Europe Ploughing and Cultivating Machinery Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, End Use, Application, Power Source, and Country – Industry Forecast From 2026 to 2034

Europe Ploughing and Cultivating Machinery Market Report Summary

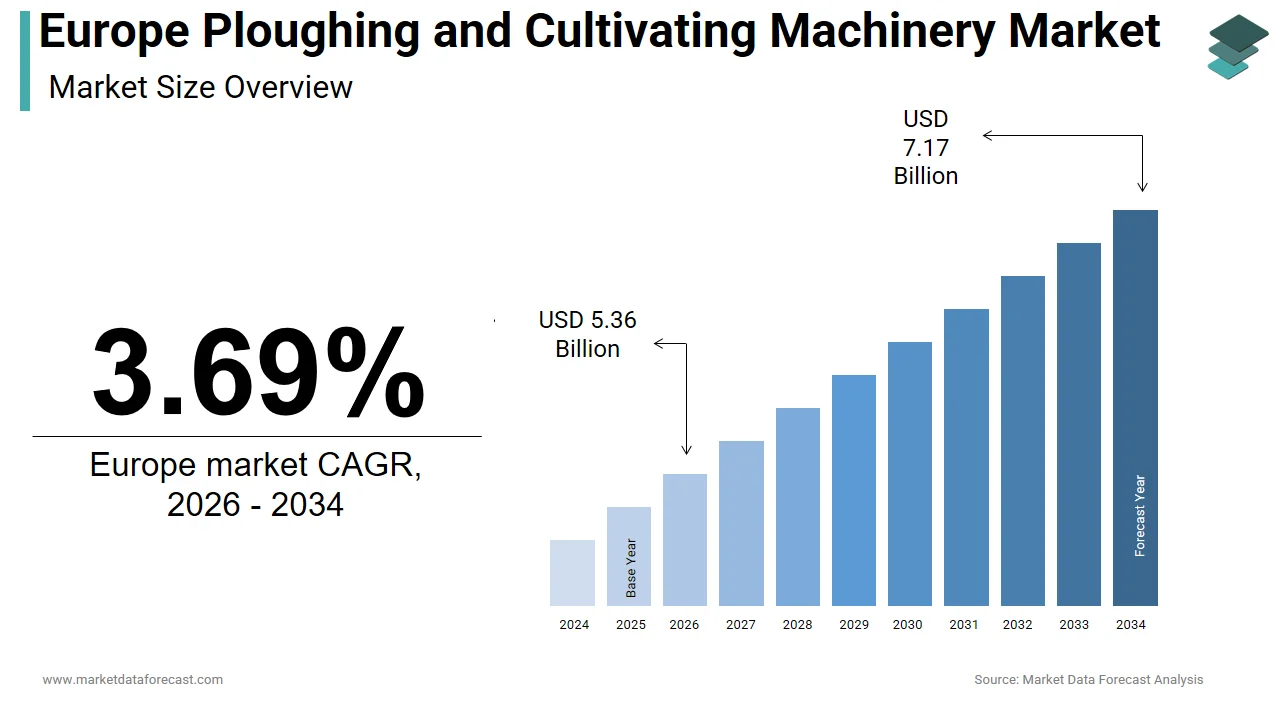

The Europe ploughing and cultivating machinery market was valued at USD 5.17 billion in 2025 and is projected to grow from USD 5.36 billion in 2026 to USD 7.17 billion by 2034, registering a CAGR of 3.69% from 2026 to 2034. Market growth is driven by increasing mechanization in agriculture, rising demand for precision farming equipment, and the need to improve operational efficiency and soil management. Growing investments in sustainable farming practices, modernization of agricultural machinery fleets, and government support for advanced farming technologies are further supporting market expansion.

Key Market Trends

- Increasing adoption of precision agriculture and smart farming technologies.

- Rising demand for high-performance cultivators and soil preparation equipment.

- Growing investments in farm mechanization and agricultural productivity enhancement.

- Expansion of fuel-efficient and technologically advanced agricultural machinery.

- Increasing focus on sustainable soil management and conservation farming practices.

Segmental Insights

- Based on type, the cultivators segment dominated the Europe ploughing and cultivating machinery market in 2025, driven by their widespread use for seedbed preparation, weed control, soil aeration, and improving crop productivity across diverse farming operations.

- Based on end use, the large-scale farming operations segment held the largest market share in 2025, supported by increasing demand for high-capacity machinery that enhances operational efficiency, reduces labor requirements, and improves field productivity.

- Based on power source, the internal combustion engine-powered machinery segment accounted for the leading share of the market in 2025, owing to its proven reliability, high torque output, extensive refueling infrastructure, and suitability for heavy-duty agricultural applications.

Regional Insights

The Europe ploughing and cultivating machinery market continues to expand across major agricultural economies, supported by technological innovation, mechanized farming practices, and increasing investments in agricultural productivity.

- Germany dominated the European market in 2025, driven by advanced agricultural mechanization, strong manufacturing capabilities, and widespread adoption of precision farming technologies.

