd., and Plastika Kritis S.A.

Europe Mulch Films Market Size

The Europe Mulch Films Market is projected to grow from USD 2.32 billion in 2025 to USD 2.47 billion in 2026 and reach USD 4.05 billion by 2034, registering a CAGR of 6.4% during the forecast period from 2026 to 2034.

Mulch films are thin, protective sheets placed over the soil around crops. Widely used in modern agriculture, they act as an artificial barrier to control soil temperature, retain moisture, and suppress weed growth, ultimately leading to healthier plants and higher crop yields. These films serve multiple functions, including weed suppression, moisture retention, soil temperature regulation, and prevention of nutrient leaching. The European agricultural landscape is undergoing a significant transformation driven by the need for sustainable intensification and resource efficiency. According to Eurostat, the utilized agricultural area in the European Union covered approximately 157 million hectares in 2023, providing a vast potential base for the adoption of advanced farming techniques. The integration of mulch films is particularly prominent in high-value crop cultivation such as vegetables, fruits, and berries, where yield quality and consistency are paramount. Regulatory frameworks across member states are increasingly scrutinizing plastic usage in agriculture, prompting a shift toward biodegradable and recyclable alternatives. As per the European Bioplastics Association, the global bioplastics production capacity reached 2.18 million tonnes in 2023, with completely biodegradable polymer fractions scaling up to meet sustainable agricultural and packaging demands. Farmers in countries like Spain, Italy, and France are early adopters of these technologies due to their intensive horticultural sectors. The market is characterized by a transition from conventional polyethylene films to innovative materials that offer environmental benefits without compromising performance. This evolution is supported by research initiatives funded by the European Commission aimed at developing circular economy models for agricultural plastics. The adoption of mulch films aligns with broader goals of reducing water consumption and chemical inputs, making it a vital tool for modern sustainable farming practices in the region.

MARKET DRIVERS

Increasing Adoption Of Precision Agriculture And Sustainable Farming Practices Drives Demand

The escalating implementation of precision agriculture techniques across the region drives the growth of the Europe mulch films market. This is because farmers are seeking to optimize resource use and maximize crop yields. Precision farming relies on data-driven decisions to apply inputs such as water and fertilizers more efficiently, and mulch films play a crucial role in this ecosystem by minimizing evaporation and preventing nutrient runoff. According to research, the deployment of precision farming systems is accelerating under the European Union’s Common Agricultural Policy frameworks, expanding the demand for integrated soil-management tools. Mulch films help maintain consistent soil moisture levels, which is essential for the effectiveness of drip irrigation systems commonly used in precision agriculture. This synergy reduces water usage compared to traditional flood irrigation methods, addressing growing concerns about water scarcity in southern European regions. Furthermore, mulch films suppress weed growth mechanically, reducing the need for herbicides and aligning with the European Green Deal’s Farm to Fork strategy, which aims to reduce pesticide use by 50% by 2030. Farmers are increasingly recognizing the economic benefits of reduced labor costs associated with weeding and improved crop uniformity. The ability to control soil temperature extends the growing season for high-value crops, allowing for earlier harvests and better market prices. This economic incentive drives widespread adoption among commercial growers who prioritize profitability and sustainability. The integration of mulch films into holistic farm management plans demonstrates their value beyond simple ground cover, positioning them as essential components of modern sustainable agriculture.

Stringent Environmental Regulations Promote Shift To Biodegradable Alternatives

Strict environmental regulations imposed by the European Union and individual member states are compelling farmers and manufacturers to transition from conventional polyethylene mulch films to biodegradable and compostable alternatives, which in turn boosts the expansion of the Europe mulch films market. According to European environmental policy guidelines, the regulatory pressure on agricultural films stems from broader circular economy frameworks and microplastic reduction strategies rather than the Single Use Plastics Directive. As per studies, agricultural plastics account for roughly 2% of total plastic waste in Europe, with ground mulch films presenting a distinct recycling challenge due to severe soil debris contamination. Conventional films often fragment into microplastics that contaminate soil and water bodies, posing long-term ecological risks. In response, governments are incentivizing the use of certified biodegradable films that break down into natural elements after use. For instance, according to regional plasticulture updates, the high adoption rate of eco-friendly farming films in France is driven by national microplastic mitigation targets and harmonized European EN 17033 standards rather than an outright mandatory ban on conventional mulch. This regulatory pressure stimulates demand for advanced materials such as polylactic acid and starch-based blends that meet international compostability standards. Manufacturers are investing heavily in research and development to improve the mechanical strength and degradation rates of these bio-based films. Farmers are increasingly willing to adopt these alternatives to comply with legal requirements and avoid penalties. The shift is also driven by consumer preference for sustainably produced food, encouraging retailers to source from farms using eco-friendly practices. This regulatory and market-driven transition ensures sustained growth for the biodegradable segment of the mulch films market.

