Europe Plasma Fractionation Market Research Report By Product, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) - Industry Analysis on Size, Share, Trends, COVId-19 Impact & Growth Forecast (2026 to 2034)

Market Size, 2025

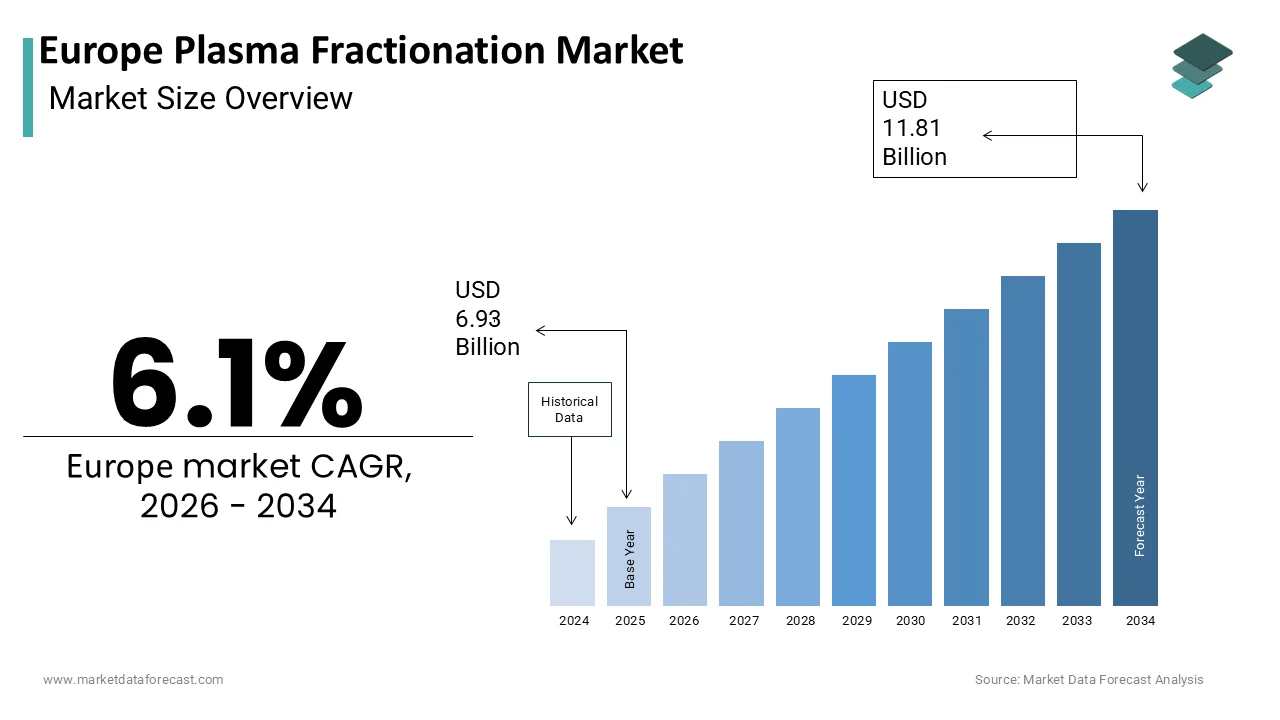

$6.93 BnMarket Estimate, 2026

$7.35 BnMarket Forecast, 2034

$11.81 BnCAGR, 2026–2034

6.1%Europe Plasma Fractionation Market Summary

Europe plasma fractionation market was valued at USD 6.53B in 2024, is estimated at USD 6.93B in 2025, and is forecast to reach USD 11.13B by 2033 (CAGR 6.1%, 2025–2033), driven by rising immunoglobulin demand, national collection expansion, and technological upgrades in fractionation.

Market snapshot

- 2024 value: USD 6.53B

- 2025 (est): USD 6.93B

- 2033 forecast: USD 11.13B

- CAGR (2025–2033): 6.1%

Core growth drivers

- Rising clinical demand for immunoglobulins and other plasma-derived proteins (immunology, neurology, hematology).

- National plasma collection programs and EU policy pressure to boost domestic supply and traceability.