- France held the second-largest position in the regional market, supported by its extensive agricultural land, large commercial farming sector, and increasing investments in modern cultivation equipment.

- The United Kingdom maintained a significant market position despite post-Brexit trade adjustments, supported by continued modernization of agricultural operations, adoption of advanced farming technologies, and demand for efficient soil preparation machinery.

Competitive Landscape

The Europe ploughing and cultivating machinery market is highly competitive, with leading agricultural equipment manufacturers focusing on product innovation, automation, fuel efficiency, and precision farming technologies. Companies are investing in research and development, smart machinery integration, and expansion of dealer and service networks to strengthen their market presence. Strategic partnerships, product launches, and continuous advancements in agricultural equipment continue to shape the competitive landscape.

Prominent companies operating in the Europe ploughing and cultivating machinery market include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Bucher Industries, Amazone Werke, SDF Group, Yanmar Co., Ltd., and Kverneland Group.

Europe Ploughing and Cultivating Machinery Market Size

The Europe ploughing and cultivating machinery market reached USD 5.17 billion in 2025, is expected to grow to USD 5.36 billion in 2026, and is anticipated to touch USD 7.17 billion by 2034, at a CAGR of 3.69% from 2026 to 2034.

'Ploughing and cultivating machinery' refers to the heavy-duty agricultural equipment used to turn, break, and loosen the soil before planting seeds. This sector includes a diverse range of equipment such as mouldboard ploughs, disc harrows, cultivators, and rotary tillers that facilitate efficient crop establishment and yield optimisation. As per Eurostat, the European Union's farms managed 156.2 million hectares of utilized agricultural area, which serves as the core geographical driver for ploughing and cultivating machinery demand. Modern farming practices increasingly prioritise precision agriculture techniques to enhance productivity while minimising environmental impact. According to European Commission agricultural census data, the average age of a European farmer is 57 years old, driving a critical demand for mechanized solutions to mitigate severe generational labor shortages. The transition from conventional tillage to conservation tillage methods has influenced machinery design, leading to innovations in low-disturbance equipment. Regulatory frameworks under the European Green Deal emphasise sustainable land management practices, which drive adoption of advanced cultivating technologies. Manufacturers focus on developing durable and fuel-efficient machines that comply with strict emission standards. The market operates within a complex ecosystem of agricultural policies, subsidy programs and technological advancements that shape purchasing decisions. Farmers seek equipment that offers versatility across different soil types and crop rotations, ensuring long-term operational efficiency. This dynamic landscape requires continuous innovation to meet evolving agronomic needs and regulatory requirements throughout the region.

MARKET DRIVERS

Adoption of Precision Agriculture Technologies Enhances Operational Efficiency

The integration of precision agriculture technologies into ploughing and cultivating machinery is a primary driver for the growth of the Europe ploughing and cultivating machinery market. This enables farmers to optimise resource usage and improve crop yields. Advanced systems such as GPS-guided auto-steering, variable rate application, and real-time soil sensors allow for precise depth control and uniform tillage patterns. According to the International Society of Precision Agriculture (ISPA), precision farming technologies can reduce fuel consumption by up to 20% through optimized field operations, heavily accelerating tractor-guidance implement adoption. Farmers increasingly invest in smart implements that collect data on soil compaction, moisture levels, and organic matter content, facilitating informed decision-making. The rise of Internet of Things connectivity enables remote monitoring and predictive maintenance, reducing downtime during critical planting windows. Government initiatives such as the Digital Europe Programme support the adoption of digital tools in agriculture, providing financial incentives for technology upgrades. Large-scale farms, particularly in Germany, France and Poland, lead this transformation due to their capacity to absorb initial investment costs. The ability to minimise soil disturbance while maintaining effective weed control aligns with sustainability goals promoted by the Common Agricultural Policy. This technological evolution transforms traditional machinery into intelligent assets that contribute to overall farm profitability and environmental stewardship.

Labor Shortages in Agricultural Sector Accelerate Mechanisation Trends

Persistent labor shortages in the agricultural sector of the region further propel the expansion of the Europe ploughing and cultivating machinery market. This significantly accelerates the demand for automated and high-efficiency ploughing and cultivating machinery. As per Eurostat, the European Union lost roughly 25% of its total farms between 2010 and 2020, fueling a massive labor consolidation that drives demand for highly automated, high-capacity machinery. Ageing farmer populations and rural-urban migration exacerbate this challenge, forcing producers to rely heavily on mechanised solutions to maintain operational continuity. Modern cultivating equipment offers greater coverage rates and reduced manual intervention, allowing single operators to manage larger land areas effectively. Autonomous and semi-autonomous tractors equipped with advanced implements enable round-the-clock operations during peak seasons without dependence on seasonal labor availability. According to the European Commission Directorate-General for Agriculture and Rural Development (DG AGRI), surging agricultural labor costs relative to farm output have made capital investments in advanced tillage machinery far more economically viable than reliant hiring of seasonal workers. Farmers prioritise equipment that simplifies operation through intuitive interfaces and automated adjustments, reducing the skill barrier for new entrants. This shift ensures consistent field preparation quality regardless of labor fluctuations. The trend toward larger farm consolidations further supports mechanisation, as economies of scale justify higher upfront costs for sophisticated machinery. Consequently, manufacturers focus on developing user-friendly and robust equipment that addresses the critical need for labor independence in modern European agriculture.