MARKET RESTRAINTS

High Costs And Limited Performance Of Biodegradable Films Restrain Market Growth

Significantly higher production costs hold back the widespread adoption of biodegradable mulch films, which hampers the growth of the Europe mulch films market. They are also occasionally limited in their performance when compared to conventional polyethylene films. Biodegradable materials such as polylactic acid and polybutylene adipate terephthalate are more expensive to produce due to complex manufacturing processes and limited economies of scale. According to sources, biodegradable mulch films can cost up to 3 times more than traditional polyethylene films, posing a financial barrier for small and medium-sized farmers operating on tight margins. Additionally, some biodegradable films exhibit lower tensile strength and durability, making them prone to tearing during installation or under harsh weather conditions. This fragility can lead to premature degradation before the end of the crop cycle, reducing their effectiveness in weed control and moisture retention. Farmers in regions with heavy rainfall or strong winds may find these films less reliable, leading to hesitation in switching from proven conventional options. The variability in degradation rates depending on soil temperature and microbial activity further complicates their use, as unpredictable breakdown can leave residues or fail to decompose fully. The lack of standardized testing protocols across different European countries creates confusion regarding product suitability and certification validity. These technical and economic challenges slow down the transition despite regulatory pressures. Manufacturers are working to address these issues through material innovation, but current limitations remain a significant restraint. Many farmers will continue to rely on conventional films or seek alternative weed management methods. This trend will persist until cost parity and performance reliability are achieved.

Complexities In Recycling Infrastructure And Collection Logistics Impede Circular Economy Goals

The complexities associated with recycling infrastructure and the logistical challenges of collecting used films from fields hinder the expansion of the Europe mulch films market. Unlike packaging plastics, agricultural mulch films are often contaminated with soil, plant debris, and pesticides, making them difficult and expensive to clean and process. According to PlasticsEurope, the agricultural sector leads European plastic circularity, with over 37.5% of its plastic materials actively derived from recycled inputs. The fragmented nature of agricultural holdings across Europe complicates the establishment of centralized collection points, increasing transportation costs and carbon footprint. Many rural areas lack specialized facilities capable of handling contaminated agricultural waste, leading to improper disposal practices. Farmers often struggle with the labor-intensive process of removing and cleaning films after harvest, discouraging participation in recycling schemes. The absence of harmonized regulations across member states regarding the definition and handling of agricultural plastic waste creates inconsistencies in management practices. Some countries have well-established producer responsibility schemes, while others lack any formal framework, leading to uneven progress. The high cost of recycling compared to virgin material production further disincentivizes investment in recycling infrastructure. These logistical and infrastructural barriers hinder the realization of a true circular economy for mulch films. Without robust and accessible recycling networks, the environmental benefits of using recyclable films are undermined. Consequently, this limits their appeal to environmentally conscious stakeholders.

MARKET OPPORTUNITIES

Development Of Advanced Bio-Based Materials Offers Significant Growth Potential

The continuous advancement in bio-based polymer technologies is a key growth area for the Europe mulch films market. This enables the creation of high-performance sustainable alternatives. Research institutions and chemical companies are developing novel materials derived from renewable resources such as corn starch, cellulose, and algae that offer improved mechanical properties and controlled degradation rates. According to the Joint Research Centre of the European Commission, ongoing projects under the Horizon Europe program are focusing on next-generation bioplastics that can withstand extreme weather conditions while ensuring complete biodegradability. These innovations address the performance gaps of earlier biodegradable films, making them viable for a wider range of crops and climatic zones. The introduction of additives that enhance UV resistance and tensile strength without compromising compostability expands the application scope of bio-based mulch films. Collaborations between materials scientists and agronomists are leading to customized solutions tailored to specific crop requirements and local soil conditions. The growing availability of raw materials for bio plastics in Europe reduces dependency on imported fossil fuels and enhances supply chain security. Governments are providing grants and subsidies to support the commercialization of these advanced materials, lowering the entry barrier for manufacturers. As production scales up, costs are expected to decrease, makingbio-basedd films more competitive with conventional options. This technological progress opens new market segments and encourages early adoption by progressive farmers. The potential for creating fully circular products that return nutrients to the soil adds further value, aligning with regenerative agriculture principles.

