Europe Nebulizer Market Size, Share, Trends & Growth Forecast Report By Product, Modality, End-User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Market Size, 2025

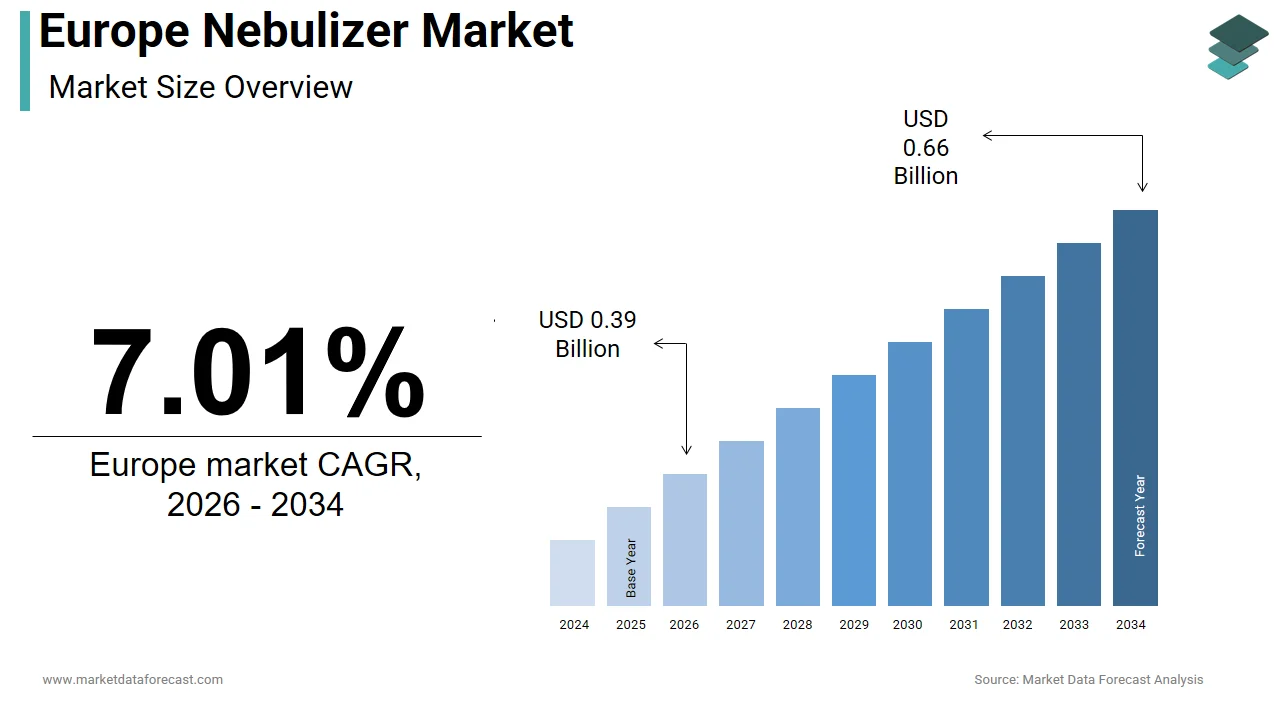

$0.36 BnMarket Estimate, 2026

$0.39 BnMarket Forecast, 2034

$0.66 BnCAGR, 2026–2034

7.01%Europe Nebulizer Market Size

The size of the Europe nebulizer market was valued at USD 0.36 billion in 2025. This market is expected to grow at a CAGR of 7.01% from 2026 to 2034, reaching USD 0.66 billion by 2034, up from USD 0.39 billion in 2026.

The nebulizer devices are used to administer aerosolized medications directly to the lungs for the treatment of respiratory conditions such as asthma, chronic obstructive pulmonary disease, and cystic fibrosis. Nebulizers convert liquid drugs into inhalable mist, offering therapeutic efficiency for patients with compromised respiratory function or those unable to use handheld inhalers. As per the European Lung Foundation, over 30 million people in the European Union live with chronic respiratory diseases that may require nebulized therapy at some stage of care. The air pollution contributes to more than 600,000 premature deaths annually across the region, exacerbating the prevalence of respiratory ailments and indirectly increasing reliance on therapeutic delivery systems like nebulizers.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases Drives Demand for Nebulizers

The chronic respiratory diseases remain a leading cause of morbidity, which is a major factor propelling the growth of the Europe nebuliser market. According to the European Respiratory Society, chronic obstructive pulmonary disease affects approximately 50 million individuals in Europe, with incidence rates continuing to climb due to aging populations and persistent environmental risk factors. Asthma prevalence is equally concerning, with the Global Asthma Network estimating that nearly 55 million Europeans suffer from asthma, including over 8 million children. These conditions often require long-term management involving bronchodilators and anti-inflammatory agents delivered via nebulization in severe or pediatric cases where metered dose inhalers prove ineffective or impractical. The UK’s National Institute for Health and Care Excellence endorses nebulizer use in hospital-at-home programs to reduce inpatient admissions, which reflects a systemic shift toward decentralized care models.