- Clinical shift to subcutaneous Ig formulations that enable home therapy and broaden uptake.

- Process innovation (continuous & chromatographic fractionation), improving yield from limited plasma volumes.

Principal restraints

- Heavy reliance on imported (mainly US) paid plasma due to the limited EU plasmapheresis scale and ethical/legal constraints.

- Stringent pathogen-safety & GMP requirements that increase processing time, cost, and barrier to new entrants.

- Workforce shortages in skilled bioprocessing and specialty fractionation roles.

High-value opportunities

- Chromatography and continuous processing platforms to increase protein yield and diversify product output per litre of plasma.

- Scale-up of subcutaneous high-concentration Ig products (with hyaluronidase) for home administration and premium pricing.

- European supply-chain resiliency programs (onshoring fractionation, strategic plasma sourcing) supported by public health policy.

Major challenges

- Geopolitical and trade risks affecting imported plasma flows and lot releases.

- Ethical/legal limits on paid donation across most EU members constrain blood/plasma volumes.

- Capital intensity & long validation timelines for new fractionation plants under tightened regulatory scrutiny.

Fastest-growing segments

- Protease inhibitors & rare protein isolates: ~9.4% CAGR (driven by hereditary angioedema, AAT demand).

- Neurology applications (Ig use): ~8.9% CAGR (expanding indications and earlier diagnosis).

- Clinical laboratories & home-care monitoring services: strong double-digit growth as treatment models decentralize.

Regional dynamics

- Germany: market leader (~24.7%) — strong collection, fractionation infrastructure and reimbursement.

- France & UK: large, policy-driven markets with strong home-treatment adoption and centralized procurement.

- Italy & Switzerland: steady growth — Italy via regulated reimbursement, Switzerland via manufacturing excellence and innovation.

- Eastern Europe: constrained by limited collection capacity and slower uptake.

Competitive snapshot

- Market is oligopolistic — global leaders (CSL Behring, Grifols, Octapharma, Takeda, Kedrion, BPL, Biotest) dominate via integrated collection + fractionation + product portfolios.

- Differentiation hinges on supply reliability, pathogen-safety records, chromatography/yield tech, and home-therapy service ecosystems rather than price alone.

Commercial playbook

- Secure diversified plasma sources (domestic collection partnerships + ethically sourced imports).

- Invest in yield-maximizing chromatography & closed continuous processing to lower cost per therapeutic gram.

- Bundle products with home-care services (patient training, remote monitoring, supply logistics).

- Engage early with regulators/HTAs to streamline approvals and demonstrate safety/resilience benefits.

- Build workforce pipelines through targeted training programs and industry–academic partnerships.

Europe Plasma Fractionation Market Size

The Europe Plasma Fractionation Market is projected to grow from USD 6.93 billion in 2025 to USD 7.35 billion in 2026 and reach USD 11.81 billion by 2034, registering a CAGR of 6.1% during the forecast period from 2026 to 2034.

Plasma fractionation refers to the industrial-scale separation of human plasma into therapeutic proteins such as immunoglobulin,s album, and clotting factors through processes like cold ethanol precipitation and chromatography. These life-saving biologics treat conditions including primary immunodeficiency, hemophilia, and severe burns. Europe’s plasma fractionation ecosystem is shaped by a dual-sourcing model combining paid plasma donations from the United States and voluntary non-remunerated donations collected within the EU under strict ethical frameworks. According to sources, European nations face a significant reliance on plasma sourced from outside Europe, primarily the United States, to meet clinical demand. There has been a substantial level of plasma collection across Europe recently. A significant volume of these collections occurred predominantly in a few major European countries. The regulatory bodies have approved several new medications derived from plasma within recent years, indicating continued clinical need and development in this therapeutic area. This interplay of ethical sourcing, advanced bioprocessing, and therapeutic necessity positions plasma fractionation as a critical pillar of Europe’s biopharmaceutical sovereignty and public health infrastructure.