Expansion Of Organic Farming and High-Value Crop Cultivation Creates Niche Demand

The rapid expansion of organic farming and the cultivation of high-value crops in the region create a lucrative niche for specialized mulch films that align with sustainable certification standards and are expected to propel the expansion of the European market. Organic farmers are prohibited from using synthetic herbicides, making mechanical weed control through mulch films an essential practice. As per Eurostat, the total organic farming area within the European Union expanded to encompass 16.9 million hectares, driving steady niche demand for environmentally compliant cultivation inputs like biodegradable mulch sheets. Mulch films help organic growers maintain weed-free fields while preserving soil health and moisture, crucial for achieving certified organic status. High-value crops such as strawberries, tomatoes, and melons benefit significantly from the microclimate control provided by mulch films, resulting in higher yields and superior fruit quality. These crops command premium prices, allowing farmers to absorb the higher costs of specialized mulch films. The trend toward local and seasonal produce encourages protected cultivation techniques where mulch films are extensively used to extend growing seasons. Retailers and consumers increasingly demand transparency and sustainability in production methods, favoring produce grown with eco-friendly technologies. This market dynamic supports the development of premium mulch film products with enhanced features such as color optimization for pest deterrence or thermal regulation. The alignment of mulch films with organic and premium farming practices ensures steady demand from a dedicated customer base. This segment offers higher profit margins and opportunities for product differentiation based on specific agronomic benefits.

MARKET CHALLENGES

Volatility In Raw Material Prices Impacts Production Costs And Profit Margins

The volatility in raw material prices, particularly for petroleum-based polymers and bio-based feedstocks, slows down the growth of the Europe mulch films market. Fluctuations in crude oil prices directly affect the cost of polyethylene, the primary material for conventional mulch films, creating uncertainty for manufacturers and buyers. According to the International Energy Agency and the ICIS, major price fluctuations in global crude oil markets have introduced significant volatility into the baseline production costs of European agricultural plastics. Similarly, the prices of bio-based raw materials such as corn and sugarcane are subject to agricultural market dynamics, weather conditions, and global supply chain disruptions. These price fluctuations make it difficult for manufacturers to maintain consistent pricing strategies and profit margins. Farmers, who operate on fixed budgets, may delay purchases or switch to cheaper alternatives when prices spike, disrupting demand patterns. The reliance on imported raw materials for some bio plastics exposes the market to geopolitical risks and trade policy changes. Currency exchange rate variations further complicate cost management for companies sourcing materials globally. These economic instabilities hinder long-term planning and investment in capacity expansion. Manufacturers must constantly adjust their formulations and sourcing strategies to mitigate cost pressures, which can affect product quality and availability. The inability to pass on increased costs to price-sensitive farmers limits the ability to invest in innovation. This financial volatility remains a persistent challenge that requires robust risk management and supply chain diversification.

Lack Of Standardized Degradation Criteria Causes Consumer Confusion And Trust Issues

The lack of harmonized and standardized criteria for biodegradation and compostability of mulch films across the countries in the region creates confusion among farmers and undermines trust in sustainable products, which holds back the expansion of the European market. Different nations have varying definitions and testing protocols for what constitutes a biodegradable film, leading to inconsistent product performance and labeling. According to the European Committee for Standardization, efforts to unify standards are ongoing, but discrepancies remain in national regulations regarding soil biodegradation timelines and residue limits. Farmers may purchase films labeled as biodegradable only to find they do not decompose adequately in their specific soil conditions, leading to contamination and dissatisfaction. This inconsistency damages the reputation of the entire biodegradable sector and slows down adoption. Retailers and certifying bodies struggle to verify claims without a unified framework, causing delays in product approval and market entry. The presence of greenwashing, where products are marketed as eco-friendly without meeting rigorous standards, further erodes consumer confidence. Agricultural advisors and extension services face difficulties in recommending specific products due to the lack of clear comparative data. This ambiguity increases the perceived risk for farmers considering the switch from conventional films. Until a single European standard is fully implemented and enforced, the market will continue to face fragmentation and skepticism. Establishing clear, science-based criteria is essential to build trust and ensure the environmental integrity of biodegradable mulch films.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Crop Type, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Spain, Italy, France, Germany, Netherlands, the rest of europe |

| Market Leaders Profiled | Berry Global Inc., BASF SE, Novamont S.p.A., RKW Group, Coveris Holdings S.A., Armando Alvarez Group, Trioplast Industrier AB, Ab Rani Plast Oy, Polythene UK Ltd., AEP Industries Inc., Ginegar Plastic Products Ltd., Plastika Kritis S.A. |