MARKET RESTRAINTS

High Initial Investment Costs Limit Accessibility for Small-Scale Farmers

The substantial initial investment required for advanced ploughing and cultivating machinery is a significant restraint on the European market. This trend is particularly true for small- and medium-sized farms that dominate the European agricultural landscape. As per sources, high-tech cultivating implements equipped with precision sensors and hydraulics routinely cost between 20,000 and 50,000 euros, representing a steep financial entry barrier for lower-margin operators. According to Eurostat, nearly 64% of all farms in the European Union are smaller than 5 hectares, severely limiting their individual financial capacity to purchase specialized ploughing equipment without cooperatives. Limited access to credit facilities and high interest rates further constrain purchasing power, especially in Eastern European countries where income levels remain lower than the regional average. Smallholders often rely on outdated or second-hand machinery which may lack efficiency and compliance with current environmental standards. The fragmented nature of land ownership in regions like Italy and Greece reduces the economic justification for large-scale mechanisation investments. Maintenance and repair costs for sophisticated electronics add to the total cost of ownership, deterring risk-averse farmers. While cooperative models exist, they face organisational challenges and uneven usage patterns that hinder widespread adoption. This financial barrier prevents many producers from benefiting from productivity gains offered by modern technology, perpetuating inefficiencies in the sector. Manufacturers struggle to balance feature richness with affordability, creating a gap between technological potential and actual market penetration among smaller entities.

Stringent Environmental Regulations Increase Compliance Complexity

Strict environmental regulations imposed by the European Union create complex compliance requirements that constrain the development and deployment of certain machinery types in the Europe ploughing and cultivating machinery market. The European Green Deal and Farm to Fork Strategy mandate significant reductions in chemical pesticide use and promote soil health preservation, which limits the applicability of intensive tillage practices. According to European Commission agricultural directives, soil erosion affects 7.2% of total European agricultural land, triggering strict CAP conditionality rules that discourage deep inversion ploughing in favor of conservation-minded minimum-till machinery. Manufacturers must redesign equipment to meet low disturbance criteria requiring extensive research and development investments that delay product launches. Noise and emission standards for tractor-mounted implements impose additional engineering constraints, increasing production costs. Certification processes for new machinery involve rigorous testing and documentation, extending time to market. Farmers face uncertainty regarding future regulatory changes, which discourages long-term investment in specialised tillage equipment. The push toward conservation agriculture favours no-till or minimum-till systems, reducing demand for traditional mouldboard ploughs and heavy cultivators. Compliance with varying national interpretations of EU directives creates fragmentation in market requirements, complicating standardisation efforts. These regulatory pressures force manufacturers to navigate a shifting landscape where traditional high-performance metrics may conflict with sustainability mandates, limiting the scope of conventional machinery sales.

MARKET OPPORTUNITIES

Expansion of Conservation Tillage Practices Creates Demand for Specialised Equipment.

The growing adoption of conservation tillage practices across the region paves the way for manufacturers to develop and supply specialised low-disturbance cultivating equipment, which is likely to promote the growth of the Europe ploughing and cultivating machinery market. Conservation tillage aims to maintain at least 30 percent crop residue cover on the soil surface, reducing erosion and improving water retention. As per Eurostat, while conventional intensive ploughing still accounts for roughly two-thirds of arable land, targeted European policy incentives are driving a gradual structural shift toward reduced-tillage machinery. This shift creates demand for disc harrows, strip tillers and vertical tillage implements that prepare seedbeds without inverting soil layers. Manufacturers can innovate by designing lightweight yet durable machines that minimise soil compaction while ensuring effective weed control. The integration of cover crop management tools into cultivating systems offers additional value propositions for farmers practising regenerative agriculture. Governments provide subsidies under the Common Agricultural Policy for adopting eco-friendly practices, encouraging investment in compliant machinery. Educational programs by agricultural extensions promote the benefits of reduced tillage, fostering market acceptance. Companies that offer modular systems allowing farmers to switch between conventional and conservation modes gain a competitive advantage. The transition requires technical support and training services, creating ancillary revenue streams. This opportunity aligns with broader sustainability goals, ensuring long-term relevance and growth potential for manufacturers who adapt their portfolios to support soil health initiatives.