MARKET DRIVERS

Rising Prevalence of Immunodeficiency and Autoimmune Disorders Drives Therapeutic Demand

The increasing incidence of primary and secondary immunodeficiency conditions across the region is a primary driver of the European plasma fractionation market. This is particularly propelling demand for intravenous and subcutaneous immunoglobulins. According to research, the diagnosis rate of primary immunodeficiency in the EU is generally increasing due to greater awareness and improved diagnostic capabilities. Besides, autoimmune diseases such as chronic inflammatory demyelinating polyneuropathy and myasthenia gravis now routinely use immunoglobulins as first-line therapy. As per studies, hospital admissions for conditions treated with immunoglobulins are trending upward across Europe. National reimbursement policies amplify access. Germany's statutory health insurance provides broad coverage for immunoglobulin therapies, which represent a high cost per patient. Similarly, the French national health system provides substantial funding and coverage for necessary immunoglobulin treatments. This clinical and financial endorsement ensures sustained and growing demand for high-purity immunoglobulin G derived from large-scale fractionation processes.

Expansion of National Plasma Collection Programs Under EU Blood Directive Framework

The European Union’s concerted effort to enhance plasma self-sufficiency through voluntary non-remunerated donations is significantly boosting feedstock availability for domestic fractionation, which boosts the expansion of the European plasma fractionation market. The EU Blood Directive mandates that member states prioritize unpaid donations while allowing imports to bridge supply gaps. In response, countries like Germany and Austria have expanded plasmapheresis centers within public blood services. Germany has a significant volume of plasma collection. A plan for the plasma supply in the European Union outlines a goal to increase the proportion of internally sourced plasma for processing. Several member states have implemented dedicated facilities for collecting plasma that use certified safety protocols. This public health investment not only strengthens supply chain resilience but also aligns with the WHO’s call for national blood system autonomy. Increased domestic collection reduces reliance on third-country plasma and ensures traceability compliance with EU GMP standards.

MARKET RESTRAINTS

Stringent Regulatory Requirements for Pathogen Safety Increase Production Complexity

The European Medicines Agency’s rigorous safety mandates, which require multiple orthogonal viral inactivation and removal steps for every plasma-derived product, are a major restraint to the European plasma fractionation market. These include solvent detergent treatment, low pH incubation, nanofiltration, and pasteurization, each adding t, time cost and yield loss. According to sources, Plasma fractionation processes now generally include a higher number of validated pathogen reduction steps. This regulatory intensification increases manufacturing costs. Additionally, new pathogen threats such as emerging arboviruses necessitate continuous process revalidation. Guidance was issued requiring the screening for the Zika virus in all plasma lots sourced from regions where the virus is present. The approval timeline for new fractionation facilities has lengthened to several months due to heightened inspections. "These requirements are vital for patient safety, yet they simultaneously limit growth and increase hurdles for potential new competitors.

Ethical and Legal Restrictions on Paid Plasma Donations Limit Domestic Feedstock Supply

The prohibition of remunerated plasma donations in most EU member states, except the Czech Republic and Hungary, severely restricts the volume of locally sourced plasma available for fractionation, which obstructs the expansion of the European plasma fractionation market. The approach to plasma collection varies significantly between different regions; one major difference is the common use of compensated donation models versus systems based purely on voluntary contribution. This difference in collection models results in a notable disparity in how often individuals donate plasma. A relatively small percentage of establishments in Europe collect plasma through plasmapheresis due to a preference among donors for whole blood donation methods. This structural gap means that a substantial majority of the required raw plasma is imported from external sources. This reliance creates potential vulnerabilities in the supply chain and is a subject of ongoing ethical discussion. Current legal interpretations allow regional jurisdictions to maintain prohibitions on paid donations based on local public health considerations, which in turn sustains this external reliance. The market will face feedstock constraints until the EU creates a cohesive plasma strategy that balances ethical concerns and sufficient supply.