Technological Advancements in Portable and Smart Nebulizers Stimulate Market Growth

Innovation in nebulizer design has significantly expanded usability and patient adherence, which is another factor boosting the growth of the Europe nebulizer market. Modern portable mesh nebulizers, which operate silently and deliver medication in under five minutes, have gained traction among working adults and school-aged children who prioritize discretion and speed. As per the European Commission’s Joint Research Centre, over 70% of European households now own at least one connected health device, which is creating fertile ground for smart nebulizers equipped with Bluetooth connectivity, usage tracking, and dose reminders. Companies such as OMRON and Philips have introduced nebulizers that sync with mobile applications to provide real-time feedback to both patients and clinicians by aligning with the European Union’s Digital Health Action Plan.

MARKET RESTRAINTS

Stringent Regulatory Approval Processes Delay Product Commercialization

The significant headwinds from the rigorous and time-intensive medical device regulatory framework, particularly under the European Union Medical Devices Regulation 2017/745, are solely restraining the growth of the Europe Nebulizer Market. Unlike previous directives, this regulation mandates comprehensive clinical evidence, post-market surveillance, and risk classification reassessments for all nebulizers, regardless of technological novelty. Currently, only 23 notified organizations across the EU are authorized to assess respiratory devices by creating disproportionately affecting small and medium enterprises lacking regulatory expertise. These delays not only increase development costs are estimated at an additional 200,000 euros per product by the European Health Management Association, but also stifle innovation cycles by preventing timely access to improved therapies.

Limited Reimbursement Coverage for Advanced Nebulizers in Key European Markets

The inconsistent and restrictive reimbursement policies across Europe constrain the widespread adoption of advanced technologies is also hampering the growth of the Europe nebulizer market. In France and Spain, public health systems reimburse only basic jet nebulizers priced below 50 euros, excluding mesh and smart variants from coverage despite their superior efficacy and adherence benefits. This fragmentation forces patients in non-reimbursing countries to pay out of pocket, with mesh devices costing up to 150 euros, with a prohibitive expense for many, given that the median disposable income in Southern and Eastern Europe remains below 1,500 euros per month, as per Eurostat. The absence of harmonized reimbursement criteria under the EU Health Technology Assessment framework perpetuates inequity in access and discourages manufacturers from investing in localized market strategies.

MARKET OPPORTUNITIES

Expanding Home Healthcare Infrastructure Creates New Market Avenues

The structural shift toward home-based care is certainly to pose new opportunities for the growth of the Europe nebulizer market with aging demographics and fiscal pressures on hospitals. European governments are actively de-institutionalizing chronic disease management. According to the Organisation for Economic Co-operation and Development, home healthcare expenditure in the EU grew by 12% annually between 2020 and 2024, with respiratory therapy constituting a major service line. Germany’s Home Treatment Initiative, launched in 2022, now covers nebulizer rentals and consumables for over 2 million patients with chronic lung conditions by reducing avoidable hospital admissions by an estimated 18%, as per the source. Similarly, the UK’s Integrated Care Systems have integrated nebulizer provision into community nursing protocols by enabling pharmacists and district nurses to dispense and train patients on device use. Manufacturers are responding by developing user-friendly, maintenance-free nebulizers with extended battery life and simplified cleaning protocols.

Integration of Nebulizers into National Respiratory Health Programs Offers Scale Potential

Several European countries are embedding nebulizer access into comprehensive public health initiatives targeting respiratory disease burden, opening scalable distribution channels, which is likely to bolster the growth of the Europe nebulizer market. As per the Polish Ministry of Health, over 50,000 nebulizers were distributed to family doctors in 2024 alone under this scheme. Likewise, Portugal’s National Asthma Plan includes subsidized nebulizer kits for children from low-income households, reaching nearly 12,000 families in its first year, as per the Directorate General of Health. The European Commission’s Horizon Europe funding stream has also prioritized projects that integrate medical devices like nebulizers into digital primary care pathways, with three cross-border consortia receiving grants exceeding 8 million euros in 2024.