Growth of Rental and Sharing Economy Models Enhances Market Access

The emergence of rental and machinery-sharing platforms offers a transformative opportunity for the Europe ploughing and cultivating machinery market. This helps to expand market reach by making advanced ploughing and cultivating equipment accessible to a broader farmer base. Digital platforms connect equipment owners with renters, optimising utilisation rates and reducing idle time for expensive assets. According to CEETTAR (European Confederation of Agricultural Contractors), the growth of specialized cooperative machinery sharing and contractor rental schemes across Europe offers an increasingly vital, cost-effective alternative to individual machinery ownership. This model allows small- and medium-sized farms to access high-tech machinery for specific seasonal tasks without bearing full purchase costs. Manufacturers can partner with rental companies to offer certified pre-owned units or dedicated rental fleets, generating recurring revenue streams. Data analytics from shared usage provide valuable insights into machine performance and durability, informing future design improvements. The flexibility of rental arrangements appeals to younger farmers who prefer asset-light business models. Insurance and maintenance packages bundled with rentals reduce operational risks for users. This trend supports circular economy principles by extending product lifecycles and reducing waste. Companies that develop robust digital ecosystems for booking, tracking, and payment streamline the user experience, enhancing adoption. Manufacturers can tap into underserved segments by embracing service-oriented business models. This approach helps build lasting customer relationships beyond traditional sales transactions.

MARKET CHALLENGES

Supply Chain Disruptions Impact Production Timelines and Component Availability

Global supply chain disruptions are a persistent challenge to the Europe ploughing and cultivating machinery market. This situation causes delays in production and component shortages. The market relies heavily on specialised steel bearings, hydraulics, and electronic components sourced from various international suppliers. As per CEMA (European Agricultural Machinery Association) industrial economic bars, extended lead times for critical hydraulics and micro-electronic components have significantly altered factory assembly schedules and delayed implement deliveries across European production hubs. Geopolitical tensions and trade restrictions further complicate procurement strategies, forcing manufacturers to seek alternative suppliers at higher costs. Logistics bottlenecks at ports and rail networks delay delivery of finished goods to dealers and end users, impacting seasonal sales windows. Inventory management becomes difficult as demand fluctuates unpredictably, leading to either excess stock or missed opportunities. The reliance on just-in-time manufacturing principles proves vulnerable to external shocks, requiring companies to hold larger safety stocks, which ties up capital. Currency fluctuations affect the import costs of raw materials, squeezing profit margins. Manufacturers must invest in supply chain diversification and local sourcing initiatives to mitigate risks, but these transitions require significant time and resources. The inability to meet delivery commitments damages brand reputation and customer trust. This volatility necessitates agile operational strategies and robust risk management frameworks to maintain competitiveness in an uncertain global environment.

Rapid Technological Obsolescence Requires Continuous Innovation Investment

The rapid pace of technological advancement in agricultural machinery creates a challenge of obsolescence, requiring manufacturers to continuously invest in research and development to remain competitive, which holds back the expansion of the Europe ploughing and cultivating machinery market. Innovations in automation, artificial intelligence and connectivity render existing models outdated quickly, pressuring companies to refresh product lines frequently. According to the European Patent Office (EPO) Patent Index, digital agriculture patent filings maintain a steady growth rate, reflecting a highly aggressive pace of technological innovation that forces continuous R&D investment. Keeping up with these developments demands substantial financial resources, which may strain smaller manufacturers with limited budgets. Farmers hesitate to invest in new technology, fearing it will become obsolete before achieving a return on investment. The complexity of integrating software updates and hardware upgrades adds to maintenance burdens for users. Training dealers and service technicians on new systems requires ongoing education efforts, increasing operational costs. Compatibility issues between different brands of smart implements hinder seamless integration on farms. The short lifecycle of electronic components contrasts with the long durability expectations for mechanical parts, creating mismatched replacement cycles. Manufacturers must balance innovation with reliability, ensuring that new features deliver tangible benefits rather than mere novelty. Failure to adapt results in loss of market share to more agile competitors. This dynamic environment requires strategic foresight and flexible development processes to sustain long-term viability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Power Source, Application, End Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Bucher Industries, Amazone Werke, SDF Group, Yanmar Co., Ltd., CNH Industrial, Kverneland Group. |

SEGMENTAL ANALYSIS

By Type Insights

The cultivators segment was the largest in the Europe ploughing and cultivating machinery market and occupied a commanding share in 2025. This supremacy of the segment was supported by its adaptability to various soil conditions and compatibility with conservation agriculture practices. The biggest reason this segment stays on top is the widespread shift toward minimum tillage systems, which require equipment that can manage crop residues and control weeds without inverting the soil profile. According to ECAF (European Conservation Agriculture Federation) datasets, roughly 26% of EU arable land relies on conservation or reduced tillage methods, acting as the primary catalyst for robust, surface-residue seedbed cultivators. Farmers prefer cultivators because they offer lower fuel consumption compared to traditional mouldboard ploughs while maintaining effective soil aeration and structure preservation. The versatility of modern cultivators allows them to be used for primary tillage, secondary tillage and weed management across different crop cycles, including cereals, oilseeds and vegetables. Manufacturers have enhanced these implements with adjustable tines and depth control mechanisms, enabling precise operation in diverse terrains. The ability to integrate with precision farming technologies such as GPS guidance further boosts their appeal among large-scale operators seeking efficiency. Regulatory support for soil health initiatives under the European Green Deal encourages the use of non-inversion tools, which aligns perfectly with cultivator functionality. This segment benefits from continuous innovation in materials and design, ensuring durability and performance in demanding agricultural environments.