SEGMENTAL ANALYSIS

By Material Type Insights

In 2025, the conventional mulch films segment held the majority share of the Europe mulch films market because of its superior cost-effectiveness and well-established manufacturing infrastructure. These films are primarily made from low-density polyethylene and linear low-density polyethylene. In addition, these materials offer a proven track record of durability, tensile strength, and resistance to environmental stressors, making them the preferred choice for large-scale commercial farming operations. According to sources, conventional plastics remain significantly cheaper to produce than bio-based alternatives, with production costs being approximately 40% lower, which is a critical factor for farmers operating on thin margins. The extensive existing supply chain for polyethylene ensures consistent availability and competitive pricing across all European regions. Farmers are familiar with the handling and application processes of conventional films, reducing the learning curve and operational risks associated with new materials. The mechanical properties of conventional films allow for easier installation using standard machinery without frequent breakage, ensuring efficient field operations. Despite growing environmental concerns, the immediate economic benefits and reliability of conventional films sustain their dominance in price-sensitive segments. The ability to recycle these films, although challenging, is supported by emerging collection schemes in countries like Germany and France, providing a partial solution to waste management issues. This combination of affordability, performance, and familiarity ensures that conventional mulch films continue to command the largest share of the market, particularly in extensive agricultural applications where cost per hectare is a primary decision criterion.

The supremacy of this segment is further reinforced by the superior mechanical performance and weather resistance of polyethylene films compared to many current biodegradable options. Conventional films exhibit high tensile strength and puncture resistance, allowing them to withstand harsh weather conditions such as strong winds, heavy rain, and intense UV exposure without tearing or degrading prematurely. According to studies, conventional mulch films can maintain their structural integrity for up to 6 months or more, covering the entire growing season for many crops without failure. This reliability is crucial for high-value crops where crop loss due to film failure can result in significant financial damage. The consistent thickness and uniformity of conventional films ensure even heat distribution and moisture retention, optimizing crop growth conditions. Farmers in regions with variable climates, such as Northern and Central Europe, prefer conventional films for their predictability and robustness. The ability to customize conventional films with specific additives for UV stabilization, color, and thickness allows for tailored solutions for different agronomic needs. This versatility supports a wide range of cropping systems and farming practices. While biodegradable films are improving, they often struggle to match the long-term durability of conventional plastics under extreme conditions. This performance gap keeps conventional films as the default choice for risk-averse farmers who prioritize crop security and yield consistency over environmental considerations. The proven track record of conventional materials builds trust and loyalty among agricultural professionals.

The biodegradable mulch films segment is predicted to witness the highest CAGR of 12.5% between 2026 and 2034 owing to stringent regulatory bans on single-use plastics and non-degradable agricultural films across Europe. According to European environmental policy guidelines, the transition toward biodegradable mulch options is driven by soil-protection initiatives and microplastic reduction strategies rather than the Single Use Plastics Directive. As per regulatory tracking from the French Agency for Ecological Transition (ADEME), the accelerating use of alternative mulch sheets in France relies on national microplastic mitigation targets and EN 17033 standardization instead of an active ban on conventional plastics. This regulatory pressure eliminates the option of using conventional films for many crops, compelling farmers to adopt bio-based solutions regardless of cost. Governments are supporting this transition through subsidies and technical assistance programs to help farmers manage the higher costs and logistical changes. The definition of biodegradability under standards such as EN 17033 provides clarity and confidence to buyers, ensuring that products meet specific decomposition criteria in soil. This legal framework creates a protected market for biodegradable films, shielding them from direct price competition with conventional plastics. Manufacturers are responding by expanding production capacities and investing in research to improve product quality. The regulatory push is not temporary but part of a long-term strategy to eliminate plastic pollution in agriculture, ensuring sustained growth for the biodegradable segment. Compliance becomes a business necessity, driving widespread adoption across the continent.