MARKET OPPORTUNITIES

Development of High-Yield Chromatography Platforms to Maximize Therapeutic Output

The adoption of advanced chromatography techniques in place of traditional cold ethanol fractionation offers a significant opportunity to increase yield purity and product diversity from limited plasma volumes, which is expected to propel the growth of the European plasma fractionation market. Affinity and ion exchange chromatography processes are capable of high levels of immunoglobulin recovery. Industry platforms have incorporated continuous chromatography, which may lead to reductions in processing time and buffer consumption. These advanced processing platforms facilitate the simultaneous production of various proteins from the same source material. Significant funding has been directed toward the advancement of next-generation bioprocessing technologies for plasma derivatives. This technological leap not only enhances resource efficiency but also unlocks new therapeutic avenues from existing feedstock.

Growth of Subcutaneous Immunoglobulin Formulations Expanding Treatment Accessibility

The shift from intravenous to subcutaneous immunoglobulin administration is creating a potential opportunity for the European plasma fractionation market. This is achieved by improving patients' quality of life and reducing the healthcare system. Subcutaneous formulations allow home-based self-administration with fewer systemic side effects and more stable IgG trough levels. Prescriptions for subcutaneous immunoglobulin have shown notable growth across several European countries, including Germany, France, and the UK. National health technology assessments now favor subcutaneous routes. Reduced hospital visits related to this therapy can lead to lower annual care costs. In response, fractionators are reformulating products with hyaluronidase to enable higher volume delivery and developing pre-filled syringes for ease of use. A significant portion of new immunodeficiency patients across Western Europe are beginning their treatment with subcutaneous therapy. This patient-centric trend drives demand for specialized high-concentration IgG products that command premium pricing and require precise fractionation control.

MARKET CHALLENGES

Geopolitical Disruptions Threaten Imported Plasma Supply Chains

Its heavy dependence on US-sourced plasma, which is vulnerable to trade policy shifts, regulatory divergence, and logistical barriers, is a major challenge to the European plasma fractionation market. A majority of plasma processed in Europe is sourced from collection centers in the US. Regulatory inspection processes in the US have contributed to delays in releasing processed plasma lots. Besides, proposed US legislation, such as the Plasma Independence Act, could restrict exports to prioritize domestic use. Plasma has been identified as a critical raw material with supply chain vulnerabilities within the European market. There is no formal trade agreement specifically for plasma between the EU and the US. This strategic vulnerability affects Europe’s ambition for health sovereignty and necessitates urgent diversification despite ethical and infrastructural constraints.

Shortage of Skilled Bioprocessing Personnel Constrains Facility Expansion

A growing impediment is a qualified workforce capable of operating complex aseptic bioprocessing facilities under current good manufacturing practice, which constrains the expansion of the European plasma fractionation market. Fractionation requires expertise in virology, protein chemistry, and regulatory compliance, skills in short supply across the continent. Biomanufacturing companies are noting challenges in finding qualified senior process engineers for their operations in certain regions. Specialized educational programs in highly niche areas of bioprocessing, such as plasma fractionation, appear to be limited within the EU higher education system. This talent gap delays the commissioning of new facilities. Industry surveys indicate a potentially lengthy timeframe for fully staffing new biomanufacturing facilities. Europe's goal of scaling domestic fractionation is threatened by a shortage of human capital; without specific educational investment and cross-industry training initiatives, policy and capital readiness alone won't be enough to overcome the workforce limitations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2026 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | CSL Ltd. (Australia) |

SEGMENTAL ANALYSIS

By Product Insights

The immunoglobulin segment led the European plasma Fractionation Market and captured a share of 48.8% in 2025. The dominance of the immunoglobulin segment is credited to its broad therapeutic application across immunology, neurology, and hematology, particularly for treating primary immunodeficiency disorders, autoimmune neuropathies, and immune thrombocytopenia. An additional driver is the rising diagnosis rates. Many patients across the EU received immunoglobulin treatment for various conditions, indicating growing use of this therapy. The frequency of immunoglobulin use is increasing each year due to factors such as enhanced screening and a growing number of older individuals within the population. Besides, national reimbursement frameworks strongly support access. In Germany, health coverage for immunoglobulin therapy extends to numerous medical issues. The annual cost associated with immunoglobulin treatment per patient is substantial. Immunoglobulins have been identified as essential medicinal products, prompting the need for strategic reserves to be maintained. This confluence of clinical necessity, policy backing, and expanding indications ensures immunoglobulin remains the cornerstone of plasma-derived therapeutics in Europe.