However, the rotary tillers segment is likely to experience the fastest CAGR of 5.8% from 2026 to 2034 owing to increasing demand for intensive soil preparation in horticulture and vegetable production. Uniform soil texture is critical for germination and root development in high-value crops. As a result, the need for fine seedbeds fuels the segment's growth. As per Eurostat's agricultural production registries, steady long-term expansion in protected cultivation and intensive greenhouse vegetable zones drives a niche, continuous demand for highly specialized rotary tillers. Rotary tillers provide superior soil pulverisation and mixing capabilities, making them ideal for greenhouse operations and small plot farming. The rise of organic farming practices, which rely on mechanical weed control rather than chemicals, has further accelerated adoption. Organic farms require frequent tillage to disrupt weed life cycles, and rotary tillers offer the aggressiveness needed for effective management. Technological advancements have led to lighter and more efficient models suitable for compact tractors used in niche farming sectors. The expansion of urban agriculture and community gardens in major European cities also contributes to demand for versatile tillage tools. Manufacturers are focusing on developing eco-friendly designs with reduced power requirements to appeal to environmentally conscious growers. This segment benefits from the trend toward diversified cropping systems where rapid soil turnaround is essential for maximising land productivity.

By End Use Insights

The large-scale farming operations segment led the Europe ploughing and cultivating machinery market and captured a significant share in 2025. This leading position of the segment was attributed to its extensive land holdings and capacity for significant capital investment. High-efficiency equipment powers this segment, allowing operators to maximise thousands of hectares within short seasonal windows. As per Eurostat, farms larger than 100 hectares account for 56 percent of the total utilised agricultural area in the European Union, creating substantial demand for wide-width and high-horsepower implements. Large operators prioritise machinery that offers precision automation and data integration to optimise input usage and maximise yields. Economies of scale allow these farms to absorb the high initial costs of advanced tillage equipment while benefiting from lower per-hectare operational costs. Contract farming arrangements further drive demand as service providers invest in versatile machinery to serve multiple clients. The consolidation of agricultural land in countries like Germany, France and Poland has accelerated the trend toward larger operational units requiring sophisticated mechanisation. These farms often participate in export-oriented production, which demands consistent quality and volume achievable only through standardised mechanised processes. Access to credit facilities and government subsidies supports continuous fleet upgrades, ensuring adoption of the latest technologies. This segment drives innovation as manufacturers tailor products to meet the rigorous demands of industrial-scale agriculture.

Apart from this, the commercial agricultural operations segment is expected to exhibit a noteworthy CAGR of 6.2% between 2026 and 2034. This swift growth of the segment is driven by increasing demand for premium fruits, vegetables, and horticultural products. Shifts toward fresh, local, and healthy foods are driving segment growth, necessitating advanced soil management practices. According to research, while commercial fruit and vegetable production volume dictates high-input operations, structural macroeconomic value adjustments are compiled by Eurostat, forcing precision tillage investments to preserve delicate horticultural root networks. Commercial growers utilise customised ploughing and cultivating machinery to maintain soil structure and hygiene in intensive rotation systems. The rise of contract growing for supermarket chains imposes strict quality standards that can only be met through controlled mechanised operations. Greenhouse and protected cultivation sectors within commercial agriculture drive demand for compact and manoeuvrable tillage tools. Investment in technology such as sensor-based tillage allows for real-time adjustments to soil conditions, enhancing crop quality. Commercial operators are quicker to adopt innovative solutions that offer competitive advantages in yield and consistency. The professionalisation of farming practices in this segment ensures higher willingness to pay for premium equipment that delivers reliable performance. This growth reflects the broader shift toward value-added agriculture, where machinery plays a critical role in maintaining product standards.

By Power Source Insights

In 2025, the internal combustion engine-powered machinery segment held the majority share of the Europe ploughing and cultivating machinery market because of its proven reliability, high torque output, and extensive refuelling infrastructure. This prominence is driven by the ability of diesel engines to handle heavy-duty tillage tasks across large acreage without range limitations. According to CEMA (European Agricultural Machinery Association), diesel-powered tractors remain the undisputed backbone of European farming operations, navigating a real-world active fleet of several million machines requiring heavy-duty implement pull. Farmers prioritise internal combustion engines for their immediate availability of power and ability to operate in remote fields where electrical infrastructure is absent. The established supply chain for spare parts and service ensures minimal downtime during critical planting seasons. Recent improvements in engine efficiency and emission controls have extended the viability of diesel technology despite environmental concerns. Modern Stage V-compliant engines meet strict European Union emission standards, reducing particulate matter and nitrogen oxide emissions significantly. The high energy density of diesel fuel allows for longer operational hours between refuelling compared to current battery technologies. This segment benefits from decades of engineering refinement, resulting in durable and cost-effective solutions for diverse agricultural applications. The familiarity of operators with diesel mechanics further supports continued preference for this power source in professional farming contexts.