MARKET CHALLENGES

Intense Price Competition from Low-Cost Manufacturers Erodes Profit Margins

The increasing challenges by aggressive pricing strategies from non-European manufacturers, particularly those based in China and India, which supply basic jet nebulizers at 30 to 50% below the average EU price, may act as a barrier for the growth of the Europe nebulizer market. As per the European Trade Statistics for Medical Devices, imports of low-cost nebulizers into the EU surged by 28% in 2024 compared to 2021, with the majority entering through distribution hubs in the Netherlands and Belgium. In Spain’s 2023 national tender for respiratory devices, 70% of awarded contracts went to Asian suppliers offering units below 35 euros, effectively excluding European innovators with higher R&D costs.

Lack of Standardized Clinical Protocols Hinders Optimal Device Utilization

The absence of unified clinical protocols governing device selection, maintenance, and patient training across member states is another factor degrading the growth of the Europe nebulizer market. According to a 2024 audit by the European Respiratory Society, only 11 of 27 EU countries have national guidelines specifying which nebulizer type is appropriate for specific respiratory conditions or patient profiles. Device contamination is another concern, with the European Centre for Disease Prevention and Control reporting that 22% of home nebulizers in community use showed microbial growth due to improper cleaning, a risk amplified by the lack of standardized hygiene instructions. These gaps not only diminish clinical effectiveness but also increase the burden on secondary care when treatments fail.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Modality, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Briggs Healthcare, Besco Medical, Ca-Mi, De Vilbiss Healthcare, Feellife Health, Flyp, Invacare, Omron, Philips Respironics, and Pari Pharma. |

SEGMENTAL ANALYSIS

By Product Insights

The jet segment was accounted for in holding 58.3% of the Europe nebulizer market share in 2024, with their widespread integration into public healthcare systems and cost effectiveness. The established procurement contracts and compatibility with a broad range of generic respiratory medications are also expected to elevate the growth of the segment. National health services in Southern Europe particularly favor these devices because they retail for as low as 25 euros compared to over 100 euros for advanced alternatives.

The mesh segment in the Europe nebulizer market is projected to register a CAGR of 12.3% from 2025 to 2033, with the rising demand for silent and efficient home-based respiratory therapy, especially among pediatric and elderly populations. A 2024 survey by the European Lung Foundation found that 71% of caregivers prefer mesh nebulizers because treatment sessions last under six minutes compared to 15 minutes with jet models. As per the research, over 40% of new mesh nebulizers launched in the EU since 2022 feature Bluetooth connectivity and companion apps that log usage patterns and send reminders. Germany’s statutory health insurers began partial reimbursement for these smart devices in early 202,4, further boosting adoption. Additionally, clinical validation supports this shift. A multicenter trial published by the European Respiratory Journal confirmed that mesh nebulizers achieve 55% higher lung deposition of bronchodilators, which directly improves symptom control and reduces rescue medication use.

By Modality Insights

The table top segment was accounted for in holding a prominent share of the Europe nebulizer market in 2024, with their entrenched presence in institutional settings where continuous use and robust performance are prioritized over portability. Hospitals across Europe, including over 90% of public facilities in Spain and Italy, rely on table-top units due to their durability and ability to handle high viscosity medications like hypertonic saline used in cystic fibrosis management. Additionally, these units require less frequent replacement with an average service life exceeding five years, as documented by the German Institute for Medical Documentation and Information, thus reducing long-term operational costs for healthcare providers.

The portable segment is expected to grow at the fastest CAGR of 13.1% from 2025 to 2033, with the rapid expansion propelled by policy shifts toward home-based care and patient-centric treatment models. The United Kingdom’s National Health Service reported in 2024 that over 600,000 nebulizer-dependent patients now receive therapy at home, a figure that has doubled since 2020, largely due to reduced hospital readmission targets. As per the European Innovation Council, over 22 new portable nebulizer models weighing under 200 grams were CE certified in 2024 alone, enabling discreet use in schools and workplaces. Battery performance has also improved significantly, with leading devices now offering up to 30 treatment cycles per charge as verified by the Swiss Federal Office of Public Health.

By End User Insights

The hospitals segment was the largest by occupying 52.3% of the Europe nebulizer market share in 2024, with the high volume of acute respiratory cases managed in emergency and inpatient departments. Data from the European Society of Intensive Care Medicine reveals that European hospitals administer over 12 million nebulized treatments annually, with jet nebulizers remaining standard due to compatibility with hospital air compressor systems and protocols for aerosolized antibiotic delivery in ventilator-associated pneumonia. According to the European Procurement Oversight Authority, hospital purchasing groups in Germany, the Netherlands, and Sweden negotiate bulk contracts that lock in device supply for three to five years, ensuring consistent volume absorption. Additionally, hospitals serve as primary training hubs for new respiratory therapies, with over 70% of specialist nurses certified in nebulizer use through hospital-based programs as per the European Federation of Nurse Practitioners, thereby reinforcing institutional reliance on established systems.