The protease inhibitors segment is estimated to register the fastest CAGR of 9.4% from 2025 to 2033, owing to the rising incidence of hereditary angioedema and chronic obstructive pulmonary disease, both treated with C1 esterase inhibitor and alpha 1 antitrypsin derived from plasma. Awareness and identification of hereditary angioedema cases are increasing across Europe. National health systems are increasingly approving on-demand and prophylactic use. Reimbursement for a specific subcutaneous C1 inhibitor treatment in France has been broadened to include a wider patient population. Besides advances in fractionation yield, enabled by chromatography, these rare proteins are economically viable to isolate. The recovery rates for individuals with alpha-1-antitrypsin deficiency have shown an upward trend in recent years. This combination of unmet medical need, regulatory support, and technological feasibility drives rapid adoption of protease inhibitors beyond niche orphan status.

By Application Insights

The immunology segment held the largest share of 42.8% of the European plasma fractionation market in 2025. The leading position of the immunology segment is attributed to the expanding use of immunoglobulins for primary and secondary immunodeficiency conditions, which affect a substantial number of patients across the EU. Early diagnosis initiatives in countries like Germany and the UK contribute to a significant increase in the identification of primary immunodeficiency patients, with the UK registry demonstrating a substantial rise in patient recruitment over recent years. Besides, immunoglobulins are first-line therapy for antibody-mediated autoimmune diseases such as Guillain-Barré syndrome and Kawasaki disease, both of which show rising incidence in pediatric populations. National treatment guidelines reinforce usage. Furthermore, the European Commission includes immunoglobulins in its list of essential medicines for rare diseases, ensuring procurement priority. This deep integration into clinical pathways across age groups and conditions sustains immunology’s dominant position.

The neurology segment is anticipated to witness the fastest CAGR of 8.9% from 2025 to 2033. The rapid expansion of the neurology segment is driven by the increasing use of intravenous and subcutaneous immunoglobulins in immune-mediated neurological disorders such as chronic inflammatory demyelinating polyneuropathy, multifocal motor neuropathy, and myasthenia gravis. The use of immunoglobulin therapy for neurological conditions is continually expanding, driven by its established efficacy in a variety of acute and chronic disorders and the development of new applications. Timely initiation of treatment, either with plasma exchange or intravenous immunoglobulin, is critical for improving the prognosis and accelerating recovery in patients with Guillain-Barré syndrome, generally recommended within the first two weeks of symptom onset. National health technology assessments support this shift. Subcutaneous immunoglobulin administration is emerging as a preferred option for some patients requiring chronic maintenance therapy for neuromuscular conditions, offering benefits such as increased autonomy and convenience compared to hospital-based intravenous infusions. Improved diagnostic capabilities through new biomarkers, combined with the expansion of specialized neuroimmunology centers, are poised to make neurological applications a primary catalyst for innovation and volume growth in the plasma derivative market.

By End User Insights

The hospitals segment dominated the European plasma fractionation market by occupying a substantial share in 2025. The prominence of this is propelled by the acute and specialized nature of plasma-derived therapies, which require controlled administration, monitoring for adverse reactions, and integration with hospital pharmacy systems. Immunoglobulins, clotting factors, and albumin are predominantly administered in inpatient settings for conditions like hemophilia, sepsis, and autoimmune crises. A different factor is the reimbursement structure. Besides, hospitals serve as centers of excellence for rare disease management. The European Medicines Agency’s risk evaluation and mitigation strategies for plasma products also mandate hospital-based administration for initial infusions. This clinical, regulatory, and financial alignment ensures hospitals remain the primary and indispensable end user channel.

The clinical laboratories segment is likely to experience the fastest CAGR of 7.6% over the forecast period. The swift acceleration of the clinical laboratories segment is due to the expanding role of specialized labs in therapeutic drug monitoring and pharmacokinetic testing for plasma-derived therapies. Hospitals rely on certified reference laboratories to manage the specialized testing of trough levels and inhibitor assays, which are critical for increasingly personalized immunoglobulin and clotting factor dosing regimens. Additionally, the rise of home therapy programs necessitates remote monitoring; patients on subcutaneous immunoglobulin mail dried blood spot samples to central labs for IgG quantification. This shift transforms labs from diagnostic support to integral components of plasma therapy management.