On the contrary, the electric-powered ploughing and cultivating machinery segment is on the rise and is expected to be the fastest-growing segment in the market, witnessing a CAGR of 12.5% over the forecast period owing to stringent environmental regulations and government incentives for zero-emission agricultural equipment. The expansion is propelled by the European Union's commitment to reduce greenhouse gas emissions. According to the European Climate Law framework, the European Union's legally binding mandate to slash total greenhouse gas emissions by 55% by 2030 puts immense systemic pressure on farms to integrate low-carbon electric implements. As per the European Commission, funding programs such as the Horizon Europe initiative provide grants for developing electric tractor prototypes and charging infrastructure in rural areas. Electric implements offer silent operation, reduced vibration, and lower maintenance costs due to fewer moving parts, appealing to farmers focused on operational efficiency. Advances in battery technology have improved energy density, allowing for sufficient runtime for typical tillage operations on medium-sized farms. Solar-powered charging stations integrated into farm buildings enable renewable energy usage, further enhancing sustainability credentials. Municipalities and organic farms are early adopters leveraging electric machinery to meet certification requirements for carbon neutrality. Manufacturers are partnering with energy companies to develop smart grid solutions that optimise charging times and costs. This segment benefits from increasing consumer pressure for sustainable food production methods, which incentivises farmers to adopt green technologies. The declining cost of batteries and improving performance metrics make electric options increasingly competitive with traditional diesel counterparts.

COUNTRY-LEVEL ANALYSIS

Germany Ploughing and Cultivating Machinery Market Analysis

Germany dominated the Europe ploughing and cultivating machinery market and accounted for a substantial share in 2025. This dominance of the German market was driven by a robust industrial base and advanced agricultural practices. According to CEMA (European Agricultural Machinery Association), Germany accounts for approximately 22% of total European machinery production, reflecting its central role in technological innovation. German farmers prioritise precision and efficiency, leading to high adoption rates of automated and GPS-enabled tillage equipment. The presence of major manufacturers such as Amazonen Werke and Lemken fosters a strong domestic supply chain and export orientation. Government policies supporting sustainable agriculture encourage investment in conservation tillage tools that reduce soil erosion. The average farm size in Germany has increased to 63 hectares as per Federal Statistical Office data, enabling economies of scale for large implements. Research and development investments focus on reducing emissions and improving fuel efficiency, aligning with strict environmental regulations. The country serves as a hub for testing new technologies before wider European rollout. Strong vocational training programs ensure skilled operators capable of utilising complex machinery effectively. Trade fairs such as Agritechnica in Hanover showcase the latest innovations, attracting global buyers and reinforcing Germany's leadership in the sector.

France Ploughing and Cultivating Machinery Market Analysis

France followed closely behind in the Europe ploughing and cultivating machinery market and captured a significant share in 2025. Factors such as its diverse agricultural landscape, ranging from large cereal plains to intensive vineyard regions, have contributed to the growth of the French market. According to sources, France imports approximately 18% of European machinery volumes, demonstrating a strong preference for versatile equipment suitable for varied crops. French farmers are increasingly adopting conservation agriculture techniques to comply with environmental directives, boosting demand for disc harrows and cultivators. As per the French Ministry of Agriculture and Food Autonomy via FranceAgriMer, targeted grants integrated with the EU Common Agricultural Policy (CAP) subsidize eco-friendly machinery to accelerate fleet modernization. Major cooperatives facilitate bulk purchasing, enabling smaller farms to access advanced technology. The wine and fruit sectors require specialised tillage tools for inter-row management, driving niche market growth. Innovation hubs in regions like Brittany focus on developing lightweight machinery to prevent soil compaction. The ageing farmer population is being replaced by younger, technologically savvy operators who prefer digital integrated solutions. Export opportunities to North Africa and Eastern Europe support domestic manufacturing activities. Strict labor laws make mechanisation essential for maintaining competitiveness in labour-intensive sectors. The combination of policy support and diverse crop requirements ensures steady demand for varied tillage equipment.

United Kingdom Ploughing and Cultivating Machinery Market Analysis

The United Kingdom maintains a significant position in the Europe ploughing and cultivating machinery market despite post-Brexit trade adjustments, maintaining steady demand driven by precision farming adoption. According to the Agricultural Engineers Association (AEA), the United Kingdom accounts for approximately 12% of European imports, with a primary focus on high-efficiency implements for large arable farms. British farmers face labor shortages and regulatory pressures prompting investment in automated tillage solutions. The flat terrain of East Anglia facilitates the use of wide-width equipment, maximising field coverage. Government initiatives promote soil health monitoring, encouraging the use of minimal disturbance tools. Local manufacturers collaborate with tech firms to integrate sensors into traditional implements, enhancing data collection capabilities. The decline in EU subsidy access has led to more strategic investment decisions focusing on long-term productivity gains. Organic farming growth drives demand for mechanical weed control equipment, reducing reliance on herbicides. Retailer requirements for sustainable sourcing influence farming practices and machinery choices. The strong pound sterling occasionally aids import affordability from non-EU suppliers. Educational institutions promote agritech careers, ensuring future workforce readiness for advanced machinery operation.