The home care settings segment is likely to grow at a projected CAGR of 14.2% from 2025 to 2033, owing to the national strategies to reduce hospital burden. Germany’s Home Ventilation and Aerosol Therapy Program now covers nebulizer costs for over 1.8 million chronic respiratory patients, as per a recent survey. Eurostat reports that 29.4% of the EU population will be aged 65 or older by 2030, up from 21.3% in 2022, increasing demand for self-administered therapies. Portable mesh nebulizers have become central to this shift, with the European Consumer Health Panel noting that 68% of home users prioritize quiet operation and fast delivery.

COUNTRY LEVEL ANALYSIS

Germany Nebulizer Market Analysis

Germany was the top performer of the Europe nebulizer market with 22.3% of share in 2024, with a combination of comprehensive health insurance coverage, advanced home care infrastructure, and a high prevalence of chronic respiratory diseases. Over 13 million Germans suffer from asthma or COPD, as documented by the Robert Koch Institute, and statutory health insurers reimburse both basic and smart nebulizers under long-term care provisions. The country’s integrated care contracts, introduced in 2023, further incentivize home-based nebulization by linking provider payments to reduced hospital admissions. Additionally, Germany hosts major nebulizer manufacturers, including PARI Pharma, whose clinical partnerships with university hospitals drive rapid adoption of next-generation devices.

United Kingdom Nebulizer Market Analysis

The United Kingdom nebulizer market held 16.3% of share in 2024. The National Health Service’s strategic pivot toward community-based respiratory care has been the primary growth engine, with over 7,00,000 nebulizer prescriptions issued annually through general practitioners and community nurses. Furthermore, the UK has one of Europe’s highest asthma prevalence rates, affecting many people, according to Asthma UK, and pediatric nebulizer use is standard in school health protocols. Recent investments in digital health, including the rollout of the NHS App, now enable remote monitoring of nebulizer adherence, strengthening the viability of home therapy. Regulatory agility post-Brexit has also allowed the Medicines and Healthcare products Regulatory Agency to fast-track innovative respiratory devices, accelerating market access.

France Nebulizer Market Analysis

France nebulizer market growth is likely to be driven by the centralized reimbursement policies and a dense network of outpatient respiratory clinics known as pneumology centers, which collectively manage over 4 million chronic respiratory patients. Additionally, France maintains stringent device safety standards through the National Agency for Medicines and Health Products Safety, which encourages domestic and EU manufacturers to prioritize quality over cost, a factor that sustains demand for clinically validated nebulizers despite price pressures.

Italy Nebulizer Market Analysis

Italy nebulizer market is anticipated to have lucrative growth opportunities in next coming years. High disease burden and regional healthcare decentralization define its market dynamics. Italy has one of the highest COPD mortality rates in Europe, with over 28,000 annual deaths, which is standard in both hospital and home management, especially in aging southern regions. However, market fragmentation persists as each of Italy’s 21 regions manages its own procurement, leading to variability in device availability.

Spain Nebulizer Market Analysis

Spain nebulizer market growth is accelerated by strong public sector dependence and growing emphasis on pediatric respiratory care. Spain’s National Health System supplies nebulizers at no cost to patients diagnosed with chronic respiratory conditions under the Specialized Pharmaceutical Provision program, which served over 1.2 million individuals in 2024. Asthma prevalence is particularly high among children, with the Spanish Society of Pediatric Pulmonology reporting that 13.5% of school-aged children require regular bronchodilator therapy, many via nebulization due to coordination challenges with inhalers.

COMPETITIVE LANDSCAPE

The Europe Nebulizer Market features a competitive landscape characterized by a blend of global medical technology giants and specialized regional players. Competition centers on clinical efficacy, user experience, regulatory agility, and integration with evolving care pathways rather than price alone. Established firms leverage longstanding relationships with national health systems and robust clinical data to maintain institutional presence while simultaneously adapting to the rise of home-based care. New entrants face significant barriers, including lengthy CE certification timelines, limited notified body capacity, and fragmented reimbursement policies across member states. Differentiation increasingly hinges on digital capabilities, battery performance, treatment speed, and compatibility with a wide range of respiratory medications. The market also sees active consolidation as larger players acquire niche innovators to bolster smart device portfolios.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe nebulizer market include