COUNTRY LEVEL ANALYSIS

Germany Plasma Fractionation Market Analysis

Germany top performer in the European plasma fractionation market and captured a 24.7% in 2025. The domination of the German market is driven by its robust plasma collection infrastructure, robust reimbursement policies, and high prevalence of treatable rare diseases. Apart from these, Germany hosts major fractionation facilities owned by CSL Behring and Biotest, ensuring domestic processing capacity. The National Rare Diseases Strategy mandates early diagnosis and treatment access, further boosting utilization. This synergy of collection capacity, clinical demand, and manufacturing presence cements Germany’s unrivaled market leadership.

France Plasma Fractionation Market Analysis

France followed closely in the European plasma fractionation market by capturing a 19 percent market share in 2025. The growth of the French market is due to its centralized healthcare system, which ensures rapid diagnosis and universal access to plasma-derived therapies. France has established a national registry to track a significant number of immunodeficiency patients, facilitating the proactive start of treatments. Full reimbursement is provided for all plasma-derived medicines through the national long-term illness support system. The country operates numerous dedicated centers for collecting plasma and is working toward increased collection volumes. The use of home-based subcutaneous immunoglobulin therapy is widespread and continues to be adopted by a majority of new patients. This combination of equity policy and clinical innovation sustains France’s strong and responsive market position.

United Kingdom Plasma Fractionation Market Analysis

The United Kingdom is another key player in the European plasma fractionation market. Post Brexit, the UK has intensified its focus on plasma supply security through the National Blood Service and strategic imports. The NHS commissions plasma-derived therapies through specialized immunology and hemophilia networks, ensuring standardized care. The UK is increasingly adopting subcutaneous immunoglobulin (SCIg) therapy for primary immunodeficiency maintenance, moving treatment from hospitals to homes to improve patient quality of life and reduce healthcare costs. This pragmatic blend of centralized commissioning, home care expansion, and stockpiling ensures the UK’s enduring relevance.

Italy Plasma Fractionation Market Analysis

Italy grew consistently in the European plasma fractionation market. The market is driven by strong regional specialization and growing rare disease diagnosis rates. A key driver is the mandatory reimbursement for all plasma-derived medicines under Law 210 1992, which guarantees treatment for victims of contaminated blood products and extends to all rare disease patients. Neurological applications are particularly strong. Italy accounts for a portion of Europe’s chronic inflammatory demyelinating polyneuropathy treatments. This legal and clinical commitment sustains steady growth despite regional fragmentation.

Switzerland Plasma Fractionation Market Analysis

Switzerland is predicted to expand notably in the European plasma fractionation market from 2025 to 2033 owing to. Despite its small population, the country exerts disproportionate influence through its role as a global hub for plasma fractionation and biopharmaceutical innovation. As per the Swiss Federal Office of Public Health, plasma-derived medicines are fully reimbursed with no prior authorization delays. Switzerland also leads in advanced product development. Additionally, the nation’s neutrality and stable regulatory framework attract strategic plasma imports from non-EUU sources. This unique combination of manufacturing scale, regulatory efficiency, and innovation ensures Switzerland’s outsized and strategic market role.

COMPETITIVE LANDSCAPE

The European plasma fractionation market is characterized by an oligopolistic structure dominated by three to four global biopharmaceutical leaders with deep integration across plasma collection, fractionation, and therapeutic delivery. Competition is not price-driven but centered on product portfolio breadth, manufacturing reliability, regulatory compliance, and patient support services. The market operates under intense scrutiny from the European Medicines Agency and national health authorities, which mandate stringent pathogen safety and traceability standards. Companies differentiate through innovation in subcutaneous formulations, extended half-life products, and rare protein recovery. Geographic advantage matters significantly; firms with European-based fractionation plants like CSL Behring and Grifols benefit from faster regulatory feedback and logistics control. The absence of significant local competitors creates high barriers to entry due to capitintensitsit,, regulatory complexity, and plasma sourcing constraints. As the EU pushes for greater self-sufficiency, the ability to balance imported plasma with domestic collection and advanced processing will define competitive leadership in this critical segment of the biopharmaceutical value chain.