Italy Ploughing and Cultivating Machinery Market Analysis

Italy grew steadily in the Europe ploughing and cultivating machinery market. The country integrates this specialised equipment into its extensive horticultural and vineyard sectors. This heavy reliance on specific equipment drives unique market dynamics that are quite distinct from northern European trends. As per research, Italy imports approximately 10% of European volumes, characterized by high demand for compact and maneuverable implements tailored to vineyard and hilly terrain. Steep terrain in many agricultural regions requires lightweight equipment that prevents soil erosion and damage to perennial crops. The olive oil and wine industries drive demand for narrow-width cultivators capable of operating between tree rows. Government incentives support modernisation of small holdings through targeted subsidy programs. Family-owned farms dominate the landscape, preferring durable and easy-to-maintain machinery. Innovation focuses on reducing soil compaction in sensitive ecosystems. Export of specialised Italian machinery to Mediterranean countries strengthens domestic manufacturing. Climate change impacts necessitate adaptive tillage practices to manage water retention. Organic certification rates are high, driving demand for chemical-free weed control tools. The cultural emphasis on food quality translates into careful soil management practices supported by appropriate technology.

Spain Ploughing and Cultivating Machinery Market Analysis

Spain is expected to showcase a promising CAGR in the Europe ploughing and cultivating machinery market during the forecast period. It is emerging as a key market for conservation tillage equipment, driven by arid climate conditions and water scarcity challenges that necessitate soil moisture preservation. According to the Spanish Ministry of Agriculture, Fisheries and Food (MAPA), Spain handles approximately 8% of European machinery flows, aligning with a growing national adoption of conservation-minded no-till and strip-till systems. Large cereal farms in Castile and León lead the transition to low-disturbance implements to combat desertification risks. Government water management policies incentivise practices that improve soil structure and infiltration capacity. Solar energy integration powers electric tillage prototypes in pilot projects addressing sustainability goals. The expansion of irrigated horticulture requires precise bed preparation tools for efficient water use. Cooperation with Latin American manufacturers facilitates technology transfer for dryland farming techniques. Rural depopulation drives mechanisation to maintain productivity with fewer workers. Export potential to North Africa leverages geographic proximity and similar climatic conditions. Research centres focus on developing drought-resistant farming systems supported by appropriate machinery. The shift toward sustainable intensification ensures long-term viability of agricultural lands through proper tillage management.

COMPETITIVE LANDSCAPE

The competition in the Europe ploughing and cultivating machinery market is characterized by a mix of established multinational corporations and specialized regional manufacturers who vie for dominance through innovation and service quality. Large players leverage economies of scale and extensive distribution networks to offer comprehensive product portfolios covering all tillage needs. These companies invest heavily in research and development to integrate digital technologies and automation into their equipment, differentiating themselves from competitors. Smaller niche manufacturers focus on specific segments such as vineyard or organic farming tools where customization and expertise provide competitive advantages. The market sees intense rivalry in the precision agriculture segment where software compatibility and data integration capabilities become key decision factors for buyers. Regulatory compliance acts as a significant barrier to entry, ensuring that only firms with robust engineering and testing capabilities can sustain operations. Price competition remains moderate as customers prioritize reliability and total cost of ownership over initial purchase price. After-sales service and spare parts availability critically influence brand loyalty in rural areas. The shift toward sustainable farming practices drives innovation in low-disturbance equipment, creating new battlegrounds for technological superiority. Manufacturers must continuously adapt to policy changes and environmental concerns to maintain relevance and profitability in this mature yet evolving sector.

KEY MARKET PLAYERS

The leading companies operating in the Europe ploughing and cultivating machinery market include:

- John Deere

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra

- Bucher Industries

- Amazone Werke

- SDF Group

- Yanmar Co., Ltd.

- Kverneland Group

TOP PLAYERS IN THE MARKET

- CNH Industrial maintains a prominent position in the European ploughing and cultivating machinery market through its Case IH and New Holland brands, which offer comprehensive tillage solutions. The company leverages advanced engineering to produce high-efficiency disc harrows and cultivators that meet strict emission standards. Recent initiatives include integrating precision agriculture technologies into their implements, allowing for real-time soil data collection and automated depth control. CNH has strengthened partnerships with local dealers across Germany and France to enhance after-sales support and service availability. Investment in sustainable manufacturing processes helps reduce the environmental footprint of production facilities. The company actively participates in agricultural trade shows to showcase innovations in conservation tillage equipment. These strategic actions reinforce their reputation for reliability and technological leadership in the competitive European landscape while addressing the evolving needs of modern farmers seeking productivity and sustainability.