- Briggs Healthcare

- Besco Medical

- Ca-Mi

- De Vilbiss Healthcare

- Feellife Health

- Flyp

- Invacare

- Omron

- Philips Respironics

- Pari Pharma

TOP PLAYERS IN THE MARKET

- PARI Pharma is a Germany-based leader in aerosol drug delivery with deep roots in the European respiratory care landscape. The company specializes in high-performance jet and mesh nebulizers integrated with proprietary inhalation systems for conditions like cystic fibrosis and COPD. In recent years, PARI has expanded its clinical collaboration network with academic hospitals across Germany and the Netherlands to validate next-generation devices under real-world conditions. It launched the PARI BOY mobile system in 2023, featuring silent mesh technology and rechargeable battery operation aimed at home and pediatric users. The firm also strengthened its regulatory strategy by securing early conformity assessments under the EU Medical Devices Regulation, ensuring uninterrupted market access across the region.

- OMRON Healthcare maintains a strong footprint in the Europe nebulizer market through its focus on user-centric portable solutions. Headquartered in Japan, the company has tailored its European portfolio to meet local reimbursement and usability expectations, particularly in France, the UK, and Italy. The company has also deepened partnerships with pharmacy chains and home care distributors to expand direct-to-consumer access. Additionally, OMRON integrated its nebulizers with its digital health ecosystem, allowing clinicians to remotely monitor adherence through its Omron Connect app, a move aligned with national digital health strategies in several EU countries.

- Philips Healthcare has significantly reinforced its position in European respiratory therapy by embedding nebulization into its broader home ventilation and sleep apnea platforms. Based in the Netherlands, the company leverages its hospital-to-home care continuum to promote integrated respiratory solutions. In 2023, Philips launched the InnoSpire Go Smart nebulizer across major EU markets, featuring Bluetooth connectivity and guided inhalation feedback. The device is now included in Germany’s statutory health insurance list for severe asthma management. Philips has also invested in clinical evidence generation through multicenter trials in Sweden and Spain, demonstrating improved lung deposition and reduced exacerbation rates.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe Nebulizer Market prioritize regulatory compliance under the EU Medical Devices Regulation to ensure uninterrupted market access. They invest heavily in clinical validation through multicenter trials to substantiate performance claims and support reimbursement applications. Companies increasingly embed digital features such as Bluetooth connectivity, usage tracking, and mobile app integration to align with national digital health initiatives. Strategic partnerships with home care providers, pharmacy networks, and hospital procurement groups enhance distribution efficiency. Product portfolios are being refined to include silent fast-acting portable nebulizers that cater to pediatric and elderly populations. Additionally, firms are localizing post-market surveillance and service support to meet stringent EU vigilance requirements and build clinician trust.

MARKET SEGMENTATION

This Europe nebulizer market research report is segmented and sub-segmented into the following categories.

By Product

- Jet Nebulizer

- Mesh Nebulizer

- Ultrasonic Nebulizer

By Modality

- Portable

- Table-top

By End-User

- Hospitals

- Clinics

- Home care settings

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe nebulizer market?

The europe nebulizer market includes devices used for delivering respiratory medications in hospitals and home care, growing due to respiratory disease prevalence in europe nebulizer market

2. What drives growth in the europe nebulizer market?

Increased respiratory illness rates, aging population, technology advances, and expanding home healthcare boost the europe nebulizer market

3. What types dominate the europe nebulizer market?

Jet nebulizers hold the largest share, while mesh nebulizers are the fastest-growing segment in the europe nebulizer market

4. Which countries lead the europe nebulizer market?

Germany, Italy, France, and the UK are key markets driving growth in the europe nebulizer market

5. How does the rising prevalence of asthma impact the europe nebulizer market?

Growing asthma cases increase demand for nebulizer therapy devices, propelling the europe nebulizer market

6. What role does home healthcare play in the europe nebulizer market?

Expanding home care services boost demand for portable and easy-to-use nebulizers in the europe nebulizer market

7. How do technological advancements affect the europe nebulizer market?

Improvements in mesh and ultrasonic technologies enhance efficiency and patient compliance in the europe nebulizer market

8. What challenges does the europe nebulizer market face?

Challenges include device cost, regulatory compliance, and patient awareness, affecting growth in the europe nebulizer market

9. How important is pediatric care in the europe nebulizer market?

Pediatric-specific nebulizers are crucial due to high childhood asthma prevalence, a key segment in the europe nebulizer market

10. How do respiratory therapies influence the europe nebulizer market?

Increasing use of inhalation therapies for COPD and cystic fibrosis supports growth in the europe nebulizer market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com