KEY MARKET PLAYERS

A few of the noteworthy companies operating in the European plasma fractionation market profiled in the report are

- CSL Ltd. (Australia)

- Grifols S.A. (Spain)

- Baxalta Incorporated (U.S.)

- Octapharma AG (Switzerland)

- Kedrion S.p.A (Italy)

- Bio Products Laboratory (U.K.)

- Sanquin (Netherlands)

- China Biologic Products, Inc. (China)

- Biotest AG (Germany)

- Laboratoire Français du Fractionnement et des Biotechnologies (France)

TOP LEADING PLAYERS IN THE MARKET

- CSL Behring GmbH is a cornerstone of the European plasma fractionation market through large-scale manufacturing facilities in Marburg, Germany, and Bern, Switzerland, which supply immunoglobulialbuminin,n and clotting factors across the continent. The company plays a pivotal role in ensuring therapeutic access for rare disease patients under national healthcare systems. It also launched a subcutaneous immunoglobulin formulation with enhanced hyaluronidase delivery approved by the European Medicines Agency. These initiatives reinforce CSL Behring’s commitment to innovation,patient-centric delivery, and supply chain resilience within Europe’s plasma ecosystem.

- Grifols S A maintains a strong presence in the European plasma fractionation market via its plasma collection network and fractionation plant in Parets del Vall,ès Spa, in which it serves as a strategic hub for Southern Europe. The company integrates its European operations with global plasma supply to ensure consistent product availability. It also partnered with French and Italian rare disease centers to support early diagnosis programs for primary immunodeficiency. These actions enhance Grifols’ alignment with EU regulatory expectations and clinical care pathways while strengthening its global leadership in plasma-derived therapeutics.

- Takeda Pharmaceutical Company Limited actively participates in the European plasma fractionation market through its HyQvia and Albumin portfolios marketed across Germany, the UK, and France. The company leverages its global R and D engine to tailor products for European treatment guidelines and reimbursement frameworks. It also expanded its home therapy support services in the Netherlands and Sweden to facilitate subcutaneous immunoglobulin adoption. These patient-focused strategies position Takeda as an innovative and responsive contributor to Europe’s evolving plasma therapy landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European plasma fractionation market are investing in advanced chromatography platforms to increase the yield and purity of high-value proteins such as immunoglobulins and protease inhibitors. Companies are expanding subcutaneous and home-based therapy programs to improve patient adherence and reduce hospital burden, aligning with national health technology assessments. Strategic partnerships with rare disease reference networks and diagnostic centers are accelerating early detection and treatment initiation. Regulatory harmonization efforts with the European Medicines Agency and European Directorate for the Quality of Medicines ensure rapid approval of novel formulations and pathogen safety upgrades. Additionally, our firms are localizing plasma processing through European manufacturing hubs to enhance supply chain security and comply with the EU’s pharmaceutical sovereignty objectives. These strategies collectively address clinical demand, nd regulatory ri,gor and supply resilience in a high-stakes therapeutic domain.

EUROPE PLASMA FRACTIONATION MARKET NEWS

- In March 2025, CSL Behring GmbH expanded its chromatography-based fractionation line at its Bern, Switzerland, facility to increase production of C1 esterase inhibitor for hereditary angioedema patients. This capacity enhancement is anticipated to meet rising European demand and strengthen the European Plasma Fractionation Market presence.

- In July 2023, Grifols S.A. A next-generation dual pathogen inactivation technology at its Parets del VallèsSpainpa, in a plant, validated for emerging arboviruses under European regulatory standards. This safety upgrade is anticipated to ensure compliance and strengthen the European Plasma Fractionation Market presence.

- In October 2023, Takeda Pharmaceutical Company Limited launched home therapy support services for subcutaneous immunoglobulin users in the Netherlands and Sweden in collaboration with national immunodeficiency networks. This patient-centric initiative is anticipated to improve treatment adherence and strengthen the European Plasma Fractionation Market presence.