- Kverneland Group operates as a specialized manufacturer focusing exclusively on tillage and soil preparation equipment with a strong heritage in European agriculture. The company provides a wide range of plows, cultivators, and disc harrows designed for diverse soil conditions and farming practices. Recent efforts involve expanding their portfolio of low-disturbance tillage tools to support conservation agriculture trends promoted by EU policies. Kverneland has invested in digital connectivity features enabling farmers to monitor implement performance via smartphone applications. Participation in regional field days allows direct engagement with users to gather feedback for product improvement. The company enhances its market position through rigorous quality control and durable design principles that appeal to professional farmers. Strict adherence to safety and environmental regulations ensures seamless market access across all member states. This dedication to specialization and innovation helps them maintain a loyal customer base seeking robust and efficient soil management solutions.

- Amazone Werke plays a significant role in the Europe ploughing and cultivating machinery market by supplying innovative tillage implements known for their precision and versatility. The family-owned company focuses on developing lightweight yet robust equipment suitable for both conventional and conservation tillage systems. Recent strategies include enhancing their modular system approach, allowing farmers to customize implements according to specific field requirements. Amazone has improved its supply chain resilience by sourcing components from multiple European suppliers to mitigate disruption risks. Collaborations with research institutions drive continuous improvement in soil interaction dynamics and energy efficiency. Their focus on user-friendly designs reduces operator fatigue and simplifies maintenance procedures. Investment in training programs for dealers ensures high-quality technical support for end users. These efforts strengthen their reputation as a trusted provider of high-quality tillage solutions that align with sustainable farming practices and operational efficiency goals in the dynamic European agricultural sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe ploughing and cultivating machinery market employ several strategic approaches to enhance their competitive positioning and drive growth. Product differentiation remains a primary strategy as companies introduce precision-enabled and conservation-focused implements to cater to sustainability mandates. Innovation in materials and design helps reduce weight and fuel consumption while maintaining durability for heavy-duty operations. Strategic partnerships with technology providers enable integration of GPS guidance and sensor systems into traditional machinery. Companies invest in digital platforms to offer remote monitoring and predictive maintenance services, improving customer retention. Expansion into rental and sharing models allows access for smaller farms unable to afford high capital expenditures. Compliance with stringent European emission and safety regulations builds trust and facilitates smoother market entry. Continuous research and development ensures adaptation to changing agronomic practices and climate challenges. These combined strategies help participants navigate regulatory complexities and capitalize on emerging opportunities in the evolving agricultural landscape.

MARKET SEGMENTATION

This Europe ploughing and cultivating machinery market research report is segmented and sub-segmented into the following categories.

By Type

- Plows

- Cultivators

- Tillage Equipment

- Disc Harrows

- Rotary Tillers

By End Use

- Small Scale Farming

- Large Scale Farming

- Commercial Agricultural Operations

By Application

- Agriculture

- Horticulture

- Landscape Gardening

- Forestry

By Power Source

- Internal Combustion Engine

- Electric

- Manual

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe ploughing and cultivating machinery market?

The Europe ploughing and cultivating machinery market includes equipment used for soil turning, loosening, and preparing fields for planting.

How does the Europe ploughing and cultivating machinery market work?

The Europe ploughing and cultivating machinery market works by supplying implements that help farmers break soil, improve structure, and ready land for crops.

What drives growth in the Europe ploughing and cultivating machinery market?

The Europe ploughing and cultivating machinery market grows with farm mechanization, higher demand for efficiency, and the need for better soil preparation.

Which equipment leads the Europe ploughing and cultivating machinery market?

Ploughs and cultivators lead the Europe ploughing and cultivating machinery market because they are widely used for routine land preparation.

Why are ploughs important in the Europe ploughing and cultivating machinery market?

Ploughs are important in the Europe ploughing and cultivating machinery market because they turn soil, bury residue, and support better seedbed conditions.

What role do cultivators play in the Europe ploughing and cultivating machinery market?

Cultivators support the Europe ploughing and cultivating machinery market by breaking clods, controlling weeds, and improving soil texture.

How does soil preparation affect the Europe ploughing and cultivating machinery market?

Soil preparation is central to the Europe ploughing and cultivating machinery market because it improves planting conditions and crop establishment.

What is the role of tractor-mounted implements in the Europe ploughing and cultivating machinery market?

Tractor-mounted implements strengthen the Europe ploughing and cultivating machinery market by improving speed, reach, and field productivity.

Which farming type uses the Europe ploughing and cultivating machinery market most?

Arable farming uses the Europe ploughing and cultivating machinery market heavily because large crop fields require regular land preparation.

What trends shape the Europe ploughing and cultivating machinery market?

The Europe ploughing and cultivating machinery market is shaped by automation, precision agriculture, and demand for efficient field operations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com