The swift expansion of the biodegradable segment is fueled by increasing consumer demand for sustainable and organic produce, which encourages retailers and farmers to adopt eco-friendly farming practices. European consumers are increasingly aware of the environmental impact of plastic pollution and prefer products grown without synthetic materials that leave residues in the soil. As per a study published by the European Consumer Organisation (BEUC), over 60% of European consumers express a willingness to support sustainable farming methods, indirectly encouraging supply chains to adopt eco-friendly production materials. Retailers and supermarket chains are responding to this demand by setting strict sustainability criteria for their suppliers, requiring the use of biodegradable inputs to maintain certification and brand image. Organic farmers, who are prohibited from using synthetic plastics, are natural adopters of biodegradable films, and the expansion of the organic sector directly boosts this segment. The marketing advantage of using biodegradable films allows farmers to differentiate their products and access premium markets. Brand owners are highlighting their use of eco-friendly technologies in packaging and advertising, appealing to environmentally conscious shoppers. This consumer-driven pull complements the regulatory push, creating a powerful dual force for growth. The alignment with corporate social responsibility goals of large food companies further accelerates adoption. As awareness grows, the preference for sustainable agriculture becomes mainstream, ensuring long-term demand for biodegradable mulch solutions.

By Crop Type Insights

The vegetables segment was the largest in the Europe mulch films market and occupied a commanding share in 2025. This prominence of the segment was driven by the high-value nature of vegetable crops and the intensive cultivation practices employed to maximize yield and quality. Vegetables such as tomatoes, peppers, cucumbers, and strawberries require precise control over soil temperature, moisture, and weed competition to achieve optimal growth and marketable output. According to Eurostat, vegetables account for a significant portion of the utilized agricultural area in Southern Europe, where mulch film usage is most prevalent due to favorable climatic conditions for intensive farming. Mulch films enable earlier planting and harvesting by warming the soil, extending the growing season, and allowing farmers to capture higher prices in early markets. The suppression of weeds reduces labor costs and eliminates the need for herbicides, which is crucial for meeting residue limits in fresh produce. The protection of fruits from soil contact prevents rotting and disease, improving overall quality and reducingpost-harvestt losses. Commercial vegetable growers operate on tight schedules and high-volume outputs, making the efficiency gains from mulch films essential for profitability. The widespread adoption of drip irrigation in vegetable farming synergizes perfectly with mulch films, enhancing water use efficiency. This combination of agronomic benefits and economic returns makes mulch films indispensable for vegetable production. The consistent demand from the fresh produce sector ensures steady consumption of mulch films. The segment benefits from continuous innovation in film types tailored to specific vegetable requirements.

The spearheading of this segment is also supported by ongoing labor shortages in the European agricultural sector and the trend toward mechanization. Weeding is one of the most labor-intensive tasks in vegetable farming, and the scarcity of seasonal workers has made manual weeding increasingly difficult and expensive. Mulch films provide an effective mechanical barrier against weeds, significantly reducing the need for manual labor and associated costs. As per the European Agricultural Machinery Association (CEMA), severe agricultural labor shortages are driving an acceleration in the procurement of high-efficiency specialized field machinery, facilitating the automated application of mulch layers over expanded commercial scales. This mechanization makes mulch filming economically viable even for larger operations where labor costs would otherwise be prohibitive. The consistency and speed of machine-applied films ensure uniform coverage and better agronomic results. Farmers are incentivized to adopt mulch films to mitigate the risk of crop loss due to weed competition when labor is unavailable. The integration of mulch films into automated farming systems enhances overall operational efficiency. This technological alignment ensures that mulch films remain a core component of modern vegetable production. The segment benefits from the broader trend toward precision agriculture and resource optimization. The reliability of mulch films in reducing labor dependency secures their position as a critical input for the vegetable industry.

The fruits segment is estimated to register the fastest CAGR of 11.8% over the forecast period due to the expansion of berry cultivation and the adoption of protected agriculture techniques across Europe. Berries such as strawberries, raspberries, and blueberries are high-value crops that benefit immensely from the microclimate control provided by mulch films. According to research, the area under berry cultivation in Europe has increased by 15% in the last five years, driven by rising consumer demand for fresh and healthy snacks. Mulch films help maintain clean fruit by preventing contact with soil, reducing disease incidence, and improving aesthetic quality. The ability to regulate soil temperature extends the harvesting window, allowing for longer production periods and higher total yields. Protected agriculture structures such as tunnels and greenhouses frequently use mulch films to enhance humidity control and root zone management. The high profit margins of berry farming allow growers to invest in premium mulch films that offer specialized features such as infrared transmission or pest deterrence. The trend towardyear-roundd availability of fresh berries drives the adoption of advanced growing techniques where mulch films play a key role. This segment benefits from the premium positioning of berries in the retail market. The sensitivity of berry roots to temperature fluctuations makes mulch films essential for stable production. The growth of this segment reflects the shifting dietary preferences of European consumers.