- In February 2025, CSL Behring GmbH received European Medicines Agency approval for high-concentration subcutaneous immunoglobulin with recombinant human hyaluronidase for weekly self-administration. This product approval is anticipated to expand home therapy access and strengthen the European Plasma Fractionation Market presence.

- In May 2023, Grifols S A partnered with rare disease diagnostic centers in France and Italy to establish early detection pathways for primary immunodeficiency through newborn screening pilot programs. This clinical collaboration is anticipated to accelerate diagnosis and strengthen the European Plasma Fractionation Market presence.

MARKET SEGMENTATION

This research report on the europe plasma fractionation market has been segmented and sub-segmented into the following categories.

By Product

- Albumin

- Immunoglobulin

- Factor VIII

- Protease Inhibitors

By Application

- Neurology

- Hematology

- Rheumatology

- Pulmonology

- Immunology

By End User

- Hospitals

- Clinical Laboratories

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the main growth drivers influencing the Europe Plasma Fractionation Market across major European countries?

The Europe Plasma Fractionation Market is driven by rising prevalence of immune and bleeding disorders, growing elderly population

with chronic diseases, and increasing use of immunoglobulins and other plasma-derived therapies in the Europe Plasma Fractionation Market.

2. Which product segment holds the largest share in the Europe Plasma Fractionation Market and why is immunoglobulins demand increasing?

In the Europe Plasma Fractionation Market, immunoglobulins account for the highest revenue due to expanded indications, off-label use

and rising diagnosis of immunodeficiency and autoimmune diseases boosting immunoglobulin consumption in the Europe Plasma Fractionation Market.

3. How is the aging population in Europe impacting demand in the Europe Plasma Fractionation Market for plasma-derived therapies?

The Europe Plasma Fractionation Market benefits from a growing geriatric base with higher rates of chronic, respiratory and bleeding disorders,

which increases utilization of albumin, coagulation factors and immunoglobulins within the Europe Plasma Fractionation Market.

4. What are the major restraints limiting the growth of the Europe Plasma Fractionation Market despite increasing clinical need?

The Europe Plasma Fractionation Market faces restraints from high costs of plasma products, limited reimbursement in some countries

and rising adoption of recombinant alternatives that compete with traditional products in the Europe Plasma Fractionation Market.

5. How do regulatory requirements in Europe affect market entry and expansion in the Europe Plasma Fractionation Market?

Stringent EU and national regulations on blood, tissues and cells raise compliance costs and lengthen approval timelines,

creating entry barriers but also ensuring high product safety in the Europe Plasma Fractionation Market.

6. Which countries lead the Europe Plasma Fractionation Market in terms of capacity and plasma collection infrastructure?

Germany, along with countries such as Austria and the Czech Republic, has the highest plasma collection capacity,

making Germany a key revenue contributor and strategic hub in the Europe Plasma Fractionation Market.

7. How is hospital and clinic demand shaping end-user dynamics in the Europe Plasma Fractionation Market?

Hospitals and clinics dominate end-user share in the Europe Plasma Fractionation Market due to rising use of plasma-derived products

for immunodeficiency, neurological and bleeding disorders across European healthcare systems.

8. What role do rare diseases and neurological disorders play in expanding the Europe Plasma Fractionation Market?

Increasing recognition of rare diseases, autoimmune neuropathies and chronic neurological conditions is driving higher immunoglobulin use,

supporting sustained growth in the Europe Plasma Fractionation Market.

9. How is investment in plasma collection centers influencing future capacity in the Europe Plasma Fractionation Market?

Ongoing investment in new plasma collection sites and fractionation facilities across Europe enhances supply security,

supporting long-term scalability and product availability in the Europe Plasma Fractionation Market.

10. What impact did recent healthcare trends and infectious disease outbreaks have on the Europe Plasma Fractionation Market?

Heightened focus on plasma-derived therapies and hospital collaborations during recent infectious disease outbreaks

helped accelerate clinical adoption and awareness in the Europe Plasma Fractionation Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com