The rapid growth of the fruits segment is also fueled by the need to adapt to climate change and address water scarcity concerns in major fruit-producing regions. Rising temperatures and irregular rainfall patterns threaten traditional fruit production, making moisture retention and temperature regulation critical for crop survival. Mulch films significantly reduce water evaporation from the soil surface, conserving precious water resources and ensuring consistent moisture levels for fruit trees and bushes. According to the European Drought Observatory, several Southern European regions have experienced severe drought conditions in recent years, prompting farmers to adopt water-saving technologies,s including mulch films. Fruit orchards and vineyards are increasingly using mulch films to protect root systems from heat stress and maintain soil health. The reduction in irrigation frequency lowers energy costs and operational complexity. Climate-resilient farming practices are becoming a priority for fruit growers who face unpredictable weather events. Mulch films provide a buffer against extreme temperatures, protecting crops from heat waves and frost. This adaptive capability makes mulch films an attractive investment for risk mitigation. The segment benefits from government incentives for sustainable water management. The alignment of mulch films with climate adaptation strategies ensureslong-termm relevance and growth. The focus on resilience drives adoption in both traditional and emerging fruit-growing areas.

COUNTRY LEVEL ANALYSIS

Spain Mulch Films Market Analysis

Spain led the Europe mulch films market and captured a significant share in 2025. This leading position of the segment was attributed to its extensive horticultural sector and favorable climatic conditions for intensive agriculture. The country is a leading producer of vegetables and fruits, particularly in regions like Almería and Murcia, where mulch films are extensively used to enhance yield and quality. According to the Spanish Ministry of Agriculture, the area under protected cultivation in Spain exceeds 60000 hectares, creating a substantial demand for agronomic plastics. Spanish farmers are early adopters of advanced mulch technologies due to the high value of their exports to the rest of Europe. The government supports sustainable farming practices through subsidies for water-saving technologies, encouraging the use of mulch films in conjunction with drip irrigation. Regulatory pressures are driving a gradual shift toward biodegradable options, although conventional films still dominate due to cost considerations. The presence of major plastic manufacturers in Spain facilitates local supply and innovation. The country’s focus on export quality standards necessitates the use of mulch films to ensure clean and uniform produce. Water scarcity issues in southern Spain further boost the adoption ofmoisture-retainingg mulch films. The mature market structure ensures steady demand and continuous technological upgrades. Spain serves as a key hub for mulch film innovation and distribution in Southern Europe.

Italy Mulch Films Market Analysis

Italy occupies a significant position in the Europe mulch films market because of its diverse agricultural output and strong emphasis on quality produce. The country is a major producer of tomatoes, peppers, and berries in regions like Emilia-Romagna and Sicily, where mulch films are integral to production systems. According to ISTAT, the Italian agricultural sector utilizes a significant amount of plastic mulch, with a growing trend toward biodegradable alternatives due to strict national regulations. As per sources, while Italy pioneered restrictions on single-use carrier bags, its expansion into biodegradable agricultural films is driven by strict corporate collection fees and organic certifications rather than an outright ban on conventional mulch films. Italian farmers value the aesthetic and quality improvements provided by mulch films, which are crucial for domestic and export markets. The presence of renowned food brands encourages sustainable sourcing practices, including the use ofeco-friendlyy mulch. Research institutions in Italy are actively developing new biodegradable formulations suited to local soil conditions. The strong cooperative structure among Italian farmers facilitates collective purchasing and knowledge sharing about mulch technologies. The focus on organic farming in certain regions further boosts demand for compliant mulch solutions. Italy’s regulatory leadership influences broader European trends. The market is characterized by a balance between tradition and innovation.

France Mulch Films Market Analysis

France holds a notable share in the Europe mulch films market due to its large agricultural base and progressive environmental policies. The country is a major producer of vegetables and fruits, with significant mulch film usage in regions like Brittany and Provence. As per the French Agency for Ecological Transition (ADEME), the integration of soil-biodegradable mulch alternatives across French farms is accelerated by strict domestic microplastic mitigation objectives and adherence to standardized European biodegradable guidelines. French consumers are highly conscious of environmental issues, pushing retailers to demand sustainably produced food. This consumer pressure complements regulatory mandates, creating a strong market for eco-friendly mulch solutions. Major French retailers have committed to reducing plastic waste in their supply chains, encouraging farmers to switch to biodegradable options. The government provides technical support and funding for farmers transitioning to sustainable practices. French manufacturers are investing in research to improve the performance and cost competitiveness of biodegradable films. The country’s strong agricultural research sector supports innovation in agronomic plastics. The market in France is characterized by high regulatory compliance and consumer awareness. The shift toward biodegradables is more advanced here than in many other European countries.

Germany Mulch Films Market Analysis

Germany is moving ahead steadfastly in the Europe mulch films market, owing to its strong focus on sustainability and efficient resource use. Although the climate is open-field suitable for extensive open-field mulching compared to Southern Europe, Germany has a significant protected cultivation sector for vegetables and berries. According to the German Agricultural Society, the adoption of precision farming techniques includes the use of specialized mulch films to optimize water and nutrient use. German farmers prioritize environmental protection, leading to a high interest in biodegradable and recyclable products. The country has a well-established recycling infrastructure for agricultural plastics, encouraging the use of recyclable conventional films. Strict environmental regulations drive innovation in sustainable materials. German manufacthigh-quality bio-basedroducing high quality bio based polymers for agricultural applications. The market is characterized by high standards for product quality and environmental performance. Consumer demand for organic produce supports the use of compliant mulch films. The focus on circular economy principles shapes market dynamics. Germany serves as a testbed for new sustainable technologies. The market values efficiency and ecological integrity.

Netherlands Mulch Films Market Analysis

The Netherlands is a key contributor to the Europe mulch films market due to its advanced greenhouse technology and horticultural expertise. The country is a global leader in protected agriculture, where mulch films are used for high-value crops such as tomatoes and peppers. Extensively, according to Wageningen University, Dutch growers are pioneers in integrating mulch films with automated irrigation and climate control systems to maximize resource efficiency. The focus on sustainability and circular agriculture drives demand for biodegradable and recyclable mulch options. Dutch regulations encourage the reduction of plastic waste, prompting innovation in material science. The country’s dense agricultural landscape requires efficient land use, making mulch films essential for intensification. Export-oriented production demands high-quality and clean produce, which mulch films help achieve. The Netherlands acts as a gateway for new mulch technologies into the European market. Collaborations between researchers and industry players accelerate product development. The market is characterized byhigh-techh adoption and environmental consciousness. The emphasis on precision and sustainability defines the Dutch approach.

COMPETITIVE LANDSCAPE

The competition in the Europe mulch films market is characterized by a mix of established multinational manufacturers and specialized regional producers who vie for dominance through innovation and sustainability credentials. The market exhibits moderate fragmentation with no single enti, ty holding overwhelming control, allowing for dynamic competition and continuous technological advancement. Key competitors distinguish themselves through product quality, regulatory compliance, and environmental stewardship rather than price alone. The barrier to entry remains relatively high due to stringent regulatory requirements for biodegradability and the need for advanced manufacturing capabilities. Companies invest significantly in research and bio-based ingredients to create proprietary bio-based formulations that offer superior performance and reliability. Brand reputation and trust are critical assets as farmers become more educated about the environmental impact of their choices. Strategic alliances with research institutions and agricultural organizations enhance credibility and facilitate knowledge sharing. The competitive landscape is further shaped by growing demand for circular solutions, which forces players to invest in recycling infrastructure and waste management systems. Innovation in film thickness,s durability, and ease of removal serves as a key differentiator. The presence of private label offerings from large distributors adds pressure on branded manufacturers to justify premium pricing through added value. Overalll,l the market rewards companies that can combine scientific rigor with transparent sourcing and effective customer engagement.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Europe Mulch Films Market include

- Berry Global Inc.

- BASF SE

- Novamont S.p.A.

- RKW Group

- Coveris Holdings S.A.

- Armando Alvarez Group

- Trioplast Industrier AB

- Ab Rani Plast Oy

- Polythene UK Ltd.

- AEP Industries Inc.

- Ginegar Plastic Products Ltd.

- Plastika Kritis S.A.

TOP LEADING PLAYERS IN THE MARKET

- Rani Plast operates as a leading manufacturer of agricultural films in Europe with a strong focus on high-performance solutions and high-performance mulch products. The company serves farmers across the continent by providing durable conventional and innovative biodegradable films that enhance crop yield and soil health. Recent actions include the expansion of its production capacity in Finland and the growing demand for eco-friendly agricultural plastics. Rani Plast has strengthened its bio-based position by launching new bio-based mulch films that comply with strict European environmental standards. The company actively collaborates with research institutions to develop materials that offer superior mechanical strength and controlled degradation rates. Their commitment to circular economy principles drives investment in recycling technologies and waste reduction initiatives. Rani Plast participates in industry forums to promote best practices for plastic use in agriculture. This proactive approach builds trust among environmentally conscious farmers and regulators. The company continues to innovate with customized film solutions tailored to specific climatic and crop requirements. Their dedication to quality and sustainability ensureslong-termm competitiveness in the evolving European market.

- RKW Group is a prominent player in the European agricultural plastics sector known for its extensive portfolio of mulch films and technical high-quality products. The company supplies high-quality polyethylene and biodegradable films to farmers in major agricultural regions including Spain, Italy, and France. Recent strategic initiatives include the development of advanced infrared transmitting films that improve early-season temperature for early-season crops. RKW Group has strengthened its presence by partnering with local distributors to improve supply chain efficiency and customer support. The company invests heavily in research and development to create films with enhanced UV stability and puncture resistance. Their focus on sustainability is evident in the introduction of recyclable mulch options that align with EU regulations. RKW Group engages in educational programs to help farmers understand the benefits of modern mulching techniques. This customer-centric approach fosters loyalty and drives adoption of premium products. The company leverages its manufacturing scale to offer competitive pricing without compromising quality. Continuous innovation in materials science keeps RKW Group at the forefront of the industry.

- Novamont stands out as a key innovator in the biodegradable mulch films segment, leveraging its proprietary Mater Bi technology to produce compostable agricultural solutions. The company plays a crucial role in helping European farmers transition away from conventional plastics by offering certified biodegradable alternatives. Recent actions include expanding partnerships with major film converters across Europe to increase the availability of MatBi-based mulch films. Novamont has strengthened its market position by obtaining additional certifications for soil biodegradability, ensuring compliance with diverse national regulations. The company actively supports field trials to demonstrate the efficacy of its products in various cropping systems. Their collaboration with agricultural associations helps educate stakeholders about the environmental benefits of biodegradable mulches. Novamont focuses on creating a circular value chain by promoting industrial composting infrastructure. The strategy addresses end-of-life production and end-of-life management challenges. The company’s technological leadership in bio polymers drives continuous improvement in product performance. Novamont remains committed to sustainability and innovation in the agricultural plastics sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe mulch films market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies developing advanced biodegradable and recyclable films to meet stringent environmental regulations. Strategic partnerships with local distributors and agricultural cooperatives enhance market penetration and ensure consistent supply across diverse regions. Companies focus heavily on research and development to improve the mechanical properties and bio-based degradation rates of bio-based materials. Investment in sustainable manufacturing processes and circular economy initiatives helps brands align with corporate social responsibility goals. Educational campaigns and technical support services assist farmers in adopting new mulching technologies effectively. Compliance with evolving EU standards such as EN 17033 is prioritized to build trust and ensure market access. Expansion into niche segments like organic farming and higher-margin cultivation offers higher-margin opportunities. Digital tools for precision agriculture are integrated to optimize film application and resource use. These combined strategies enable participants to navigate regulatory challenges and capitalize on the growing demand for sustainable agricultural solutions.

EUROPE MULCH FILMS MARKET NEWS

In September 2023, Novamont partnered with several Italian film converters to expand the Bi-based network of its Mater Bi-based biodegradable mulch solutions across Southern Europe.

In November 2023, RKW Group collaborated with a Spanish agricultural cooperative to conduct field trials for new durable biodegradable mulch films in strawberry cultivation.

MARKET SEGMENTATION

This research report on the europe mulch films market is segmented and sub-segmented into the following categories.

By Material Type

- Conventional Mulch Films

- Biodegradable Mulch Films

By Crop Type

- Vegetables

- Fruits

By Country

- Spain

- Italy

- France

- Germany

- Netherlands

Frequently Asked Questions

1. Which material type leads the market?

Conventional polyethylene (PE) films, especially LLDPE/LDPE, still dominate by volume, while biodegradable mulches are a smaller but fast‑growing segment.

2. Which application is most important?

Vegetable farming is the largest application, followed by horticulture and floriculture, where mulch films help improve yield quality and reduce labor for weeding and irrigation.

3. Which countries are key markets?

Italy, France, Germany, Spain, and the Benelux region are major users, with strong adoption in Southern and Western Europe where intensive horticulture and protected cultivation are concentrated

4. How big is the market in volume terms?

The overall European mulch film market is around 80,000 tonnes per year, with only a small share currently certified biodegradable but growing as regulations and awareness increase.

5. What are the main challenges?

Challenges include plastic waste and microplastic concerns from conventional PE films, collection and disposal issues, higher cost of biodegradable films, and varying national regulations on film use and disposal.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com